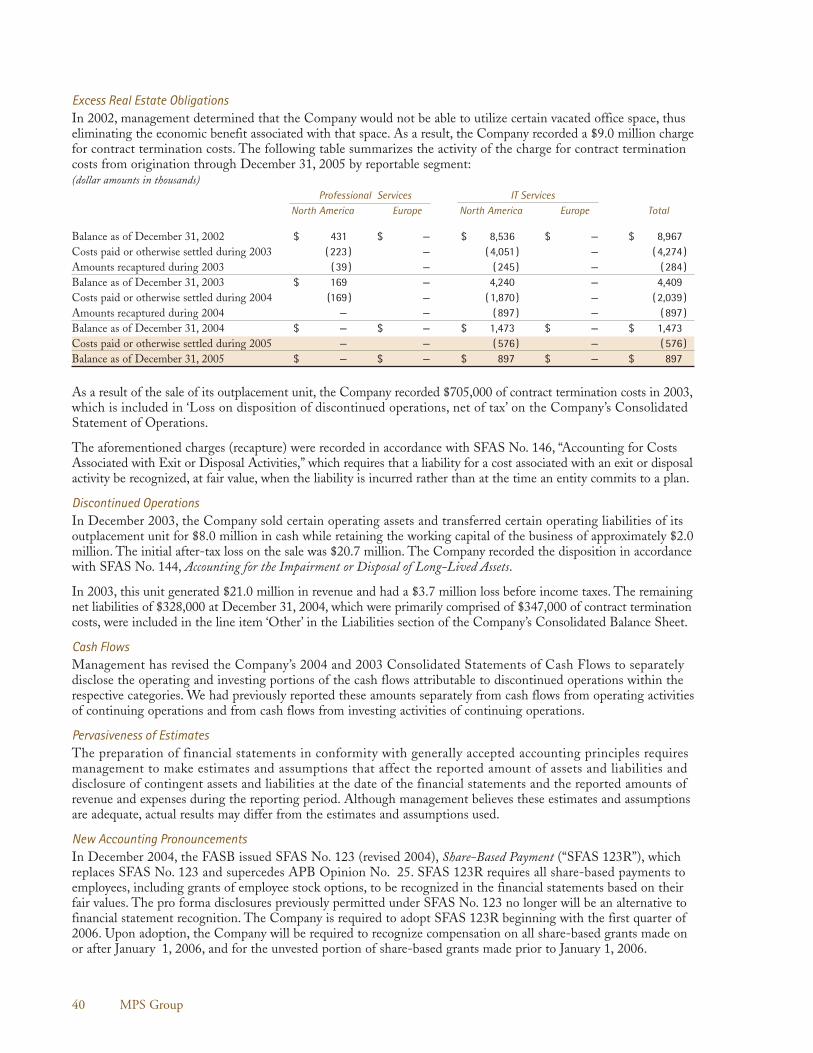

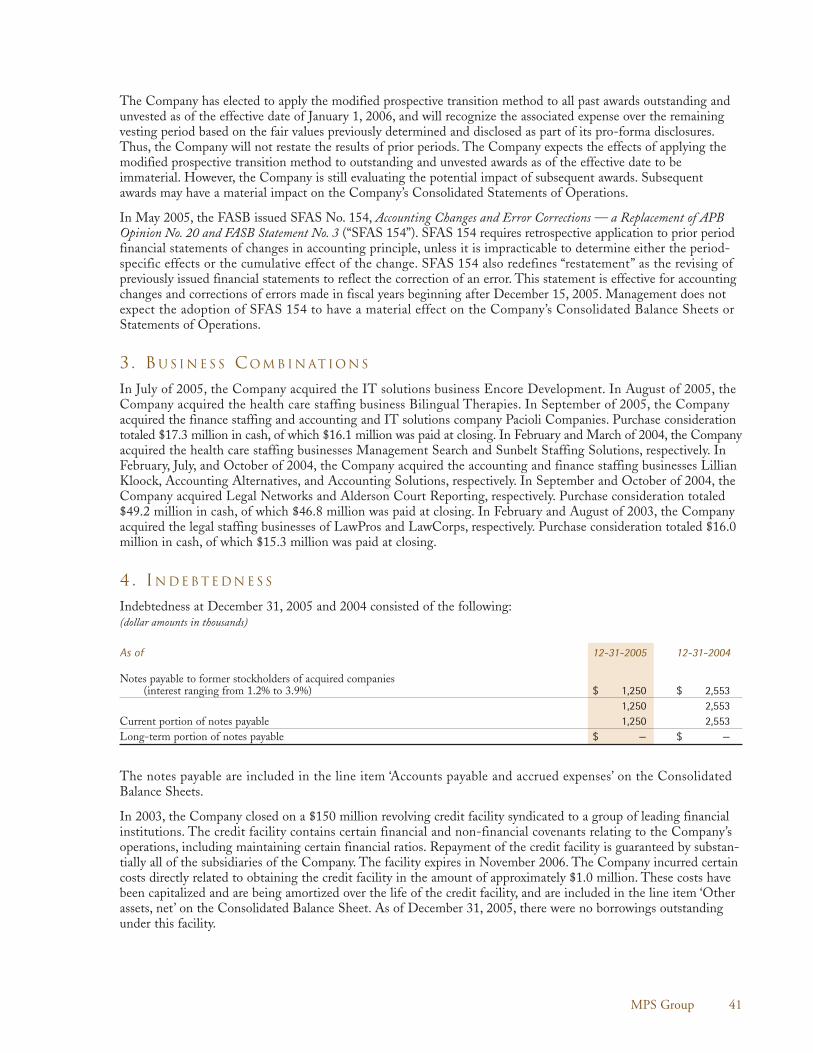

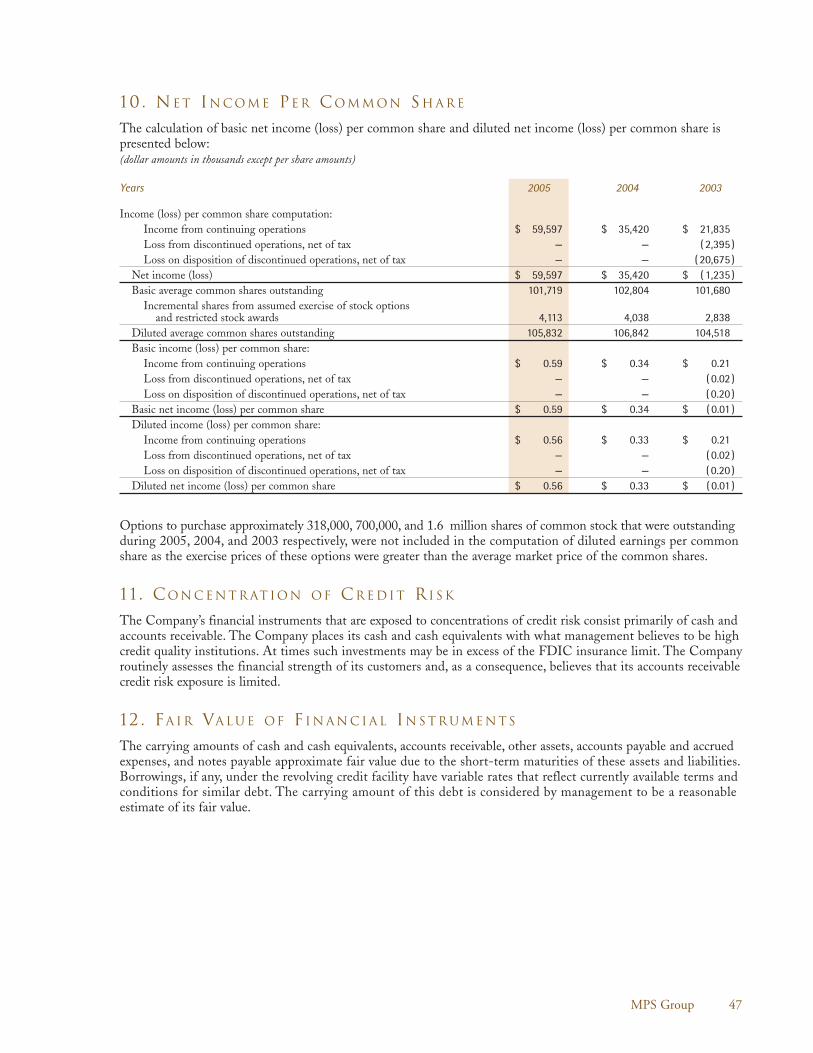

56

2005 Annual Report

| Date post: | 14-Jan-2017 |

| Category: |

Documents |

| Upload: | mark-stevens |

| View: | 43 times |

| Download: | 0 times |

2005 Annual Report

TA B L E OF CO N T E N TS

1 Financial Highlights

2 Letter to Shareholders

6 Professional Services Division

8 Information Technology Services Division

10 Revenue Mix

11 Discussion of the Company

18 Selected Financial Data

19 Management’s Discussion and Analysis of

Financial Condition and Results of Operations

27 Quantitative and Qualitative DisclosuresAbout Market Risk

28 Financial Statements and Supplementary Data

51 Reconciliation of Non-GAAP Financial

Measure to GAAP Financial Measure

52 Common Stock Data and Other Information

53 Board of Directors, MPS Group Executives,and Business Unit Presidents

OU R BU S I N E S S

MPS Group, Inc. is a leading provider of

staffing, consulting, and solutions in the

disciplines of information technology,

accounting and finance, law, engineering,

and health care. MPS Group delivers its

services to businesses and government

entities in virtually all industries

throughout the United States, Canada,

the United Kingdom, and Europe.

