EUROPEAN PARLIAMENT Scientific Technology Options Assessment S T O A Galileo Applications STOA Workshop Report (Workshop held in Brussels on 13 September 2006) IPOL/A/STOA/WS/2006-007 PE 375.883

Transcript

EUROPEAN PARLIAMENT

Scientific Technology Options Assessment

S T O A

Galileo Applications

STOA Workshop Report

(Workshop held in Brussels on 13 September 2006) IPOL/A/STOA/WS/2006-007 PE 375.883

The "Galileo Applications" workshop, organised by the European Parliament's Scientific and Technology Options Assessment Panel (STOA), was held on 13 September 2006. Only published in English. Author: ETAG

European Technology Assessment Group Institute for Technology Assessment & Systems Analysis (ITAS) Danish Board of Technology (DBT) Flemish Institute for Science and Technology Assessment (viWTA) Parliamentary Office of Science & Technology (POST) Rathenau Institute Dr Leonhard Hennen, ITAS

Administrator: Theo Karapiperis Policy Department A - Economy and Science Internal Policies Directorate-General European Parliament Rue Wiertz 60 - office number B-1047 Brussels ATR 0L004 Tel: +32-2-2843812 Fax: +32-2-2849002 E-mail: [email protected] Manuscript completed in January 2007. The opinions expressed in this document do not necessarily represent the official position of the European Parliament. Reproduction and translation for non-commercial purposes are authorised provided the source is acknowledged and the publisher is given prior notice and receives a copy.

Rue Wiertz – B-1047 Bruxelles - 32/2.284.43.74 Fax: 32/2.284.68.05 Palais de l‘Europe – F-67000 Strasbourg - 33/3.88.17.25.56 Fax: 33/3.88.36.92.14

Executive Summary The present paper provides the documentation of a Workshop on the perspectives of the European Galileo satellite navigation system which took place at the European Parliament on September 13th, 2006.

The Galileo Programme – a joint initiative of the European Community and the European Space Agency – is a European infrastructure project with a great potential for the European economy. The system is meant to ensure Europe’s competitiveness in a global market in satellite navigation products and services. It is planned to be interoperable with the existing global satellite navigation system GPS (USA). It will, however, – other than GPS – be under civilian control and will provide a high level of accuracy, integrity and authentication of signals. The total public sector money committed so far for research and development activities by the EU and ESA is in the range of 2.5 billion €.

The workshop has been prepared by means of a questionnaire sent around to selected experts and by a background paper that was meant to illustrate different opinions and statements, which play a role in discussions about the programme. It was the objective of the workshop to clarify the validity of different statements and to provide the latest, up-to-date view on the Galileo programme and its perspectives. The discussion during the workshop made obvious that the Galileo project has entered a phase which is decisive for its further development and the realisation of its economic potential.

It was pointed out that the Galileo programme can be regarded in the same line as the development of the mobile phone or the internet. Markets for the use of satellite navigation services by consumers, public authorities and industry are currently emerging. More than 150.000 jobs are expected to be generated in downstream industries of Galileo applications and services. For 2025 the global market for satellite navigation is expected to comprise a couple of hundred billion euros annually.

The currently running negotiations on the terms of a Public Private Partnership (PPP) are decisive for the further progress of the programme. With the signature of a concession contract scheduled for 2007 the responsibilities for the further development of Galileo will be handed over to a private consortium.

The main subject of negotiations is risk sharing. It has been agreed that some of the risks have to be retained mainly by the private concessionaire. Negotiations are underway on the allocation of market risks (uncertainty about the amount and timing of revenues), replenishment risks (in view of uncertainties of technology and market environment) and third party liability risks between the private and the public side.

The experts present at the workshop were confident that they would bring negotiations to a successful closure. Apart from an agreement on risk sharing there are, however, some other issues that have to be clarified and problems to be solved.

IP/A/STOA/WS/2006-007 Page i PE 375.883

Among these are:

The terms of the hand-over of the system developed so far by ESA from the public to the private partner have to be settled.

Continuity of the development process has to be ensured, since technical capacities built up by European industry companies involved have to be maintained.

Commitments for covering costs have to be made. For the deployment of the full system a cost sharing scheme of 2/3 of costs covered by the private partner and 1/3 by the public partner was foreseen (total costs estimated to comprise 2.3 billion €). This cost sharing model is still regarded to be valid. However experts expect that plans have to be made for additional costs, which were not subject of calculation in the original business plan.

