Page 1

Get Homework/Assignment Done Homeworkping.comHomework Help https://www.homeworkping.com/

Research Paper helphttps://www.homeworkping.com/

Online Tutoringhttps://www.homeworkping.com/

click here for freelancing tutoring sitesEXECUTIVE SUMMARY

Markets have always played a central role in the economic development and ensuring orderly

conduct of markets had been a constant endeavor various theories have provided an essential back drop to analyze

and understand market behavior. In the case of financial markets, the prominent ones are. Efficient market

hypothesis agency theory and information theory. Whenever the assumptions of these theories are not met fully

there begins a case for regulation. The key concerns of financial market regulators are market integrity systemic

safety and customer protection. These three concerns are inter wined and inter related.

As it is evident from the growth pattern of the international markets that develop countries have

maintained their position, while the emerging markets are also coming forward with full strength. A few

prominent emerging trends are the investors are becoming more market savvy information and communication

technology is revolutionizing the way transactions are carried out world is becoming a financial village

emergence of trans-national business demands better coordination among regulators etc. In the future Indian

markets are expected to become more vibrant and attain a leading position in the global financial system. With

1

Page 2

increasing role of information and communication technology information asymmetry is expected to reduce at an

increasing rate organized exchanges are likely to become one-stop financial shopping malls.

The committee has noted recent introduction of new products based on its interim recommendations and it

has further recommended widening the range of new products. It is expected that these new products, namely

mini contracts on equity index, options contract with longer life/tenure creation of volatility index and futures and

options contracts on it, options on futures, creation of bond indexes and futures and options contracts on them,

exchange traded currency [foreign exchange] futures and options contracts, exchange –traded products involving

different strategies, exchange traded credit derivatives over the count or product and exchange traded third party

products will be able to meet the needs of various classes of investors. Each class of these products needs to be

carefully designed and risk management specified by the exchanged with due approval by SEBI.

Finally the committee feels that while the small individual investors could best protect their investments by

hedging their positions in options market, they should carefully consider taking positions on futures markets

because mark-to-market losses resulting in margin calls could wipe out small individual investors.

2

Page 3

INTRODUCTION:

DERIVATIVES:

A Derivative is a financial instrument that derives its value from an underlying asset. Derivative is an

financial contract whose price/value is dependent upon price of one or more basic underlying asset, these

contracts are legally binding agreements made on trading screens of stock exchanges to buy or sell an asset in the

future. These assets can be anything ranging from share, index, bond, rupee dollar exchange rate, sugar crude,

soya bean, cotton, coffee etc.

Derivative on its own does not have any value. It is considered important because of its underlying asset.

Derivatives can of different types like forwards, futures, option, swaps, collars, caps, floor etc. The most popular

derivative instruments are futures and options.

Example:

A very simple example of derivative is curd, which is derivative of milk. The price of curd depends upon

the price of milk, which in turn depends upon the demand, and supply of milk. Let’s see it in this way, the price of

the Reliance Triple Option Convertible debentures (Reliance TOCD) varies upon the price of the Reliance Shares,

similarly the price of TELCO Warrants depends upon the price of the TELCO shares.

The American Depository Receipts (ADR) and Global Depository Receipts (GDR) Of ICICI, Satyam and

Infosys Traded on stock exchanges in NASDAQ of USA, draw their values from the prices of shares traded in

India. Similarly in mutual funds the prices of mutual fund units depends upon the prices of portfolio of securities

under that scheme.

History of Derivatives

The Derivatives market has existed from centuries as need for both users and producers of natural

resources to hedge against price fluctuations in underlying commodities. Although trading in agriculture and other

commodities has been the driving force behind the development of Derivatives market in India, the demand for

products based on financial instruments – such as bond, currencies, stocks and stock indices had outstripped the

commodities markets.

India has been trading in derivatives market in Silver, spices, gold, coffee, cotton and in oil markets for

decade’s gray market. Trading in derivatives market was legal before Morarji Desai’s Government had banned

forward contracts. Derivatives on stocks were traded in the form of Teji and mandi in unorganized markets.

Recently futures contracts various commodities were allowed to be on various exchanges. For Example Cotton

3

Page 4

and Oil futures were traded in Mumbai, Soya bean futures in Bhopal, Pepper futures in Kochi, Coffee futures in

Bangalore etc.

In June 2000, National stock exchange and Bombay stock exchange started trading in futures in Sensex

and Nifty. Options trading on Sensex and Nifty commenced in June 2001. Very soon thereafter trading began on

futures and options on 31 prominent stocks in the month of July and November respectively, currently there are

41 stocks trading in NSE derivatives and the list keeps growing.

Derivatives products initially emerged has hedging devices against fluctuations in commodity prices and

commodity linked derivatives remained the sole form of such products for almost three hundred years. The

financial derivatives came into spotlight in post 1970 period, due to the in stability in the financial markets.

Financial derivatives are instruments that their value from financial assets. These assets can be stocks,

bonds, currency etc. These Derivatives can be Forward rate agreements, Futures, Options, and Swaps. As stated

earlier the most traded instruments are futures and options. However these products became very popular and by

1990s, they accounted for about two-thirds of total transactions in derivatives products. In recent years, the market

for financial derivatives has grown tremendously.

Both in terms of variety of instruments available, their complexity and also turnover. In class of equity

derivatives, futures and options on stock indices have gained more popularity than on individual stocks, especially

among the institutional investors, who are major users of index-linked derivatives. Even small investors find these

useful due to high correlation of popular indices with various portfolios and ease of use.

The following factors have been driving the growth of financial derivatives:

Increased volatility in asset prices in financial markets.

Increased integration of national financial markets with the international markets.

Marked improvement in communication facilities and sharp decline in their costs.

Innovations in the derivatives markets, which optimally combine the risks and returns over a large

number of financial assets, leading to higher returns, reduced risks as well as transactions costs as

compared to individual financial assets.

PLAYERS IN THE MARKET

The following are the players in the Derivatives markets:

Speculators:

4

Page 5

People who buy or sell in the market to make profits. For example, if you will the stock price of

Reliance is expected to go up to Rs. 400 in one month; one can buy a one-month future of Reliance at Rs. 350 and

make profits.

Hedgers:

People who buy or sell to minimize their losses. For example, an importer has to pay US $ to buy goods

and rupee is expected to fall to Rs.50/$ from Rs.48/$, then the importer can minimize his losses by buying a

currency future at Rs.49/$.

Arbitrageurs:

People who buy or sell to make money on price differentials in different markets. For example, a futures

price is simply the current price plus the interest cost. If there is any change in the interest, it presents an arbitrage

opportunity. We will examine this in detail when we look at futures in a separate chapter. Basically, every

investor assumes one or more of the above and derivatives are a very good option for him.

TYPES OF DERIVATIVES

The most commonly used derivatives contracts are forwards, futures and options, which we shall discuss

in detail later. Here we take a brief look at various derivatives contracts that have come to be used.

Forwards:

A forward contract is a customized contract between two entities, where settlement takes place on

specific date in the future at today’s pre-agreed price.

Futures: A futures contract is an agreement between two parties to buy or sell an asset at a certain time

in the future at a certain price. Futures contracts are special types of forward contracts in the sense that

the former are standardized exchange-traded contracts.

Options:

Options are of two types

Call option

Put option

Call option:

Call option gives the buyer the right but not the obligation to buy a given quantity of the underlying

asset, at a given price on or before a given future date.

5

Page 6

Put option:

Put option gives the buyer the right, but not the obligation to sell a given quantity of the underlying asset

at a given price on or before a given date.

Warrants:

Options generally have lives of unto one year, the majority of options traded on options exchanges

having a maximum maturity of nine months. Longer-dated options are called warrants and are generally traded

over the years.

Baskets:

Basket options are on portfolios of underlying assets. The underlying asset is usually a moving average or

a basket of assets. Equity index options are a form of basket options

Swaps:

Swaps are private agreements between two parties to exchange cash flows in the future according to a

prearranged formula. They can be regarded as portfolios of forward contracts. The two commonly used swaps are:

Interest rate swaps:

These entail swapping only the interest related cash flows between the parties in the same currency.

Currency swaps:

These entail swapping both principal and interest between the parties, with the cash flows in one direction

being in a different currency than those in the opposite direction.

