28

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

Agenda

1. Industry Facts

2. Ship recycling Boom and Corrections

3. Ship Recycling: Source of Recovery?

4. Changing Role of Cash Buyer

5. Closing Thoughts

18th November 2013 GMS Ship Recycling Conference - Tokyo 2

1.1. Industry Facts

Cash Buying has evolved into a huge industry with large economic, environmental and

social impacts. In 2012 alone, roughly $5.1 billion worth of scrap ships were

purchased for recycling.

Throughout 2012 about 56.5 million DWT was recycled vs. total of 40.6 million in 2011

• Dry Bulk: 35.7 mill DWT vs. 25.3 mill in 2011

• Wet: 13.7 mill DWT vs. 10.4 mill in 2011

Average age:

2011 - 37 years old 2012 - 31 years old 2013 - 29 years old

INDUSTRY BREAKDOWN (2012)

INDIAN SUB

CONTINENT CHINA TURKEY

No. of Vessels 760 232 282

Lightweight (lt) 8,790,220 2,027,000 912,401

Amount (US$) 3.9 bill 850 mill 283 mill

Note: all figures are approximates

18th November 2013 GMS Ship Recycling Conference - Tokyo 3

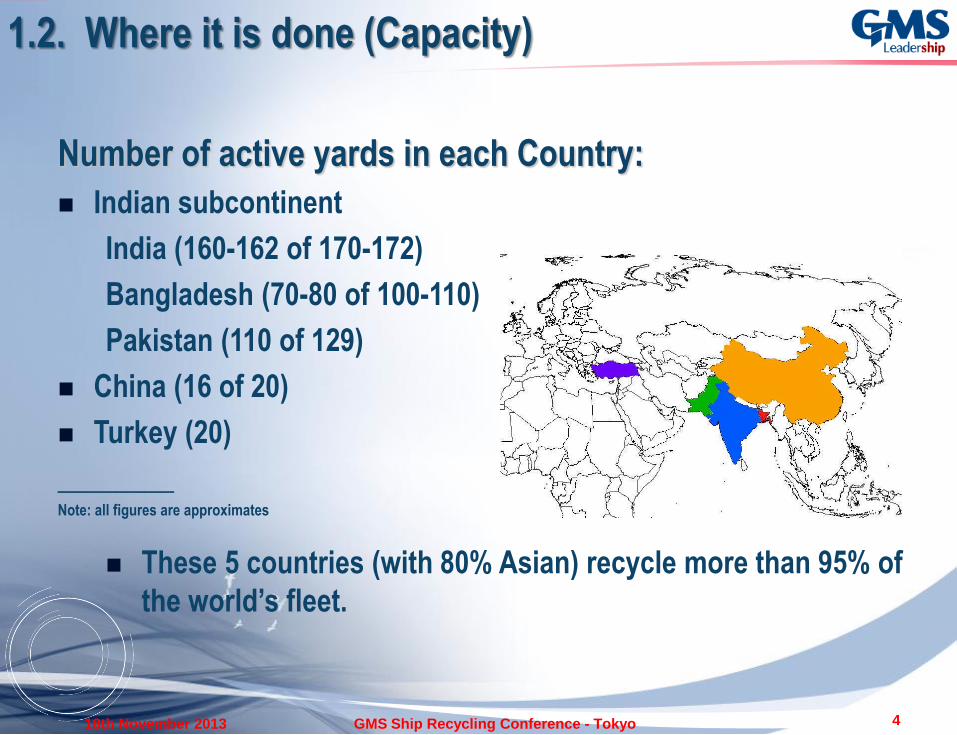

1.2. Where it is done (Capacity)

Number of active yards in each Country:

Indian subcontinent

India (160-162 of 170-172)

Bangladesh (70-80 of 100-110)

Pakistan (110 of 129)

China (16 of 20)

Turkey (20)

________ Note: all figures are approximates

These 5 countries (with 80% Asian) recycle more than 95% of

the world’s fleet.

18th November 2013 GMS Ship Recycling Conference - Tokyo 4

1.3.1. India

18th November 2013 GMS Ship Recycling Conference - Tokyo 5

1.3.2. India

18th November 2013 GMS Ship Recycling Conference - Tokyo 6

1.3.3. India

18th November 2013 GMS Ship Recycling Conference - Tokyo 7

1.3.4. China

18th November 2013 GMS Ship Recycling Conference - Tokyo 8

1.3.5. China

18th November 2013 GMS Ship Recycling Conference - Tokyo 9

2.1. Historical Highs – Ship Recycling BOOM…and

2013!