A Fortune 1000 company with

headquarters in Jacksonville, Florida,

MPS Group trades on the New York

Stock Exchange (NYSE:MPS).

1MPS Group

2005 F I N A N C I A L HIG H L IG H TS

(dollar amounts in thousands except per share amounts)

Year 2005 2004 2003

Revenue $ 1,684,699 $ 1,426,842 $ 1,096,030

Cost of revenue 1,242,331 1,066,055 808,890

Gross profit 442,368 360,787 287,140

Operating expenses 355,382 308,654 251,339

Operating income $ 86,986 $ 52,133 $ 35,801

Income from continuing operations $ 59,597 $ 35,420 $ 21,835

Diluted income per common share from continuing operations (EPS) $ 0.56 $ 0.33 $ 0.21

RE V E N U E EPSEBITDA

EBITDA is a non-GAAP financial measure representing earnings before interest, taxes, depreciation, and amortization. See page 51 for a schedulereconciling EBITDA used above and in the letter to shareholders to the most comparable GAAP financial measure.

OPERATING MARGINGR O S S M A R G I N

2 MPS Group

OOne year ago I wrote to you about our plans to grow, strengthen, and diversify our business.

Thanks to the exceptional efforts of our consultants, staff, and leadership team, in 2005 we made

outstanding progress toward these goals.

Timothy D. Payne, President and Chief Executive Officer

TO OU R SH A R E HOL D E R S :

2005 YE A R I N RE V I E W

Total company revenues increased 18% to $1.685 billion for the

year. Revenues from our professional services businesses—which

provide staffing and recruiting services in the disciplines of accounting

and finance, law, engineering, and health care—rose 26%. At the

same time, our information technology (IT) businesses, which

provide IT staffing, IT solutions, and work force solutions, posted

an 11% increase in revenues as we balanced growth with more

selectivity in our client relationships.

Earnings growth was very strong in 2005 with diluted net income

per common share of $0.56, up 70% from 2004. EBITDA grew to

$102 million, an increase of 50% versus the prior year. Operating

income surpassed $86 million, up 67% compared with 2004. Our

ability to grow the bottom line faster than the top demonstrates

our strong operating leverage.

2005 AT A GL A N C E

Revenue GrossProfit

OperatingIncome

3MPS Group

Our balance sheet and overall financial position continued

to strengthen as well in 2005. For the year, we generated

more than $90 million in cash flow from operations. At

the close of 2005, we had $143 million in cash on hand

with no long-term debt and an untapped credit facility

of $150 million. Our financial strength should enable us

to continue to execute our growth strategy.

Overall, we were very pleased with our financial

performance in 2005.

BU S I N E S S UN I T HIG H L IG H TS

MPS Group is composed of nine branded business units

focused on delivering very specialized services and

solutions to our clients. In 2005, the business units

focused on increasing revenues while also improving

gross and operating margins. This is a challenging task

because larger volume client contracts are generally

accompanied by lower pricing. Across the board, we

were pleased with how our business units responded to

the challenge. For financial reporting purposes, these

business units are grouped into four segments: North

American Information Technology (IT) Services, European

IT Services, North American Professional Services, and

European Professional Services. Revenues were up in

each of our four reporting segments in 2005. Margins

improved in all segments except for our European IT

Services segment, which showed encouraging margin

improvement during the second half of the year. The

chart on this page illustrates the performances of our

business units in 2005.

PO S I T IO N I N G T H E CO M PA N Y

Over the past five years, we have worked to position the

company for optimum performance under varying

economic and hiring conditions. To do this, we knew

we needed to generate a greater portion of our revenue

from our professional businesses. We also knew that we

needed to build a larger market share in certain high-

growth professional staffing markets that are driven by

skill shortages and increasing client acceptance. Finally, it

was important for us to take action toward becoming a

truly global company so we would not be too reliant on

any one country’s economy. Today, MPS Group is a very

different—and stronger—company than it was five years

ago. Consider:

Diversification — Five years ago, MPS Group was often

viewed as an IT services company, with over 60% of our

revenue derived from IT services in 2000. Currently, our

IT businesses are strong and consistent profit makers;

however, spending on IT services tends to follow the

capital investment cycle, which can turn downward during

periods of economic weakness. We decided to change

our business mix so that IT services would generate a

lower percentage of our overall revenue, making us less

vulnerable to changes in economic conditions. We set out

to do this by investing in the less cyclical professional

staffing disciplines of accounting, health care, and legal.

Today, IT services represent 45% of our revenues with

professional services making up 55% of our revenues.

We anticipate that professional staffing revenues will

comprise 60% of revenues by the end of 2006. Today,

we are a diversified professional and IT services firm that

is better prepared to face varying economic conditions.

2005 BUSINESS UNIT REVENUE GROWTH BY SEGMENT

North American IT Services 11%

European IT Services 9%

North American Professional Services 25%

European Professional Services 26%

4 MPS Group

Acceptance — The market for staffing specialties tends

to go through several clearly identifiable phases. The key

to maximizing growth is to be properly positioned when

clients enter the “acceptance” phase, which means they

begin using temporary professionals for roles previously

confined to full-time workers. Ten years ago, it was fairly

uncommon for law firms and corporate legal departments

to use temporary lawyers and paralegals. Five years ago, we

believed that acceptance of temporary legal professionals

would soon be on the rise, so we made investments in

this area of our business. Since 2002, our legal staffing

business has more than tripled, and we anticipate 2006

legal revenues of over $150 million. We think other areas

are ripe for increasing client acceptance, such as pharmacy,

school therapy, and marketing. We will continue to seek out

new staffing markets that are entering the acceptance phase.

Skill Shortages — Demand for specialty staffing services

is frequently driven by skill shortages, which often can be

attributed to a variety of factors. These factors include

declining graduation rates, an aging work force, and

changes in government regulation. The first two factors

have combined to create both acute and long-term

shortages of both health care professionals and

accountants. Adding to these shortages are increases in

government regulation. For example, states such as

California have passed legislation mandating a lower

nurse-to-patient ratio. And in the wake of widespread

accounting scandals, the Sarbanes-Oxley Act stoked

demand for accountants that already were in short

supply. Over the past several years, we have focused

on building our health care and accounting staffing

businesses to meet what we believe will be a period of

long-term strong demand. We entered the health care

staffing market in 2002 and have rapidly grown this

business, with revenues approaching $100 million

expected in 2006. We also made investments to grow

our accounting staffing business in both North America

and Europe. We anticipate that revenues from our global

accounting staffing operations will exceed $500 million

in 2006. We will continue to seek growth opportunities

driven by professional skill shortages.

International — Five years ago, only $429 million of

our revenues were derived from business outside the

United States. While the United States is perhaps the

world’s most vibrant market for specialty staffing services,

we saw the opportunity to enhance our growth potential

through international expansion. As a result, in 2005 we

generated revenues of $637 million from outside the

United States, an increase of 48% from 2000. We now

operate in 10 countries: Belgium, Canada, England,

Germany, Hungary, Luxembourg, Netherlands, Poland,

Scotland, and the United States. While our presence is

still small in many of these countries, we now have new

sources of growth and greater geographic diversity. We will

continue to focus on growing our current international

business while expanding into countries with favorable

conditions for growth.

MPS Group now is more diverse, better positioned in

key growth markets, and better positioned for

international expansion.

FU T U R E OF SPE C I A LT Y STA F F I N G

While we are pleased with how we have positioned the

company, our future growth and prosperity will depend

on the overall strength of the markets for specialty

staffing. We believe demographics, liberalization of labor

laws, and a growing utilization of contingent labor all

add up to a bright future for our industry.

Demographics — By 2008, the so-called “baby boomers”

will begin to retire from the work force. This highly

trained, well-educated group will be replaced by a much

smaller generation, leading many experts to believe that a

“skilled-worker gap” will materialize. It has been estimated

that by 2020 the United States alone may face a shortfall

of 14 million skilled workers, and many other countries

are facing similar potential shortfalls. Should this scenario

materialize, long-term demand for knowledge workers

will be strong, particularly in highly skilled professions

such as health care, accounting, information technology,

and engineering.

5MPS Group

Labor Practices — Unlike the United States, Canada,

and the United Kingdom, many countries traditionally

have had labor laws and practices that discourage the

use of contingent labor. For example, the utilization of

contingent labor in Germany is only 1%, compared with

3% in the United Kingdom. Many countries, particularly

in Europe, now are examining their labor laws and

considering liberalization policies that could lead to

greater use of professional contingent labor. We believe

that if this trend toward liberalization of labor laws and

practices continues, it will help create new opportunities

for expansion in Europe and beyond.

Contingent Labor Growth — In countries that already

have flexible labor environments, utilization of contingent

labor is on the rise for different reasons. From the employer

standpoint, contingent workers allow for just-in-time

delivery of critical skill sets and allow for variable staff

costs that can fluctuate with business conditions. From

the employee standpoint, a growing number of profes-

sionals prefer working on a contingent basis due to

family requirements, the need for a flexible work schedule,

or simply the desire for variety. In 1975, the percentage

of temporary workers within the overall United States

work force was less than one-half of 1%. Today, that

percentage is approaching an all-time high of about 2%.

The United States Bureau of Labor Statistics estimates

that 1.8 million contingent worker positions will be

added to the U.S. economy between 2002 and 2012.