6

Page 7

NEED OF THE STUDY

The turnover of the stock exchange has been tremendously increasing from last 10 years. The

number of trades and the number of investors, who are participating, have increased. The investors are

willing to reduce their risk, so they are seeking for the risk management tools.

Prior to SEBI abolishing the BADLA system, the investors had this system as a source of

reducing the risk, as it has many problems like no strong margining system, unclear expiration date and

generating counter party risk. In view of this problem SEBI abolished the BADLA system.

After the abolition of the BADLA system, the investors are seeking for a hedging system, which

could reduce their portfolio risk. SEBI thought the introduction of the derivatives trading, as a first step it

has set up a 24 member committee under the chairmanship of Dr. L.C. Gupta to develop the appropriate

framework for derivatives trading in India, SEBI accepted the recommendation of the committee on may

11, 1998 and approved the phase introduction of the derivatives trading beginning with stock index

futures.

There are many investors who are willing to trade in the derivatives segment, because of its

advantages like limited loss unlimited profit by paying the small premiums.

SCOPE OF THE STUDY:

The study is limited to “Risk Return Analysis of Futures & Options” with special reference to

futures and option in the Indian context and the Inter-Connected Stock Exchange has been taken as a

representative sample for the study. The study can’t be said as totally perfect. Any alteration may come.

The study has only made a humble attempt at evaluation derivatives market only in India context. The

study is not based on the international perspective of derivatives markets, which exists in NASDAQ,

CBOT etc.

OBJECTIVE OF THE STUDY

To study the benefits of Futures and Options in Indian Market.

To study the functioning of futures & options in financial market.

7

Page 8

To make decisions of the shareholders in overcoming by investing in futures and

options

To study & compare the returns on inviting in future options.

To study the different ways of buying and selling of options.

To study the role of derivatives in India financial market.

LIMITATIONS OF THE STUDY:

The following are the limitation of this study.

The study of this project is limited to only 45 days.

The major limitation of this project is time fact.

The scrip is selected for analysis through secondary data so the analysis cannot be taken as

universal.

8

Page 9

DESCRIPTION OF THE METHODOLOGY:

The following are the steps involved in the study.

1. Selection of the scrip:-

The scrip selection is done on a random and the scrip selected is AIR DECCAN, BHARATI

AIRTEL, and WIPRO. Risk & return Involved in the Futures contracts & option Contract.

2. Data Collection:-

The data of the AIR DECCAN, BHARATI AIRTEL, and WIPRO has been collected from the

web site of National Stock Exchange i.e. “www.nseindia.com”. The data consist of the March

contract and the period of data collection is from 1st February 2012 – 31st March 2012.

9

Page 10

3. Analysis:-

The analysis consist of the tabulation of the data assessing the Risk & Return of Futures

Contracts & Option Contracts, representing the data with graphs and making the interpretation using

data.

INDUSTRY PROFILE

HISTORY OF STOCK EXCHANGE:

The only stock exchange operating in the 19th century were those of Bombay set up in

1875 and Ahmadabad set up in 1894. These were organized as voluntary non profit-making

association of brokers to regulate and protect their interests. Before the controls on securities

trading became central subject under the constitution in 1950, it was a state subject and the

Bombay securities contracts (control) Act of 1925 used to regulate trading in securities. Under

this act, the Bombay stock was recognized in 1927 and Ahmadabad in 1937.

During the war boom, a number of stock exchanges were organized in Bombay,

Ahmadabad and other centers, but they were not recognized. Soon after it became a central

subject, central legislation was proposed and a committee headed by A.D Gorwala went into the

bill for securities regulation. On the basis of the committee’s recommendations and public

discussion, the securities contracts (regulation) Act became law in 1956.

DEFINATION OF STOCK EXCHANGE:

10

Page 11

“Stock exchange means anybody or individuals whether incorporated or not, constituted

for the purpose of assisting, regulating or controlling the business of buying, selling or dealing in

securities.”

It is an association of member brokers for the purpose of self-regulation and protecting the

interests of its members.

It can operate only. If that Government under securities recognizes it contracts (regulation) Act

1956.The recognition is granted under section 3 of the act by the central government, ministry of

Finance.

NEED FOR STOCK EXCHANGE:

As the business and industry expanded and economy became more complex in nature, a

need for permanent finance arose. Entrepreneurs require money for long-term needs, where as

investors demand liquidity. The solution to this problem gave way for the origin of ‘Stock

Exchange’, which is a ready market for investment and liquidity.

FUNCTIONS OF STOCK EXCHANGE:

Maintains Active Trading:

Shares are traded on the stock exchanges, enabling the investors to buy and sell securities.

The prices may vary from transaction to transaction. A continues trading increases the liquidity or

marketability of the shares traded on the stock exchanges.

Fixations of prices:

Prices are determined by the transactions that flow from investors demand and the supplies

preferences. Usually the traded prices are named known to the public. This helps the investors to

make better decisions.

Ensures safe and fair dealings:

The rules, regulations and bye laws of the stock exchanges provide a measure of safety to the

investors to get a fair deal.

Aids in financing the industry:

A continuous market for shares provided a favorable climate for raising capital. The negotiability

and transferability of the securities help the companies to raise long-term funds. As it is easy to

trade the securities, investors are willing to subscribe the Initial public offerings (IPO). This

stimulates the capital formation.

Dissemination of Information:

11

Page 12

Stock Exchange provides information through their various publications. They publish the share

prices traded on their basis along with the volume traded. Directory of corporate information is

useful for the investor’s assessment regarding the corporate. Handouts and pamphlets provide

information regarding the functioning of the stock exchanges.

Performance inducers:

The prices of stocks reflect the performance of the traded companies. This makes the corporate

more concerned with its public image and tries to maintain good performance.

Self-regulating organizations:

The stock exchanges monitor the integrity of the members, brokers, listed companies and clients.

Continuous internal audit safeguards the investors against unfair trade practices. It settles the

disputes between member broker, investors and brokers.

The national stock Exchange (NSE) of India became operational in the capital market segment on

3rd November 1994 in Mumbai. The genesis of NSE lies in the recommendations of the pertains

committee 1991. A part from the NSE, it had recommended for the establishment of national

stock market system also. The committee pointed out some major defects in the Indian stock

market. The Defects specified are

1. Lack of infrastructure facilities and outdated trading system.

2. Lack of transparency in the operations that effect investor’s confidence.

3. Out dated settlement systems that are inadequate to cater to the growing volume, leading to

delays.

4. Lack of single market due to inability of various stock exchanges to function cohesively with

legal structure and regularity framework.

These factors led to the establishment of the NSE.

OBJECTIVES:

1. To establish a nationwide trading facility for equities, debt instruments and hybrids.

2. To ensure equal access investors all over the country through appropriate communication

network.

3. To provide a fair, efficient and transparent securities market to investors using an electronic

communication network.

4. To enable shorter settlement cycle and book entry settlement system.

5. To meet current international standards of securities market.

PROMOTERS:

12

Page 13

Industrial Development Bank of India (IDBI)

Industrial Credit and Investment Corporation of India (ICICI)

Industrial Financing Corporation of India (IFCI)

Life Insurance Corporation of India (LIC)

State Bank of India (SBI)

General Insurance Corporation (GIC)

Bank of Baroda

Canara Bank

Corporation Bank

Indian Bank

Oriental Bank of Commererce

Union Bank of India

Punjab National Bank

Infrastructure Leasing and Financial Services

Stock Holding Corporation of India

SBI capital market

MEMBERSHIP:

The membership is based on the factors as capital adequacy, corporate structure, Track

record, Education, Experience etc.Admission is a two-storage process with applicants required to

go through a written examination followed by an interview. A committee consisting of

experienced professionals from the industry, to access the applicant’s capability to operate as an

exchange member. The exchange admits members separately to whole sale debt market (WDM)

segment and the capital market segment. Only corporate members are admitted to the debt market

segment where as individuals and firms are also eligible to the capital market segment.

Eligibility criteria for trading membership on the segment of WCM are as follows:

1. The person eligible to become trading members are bodies corporate, companies, institutions

including subsidiaries of banks engaged in financial services and such other persons or entities

are may be permitted from time to time by RBI\SEBI.

2. The Whole-Time Directors should possess at least two years experience in any activity related

to banking or financial services.

3. The applicant must be engaged solely in the business of the securities and must not be engaged

in any fund-based activities.