It is decisive for the programme that co-operation with international partners be extended, since Galileo is designed to be a global system.

There are a couple of policy issues to be addressed in order to support the development of the Galileo by an appropriate regulatory environment.

The European Commission (EC) will inform the Council and the Parliament on the features of the PPP scheme by the end of 2006. Part of the communication from the EC will be a request for budget, as well as a request to approve a number of financial mechanisms arising from the commitment of the public sector for a period of 20 years.

IP/A/STOA/WS/2006-007 Page ii PE 375.883

Contents

Executive Summary…………………………………………………………….iii

Contents…………………………………………………………………………iii

I. Documentation of the Workshop……………………………………………....1

1. Programme of the Workshop……………………………………………..1 2. CVs of Speakers…………………………………………………………..2 3. Minutes of the Workshop…………………………………………………4 4. Background Paper Prepared for the Workshop………………………….15

II. Briefing Note for MEPs……………………………………………………..31

Annex: Slides of Presentations…………………………………………………35

IP/A/STOA/WS/2006-007 Page iii PE 375.883

I. Documentation of the Workshop

1. Programme of the Workshop “Perspectives of the European GALILEO Satellite

Navigation System and its Applications”

Workshop organised as part of the Project “Galileo Applications” commissioned by the Scientific Technology Options Assessment Panel of the European Parliament (STOA) and carried out by the European Technology Assessment Group (ETAG)

Wednesday, 13 September 2006

14.30 – 18.30, Room ASP 5G3

European Parliament, Brussels

14.30 Welcome and Introduction Etelka Barsi-Pataky, MEP, STOA Panel Leonhard Hennen (ETAG) 14.45 – 18.15 Presentations and Discussion moderated by Prof. Günter Hein (University FAF, Munich; Institute of Geodesy and Navigation). 14.45 -15.15 Rainer Grohe (Galileo Joint Undertaking, Executive Director) State and perspectives of the GALILEO programme 15.15 – 15.45 Paul Verhoef (European Commission, DG TREN, Head of Satellite Navigation Unit) Policy issues (Regulations, R&D) 15.45 – 16.15 Giuseppe Viriglio, (ESA, Director of European Union and Industrial Programmes) Didier Faivre (ESA, Head of Navigation Department) EGNOS and GALILEO – achievements and perspectives - Break - 16.30 – 17.00 Mark Dumville (Nottingham Scientific Ltd, General Manager) Scope of possible applications and competition with GPS 17.00 – 17.30 Stefan Sassen (TeleOp GmbH, Managing Director) The Implementation of the Galileo Concession 17.30 – 18.15 General Discussion 18.15 – 18.30 Etelka Barsi-Pataky, MEP Concluding remarks

IP/A/STOA/WS/2006-007 Page 1 of 73 PE 375.883

2. CVs of Speakers Etelka Barsi-Pataky is a Hungarian member of the European Parliament's STOA Panel. As a civil engineer she is active in the EP's Committee on Transport and Tourism, further in the Committee on Industry, Research and Energy. After several research fellowships in her profession (e. g. Hamburg, Helsinki, Otaniemi) Mrs Barsi-Pataky worked as Principal Private Secretary in the Hungarian Ministry of Transport and Titular Undersecretary of State in the Ministry of Economic Affairs in the early 1990's. Hungary's former Ambassador to Austria became the member of the European Parliament in 2004. Mark Dumville is General Manager of Nottingham Scientific Ltd, where he is responsible for strategic planning and business development. He is currently working on projects relating to the use of the GNSS for aviation, maritime, rail and road applications. He has over 10 years of experience in developing and supporting applications of GNSS technology. Mark's main interests relate to addressing the technical and operational challenges facing different user communities in their transition to satellite navigation systems. Rainer Grohe became executive director of the Galileo Joint Undertaking in June 2003. As head of the organization he manages development of Europe’s Galileo satellite navigation system. Mr Grohe studied electrical engineering and was graduated as an engineer from Aachen Polytechnic University. His professional career in private industry began in 1964. Since then he has held management positions at ABB and VIAG, working in areas involving power systems, metallurgical products, and transport services. He also serves as the deputy chairman of the German Council for Sustainable Development and is a member of several supervisory boards. Günter Hein is a university professor of Geodesy at FAF Munich and head of the Institute of Geodesy and Navigation there. From the late 1990's Mr Hein became Dean of the Faculty of Civil Engineering, Surveying and Geodesy in Munich. Beginning from the 1980's he worked as Visiting Senior Scientist at the U.S. National Geodetic Survey, further at the University of New South Wales, Sydney and at the University of Maine, USA. He is member of various national and international associations. Mr Hein published more than 185 scientific publications on Geodesy and Navigation, and received more than 100 research grants. Leonhard Hennen works as a coordinator of the European Technology Assessment group (ETAG) and is senior researcher at the Institute for Technology Assessment and Systems Analysis in Karlsruhe. His scientific publications include the topics of participatory methods in technology assessment, the wider perspectives of technology assessment in Europe, the questions of the relationship between democracy and the internet, further biomedical and bioethical issues in parliamentary TA and in health technology assessment. Stefan Sassen studied Physics and made his Ph.D. in Electrical Engineering. He joined DaimlerChrysler/DASA in 1995 working in various positions in the Corporate Research Centre including research assignments in Toulouse, France and Sendai, Japan. His research work focused on microwave and navigation technologies and the development of autonomous air-vehicles. Since 2002 he is dedicated to Satellite Navigation and Galileo. Since 2005 he is Managing Director of TeleOp GmbH, a shareholder of the Galileo concessionaire and operator of the Galileo infrastructure.