This trend toward increasing utilization of contingent

labor is a positive development for MPS Group.

We believe these three trends create a favorable

environment for specialty staffing providers such as

MPS Group—and will do so for many years to come.

SUM M A RY

We anticipate another strong performance for MPS Group

in 2006. Our financial position is sound, with no long-

term debt and $143 million in cash reserves. The growth

and performance of our branded business units in 2005

was attributable to the talents, creativity, and drive of our

people, who we consider to be the best in our industry.

We also are positive about the changes our business has

undergone in recent years and believe we are better

positioned for optimum performance under varying

economic conditions. The future appears bright for our

industry in the coming years.

In closing, I would like express to each client how much

we value our business relationship with you. To our

people, thank you for your hard work and your many

contributions to our success. Finally, thank you, our

shareholders, for the trust and support you have placed

in us through your investment in MPS Group.

TI M OT H Y D. PAY N E

PR E S I D E N T A N D CH I E F E X E C U T I V E OF F IC E R

April 14, 2006

6 MPS Group

Accounting Principals is a leader in the recruitment and placement of accounting and

finance professionals. Accounting Principals offers a complete range of work force

solutions in accounting and finance through a nationwide office network.

• Continued to expand its service delivery network

• Improved the breadth and capability of its permanent placement practice

• Developed and implemented innovative recruiting techniques to attract talent amid a worldwide shortage of accountants

• Expanded its client base across Fortune 1000 companies, middle-market clients, and government entities

Entegee is a leading provider of technical and engineering staffing services. Entegee

serves clients in the manufacturing, aerospace, defense, and telecommunications

industries.

• Realized the best financial performance since its inception, with revenues up 15% and strong profitability

• Continued to build on the strength of defense and aerospace while new avenues of growthwere seen in the telecommunications and construction equipment industries

• Renewed long-term contracts with a number of its largest clients

• Opened three start-up offices in key markets

Special Counsel provides legal staffing services to corporate legal departments and

law firms. Special Counsel offers workload management, litigation support, business

transaction support, and customized staffing and project management.

• Grew revenues over 20% while maintaining position as the largest provider of legal staffing services

• Successfully won and delivered a number of large legal outsourcing projects

• Continued rapid expansion of its permanent placement practice

• Continued to expand its suite of service offerings in court reporting, deposition digesting, and medical document review

PROFESSIONAL SERVICES DIVISION – 2005 HIGHLIGHTS

7MPS Group

Soliant Health delivers specialized health care staffing services to hospitals and health

care providers. Soliant supplies traveling nurses and allied health care professionals on

both temporary and direct-hire assignments to leading facilities across the United States.

• Awarded the Gold Seal of Approval for Healthcare Staffing Services by The JointCommission on Accreditation of Healthcare Organizations (JCAHO)

• Grew operating income by more than 150% when compared to 2004

• Continued to expand service offerings to include bilingual speech therapy, physician search, pharmacy, and health care operations

• Surpassed health care staffing peer group in revenue growth, margin improvement, and business mix

Badenoch & Clark specializes in professional services recruitment in the United

Kingdom and Europe on a direct-hire, temporary, and contract basis. Badenoch & Clark

serves clients in the accounting, financial services, banking, insurance, legal, and

human resources disciplines.

• Delivered superior financial performance with revenue growth of 26% and operatingincome growth of 98% when compared to 2004

• Continued to expand on-site outsourcing arrangements with key clients, such as the

London Borough of Newham

• Recently ranked 7th on the list of 100 Best U.K. Companies To Work For by London’s The Sunday Times

• Named Best Public Sector Recruitment Agency by Recruiter magazine

PR OF E S S IO N A L SE RV IC E S DI V I S IO N RE V E N U E(in thousands)

8 MPS Group

Modis is one of North America’s leading providers of information technology (IT)

staffing services and solutions including contract, contract-to-hire, direct hire, and

project management. Modis serves more than 1,000 clients in virtually every industry.

• Grew revenues by over 10% on an organic basis

• Grew permanent placement fees by over 100%

• Named one of the top 500 IT solutions providers by VARBusiness magazine

• Maintained its position as a leading provider to the Fortune 1000 while significantly expanding its footprint among middle-market companies

Beeline delivers solutions that automate work force acquisition, management, and

analytics to help organizations streamline the process of recruiting, hiring, procuring,

and managing full-time and contingent work forces.

• Processed over $2 billion in labor spending through its leading Web-based, contingent laborprocurement application

• Continued to build its client base of Fortune 1000 companies

• Successfully delivered a next generation application built upon the Microsoft.NETarchitecture

• Significantly grew its international client base

Idea Integration provides technology solutions and systems integration services. Idea

Integration specializes in application development, digital data management,

business intelligence, infrastructure and security, and interactive marketing.

• Grew market share across its service delivery network with sharp gains in the southeastern

United States

• Experienced strong increases in project activity among state and local government clients

• Named one of the top 50 interactive agencies by AdWeek magazine

• Awarded two Manager Excellence Awards by Microsoft

IT SE RV IC E S DI V I S IO N – 2005 HIGHLIGHTS

9MPS Group

Modis International is one of Europe’s largest and most respected providers of IT

staffing services and solutions. Modis International serves FTSE 1000 companies

and government entities in the United Kingdom and continental Europe.

• Improved margins in second half of year by focusing efforts on higher-margin clients andhigher-margin services

• Expanded European footprint to seven countries with the establishment of operations in Scotland

• Won significant contract to provide full-time IT professionals to the United Kingdom’sNational Health Service

• Won competitive bids to secure renewals with a number of key clients

INFORMATION TECHNOLOGY SERVICES DIVISION REVENUE(in thousands)

NORTH AMERICAN

IN F OR M AT IO N

TE C H N OLO G Y :

IT SE RV IC E S 25%

IT SOL U T IO N S 4%

WOR K FOR C E

AU TO M AT IO N 1%

10 MPS Group

NORT H A M E R IC A N PR OF E S S IO N A L SE RV IC E S :

HE A LT H CA R E 4%

ACCOUNTING AND FINANCE 5.5%

LE G A L 8%

EN G I N E E R I N G 14 .5%

NORT H A M E R IC A 62%

UN I T E D KI N G D O M 35%

CO N T I N E N TA L EU R OPE 3%

EU R OPE A N

IN F OR M AT IO N

TE C H N OLO G Y 16%

EU R OPE A N

PR OF E S S IO N A L

SE RV IC E S 22%

2005 RE V E N U E BY GE O G R A PH IC AR E A

2005 RE V E N U E BY SE G M E N T

MPS Group 11

FORWARD-LOOKING STATEMENTS

This Annual Report to Shareholders contains forward-looking statements that are subject to certain risks,uncertainties or assumptions and may be affected bycertain factors, including but not limited to the specificfactors discussed below, under “Risk Factors,” “Marketfor Registrant’s Common Equity, Related StockholderMatters and Issuer Purchases of Equity Securities,” and“Management’s Discussion and Analysis of FinancialCondition and Results of Operations—Liquidity andCapital Resources.” In some cases, you can identifyforward-looking statements by terminology such as“may,” “should,” “could,” “expects,” “plans,” “indicates,”“projects,” “anticipates,” “believes,” “estimates,” “appears,”“predicts,” “potential,” “continues,” “can,” “hopes,”“perhaps,” “would,” or “become,” or the negative ofthese terms or other comparable terminology. Inaddition, except for historical facts, all informationprovided below, under “Quantitative and QualitativeDisclosures About Market Risk” should be considered

forward-looking statements. Should one or more ofthese risks, uncertainties or other factors materialize,or should underlying assumptions prove incorrect,actual results, performance or achievements of theCompany may vary materially from any future results,performance or achievements expressed or implied bysuch forward-looking statements.

Forward-looking statements are based on beliefs andassumptions of the Company’s management and oninformation currently available to such management.Forward looking statements speak only as of the datethey are made, and the Company undertakes noobligation to publicly update any of them in light ofnew information or future events. Undue reliance shouldnot be placed on such forward-looking statements,which are based on current expectations. Forward-looking statements are not guarantees of performance.

IN T R OD U C T IO N

MPS Group, Inc. is a leading provider of businessservices with over 190 offices throughout the UnitedStates, Canada, the United Kingdom, and continentalEurope. We deliver specialty staffing, consulting andbusiness solutions to virtually all industries in thefollowing disciplines, through the following primarybrands:

BR A N D(S ) DI S C I P L I N E

Information Technology (IT) Services

Accounting and Finance

Engineering

Legal

IT Solutions

Health Care

Work Force Automation

Our strategy is to focus on increasing revenue andprofits, through a combination of internal growth andacquisitions, primarily within our core disciplines and,to a lesser extent, expansion into new specialties.

Specifically, we aim to maintain a leadership positionin our IT-related disciplines, while growing ourprofessional-related disciplines both organically andthrough acquisitions, which should result in theProfessional Services Division providing a largeroverall percentage contribution to our total revenues.

The key elements to our internal growth strategyinclude:

• increasing penetration of existing markets andcustomer segments,

• expanding current specialties into new andcontiguous geographic markets,

• concentrating on skill areas that value high levelsof service, and

• identifying and adding new practice areas.

While we look to strengthen relationships with ourclients, we are not dependent upon a single customeror a limited number of customers.

