24

Managerial Accounting and Cost Concepts Chapter 2 McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

| Date post: | 24-Oct-2015 |

| Category: |

Documents |

| Upload: | iamruzehl-villaver |

| View: | 33 times |

| Download: | 0 times |

Managerial Accounting and Cost Concepts

Chapter 2

McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Planning

Identifyalternatives.

Select alternative that does the best job of furtheringorganization’s objectives.

Develop budgets to guideprogress toward theselected alternative.

2-2

Directing and Motivating

Directing and motivating involves managing day-to-day activities to keep the organization running smoothly. Employee work assignments. Routine problem solving. Conflict resolution. Effective communications.

2-3

Controlling

The control function ensuresthat plans are being followed.

Feedback in the form of performance reportsthat compare actual results with the budgetare an essential part of the control function.

2-4

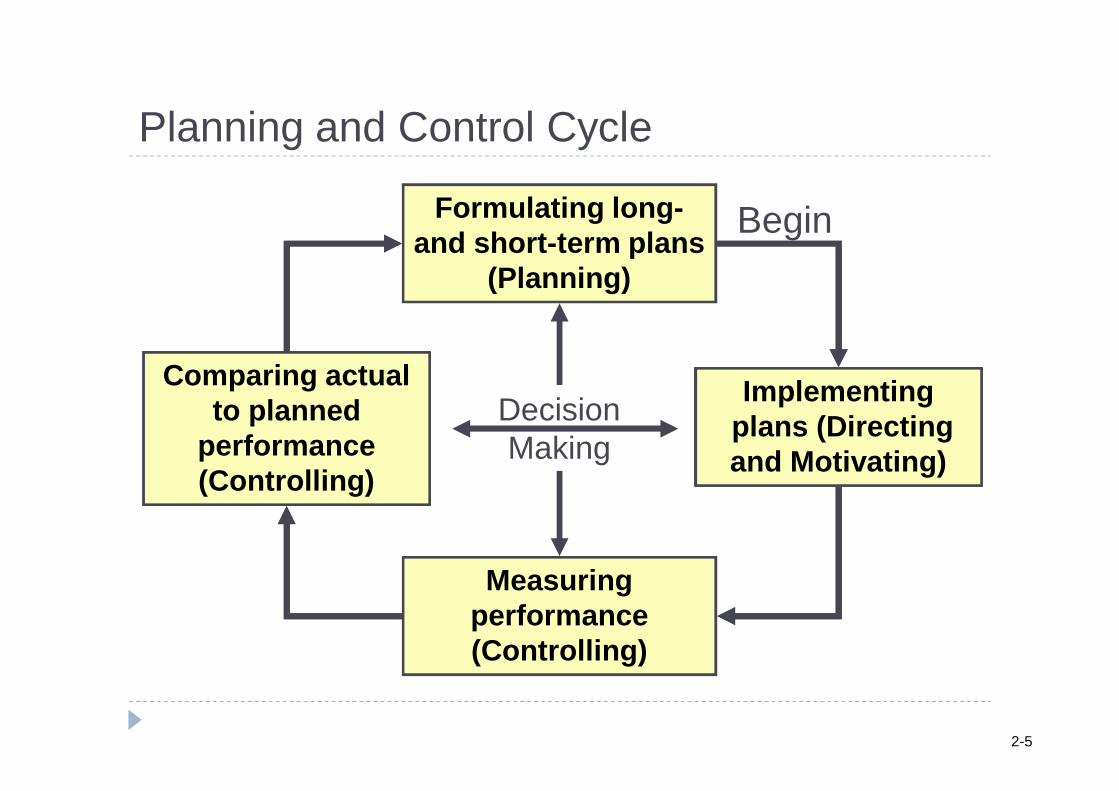

Planning and Control Cycle

DecisionMaking

Formulating long-and short-term plans

(Planning)

Measuringperformance (Controlling)

Implementingplans (Directing and Motivating)

Comparing actualto planned

performance (Controlling)

Begin

2-5

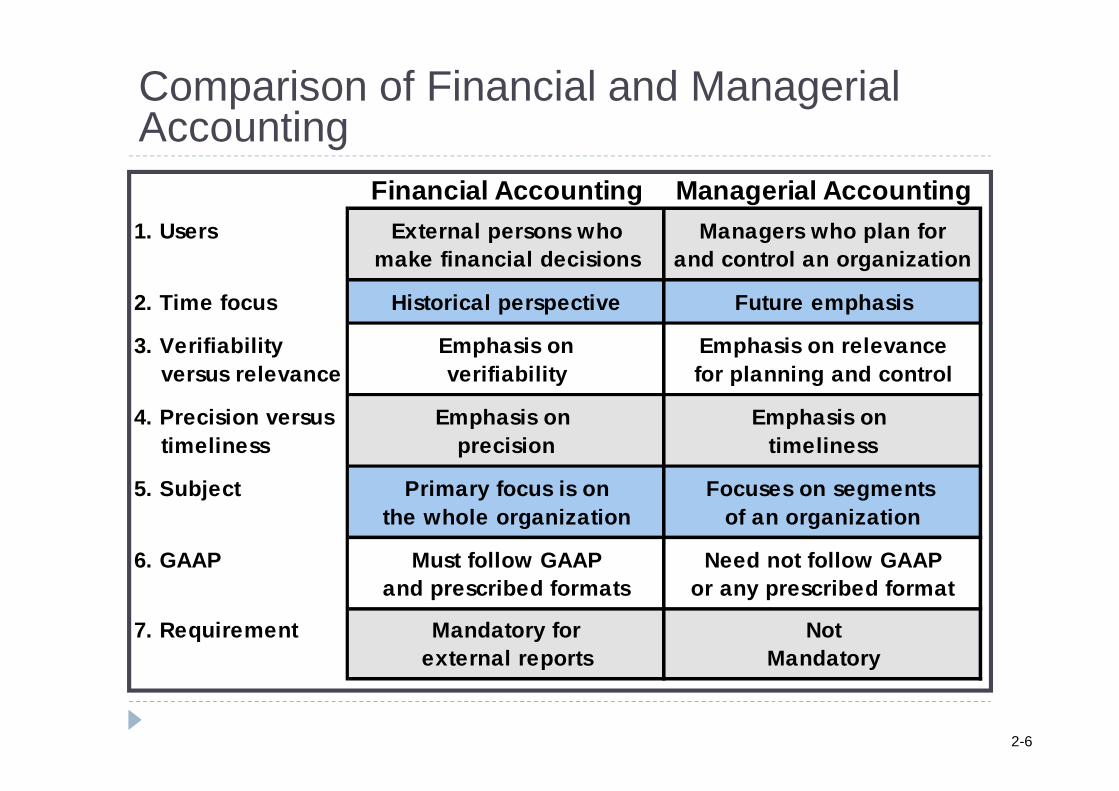

Comparison of Financial and Managerial Accounting

Financial Accounting Managerial Accounting1. Users External persons who Managers who plan for