IP/A/STOA/WS/2006-007 Page 2 of 73 PE 375.883

Paul Verhoef is head of the unit for satellite navigation at DG TREN of the European Commissioan. For the past decade, Paul Verhoef has been working for the European Commission in various capacities. Most recently he has been with the DG Information Society in Brussels. Here, he directed a team with responsibility for international policies in telecommunications, Internet, e-commerce, and Information Society. Mr. Verhoef also worked as Advisor to the Director-General and was a staff member of Commissioner Martin Bangemann for the European Commission. Mr. Verhoef’s background and experience also include project management for the European Space Agency, engineering management for Eutelsat in France and the International Telecommunication Union for the Pacific Regional Development Programme.

Giuseppe Viriglio of the European Space Agency was appointed Director of European Union and Industrial Programmes (D/EUI) in June 2004. Mr. Viriglio was awarded a doctorate in aeronautical engineering from the Polytechnic of Turin. Most of his career has been spent within the aerospace industry where he has held increasingly senior positions. At Aeritalia he led the Space System group and at Alenia Spazio the last position he held was CEO. Before joining ESA, he also served as Vice CEO of Galileo Industries. During the time spent working in the Italian industry he worked on a number of European projects such as Spacelab and Columbus.

IP/A/STOA/WS/2006-007 Page 3 of 73 PE 375.883

3. Minutes of the Workshop The workshop was chaired by Mrs. Etelka Barsi-Pataky, MEP, and moderated by Prof. Günter Hein, University FAF Munich. A short introduction was given by Leonhard Hennen (ETAG). 3.1 Presentation by Rainer Grohe (Galileo Joint Undertaking)

The tasks of the Galileo Joint Undertaking (GJU) are: to manage the development phase of Galileo, to manage Galileo related parts of the 6th Framework Programme, to attract private investors and non-European partners, to integrate the EGNOS system, to elect the concessionaire and negotiate the concession contract and at the end: to transfer the ownership of the system to the GNSS (Global Navigation Satellite System) Supervisory Authority (GSA).

The Galileo Programme is currently in the development phase (first test-satellite has successfully been launched in 2005). The programme will enter the so called In-Orbit Validation (IOV) phase in 2008 (including the launch of the first 4 Galileo-Satellites). The “Galileo Full Operation Constellation” will be reached in 2010; the system will be fully operational at the beginning of 2011. It is often asked whether Galileo will not be too late in the market. An answer to this is that the next improved GPS version is scheduled to be operable in 2015.

GPS is an open system; it offers the open signal but does not guarantee it. GPS as a military system will not guarantee this for civil users. The US authorities will keep the right to switch the system off when they feel at risk. Galileo will also offer guaranteed services which is a crucial feature for safety relevant applications, e.g. aviation.

The European satellite navigation augmentation system, EGNOS, will be fully operable in March next year. EGNOS delivers accuracy in the range of 1 meter for Europe. Galileo will provide this level of accuracy and even a better one worldwide.

With its broad scope of applications Galileo will contribute to the realisation of the Lisbon strategy by prompting investments in research and development and by the programme’s international scale. It is expected that 150,000 jobs can be created in Europe. GJU is convinced that in downstream industries many more jobs will be created via new applications.

