21

Consolidations

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| Upload: | bonnie-chase |

| View: | 219 times |

| Download: | 5 times |

Consolidations

2

IntroductionWhen a holding company (parent) purchases the share

capital of its subsidiary (or subsidiaries), each company in the group: remains a legal entity in its own right; and is bound to maintain separate accounting records

The parent company must present to its shareholders its own financial statements and consolidated financial statements.

Exceptions – NZ IFRS 10 para 4A parent prepares consolidated financial statements

using uniform accounting policies for like transactions and other events in similar circumstances (para 19).

3

Consolidation (NZ IFRS 10)In consolidation the parent entity combines like its items of

assets, liabilities, equity, income, expenses and cash flows with those of its subsidiaries (para B86 (a))

The carrying amount of the parent's investment in each subsidiary should be offset against the parent's portion of equity of each subsidiary (para B86 (b))

Intragroup balances, transactions, income and expenses shall be eliminated in full (para B86(c))

A parent presents non-controlling interests in its consolidated statement of financial position within equity, separately from the equity of the owners of the parent (para 22).

Consolidation journalsAdjustments for the purposes of consolidation are

made through consolidation journal entries.These consolidation journals are ONLY prepared for

the purposes of consolidation. (There are no consolidated ledger accounts)

They are posted onto the consolidation worksheet only – they are NOT recorded in the books of the parent or the subsidiary

As a result, some consolidation adjustments are repeated every time consolidated financial statements are prepared

4

Consolidation journals are posted into the consolidation worksheet in “adjustment” columns as follows:

Consolidation Worksheets

Parent

Parent

Subsidiary

Subsidiary

Add down for sub-totals

Add down for sub-totals

Purpose: to remove the parent’s investment in the subsidiary and the effect of all inter-entity transactions so that the final column shows an “external view”

Purpose: to remove the parent’s investment in the subsidiary and the effect of all inter-entity transactions so that the final column shows an “external view”

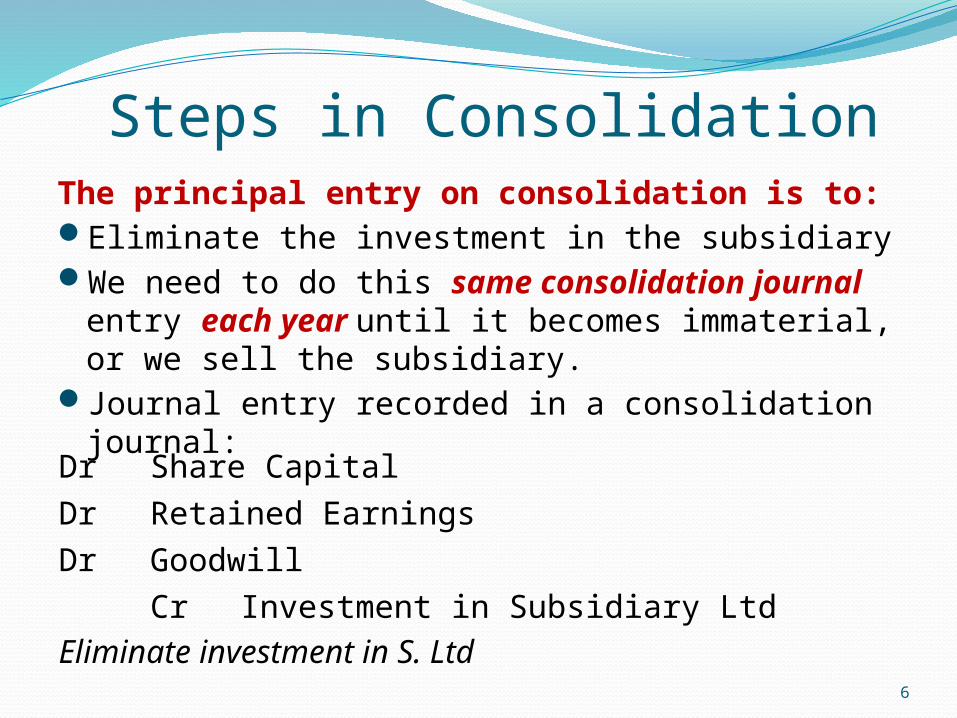

6

Steps in ConsolidationThe principal entry on consolidation is to:Eliminate the investment in the subsidiaryWe need to do this same consolidation journal entry

each year until it becomes immaterial, or we sell the subsidiary.