make financial decisions and control an organization

2. Time focus Historical perspective Future emphasis

3. Verifiability Emphasis on Emphasis on relevance versus relevance verifiability for planning and control

4. Precision versus Emphasis on Emphasis on timeliness precision timeliness

5. Subject Primary focus is on Focuses on segments the whole organization of an organization

6. GAAP Must follow GAAP Need not follow GAAPand prescribed formats or any prescribed format

7. Requirement Mandatory for Notexternal reports Mandatory

2-6

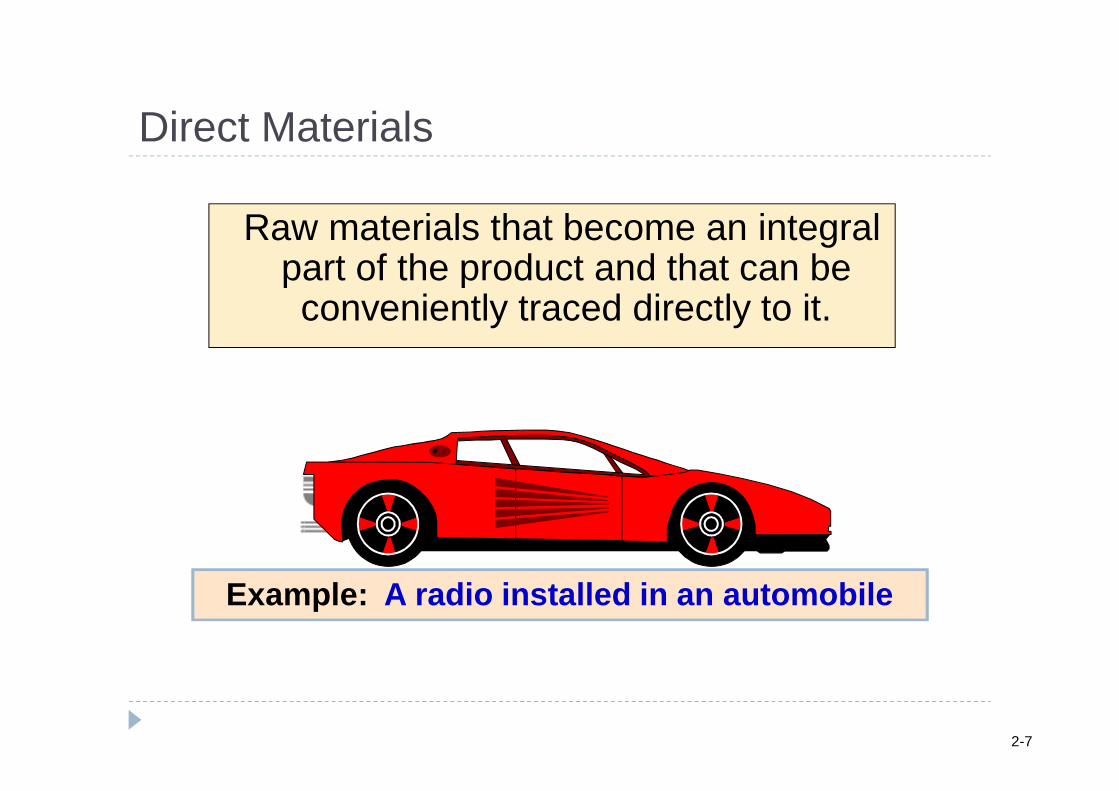

Direct Materials

Raw materials that become an integral part of the product and that can be conveniently traced directly to it.

Example: A radio installed in an automobile

2-7

Direct Labor

Those labor costs that can be easily traced to individual units of product.

Example: Wages paid to automobile assembly workers

2-8

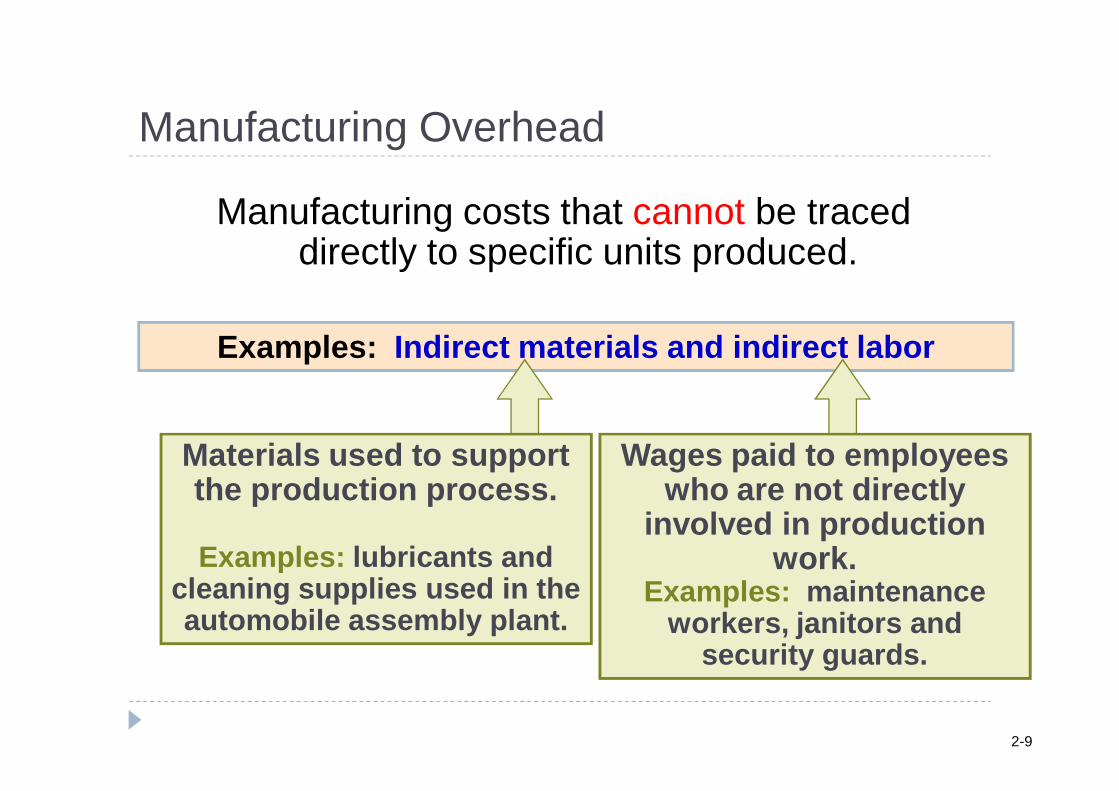

Manufacturing costs that cannot be traced directly to specific units produced.