Before GJU was established it had been decided to run Galileo under the scheme of a Public Private Partnership. Currently the programme is in the middle of the concession process (i.e. preparing a contract with a consortium of bidders, the private partner). The private partner is asked to mainly finance, operate, maintain, replenish and commercially exploit the system for twenty years. Revenues of the private partners will be partly shared with the public partner.

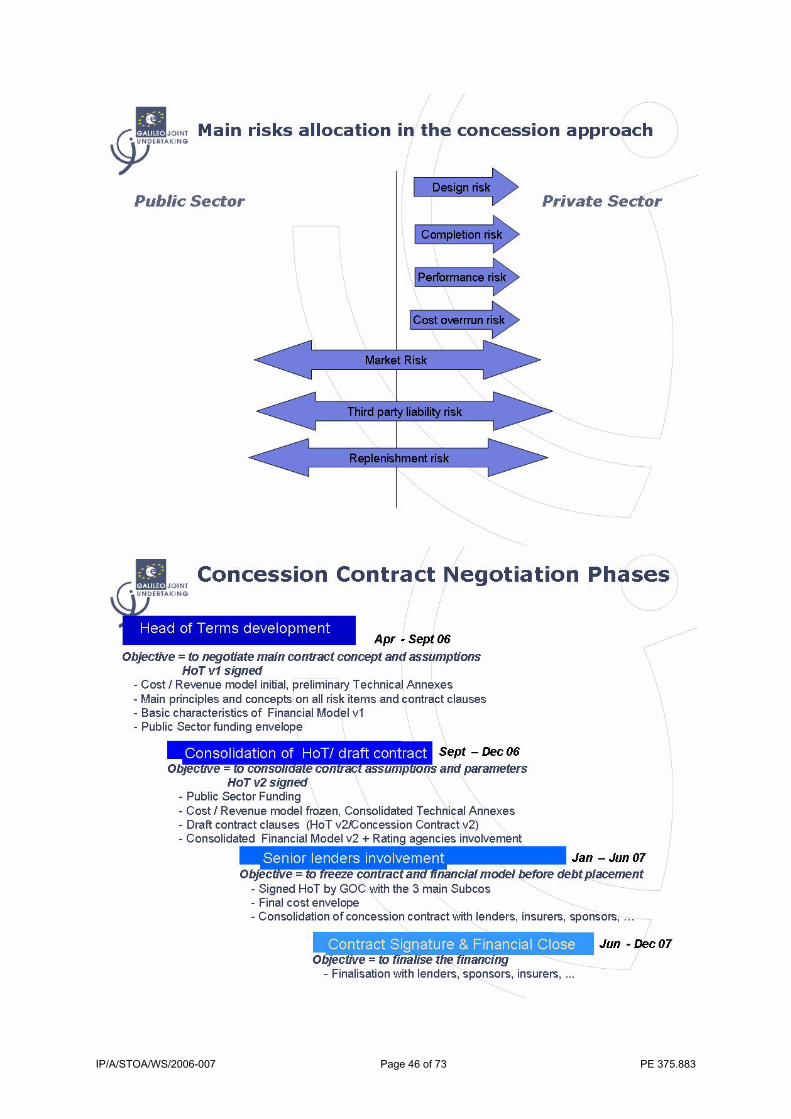

The concession scheme is demanding and so is the current negotiation process, which is mainly about risk sharing. Risk should be retained by the party which is best capable to manage it.

After a call for an expression of interest (in 2003/2004) 74 parties expressed their interest for the concession. In a process of down-selection two consortia remained which then merged to one consortium which currently is negotiating the concession contract with GJU. On 27th June 2005 the joint proposal was accepted by GJU since the merging of bidders creates benefits for the public side.

IP/A/STOA/WS/2006-007 Page 4 of 73 PE 375.883

The time schedule for running negotiations is as follows: It is planned that in December 2006 a Head of Terms agreement (HoT) will be signed, which indicates the key elements of the coming concession contract. In the course of 2007 the details of the contract will be negotiated. The financial close and the signature of the concession contract are foreseen for the end of 2007. It is crucial that the contract provides value for money and affordability for the public sector, that discontinuity between project phases (In-Orbit Validation to Full Operable Constellation) is avoided and that bankability of the business case is achieved.

The public side as the owner of the system has to provide some comfort to the lenders (banks) that in case the system fails, their loans are secure. Public underpinning reduces the costs for financing. As a balance for this, GJU asks the bidder for the concession to increase its equity in the special purpose company (Galileo Operating Company: GOC) which will execute the contract.