Journal entry recorded in a consolidation journal:

Dr Share Capital

Dr Retained Earnings

Dr Goodwill

Cr Investment in Subsidiary LtdEliminate investment in S. Ltd

7

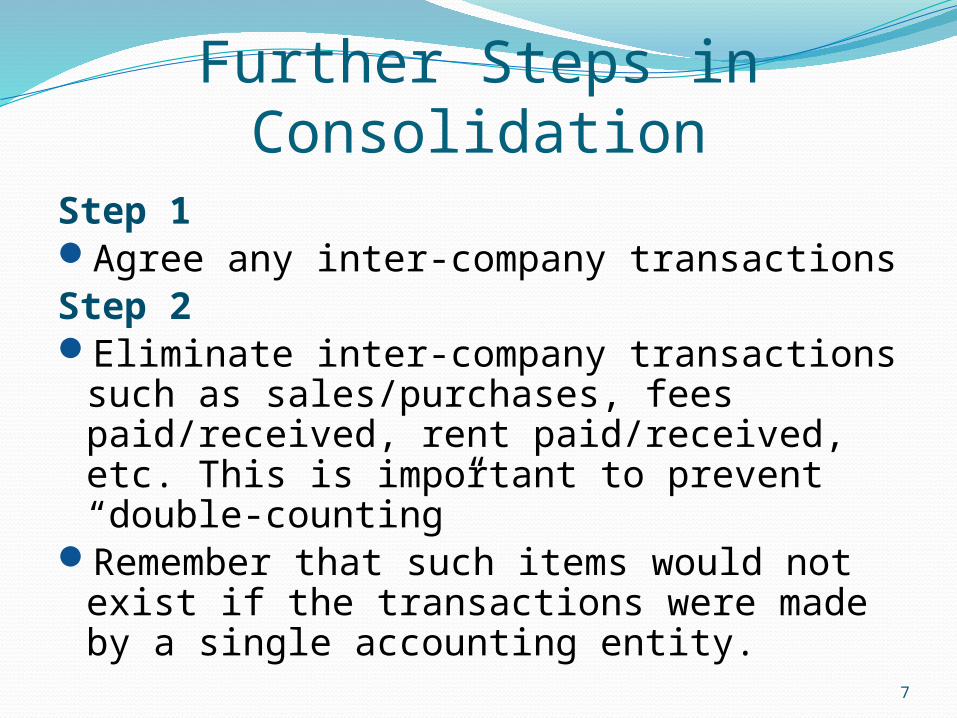

Further Steps in ConsolidationStep 1Agree any inter-company transactionsStep 2Eliminate inter-company transactions such as

sales/purchases, fees paid/received, rent paid/received, etc. This is important to prevent “double-counting”

Remember that such items would not exist if the transactions were made by a single accounting entity.

8

Steps in Consolidation - 3 & 4Step 3Eliminate inter-company balances – they

wouldn’t exist if the two companies were a single entity.

Step 4Eliminate unrealised inter-company profits

because such profits are illusory until realised outside the group.

