Understand the meaning and significance of Framework for the Preparation and

Presentation of Financial Statements.

♦

Learn objectives of Financial Statements.

♦

Understand qualitative characteristics of Financial Statements.

♦ Comprehend recognition and measurement of elements of Financial Statements.

♦

Know concepts of capital, capital maintenance and determination of profit.

1. Introduction

The development of accounting standards or any other accounting guidelines need a

foundation of underlying principles. The Accounting Standards Board (ASB) of the ICAIissued framework in July, 2000 which provides the fundamental basis for development of new

standards as also for review of existing standards. The principal areas covered by the

framework are as follows:

(a) Components of financial statements;

(b) Objectives of financial statements;

(c) Assumptions underlying financial statements;

(d) Qualitative characteristics of financial statements;

(e) Elements of financial statements;

(f) Criteria for recognition of elements in financial statements;

(g) Principles of measurement of financial elements;

The framework sets out the concepts underlying the preparation and presentation of general-purpose financial statements prepared by enterprises for external users. The main purpose of

the framework is to assist:

(a) Enterprises in preparation of their financial statements in compliance with the accounting

standards and in dealing with the topics not yet covered by any accounting standard.

(b) Accounting Standard Board (ASB) in its task of development and review of accounting

standards.

(c) ASB in promoting harmonisation of regulations, accounting standards and procedures

relating to the preparation and presentation of financial statements by providing a basisfor reducing the number of alternative accounting treatments permitted by accounting

standards.

(d) Auditors in forming an opinion as to whether financial statements conform to the

accounting standards.

(e) Users in interpretation of financial statements.

3. Status and Scope of the Framework

The framework applies to general-purpose financial statements (hereafter referred to as

‘financial statements’ usually prepared annually for external users, by all commercial,

industrial and business enterprises, whether in public or private sector. The special purposefinancial reports, for example prospectuses and computations prepared for tax purposes areoutside the scope of the framework. Nevertheless, the framework may be applied in

preparation of such reports, to the extent not inconsistent with their requirements.

Nothing in the framework overrides any specific Accounting Standard. In case of conflict

between an accounting standard and the framework, the requirements of the AccountingStandard will prevail over those of the framework.

4. Components of Financial Statements

A complete set of financial statements normally consists of a Balance Sheet, a Statement ofProfit and Loss and a Cash Flow Statement together with notes, statements and other

explanatory materials that form integral parts of the financial statements.

All parts of financial statements are interrelated because they reflect different aspects of same

transactions or other events. Although each statement provides information that is differentfrom each other, none in isolation is likely to serve any single purpose nor can any one

Framework for Preparation and Presentation of Financial Statements 1.5

Profit and Loss Account 25,000 Stock 30,00010% Loan 35,000 Trade receivables 20,000Trade payables 10,000 Deferred costs 10,000

Bank 5,0001,30,000 1,30,000

Addit ional information:

(a) The remaining life of fixed assets is 5 years. The pattern of use of the asset is even. Thenet realisable value of fixed assets on 31.03.13 was ` 60,000.

(b) The trader’s purchases and sales in 2012-13 amounted to ` 4 lakh and ` 4.5 lakhrespectively.

(c) The cost and net realisable value of stock on 31.03.13 were `

32,000 and` 40,000 respectively.

(d) Expenses for the year amounted to ` 14,900.

(e) Deferred cost is amortised equally over 4 years.

(f) Debtors on 31.03.13 is ` 25,000, of which ` 2,000 is doubtful. Collection of another` 4,000 depends on successful re-installation of certain product supplied to thecustomer.

(g) Closing trade payable is ` 12,000, which is likely to be settled at 5% discount.

(h) Cash balance on 31.03.13 is ` 37,100.

(i) There is an early repayment penalty for the loan `

2,500.The Profit and Loss Accounts and Balance Sheets of the trader are shown below in two cases(i) assuming going concern (ii) not assuming going concern.