4. The applicant must possess a minimum of Rs.2crores.

13

Page 14

Eligibility criteria for the capital market segment are:

1. Individual, registered firms, corporate bodies, companies and such other persons may be

permitted under the SCR Act, 1957.

2. The applicant may be engaged in the business of securities and must not be engaged in any

fund-based activities.

3. The minimum net worth requirements prescribed are as follows:

Individuals and registered firms-Rs.75Lakhs.

Corporate bodies-Rs100Lakhs

In case of partnership firm each partner should contribute at least 5% of the net

worth of the firm.

4. A corporate trading member should consist only of individuals (maximum of 4)

Who should directly hold at least 40% of the paid-up capital in case of listed companies and at

least 51% in case of these companies.

5.The minimum prescribed qualification of graduation and two years experience of handling

securities as broker , Sub-broker, authorized assistant etc.,must be fulfilled by

Minimum two directors in case the applicant are a corporate

Minimum two partners in case of partnership firms

In case of individual or sole proprietary concerns. The two experienced directors in a corporate

applicant or trading member should hold minimum 5% of the capital of the company.

MARK-TO-MARKET MARGIN AND INTRADAY LIMIT

Under the current clearing and settlement system, if an Indian investor buys and

subsequently sells the same number of shares of stock during a settlement period, or sells and

subsequently buys, it is not necessary to take. Or deliver the shares. The difference between the

selling and buying prices can be paid or received .In other words, the squaring –off of the trading

position during the same settlement period results in non-delivery of the shares that the investor

traded.

Thus, possible at a relatively low cost.FII’s and domestic institutional increasing Number of no

delivery transactions as the stock market becomes excessively speculative. Accordingly, SEBI

has introduced a daily mark-to-market margin and intraday trading limit. The daily market-to-

14

Page 15

market margin is a margin on a broker’s daily position. The intraday trading limit is the limit to a

broker’s intraday trading volume. Every broker is subject to these requirements.

Each stock exchange may take any other measures to ensure the safety of the market.BSE and

NSE impose on members a more stringent daily margin, including one based on concentration of

business .A daily mark-to-market margin is 100 percent of the notional loss of the stockbroker for

every stock, calculated as the difference between buying or selling price and the closing price of

that stock at the end of that day. However, there is a threshold limit of 25 percent of the base

minimum capital plus additional capital kept with the stock exchange or Rs 1 million, whichever

is lower. Until the notional loss exceeds the threshold limit, the margin is not payable.

This margin is payable by a stockbroker to the stock exchange in cash or as a bank guarantee

from a scheduled commercial bank, on a net basis. It will be released ion the pay-in day for the

settlement period .The margin money is held by the exchange for 6-12 days.

This cost the broker about 0.4-1.2 percent of the notional loss, assuming that the

broker’s funding cost is about 24-36 percent. Thus Speculative trading without the delivery of

shares is no longer cost-free. Each broker’s trading volume during a day is not allowed to exceed

the intraday trading limit. This limit is 33.3 times the base minimum capital deposited with the

exchange on a gross basis.

i.e., purchase plus sale. In the event of brokers wishing to exceed this limit, they have to deposit

additional capital with the exchange and this cannot be withdrawn for six months.

NEATSYSTEM:

Neat IS A STATE-OF-THE- ART CLIENT SERVER BASED APPLICATION. At the

server end, all trading information is stored in an in-memory database to achieve minimum

response time and maximum system availability for users. Each trading member trades on the

NSE with other members through a PC located in the trading member’s office, anywhere in India.

The trading members on the Wholesale Debt Market segment are linked to the central computer

at the NSE through dedicated 64Kbps leased lines and VSAT terminals. These leased lines are

multiplexed using dedicated 2 Mbps, optical-fiber links. The WDM participants connect to the

trading system through dial-uplinks.

NSE is one the largest interactive VSAT based stocked exchange in the world. Today

it supports more than 3000 VSATs and is expected to grow to more than 4000 VSATs in the next

year. The NSE – network in the world. Currently more than 9000 users are trading on the real

time-online NSE application. There are over 15 large computer systems.

15

Page 16

INDICES

An Index is used to give information about the price movements of products in the

financial, commodities or any other markets. Financial indexes are constructed to measure price

movements of stocks, bonds-bills and other forms of investments. Stock market indexes are

meant to capture the overall behavior of equity markets. A stock market index is created by

selecting a group of stock that are representative of the whole market or a specified sector or

segment of market. An Index is calculated with reference to a base period and base index value.

Stock market indexes are useful for a Varity of reasons. Some of them are

They provide a historical comparison of returns on money invested in the stock

market against other forms of investments such as gold or debt.

They can be used as a standard against which to compare the performance of an

equity fund.

It is a lead indicator of the performance of the overall economy or a sector of the

economy

Stock indexes reflect highly up to date information

Modern financial applications such as Index Funds, Index Futures, Index Options

play an important role in financial investments and risk management

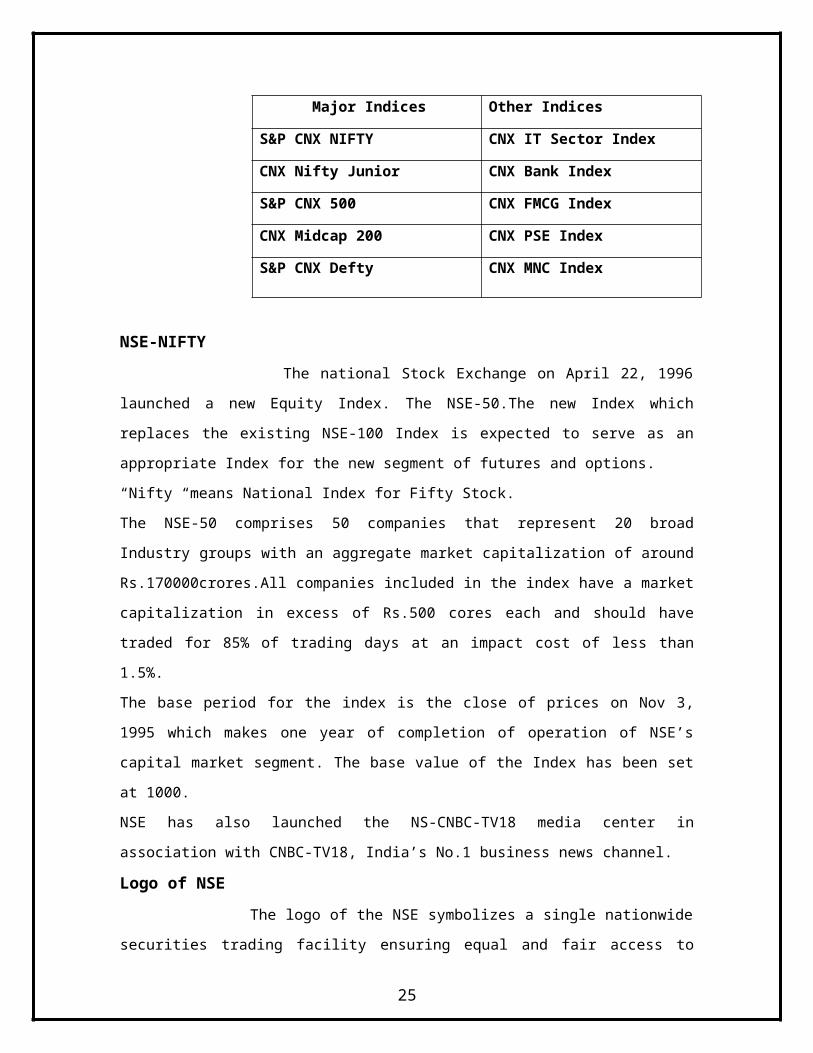

Major Indices Other Indices

S&P CNX NIFTY CNX IT Sector Index

CNX Nifty Junior CNX Bank Index

S&P CNX 500 CNX FMCG Index

CNX Midcap 200 CNX PSE Index

S&P CNX Defty CNX MNC Index

NSE-NIFTY

The national Stock Exchange on April 22, 1996 launched a new Equity Index. The

NSE-50.The new Index which replaces the existing NSE-100 Index is expected to serve as an

appropriate Index for the new segment of futures and options.

“Nifty “means National Index for Fifty Stock.