9

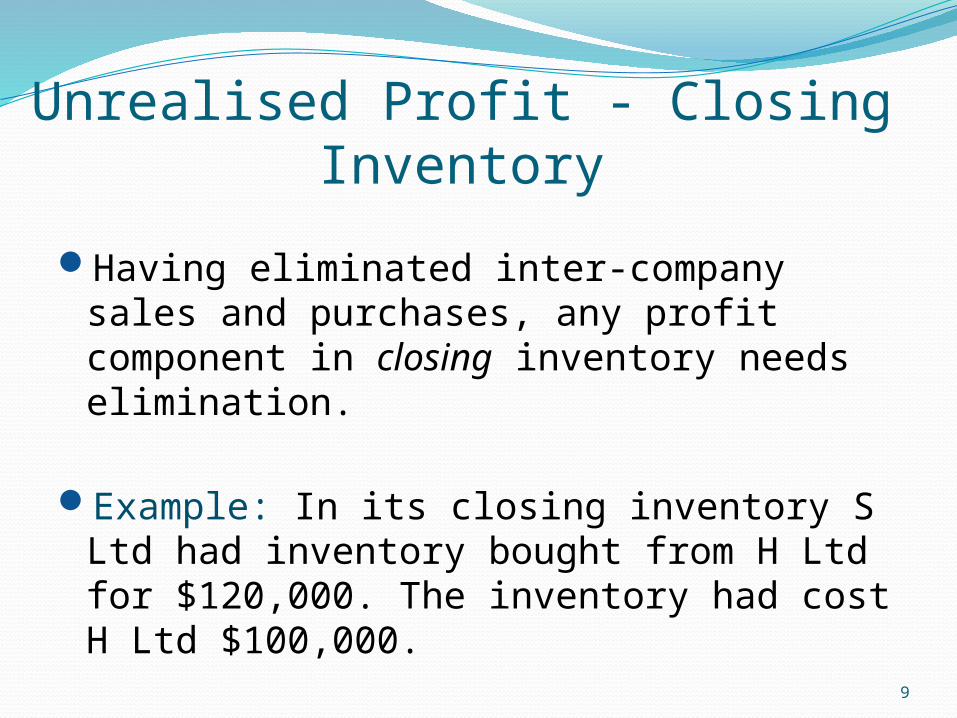

Unrealised Profit - Closing Inventory

Having eliminated inter-company sales and purchases, any profit component in closing inventory needs elimination.

Example: In its closing inventory S Ltd had inventory bought from H Ltd for $120,000. The inventory had cost H Ltd $100,000.

10

Unrealised profit cont’dEliminate the $20,000 unrealised profit:

Dr Cost of sales (Closing inventory) $20,000 Cr Inventory on hand (Bal. Sheet)

$20,000Elimination of unrealised profit on closing inventory

If this related to the year ended 31 March 2012, we would then have to consider the effect on the following income year – ended 31 March 2013

11

Unrealised Profit - Opening Inventory

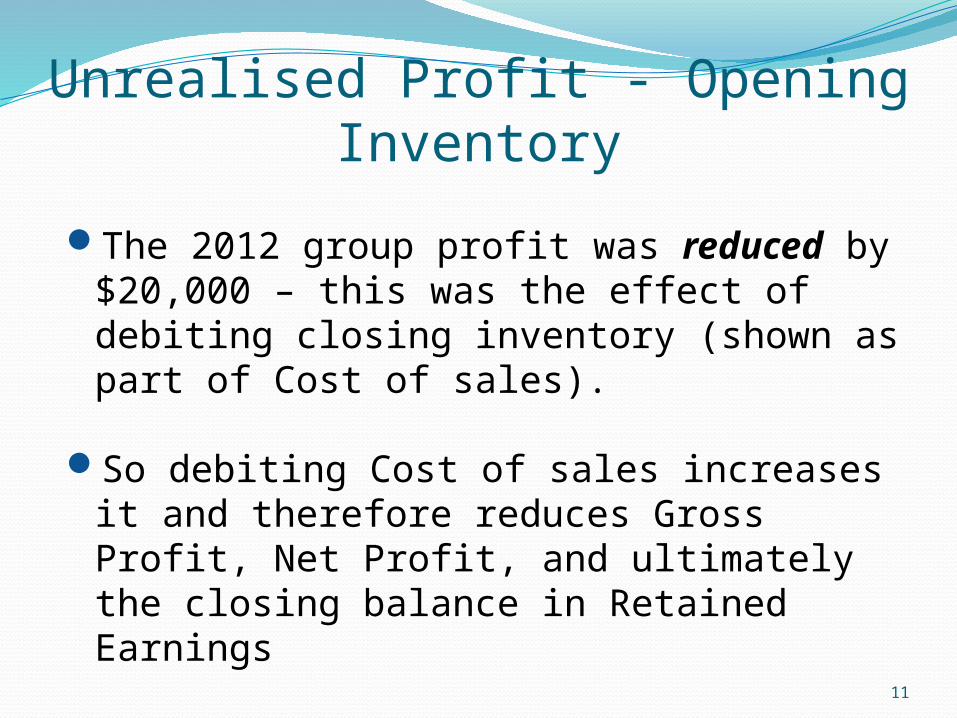

The 2012 group profit was reduced by $20,000 – this was the effect of debiting closing inventory (shown as part of Cost of sales).

