56

WELCOME Presentation by: Ram Prakash Gautam B.Com.(H) C.A. P.E.II MOBILE NO. 08010422094

| Date post: | 22-Oct-2015 |

| Category: |

Documents |

| Upload: | glorydharmaraj |

| View: | 6 times |

| Download: | 2 times |

WELCOMEPresentation by:

Ram Prakash Gautam

B.Com.(H)

C.A. P.E.II

MOBILE NO. 08010422094

TAXATION FOR SALARY PERSON

TAXATION FOR SALARY PERSON

SALARY INCOME

Department Website• The relevant Acts, Rules, Forms

and Notifications are available at the website of the Income-tax Department -www.incometaxindia.gov.in

TDS RATE FOR THE F/Y 2011-12

OTHER AGE < 60 YEARS

WOMAN < 60 YEARS

SENIOR CITIZEN > 60 YRS

AGE > 80 YEARS

TAX (%)

For Income Between 0 to 1,80,000

For Income Between 0 to 1,90,000

For Income Between 0 to 2,50,000

For Income Between 0 to 5,00,000

0 %

For Income Between 1,80,001 to 5,00,000

For Income Between 1,90,001 to 5,00,000

For Income Between 2,50,001 to 5,00,000

10 %

For Income Between 5,00,001 to 8,00,000

For Income Between 5,00,001 to 8,00,000

For Income Between 5,00,001 to 8,00,000

For Income Between 5,00,001 to 8,00,000

20 %

For Income above 8,00,001

For Income above 8,00,001

For Income above 8,00,001

For Income above 8,00,001

30 %

Surcharge 0

Education Cess 3 %

TopicsTopics

WHAT IS SALARY PERQUISITES ALLOWANCES INCOMES WHICH DO NOT FORM PART OF TOTAL INCOME. DEDUCTION UNDER SECTION 16 DEDUCTION OF INTEREST PAID/ACCRUED ON SOP DEDUCTIONS UNDER CHAPTER vi A. DUTIES OF PERSONS RESPONSIBLE FOR DEDUCTION TAX

THINK IT

• Motto for Life: If you chase it, it will run!

• Confidence comes naturally with Success But, Success comes only, who are Confident So, Begin your day with great confidence.

What is salary ?(Sec.15)

• Employer and Employee relationship• Full time or Part time Employment.• Foregoing or Sacrificing of Salary.• Surrender of Salary.• Salary paid tax-free.• Voluntary Payments.

What is salary ?{Sec. 17(1)}

• Salary includes• Wages, Any Annuity or Pension, any Gratuity,

any Fees, Commission, Perquisites, Leave encashment, Arrears of salary , Interest earned in excess of 9.5% on RPF, Amount transferred in excess of 12% of salary to RPF.

What is salary ?• Any salary, bonus, commission or

remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as “Salary”.

What is salary ?{Sec. 17(3)}

• Compensation due or received from present / former employer in connection with (a) termination of employment or (b) modification of terms & conditions of employment.

• Any amount received from an Unrecognized Provident Fund , to the extant of Employer’s contribution along with interest on such contribution.

• Sum received under Key man Insurance Policy , Including Bonus on it.

• Any sum received , either prior to employment or after cessation of employment.

Specified Employee {U/S 17(3)}

An Individual will be considered as a Specified Employee if :-

• He is a Director of a Company or,

• He hold 20% or more of equity voting power in the Company,

• **Monetary salary in excess of `50000/-.