16

Page 17

The NSE-50 comprises 50 companies that represent 20 broad Industry groups with an aggregate

market capitalization of around Rs.170000crores.All companies included in the index have a

market capitalization in excess of Rs.500 cores each and should have traded for 85% of trading

days at an impact cost of less than 1.5%.

The base period for the index is the close of prices on Nov 3, 1995 which makes one year of

completion of operation of NSE’s capital market segment. The base value of the Index has been

set at 1000.

NSE has also launched the NS-CNBC-TV18 media center in association with CNBC-TV18,

India’s No.1 business news channel.

Logo of NSE

The logo of the NSE symbolizes a single nationwide securities trading facility ensuring

equal and fair access to investors, trading members and issuers all over the country. The initials

of the Exchange viz., N, S and E have been etched on the logo and are distinctly visible. The logo

symbolizes use of state of the art information technology and satellite connectivity to bring about

the change within the securities industry. The logo symbolizes vibrancy and unleashing of

creative energy to constantly bring about change through innovation.

Mission OF NSE

NSE’s mission is setting the agenda for change in the securities markets in the India. The

NSE was set-up with the main objective of:

Establishing a nation-wide trading facility for equities, debt instruments and hybrids,

Ensuring equal access to investors all over the country through an appropriate

communication network.

Providing a fair , efficient and transparent securities market to investors using

electronic trading systems,

Enabling shorter settlement cycles and book entry settlements systems, and

Meeting the current international standards of securities markets.

The standards set by NSE in terms of market practices and technologies have become industry

benchmarks and are being emulated by other market participants.NSE is more than a mere market

facilitators. It’s that force which is guiding the industry towards new horizons and greater

opportunities.

17

Page 18

Corporate Structure:

NSE is one of the first de-mutualised stock exchanges in the country, where the ownership

and management of the Exchange is completely divorced from the right to trade on it. Though the

impetus for its establishment came from policy makers in the country, it has been set up a public

limited company, owned by the leading institutional investors in the country. From day one, NSE

has adopted the form of a demutualised exchange the ownership, management and trading is in

the hands of three different sets of people.NSE is owned by a set of leading financial institutions,

banks, insurance companies and other financial intermediaries and is managed by professionals,

who do not directly or indirectly trade on the Exchange. This has completely eliminated any

conflict of interest and helped NSE in aggressively pursuing policies and practices within a public

interest framework. The NSE model however, does not preclude, but in fact accommodates

involvement, support and contribution of trading members in a variety of ways. Its Board

companies of senior executives from promoter institutions, eminent professionals in the fields of

law, economics, accountancy ,finance, taxation, etc, public representatives, nominees of SEBI

While the Board deals with broad policy issues, decisions relating to market operations are

delegated by the Board to various committees constituted by it. Such committee includes

representatives from trading members, professionals, the public and management. The day-to-day

management of the Exchange is delegated to the Managing Director who is supported by a team

of professional.

Committees:

The Exchange has constituted various committees to advise it on areas such as good

market practices, settlement procedures, risk containment systems etc.Industry professionals

manage these committees, trading members, Exchange staff as also representatives from the

market regulator.

Executive Committee

Committee On Trade Related Issues(COTI)

SECURITITIES AND EXCHANGE BOARD OF INDIA

SEBI’S ROLE IN A STOCK EXCHANGE

18

Page 19

The SEBI was established on April 12, 1998 through an administrative order, but it

became a statutory and really powerful organization only since 1992.The SEBI is under the

overall control of the Ministry of Finance, and has its head office at Mumbai.

The philosophy underlying the certain of the SEBI is that multiple regulatory bodies for securities

industry mean that the regulatory system gets dividend, causing confusion among market

participants as to who is really in command. In a multiple regulatory structure, there is also an

overlap of functions of different regulatory bodies .Through the SEBI, the regulation model

which is sought to be put in place in India is one in which every aspect of securities market

regulation is entrusted to a single highly visible and independent organization, which is backed by

a statute, and which is accountable to the parliament and in which investors can have trust.

POWER, SCOPE, AND FUNCTIONS OF SEBI:

The scope of operations of the SEBI is very wide; it can frame or issue rules,

regulations, directives, guidelines, norms in respect of both primary and secondary markets, and

certain financial institutions.

The SEBI is empowered to register any agency or intermediary who may be associated

with the securities market and none of them shall by, sell or deal in securities except under and in

accordance with the conditions of certificate of registration issued by the SEBI.

The SEBI can suspend or cancel a certificate of registration issued by it to anyone after

giving him a reasonable opportunity of being heard.

However, in exercise of its powers and in performing its functions, such directions on

questions of policy bind the SEBI as the GOI may give in writing from time to time. Although it

has the opportunity to express its views before any direction is given, the decision of the GOI is

final in every case.

19

Page 20

COMPANY PROFILE:

ZEN SECURITIES LTD:

Zen Securities Limited (ZSL) is one of the leading financial services company -

providing Financial and Investment related Services and Products. The Company commenced as

a proprietary concern of M/s K. Ravindra Babu in 1986 was converted to a Limited company in

February 1995 as Zen Securities Ltd. Zen has the distinction of being the First Corporate Member

from Hyderabad and also the first A.P. based broking firm to start trading on the National Stock

Exchange (NSE). ZEN is a registered Member on the Capital Market Segment and Futures &

Options segment of both NSE and BSE.

ZEN is also a Depository Participant (DP) with National Securities Depository Ltd.

(NSDL) and also with Central Depositories Services Ltd. (CDSL). ZEN is also a SEBI Registered

Portfolio Manager offering Portfolio Management Services to clients.

In 29-08-2008 Zen Securities lanches brand name as ZEN MONEY LTD.

Zen Comtrade Pvt. Limited:

A 100% subsidiary of ZSL and is a member of National Commodities & Derivatives

Exchange Limited (NCDEX) and Multi Commodity Exchange (MCX). ZEN operates from

Hyderabad as it head office and has branches and associates in Andhra Pradesh, Tamil Nadu,

Maharashtra, Karnataka, West Bengal and Orissa. The Company operates from over 140

locations with over 500 trading terminals.

Services Offered by Zen Securities Limited:

20

Page 21

Investment advisory services

Trading in cash market of NSE and BSE

Trading in Futures and Options on NSE and BSE

Internet Trading in Stocks, futures and Options both NSE and BSE

Mutual Funds advisory service

Depository Services in Both NSDL and CDSL

Trading in Commodities on MCX and NCDEX

Portfolio Management Services

NRI Investor Services

PAN Application Service

Mutual Fund KYC Registration Service

Fixed Income Securities / Fixed Deposits / RBI Bonds / Tax Saving Bonds

FOUNDER:

Shri Ravindra Babu Kantheti founded Zen Securities Ltd as a stock broking company and led its

evolution into a highly respectable financial services company known for its ethics and values.

He passionately believed that one can be successful in business without compromising on ethics.

Thru Zen he demonstrated this philosophy and inspired every one of us by setting an example.

His ethical, transparent and trustworthy approach to business has inspired all of us to build a very

vibrant, successful and strong organization.

We at Zen totally rededicate ourselves to continue to build the organization on sound foundations

of trust, values and relationship with clients, servicing their investment needs as set out by our

founder Sri K.Ravindra Babu.

The board of directors of Zen Securities Ltd has appointed Mr Pratap Kantheti and Mr Satish

Kantheti as Managing Director and Joint Managing Director, respectively, of the company. The

board at its meeting on 16-04-2008 expressed sorrow at the sudden demise of Mr K. Ravindra

Babu, Founder Managing Director of Zen Securities Ltd. Both Mr Pratap and Mr Satish have

been working with Zen Securities as Directors for over a decade.

21

Page 22

BOARD OF DIRECTORS:

Directors of Zen Securities Ltd. have considerable experience and expertise ranging over many

industries such as financial services, pharmaceuticals, manufacturing, banking and Information

Technology among others. They are some of the most highly respected people in their

professional circles.

Mr. Pratap Kantheti, Managing DirectorMr. Pratap Kantheti is the Managing Director of the company. He is a Chartered Financial

Analyst (CFA) and also has a Masters in Business Administration (MBA) in Finance. He has a

deep understanding of and exposure to the financial services sector.

Mr. Satish Kantheti, Jt. Managing DirectorMr. Satish Kantheti looks after the Portfolio Management Services and Equity Research divisions

of the Company. He is a Chartered Financial Analyst (CFA) and also has a Masters in Business

Administration (MBA) in Finance. He oversees the Equity Research division and the Portfolio

Management divisions.