•1985

42.6 Million Dwt

9 Million LDT

•2012

56.5 Million Dwt

11.7 Million LDT

•September 2013

37.56 Million Dwt

7.9 Million LDT

Note: All figures are approximate

18th November 2013 GMS Ship Recycling Conference - Tokyo 10

2.2. Bulk Carriers

Sold for Recycling 2011

(No./DWT)

2012

(No./DWT)

2013 YTD

(No./DWT)

Capesize 74 11,533,655 87 13,885,067 40 6,734,449

Panamax 66 4,481,196 118 7,945,415 51 3,438,242

Handymax 48 2,239,479 102 4,630,781 61 2,715,547

Handysize 291 6,536,167 322 8,459,421 248 6,663,369

Minibulk 86 511,316 69 456,105 70 434,065

Total 565 25,301,813 698 35,376,789 470 19,985,722

Source: Allied

Shipbroking Inc.

November 2013

18th November 2013 GMS Ship Recycling Conference - Tokyo 11

Sold For Recycling 2011

(No./DWT)

2012

(No./ DWT)

2013 YTD

(No./ DWT)

ULCC 2 618,576 3 918,638 5 1,564,191

VLCC 12 3,239,246 12 3,209,269 17 4,727,514

Suezmax 7 1,002,063 22 3,239,167 9 1,347,458

Aframax 28 2,656,659 39 3,714,797 22 2,168,617

Panamax 6 411,956 7 473,380 8 565,937

Product 68 2,207,837 62 2,033,749 43 1,394,146

Minitank 44 225,574 26 152,370 21 95,707

Total 167 10,361,911 171 13,741,370 125 11,863,570

2.3 Tankers

18th November 2013 GMS Ship Recycling Conference - Tokyo 12

Source: Allied

Shipbroking Inc.

November 2013

2.4. Baltic Demolition Assessment 2013

18th November 2013 GMS Ship Recycling Conference - Tokyo 13

290

310

330

350

370

390

410

430

450

470

2013/1/7 2013/2/7 2013/3/7 2013/4/7 2013/5/7 2013/6/7 2013/7/7 2013/8/7 2013/9/7 2013/10/7

D/TKR CHINA

D/TKR SUBCON

C/TKR CHINA

C/TKR SUBCON

B/C CHINA

B/C SUBCON

2.5. Factors that Affect Pricing 1. Supply

2. Demand

3. Steel Prices

4. Currency exchange rates

5. Government Regulations

18th November 2013 GMS Ship Recycling Conference - Tokyo 14

2.6. Steel Prices – Currency 2013: India

• IR on 1st January : 54.80 per USD / Steel prices: IR 26,000 per 12 mm

scrap metal

• IR on 28th August: 68.34!!! / Steel prices: IR 25,900

• IR on 1st September: 65.70 / Steel prices: IR 26,600

• IR on 1st October: 62.52 / Steel prices: IR 26,800

• IR on 1st November: 62.33 / Steel prices: IR 26,000

18th November 2013 GMS Ship Recycling Conference - Tokyo 15

22,500.00

23,000.00

23,500.00

24,000.00

24,500.00

25,000.00

25,500.00

26,000.00

26,500.00

27,000.00

27,500.00

28,000.00

STEEL INDIA (RS)

STEEL INDIA(RS)

370

390

410

430

450

470

490

STEEL INDIA (USD)

INDIA (USD)

2.7. Steel Prices – Currency 2013: Pakistan

• PKR on 1st January : 97.27 per USD / Steel prices: PKR 52,000 per 12

mm scrap metal

• PKR on 1st August: 101.76 / Steel prices: PKR 54,500

• PKR on 1st September: 104.55 / Steel prices: PKR 54,500

• PKR on 1st October: 105.90 / Steel Prices: PKR 55,000

• PKR on 1st November: 106.89!!! / Steel Prices: PKR 55,500

18th November 2013 GMS Ship Recycling Conference - Tokyo 16

50,000.00

51,000.00

52,000.00

53,000.00

54,000.00

55,000.00

56,000.00

57,000.00

STEEL PAKISTAN (PKR)

STEELPAKISTAN(PKR)

510

520

530

540

550

560

570

STEEL PAKISTAN (USD)

PAKISTANUSD

2.8. Steel Prices – Currency 2013: Bangladesh

• BDT on 1st January : 79.67 per USD / Steel prices: BDT 42,500 per 12

mm scrap metal

• BDT on 1st August: 77.78 / Steel prices: BDT 35,100

• BDT on 1st September: 77.78 / Steel prices: BDT 32,000!!!