Pursuant to our acquisition strategy, we acquiredeleven businesses from 2003 to 2005: four legal staffingbusinesses acquired in February of 2003, August of2003, August of 2004, and October of 2004; threehealth care staffing businesses acquired in February of2004, March of 2004, and September of 2005; fouraccounting and finance staffing businesses acquired inFebruary of 2004, July of 2004, October of 2004, andSeptember of 2005; and two IT Solutions businesses,acquired in July of 2005 and September of 2005. Theaccounting and financing business and IT solutions

business acquired in September of 2005 were part ofthe same acquisition. The businesses acquired in 2005,2004, and 2003, had a combined annualized revenue of$25 million, $95 million, and $22 million at acquisitiondate, respectively.

In addition, we look to focus our efforts intensely onour core businesses. Toward this end, we have divestedcertain businesses we deemed not central to our strategy,including the 2003 sale of our outplacement unit, andthe 2004 sale of our retained executive search unit. Wefeel we are able to execute and profit from our internalgrowth and acquisition strategies due to our strongmanagement team, our integrated and scalable backoffice support services, and to the continued develop-ment of our strategic management information systems.

In all of our markets and disciplines, we encounteraggressive and capable competition, with a number offirms offering services similar to ours on a national,regional or local basis. Our ability to compete success-fully depends on our reputation, pricing and quality ofservice provided, our understanding of clients’ specificjob requirements, and our ability to provide qualifiedpersonnel in a timely manner.

The Company was incorporated under the laws of theState of Florida in 1992 under the name AccustaffIncorporated, and changed its name to MPS Group,

Inc. in 2002. Our principal executive offices are locatedin Jacksonville, Florida. Strategically, our operations arecoordinated primarily from facilities in Jacksonville,Florida, and London, England, and to a lesser extent,Burlington, Massachusetts. Both of our Jacksonvilleand London facilities provide support and centralizedservices to our offices in the administrative, marketing,public relations, accounting, training and legal areas.Regional and local office managers are responsible formost activities of their offices, including sales, localand regional marketing and recruitment.

SE G M E N TS

We present the financial results of our operationsunder our four reporting segments: North AmericanProfessional services, European Professional services,North American IT services and European IT services.In addition, we have both a Professional services and anIT services division. The Professional services divisionis comprised of both the North American Professionalservices segment and the European Professional servicessegment. The IT services division is comprised ofboth the North American IT services segment andthe European IT services segment. The table belowhighlights the percentage contribution of revenue andgross profit from our four segments for 2005 and 2004:

12 MPS Group

Professional Services division Our Professional services division provides specializedstaffing and recruiting in the disciplines of accounting,finance staffing, law, engineering and healthcare forvarying periods of time to companies or other organiza-tions (including government agencies) that have a needfor such personnel, but are unable to, or choose not to,engage certain personnel as their own employees.Businesses increasingly view the use of temporaryemployees as a means of controlling personnel costsand converting the nature of such costs from fixed tovariable. Examples of client needs for staffing solutionsinclude the need for specialized or highly-skilledpersonnel for the completion of a specific project orsubproject, substitution for regular employees duringvacation or sick leave, and staffing of high turnoverpositions or during seasonal peaks.

We operate this division under a variable cost businessmodel whereby revenue and cost of revenue are primarilyrecognized and incurred on a time-and-materialsbasis. The vast majority of the billable consultants arecompensated on an hourly basis only for the hourswhich are billed to our clients.

Clients also hire our skilled consultants on a permanentbasis, whether it is from a conversion of a temporaryassignment to, or a direct placement of, a full-timeposition. We earn a one-time fee for these services.These fees represent approximately 6% of this division’srevenue.

2005 2004 2005 2004Revenue Revenue Gross Profit Gross Profit

North American Professional Services 31.9% 30.1% 36.3% 34.3%European Professional Services 21.6% 20.3% 23.5% 22.3%

Professional Services Division 53.5% 50.4% 59.8% 56.6%

North American IT Services 30.3% 32.2% 32.1% 34.3%European IT Services 16.2% 17.4% 8.1% 9.1%

IT Services Division 46.5% 49.6% 40.2% 43.4%

North American Segments 62.2% 62.3% 68.4% 68.6%European Segments 37.8% 37.7% 31.6% 31.4%

Additional financial information relating to our segments can be found in Footnote 15 to the Consolidated Financial Statements.

The principal national and international competitorsof our Professional services division include RobertHalf International Inc., Resources Connection, Inc.,Spherion Corporation, Kelly Law Registry, AjilonConsulting (a wholly owned subsidiary of Adecco SA),Michael Page International, Robert Walters PLC,Hays PLC, Cross Country Healthcare, Inc., and CDICorporation.

North American Professional Services segment Our North American Professional services segment goesto market under the primary brands and operating unitsEntegee, Special Counsel, Accounting Principals, andSoliant Health. The demands of our clients (the need forconfidentiality, accuracy and reliability, cost-effectiveness,and frequent peak workload periods) are similar amongthe businesses within this segment.

Entegee provides technical and engineering strategicworkforce solutions. From on-site managementconsulting and in-house project services to temporaryand direct placement, Entegee combines industryknowledge and experience to fill highly skilledtechnical and engineering positions. These positionsinclude, but are not limited to, engineers, designers,drafters, inspectors and assemblers. Entegee operatesthrough a domestic network of national practicebranches with offices in 10 markets, and employsapproximately 2,700 billable consultants. Entegeealso provides engineering and drafting design servicesthrough two company-owned centers that utilizestate-of-the-art computer technology. Its primaryclients include government and defense contractors,manufacturing and engineering companies.

Special Counsel staffs temporary and full-timeemployees in attorney, paralegal, legal administrativeand legal secretarial positions for workload manage-ment, litigation support, business transaction support,pre-litigation and document management support, aswell as medical document review, deposition digesting,court reporting and other trial-related services.Special Counsel has a network of 37 offices acrossthe United States, and employs approximately 1,700billable consultants. Its primary clients are Fortune1000 companies and law firms.

Accounting Principals specializes in placing temporaryand full-time employees in accounting and financepositions. Accounting Principals has a network of40 offices across the United States, and employsapproximately 1,400 billable consultants.

In 2005, we expanded Accounting Principals’geographic footprint with the acquisition of PacioliCompanies in September. Pacioli Companies provideshigh-end accounting candidates to clients primarilylocated in the Minneapolis, St. Paul, Minnesota area.

Soliant Health specializes primarily in placingtraveling healthcare professionals, in the areas ofnursing, physical and occupational therapy, alongwith imaging technicians. Soliant Health employsapproximately 700 consultants, and its clients includehospitals and healthcare providers across theUnited States.

In 2005, we expanded Soliant Health’s service linewith the acquisition of Bilingual Therapies inSeptember. Bilingual Therapies provides bilingualand monolingual Speech Language Pathologists(SLPs) to school systems throughout the country.Bilingual Therapies is the national market leader inthe placement of bilingual SLPs.

Dispositions In 2003, we sold certain operating assets and transferredcertain operating liabilities of our outplacement unit.The decision to sell our outplacement unit was inkeeping with our long-term strategy of focusing onour core businesses. As a result of the sale of ouroutplacement unit and in accordance with GenerallyAccepted Accounting Principles (GAAP), ourConsolidated Financial Statements and Management’sDiscussion and Analysis of Financial Condition andResults of Operations report the results of operationsof this unit as Discontinued Operations for all periodspresented. In 2004, we sold certain assets and transferredcertain liabilities of our retained executive search brand.

European Professional Services segment Since 1980, our European professional services business,Badenoch & Clark, has specialized in placing temporary,full-time, contract and interim recruitment employeesin accounting and finance, financial services, legal,human resources, and marketing positions. Badenoch& Clark has 19 offices across the United Kingdom andan office in Luxembourg. Badenoch & Clark employsapproximately 4,200 billable consultants.

IT Services division Our IT services division provides specialty staffing,consulting and business solutions under the brands/operating units Modis, Modis International, IdeaIntegration and Beeline. We utilize the brand Modisin both our North American and European segments;however, the overall business culture distinguishes theoperation of these two segments.

We operate this division primarily under a variable costbusiness model whereby revenue and cost of revenueare primarily recognized and incurred on a time-and-materials basis. The vast majority of the billable con-sultants are compensated on an hourly basis only for thehours which are billed to our clients. Approximately1% of this division’s revenue is generated from fees forclients directly hiring our consultants.

13MPS Group

The principal national and international competitors ofour IT services division include Keane, Inc., ComputerHorizons Corp., Comsys IT Partners, Inc., CIBER,Inc., Computer People (a division of Ajilon Group),Hays PLC, Elan, Lorien PLC, and Sapient Corporation.In addition, we may compete against the internalmanagement information services and IT departmentsof our clients and potential clients.

North American IT Services segment Modis specializes in the placement of IT contractconsultants for IT project support and staffing,recruitment of full-time positions, project-basedsolutions, supplier management solutions, and on-siterecruiting support for application development, systemsintegration, and enterprise application integration.Modis has a network of 44 offices across the UnitedStates, and employs approximately 3,700 billableconsultants. Its primary clients are Fortune 1000companies.

Idea Integration specializes in Web design anddevelopment, information management solutions,wireless workflow applications, portal solutions, andenterprise resource management. Idea utilizes bothsalaried and hourly consultants to deliver solutionsprimarily under time-and-materials contracts and toa lesser extent under fixed-fee contracts. It operatesin certain markets across the United States and itsclients include Fortune 1000 companies, governmentand middle-market companies.

