USING A CHAR ACTERISTICS AND NEW COMMODITIES APPROACH TO EXPLAIN IRA SELECTION Alice E. Simon, Ohio Wesleyan University--De l aware, Ohio 1 Whether consumers made efficient IRA pur chase de- cisions was analyzed using a framework adapted from Lancaster 's characteristic and Ironmonger' s new commodities approaches to explain consumer behavior. The extent to which financial charac- teristics existed within three types of IRAs was compared to the importance of these characteris- tics for consumers to determine an ideal IRA. Efficiency was defined as the difference between ideal and actual IRA purchase behavior. THEORETICAL FRAMEWORK The traditional microeconomic approach to the study of consumer behavior is based upon the principles of utility maximization: satisfy ing unlimited wants through the purchase of goods and servic es in the most efficient way possible, g iven limited r esources . Utility is viewed as being a function of a goods and Al terna ti ve microe conomi c app roach es to the study of consumer behavior based on the tradi- tional approach have been proposed. Two in par- ticular view utility as s ome function of the characteristics of goods and se rvi ces. One is offered by K elvin Lancaster and will be referred to as the characteristics approach [ 4 ] . The key difference between the characteristics approac h and the tradit ional approach lies in the assump - tions regarding the utility funct ion. L anc aster assumes that utility is a function of th e charac- teristics of goods and services rather than of the goods and services themse lve s. H is approach, which accounts for both changes in a product's characteristics and changes in individual tastes a nd prefere nces for those characteristics may be a better tool for some consumer behavior problems than is the traditional a pproach which ignore s information about product characteristics . The second approach is offered by D.S . Iron- monger and will be referred to as the new commod- ities approach (2 ]. The major difference between the traditional approach and the new commodities approach is that the former assumes a fixed number of commodities and fixed t as tes and preferences on the part of consumer s, whereas the l atte r allows these components of utility maximi- zation to vary ( 2]. The traditional approach is unable to handle variations of this type, and as 1 Assistant Professor of Econom ics 72 a result ignores the existence of such variations or is forced to dea l with them in a type of re - sidual-trend analysis, whereby such changes are treated as the " everything else held constant" under ceteris conditions. Ironmonger, on the other hand, recognizes the need to account for the existence of new commodities (defined as either a new good or as a good whose characteris- tics have changed) and to account for t he effect that such commodities have on the consumer's existi ng utility function. Such a theo r etical framework is similar to Lancaster's approach in the sense that goods or commodities ar e defined in terms of their characteristics . Like Lancaster, new goods can be defined as exhibiting different characteristics or different proportions of like characteristics. However, unlike Lancaster, utility i s viewed as a function of sa ti sfyi ng wants, not of characteristics. Satisfying wants is viewed as a fun ction of com- modity characteristics and utility is obtained only when wan ts are satisfied . Iron monger argues that even though one consumes commodities to r ?.- cei ve characteristics, some characteristics are consu med in the process for which the consumer never expressed a de sire . No utility is received by consuming characte ri stics for which there was no expressed want . Hence, utility is only achieved by consuming characteristics for wh ich there was an expressed want. In s um , traditional neocl assical utility theory views utility as a function of goods and services. Lanca ste r' s characteristic views utility as a fu nct ion of the charac t eris- tics of goods and services. Ironmonger's new commodities approach views utility as a function of sa ti sfied wants and satisfied wants as a func- tion of the characteristics of goods a nd services . Hence, characteristic s are used to satisfy wants from whch utility is received; utility is not received from characteristics un- l ess the characteristics are wanted. Equations ( 1), ( 2), and (3) present the utility functions of the traditional, characteristic , and new com- modities approaches, respectively. U = f(X,Y) where X and Y are goods U = U(Z) wit h Z = BX ( 1) (2 ) where Z = vecto r of characteri st ics X = vector of goods B = tr ansformer of goods into characteristics.

Transcript

USING A CHARACTERISTICS AND NEW COMMODITIES APPROACH TO EXPLAIN IRA SELECTION

Alice E. Simon , Ohio Wesleyan University--Del aware, Ohio1

~~~~~~ ~~~-ABSTRACT~~~~~~~~ Whether consumers made efficient IRA pur chase decisions was analyzed using a framework adapted from Lancaster ' s characteristic and Ironmonger' s new commodities approaches to explain consumer behavior. The extent to which financial characteristics existed within three types of IRAs was compared to the importance of these characteristics for consumers to determine an ideal IRA. Efficiency was defined as the difference between ideal and actual I RA purchase behavior.