Manufacturing Overhead

Examples: Indirect materials and indirect labor

Wages paid to employees who are not directly

involved in production work.

Examples: maintenance workers, janitors and

security guards.

Materials used to support the production process.

Examples: lubricants and cleaning supplies used in the automobile assembly plant.

2-9

Nonmanufacturing Costs

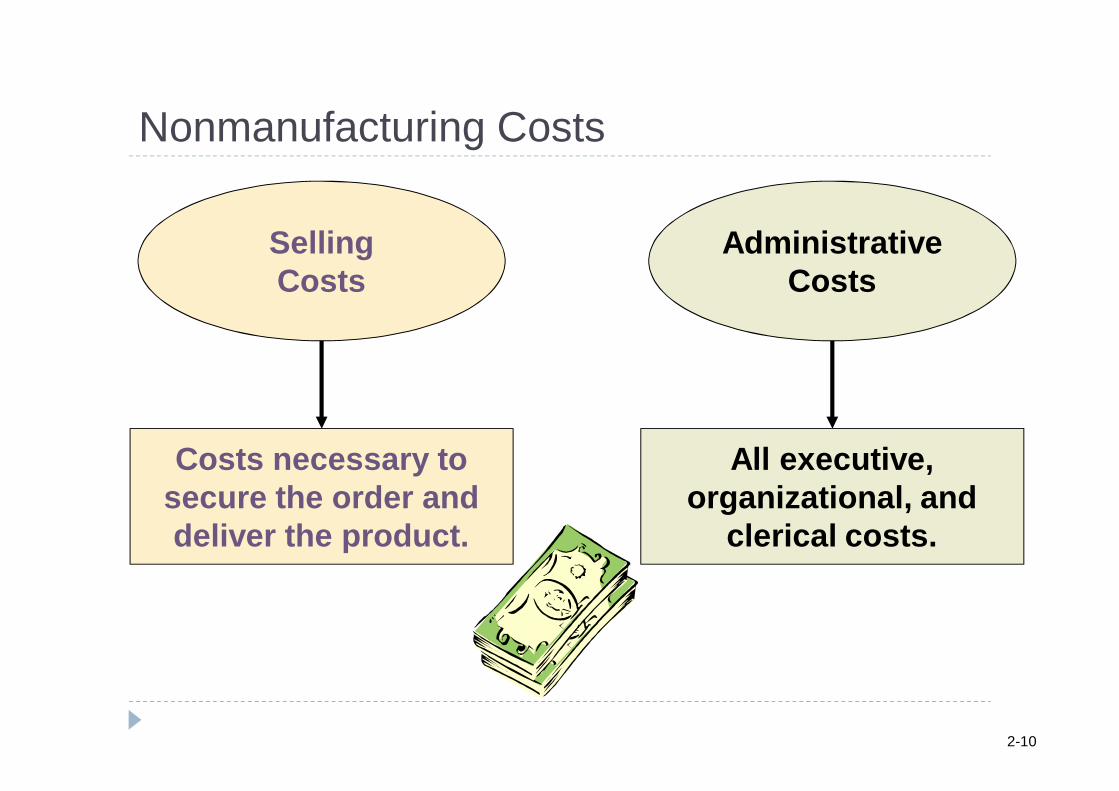

Selling Costs

Costs necessary to secure the order and deliver the product.

Administrative Costs

All executive, organizational, and

clerical costs.

2-10

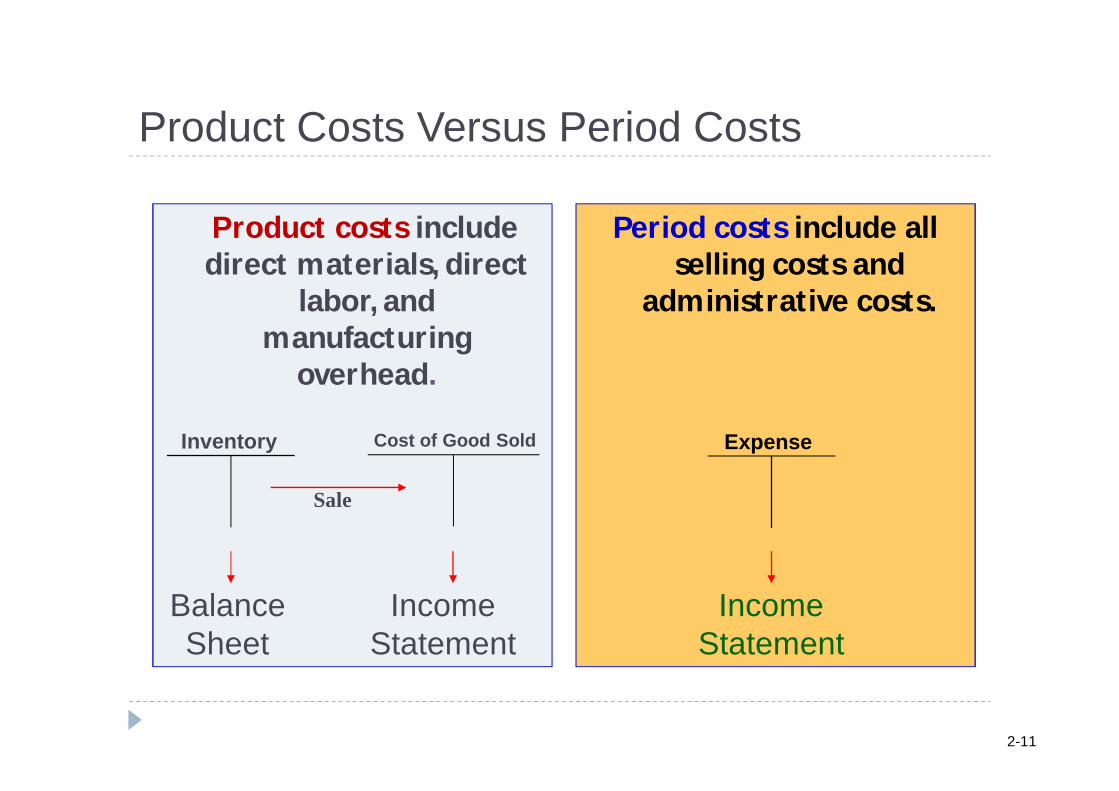

Product Costs Versus Period Costs

Product costs include direct materials, direct

labor, and manufacturing

overhead.