In 2005, we expanded Idea Integration’s geographicfootprint with the acquisitions of two IT solutionsbusinesses: Encore Development in July and PacioliCompanies in September. Encore Development is aFlorida-based IT solutions company specializing inMicrosoft development capabilities with clientsprimarily located in northeast Florida. PacioliCompanies provides IT programmers, statisticalanalysts, modelers, architects, and implementers toclients using SAS Software.

Beeline is our software-based human capitalmanagement services solution that automates theacquisition and management of both full-time andcontingent workers. Beeline operates primarily inthe United States and its’ clients are principallyFortune 1000 companies.

Beeline maintains a full-time staff to support itsoperations and seeks to collect a service charge basedupon the usage of this service. Subsequent to the initialstart up costs and time, minimal cost and resourcesare required for the usage of Beeline’s services.

European IT Services segment Our European IT services segment is comprised ofModis International. Modis International, headquar-tered in the United Kingdom, specializes in providingIT contract consultants throughout the UnitedKingdom and certain continental European markets.Modis International has been in operation for over 30years. It has 11 offices across the United Kingdom, andan office each in Belgium, Germany, and the Netherlands.It employs approximately 2,100 billable consultants.

EM P LO Y E E S

MPS employs approximately 16,800 consultants andapproximately 2,600 full-time staff employees. Approx-imately 250 of the employees work at corporateheadquarters.

As described below, in most jurisdictions, we, as theemployer of the consultants or as otherwise requiredby applicable law, are responsible for employmentadministration. This administration includes collectionof withholding taxes, employer contributions for socialsecurity or its equivalent outside the United States,unemployment tax, maintaining workers’ compensationand fidelity and liability insurance, and other govern-mental requirements imposed on employers. Full-timeemployees are covered by life and disability insuranceand receive health insurance and other benefits.

GO V E R N M E N T RE G U L AT IO N S

Outside of the United States and Canada, the staffingservices industry is closely regulated. These regulationsdiffer among countries but generally may regulate:(i) the relationship between us and our temporaryemployees; (ii) registration, licensing, record keeping,and reporting requirements; and (iii) types of operationspermitted. Regulation within the United States andCanada has not materially impacted our operations.

In many countries, including the United States and theUnited Kingdom, staffing services firms are consideredthe legal employers of the temporary consultants whilethe consultant is on assignment with a company client.Therefore, laws regulating the employer/employeerelationship, such as tax withholding or reporting,social security or retirement, anti-discrimination, andworkers’ compensation, govern us. In other countries,staffing services firms, while not the direct legalemployer of the consultant, are still responsible forcollecting taxes and social security deductions andtransmitting such amounts to the taxing authorities.

14 MPS Group

IN T E L L E C T UA L PR OPE RT Y

We seek to protect our intellectual property throughcopyright, trade secret and trademark law and throughcontractual non-disclosure restrictions. Our servicesoften involve the development of work and materialsfor specific client engagements, the ownership of whichis frequently assigned to the client. We do at times, andwhen appropriate, negotiate to retain the ownership orcontinued use of development tools or know howcreated or generated by us for a client in the deliveryof our services, which we may then license or use inthe delivery of our services to other clients.

SE A S O N A L I T Y

Our quarterly operating results are affected by thenumber of billing days in the quarter and the seasonalityof our customers’ businesses. Demand for our serviceshas historically been lower during the calendar year-end, as a result of holidays, through February of thefollowing year. Extreme weather conditions may alsoaffect demand in the early part of the year as certainof our clients’ facilities are located in geographic areassubject to closure or reduced hours due to inclementweather. In addition, we experience an increase in ourcost of sales and a corresponding decrease in grossprofit and gross margin in the first fiscal quarter ofeach year, as a result of certain U.S. state and federalemployment tax resets.

ACCESS TO COMPANY INFORMATION

Our common stock is listed on the New York StockExchange (‘NYSE’) under the ticker symbol ‘MPS’.Our Internet address is www.mpsgroup.com. We makeavailable through our Internet website our annualreports on Form 10-K, quarterly reports on Form 10-Q,and current reports on Form 8-K, as soon as reasonablypracticable after filing such material with, or furnishingit to, the Securities and Exchange Commission. Theinformation contained on our website, or on other web-sites linked to our website, is not part of this document.

RI S K FA C TOR S

Our results of operations and financial condition can beadversely affected by numerous risks and uncertainties.The most important of these risks and uncertaintiesare detailed below. You should carefully consider therisk factors detailed below in conjunction with theother information contained in this document. Shouldany of these risks actually materialize, our business,financial condition, and future prospects could benegatively impacted.

Demand for our services is affected by the economicclimate in the industries and markets we serve. Thedemand for our services, in particular our staffingservices, is highly dependent upon the state of economyand upon the staffing needs of our clients. Any negativevariation in the economic condition of the UnitedStates, United Kingdom or of any of the other foreigncountries in which we do business, may severely reducethe demand for our services and thereby significantlydecrease our revenues and profits.

Our market is highly competitive with low barriers toentry. Our industry is intensely competitive and highlyfragmented, and the barriers to entry are quite low.There are many competitors, and new ones are enteringthe market constantly. In addition, some of these com-petitors have greater resources than us. Competitionarises locally, regionally, nationally, internationally andin certain cases from remote locations, particularlyfrom offshore locations such as India and China.

Certain of our contracts are awarded on the basis ofcompetitive proposals, which can be periodically re-bidby the client. There can be no assurance that existingcontracts will be renewed on satisfactory terms or thatadditional or replacement contracts will be awarded tous. In addition, long-term contracts form a negligibleportion of our revenue. There can be no assurance wewill be able to retain clients or market share in thefuture. Nor can there be any assurance that we will, inlight of competitive pressures, be able to remain profitableor, if profitable, maintain our current profit margins.

Our business requires a qualified candidate pool,which we may not be able to recruit or maintain. Ourstaffing services consist of the placement of individualsseeking employment in specialized IT and professionalpositions. Some of these sectors are characterized by ashortage of qualified candidates. There can be noassurance that suitable candidates for employmentwill continue to be available or will continue to seekemployment through us. Candidates generally seektemporary or regular positions through multiple sources,including us and our competitors. Any shortage ofqualified candidates could materially adversely affect us.

Our business depends on key personnel, includingexecutive officers, local managers and field personnel.We are engaged in a services business. As such, oursuccess or failure is highly dependent upon the perfor-mance of our management personnel and employees,rather than upon technology or upon tangible assets(of which we have few). There can be no assurancethat we will be able to attract and retain the personnelthat are essential to our success.

15MPS Group

We have to comply with existing governmentregulation and are exposed to increased regulation ofthe workplace. Our business is subject to regulation orlicensing in many states and in certain foreign countries.There can be no assurance we will be able to continueto obtain all necessary licenses or approvals or that thecost of compliance will not prove to be material in thefuture. Any inability to comply with governmentregulation or licensing requirements, or increase in thecost of compliance, could materially adversely affectus. Additionally, our staffing services entail employingindividuals on a temporary basis and placing suchindividuals in clients’ workplaces. Increased governmentregulation of the workplace or of the employer-employeerelationship could materially adversely affect us.

We are exposed to claims and costs, liabilities andlitigation arising from the delivery of our services.Our recruiting services involve our referring candidatesto clients for potential employment, and our staffingservices entail employing or retaining individuals on atemporary basis and placing such individuals in clients’workplaces. Our recruiting services entail a risk ofliability to our clients and others, contractually andotherwise, arising from allegations of inadequatebackground checks, inadequate credentialing of ournursing and healthcare workers, and negligent referralof candidates to our clients. Our staffing services entaila risk of liability to our clients and others, contractuallyand otherwise, arising from various workplace events,often beyond our control, including allegations of errorsand omissions, injury to property or persons, ormisappropriation or theft of property or proprietaryinformation allegedly caused or contributed to by ourtemporary workers. Our staffing services also entail arisk of employment and co-employment liability, toeither or both our clients and our temporary workers,arising from allegations by our temporary workers ofdiscrimination, harassment, inadequate workplaceconditions, or entitlement to employee benefits or payfrom clients to which they are assigned. The Companymaintains insurance with respect to many of theaforementioned claims. While such claims have nothistorically had a material adverse effect upon theCompany, there can be no assurance that the Companywill continue to be able to obtain insurance at a costthat does not have a material adverse effect upon theCompany or that such claims (whether by reason ofthe Company not having insurance or by reason ofsuch claims being outside the scope of the Company’sinsurance) will not have a material adverse effect uponthe Company.

We have acquired, and may continue to acquire,companies, and these acquisitions could disrupt ourbusiness or adversely affect our earnings. We haveacquired several companies and may continue to acquire

companies in the future. Entering into an acquisitionentails many risks, any of which could harm ourbusiness, including failure to successfully integrate theacquired company with our existing business, alienationor impairment of relationships with substantialcustomers or key employees of the acquired businessor our existing business, and assumption of liabilitiesof the acquired business. Any acquisition that weconsummate also may have an adverse affect on ourliquidity or earnings and may be dilutive to our earnings.Adverse business conditions or developments sufferedby or associated with any business we acquire additionallycould result in impairment to the goodwill or intangibleassets associated with the acquired business, and arelated write down of the value of these assets, andadversely affect our earnings.

The price of our common stock may fluctuatesignificantly. The market price for our common stockcan fluctuate as a result of a variety of factors, includingthe factors listed above, many of which are beyond ourcontrol. These factors include: actual or anticipatedvariations in quarterly operating results; announcementsof new services by our competitors or us; announce-ments relating to strategic relationships or acquisitions;changes in financial estimates or other statements bysecurities analysts; and other changes in generaleconomic conditions. Because of this, we may fail tomeet or exceed the expectations of our shareholders orof our securities analysts, and the market price for ourcommon stock could fluctuate as a result.