THEORETICAL FRAMEWORK

The traditional microeconomic approach to the study of consumer behavior is based upon the principles of utility maximization: satisfying unlimited wants through the purchase of goods and services in the most efficient way possible, given limited resources . Utility is viewed as being a function of a goods and services~~·

Al terna ti ve microeconomi c approaches to the study of consumer behavior based on the traditional approach have been proposed. Two in particular view utility as s ome function of the characteristics of goods and services. One is offered by Kelvin Lancaster and will be referred to as the characteristics approach [ 4 ] . The key difference between the characteristics approach and the traditional approach lies in the assumptions regarding the utility f unc t ion. Lancaster assumes that utility is a function of the characteristics of goods and services rather than of the goods and services themselves. His approach, which accounts for both changes in a product's characteristics and changes in individual tastes and preferences for those characteristics may be a better tool for some consumer behavior problems than is the traditional approach which ignores information about product characteristics .

The second approach is offered by D.S . Ironmonger and will be referred to as the new commodities approach (2 ] . The major difference between the traditional approach and the new commodities approach is that the former assumes a fixed number of commodities and fixed t astes and preferences on the part of consumer s, whereas the l atter allows these components of utility maximization to vary ( 2]. The traditional approach is unable to handle variations of this type, and as

1Assistant Professor of Economics

72

a result ignores the existence of such variations or is forced to deal with them in a type of residual-trend analysis, whereby such changes are treated as the "everything else held constant" under ceteris ~ribus conditions. Ironmonger, on the other hand, recognizes the need to account for the existence of new commodities (defined as either a new good or as a good whose characteristics have changed) and to account for t he effect that such commodities have on the consumer's existing utility function. Such a theor etical framework is similar to Lancaster's approach in the sense that goods or commodities a r e defined in terms of their characteristics . Like Lancaster, new goods can be defined as exhibiting different characteristics or different proportions of like characteristics. However, unlike Lancaster, utility i s viewed as a function of satisfying wants, not of characteristics. Satisfying wants is viewed as a function of commodity characteristics and utility i s obtained only when wants are satisfied . Ironmonger argues that even though one consumes commodities to r ?.cei ve characteristics, some characteristics are consumed in the process for which the consumer never expressed a desire . No utility is received by consuming characteristics for which there was no expressed want . Hence, utility is only achieved by consuming characteristics for which there was an expressed want.

In s um , traditional neoclassical utility theory views utility as a function of goods and services. Lancaster' s characteristic ~pproach

views utility as a function of the charac t eristics of goods and services. Ironmonger's new commodities approach views utility as a function of satisfied wants and satisfied wants as a function of the characteristics of goods and services . Hence, characteristics are used to satisfy wants from whch utility is received; utility i s not received from characteristics unl ess the characteristics are wanted. Equations ( 1), ( 2), and (3) present the utility functions of the traditional, characteristic , and new commodities approaches, respectively.

U = f(X,Y) where X and Y are goods

U = U(Z) with Z = BX

( 1)

(2 )

where Z = vector of characteristics X = vector of goods B = t r ansformer of goods

into characteristics.

= units of satisfaction of want i

(3)

= units of satisfaction of want i obtained from one unit of commodity j.

To operationalize the characteristic approach, the extent to which characteristics exist within any good or service must be known. To operationalize the new commodities approach, the extent to which characteristics exist within a good or service mus t also be known , but in addition, the importance or desireability of product characteristics to a consumer is also necessary. To identify both components of t he new commodities approach , two ratings were constructed: an Existence Rating (ER) which measured the extent to which characteristics existed within a given product; and an Importance Rating (IR) which measured the extent to which characteristics were desired or considered important by consumers.

According to the traditional approach, if a good or service exists it has the potential to provide utility. No accounting of i;he IRs and ERs of characteristics is necessary. According to the characteristics approach, if a characteristic exists it has the potential to provide utility. Therefore, products with the highest ERs for all characteristics would be potential candidates for maximizing a consumer ' s utility. However, according to the new commodities approach, three different situations are possibl e:

IR = ER (4)

The extent to which characteristics are wanted could be equal to the extent to which characteristics exist. This is a potential utility producing situation.

IR >,ER (5)

The extent to which characteristics are wanted could be greater than the extent to which characteristics exist. Utility is rP.ceived up to where IR = ER. The excess of the IR over the ER creates a potential disutility situation.

ER > IR (6)

The extent to which characteristics are wanted could be less than the extent to which characteristics exist. Utility is received up to where ER = IR . The excess of the ER over the IR is a neutr<!J situation.

