58

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | baylee-dowen |

| View: | 216 times |

| Download: | 3 times |

2

Five forces of change in the

Australian Agrifood sector

Dr David McKinna

July 2013

The agrifood sector is undergoing its biggest shift in history . . .

. . . and regional Australia is feeling the impact!

This change is being driven by 5 forces

2Private Label Renaissance

1Supermarket Oligopsony

4Corporatisation &

technology

5Water

3Global

competitiveness

. . . with apologies to Michael Porter

1Supermarket Oligopsony

7

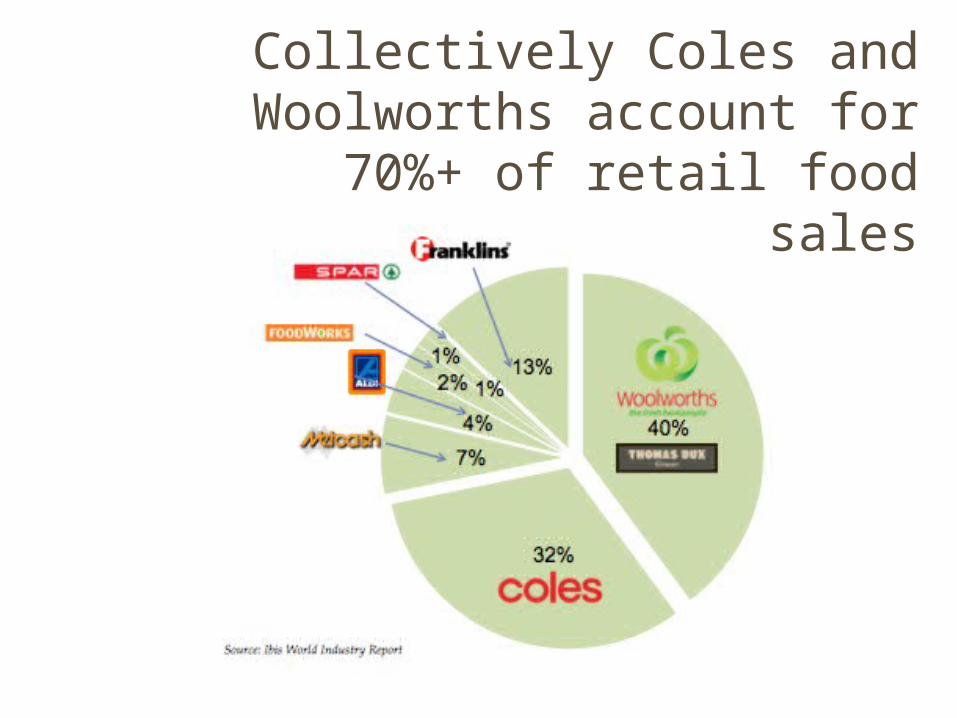

Collectively Coles and Woolworths account for 70%+

of retail food sales

8

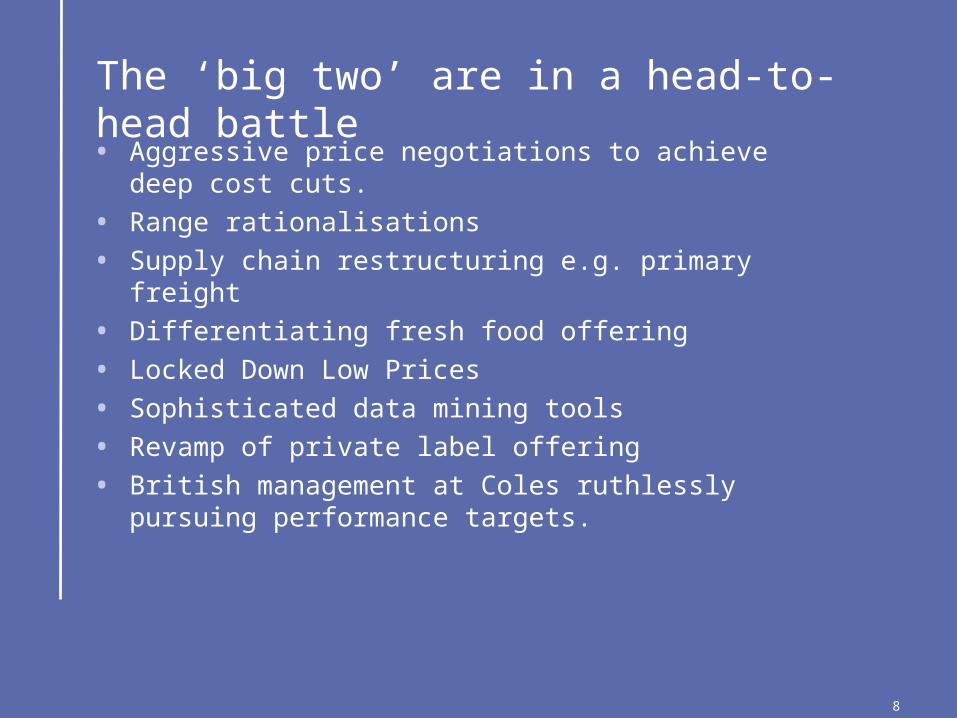

The ‘big two’ are in a head-to-head battle

• Aggressive price negotiations to achieve deep cost cuts.

• Range rationalisations

• Supply chain restructuring e.g. primary freight

• Differentiating fresh food offering

• Locked Down Low Prices

• Sophisticated data mining tools

• Revamp of private label offering

• British management at Coles ruthlessly pursuing performance targets.

Bread and milk are

now loss leaders

Large scale food producers have no option but to roll the dice with the devil

Most major food companies have

over 60% of their business with

Coles and Woolworths

50% of food sold in

supermarkets is sold on promotion

13

Down, down, down goes category value

Category value is being destroyedProfitability is declining for all processorsReduced investment in R&D and innovationProduct de-engineeringMultinationals are rewriting their Australian strategiesSMEs are a threatened species – many are in

receivership

There is an everyday battle for shelf space

‘Cliffing’ is just one of their tactics

15

Supermarkets are using smart cards to build data bases on shopper behaviour

The Aldi factor added fuel to the discounting fire

Supermarkets don’t profit more from their power

Consumers are the main beneficiaries of the price war - at least in the short term.

This is why ACCC wont step in.Supermarket margins are low, they work on shopper

traffic and volume.In the longer term, consumers will have less choice and

many Australians will lose their jobs.

19

Most food companies have had enforced price cuts despite significant cost increases

20

Over the past three years Australian consumers have enjoyed a 4% deflation in food prices!

$ 1Milk has resulted in a transfer of value of approximately $2 billion p.a from processors and and producers

22

Supermarkets are exploiting social sensitivities

23

Processor margins are not sufficient to

support the reinvestment needed

to remain globally competitive

24

Global food companies are closing Australian factories

25

Once the plants are closed down, they will not reopen

“The Australian market is the worst market . . . (to do business in)”