UN R E S OLV E D STA F F CO M M E N TS

There are no unresolved comments from the Staff ofthe Securities and Exchange Commission concerningour periodic or current reports under the SecuritiesExchange Act of 1934.

PR OPE RT I E S

Our corporate headquarters, located in Jacksonville,Florida, is on lease through 2012. Our business servicesare conducted through more than 190 offices locatedin the United States, Canada, the United Kingdom,and continental Europe. Almost all of our offices areon lease, with the terms of an average office leasebeing from three to six years.

We believe our facilities are generally adequate for ourneeds and do not anticipate difficulty replacing suchfacilities or locating additional facilities, if needed.Additional information on lease commitments can befound in Footnote 6 to the Consolidated FinancialStatements.

16 MPS Group

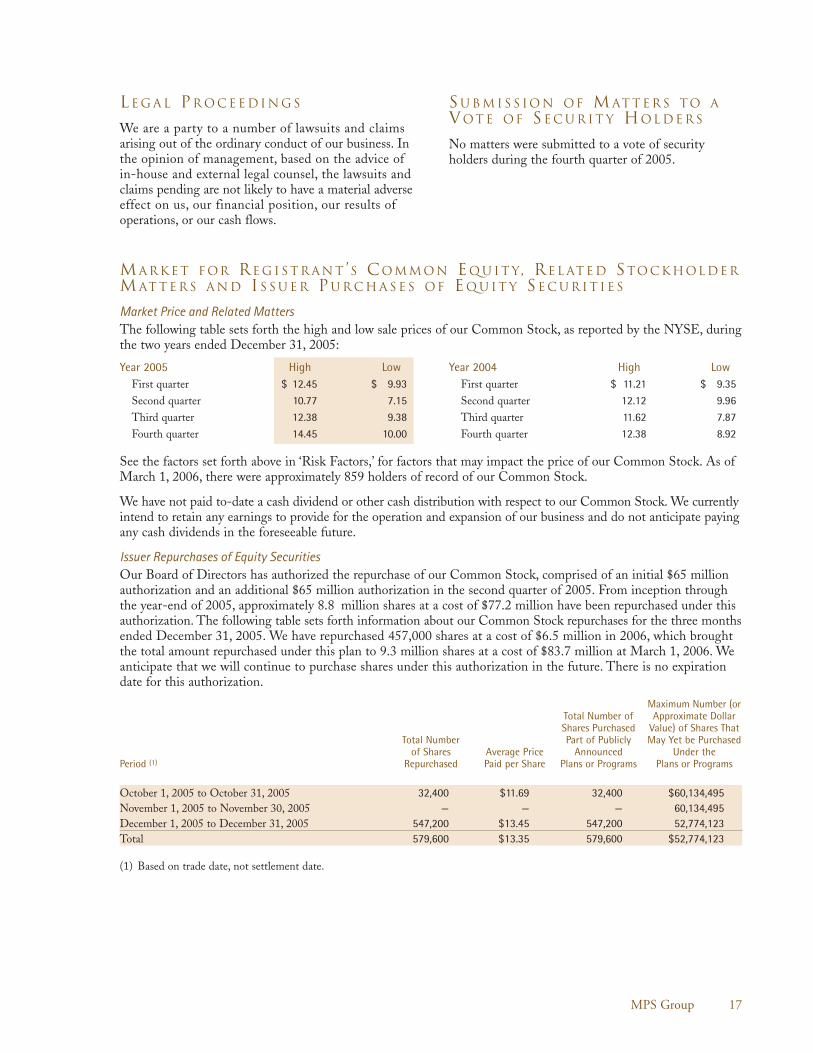

LE G A L PR O C E E D I N G S

We are a party to a number of lawsuits and claimsarising out of the ordinary conduct of our business. Inthe opinion of management, based on the advice ofin-house and external legal counsel, the lawsuits andclaims pending are not likely to have a material adverseeffect on us, our financial position, our results ofoperations, or our cash flows.

SU B M I S S IO N OF M AT T E R S TO AVOT E OF SE C U R I T Y HOL D E R S

No matters were submitted to a vote of securityholders during the fourth quarter of 2005.

17MPS Group

MA R K E T F OR RE G I S T R A N T ’S COM M ON EQ U I T Y, RE L AT E D STO C K HOL DE RM AT T E R S A N D IS S U E R PU R C H A S E S OF EQ U I T Y SE C U R I T I E S

Market Price and Related Matters The following table sets forth the high and low sale prices of our Common Stock, as reported by the NYSE, duringthe two years ended December 31, 2005:

See the factors set forth above in ‘Risk Factors,’ for factors that may impact the price of our Common Stock. As ofMarch 1, 2006, there were approximately 859 holders of record of our Common Stock.

We have not paid to-date a cash dividend or other cash distribution with respect to our Common Stock. We currentlyintend to retain any earnings to provide for the operation and expansion of our business and do not anticipate payingany cash dividends in the foreseeable future.

Issuer Repurchases of Equity Securities Our Board of Directors has authorized the repurchase of our Common Stock, comprised of an initial $65 millionauthorization and an additional $65 million authorization in the second quarter of 2005. From inception throughthe year-end of 2005, approximately 8.8 million shares at a cost of $77.2 million have been repurchased under thisauthorization. The following table sets forth information about our Common Stock repurchases for the three monthsended December 31, 2005. We have repurchased 457,000 shares at a cost of $6.5 million in 2006, which broughtthe total amount repurchased under this plan to 9.3 million shares at a cost of $83.7 million at March 1, 2006. Weanticipate that we will continue to purchase shares under this authorization in the future. There is no expirationdate for this authorization.

Maximum Number (orTotal Number of Approximate DollarShares Purchased Value) of Shares That

Total Number Part of Publicly May Yet be Purchasedof Shares Average Price Announced Under the

Period (1) Repurchased Paid per Share Plans or Programs Plans or Programs

October 1, 2005 to October 31, 2005 32,400 $11.69 32,400 $60,134,495November 1, 2005 to November 30, 2005 — — — 60,134,495December 1, 2005 to December 31, 2005 547,200 $13.45 547,200 52,774,123Total 579,600 $13.35 579,600 $52,774,123

(1) Based on trade date, not settlement date.

Year 2005 High LowFirst quarter $ 12.45 $ 9.93

Second quarter 10.77 7.15

Third quarter 12.38 9.38

Fourth quarter 14.45 10.00

Year 2004 High LowFirst quarter $ 11.21 $ 9.35

Second quarter 12.12 9.96

Third quarter 11.62 7.87

Fourth quarter 12.38 8.92

SE L E C T E D FI N A N C I A L DATA(in thousands, except per share amounts)

Years Ended 12-31-2005 12-31-2004 12-31-2003 12-31-2002 12-31-2001

Consolidated Statements of Operations data:Revenue $ 1,684,699 $ 1,426,842 $ 1,096,030 $ 1,119,156 $ 1,500,615Cost of revenue 1,242,331 1,066,055 808,890 834,318 1,105,781Gross profit 442,368 360,787 287,140 284,838 394,834Operating expenses 355,382 309,551 251,623 255,929 342,918Amortization of goodwill (1) — — — — 37,312Impairment of investment — — — 16,165 —Exit costs (recapture) — ( 897 ) ( 284 ) 8,967 —Operating income 86,986 52,133 35,801 3,777 14,604Other income (expense), net 3,799 1,437 553 ( 3,947 ) ( 9,199 )Income (loss) from continuing operations

before income taxes and cumulativeeffect of accounting change 90,785 53,570 36,354 ( 170 ) 5,405

Provision for income taxes 31,188 18,150 14,519 13,832 3,102Income (loss) from continuing

operations before cumulativeeffect of accounting change 59,597 35,420 21,835 ( 14,002 ) 2,303

Discontinued operations: (2)

Income (loss) from discontinuedoperations, net of tax — — ( 2,395 ) 1,410 6,040

Loss on sale of discontinuedoperations, net of tax — — ( 20,675 ) — —

Income (loss) before cumulativeeffect of accounting change 59,597 35,420 ( 1,235 ) ( 12,592 ) 8,343

Cumulative effect of accountingchange, net of tax (1) — — — ( 553,712 ) —

Net income (loss) $ 59,597 $ 35,420 $ ( 1,235 ) $ ( 566,304 ) $ 8,343

Basic income (loss) per common share:From continuing operations $ 0.59 $ 0.34 $ 0.21 $ ( 0.14 ) $ 0.02From discontinued operations $ — $ — $ ( 0.02 ) $ 0.01 $ 0.06From sale of discontinued operations $ — $ — $ ( 0.20 ) $ — $ —From accounting change $ — $ — $ — $ ( 5.49 ) $ —

Basic income (loss) per common share $ 0.59 $ 0.34 $ ( 0.01 ) $ (5.62 ) $ 0.09

Diluted income (loss) per common share:From continuing operations $ 0.56 $ 0.33 $ 0.21 $ (0.14 ) $ 0.02From discontinued operations $ — $ — $ (0.02 ) $ 0.01 $ 0.06From sale of discontinued operations $ — $ — $ (0.20 ) $ — $ —From accounting change $ — $ — $ — $ (5.49 ) $ —

Diluted income (loss) per common share $ 0.56 $ 0.33 $ (0.01 ) $ (5.62 ) $ 0.08

Basic average common shares outstanding 101,719 102,804 101,680 100,833 97,868

Diluted average common shares outstanding 105,832 106,842 104,518 100,833 98,178

18 MPS Group

December 31, 2005 2004 2003 2002 2001(in thousands)

Consolidated Balance Sheet data:Working capital $ 279,859 $ 232,133 $ 216,879 $ 171,154 $ 200,887Total assets 1,028,006 954,604 893,151 892,974 1,533,863Long term debt — — — — 101,000Stockholders’ equity (1) 876,040 835,663 793,462 781,559 1,310,811

(1) The Company recognized an impairment loss associated with its adoption of Statement of Financial Accounting Standards (SFAS)No. 142 “Goodwill and Other Intangible Assets,” effective January 1, 2002. This loss was recorded as a Cumulative Effect of AccountingChange, and reduced Stockholders’ Equity. In addition, SFAS No. 142 discontinued the periodic amortization of goodwill.