Period costs include all selling costs and

administrative costs.

Inventory Cost of Good Sold

BalanceSheet

IncomeStatement

Sale

Expense

IncomeStatement

2-11

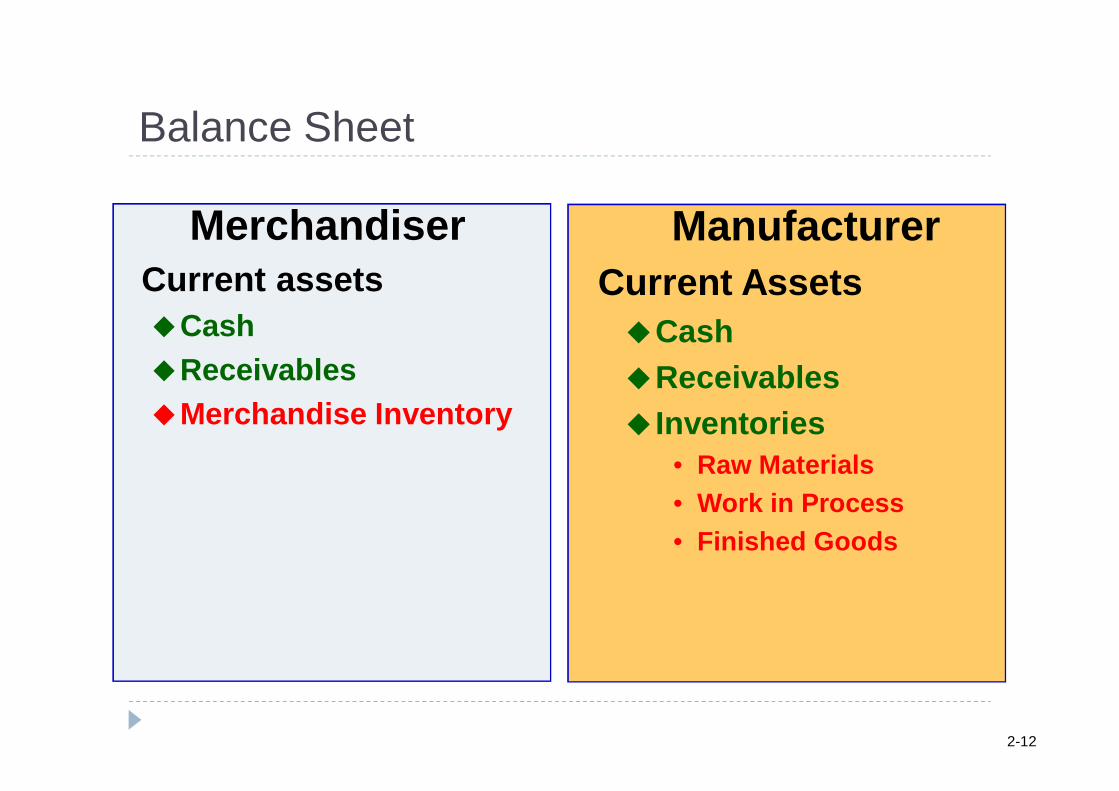

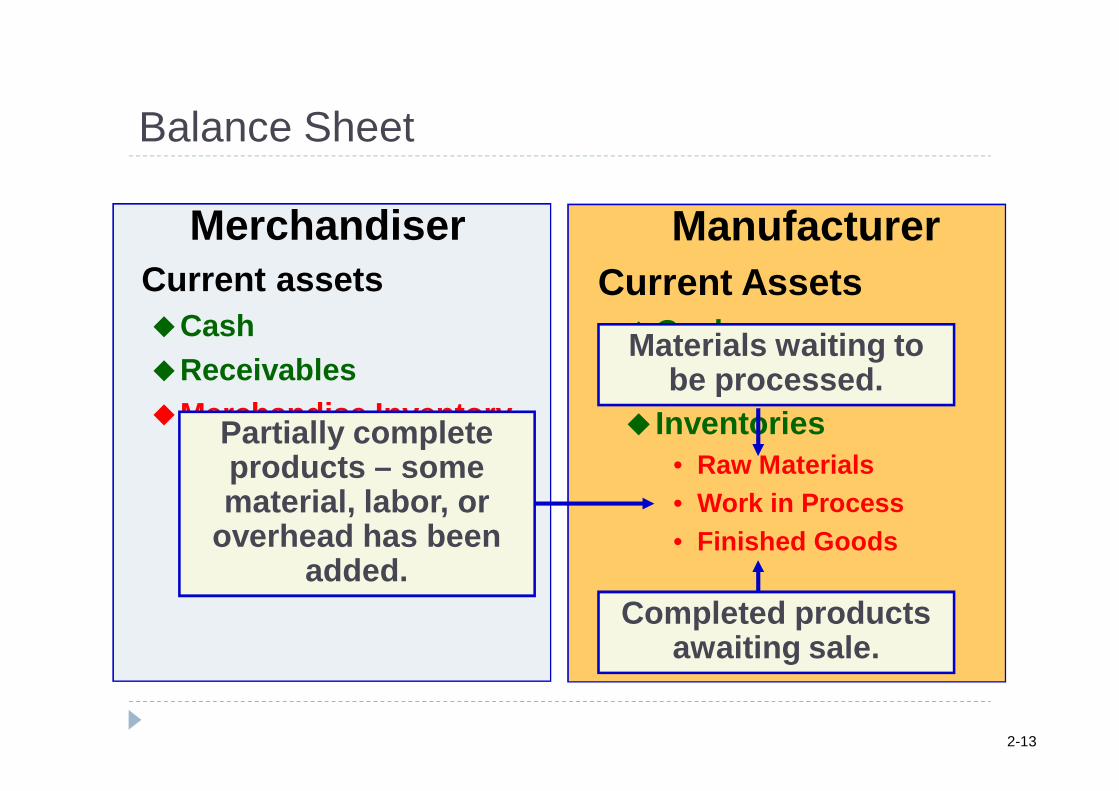

Balance Sheet

MerchandiserCurrent assetsCashReceivablesMerchandise Inventory

ManufacturerCurrent AssetsCashReceivables Inventories

• Raw Materials• Work in Process• Finished Goods

2-12

MerchandiserCurrent assetsCashReceivablesMerchandise Inventory

ManufacturerCurrent AssetsCashReceivables Inventories

• Raw Materials• Work in Process• Finished Goods

Balance Sheet

Partially complete products – some material, labor, or

overhead has been added.