Profit and Loss Account for the year ended 31 st March, 2013

Case (i) Case (ii) Case (i) Case (ii)

` ` ` `

To Opening Stock 30,000 30,000 By Sales 4,50,000 4,50,000

To Purchases 4,00,000 4,00,000 By Closing Stock 32,000 40,000

(b) Accru al Basis: Under this basis of accounting, transactions are recognised as soon asthey occur, whether or not cash or cash equivalent is actually received or paid. Accrual basis

ensures better matching between revenue and cost and profit/loss obtained on this basisreflects activities of the enterprise during an accounting period, rather than cash flows

generated by it. Hence, accrual basis is a more logical approach for profit determination

compared to cash basis of accounting.

Accrual basis exposes an enterprise to the risk of recognising an income before actual receipt.The accrual basis can therefore overstate the divisible profits and dividend decisions based on

such overstated profit lead to erosion of capital. For this reason, accounting standards require

that no revenue should be recognised unless the amount of consideration and actualrealisation of the consideration is reasonably certain. Despite the possibility of distribution ofprofit not actually earned, accrual basis of accounting is generally followed because of its

logical superiority over cash basis of accounting. Section 209(3)(b) of the Companies Actmakes it mandatory for companies to maintain accounts on accrual basis only. It is not

necessary to expressly state that accrual basis of accounting has been followed in preparationof a financial statement. In case, any income/expense is recognised on cash basis, the fact

should be stated.

Example 2

(a) A trader purchased article A on credit in period 1 for ` 50,000.

(b) He also purchased article B in period 1 for ` 2,000 cash.

(c) The trader sold article A in period 1 for ` 60,000 in cash.

(d) He also sold article B in period 1 for ` 2,500 on credit.

Profit and Loss Account of the trader by two basis of accounting are shown below. A look atthe cash basis Profit and Loss Account will convince any reader of the irrationality of cashbasis of accounting.

Framework for Preparation and Presentation of Financial Statements 1.7

Cash basis of accounting

Cash purchase of article B and cash sale of article A is recognised in period 1 while purchaseof article A on payment and sale of article B on receipt is recognised in period 2.

Profit and Loss Account

` `

Period 1 To Purchase 2,000 Period 1 By Sale 60,000

To Net Profit 58,000

60,000 60,000

Period 2 To Purchase 50,000 Period 2 By Sale 2,500

By Net Loss 47,50050,000 50,000

Accrual basis of accounting

Credit purchase of article A and cash purchase of article B and cash sale of article A andcredit sale of article B is recognised in period 1 only.

Profit and Loss Account

` `

Period 1 To Purchase 52,000 Period 1 By Sale 62,500

To Net Profit 10,500

62,500 62,500

(c) Consistency: The principle of consistency refers to the practice of using sameaccounting policies for similar transactions in all accounting periods. The consistency

improves comparability of financial statements through time. An accounting policy can be

changed if the change is required

(i) by a statute or

(ii) by an accounting standard or

(iii) for more appropriate presentation of financial statements.

7. Qualitative Characterist icsThe qualitative characteristics are attributes that improve the usefulness of information

provided in financial statements. The framework suggests that the financial statements should

observe and maintain the following five qualitative characteristics as far as possible withinlimits of reasonable cost/ benefit.

Let us discuss each element of financial statement in detail.

1. Asset: An asset is a resource controlled by the enterprise as a result of past events from

which future economic benefits are expected to flow to the enterprise. The following pointsmust be considered while recognizing an asset:

(a) The resource regarded as an asset, need not have a physical substance. The resource

may represent a right generating future economic benefit, e.g. patents, copyrights,debtors and bills receivable. An asset without physical substance can be either

intangible asset, e.g. patents and copyrights or monetary assets, e.g. debtors and billsreceivable. The monetary assets are money held and assets to be received in fixed or

determinable amounts of money.

(b) An asset is a resource controlled by the enterprise. This means it is possible to recognise aresource not owned but controlled by the enterprise as an asset. Such is the case of

financial lease, where lessee recognises the asset taken on lease, even if ownership lies

with the lessor. Likewise, the lessor does not recognise the asset given on finance lease as

asset in his books, because despite of ownership, he does not control the asset.

(c) A resource cannot be recognised as an asset if the control is not sufficient. For this

reason specific management or technical talent of an employee cannot be recognised

because of insufficient control. When the control over a resource is protected by a legalright, e.g. copyright, the resource can be recognised as an asset.