(2) The income (loss) from discontinued operations for the periods presented above and the 2003 loss on sale related to the discontinuedoutplacement unit, sold in December 2003.

19MPS Group

MA N A G E M E N T ’S DI S C U S S ION A N DANALYSIS OF FINANCIAL CONDITIONA N D RE S U LTS OF OPE R AT IO N S

MPS Group, Inc. is a leading provider of businessservices with over 190 offices throughout the UnitedStates, Canada, the United Kingdom, and continentalEurope. The Company delivers specialty staffing,consulting and business solutions to virtually allindustries in the following disciplines and through thefollowing primary brands:

Brand(s) DisciplineModis® Information Technology (IT)

ServicesBadenoch & Clark®, Accounting and FinanceAccounting Principals®Entegee® EngineeringSpecial Counsel® LegalIdea Integration® IT SolutionsSoliant Health® Health CareBeeline® Work Force Automation

The Company presents the financial results of theabove brands under its four reporting segments: NorthAmerican Professional services, European Professionalservices, North American IT services and EuropeanIT services.

Non-GAAP Financial Measures From time to time we may measure certain financialinformation on a ‘constant currency’ basis. Such constantcurrency financial data is not a U.S. generally acceptedaccounting principles (‘GAAP’) financial measure.Constant currency removes from financial data theimpact of changes in exchange rates between the U.S.dollar and the functional currencies of our foreignsubsidiaries, by translating the current period financialdata into U.S. dollars using the same foreign currency

exchange rates that were used to translate the financialdata for the previous period. We believe presentingcertain results on a constant currency basis is useful toinvestors because it allows a more meaningful comparisonof the performance of our foreign operations fromperiod to period. Additionally, certain internal reportingand compensation targets are based on constant currencyfinancial data for our various foreign subsidiaries.However, constant currency measures should not beconsidered in isolation or as an alternative to financialmeasures that reflect current period exchange rates, orto other financial measures calculated and presentedin accordance with GAAP.

From 2003 to 2005, we acquired eleven businesses forour North American professional services segment:four legal staffing businesses acquired in February of2003, August of 2003, August of 2004, and Octoberof 2004; three health care staffing businesses acquiredin February of 2004, March of 2004, and Septemberof 2005; and four accounting and finance staffingbusinesses acquired in February of 2004, July of 2004,October of 2004, and September of 2005. In addition,we acquired two IT solutions businesses, in July andSeptember of 2005, in our North American IT Servicessegment. The accounting and finance staffing businessand the IT solutions business acquired in Septemberof 2005 were part of the same acquisition. From timeto time we may measure certain financial informationexcluding the effect of acquisitions. Such financialdata that excludes the effect of businesses we acquire isnot a GAAP financial measure. We believe presentingsome results excluding the effects of businesses weacquire is helpful to investors because it permits acomparison of the performance of our core internaloperations from period to period. Additionally, certaininternal reporting and compensation targets are basedon the performance of core internal operations. Theeffect of a business we acquire is generally excludedfor only the first 12 months following the acquisition

date. Subsequent to this, a business is considered to beintegrated for reporting purposes. Again however, suchmeasures should be considered only in conjunctionwith the correlative measures that include the resultsfrom acquisitions, as calculated and presented inaccordance with GAAP.

Additionally, from time to time we may use EBITDAto measure results of operations. EBITDA is a non-GAAP financial measure that is defined as earningsbefore interest, taxes, depreciation and amortization.We believe EBITDA is a meaningful measure ofoperating performance as it gives management a consis-tent measurement tool for evaluating the operatingactivities of the business as a whole, as well as, thevarious operating units, before the effect of investingactivities, interest and taxes. In addition, we believeEBITDA provides useful information to investors,analysts, lenders, and other interested parties becauseit excludes transactions that management considersunrelated to core business operations, thereby helpinginterested parties to more meaningfully evaluate, trendand analyze the operating performance of our business.We also use EBITDA for certain internal reportingpurposes, and certain compensation targets may bebased on EBITDA. Finally, certain covenants in ourdebt facility are based on EBITDA performancemeasures. EBITDA, as with all non-GAAP financialmeasures, should be considered only in conjunction withthe comparable measures, as calculated and presentedin accordance with GAAP, including net income.

Discontinued Operations In December 2003, we sold certain operating assets andtransferred certain operating liabilities of our outplace-ment unit. As a result of the sale of this unit and inaccordance with GAAP, the Consolidated FinancialStatements and Management’s Discussion and Analysisof Financial Condition and Results of Operationsreport the results of operations of our outplacementunit as Discontinued Operations for all periodspresented. In 2003, this unit generated $21.0 millionin revenue and had a $3.7 million loss before incometaxes. We recorded contract termination costs of$705,000 in 2003 as a result of the sale. Additionalinformation can be found in Footnote 2 to theConsolidated Financial Statements.

Critical Accounting Policies We prepare our financial statements in conformitywith accounting principles generally accepted in theUnited States of America. Associated with this, webelieve the following are our most critical accountingpolicies in that they are the most important to theportrayal of our financial condition and results andrequire management’s most difficult, subjective orcomplex judgments.

Revenue Recognition We recognize substantially all revenue at the timeservices are provided, and on a time and materials basis.In most cases, the consultant is our employee and allcosts of employing the worker are our responsibilityand are included in cost of revenue. Revenuesgenerated when we permanently place an individualwith a client are recorded at the time of start.

In addition and to a lesser extent, we are involved infixed price or lump-sum engagements. The services werender under the relevant contracts generally requireperformance spanning more than one accountingperiod. We recognize revenue for these engagementsunder the proportional performance accounting model.

Allowance for Doubtful Accounts We regularly monitor and assess our risk of not collectingamounts we are owed by our customers. This evaluationis based upon a variety of factors including: an analysisof amounts current and past due along with relevanthistory and facts particular to the customer. Based uponthe results of this analysis, we record an allowance foruncollectible accounts for this risk. This analysis requiresus to make significant estimates, and changes in factsand circumstances could result in material changes inthe allowance for doubtful accounts.

Income Taxes The provision for income taxes is based on incomebefore taxes as reported in the Consolidated Statementsof Operations. Deferred tax assets and liabilities arerecognized for the expected future tax consequences ofevents that have been included in the financial state-ments or tax returns. Under this method, deferred taxassets and liabilities are determined based on thedifferences between the financial statement carryingamounts and the tax basis of assets and liabilitiesusing enacted tax rates in effect for the year in whichthe differences are expected to reverse. An assessmentis made as to whether or not a valuation allowance isrequired to offset deferred tax assets. This assessmentincludes anticipating future income.

Significant management judgment is required indetermining the provision for income taxes, deferredtax assets and liabilities and any valuation allowancerecorded against our deferred tax assets. Managementevaluates all available evidence to determine whetherit is more likely than not that some portion or all ofthe deferred income tax assets will not be realized. Theestablishment and amount of a valuation allowancerequires significant estimates and judgment and canmaterially affect our results of operations. Our effectivetax rate may vary from period to period based, forexample, on changes in estimated taxable income orloss, changes to the valuation allowance, changes to

20 MPS Group

federal, state or foreign tax laws, completion of federal,state or foreign audits, deductibility of certain costs andexpenses by jurisdiction, and as a result of acquisitions.

We have future tax deductions associated with tax-deductible goodwill. Our tax basis in tax-deductiblegoodwill will be deducted in our income tax returns,generating $338.9 million of future tax deductions overthe next 15 years. In addition, we have a net deferredtax asset as of December 31, 2005 and 2004. Thecomponents of our net deferred tax assets as well asother information on income taxes can be found inFootnote 7 to the Consolidated Financial Statements.

Stock Option Plans We have historically issued stock options to employeesand directors as an integral part of our compensationprograms. U.S. GAAP allowed alternative methods ofaccounting for these plans. We have chosen to accountfor our stock option plans under Accounting PrinciplesBoard Opinion No. 25, Accounting for Stock Issued toEmployees (“APB 25”). Under APB 25, the intrinsicvalue of the options is used to record compensationexpense and, as a result, no compensation expenserelated to stock options is included in determining netincome and net income per share in the ConsolidatedFinancial Statements. Restricted stock grants areaccounted for in accordance with APB 25, whichmandates that restricted stock grants with performanceconditions be calculated using the intrinsic value. Asrequired by SFAS No. 148, Accounting for Stock-BasedCompensation—Transition and Disclosure (“SFAS 148”),calculations of pro forma net income (loss) and netincome (loss) per share, computed in accordance withthe method prescribed by SFAS No. 123, Accounting forStock-Based Compensation (“SFAS 123”), are set forth inFootnote 2 to the Consolidated Financial Statements.