Completed products awaiting sale.

Materials waiting to be processed.

2-13

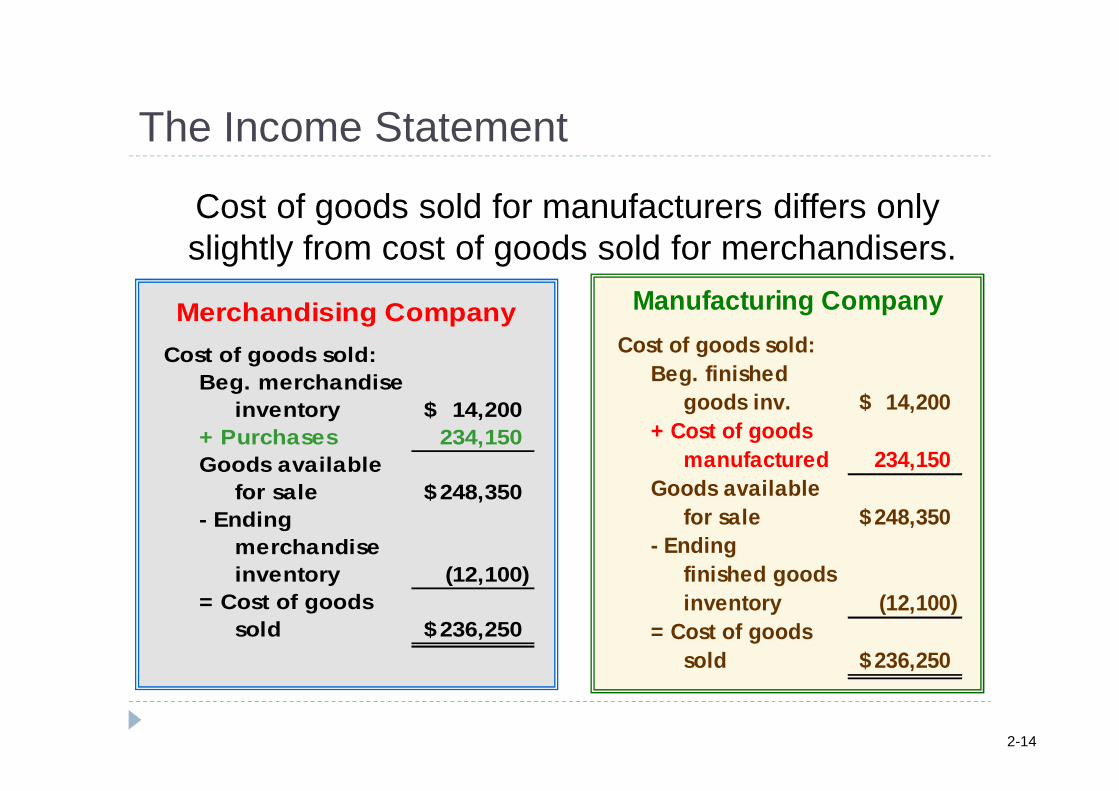

The Income Statement

Cost of goods sold for manufacturers differs only slightly from cost of goods sold for merchandisers.

Manufacturing CompanyCost of goods sold: Beg. finished goods inv. 14,200$ + Cost of goods manufactured 234,150 Goods available for sale 248,350$ - Ending finished goods inventory (12,100) = Cost of goods sold 236,250$

Merchandising CompanyCost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goods sold 236,250$

2-14

Basic Equation for Inventory Accounts

Beginningbalance

Additionsto inventory++ == Ending

balance

Withdrawalsfrom

inventory++

2-15

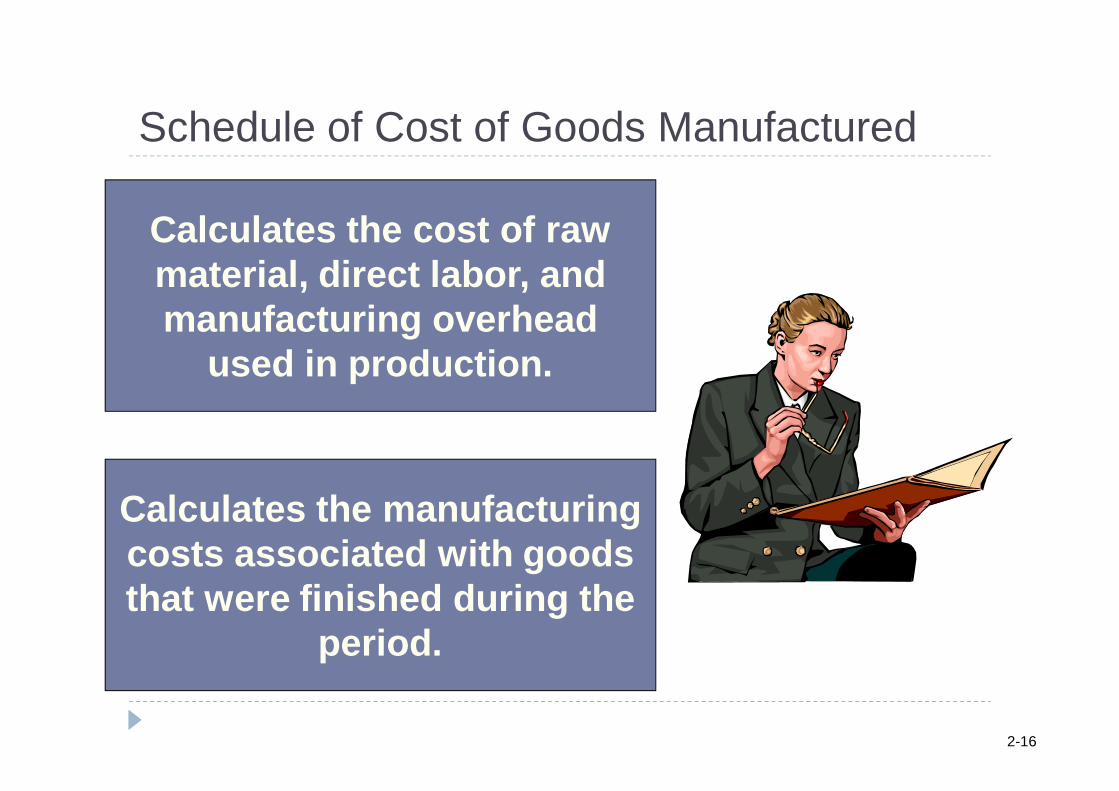

Schedule of Cost of Goods Manufactured

Calculates the cost of raw material, direct labor, and manufacturing overhead

used in production.