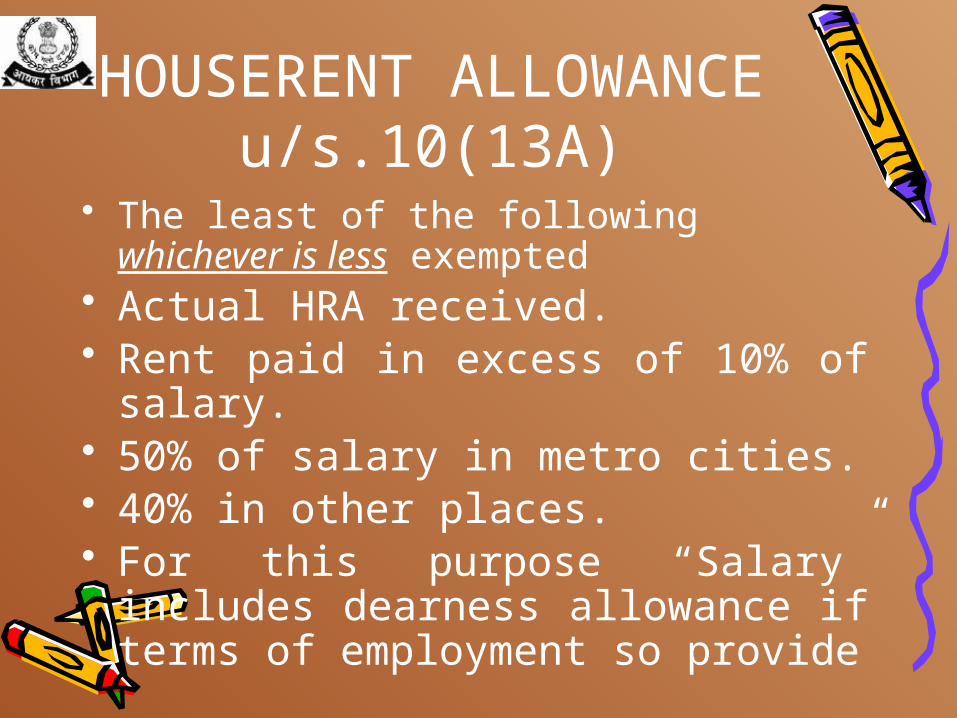

HOUSERENT ALLOWANCE

u/s.10(13A)• The least of the following whichever is less exempted

• Actual HRA received.• Rent paid in excess of 10% of salary.• 50% of salary in metro cities.• 40% in other places.• For this purpose “Salary” includes dearness

allowance if terms of employment so provide

House Rent Allowance• The disbursing authorities should satisfy

themselves in this regard by insisting on production of evidence of actual payment of rent.

• It has been decided as an administrative measure that salaried employees drawing house rent allowance up to ` 3,000 per month will be exempted from production of rent receipt. (CBDT Circular No. 01/2010 dated January 11,2010)

Declaration of Circular No. 01/2010 dtd. 11.01.10

• Though incurring actual expenditure on payment of rent is a pre-requisite for claiming deduction under section 10(13A), it has been decided as an administrative measure that salaried employees drawing house rent allowance up to Rs. 3,000 per month will be exempted from production of rent receipt. It may, however, be noted that this concession is only for the purpose of tax-deduction at source, and, in the regular assessment of the employee, the Assessing Officer will be free to make such enquiry as he deems fit for the purpose of satisfying himself that the employee has incurred actual expenditure on payment of rent.

Allowances exempt, amount received or limit specified, which

ever is less1. Children Education Allowance : Exempt up to

actual amount received per child or `100 p.m. per child up to maximum of two children, which ever is less.

2. Hostel Expenditure Allowance : Exempt up to actual amount received per child or `.300 p.m. per child up to maximum of two children, which ever is less.

3. Transport Allowance :Exempt to the extent of `.800 p.m.(In case of Handicapped ` 1600)

1. The value of any benefit or amenity granted or provided free of cost or at concessional rate.

2. With effect from 1.4.2010 (assessment year 2010-11), the value any specified security (stock option) or sweat equity shares allotted or transferred.

PERQUISITES

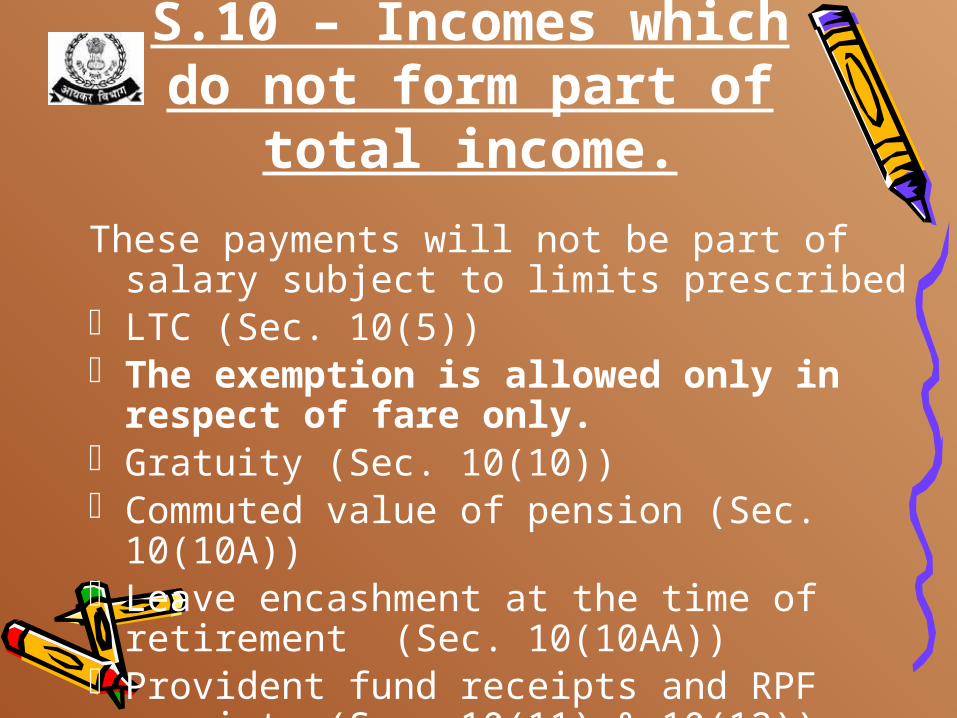

S.10 – Incomes which do not form part of total income.