The central subject of negotiations is risk allocation (agreements on this will be the main features of HoT). Difficulties include the transfer of tasks from the public to the private sector. For example design risk: The design of the system has been made by ESA but the concessionaire has to stand up for it.

Market risk: GJU believe in a big market for Galileo but markets will appear in connection with the application. So far only the marketing of the signals is part of the revenues which are generated by GOC. The concessionaire is encouraged to develop applications down the value chain (he has to treat his subsidiaries who develop applications in the same way as he treats other users of signals). So far there is no market for satellite navigation applications since GPS is free. Support is needed from policy making institutions in the area of regulated applications.

Whereas there is an agreement that the private sector will take the design risk, the completion risk, the performance risk and the cost overrun risk, schemes of risk sharing for other risks have still to be negotiated. Risk sharing schemes have to be accepted for market risks, third party liability risks and replenishment risks.

Head of Terms: at the end of 2006 all key elements of the contract will be in place. After that the elements of HoT will be transferred into a legally binding contract (implementation). Financial close: both sides will have to make available their financial resources. The private side will have to find lenders for financing the operation of Galileo. The lenders will ask that the public side is in a position to deliver what they are supposed to deliver.

The concession contract is for a period of 20 years. This is “a sensitive issue”: The public side has to accept commitments for this 20-year period of time.

The integration of international partners is crucial since Galileo is planned to be a global system. Contracts have been signed with the US, China, Israel and theUkraine. Negotiations with many other partners (worldwide) are running. Galileo will be a success and can already be called a success if one considers the worldwide recognition of the system.

IP/A/STOA/WS/2006-007 Page 5 of 73 PE 375.883

3.2 Statement of Giuseppe Viriglio (ESA)

ESA’s current responsibility is the design and launch of the test satellites, the design and launch of three to four IOV-satellites as well as the designing of the complete ground infrastructure, which will be used in the deployment phase. Thus ESA’s current work forms the basis of any future development.

The design work has been completed. The procurement for the IOV satellites is almost completed. This includes 200 contracts for a value of around 1 billion. The first prototype of the Galileo satellite is under production. International contracts are concluded. A delay for the start of IOV is not expected.

At the end of the year EGNOS will undergo its final qualification review for utilisation. Other augmentation systems like the American WAAS do not provide a quality and capability comparable to EGNOS. Europe is ahead of the rest of the world.

The concessionaire will have to share the design approach selected by ESA (problem of design risk). In order to have a smooth transition from one phase to the other a clear division of responsibilities and risk sharing between the public and the private partner is needed. The future responsibilities of ESA have to be clarified (in case of malfunctioning, modifications of the system).

Upcoming tasks:

1. All has to be done so that expectations are fulfilled. EGNOS has to be further developed.

2. A system of transfer of the expertise that has so far been established in the deployment phase has to be developed. Expertise on the industrial side in Europe has been built up and care has to be taken that this is not lost due to discontinuity of the programme. ESA cannot start a new process of implementing technologies (costs, capabilities are lost). Too wide a gap between IOV and the Full Operable Constellation (FOC) will be detrimental because capabilities built up within the industries cannot be maintained. More than one hundred companies are involved in Europe.

3. Complete the plan of utilisation. For further development an assessment of the final requirements from the final user is needed – at least from the public side.

4. Prepare for the future: There are competitors and that is GPS III (which is planned to become operable in 2015). At the moment this causes no problems however.

IP/A/STOA/WS/2006-007 Page 6 of 73 PE 375.883

3.3 Statement of Paul Verhoef (European Commission)

Challenges connected to the Galileo programme are tremendous, technological as well as economic. The success of Galileo has to be seen in the same line as the development of the mobile phone, the personal computer and the internet. Satellite navigation will change our everyday life. The use of location data on the internet has already been started.

The complexity is made up (apart from technical challenges) by the scope of partners involved: ESA, the EC, 25 Member States, many industrial enterprises.

The programme is in a “critical phase”. An agreement on the Head of Terms is needed to move ahead with the project.

Based on this agreement (Head of Terms) the EC will inform the Council and the Parliament and request their agreement to move ahead, i.e. to allocate the necessary budget to the project. In this process the Council and the Parliament will then need to judge, indeed: is this project meeting our ambitions? It will be the EC’s task to prove that the agreement reached is the best that can be achieved for the moment. The question for the Council and the Parliament will be: Is that good enough?