Calculates the manufacturing costs associated with goods that were finished during the

period.

2-16

Manufacturing Cost Flows

FinishedGoods

Cost of GoodsSold

Selling andAdministrative

Period CostsSelling andAdministrative

ManufacturingOverhead

Work inProcess

Direct Labor

Balance SheetCosts Inventories

Income StatementExpensesMaterial Purchases Raw Materials

2-17

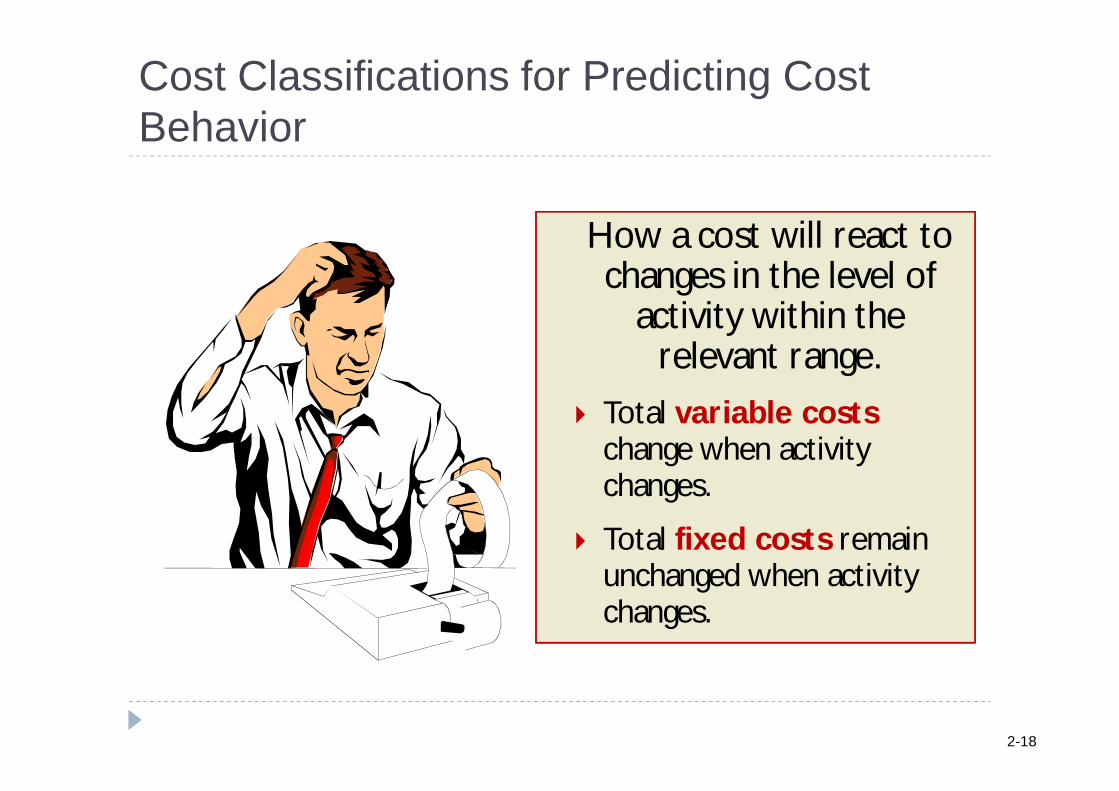

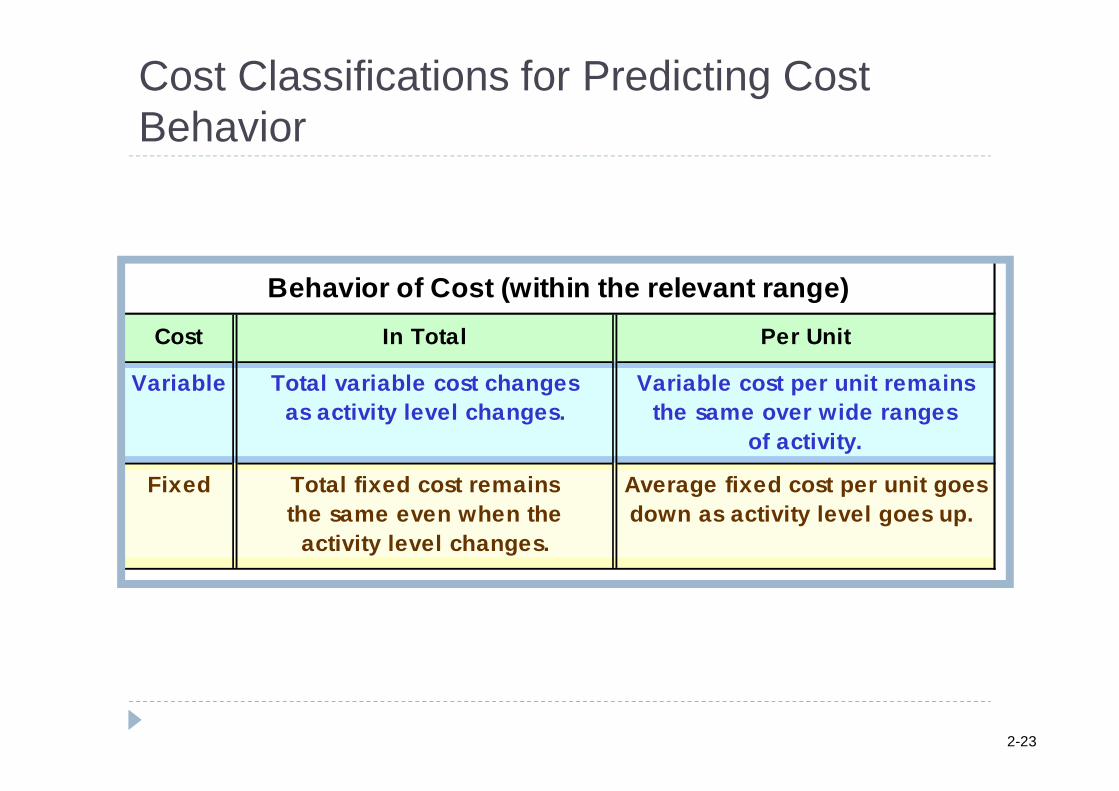

Cost Classifications for Predicting Cost Behavior

How a cost will react to How a cost will react to changes in the level of

activity within the relevant range.

Total variable costschange when activity changes.

Total fixed costs remain unchanged when activity changes.