(d) To be considered as an asset, it must be probable that the resource generates future

economic benefit. If the economic benefit from a resource is expected to expire within the

current accounting period, it is not an asset. For example, economic benefit, i.e. profit onsale, from machinery purchased by a machinery dealer is expected to expire within the

current accounting period. Such purchase of machinery is therefore booked as an expenserather than capitalised in the machinery account. However, if the articles purchased by adealer remain unsold at the end of accounting period, the unsold items are recognised as

assets, i.e. closing stock, because the sale of the article and resultant economic benefit, i.e.

profit is expected to be earned in the next accounting period.

(e) To be considered as an asset, the resource must have a cost or value that can be

measured reliably.

(f) When flow of economic benefit to the enterprise beyond the current accounting period is

considered improbable, the expenditure incurred is recognised as an expense ratherthan as an asset.

2. Liability: A liability is a present obligation of the enterprise arising from past events, the

settlement of which is expected to result in an outflow of a resource embodying economic

benefits. The following points may be noted:

(a) A liability is a present obligation, i.e. an obligation the existence of which, based on theevidence available on the balance sheet date is considered probable. For example, anenterprise may have to pay compensation if it loses a damage suit filed against it. The

Framework for Preparation and Presentation of Financial Statements 1.11

damage suit is pending on the balance sheet date. The enterprise should recognise aliability for damages payable by a charge against profit if possibility of losing the suit isreasonably certain and if the amount of damages payable can be ascertained with

reasonable accuracy. The enterprise should create a provision for damages payable by

charge against profit, if possibility of losing the suit is more than not losing it and if theamount of damages payable cannot be ascertained with reasonable accuracy. In othercases, the company reports the damages payable as ‘contingent liability’, which does

not meet the definition of liability. AS 29 defines provision as a liability, which can be

measured only by using a substantial degree of estimation.

(b) It may be noted that certain provisions, e.g. provisions for doubtful debts, depreciationand impairment losses, represent diminution in value of assets rather than obligations.

These provisions are outside the scope of AS 29 and hence should not be consideredas liability.

(c) A liability is recognised only when outflow of economic resources in settlement of apresent obligation can be anticipated and the value of outflow can be reliably measured.

Otherwise, the liability is not recognised. For example, future obligations againstinventory ordered but not received) are not usually recognised as liabilities. If in some

circumstances such an obligation is recognised as liability, the related asset / expense

should also be recognised.

Example 3

A Ltd. has entered into a binding agreement with P Ltd. to buy a custom-made machine

`

40,000. At the end of 2012-13, before delivery of the machine, A Ltd. had to change itsmethod of production. The new method will not require the machine ordered and shall bescrapped after delivery. The expected scrap value is nil.

A liability is recognised when outflow of economic resources in sett lement of a presentobligation can be anticipated and the value of outflow can be reliably measured. In the givencase, A Ltd. should recognise a liability of ` 40,000 to P Ltd.

When flow of economic benefit to the enterprise beyond the current accounting period isconsidered improbable, the expenditure incurred is recognised as an expense rather than asan asset. In the present case, flow of future economic benefit from the machine to theenterprise is improbable. The entire amount of purchase price of the machine should berecognised as an expense. The accounting entry is suggested below:

` `

Profit and Loss Account(Loss due to change in production method)

Dr. 40,000

To P Ltd. 40,000

3. Equity: Equity is defined as residual interest in the assets of an enterprise after

deducting all its liabilities. It is important to avoid mixing up liabilities with equity. Equity is the

excess of aggregate assets of an enterprise over its aggregate liabilities. In other words,equity represents owners’ claim consisting of items like capital and reserves, which are clearlydistinct from liabilities, i.e. claims of parties other than owners. The value of equity may

change either through contribution from / distribution to equity participants or due to income

earned /expenses incurred.

4. Income: Income is increase in economic benefits during the accounting period in theform of inflows or enhancement of assets or decreases in liabilities that result in increase in

equity other than those relating to contributions from equity participants. The definition ofincome encompasses revenue and gains. Revenue is an income that arises in the ordinary

course of activities of the enterprise, e.g. sales by a trader. Gains are income, which may ormay not arise in the ordinary course of activity of the enterprise, e.g. profit on disposal of fixed

assets. Gains are showed separately in the statement of profit and loss because thisknowledge is useful in assessing performance of the enterprise.