The total public sector money committed for research and development activities by the EU and ESA is in the range of € 2.5 billion. Thousands of people are working on the system. The organisations involved are responsible for making Galileo a success.

Part of the foreseen communication of the Commission to the Parliament (after completion of the Head of Terms) will be a request for budget, as well as a request to approve a number of financial mechanisms connected with the 20 years of financial commitment to the system. The EU will be the owner of the system; this includes responsibilities which have to be transformed into contractual commitments.

The focus of PPP is on risk sharing which is a “delicate process”. There is still much work to be done but there is hope that the Head of Terms will be completed by the end of this year.

Galileo is not a “space project” but a project to make available a tool for the economy. In the next phase the focus has to be on applications. A Green Paper on applications will be provided by the end of this year.

The real macro economic value of the project is in the downstream markets. For 2025 a global market for satellite navigation applications is expected to comprise 400 billion € annually.

Issues of standards and certification have to be considered as well as the adaptation of national law in several fields of application.

There is the question of data protection and privacy: “We don’t know quite yet, but it need definitely to be looked into. It is an issue and it needs evaluation”. The Green Paper will also touch on this problem. The Green Paper is part of the EC’s proposal of a policy way to support the development of applications.

IP/A/STOA/WS/2006-007 Page 7 of 73 PE 375.883

In the 7th Framework Programme 350 million € in 7 years are foreseen for R&D in satellite navigation and applications. The management of this programme will be carried out by GSA on behalf of the Commission.

International dimension: The cooperation with the US is running very well. The US has come to appreciate Galileo as a driver of a commercial market for satellite navigation. Recently a joint recommendation for a new open signal for both systems has been achieved. International agreements are important. The EC expects that a critical mass of partners – 12 to 15 partners – some with large markets and expertise will soon be achieved. Modalities of participation of partners in the GSA as the owner of the system have still to be clarified.

The central problem is to keep the programme realities synchronized with the institutional realities: i.e. milestones have to be achieved. If milestones are not met, problems will arise (ref. to Mr. Viriglio’s remarks). Tight schedule: Institutional approval processes need their time. If however deadlines actually foreseen are missed, an increase of costs will be unavoidable. It is not possible to take two years time for the approval of the concession contract and put everything on ice. If ESA has to freeze the development phase, thousands of engineers have to be put in a waiting loop.

The project will keep partners busy for a long time: new issues, opportunities (technical as well as non-technical) will arise. Not everything has been considered, not all problems have been raised yet. V. encourages the Parliament to raise critical issues.

3.4 Discussion (I)

Question: What is Galileo’s position with regard to GPS?

Paul Verhoef: GPS is going to be modernised, also for civilian systems. But this is nothing to be afraid of. It will push us to do better with the second Galileo generation. For the foreseeable future: The US will improve the signals but not offer the signal on a commercial basis. Galileo is more interesting for services like safety of life services. Features needed here (integrity of the signal) will not be provided by GPS.

Rainer Grohe: We have an agreement with the US on the open signal: The user can have both systems without any cost for using them. The systems are however completely separate. The US are not considering to make GPS a commercial system, thus the differentiators of Galileo will remain in place.

Question: Problems of the PPP: What are the terms of risk sharing and sharing of costs between the public and the private partner?

Paul Verhoef: Negotiations on PPP in the dimension of Galileo are always complex. The problem is (if any) the time schedule. Delays have already been accumulated due to the complexity of the programme. V. however is sure that the time schedule will now be met.

Cost sharing: In terms of pure costs of the system the foreseen cost split of 1/3 public and 2/3 private is still valid. Although this should have been obvious, discussions in the press have included such elements as the costs of financing as well as aspects of risk sharing and underpinning of debts.

IP/A/STOA/WS/2006-007 Page 8 of 73 PE 375.883

Rainer Grohe: The problem of risk sharing is that nobody has any experience with the commercialisation of signals in space. The concessionaire can now expect revenues in the range of 9 to 10 billion € in the period of the concession. This would lead to a situation of a repay of the bigger share if not of all of the public money investments – this is an extremely attractive deal for the public side. The overall cost scheme developed by PricewaterhouseCoopers is still valid. But: In the negotiations today all the elements which have not been addressed in that study have to be dealt with, like e.g. the establishment of a special company by the concessionaire (GOC). This company will be the counterpart to the lending institutions. This company has to be established in order that a bank is ready to grant them a loan of a couple of billion €. The bidders are establishing this company on an equity scheme. The equity has to be in a specific ratio to the loans – this has to be balanced. Another element not foreseen in the beginning, are financing costs for the company taking a loan for investments. If we now see figures that are different from those in previous studies: it is not different, it only includes costs not calculated in studies before.