However , it is more likely the case that Equation ( 6) does not represent a neutral situation. Rather, the excess of the ER over the IR may create a potential disutility situation. This disutility may be a function of non-optimal resource allocation. When paying for a characteristic which is not desired or for amounts of a

73

characteristi c above a desired level , consumers may be usi ng financial r esources in excess of an optimal level. In addition , consumers may have to incur costs of substitution by giving up some characteristics in exchange for others when faced with real world products containing fixed combinations of characteristics. For example, a consumer may wish to purchase a microwave oven which defrosts and has a temperature probe. However , the only models which contain these two features also has a memory . The consumer must pay for the existence of the memory, implicit in the price of the oven, in order to consume the other two desired characteristics . Therefore, i t may be more appropriate to assume that only two, not three , possible situations may arise :

IR = ER (7)

A utility producing situat ion analogous to Ironmonger as illustrated in Equation (4).

IR I ER (8)

A ~isutility producing situation caused by a less than optimal resource allocation. This situation can arise from either the IR exceeding the ER (analogous to Ironmonger as illustrated in Equation (5)) or by the ER exceeding the IR.

OPERATIONALIZING THE FRAMEWORK

To illustrate the adaption of Ironmonger ' s approach , it was necessary to identify a new good or service which contained a variety of unique and overlapping characteristics. Individual Retirement Accounts (IRAs) were chosen for this purpose. IRAs met the new good or service requirement since for a large proportion of the American labor force such accounts first became available on January 1, 1982 with the passage of The Economic Recovery Act of 1981. Prior to that date IRAs were only availablP. to workers who were not covP.red by other retirement plans . Further, there are a wide variety of IRAs to choose from. Since numerous unique and overlapping characteristics could be identified across IRA types, this new commodity met the criteria for the selecting of a good or service to illustrate the framework .

The demand for IRAs is assumed to exist. The focus of this research, therefore, li.P.s i.n the selection process for a particular t ype of IRA. Specifically, efficient utility maximizing consumers are defined as those consumers who purchase that type of IRA which contains the most of characteristics they consider to be important.

Empiri.cal r esearch in the area of P.fflciency offers varied definitions and measures of the concept, one being the difference between ideal and actual behavior (9). Ideal consumer behavior leads to a utility max i mizing consumption choice, assuming ful l and perfect

information . Ac t ual consumer behavior reflects what consumers actually selP,Ct. If the ideal and actual consumption choice are not the same , it is assumed that an inefficient consumption decision results with the degree of inefficiency being the gap between the ideal and actual consumption choice.

Other research has defined efficlP,ncy as that behavior which yielded the "greatest utility from a consumption decision given fixed resources," and efficient consumers were those who could "successfully identify the relative abilities of a set of alternative choices to provide utility" [ 10 , p. 37]. This definition of an efficient consumer (not merely one who could match ideal and actual behavior but one who could determine the utility providing capabilities of various consumption decisions) resembles Ironmonger ' s approach whereby consumers are assumed to know which characteristics or choices will provide utility.

The concepts of ideal and actual behavior have also been used in studies of brand choice behavior with an ideal brand defined as tha~

brand which contained those dimensions deemed most important by consumers[~. Comparisons between their ideal and selected brand were made using an absolute difference weighting procedure.

I n this study, efficiency is also defined as the difference between ideal and actual behavior . Actual behavior is directly observable; which IRA did a consumer purchase. The approach used to define and measure ideal behavior is more complex. First , the characteristics of IRAs must be identified and defined. Second, the extent to which each characteristic is desired or wanted by consumers must be determined (IR) followed by determining the extent to which each characteristic exists within IRA types in the real world (ER). Third, the IRs and ERs across all characteristics and across all IRA types must be compared to determine one ideal IRA. Consumers ' ideal IRAs are hence defined as those IRAs which contain characteristics that consumers want in the amounts that they want them. Effie lent consumers are defined as those consumers whose ideal IRA and actual IRA purchase are the same.

Defining Characteristics

In the late 1970s the issue of defining characteristics was recognized in the consumer economics literature as having an important impact on the operationalization of consumer behavior models. Hence, a variety of alternative approaches to defining characteristics were offered. One defines a product service characteristic as a "basic feature which gives rise to utility" [ 5, p. 52-53 ). Hence, "manageability" would be considered as a product characteristic of an IRA. Such factors as number of alternative investments in a portfolio , frequency of brokers '

74

phone calls , and availability of newsletters or other pertinent information on a regular basis , all of which contribute to the "manageability" of an IRA , would not be.

A second approach suggests that a hierarchy of product characteristics can be developed [1]. Thi s hierarchy should include all types of product definitions with each type representing a different level of abstraction from the original product . For example, using a three level system, the first level could contain specific , objective , uni- dimentional, measureable product characteristics . Level two could consist of multi- dimentional and measureable characteristics which are functional l y related to level one character istics and which affect the overall desireabili ty of a product. Level three refers to the overall product character, characterized by levels one and two .