2-18

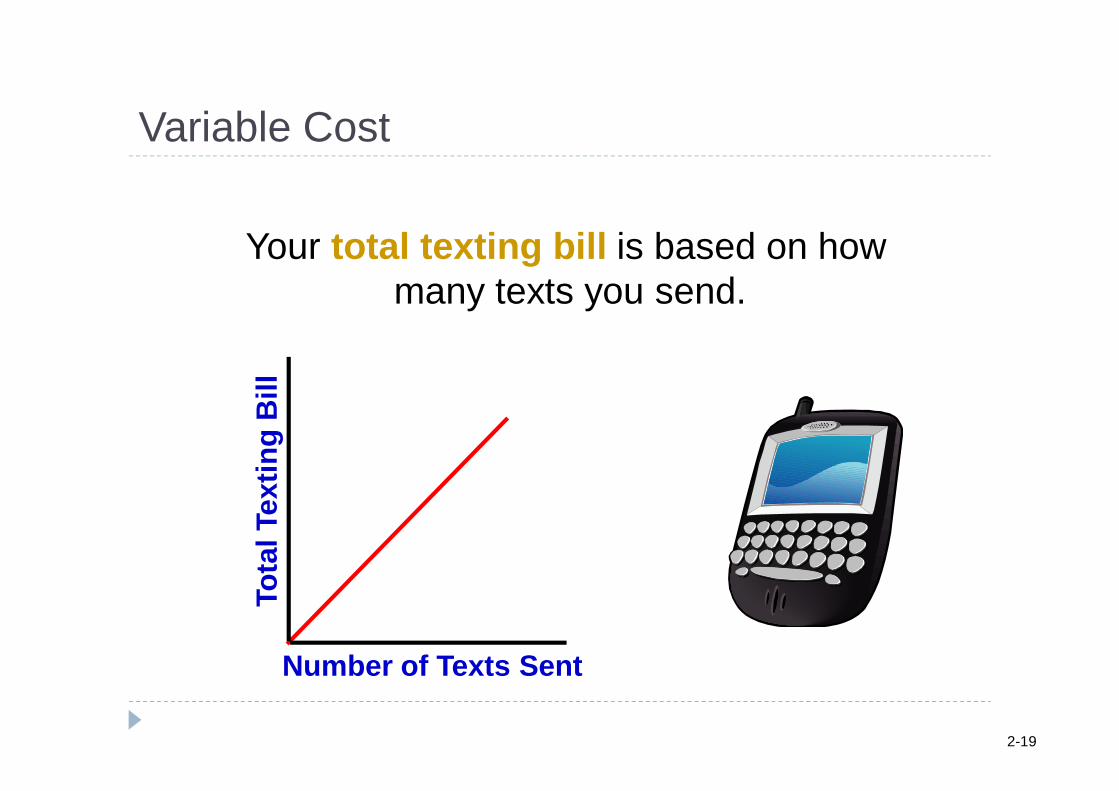

Variable Cost

Your total texting bill is based on how many texts you send.

Number of Texts Sent

Tota

l Tex

ting

Bill

2-19

Variable Cost Per Unit

Number of Texts SentC

ost P

er T

ext S

ent

The cost per text sent is constant at 5 cents per text.

2-20

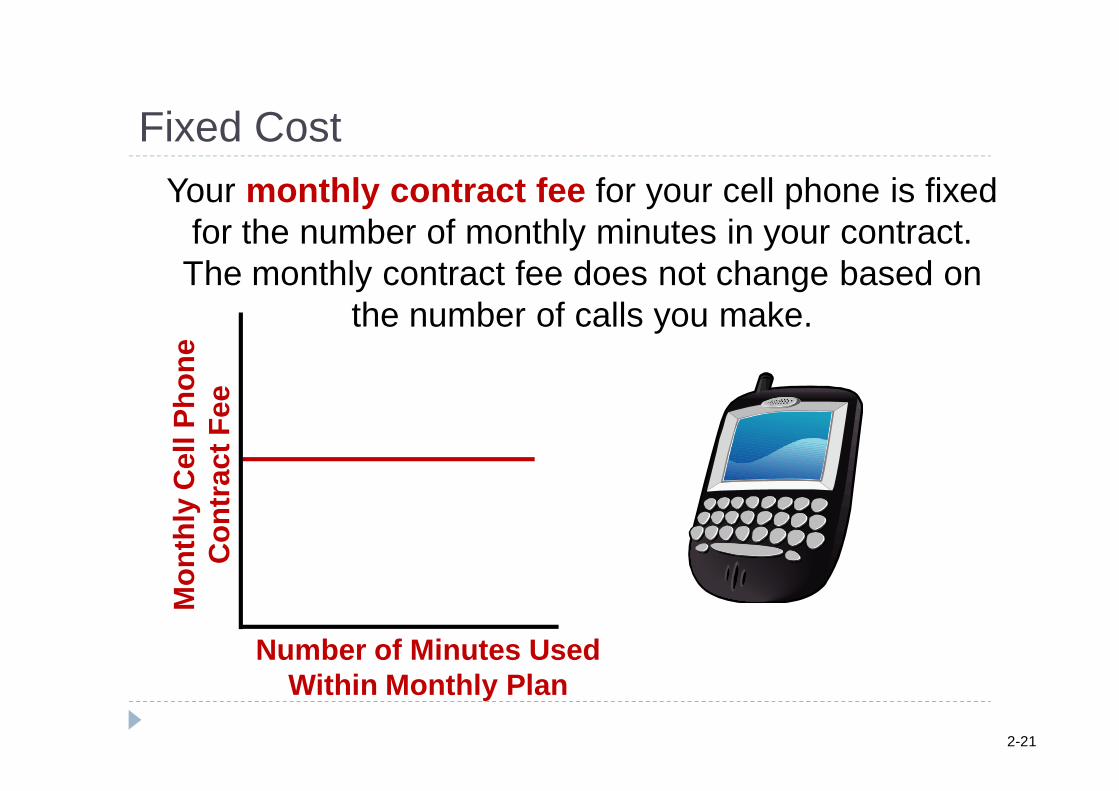

Fixed CostYour monthly contract fee for your cell phone is fixed

for the number of monthly minutes in your contract. The monthly contract fee does not change based on

the number of calls you make.