Income earned is always associated with either increase of asset or reduction of liability. Thismeans, no income can be recognised unless the corresponding increase of asset or decrease

of liability can be recognised. For example, a bank does not recognise interest earned on non-performing assets because the corresponding asset (increase in advances) cannot be

recognised, as flow of economic benefit to the bank beyond current accounting period is not

probable. Thus

Balance sheet of an enterprise can be written in form of:

A – L = E.

Where:

A = Aggregate value of asset

L = Aggregate value of liabilities

E = Aggregate value of equity

Example 4

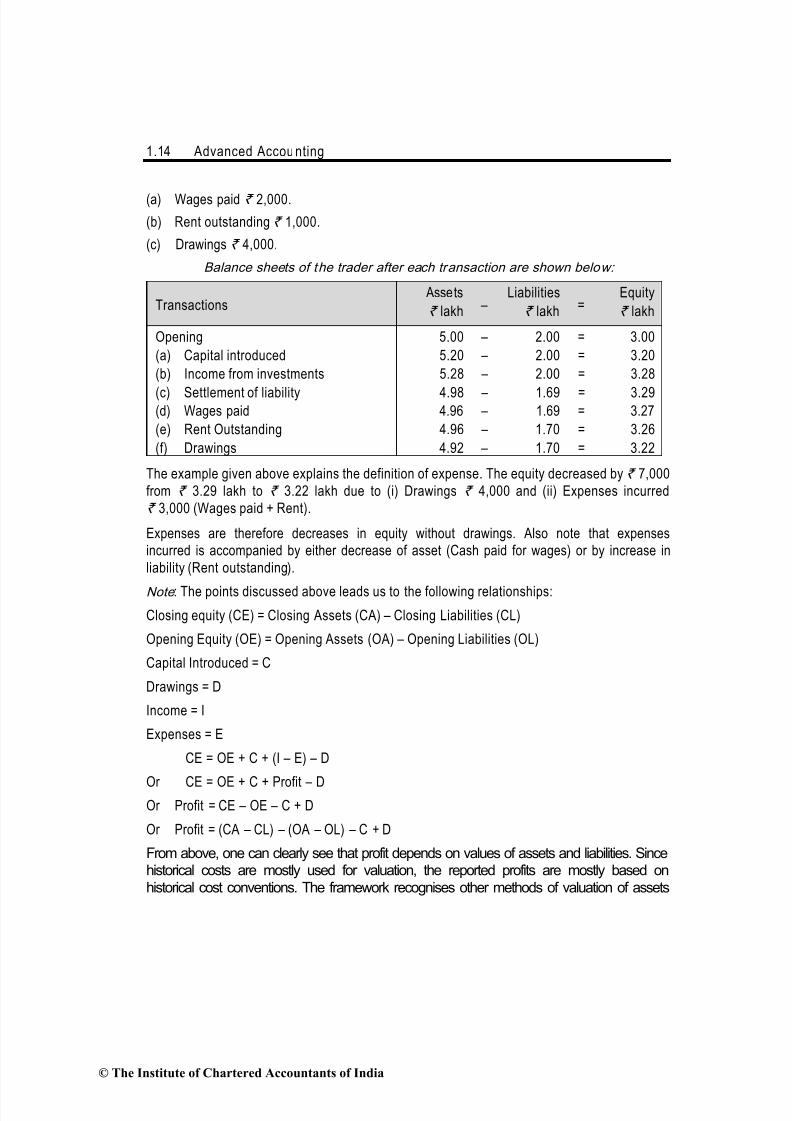

Suppose at the beginning of an accounting period, aggregate values of assets, liabilities andequity of a trader are ` 5 lakh, ` 2 lakh and ` 3 lakh respectively.

Also suppose that the trader had the following transactions during the accounting period.

(a) Introduced capital ` 20,000.

(b) Earned income from investment ` 8,000.

(c) A liability of ` 31,000 was finally settled on payment of ` 30,000.