In this study , seven IRA characteristics were defined . The specific attributes of IRAs which were included in these definitions were based upon research and promotional literature prepared by financial analysts and investment experts. Specifically, these materials included investment portfolios, prospecti, and brochures prepared by a wide variety of IRA providers . Survey articles published in financial magazines which described IRA investment alternatives and/or' traced the performance of various I RA investments were also used. Attributes of IRAs which providers mentioned mos t often in their advertisements , attributes which analysts emphasized in their assessments of IRA performance , and attributes listed as being either advantages or disadvantages of any given IRA type by users and providers alike were used. These definitions also reflect the IRA attributes which consumers might use to distinguish among IRA types . These seven characteristic defintions are: convenience-the accessibility of an IRA provider to the consumer; ~-~~liarity--previous knowledge on the part of the consumer about a financial institution and its investments; extra costs- -the extent to which the purchase of a particular type of IRA incurred extra costs such as fees, commissions, and/or penalties; interest ra tes--whether the IRA' s interest rates were fixed, variable, stable, or volatile; flexi~t3=.~~Y.,--the ease with which IRAs could be transferred or rolled over and whether the IRA included a diversified portfolio of investments; risk--the expected outcome from an IRA investment based on previous performance and consumer expectations; and management-the degree to which an IRA was self-directed or managed by a representative of an IRA provider.

In general, these definitions are consistent with the elements of product characteristic and level two characteristic definitions cited above. They consist of many related IRA attributes which combine to produce a product service. For example , the product service "convenience" represents the ability of an investor to gain access to IRAs through their employer, local bank locations, and direct deposit facil-

ities, as well as the degree to which phone call and mail contact is made with agents. Similarly, "flexibility" is an example of a product service which represents the ease with which funds can be rolled over or liquidated, the degree of diversification in investments , as well as the extent to which returns will reflect market conditions.

Existence Ratings

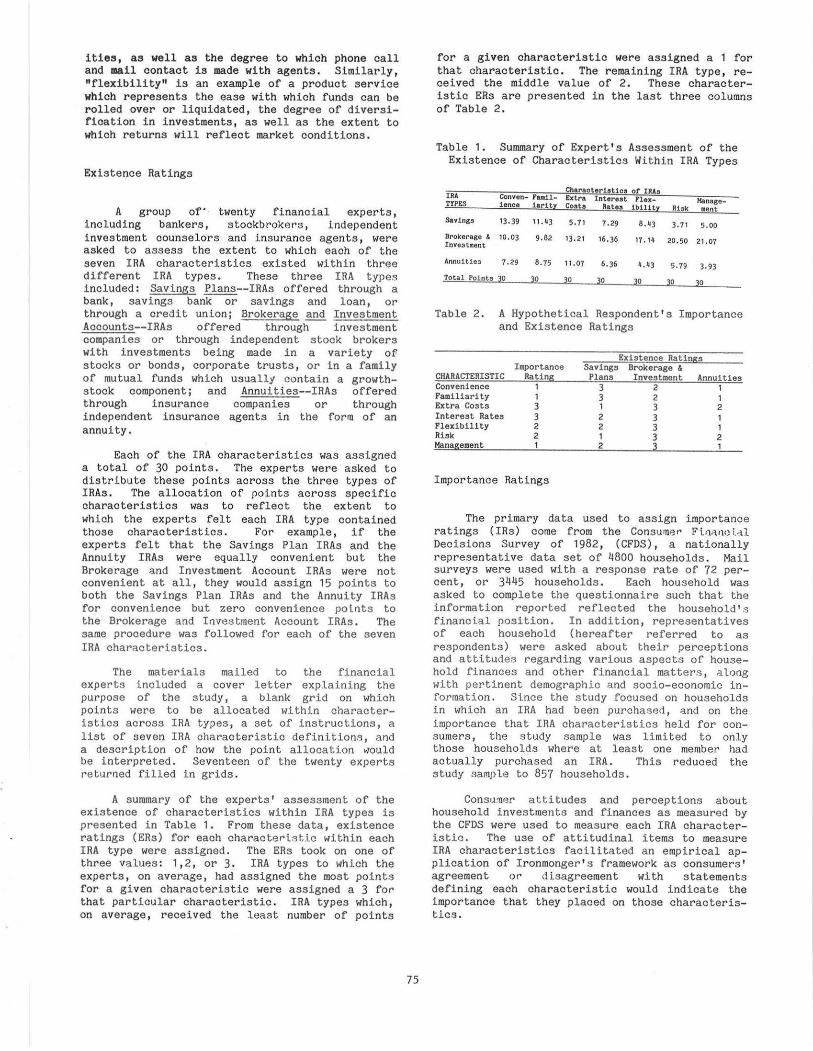

A group of• twenty financial experts, including bankers, stockbrokers , independent investment counselors and insurance agents, were asked to assess the extent to which each of the seven IRA characteristics existed within three different IRA types. These three IRA types i ncluded : Savings Plans--IRAs offered through a bank, savings bank or savings and loan, or through a credit union; Brokerage and Investment Accounts--IRAs offered through investment companies or through independent stock brokers with investments being made in a variety of stocks or bonds, corporate trusts, or in a family of mutual funds which usuallt contain a growthstock component; and Annuities--IRAs offered through insurance companies or through independent insurance agents in the form of an annuity .