These payments will not be part of salary subject to limits prescribed

o LTC (Sec. 10(5))o The exemption is allowed only in respect of fare

only.o Gratuity (Sec. 10(10))o Commuted value of pension (Sec. 10(10A))o Leave encashment at the time of retirement (Sec.

10(10AA))o Provident fund receipts and RPF receipts (Sec. 10(11)

& 10(12))

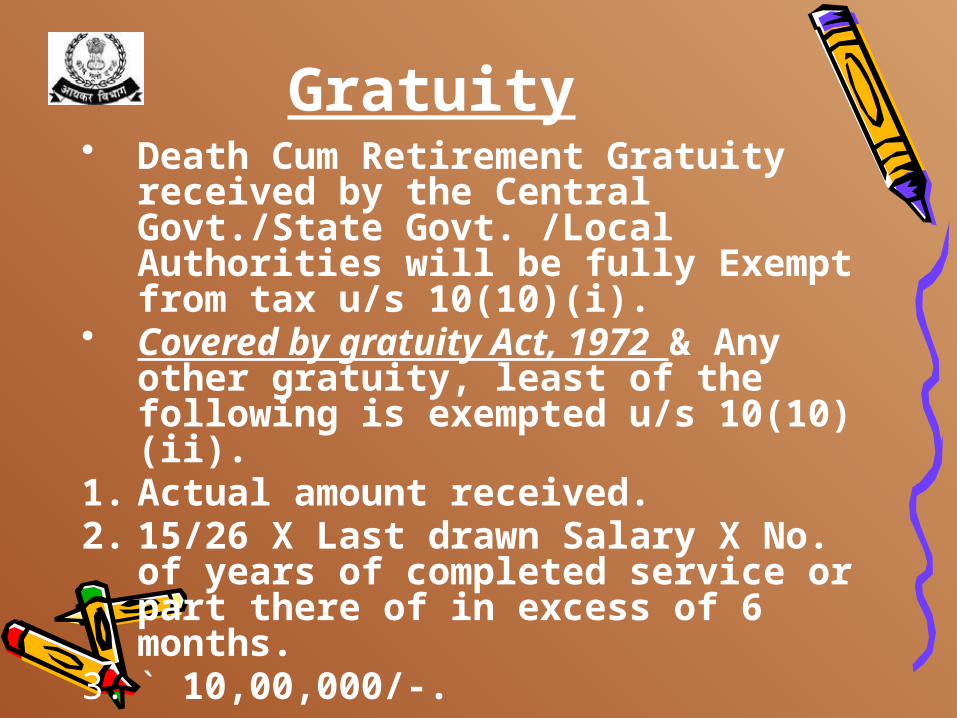

Gratuity• Death Cum Retirement Gratuity received by

the Central Govt./State Govt. /Local Authorities will be fully Exempt from tax u/s 10(10)(i).

• Covered by gratuity Act, 1972 & Any other gratuity, least of the following is exempted u/s 10(10)(ii).

1. Actual amount received.2. 15/26 X Last drawn Salary X No. of years of

completed service or part there of in excess of 6 months.

3. ` 10,00,000/-.

"Eleven Hints for Life" 1. It hurts to love someone and not be loved in return.

But what is more painful is to love someone and neverfind the courage to let that person know how you feel.

2. A sad thing in life is when you meet someone whomeans a lot to you, only to find out in the end that it wasnever meant to be and you just have to let go.

3. The best kind of friend is the kind you can sit on aporch swing with, never say a word, and then walk awayfeeling like it was the best conversation you've ever had.

4. It's true that we don't know what we've got until we loseit, but it's also true that we don't know what we've beenmissing until it arrives.

5. It takes only a minute to get a crush on someone, anhour to like someone, and a day to love someone-but ittakes a lifetime to forget someone.

BALANCE ON SLIDE :- 24

Gratuity

Covered by not gratuity Act, 1972 u/s 10(10)(iii)1. Actual amount received.

2. ½ X Average Salary X No. of fully completed years of service.