So debiting Cost of sales increases it and therefore reduces Gross Profit, Net Profit, and ultimately the closing balance in Retained Earnings

12

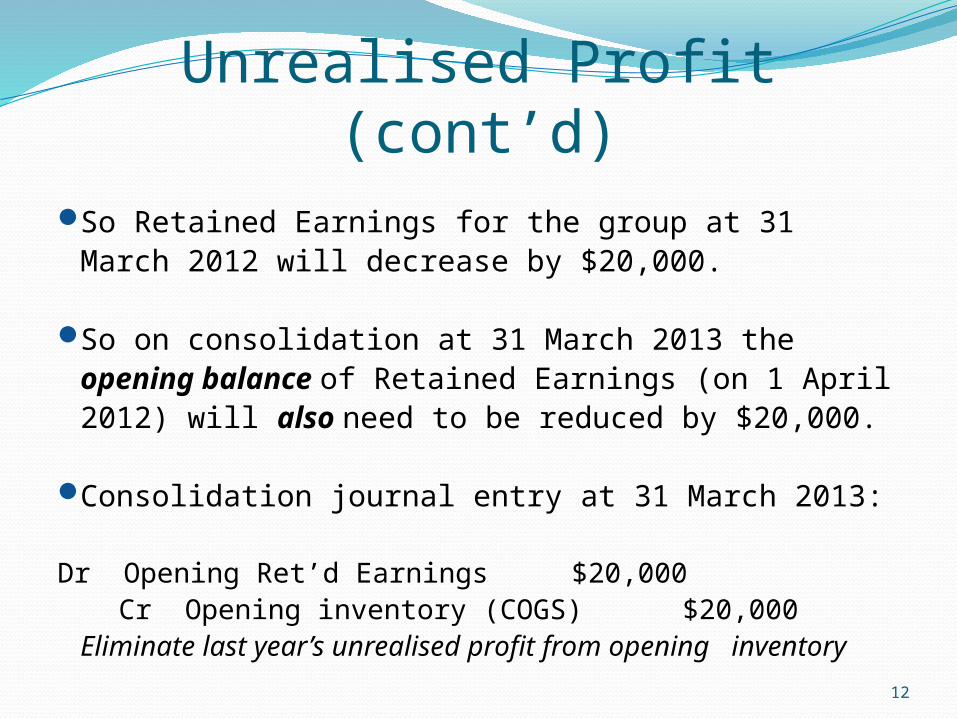

Unrealised Profit (cont’d)So Retained Earnings for the group at 31 March 2012 will

decrease by $20,000.

So on consolidation at 31 March 2013 the opening balance of Retained Earnings (on 1 April 2012) will also need to be reduced by $20,000.

Consolidation journal entry at 31 March 2013: Dr Opening Ret’d Earnings $20,000

Cr Opening inventory (COGS) $20,000Eliminate last year’s unrealised profit from opening

inventory

13

Shifting the unrealised profitThe credit to opening inventory for 2012/13 in

Cost of sales has the effect of increasing gross profit for that year - and eventually Retained Earnings.

So the adjustment for unrealised profit last year is reversed the following year. This shifts the unrealised profit into the year that it will be sold outside the group. Profit is realised in that following year.

14

Unrealised Profit – Non-current Asset Transfers

If a non-current asset is transferred between companies in the group, then where sale price = book value, no further adjustment is required.

But what if the asset is sold above or below book value?

There needs to be a restatement of the position, as if the asset had been transferred at book value.