No delays are expected for the signing of the HoT. The question is how fast the public side will then approve the contract and make necessary commitments, and how easily and fast the lending side can respond. The cost sharing model of 2/3 private and 1/3 public for the Deployment Phase is still valid.

International aspect: Two non-European stakeholders are contributing with money (China: 200 Million €, Israel 18 Million €). The Chinese partners expect participation of their industries in the realisation of the system. It is clear to the partners that they will not have access to core technologies of the system, this will be respected. Galileo is a global system, therefore international partners are necessary. Galileo is planned to become the “default” of navigation systems.

Question: Isn’t PPP the wrong approach? The risk sharing problem shows that Galileo should rather be managed as a public procurement (market risk and revenue risks are held by the public sector anyway).

Rainer Grohe: The decision on PPP has been taken before GJU came in. The private side is actually taking a lot of risks. The market risk: If the public sector is ready to underpin debts, this does not imply that the public sector is taking the risk. This is the last resort to give comfort to the lending institutions that in case the contract must be terminated the public side as the owner of the system would step in guaranteeing that they get their loans back. It is not disputed by either side that the private side will take market risks to a certain extent.

Question: “System completion in 2010”, does this mean that all the five services are ready?

Rainer Grohe: At the end of 2010 the full system will be operable (it has then of course to undergo some testing). Commercialisation may begin a little bit later, beginning of 2011.

IP/A/STOA/WS/2006-007 Page 9 of 73 PE 375.883

Question: Is the PPP suitable for this project? Would it be not much easier with a different framework? It has been said that there cannot be too long a wait for the approval of the contract. The Parliament voted on the Galileo budget in September 2005 and is waiting for a result of negotiations. Shouldn’t we try to create an easier regulation framework?

Paul Verhoef: The question of PPP vs. public procurement is a core issue. But once a scheme has been chosen you cannot easily shift to another one. The decision has been taken on the basis of certain assumptions. Some of them have been changing slightly: There was always the assumption that the industry would take the market risk. Today it is clear that industry is not willing to take 100% of the market risk. This does not imply that the PPP is the wrong approach. Whether another approach is suitable at the moment will require a lot of evaluations, some of which will be done in order to come to an assessment for the approval of the project (by the Council and the Parliament). The EC’s current view is: The PPP is still the appropriate approach.

Delays will have impacts on the budget. Discontinuity and freezing of the progress of the programme would cost a lot of money. So there is a lot of pressure to finalise negotiations but the public side is not willing to accept just any deal. The industry cannot expect that the public side will follow at any price because it has shown itself so much in favour of Galileo.

Easier regulatory framework: On the budget regulatory side there are a lot of new elements that are being studied at the moment. An example: responsibility that has to be taken on third party liability. The concession holder will have to accept a certain share of third party liability. A certain level can be insured. But everything that goes over that, which cannot be insured and integrated in the contract, will automatically fall on the owner of the system. Third party liability commitments have to be foreseen in the budgetary instruments. It is under investigation now how this will be done. To V’s knowledge it is not sure whether this can be done from the EU budget or whether this has to be handed over to the Member States.

Moreover, the lenders expect a clear commitment of the public side for the whole 20-year concession period. There will be a number of challenges. For ITER a commitment has been taken for a period of 3 years; now a commitment for 20 years is needed, which is new in the institutional history.

3.5 Presentation by Mark Dumville (Nottingham Scientific, Ltd)

The core business of NSL at the moment is supporting governmental authorities with regard to public regulated applications of GPS. D. reports mainly on the scope of applications in the context of regulated services in the UK. GPS is widely used by governmental agencies in the U.K. and there are several plans or visions to expand the use of satellite navigation in the U.K.

Performance of GPS has been assessed by NSL. Positioning accuracy is within 3 meters. This is sufficient for many applications; and GPS is free of charge. “So why not use it?”

IP/A/STOA/WS/2006-007 Page 10 of 73 PE 375.883

Applications for government authorities under consideration include the following fields:

Vehicle crime: Tracking of stolen cars, immobilisation of cars dependent on location.

Tracking of cargoes and assets: e.g. petrol cars have to follow certain routes; satellite navigation allows for alarm if they go off these routes.

Electronic monitoring of offenders.

Monitoring of people with dementia.