Framework for Preparation and Presentation of Financial Statements 1.13

Balance sheets of the trader after each transaction are shown below:

Transactions Assets

` lakh –

Liabilities

` lakh=

Equity

` lakh

Opening 5.00 – 2.00 = 3.00

(a) Capital introduced 5.20 – 2.00 = 3.20

(b) Income from investments 5.28 – 2.00 = 3.28

(c) Settlement of liability 4.98 – 1.69 = 3.29

This example given explains the definition of income. The equity increased by` 29,000 during the accounting period, due to (i) Capital introduction ` 20,000 and (ii) Income

earned`

9,000 (Income from investment + Discount earned). Incomes are therefore increasesin equity without introduction of capital.

Also note that income earned is accompanied by either increase of asset (Cash received asinvestment income) or by decrease of liability (Discount earned).

5. Expense: An expense is decrease in economic benefits during the accounting period inthe form of outflows or depletions of assets or incurrence of liabilities that result in decrease in

equity other than those relating to distributions to equity participants. The definition ofexpenses encompasses expenses that arise in the ordinary course of activities of the

enterprise, e.g. wages paid. Losses may or may not arise in the ordinary course of activity ofthe enterprise, e.g. loss on disposal of fixed assets. Losses are separately showed in the

statement of profit and loss because this knowledge is useful in assessing performance of the

enterprise.

Expenses are always incurred simultaneously with either reduction of asset or increase ofliability. Thus, expenses are recognised when the corresponding decrease of asset or

increase of liability are recognised by application of the recognition criteria stated above.Expenses are recognised in Profit & Loss A/c by matching them with the revenue generated.

However, application of matching concept should not result in recognition of an item as asset(or liability), which does not meet the definition of asset or liability as the case may be.

Where economic benefits are expected to arise over several accounting periods, expenses are

recognised in the profit and loss statement on the basis of systematic and rational allocationprocedures. The obvious example is that of depreciation.

An expense is recognised immediately in the profit and loss statement when it does not meetor ceases to meet the definition of asset or when no future economic benefit is expected. An

expense is also recognised in the profit and loss statement when a liability is incurred withoutrecognition of an asset, as is the case when a liability under a product warranty arises.

Example 5

Continuing with the example 4 given above, suppose the trader had the following furthertransactions during the period:

The example given above explains the definition of expense. The equity decreased by ` 7,000from ` 3.29 lakh to ` 3.22 lakh due to (i) Drawings ` 4,000 and (ii) Expenses incurred` 3,000 (Wages paid + Rent).

Expenses are therefore decreases in equity without drawings. Also note that expensesincurred is accompanied by either decrease of asset (Cash paid for wages) or by increase inliability (Rent outstanding).

Note : The points discussed above leads us to the following relationships:

Or CE = OE + C + Profit – DOr Profit = CE – OE – C + D

Or Profit = (CA – CL) – (OA – OL) – C + D

From above, one can clearly see that profit depends on values of assets and liabilities. Sincehistorical costs are mostly used for valuation, the reported profits are mostly based on

historical cost conventions. The framework recognises other methods of valuation of assets

Framework for Preparation and Presentation of Financial Statements 1.17

By historical cost convention, the machine would have been recorded at `

4,90,000.

To settle the deferred payment on current date one must buy dollars at ` 49/$. The liability istherefore recognised at ` 4,90,000 ($ 10,000 × ` 49). Note that the amount of liabilityrecognised is not the present value of future payments. This is because, in current costconvention, liabilities are recognised at undiscounted amount.

3. Realis able (Settlement ) Value: For assets, this is the amount currently realisable onsale of the asset in an orderly disposal. For liabilities, this is the undiscounted amount

expected to be paid on settlement of liability in the normal course of business. As perrealisable value, assets are carried at the amount of cash or cash equivalents that could

currently be obtained by selling the assets in an orderly disposal. Haphazard disposal mayyield something less. Liabilities are carried at their settlement values; i.e. the undiscounted

amount of cash or cash equivalents expressed to be paid to satisfy the liabilities in the normal

course of business.

4. Present Value: Present value of an amount A, after n years is the amount P, one has toinvest on current date to have A after n years. If the rate of interest is R then,

A = P(1 + R)n

Or P (Present value of A after n years) =( ) ( )nn

R1

1 A

R1

A

+

×=

+

The process of obtaining present value of future cash flow is called discounting. The rate of

interest used for discounting is called the discounting rate. The expression [1/(1+R)n], called

discounting factor depends on values of R and n.