• BDT on 1st October : 77.95 /Steel prices: BDT 34,200

• BDT on 1st November: 77.74 / Steel prices: BDT 35,100

18th November 2013 GMS Ship Recycling Conference - Tokyo 17

29,000.00

31,000.00

33,000.00

35,000.00

37,000.00

39,000.00

41,000.00

43,000.00

45,000.00

STEEL BANGLADESH (BDT)

STEELBANGLADESH(BDT)

400

420

440

460

480

500

520

540

560

STEEL BANGLADESH (USD)

BANGLADESH USD

Chartering earnings: from region USD 4.9k/day during beginning of January

2013 to region USD 40k /day during end of September. Improvement of more

than 700%!!!

On 4th November abt USD 19k /day

3.1 Recovery(?): Capesize

1000

1500

2000

2500

3000

3500

4000

4500

1/2/13 2/2/13 3/2/13 4/2/13 5/2/13 6/2/13 7/2/13 8/2/13 9/2/13

BCI – 2013 / September 2013

BCI -2013

18th November 2013 GMS Ship Recycling Conference - Tokyo 18

2000

2500

3000

3500

4000

4500

BCI – October 2013

BCI

Chartering earnings: from region USD 5.3k/day during beginning of January

2013 to region USD 14.3k /day during end of September. Improvement of about

169.8%!!!

3.2. Recovery(?): Panamax

600

800

1000

1200

1400

1600

1800

1/2/13 2/2/13 3/2/13 4/2/13 5/2/13 6/2/13 7/2/13 8/2/13 9/2/13

BPI – 2013 / September

BPI -2013

18th November 2013 GMS Ship Recycling Conference - Tokyo 19

1500

1600

1700

1800

1900

2000

2100

BPI October 2013

BPI

On 4th November abt USD 13k /day

As of September 2013

drop of about:

40% comparing

to the total fleet

recycled in 2012

Or

48% comparing to

the total DWT

supplied in 2012

500

1000

1500

2000

2500

BDI 2013 BDI 2013

3.3. Bulk Carriers: The effect of chartering

improvement

0

500

1000

1500

2000

1/3/

12

2/3/

12

3/3/

12

4/3/

12

5/3/

12

6/3/

12

7/3/

12

8/3/

12

9/3/

12

10/3

/12

11/3

/12

12/3

/12

BDI 2012 BDI 2012

18th November 2013 GMS Ship Recycling Conference - Tokyo 20

1400

1600

1800

2000

2200

BDI October 2013

BDI

TANKERS

SCRAPPED 2011 NEWBUILDING

ORDERBOOK JAN 2012 %

SCRAPPED 2012 NEWBUILDING

ORDERBOOK JAN 2013 %

ULCC/VLCC 14 67 20.9 15 57 26.3

SUEZMAX 7 67 10.4 22 64 34.4

AFRAMAX 28 60 46.7 39 30 130

PANAMAX 6 22 27.3 7 23 30.4

MR TANKER 68 94 72.3 62 116 53.4

MINI TANK 44 95 46.3 26 61 42.6

BULKERS

SCRAPPED 2011 NEWBUILDING

ORDERBOOK JAN 2012 %

SCRAPPED 2012 NEWBUILDING

ORDERBOOK JAN 2013 %

CAPESIZE 74 291 25.4 89 179 49.7

PANAMAX 66 165 40 117 223 52.5

SUPRAMAX 48 389 12.3 102 324 31.5

HANDYSIZE 291 337 86.4 324 275 118

MINI BULK 86 330 26.1 69 267 25.8

3.4 Beaching vs. Newbuilding

18th November 2013 GMS Ship Recycling Conference - Tokyo 21

Important Pillar of Shipping (facilitates market balance)

• Newbuilding – record years (pre-2008)

• Recycling – record years (2012-?)