3. ` 10,00,000/-.

Pension 10(10A)• I. Uncommuted Pension :-It is taxable for all

employees as salary.• II. Commuted Pension:- It is taxable as under• (i) received by govt. employee wholly exempt.• (ii) received by non govt. employees – following is

exempt:-• (a) If received gratuity – Commuted value of One-

third of the pension which he is normally entitled to receive.

• (b) In any other case :- Commuted value of One-half of such pension.

• Central Govt / State Govt Employees – Exempt

• Other Employees - Exemption will be determined with reference to the leave to their credit at the time of retirement on superannuation, or otherwise, subject to a maximum of ten months’ leave. This exemption will be further limited to the maximum amount of Rs. 3,00,000.

EL Encashment

BALANCE OF SLIDE 206. Don't go for looks, they can deceive. Don't go for wealth,even that fades away. Go for someone who makes yousmile because it takes only a smile to make a dark dayseem bright.

7. Dream what you want to dream, go where you want to go,be what you want to be. Because you have only one life andone chance to do all the things you want to do.

8. Always put yourself in the other's shoes. If you feel that ithurts you, it probably hurts the person too.

9. A careless word may kindle strife. A cruel word may wrecka life. A timely word may level stress. But a loving word mayheal and bless.

10. The happiest of people don't necessarily have the bestof everything they just make the most of everything that comesalong their way.

11. Love begins with a smile, grows with a kiss, ends witha tear. When you were born, you were crying and everyonearound you was smiling. Live your life so that when you die,you're the one smiling and everyone around you is crying.

• Tax on employment (professional tax) paid is allowable as deduction from salary.

• Entertainment Allowance : This deduction is allowed only to a Government employee to the least of following.

• Actual amount received.• 20% of salary exclusive of any

allowance.• `5000.

Deduction under section 16

Deduction on income fromHouse property

• interest up to a maximum limit of ` 1,50,000 is allowed – Loan taken on or after 1-4-1999 – for constructing/acquiring the residential.

house and – completed within three years from the end

of the financial year in which capital was borrowed.

– No limits for the let out property– Only one property is eligible for deduction

Deductions under chapter VI A –u/s.80C,80CCD&80CCD

• The following investments are eligible for deduction:

• Life Insurance Premium, Statutory Provident Fund, RPF, PPF, NSC, ULIP, Notified Units of Mutual Fund, Re-payment of housing loan, Tuition Fee paid, fixed deposit for 5 years or more with a scheduled Bank, Senior Citizen Saving Scheme, five year time deposit scheme in Post Office etc.

Deductions u/s.80C,80CCD&80CCD

• Amount of deduction allowable; gross qualifying amount or `1,00,000 which ever is lower.

Deduction u/s.80CCF

• Deduction in respect of subscription to long term infrastructure bonds.

• · This deduction applicable from the assessment year 2011-12

• Maximum deduction allowable is ` 20,000.

Deduction u/s.80D

• Medical insurance premium (Medi claim Policy) paid:On the health of taxpayer, spouse, parents and dependent children

• The premium can be paid by any mode other than cash.

• It is paid out of income chargeable to tax.

Deduction u/s.80D

• Amount of deduction `15,000 – • additional deduction `5,000 is

allowed if the policy is taken on the health of senior citizen.

• Deduction in respect of maintenance including medical treatment of a handicapped dependent :

• Furnish a certificate issued by the medical authority in form No.10-IA.

• Amount of deduction ` 50,000 is allowed.• In case severe disability (80% or more), `

1,00,000 is allowed.• The person claiming deduction under this

section, he should not claim any deduction under section 80U.

Deduction u/s.80DD

Deduction u/s.80DDB• Medical treatment of dependent or self for

specified disease/ailment.• Amount of deduction ` 40,000: if the

person is a senior citizen ` 60,000 is allowed.

• This deduction is not allowable by the employer.

Deductions -u/s.80E• Payment of interest on loan taken for

higher education: spouse or children• The loan has to be taken from any financial

institution or approved charitable institution.

• Such amount is paid out of his income chargeable to tax.

• The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier.

Deductions -u/s.80G– Deduction in respect of donations to certain

funds, charitable institutions etc.– · Deduction can be allowed by the

employer only in respect of donations made to Prime Minister Relief Fund, Chief Ministers Relief Fund, Earthquake Fund, etc.

– · In respect of donations to charitable institutions, deductions cannot be allowed by the employer.

Deductions -u/s.80GG• Deduction in respect of rent paid :• The assessee should not be receipt of HRA

and he should not own any house• The least of the following amount is

exempted• 1. Rent paid in excess of 10% of total

income before allowing deduction under this section.