Let us take a numerical example assuming interest 10%, A = ` 11,000 and n = 1 year

11,000 = 10,000(1 + 0.1)1

Or Present value of ` 11,000 after 1 year =( ) ( )

1 1

11,000 111,000

1.10 1.10= ×

Or Present value of ` 11,000 after 1 year = 11,000 × 0.909 = ` 10,000

Note that a receipt of ` 10,000 (present value) now is equivalent of a receipt of ` 11,000(future cash inflow) after 1 year, because if one gets ` 10,000 now he can invest to collect` 11,000 after 1 year. Likewise, a payment of ` 10,000 (present value) now is equivalent of

paying of `

11,000 (future cash outflow) after 1 year.

Thus if an asset generates ` 11,000 after 1 year, it is actually contributing ` 10,000 at thecurrent date if the rate of earning required is 10%. In other words, the value of the asset is` 10, 000. which is the present value of net future cash inflow it generates.

If an asset generates ` 11,000 after 1 year, and ` 12,100 after two years, it is actuallycontributing ` 20,000 (approx.) at the current date if the rate of earning required is 10%

12,100 × 0.826). In other words the value of the asset is` 20,000(approx.), i.e. the present value of net future cash inflow it generates.

Under present value convention, assets are carried at present value of future net cash flows

generated by the concerned assets in the normal course of business. Liabilities under thisconvention are carried at present value of future net cash flows that are expected to be

required to settle the liability in the normal course of business.

Example 8

Carrying amount of a machine is ` 40,000 (Historical cost less depreciation). The machine isexpected to generate ` 10,000 net cash inflow. The net realisable value (or net selling price) of themachine on current date is ` 35,000. The enterprise’s required earning rate is 10% per year.

The enterprise can either use the machine to earn `

10,000 for 5 years. This is equivalent ofreceiving present value of ` 10,000 for 5 years at discounting rate 10% on current date. Thevalue realised by use of the asset is called value in use. The value in use is the value of assetby present value convention.

Value in use = ` 10,000 (0.909 + 0.826 + 0.751 + 0.683 + 0.621) = ` 37,900

Net selling price = ` 35,000

The present value of the asset is ` 37,900, which is called its recoverable value. It isobviously not appropriate to carry any asset at a value higher than its recoverable value. Thusthe asset is currently overstated by ` 2,100 (` 40,000 – ` 37,900).

10. Capital MaintenanceCapital refers to net assets of a business. Since a business uses its assets for its operations,

a fall in net assets will usually mean a fall in its activity level. It is therefore important for anybusiness to maintain its net assets in such a way, as to ensure continued operations at least

at the same level year after year. In other words, dividends should not exceed profit afterappropriate provisions for replacement of assets consumed in operations. For this reason, the

Companies Act does not permit distribution of dividend without providing for depreciation onfixed assets. Unfortunately, this may not be enough in case of rising prices. The point is

explained below:

We have already observed: P = (CA – CL) – (OA – OL) – C + D

Where: Profit = POpening Assets = OA and Opening Liabilities = OL

Closing Assets = CA and Closing Liabilities = CL

Introduction of capital = C and Drawings / Dividends = D

Retained Profit = P – D = (CA – CL) – (OA – OL) – C

Or Retained Profit = Closing Equity – (Opening Equity + Capital Introduced)

Framework for Preparation and Presentation of Financial Statements 1.19

A business must ensure that Retained Profit (RP) is not negative, i.e. closing equity should notbe less than capital to be maintained, which is sum of opening equity and capital introduced.

It should be clear from above that the value of retained profit depends on the valuation of

assets and liabilities. In order to check maintenance of capital, i.e. whether or not retained

profit is negative, we can use any of following three bases:

Financial capital maintenance at historical cost: Under this convention, opening andclosing assets are stated at respective historical costs to ascertain opening and closing equity.If retained profit is greater than zero, the capital is said to be maintained at historical costs.

This means the business will have enough funds to replace its assets at historical costs. This

is quite right as long as prices do not rise.