Number of Minutes UsedWithin Monthly Plan

Mon

thly

Cel

l Pho

ne

Con

trac

t Fee

2-21

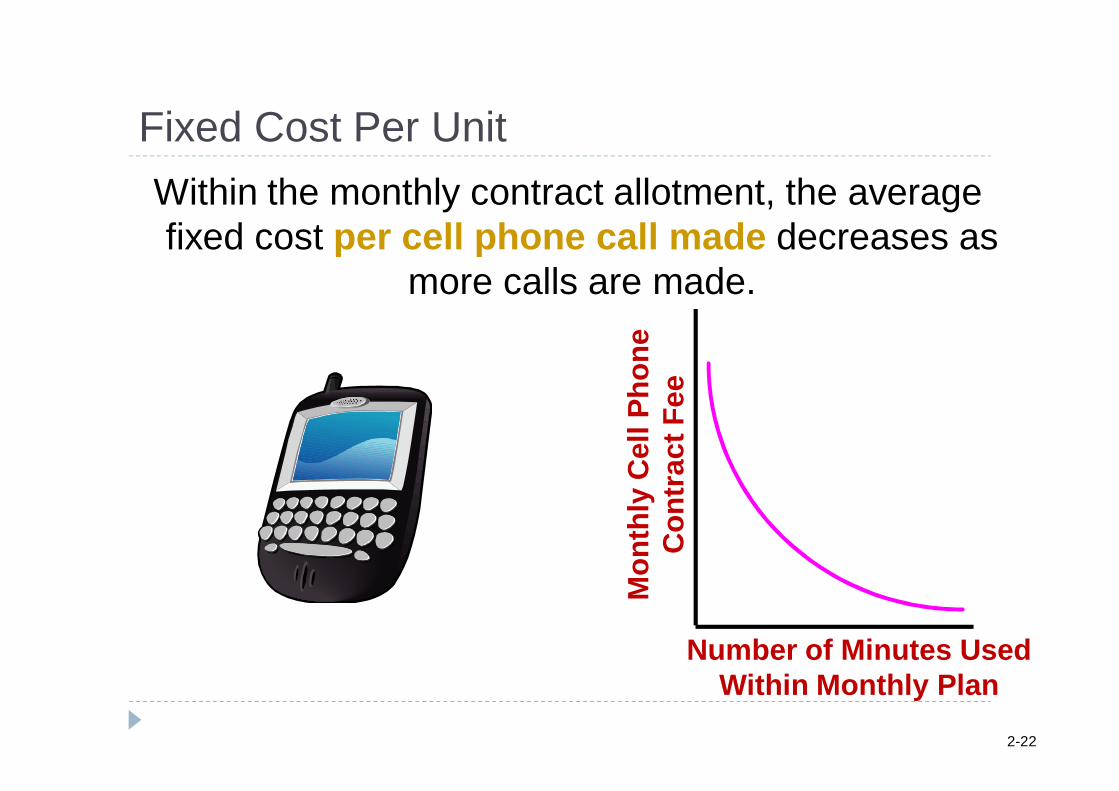

Fixed Cost Per Unit

Number of Minutes UsedWithin Monthly Plan

Mon

thly

Cel

l Pho

ne

Con

trac

t Fee

Within the monthly contract allotment, the average fixed cost per cell phone call made decreases as

more calls are made.

2-22

Cost Classifications for Predicting Cost Behavior

Behavior of Cost (within the relevant range)Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remainsas activity level changes. the same over wide ranges

of activity.

Fixed Total fixed cost remains Average fixed cost per unit goesthe same even when the down as activity level goes up.

activity level changes.

2-23

End of Chapter 2

2-24

![Lecture_truss [Compatibility Mode]](https://static.documents.pub/doc/80x56/577cd8441a28ab9e78a0d235/lecturetruss-compatibility-mode.jpg)

![Dynamics_Lecture8 [Compatibility Mode]](https://static.documents.pub/doc/80x56/577d2aea1a28ab4e1eaa7060/dynamicslecture8-compatibility-mode.jpg)

![Chap11_Sec4 [Compatibility Mode]](https://static.documents.pub/doc/80x56/5695d1bc1a28ab9b0297b7ae/chap11sec4-compatibility-mode.jpg)

![Lec_08 [Compatibility Mode]](https://static.documents.pub/doc/80x56/577d2f7d1a28ab4e1eb1dd1f/lec08-compatibility-mode.jpg)

![DIC_IMELS [Compatibility Mode]](https://static.documents.pub/doc/80x56/5695d0c61a28ab9b0293d366/dicimels-compatibility-mode.jpg)

![VALVES [Compatibility Mode]](https://static.documents.pub/doc/80x56/55cf9041550346703ba45bf6/valves-compatibility-mode.jpg)

![Colour [Compatibility Mode]](https://static.documents.pub/doc/80x56/55cf8c685503462b138c1b8d/colour-compatibility-mode.jpg)

![Ishikawa213 [compatibility mode]](https://static.documents.pub/doc/80x56/54bef6e24a7959ff458b4640/ishikawa213-compatibility-mode.jpg)

![Stromingsleer_college4 [Compatibility Mode]](https://static.documents.pub/doc/80x56/586a1f581a28ab39568c1718/stromingsleercollege4-compatibility-mode.jpg)

![Chap12_Sec3 [Compatibility Mode]](https://static.documents.pub/doc/80x56/5695d1bd1a28ab9b0297b830/chap12sec3-compatibility-mode.jpg)

![Astronomy [Compatibility Mode]](https://static.documents.pub/doc/80x56/558422bed8b42a785e8b460a/astronomy-compatibility-mode.jpg)

![Organizing [Compatibility Mode]](https://static.documents.pub/doc/80x56/553d1238550346e2498b4c66/organizing-compatibility-mode.jpg)

![SOSIOLINGUISTIK [Compatibility Mode]](https://static.documents.pub/doc/80x56/586cd4021a28abe2128b90a3/sosiolinguistik-compatibility-mode.jpg)

![Dvt.warda [compatibility mode]](https://static.documents.pub/doc/80x56/554b2485b4c905da088b45bb/dvtwarda-compatibility-mode.jpg)

![Swansea [compatibility mode]](https://static.documents.pub/doc/80x56/5594068d1a28ab74288b45e7/swansea-compatibility-mode.jpg)

![Reciprocatingcom [Compatibility Mode]](https://static.documents.pub/doc/80x56/55cf8fca550346703b9fe10b/reciprocatingcom-compatibility-mode.jpg)

![BIOM2012_Advanced_Neuromotor_NOAKES_2010 [Compatibility Mode]](https://static.documents.pub/doc/80x56/577d2be51a28ab4e1eab6809/biom2012advancedneuromotornoakes2010-compatibility-mode.jpg)

![Aspect [Compatibility Mode]](https://static.documents.pub/doc/80x56/577ce6661a28abf10392bc30/aspect-compatibility-mode.jpg)