Mr. K. Gandhi, Director

Mr. K. Gandhi is one of the founder directors of the company. He holds a Masters degree in

Electrical and Communication Engineering from IIT Bombay. He has extensive experience in IT

and General Management.

Mr. Satyanarayana Ch. Ravi (RS), Whole Time Director

Mr. Satyanarayana Ch. Ravi has more than two decades of experience in the fields of

Management, Administration, Manufacturing, and Marketing. He holds a Bachelors degree in

Chemical Engineering.

Mr. Sambasiva Rao Patibandla, Executive DirectorMr. Sambasiva Rao has worked with several multinational pharmaceuticals companies before

incorporating and running a successful pharmacy business venture in U.S. He relocated to India

entered the Stock broking industry in 1994. He is the Executive Director of company. He has a

Masters degree in Pharmacy.

Mr. Narayanan Narayanan, Director

22

Page 23

Mr. Narayanan is a very experienced Investment Analyst and Tax Consultant possessing a deep

understanding about investments and stock market dynamics.

Mr. Ajay Kumar Mikkilineni, DirectorMr. Ajay Kumar Mikkilineni has over a decade of experience in senior positions of the

Pharmaceutical industry and also has twelve years of experience in the banking sector. He holds a

Masters degree in Agriculture.

Mr. K.Venkat Reddy, DirectorMr. K.Venkat Reddy is a chemical engineer. He worked in reputed industrial houses in Paper &

Power sectors for 16 years and in financial markets for 10 years. He has extensive experience in

the areas of project management and strategic management..

Mr. K. Narasimha Rao, Director

Mr. K. Narasimha Rao is a Post Graduate in Literature. He is the Chief Agent of A.P. LIC Mutual

Fund since June 2002. He is an LIC agent since 1980 and has extensive knowledge about the

securities and insurance markets.

Mr. Namashivaya Renukuntla, Director and Head of ComplianceMr. Namashivaya Renukuntla has vast experience in the field of stock broking and has a deep

understanding of the regulatory framework of the Capital Markets. He heads the Commodity

Broking business of the Company. He holds a bachelors degree in Civil Engineering and a

Masters in Business Administration (MBA.)

SERVICES:

Stock Broking

Zen Securities Limited provides the following equity related trading services to the investors:

o Capital Market Segment of NSE and BSE

o Futures & Options segment of NSE and BSE

ZEN operates from Hyderabad as it head office and has branches and associates in Andhra

Pradesh, Tamil Nadu, Maharashtra, Karnataka, West Bengal and Orissa. The Company operates

from over 140 locations with over 500 trading terminals.

23

Page 24

Internet Trading:

Internet trading is easy, convenient and reliable with ZenTr@de

Advantages of ZenTr@de - Internet Trading Platform

Flexible and advanced trading platform

Simple, reliable and easy to use

Futures & Options segment of NSE and BSE

Integrated payment gateways – facilitates online transfer of funds from your banks (ICICI

/Axis/Corp / Yes bank etc.) for instant limits (on funds transferred)

Integrated with Zen DP account – seamless settlement

Take full control of trading and trade with privacy from any place of your choice.

Choice of Trading from Internet or Branch

Choice of Browser based or EXE based trading

Market watch

Streaming market quotes

Multiple market watch

Integrated market watch for viewing NSE / BSE / NSE FAO on one screen

Access to trade in NSE / BSE and NSE FAO Segments

INTRADAY and DELIVERY differentiation

Different limits for INTRADAY and DELIVERY

Auto square off of all INTRADAY orders 15 minutes before close of trading

Convert INTRADAY trades to DELIVERY trades on availability of credit/margin source

Access to statements

Stock Statements - View Stocks in your DP account and also Zen Benf account

Statements – View Cash available in your Zen Broking account

Mutual Funds – View Transaction/Holding statements with Latest NAV’s

24

Page 25

Net worth Statement - Net worth statement of assets with Zen, (Stocks+Cash+Mutual

funds).

Mutual Funds:

ZEN’S MUTUAL FUND SERVICES - HIGHLIGHTS

One stop shop for a range of Mutual fund products from top Mutual funds such as HDFC,

ICICI Prudential, Birla sun life, Franklin Templeton, Reliance , HSBC, Sundaram BNP

Paribas, Fidelity and many more

Cost-effective, prompt and trustworthy service

Facility to view your account information online 24 X 7, Updates every day.

o You can view your latest Holding statement

o You can view your latest transaction statement

o You can view value of all your mutual funds in one consolidated statement

Easy and convenient application process

Good Advice keeping your financial goals in mind

Offline presence in various locations convenient to you for better service

¤ CONCEPT

¤ ORGANISATION OF A MUTUAL FUND

¤ ADVANTAGES OF MUTUAL FUNDS

CONCEPT: A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is then invested in capital market instruments

such as shares, debentures and other securities. The income earned through these investments and

the capital appreciation realized is shared by its unit holders in proportion to the number of units

owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it

offers an opportunity to invest in a diversified, professionally managed basket of securities at a

relatively low cost. The flow chart below describes broadly the working of a mutual fund:

25

Page 26

Organization of a Mutual Fund

There are many entities involved and the diagram below illustrates the organizational

set: up of a mutual fund.

ADVANTAGES OF INVESTING IN MUTUAL FUNDS

Professional Money Management & Research

Mutual funds are managed by professional fund managers who regularly monitor market

trends and economic trends for taking investment decisions. They also have dedicated research

professionals working with them who make an in depth study of the investment option to take an

informed decision.

Risk Diversification Diversification reduces risk contained in a portfolio by spreading it. It is about not putting

all your eggs in one basket. As mutual funds have huge corpuses to invest in, one can be part of a

large and well-diversified portfolio with very little investment.

Convenience

26

Page 27

With features like dematerialized account statements, easy subscription and redemption

processes, availability of NAVs and performance details through journals, newspapers and

updates and lot more; Mutual funds are sure a convenient way of investing.

Liquidity

One of the greatest advantages of Mutual funds investment is liquidity. Open-ended

funds provide option to redeem on demand, which is extremely beneficial especially during rising

or falling Markets.

Reduction in Costs

Mutual funds have a pool of money that they have to invest. So they are often involved

in buying and selling of large amounts of securities that will cost much lower than when you

invest on your own.

Tax Advantages

Investment in mutual funds also enjoys several tax advantages. Dividends from Mutual

Funds are tax-free in the hands of the investor (This however depends upon changes in Finance

Act). Also Capital Gain accrued from Mutual Fund investment for a period of over one year is

treated as long term capital appreciation and is tax free.

Other Advantages

Indian Mutual fund industry also presents several other benefits to the investor like:

transparency - as funds have to make full disclosure of investments on a periodic basis, flexibility

in terms of needs based choices, very well regulated by SEBI with very strict compliance

requirements to investor friendly norms.

DEPOSITORY SERVICES:

DEPOSITORY:

Zen is a depository participant offering flexible, cost effective and transparent

depository services to its clients .Zen is a depository participant with the National Securities

Depository Limited and Central Depository Services (India) Limited for trading and settlement of

dematerialized shares. Zen performs clearing services for all securities transactions through its

accounts. Zen offers depository services to create a seamless transaction platform – execute trades

through Zen Securities and settle these transactions through the Zen Depository Services. Zen

Depository Services is a part of our value added services for our clients that creates multiple

interfaces with the client and provides for a solution that takes care of all your needs

27

Page 28

Basic Services Provided by Zen DP

Account Opening

Account Transfers - Market and Off-Market

Dematerialization

Re-materialization

Pledge

FEATURES:

Zen is a depository participant with National Securities Depository Limited (NSDL) and Central

Depository Service Limited (CDSL) offering flexible, cost effective and transparent depository

services to its clients. Owning a demat a/c with Zen is the ideal option as it entails:

Access to DP account like Holdings (With Holding valuation), Transactions & ISIN

details in our site.

Provision of Portfolio value on account statement.

Limited power of attorney (LPOA) facility for clients having broking / trading A/c. with

Zen, eliminating the need for giving instructions every time a sale is executed l through

Zen.

Very low annual charge and transaction charges.

Mailing of a regular transaction statement, free of cost to all account holders showing an

opening balance, debit/credit and closing balance for securities held.