15

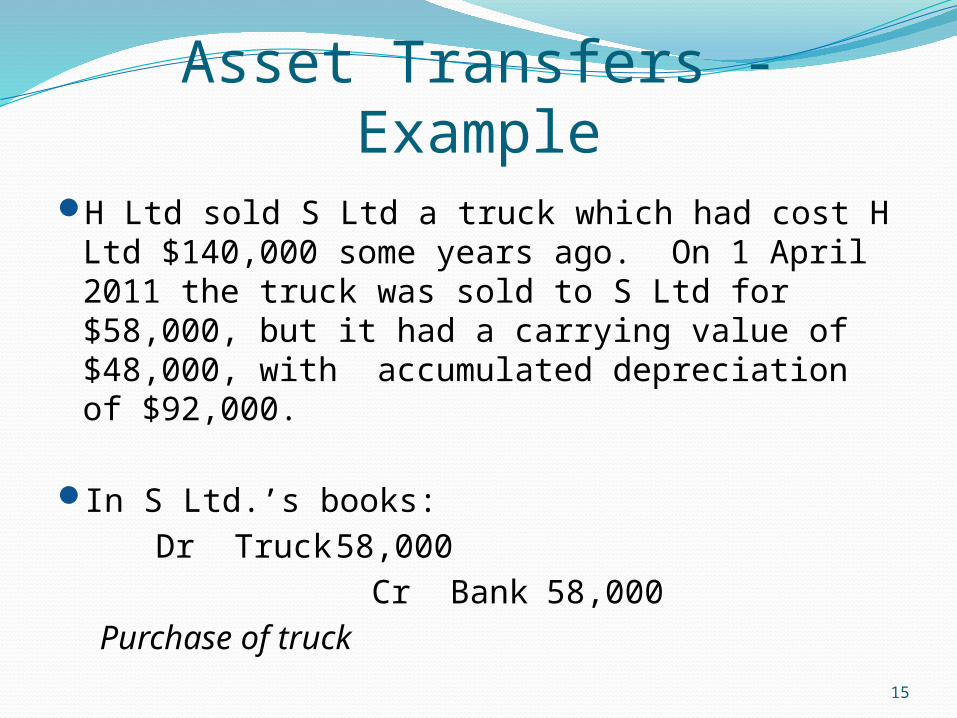

Asset Transfers - ExampleH Ltd sold S Ltd a truck which had cost H Ltd

$140,000 some years ago. On 1 April 2011 the truck was sold to S Ltd for $58,000, but it had a carrying value of $48,000, with accumulated depreciation of $92,000.

In S Ltd.’s books:

Dr Truck 58,000

Cr Bank 58,000

Purchase of truck

16

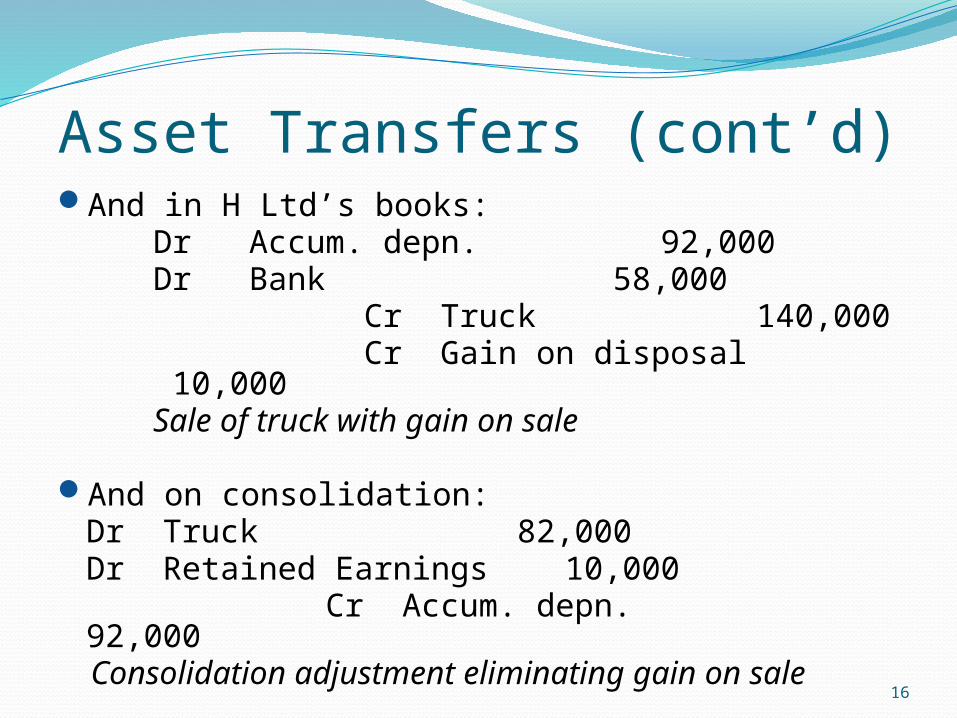

Asset Transfers (cont’d)And in H Ltd’s books: Dr Accum. depn. 92,000 Dr Bank 58,000 Cr Truck 140,000 Cr Gain on disposal 10,000 Sale of truck with gain on sale