Each of the IRA characteristics was assigned a total of 30 points. The experts were asked to distribute these points across the three types of IRAs. The allocation of points across specific characteristics was to reflect the extent to which the experts felt each IRA type contained those characteristics . For example, if the experts felt that the Savings Plan IRAs and the Annuity IRAs were equally convenient but the Brokerage and Investment Account IRAs were not convenient at all, they would assign 15 points to both the Savings Plan IRAs and the Annuity IRAs for convenience but zero convenience polnts to the Brokerage and Investment Account IRAs. The same procedure was followed for each of the seven IRA characteristics.

The materials mailed to the financial experts included a cover letter explaining the purpose of the study , a blank grid on which points were to be allocated within characteristics acr oss IRA types, a set of instructions, a list of seven IRA characteristic definitions, and a description of how the point allocation Vlould be interpreted. Seventeen of the twenty experts returned filled in grids.

A summary of the experts' assessment of the existence of characteristics within IRA types is presented in Table 1. From these data, existence ratings (ERs) for each characterlstlc within each IRA type were assigned . The ERs took on one of three values : 1, 2, or 3. IRA types to which the experts, on average, had assigned the most points for a given characteristic were assigned a 3 for that particular characteristic. IRA types which, on average , received the least number of points

75

for a given characteristic were assigned a 1 for that characteristic . The remaining IRA type, received the middle value of 2. These characteristic ERs are presented in the last three columns of Table 2.

Table 1. Summary of Expert ' s Assessment of the Existence of Characteristics Within IRA Types

IRA TYPES

Savings

Brokerage & Investment

Annuities

Conven- Fa.11-ienoe iaritr

13 , 39 11.43

10.03 9.82

7.29 8,75

Total Points 30 30

Charaoteristios ot IRA:t Extra Interest FlexCos ts Rates 1b111tr

5. 71 7 .29 8.43

13.21 16.36 17 .14

11.07 6.36 4 .43

30 30 30

Riok

3. 71

20 . 50

5, 79

30

Management

5.00

21.07

3,93

30

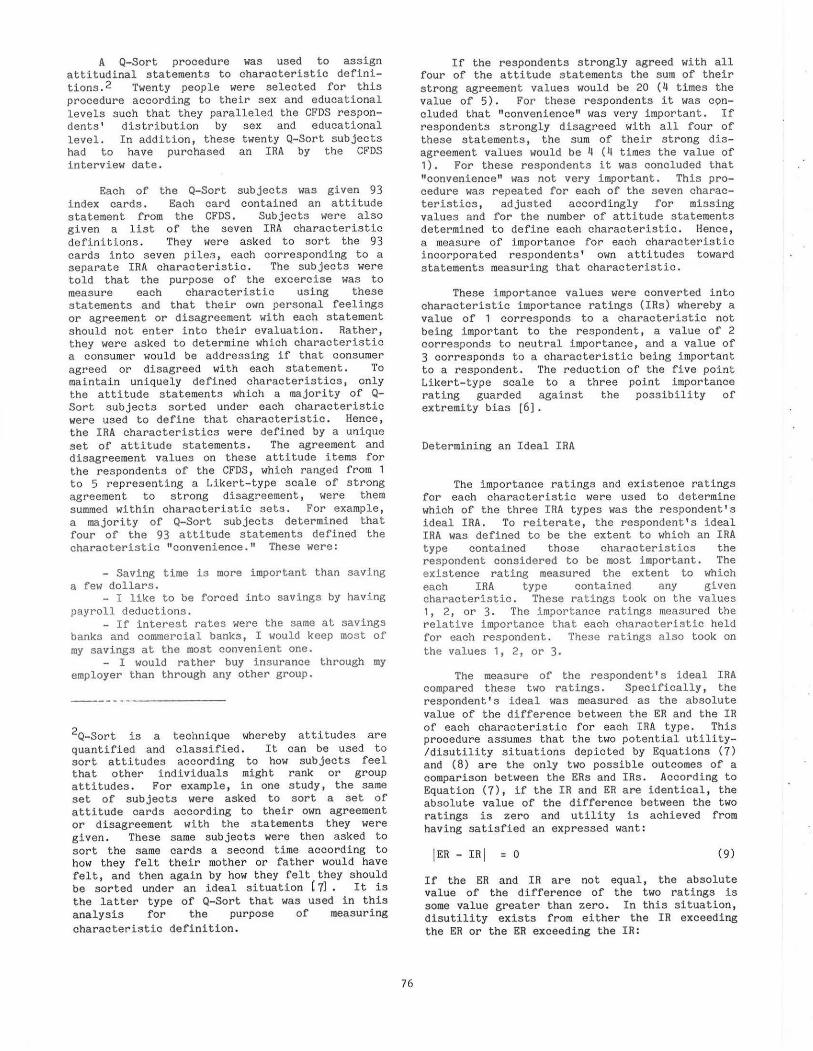

Table 2. A Hypothetical Respondent's Importance and Existence Ratings

The primary data used to assign importance ratings ( IRs) come from the Consumer Fi.11il•le i . ..i.l Decisions Survey of 1982, ( CFDS), a nationally representative data set of 4800 households . Mail surveys were used with a response rate of 72 percent, or 3445 households. Each household was asked to complete the questionnaire such that the information reported reflected the household' s financi.al position. In addition, representatives of each household (hereafter referred to as respondents) were asked about their perceptions and attitudes regarding various aspects of household finances and other financial matters , along with pertinent demographic and socio-economic information. Si.nee the study focused on households in which an IRA had been purchasF?<i, and on the importance that I RA characteristics held for consumers, the study sample was limited to only those households where at least one member had actually purchased an IRA. This reduced the study sample to 857 households.

Consu~F?r attitudes and perceptions about household investments and finances as measured by the CFDS were used to measure each IRA characteristic. The use of attitudinal items to measure IRA characteristic.s facilitated an empirical application of Ironmonger's framework as consumers' agreement or disagreement with statements defining each characteristic would indicate the importance that they placed on those characteristics .