Facility to log on to the NSDL web site ( IDEAS ) and view your account/ transactions

directly from NSDL (Note : This service is available on subscription to Ideas)

Accounts freeze/defreeze facility, security wise and quantity wise.

DOCUMENTATIONS:

Documentation for Account OpeningIn order to open a Demat account, you will need to provide/produce the following documents

1. INDIVIDUALS

Duly filled (in block letters) Demat Account Opening Form & Depository Client

Agreement.

A photograph of each holder / signatory to be pasted on the form and signed across.

28

Page 29

A photocopy of the PAN card for each holder is compulsory.

Proof of identity (any one of the below mentioned)

o Passport, Voter ID Card, Driving license,

o PAN card with Photograph,

o MAPIN card,

o Proof of Identity cum Address form (Attested by a scheduled commercial Bank

Manage

o Identity card/document with applicant’s photo, issued by:

Central/State Government and its Departments,

Statutory/ Regulatory Authorities,

Public Sector Undertakings,

Scheduled Commercial Banks,

Public Financial Institutions,

Colleges affiliated to Universities,

Professional Bodies such as ICAI, ICWAI, and ICSI, Bar Council etc. to

their Members

Credit cards/Debit cards issued by Banks.

Proof of Address (any one of the below mentioned)

o Ration card, Passport, Voter ID Card, Driving license, Bank passbook,

o Verified copies of Electricity bills (Not more than two months old)/ Residence

Telephone bills (not more than two months old).

o License agreement / Agreement for sale, Self-declaration by High Court &

Supreme Court judges, giving the new address in respect of their own accounts.

o Proof of Identity cum Address form (Attested by a scheduled commercial Bank

Manager)

o Identity card/document with address, issued by

Central/State Government and its Departments.

Statutory/Regulatory Authorities.

Public Sector Under takings.

Scheduled Commercial Banks.

Public Financial Institutions.

29

Page 30

Colleges affiliated to universities and

Professional Bodies such as ICAI, ICWAI, Bar Council etc., to their

Members.

Nomination form (If required)

Note:

If the Current Address is same as in Passport / Voter's ID card / Driving license / MAPIN Card

then Proof of Address not required.

2. CORPORATE ACCOUNTS

Duly filled (in block letters) Demat Account Opening Form & Depository Client

Agreement.

A copy of

Certificate of Incorporation,

Certificate of Commencement of Business

Memorandum and Articles of Association.

Board Resolution for opening of the Demat Account and authorising the authorised

signatories to operate the Demat account.

A copy of Bank Pass Book.

Authorised Signatory Photos, Company Common seal on resolution.

Pool Accounts:

NSE Pool A/c

CM / Client Id: 10000634

CM / Client Name: Zen Securities Ltd.

CM-BP-Id: IN562308

DP Id: IN302863

DP Name: Zen Securities Ltd.

BSE Pool A/c

30

Page 31

CM / Client Id: 10005679

CM / Client Name: Zen Securities Ltd.

CM-BP-Id: IN609255

DP Id: IN302863

DP Name: Zen Securities Ltd.

F & O Benf. A/c

Client Id: 10000116

Client Name: Zen Securities Ltd.

DP Id: IN302863

DP Name: Zen Securities Ltd.

LITERATURE SURVEY

DERIVATIVES:-

The emergence of the market for derivatives products, most notably forwards, futures and options,

can be tracked back to the willingness of risk-averse economic agents to guard themselves against uncertainties

arising out of fluctuations in asset prices. By their very nature, the financial markets are marked by a very high

degree of volatility. Through the use of derivative products, it is possible to partially or fully transfer price risks

by locking-in asset prices. As instruments of risk management, these generally do not influence the fluctuations

in the underlying asset prices. However, by locking-in asset prices, derivative product minimizes the impact of

fluctuations in asset prices on the profitability and cash flow situation of risk-averse investors.

Derivatives are risk management instruments, which derive their value from an underlying asset. The

underlying asset can be bullion, index, share, bonds, currency, interest, etc.. Banks, Securities firms, companies

and investors to hedge risks, to gain access to cheaper money and to make profit, use derivatives. Derivatives are

likely to grow even at a faster rate in future.

31

Page 32

INTRODUCTION TO FUTURES CONTRACTS:

In the Derivatives market Futures contract is most actively traded contract. It has gained its

momentum in recent years, after forwards contract were banned in some parts of the world. It is one of

the most popular types of contracts for the traders in the world.

FUTURES CONTRACT:

Futures contract was designed to solve limitations that existed in forward contracts. Futures

contract is an agreement between two parties to buy or sell an asset at a certain time in future at a certain

price. To make it simple Futures are exchange-traded contracts to buy or sell an asset in future at a price

agreed upon today. The asset can be share, index, interest rate, bond, rupee-dollar exchange rate, sugar,

crude oil, soybean, cotton, coffee etc.

To facilitate liquidity in the futures contract, the exchange specifies certain standard features of

the contract. It is a standardized contract with standard underlying instrument.

The following are the Standard terms in any Futures contract:

Quantity of the underlying asset

Quality of the underlying asset (not required in case of financial futures)

Expiration date

The unit of price quotation (not the price)

Minimum fluctuation in price (tick size)

Settlement style

Example:

when you are dealing in March 2002 Satyam futures contract, you know that the market lot,

i.e. the minimum quantity you can buy or sell, is 1,200 shares of Satyam, the contract would expiry on

March 28, 2002, the price is quoted per share, the tick size is 5 paisa per share or (1200*0.05) = Rs 60 per

contract/ market lot, the contract would be settled in cash and the closing price in the cash market on

expiry date would be the settlement price.

TERMINOLOGY USED IN FUTURES MARKET:

32

Page 33

The terminologies used in futures market are as follows:

SPOT PRICE:

The price at which an asset trades in the spot market.

FUTURE PRICE:

The price at which the futures contract trades in the futures market.

CONTRACT CYCLE:

The period over which a contract trades.

BASIS :

It is the difference between future price and the spot price. Popularly termed as spread among the trading

community.

INITIAL MARGIN:

The amount deposited in the margin account, when the future contract is first entered.

MARKING TO MARKET:

In the futures market, at the end of each trading day, the margin account is adjusted to reflect

the investors gain or loss depending upon the futures closing price. This is called as marking to market.

MAINTENANCE MARGIN:

It is the minimum margin the investor has to keep in his account, so that it never shows negative

balance.

PRICING FUTURES THEORYTICALY:

The theoretical price of a futures contract is spot price of the underlying plus the cost of carry.

Please note that futures are not about predicting future prices of the underlying assets.

In general, Futures Price = Spot Price + Cost of Carry

The Cost of Carry is the sum of all costs incurred if a similar position is taken in cash market and

carried to expiry of the futures contract less any revenue that may arise out of holding the asset. The cost

typically includes interest cost in case of financial futures (insurance and storage costs are also considered

33

Page 34

in case of commodity futures). Revenue may be in the form of dividend. Though one can calculate the

theoretical price, the actual price may vary depending upon the demand and supply of the underlying

asset.

Example:

Suppose Reliance shares are quoting at Rs 300 in the cash market. The interest rate is about

12% per annum. The cost of carry for one month would be about Rs 3. As such a Reliance future contract

with one-month maturity should quote at nearly Rs303. Similarly Nifty level in the cash market is about

1100. One month Nifty future should quote at about 1111. However it has been observed on several

occasions that futures quote at a discount or premium to their theoretical price, meaning below or above

the theoretical price. This is due to demand-supply pressures. Every time a Stock Future trades over and

above its cost of carry i.e. above Rs. the arbitragers would step in and reduce the extra premium

commanded by the future due to demand. E.g.: would buy in the cash market and sell the equal amount in

the future, Hence creating a risk free arbitrage, vice-versa for the discount.

When the future contract approaches expiry date, the cost of carry reduces as the time to expiry

reduces; thus futures and cash prices start converging. On expiry date, futures price should equal cash

market price.

Settlement in Futures markets:

34

Page 35

Presently both stock and index futures are settled in cash. The closing price in the cash segment is

considered as the settlement price. The difference between the trade price and the settlement price is

ultimately your profit/loss.

In case of delivery based settlement Stock-based derivatives are expected to be settled in delivery.