And on consolidation:Dr Truck 82,000 Dr Retained Earnings 10,000

Cr Accum. depn. 92,000 Consolidation adjustment eliminating gain on sale

17

Depreciation AdjustmentS Ltd will depreciate the truck for the 2011/12 and

20012/13 income years. Assuming a common depn. rate (say 30% D.V.), in S Ltd.’s books:

2011/12:Dr Depn. expense 17,400

Cr Accum. depn. 17,400 Depreciation charge (58,000 @ 30% DV)

2012/13:Dr Depn. expense 12,180 Cr Accum. depn. 12,180 Depreciation charge (40,600 @ 30% DV)

18

Depreciation (cont’d)

However, if the asset had not been sold to S Ltd then H Ltd would have continued to depreciate it as follows:

2011/12:Dr Depn. expense 14,400

Cr Accum. depn. 14,400 Depreciation charge (48,000 @ 30% DV)

2012/13:Dr Depn. expense 10,080

Cr Accum. depn. 10,080 Depreciation charge (33,600 @ 30% DV)

19

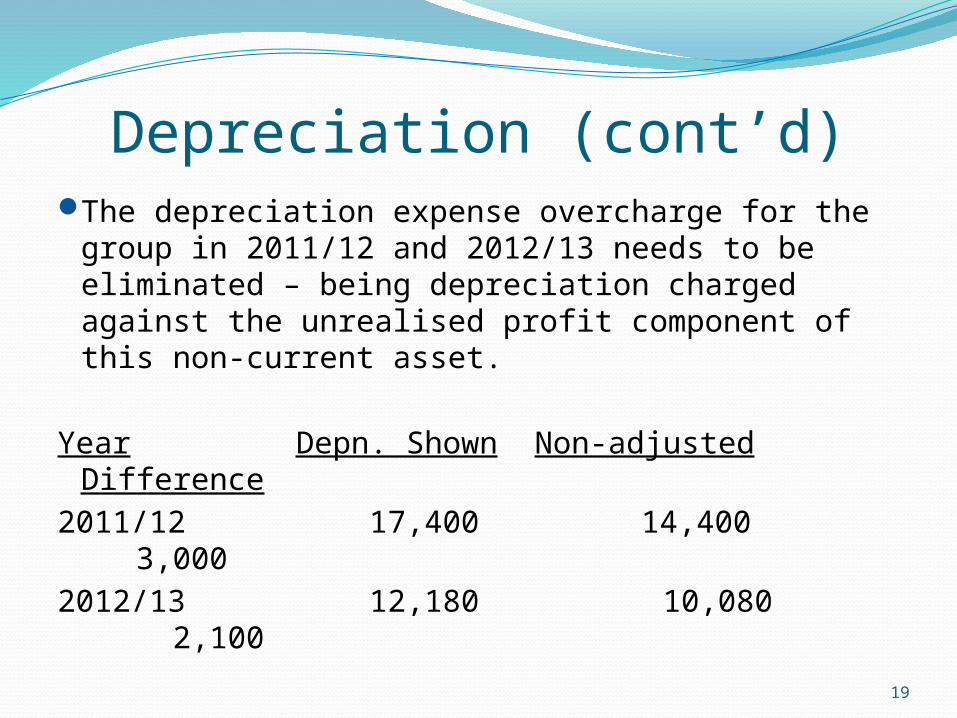

Depreciation (cont’d)The depreciation expense overcharge for the

group in 2011/12 and 2012/13 needs to be eliminated – being depreciation charged against the unrealised profit component of this non-current asset.

Year Depn. Shown Non-adjusted Difference

2011/12 17,400 14,400 3,000

2012/13 12,180 10,080 2,100

20

Depreciation (cont’d)

Alternatively, based on the unrealised profit component of $10,000 the overcharge is:2012 10,000 @ 30% DV = 3,0002013 7,000 @ 30% DV = 2,100

Consolidated Journal entry in 2013:Dr Accum. depn. 5,100

Cr Opening Ret’d Earnings 3,000Cr Depn. expense 2,100

Depreciation adjustment for current and prior periods

21

Steps in Consolidation - 5Step 5

Eliminate inter-company dividends paid/received, otherwise the holding company is effectively paying dividends to itself!

Only dividends paid externally should be shown in consolidated financial statements