Example 9 A trader commenced business on 01/01/2012 with ` 12,000 represented by 6,000 units of acertain product at ` 2 per unit. During the year 2012 he sold these units at ` 3 per unit andhad withdrawn ` 6,000. Thus:

Opening Equity = ` 12,000 represented by 6,000 units at ` 2 per unit.

The trader can start year 2013 by purchasing 6,000 units at ` 2 per unit once again for sellingthem at ` 3 per unit. The whole process can repeat endlessly if there is no change inpurchase price of the product.

Financial capital maintenance at current purchasing power: Under this convention,

opening and closing equity at historical costs are restated at closing prices using averageprice indices. (For example, suppose opening equity at historical cost is ` 3,00,000 andopening price index is 100. The opening equity at closing prices is ` 3,60,000 if closing priceindex is 120). A positive retained profit by this method means the business has enough funds

to replace its assets at average closing price. This may not serve the purpose because pricesof all assets do not change at average rate in real situations. For example, price of a machine

can increase by 30% while the average increase is 20%.

Example 10

In the previous example (Example 9), suppose that the average price indices at the beginning

and at the end of year are 100 and 120 respectively.Opening Equity = ` 12,000 represented by 6,000 units at ` 2 per unit.

Opening equity at closing price = (` 12,000 / 100) x 120 = ` 14,400 (6,000 x ` 2.40)

The negative retained profit indicates that the trader has failed to maintain his capital. Theavailable fund ` 12,000 is not sufficient to buy 6,000 units again at increased price ` 2.40 per

unit. In fact, he should have restricted his drawings to ` 3,600 (` 6,000 – ` 2,400).

Had the trader withdrawn ` 3,600 instead of ` 6,000, he would have left with ` 14,400, the

fund required to buy 6,000 units at ` 2.40 per unit.

Physical capital maintenance at current costs: Under this convention, the historical costs

of opening and closing assets are restated at closing prices using specific price indices

applicable to each asset. The liabilities are also restated at a value of economic resources to

be sacrificed to settle the obligation at current, i.e. closing date. The opening and closing

equity at closing current costs are obtained as excess of aggregate of current cost values of

assets over aggregate of current cost values of liabilities. A positive retained profit by this

method ensures retention of funds for replacement of each asset at respective closing prices.

Example 11 (Physical capital maintenance)

In the previous example(Example 9) suppose that the price of the product at the end of year is

` 2.50 per unit. In other words, the specific price index applicable to the product is 125.

Current cost of opening stock = (` 12,000 / 100) x 125 = 6,000 x ` 2.50 = ` 15,000

Current cost of closing cash = ` 12,000 (` 18,000 – ` 6,000)

Opening equity at closing current costs = ` 15,000

Framework for Preparation and Presentation of Financial Statements 1.23

outflow of a resource embodying economic benefits.

Equity Residual interest in the assets of an enterprise afterdeducting all its liabilities.

Income/gain Increase in economic benefits during the accounting periodin the form of inflows or enhancement of assets ordecreases in liabilities that result in increase in equity otherthan those relating to contributions from equity participants

Expense/loss Decrease in economic benefits during the accounting periodin the form of outflows or depletions of assets or incurrenceof liabilities that result in decrease in equity other than thoserelating to distributions to equity participants.

• Measurement of Elements in Financi al Statements

Historical cost Acquisition price

Current Cost Assets are carried out at the amount of cash or cashequivalent that would have to be paid if the same or an

equivalent asset was acquired currently. Liabilities arecarried at the undiscounted amount of cash or cashequivalents that would be required to settle the

obligation currently.

Realisable (Settlement)

Value

For assets, amount currently realisable on sale of the

asset in an orderly disposal. For liabilities, this is theundiscounted amount expected to be paid on settlement

of liability in the normal course of business.

Present Value Assets are carried at present value of future net cashflows generated by the concerned assets in the normalcourse of business. Liabilities are carried at present

value of future net cash flows that are expected to berequired to settle the liability in the normal course of

business.

• Capital Maintenance

Financial capital maintenance At historical cost Opening and closing assets are stated athistorical costs.

At current purchasing power Restatement at closing prices using averageprice indices.

Physical capital maintenance Restatement at closing prices using specific priceindices.