On expiry of the futures contract, the buyer/seller of the future would receive a long/short position at the

closing price in the cash segment on the next trading day. This position in the cash segment would merge

with any other position the buyer/seller has. In case the buyer/seller wants he can square up this position

by selling/buying the shares. Or else he would be required to deliver/receive the underlying shares on the

settlement day (e.g. T+2) in the cash segment.

The aforesaid methodology is not final yet. Sebi guidelines in this regard are awaited. You can call

exchanges and me to know the exact methodology once the regulator. Index based Derivatives would

continue to be settled in cash

USAGE of Futures contracts:

You can do directional trading using futures. In case you are bullish on the underlying stock or

index, you can simply buy futures on stock/index. Similarly if you are bearish on the underlying, you can

sell futures on stock/index.

There are eight basic modes of trading on the index futures market:

Hedging

H1 Long stock, short Nifty futures

H2 Short stock, long Nifty futures

H3 Have portfolio, short Nifty futures

H4 Have funds, long Nifty futures

Speculation

S1 Bullish index, long Nifty futures

S2 Bearish index, short Nifty futures

Arbitrage

A1 Have funds, lend them to market

A2 Have securities, lend to the market

35

Page 36

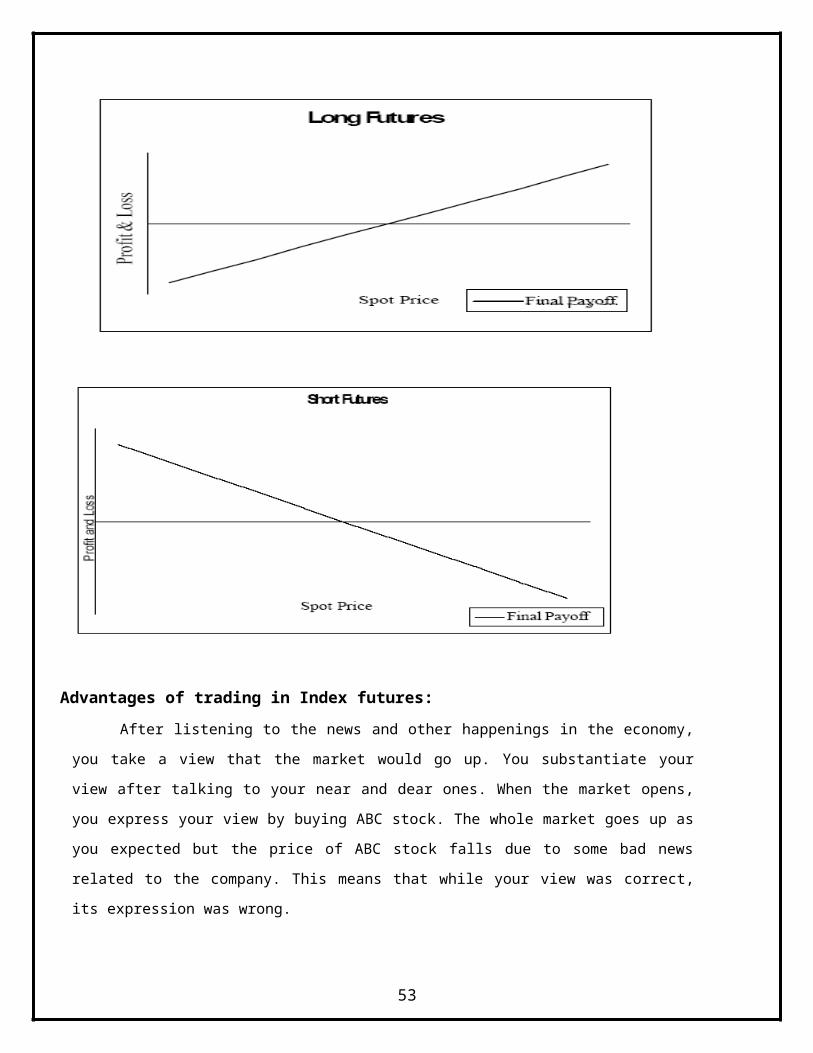

Advantages of trading in Index futures:

After listening to the news and other happenings in the economy, you take a view that the market

would go up. You substantiate your view after talking to your near and dear ones. When the market

opens, you express your view by buying ABC stock. The whole market goes up as you expected but the

price of ABC stock falls due to some bad news related to the company. This means that while your view

was correct, its expression was wrong.

Using Nifty/Sensex futures you can express your view on the market as a whole. In this case you

take only market risk without exposing yourself to any company specific risk. Though trading on Nifty or

Sensex might not give you a very high return as trading in stock can, yet at the same time your risk is also

limited as index movements are smooth, less volatile with unwanted swings.

36

Page 37

When trading futures in cash the biggest advantage of futures is that you can short sell without

having stock and you can carry your position for a long time, which is not possible in the cash segment

because of rolling settlement. Conversely you can buy futures and carry the position for a long time

without taking delivery, unlike in the cash segment where you have to take delivery because of rolling

settlement.

Further futures positions are leveraged positions, meaning you can take an Rs 100 position by paying Rs

25 margin and daily mark-to-market loss, if any. This can enhance the return on capital deployed. For

example, you expect an Rs 100 stock to go up by Rs 10. One way is to buy the stock in the cash segment

by paying Rs 100. You make Rs 10 on investment of Rs 100, giving about 10% returns. Alternatively you

take futures position in the stock by paying about Rs 30 toward initial and mark-to-market margin. You

make Rs 10 on investment of Rs 30, i.e. about 33% returns. Please note that taking leveraged position is

very risky, you can even lose your full capital in case the price moves against your position. You can

square up your future at any time once you have initiated the position, you need not wait until its expiry

you can book profits or cut losses.

One can use volume and open interest rates to predict the movement of the market this is done

like this, the total outstanding position in the market is called open interest. In case volumes are rising and

the open interest is also increasing, it suggests that more and more market participants are keeping their

positions outstanding. This implies that the market participants are expecting a big move in the price of

the underlying. However to find in which direction this move would be, one needs to take help of charts.

In case the volumes are sluggish and the open interest is almost constant, it suggests that a lot of

day trading is taking place. This implies sideways price movement in the underlying.

When Corporate Dividends are announced:

In the event of such corporate announcements, the exchanges adjust the position such that

economical value of your position on cum-benefit and on ex-benefit day is the same. While calculating

the theoretical price of a futures contract, the interest rate should be taken as net of dividend yield. So on

announcement of the dividend, the futures price should be discounted by the dividend amount. However

as per the policy of Sebi and stock exchanges, if the dividend is more than 10% of the market price of the

stock on the day of dividend announcement, the futures price is adjusted. The exchanges roll over the

positions from last-cum-dividend day to the ex-dividend day by reducing the settlement price by

dividend. In such a case, the announcement of such exceptional dividends does affect the price of futures.

37

Page 38

Suppose Reliance is trading at Rs 300 and a two-month Reliance future which has 45 days to

maturity is trading at Rs 304. Reliance declares 50% dividend, i.e. Rs 5. The dividend amount is less than

10% of the market price of Reliance, so the exchange would not adjust the position. As such the market

adjusts this dividend in the market price and the futures price goes down by Rs 5 to Rs 299.

In case of Bonus the lot size of the stock that gives bonus gets adjusted according to the ratio of

the bonus. The position is transferred from cum-bonus to ex-bonus day by adjusting the settlement price

to neutralize the effect of bonus.

For example:

The current lot size of Cipla is 200. Suppose Cipla announces a bonus of 1:1. You are long on 200

shares of Cipla and the settlement price of Cipla on cum-bonus day is Rs 1,000. On ex-bonus day your

position becomes long on 400 shares at Rs 500. Thereafter the lot size of Cipla would be 400.

Hedging of stock positions using futures:

Suppose you are holding a stock that has futures on it and for two to three weeks the stock does

not look good to you. You do not want to lose the stock but at the same time you want to hedge against

the expected adverse price movement of the stock for two to three weeks. One option is to sell the stock

and buy it back after two to three weeks. This involves a heavy transaction cost and issue of capital gain

taxes. Alternatively you can sell futures on the stock to hedge your position in the stock. In case the stock

price falls, you make profit out of your short position in the futures. Using stock futures you would

virtually sell your stock and buy it back without losing it. This transaction is much more economical as it

does not involve cost of transferring the stock to and from depository account. You might say that if the

stock had moved up, you would have made profit without hedging. However it is also true that in case of

a fall, you might have lost the value too without hedging. Please remember that a hedge is not a device to

maximize profits, it is a device to minimize losses. As they say, a hedge does not result in better outcome

but in predictable outcome.