We are required to adopt SFAS No. 123 (revised 2004),Share-Based Payment (“SFAS 123R”) beginning withthe first quarter of 2006. SFAS 123R requires allshare-based payments to employees, including grantsof employee stock options, to be recognized in thefinancial statements based on their fair values. The proforma disclosures previously permitted under SFASNo. 123 no longer will be an alternative to financialstatement recognition. Upon adoption of SFAS 123R,we will be required to recognize compensation on allshare-based grants made on or after January 1, 2006,and for the unvested portion of share-based grantsmade prior to January 1, 2006.

Impairment of Tangible and Intangible Assets For acquisitions, we allocate the excess of cost overthe fair market value of the net tangible assets first toidentifiable intangible assets, if any, and then togoodwill. In connection with SFAS No. 142, Goodwilland Other Intangible Assets, we are required to performgoodwill impairment reviews, at least annually, utilizinga fair-value approach.

We performed valuation testing during the fourthquarters of 2003, 2004 and 2005 (our designatedtiming of the annual impairment test under SFASNo. 142) and did not incur any impairment. We plan toperform our next annual impairment review during thefourth quarter of 2006. An impairment review prior toour next scheduled annual review may be required ifcertain events occur, including lower than forecastedearnings levels for various reporting units. In addition,changes to other assumptions could significantly impactour estimate of the fair value of our reporting units.Such a change may result in a goodwill impairmentcharge, which could have a significant impact on thereportable segments that include the related reportingunits and the Consolidated Financial Statements.

We used an equally blended value of a discounted cashflow analysis and market comparables to arrive at fairvalue for SFAS No. 142. For the discounted cash flowanalysis, significant assumptions included expectedfuture revenue growth rates, reporting unit profitmargins, working capital levels and a discount rate.The revenue growth rates and reporting unit profitmargins are based, in part, on its expectation of animproving economic environment. Market comparablesincluded a comparison of the market ratios and per-formance fundamentals from comparable companies.The use of these measurement criteria is consistentwith the underlying concepts used in determining thefair value of a company or reportable unit under themarket approach. The market ratios we used refer tothe multiples of revenue and earnings of comparablecompanies and the performance fundamentals refer tothe consideration of the effects of the differences in theoperating metrics, ie. growth rates, operating margins,gross margins, etc. on our value versus the comparablecompanies. Additional information on Goodwill canbe found in Footnote 5 to the Consolidated FinancialStatements.

We amortize the cost of identifiable intangible assets(either through acquisition or as part of intellectualproperty) over their estimated useful lives unless suchlives are deemed indefinite. We review our long-livedassets and identifiable intangibles for impairmentwhenever events or changes in circumstances indicatethat the carrying amount of the asset may not berecoverable. In performing the review for recoverability,

21MPS Group

we estimate the future cash flows expected to resultfrom the use of the asset and its eventual disposition.If the sum of the expected future cash flows (undis-counted and without interest charges) is less than thecarrying amount of the asset, an impairment loss isrecognized. Otherwise, an impairment loss is notrecognized. Measurement of an impairment loss forlong-lived assets and identifiable intangibles would bebased on the fair value of the asset.

E X E C U T I V E SUM M A RY

We believe that economic conditions strengthenedduring 2004 and 2005, both in the United States andabroad, which had a favorable impact on both MPSand our industry. For 2004 and 2005, we were able togrow revenue in all of our segments. In addition to theimproved macroeconomic conditions, we believe thisrevenue growth is attributable to recent investments wehave made in our business including investments inadditional sales and recruiting staff, acquisitions, newservice offerings, and new office openings. Specificallyin 2004 and 2005, we acquired nine businesses for ourNorth American Professional Services segment(together, the ‘Professional Acquisitions’): two legalstaffing businesses acquired in August and October of2004; three health care staffing businesses acquired inFebruary of 2004, March of 2004, and September of2005; and four accounting and finance staffingbusinesses acquired in February of 2004, July of 2004,October of 2004, and September of 2005. In addition,we acquired two IT services solutions businesses forour North American IT segment (together, the ‘ITAcquisitions’), in July and September of 2005. Whilewe continue to believe we will experience future revenuegrowth, we expect our revenue to continue to beimpacted by general macroeconomic conditions in 2006.

Our consolidated revenue increased 18.1% and ouroperating income increased 67.0% from 2004. Directhire fees increased 44% from 2004, and now represent4.0% of revenue, up from 3.3% in 2004. In addition,we continued to diversify, with revenue from ourProfessional Services division now representing 54% ofconsolidated revenue in 2005 compared to 50% in 2004.For 2006, we will continue to look for opportunities toincrease gross margin along with increasing operatingleverage within each segment. Specifically, within theEuropean IT services segment, our lowest gross marginsegment, we are realizing the positive margin impactfrom scaling back relationships with certain low-margin,high-volume clients in order to focus on higher-marginclients. In addition, we have a foundation for growthwith $143 million of cash on hand at year-end, a $150million credit facility with no outstanding borrowings,no long-term debt, and working capital of $280 million.

The following detailed analysis of operations shouldbe read in conjunction with the 2005 ConsolidatedFinancial Statements and related footnotes includedelsewhere in this Annual Report.

Results of Operations for the Three Years EndedDecember 31, 2005 Consolidated revenue was $1,684.7 million, $1,426.8million, and $1,096.0 million in 2005, 2004 and 2003,respectively, increasing by 18.1% and 30.2% in 2005and 2004, respectively.

Consolidated gross profit was $442.4 million, $360.8million, and $287.1 million in 2005, 2004 and 2003,respectively, increasing by 22.6% and by 25.7% in 2005and 2004, respectively. The consolidated gross marginwas 26.3%, 25.3% and 26.2% in 2005, 2004 and 2003,respectively.

Consolidated operating expenses were $355.4 million,$308.7 million, and $251.3 million, in 2005, 2004 and2003, respectively, increasing by 15.1% and 22.8% in2005 and 2004, respectively. General and administrative(G&A) expenses, which are included in operatingexpenses, were $340.1 million, $293.8 million, and$234.6 million, in 2005, 2004 and 2003, respectively,increasing by 15.8% and 25.2% in 2005 and 2004,respectively.

Consolidated operating income was $87.0 million,$52.1 million, and $35.8 million in 2005, 2004 and2003, respectively, increasing by 67.0% and 45.5% in2005 and 2004, respectively. Operating income as apercentage of revenue was 5.2%, 3.7% and 3.3% in2005, 2004 and 2003, respectively.

SE G M E N TS

Professional Services division North American Professional Services segment Revenue in our North American Professional servicessegment was $537.3 million, $429.6 million, and$315.8 million, for 2005, 2004 and 2003, respectively,increasing by 25.1% and by 36.0% in 2005 and 2004,respectively. Professional Acquisitions contributed$47.5 million, $60.6 million, and $19.6 million inrevenue in 2005, 2004 and 2003, respectively. Thefollowing contributed to the increase in revenue forboth 2005 and 2004: we executed on our acquisitionstrategy; we made considerable investments in sales andrecruiting staff; and we introduced additional serviceofferings. We completed nine acquisitions from 2003to 2005, and between these acquisitions and internalstaff investments, we increased our staff headcount by51% from 2003. The internal staff investments were inanticipation of increased demand and were coupled with

22 MPS Group

the added service offerings to our Special Counsel,Accounting Principals, and Soliant Health businessesin 2004.

Revenue contribution in the North AmericanProfessional services specialties for 2005, 2004 and2003 was as follows:

2005 2004 2003 Entegee 45.7% 49.6% 56.9%Special Counsel 24.1 24.5 24.8Accounting Principals 17.6 13.3 9.6Soliant Health 12.6 11.7 6.2Other 0.0 0.9 2.5

Gross profit in our North American Professional servicessegment was $160.4 million, $123.8 million, and$89.1 million, for 2005, 2004 and 2003, respectively,increasing by 29.6% and by 38.9% in 2005 and 2004,respectively. Professional Acquisitions contributed$17.0 million, $19.7 million, and $6.1 million in grossprofit in 2005, 2004 and 2003, respectively. Gross marginin our North American Professional services segmentwas 29.9%, 28.8% and 28.2% in 2005, 2004 and 2003,respectively. The increase in gross margin in 2005 wasdue primarily to an increase in direct hire fees, and to alesser extent, improved gross margins from the segment’sstaffing services. The increase in gross margin in 2004was due primarily to an increase in direct hire fees.Direct hire fees, which generate higher margin, increasedto 5.6% of the segment’s revenue in 2005, from 4.5%and 3.6% in 2004 and 2003, respectively.

G&A expenses in our North American Professionalservices segment were $110.8 million, $88.4 million, and$69.3 million, in 2005, 2004 and 2003, respectively,increasing by 25.3% and by 27.6% in 2005 and 2004,respectively. As a percentage of revenue, G&A expenseswere 20.6% for 2005 and 2004, and 21.9% for 2003.The increase in G&A expenses for both 2005 and 2004was due primarily to the increase in compensationexpense related to the increases in the segment’srevenue, our investment in additional sales andrecruiting personnel, and additional G&A fromProfessional Acquisitions.

Operating income was $44.5 million, $30.9 million, and$16.0 million in 2005, 2004 and 2003, respectively,increasing by 44.0% and by 93.1% in 2005 and 2004,respectively. Operating income as a percentage ofrevenue was 8.3%, 7.2% and 5.1% in 2005, 2004 and2003, respectively.