A Q-Sort procedure was used to assign attitudinal statements to characteristic definitions. 2 Twenty people were selected for this procedure according to their sex and educational levels such that they paral leled t he CFDS respondents ' dis tribution by sex and educational level. In addition, these twenty Q-Sort sub j ects had to have purchased an IRA by the CFDS interview date.

Each of the Q-Sort subjects was given 93 index cards. Each card contained an attitude statement from the CFDS. Subjects were also given a list of t he seven IRA char acteri stic definitions. They were asked to sor t t he 93 cards into seven piles , each corresponding to a separate IRA characteristic. The subjects were told that the purpose of the excercise was to measure each characteristic using these statements and that their own personal feelings or agreement or disagreement with each statement should not enter into their evaluation. Rather , they were asked to determine which characteristic a consumer would be addressing i f t hat consumer agreed or disagreed with each s t atement . To maintain uniquely defined characteristics, only the attitude statements which a majority of QSort sub jects sorted under each characteristic were used to define that characteristic. Hence , the IRA characteristics were defined by a unique set of attitude statements. The agreement and disagreement values on these attitude items for the respondents of the CFDS, which ranged from 1 to 5 representing a Likert-type scal e of s trong agreement to strong disagreement, were t hem summed wi thin characteristic sets. For example, a majority of Q-Sort sub jects determined that four of the 93 attitude statements defined the characteristic "convenience. " These were:

- Saving time is more important than saving a few dollars.

- I like to be forced into savings by havi ng payroll deductions.

- If interest rates were the same at savings banks and commercial banks, I would keep most of my savings at the most convenient one.

- I would rather buy insurance through my employer than through any other group.

--------------

2Q-Sort is a technique whereby attitudes are quantified and classifi ed . It can be used to sort attitudes according to how sub jects feel t hat other i ndividuals might rank or group attitudes. For example , in one study , the same set of subjects were asked to sort a set of attitude cards accord ing to their own agreement or disagreement with the statements they were given. These same subjects were then asked to sort the same cards a second time according to how they felt their mother or fa ther would have felt, and then again by how they felt they should be sorted under an ideal situation ( 71 • It is the latter t ype of Q-Sort that was used in this analysis for the purpose of measuring characteristic definition.

76

If the respondents s trongly agreed with all four of the attitude statements the sum of their strong agreement values would be 20 (4 times the value of 5). For these respondents it was concluded t hat "convenience" was very i mportant . If respondents strongly disagreed with all four of these statements, the sum of their strong disagreement values would be 4 (4 times the value of 1). For these respondents it was concluded that "convenience" was not very important . This procedure was repeated for each of the seven characteristics, adjusted accordingly for missing values and for the number of attitude statements determined to define each characteristic. Hence, a measure of i mportance for each characteristic incorporated respondents' own attitudes toward statements measuring that characteristic.