You can hedge your cash market position in stocks that do not have stock futures by using index

futures. Before we go any further, we need to understand the term called beta. Beta of a stock is nothing

but the movement of the stock relative to the index. So suppose a stock X moves up by 2% when the

Nifty moves up by 1% and it goes down by 2% when the Nifty falls by 1%, the beta of this stock is 2.

Beta is crucial in deciding how much position should be taken in index futures to hedge the cash market

position. Suppose you have a long position in ABB worth Rs 2 lakh. The beta of ABB is 1.1. To hedge

38

Page 39

this position in the cash market you need to take an opposite position in Nifty futures worth 1.1 x 2, i.e.

worth Rs 2.2 lakh. Suppose Nifty futures are trading at 1100 and the market lot for Nifty futures is 200.

Then each market lot of Nifty is worth Rs 2.2 lakh. Therefore to hedge your position in ABB you need to

sell one contract of Nifty futures.

Hedging with index futures are not perfect, Hedging is like marriage and one should not expect it

to be perfect. The beta taken in the calculation of the position of Nifty futures is historical and there is no

guarantee that it will be the same in future. So, any deviation of beta makes the hedge imperfect. Suppose

you want to hedge your position in ABB for 15 days and during those 15 days ABB becomes very

volatile and the beta goes up as high as 1.5. In this case your hedging position of one contract is not

sufficient and you will be under hedged. It is very difficult (in fact impossible) to get perfect hedge but

one can improve the perfection by adjusting the position in Nifty futures from time to time.

Demystifying Stock Futures

Here we try to solve some myths about futures

When some liquid money is available to you and you are trying to buy future stocks for risk free interest.

Using stock futures you can deploy this money to earn risk-free interest. Suppose Satyam is quoting at Rs

300 in the cash segment and one-month future is quoting at 305, you can earn risk-free interest by

following the steps mentioned below:

Buy Satyam in cash market at Rs 300 and simultaneously sell Satyam future at Rs 305.

Pay Rs 300 to take delivery of Satyam stock in cash market.

On expiry of Satyam future contract, the short position would be transferred to your account

in the cash segment and a delivery order would be issued against you.

Deliver the Satyam stock.

Whatever happens to the price of Satyam, you earn Rs 305 - 300 = 5 on Rs 300 for one

month.

Need to have mark-to-mark margins in your account, incase Satyam moves up.

If required the future position can be rolled over to the next month position with a difference of Rs 4-5.

This roll-over process can continue till you want to get your money back.

The above example was about how earn risk free interest when liquid cash is available with you, when

the futures stock is going down in futures market but going up in the cash segment then we can do the

following:

39

Page 40

Suppose one-month SBI future is quoting at 200 while SBI is quoting at Rs 205 in the cash segment.

Follow the steps mentioned below to make risk-free money.

Sell SBI in the cash market at Rs 205 and simultaneously buy SBI future at 200.

Receive Rs 205 and make delivery of SBI stock in the cash market.

On expiry of the SBI future contract, the long position would be transferred to your account in the

cash segment and a receive order would be issued to you.

Get your SBI stock back.

Whatever happens to the price of SBI, you earn Rs 205 – 200 = 5 on your stock.

rrow against the future stock and that is the advantage of futures. Instead of going to the banker

and complying with a whole lot of formalities, you can in fact just call me to help you raise

money against your shares using futures.

Suppose ACC is quoting at Rs 150 in the cash segment and one-month ACC futures are quoting at 152.

Follow the steps mentioned below to raise money against your ACC shares.

Sell ACC in the cash market at Rs 150 and simultaneously buy ACC futures at 152.

Receive Rs 150 and make delivery of ACC stock in the cash market.

On expiry of the ACC futures contract, the long position would be transferred to your account in

the cash segment and a receive order would be issued to you.

Get your ACC stock back.

Whatever happens to the price of ACC, you lose Rs 152 – 150 = 2 to raise money against your

shares as cost.

You might have seen that spot price and future price varies in the intra day trading, in that

case you can do arbitrage to raise money in that situations. When the futures are quoting at a premium to

their theoretical price, one can buy cash and short futures. When the prices come in line, that is when the

difference between the futures and cash prices comes down, reverse the positions. Conversely when the

futures are quoting at a discount to the theoretical price, one can sell cash and buy futures. When the

prices come in line, that is the difference between the futures and cash prices goes up, reverse the

positions. This way it is possible to take advantage of fluctuations in the basis. Please note that there is the

risk of execution of order. Also you need to decide the arbitration band depending on the transaction cost

you bear.

INTRODUCTION TO OPTIONS MARKET:

40

Page 41

In this section, we look at the next Derivative product to be traded at NSE, namely Options.

Options are fundamentally different from Forward and Futures contracts. An option gives the holder the

right do something; the holder does not have to exercise this price.

OPTIONS MARKET:

Options are contracts that give the buyers the right (but not the obligation) to buy or sell a

specified quantity of certain underlying asset at a specified price on or before a specified date. On the

other hand, the seller is under obligation to perform the contract (buy or sell the underlying). The

underlying asset can be share, index, interest rate, bond, rupee-dollar exchange rate, sugar, crude oil,

soybean, cotton, coffee etc.

For example:

A railway ticket is an option in daily life. Using the ticket, a passenger has an option to travel. In

case he decides not to travel, he can cancel the ticket and get a refund. But he has to pay a cancellation

fee, which is analogous to the premium paid in an option contract. The railways on the other hand have an

obligation to carry the passenger if he decides to travel and refund his money if he decides not to travel.

In case the passenger decides to travel the railways get the ticket fare. In case he does not then they get

the cancellation fee. The passenger on the other hand, by booking ticket he has hedged his position in

case he has to travel as anticipated. In case the travel does not materialize, he can get out of the position

by canceling the ticket at a cost, which is the cancellation fee.

Example 2:

Suppose you have a right to buy 1,000 shares of Hindustan Lever at Rs 250 per share on or

before March 28, 2002. In other words you are a buyer of a call option on Hindustan Lever. The option

gives you the right to buy 1,000 shares. You have the right to buy Hindustan Lever shares at Rs250 per

share. The seller of this call option who has given you the right to buy from him is under obligation to sell

1,000 shares of Hindustan Lever at Rs250 per share on or before March 28, 2002 whenever asked.

Option Terminology:

There are some basic terminologies used in options, they are as follows:

Index option: These options have the index as the underlying. Some options are European options

while others are American options. Indexed option contracts settled in cash.

Stock option:

41

Page 42

Stock options are options on individual stocks. Options currently traded on more than 500

stocks in the United States. The contract gives the holder the right to buy or sell shares.

Option holder: Buyer if the option who has the right.

Option writer: Seller of the option who has the obligation.

Premium: The consideration paid by the buyer for the right.

Call option: Option that gives the holder the right to buy.

Put option: The option that gives the holder the right to sell.

American option: These are options that are exercised at any point till the expiration date.

European option: These are option that can be exercised only on the expiration date.

In the money: It is an option that would lead to profits if it were exercised immediately.

Out of money: It is an option that would lead to loss if exercised immediately.

At the money: It is an option that would even the holder’s option if exercised immediately.

How money is made in the option market?

The money made in the option market is known as option pay off. There can be two

types of option pay off.

Call option

Put option

Call option:

A call option gives the holder the right to buy shares. The option holder will make money if

the spot price is higher than the strike price. The pay off assumes that the option holder will buy at the

strike price and sell immediately at the spot price. But if the spot price is lower than the strike price the

holder can simply ignore the option. Here the profits for the option holder are unlimited while the losses

are limited.

Example1:

Suppose you have a right to buy 1,000 shares of Hindustan Lever at Rs250 per share on or before

March 28, 2002. In other words you are a buyer of a call option on Hindustan Lever. The option gives

you the right to buy 1,000 shares. You have the right to buy Hindustan Lever shares at Rs250 per share.

The seller of this call option who has given you the right to buy from him is under obligation to sell 1,000

shares of Hindustan Lever at Rs250 per share on or before March 28, 2002 whenever asked.

42

Page 43

Example2:

Assume you have the right to buy 200 Nifty units at 1100. In other words, you are a buyer of a call