Bill JohnsonHeinz Global Chair

2Private Label Renaissance

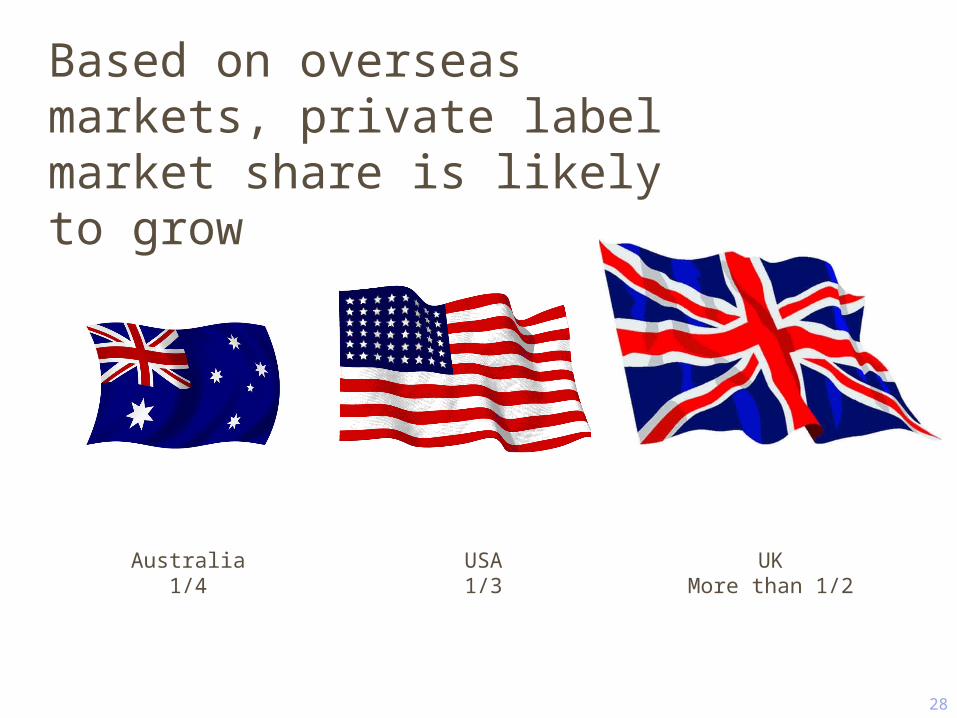

Based on overseas markets, private label market share is likely to grow

28

Australia1/4

USA1/3

UKMore than 1/2

Private label has now become the smart shopper’s choice

30

Private label is seriously eroding the value of most food categories

It is benchmarked against market leaders,Sold at 30-50% discount.Takes shelf space from proprietary brands.Proprietary brand owners are forced to discount to

protect market share and shelf-space.The profit margins for producing private label are razor

thin.For products that can be economically shipped, there is

direct competition from low cost imported product.

Valrhona ChocolateSimon Johnson

$21.95

Private Label Chocolate Aldi

$2.49

Strong proprietary brands generate the margins required to fund innovation and category growth

32

3Global

competitiveness

In most agrifood products with a high labour component, Australia is hopelessly uncompetitive

35

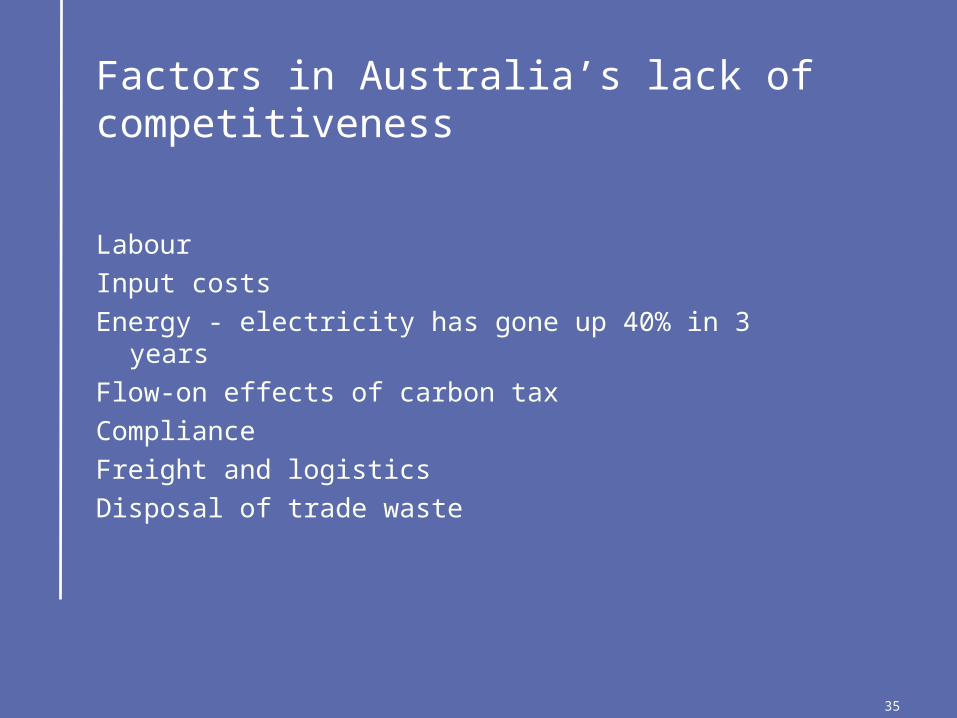

Factors in Australia’s lack of competitiveness

LabourInput costsEnergy - electricity has gone up 40% in 3 yearsFlow-on effects of carbon taxComplianceFreight and logisticsDisposal of trade waste

The weighted average labour cost in a processing plant is:

Australia: $56 per hourNew Zealand: $18 per hour China: $4 per hour

37

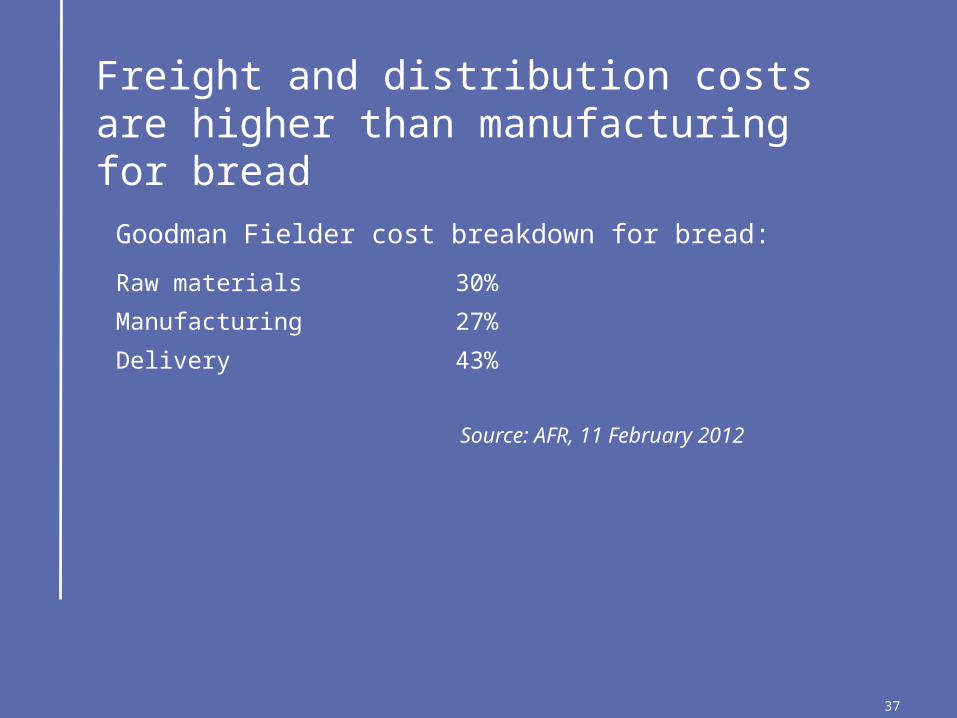

Freight and distribution costs are higher than manufacturing for bread

Source: AFR, 11 February 2012

Goodman Fielder cost breakdown for bread:

Raw materials 30%

Manufacturing 27%

Delivery 43%

$AUD needs to be around 70-80c to the $USD for Australia to be competitive. Economists predict it will stay at around 90c for the next five years

The free trade agenda benefits some industries at the expense

of others

40

For multinationals, margins are no longer sufficient to manufacture in Australia

4Corporatisation& technology

The economics of agriculture demands scale

43

The critical importance of scale

Major improvements in overhead recovery

Farms have to double in size every 10 years to produce the same income.

Farm productivity is growing at 2% PA.

Commodity prices are cyclical but on average are not keeping up with inflation rates.

Scale requires technology and capital

45

Demand for capital is driving corporate farming models

ScaleGeographic spread Production volumeCapitalBest practice technology and IPLogistics capabilityTight cost control

Corporate models demand:

In most horticultural industries fewer than 8 businesses supply 70+% of the market

47

There is a growing interest in Australian agrifood assets by foreign investors

They see assets agrifood assets as undervaluedAnticipate growing demand for foodExpect long term capital gainsEnsuring food supply for sovereign needs

48

Technology reduces need for labour

Direct seedingLarge GPS controlled machineryRoboticsSelf-guided vehiclesDronesSmart phone apps

Because of efficiency, corporatisation can be profitable and substantially reduce costs

Smaller farm businesses aren’t viable at these prices

5Water

Today farming is about managing water

52

Impact of the MDB Plan

Loss of production- irrigation land is 20 times more productive than dry land

Loss of processing jobsMany farms off the backbone channels will become

uneconomic to irrigate Farms are too small to support a family in a dry land

farming enterprise.It will be uneconomic to use irrigation for grazing.

Around 30% of water has been removed from Victoria’s irrigation system

What does this mean for regional Victoria?

54

The prognosis

Many agrifood companies will disappear More jobs will be lostDry land farming towns will be under continued

pressureSmaller family farms will exit the industry, selling out

to lifestyle hobby farmers Corporate investors will move in

What can local government do about this?

InformationInfrastructureIntroductions

56

LGAs must become change leaders

Provide information and knowledge transfer about industry trends

Help farmers adapt to changing circumstancesTreat food processing businesses as a threatened species Be business friendlyHelp towns suffering the loss of irrigation water to find new

dry land enterprisesImplement sensible land use planning regulationsManage peri urban interfaces Make your shire investor friendlySupport farmers markets and buy-local programsSupport more business building capability in online

marketing and farmers markets Support networking and information sharing

This is the reality of a

free market, global

economy

mckinna.com.au