These importance values were converted i nto characteristic importance ratings (!Rs) whereby a value of 1 corresponds to a characteristic not being important to the respondent, a value of 2 corresponds to neutral importance , and a value of 3 corresponds to a characteristic being important to a respondent . The reduction of the five point Likert-type scale to a three point i mportance rating guarded against the possibility of extremity bias (6).

Determining an Ideal I RA

The i mportance ratings and exi stence ratings for each characteristic were used to determine which of the three IRA types was t he respondent ' s ideal I RA. To reiterate , the respondent's ideal IRA was defined to be the extent to which an IRA type contained those characteristics the respondent considered to be most important. The existence rating measured the extent to which each I RA type contained any given characteristic. These ratings took on the values 1, 2, or 3. The importance ratings measured the relative importance that each characteristic held for each respondent . These ratings a lso took on the values 1, 2, or 3.

The measure of the respondent's ideal IRA compared these two ratings. Specifically, the respondent ' s ideal was measured as the absolute value of the difference between the ER and the IR of each characteri s t ic for each IRA type. This procedure assumes that the two potential utili ty/ disutility situations depicted by Equations (7) and (8 ) are t he only two possible outcomes of a comparison between the ERs and !Rs. According to Equation (7) , if t he IR and ER a re identical , the absolute value of the difference between the t wo ratings is zero and utility is achieved from having satis f ied an expressed want :

IER - IR I = 0 (9)

If the ER and IR are not equal, the absolute value of the difference of the t wo ratings is some value greater than zero . In this situation, disutility exists from either the IR exceeding the ER or the ER exceeding the IR:

I ER - IRI > 0 ( 10)

Since the respondent's ideal IRA is defined as that IRA which maximizes utility and mi nimizes disutilty, the IRA with the lowest absolute value of the difference between the ER and IR across all characteristics and all IRAs would be that respondent' s ideal.

A numerical example is presented in Table 2 above . The las t three columns are t he existence ratings for each charac t eristic by IRA t ype as assigned by the financial experts. The first column lists characteristic importance ratings for a hypothetical respondent . For t his respondent, the characteristcs extra cos t s and inter est rates were most important; wher eas the characteristics convenience, familiarity, and management were l east important . Flexibili ty and risk were between the extremes . This respondent ' s IR for convenience was 1. The existence ratings for Savings Plan IRAs , Brokerage and Investment Account IRAs , and Annuity IRAs for convenience are 3, 2, and 1, respectively. Hence, the absolute value of the difference for convenience is I 3-1 I =2 for Savings Plan IRAs , 12-1 1 =1 for Brokerage and Investment Account IRAs , and I 1-1 I =0 for Annuity IRAs. Since the Annuity IRA produced the lowes t absolute value of the difference between t he IR and ER, it yielded the highest level of convenience utility for this respondent; therefore the Annuity IRA was assigned one point representing i ts potential t o become the r espondent' s ideal IRA. If two IRA types tied for the lowest absol ute val ue of the differ ence between the IR and ER for a given characteristic, they both were identified as yielding the highest level of utility for that characteristic and both were assigned a point.

This procedure was repeated for each of the seven characteris tics . After each set of compari sons , one or more IRA types were identified as yie ldi ng the highest level of utility for that characteristic and was assigned one point . For each respondent, the IRA type or combination of types which received the most points was defined as the respondent ' s ideal IRA. The assigning of points to characteristics which yielded the highest l evels of utility by IRA type for the hypothetical respondent is presented in Table 3. This respondent' s ideal IRA is an Annuity IRA which r eceived four of the seven possible characteristic points .

The ideal IRA or ideal combination of IRAs was then compared to the actual IRA or combination of IRAs tha t the respondents had purchased . If the ideal and actual IRA measures were the same, the respondent was classified as an efficient IRA purchaser. If the ideal and actual measures were not equal, t he respondent was classified as an i nefficient IRA purchaser , one who did not purchase that IRA which contained those charaqteristics which were important to them.

Approximately forty percent of the respondents' households were classified as efficient. Why certain households were efficient IRA purchasers and others not is an interesting empirical question. Factors thought to impact on the probability of a household being efficient or not could be analyzed using probit analysis. Such an analysis has been completed by Simon ( 8]. Findings indicate that households who are more likely to purchase their ideal IRA had been exposed to the financial institution which provided their ideal IRA through the purchase of other financ ial services, had relatively fewer years of education, were located i n central , midwestern areas of the country, were not familiar with tax sheltered investments in general, had lower incomes, wer e newly eligible to purchase IRAs, were not self-employed but members were working as wage and salary workers, and found the IRA selecti on process to be fai r ly s imple .