• 2. ` 2000 per month.• 3. 25% of total income before allowing

deduction under this section

Deduction-u/s.80GGC• Any amount of contribution made by a

person to a political party or an electoral trust is deductible.

• This deduction is not allowable by the employer.

Deductions under Chapter VI A-u/s.80U

• Deduction in case of a person with disability: blindness, low vision, leprosy, hearing impairment, mental retardation and mental illness.

• Conditions: Furnish a certificate issued by the medical authority in form No.10-IA.

• Amount of deduction (fixed) ` 50,000 is allowed. In case severe disability (80% or more), `1,00,000 is allowed.

Particulars of income other than salary

• Employee has to furnish particulars of income under any head other than “Salaries” in a simple statement, which is properly verified by him. Such income should not be a loss under any such head other than the loss under the head “Income from House Property”.

• Relief is available when salary is received in arrears or advance.

• Application in Form-10E has to be obtained from the employee.

• Form 10E is required to allow claim of relief u/s. 89(1)

Relief u/s.89(1)

Relief u/s.89(1)

• from 1-4-2010 (assessment year 2010-11) that no such relief shall be granted in respect of any amount received or receivable by an assessee on his voluntary retirement or termination of his service.

Estimation of Income for deducting tax

• Method of calculation : Estimate the salary including perquisites for the financial year 2010, apply the rates, calculate the tax and divide it by 12.

Estimation of Income for deducting tax

• The amount of tax so arrived should be deducted every month in equal installments. However, Any excess or deficit arising out of any previous deduction can be adjusted by increasing or decreasing the amount of subsequent deductions during the same financial year.

Duties of Persons responsible for deducting tax

• DDOs to satisfy themselves of the genuineness of claim:

• The Drawing and Disbursing Officers should satisfy themselves about the actual deposits/subscriptions/payments made by the employees, by calling for such particulars/information as they deem necessary before allowing the aforesaid deductions.

DDOs to satisfy themselves of the genuineness of claim:

• In case the DDO is not satisfied about the genuineness of the employee’s claim regarding any deposit/subscription/payment made by the employee, he should not allow the same, and the employee would be free to claim the deduction/rebate on such amount by filing his return of income and furnishing the necessary proof etc., therewith, to the satisfaction of the Assessing Officer.

Duties of Persons responsible for deducting tax

• File Quarterly statements in form No.24Q within time i.e. 15th July, 15 th October, 15th January of the relevant financial year and for the last quarter is 15th May following financial year.

• Challans for deposit of TDS - for salaries challan No.ITNS-281.

Attn: Govt. DDOs’

(a)Who are paying taxes by Book Adjustment - submit a statement in Form No. 24G within ten days from the end of the month to the agency authorized by the Director General of Income-tax (Systems) in respect of tax deducted by the deductors and reported to him for that month; and

(b) intimate the number (hereinafter referred to as the Book Identification Number) generated by the agency to each of the deductors in respect of whom the sum deducted has been credited.

The deductor has to issue a certificate in Form No. 16 along with annexure A or B and 12BA before 31st May from the end of financial year, in which the deduction was made.

FORM 16

FORM 16

Form No. 16, - for SALARIES(2) The certificate referred to in sub-rule (1) shall specify:(a) valid permanent account number (PAN)(b) valid TAN (c) (i) book identification number; (ii) Challan identification number (d) (i) receipt number of the relevant quarterly statement (ii) receipt numbers of all the relevant quarterly statements for “Salaries”.

Revised Form -16

• If the House Property is transferred before expiry of five years no deduction in the year of transfer and earlier deductions allowed will become income in the year of transfer .

• No deductions u/s. 80C for the repayment of principal amount if the loan is taken from the private persons and also not for commercial properties.

Points to Ponder

?

Points to Ponder• Any contributions made towards the ULIP,

deposit under Senior Citizen Saving Scheme, Time deposit in Post Office during the financial year and the same terminates within 5 years and LIP terminates within 2 years.

• The above contributions not qualified for deduction u/s.80C.

Points to Ponder• The quantum of deduction already taken in

the preceding years would be deemed as income of the taxpayer in the year in which contribution to the above plan/scheme/deposit is terminated.

You may not be able to cover the tax liability.

Employee may not submit the details to arrive at the correct liability.

I will submit the details in February

NOT DEDUCTING TAX STARTING FROM FINANCIAL YEAR

Withholding of salary leading to grievance of employees.

Employee paying tax on his own indicating failure of the DDO.

Don’t deduct, I will pay

NOT DEDUCTING TAX STARTING FROM FINANCIAL YEAR

Thank you