Impact of Ship Recycling on:

• New Building Orders

• Charter rates (new/old ships, availability, etc.)

• Sale and Purchase (2nd values at par with scrap values)

• Ship Finance (residual values and future acquisitions)

• Developments in Ship Design and Fuel Efficiency

Cash Buyers as a source of vessel financing

• High Deposits and Loans

• Asset acquisitions (Companies, Vessels)

• Sale/Leaseback (BBC)

• Private Equity

4.1 Ship Recycling & Changing role of Cash Buyers

18th November 2013 GMS Ship Recycling Conference - Tokyo 22

4.1 Ship Finance Facts and Trends

Top 40 Shipping Banks = $408 BILLION worth of exposure to the sector

Accounts for about 78% of global ship finance

Roughly 75% of this exposure comes from European banks

As of June, 42% of these institutions claimed to be prepared to lend while it

was only 22% one year earlier (but these banks are focusing on

conservative deals with Top Tier, existing owners/clients

Many banks with a “legacy book” are more reluctant to lend as they are

overexposed to previous “bad deals”

Increased pressure on European banks is making portfolio sales more likely

– perhaps creating a more liquid market

~Source: NORD LB

18th November 2013 GMS Ship Recycling Conference - Tokyo 23

4.2 Ship Finance Facts and Trends

18th November 2013 GMS Ship Recycling Conference - Tokyo 24

4.3 (cont.) Ship Finance Facts and Trends

With traditional banks more reluctant to lend, we now witness a more eclectic

financing mix (blurred lines in terms of PE)

Capital Markets (ie Scorpio w/ $230+ mill.)

Private Equity (Wilbur Ross – Navigator Gas Transport)

Aircraft style leasing and/or sale leaseback transactions

The USA based capital markets have gone through a Renaissance of sorts as

it applies to ship finance

Slowly but surely, European banks will become more aggressive – For the

moment, however, PE seems to be taking the stage although most of the

deals are accompanied by some sort of bank financing as well

18th November 2013 GMS Ship Recycling Conference - Tokyo 25

4.4 GMS in PE Markets

GMS Examples of Private Equity Transactions :

Example 1 – Acquisition of Existing Company (i.e. Konig & Cie)

Example 2 – Struggling Owner Needs Cash – GMS Buys 50% of vessel acts as JV

partner

Example 3 – Owner Needs to Sell Vessel but Wants to Continue Operations – GMS

buys 100% of the vessel and structures a sale leaseback / BB back

Example 4 - Cash strapped owner wants to buy a new vessel but has no funds on hand

– GMS buys the “new” asset and takes in one of the owner’s “older” assets as a down

payment and holds a note for the balance

Example 4 – Owner does not want to handle recycling of the vessel – GMS buys vessel

clean or with cash flows attached and maintains ownership for set period of time until

current employment obligations expire and vessel is recycled

18th November 2013 GMS Ship Recycling Conference - Tokyo 26

5. Closing Thoughts

1) Ship recycling is a critical aspect of greater maritime industry

2) With return of newbuildings, weak freight markets and large

inventory of vessels, life cycle of ships continue to get shorter

3) Cash Buyers play a major role in the ship recycling process

4) Environmentally safe and responsible ship recycling programs

exist in several countries, including India. However, “headline

risk” often has a greater impact on the decision making

process than facts

5) Japanese ship owners have an exceptional opportunity to

occupy a leadership position in the “green” ship recycling

industry.

6) Time to act is now!

18th November 2013 GMS Ship Recycling Conference - Tokyo 27

Established in USA in 1992….LARGEST CASH BUYER IN THE WORLD!

In last two years, principals of GMS have delivered more than a quarter of the world’s fleet sold for

recycling.

World's FIRST ISO 9001:2000 certified Cash Buyer.

EXCLUSIVE sales offices in all FIVE of the major ship recycling markets in the world (Bangladesh,

China, India, Pakistan and Turkey).

Offices in USA, UAE, SINGAPORE and CHINA to provide 24/7 service to clients worldwide.

Financial and Management capability to:

Buy fleets on simple CASH "as is where is“ terms.

Take forward positions

Structure deals

Leader in Green Recycling:

IMO’s Hong Kong Convention

Safe and Responsible Ship Recycling Programs

Development of Green Yards

18th November 2013 GMS Ship Recycling Conference - Tokyo 28