In addition to the probit analysis of efficient versus inefficient respondents, an alternative theoretical application of this f r amework may be of interest . There is reason to believe that the amount by which utility is reduced when the IR is greater than the ER is not equivalent to the amount of utility reduced when the ER is greater than the IR. Therefore, whether t he difference between the ER and IR is positive or negative, if incorporated into an ideal IRA measure, may yield different results.

SUMMARY AND IMPLICATIONS

Alternative microeconomi c approaches to explain consumer behavior were explored and compar ed . It was concluded t hat for certain types of goods and services, an approach whi ch accounted for product charac t eristics as well as t he i mportance that consumers placed on those characteristics, might be preferred . The selection of a specific type of IRA was selected to illustrate such an approach . IRA character istics were defined based upon research and promotional literature prepared by finacial analysts and investment experts using the guidelines of a characteristic definition hier archy. Q-Sort was used to verify and operationalize characteris tic definitions using

attitude items on household finances and investments. Levels of agreement and disagreement with the attitude items were converted into characteristic importance ratings which measured the importance that each IRA characteristic held for respondents. The extent to which a particular characteristic existed within an IRA type was measured by existence ratings to allow assessment of whether respondents purchased those types of IRAs which contained characteristics most important to them. A panel of financial experts determined the existence ratings for each characteristic for three types of IRAs currently on the market. A respondent's ideal IRA was defined to be the extent to which a specific IRA contained those characteristics the respondent considered to be most important . Ideal IRAs were compared to actual purchases to determine whether the respondent made an efficient IRA purchase decision.

The technique developed by this research for defining and operationalizing product characteristics can be used to help consumers make efficient purchase decisions . First, appropriate characteristics must be defined. For IRAs, composite characteristics which identified product services were used. By using materials prepared by manufacturers, consumer information services, retailers and other forms of advertising, consumers can identify characteristic s appropriate to a given product.

Second, the importance that each product characteristic holds for consumers could be identified. Consumers could list characteristics and rank them according to importance . To make the ranking process easier, manufacturers or consumer information services could prepare lists of product characteristics and suggest ways in which products coul d be prioritized to reflect the existence of characteristics . For example , Consumer Reports lis t s product characteristi cs and then i dentifies which products contain them. Manufacturers may want to follow suit.

Third, by i dentifying which characteristics are most important, even in the absence of a prepared chart i dentifying where product characteristics might be found, consumer s can limit their search act ivity. Information search could be focused more dir ectly on specific product characteristics, reducing both the time and money costs of search.

If the goal of consumer policy is to help consumers make efficient consumption decisions, the technique sugges ted here offers a way to achieve this goal. This technique can be used to reduce consumer dissatisfaction or frustration caused by purchasing products which do not meet their expectations. If desired characteristics are identified prior to purchase and products which contain those desired characteris tics are also identified prior to purchase, the probability of buying t he "wrong" product is reduced.

78

REFERENCES

1. Geistfeld, Loren V., Sproles, George B. and Badenhop, Suzanne B. "The Concepts and Measurment of a Hierarchy of Product Characteristics." Advances in Consumer Resear_9_h_, 4: 302-307. -- -------

2. Ironmonger , D.S. New Commodities and Consumer Behavior. Cambridge: University Press, 1972.

3. Jacoby, Jacob, Speller , E. and Kohn, Carol A. "Brand Choice Behavior as a Function of Information Load." Journa]. __ ~L Marketing, February, 1974. pp. 63-69 .

4. Lancaster, Kelvin. Consumer Demand. New York: Columbia University Press , 197f:-

5. Maynes, E. Scott . Decision Making for__ Consumers: An Introduction to Consumer Economics. New York: MacMillian Publishing Company, 1976 .

6. Nunnally, J im. Psychometric Theory. New York: McGraw Hill Book Company, 1967.

7. Sellitz, Claire, Jahodo, Marie, Deutsch, Morton and Cook , Stuart W. Research Methods in Social Relations . New York: Holt; Rinehart and Winston, 1959.

8 . Simon, Alice E. "Selecting an IRA: An Application of a Characteristics and New Commodities Approach to Explain Cons umer Behavior. " Unpublished disser tation, The Ohio Stat e University, 1984.

9. Sproles , George, Geistfeld , Loren V. and Badenhop , Suzanne B. "Informationa l Inputs as Influences on Efficient Consumer DecisionMaking ." Journal of Consumer Affairs, Summer, 1978 . pp. 88- 103.

10. Sproles, George, Geistfeld, Loren V. and Badenhop, Suzanne B .. "Types and Amounts of Information Used by Efficient Consumers." Journal of Consumer Affairs, Summer, 1980. pp. 37-48.