Replacing the guide dog for blind people.

Aviation: six airports are currently testing the use of GPS (pilots reporting their experiences with GPS). Thomas Cook got the approval to use GPS from U.K. authorities.

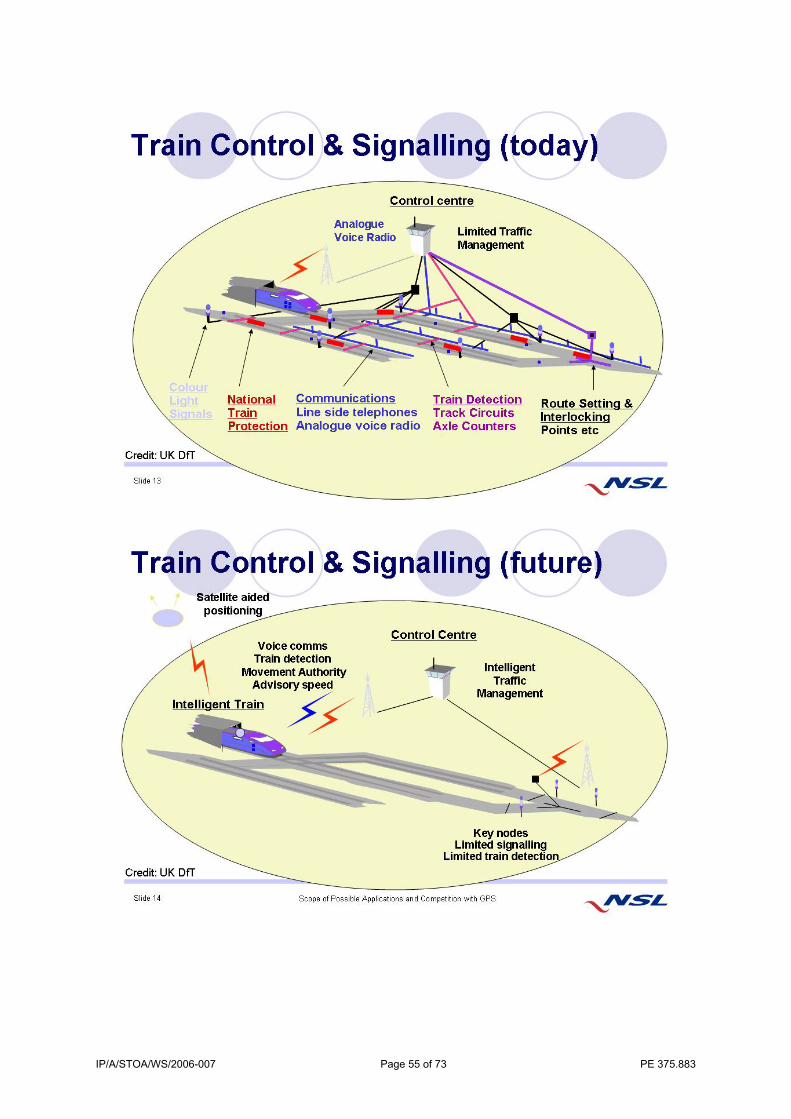

Public Transport: Attempts to use GPS for controlling railway tracks. The Department of Transport is considering handling train control and signalling by GNSS, thus establishing a much more reliable system by implementing most of the intelligence needed directly in the train.

Public Transport: Real time information on bus location for customers at bus stops, tracking buses to give next arrival information, adding location-based advertising on LCDs on buses.

Road Transport: industry and authorities have an appreciation for Galileo but they are not willing to wait for Galileo at all. The Secretary of State for Transport announced 3 billion € two years ago, just to test different ways for road user charging.

Road safety: trials for intelligent speed adaptation; in low emission zones an automatic change to different source of energy can be induced by satellite navigation, intelligent speed adoption of cars depending on traffic situations.

Infrastructure: Locating defects in water, gas, electricity infrastructure.

Performance of GPS: A test of GPS carried out by NSL revealed the weaknesses of the system. There are periods with bad performance (GNSS propagation errors, receiver errors). Problems emerge from the fact that the signal has to go through the atmosphere, because of errors due to solar storms, there have been times when GPS was not available at all. The technology to get around problems of accuracy or availability is not widely deployed (augmentation systems). Thus it is unlikely that public authorities channel all their activities on GPS.

The potential for Galileo is to provide signals that avoid problems GPS causes. There is no direct competition between GPS and Galileo, but better signals, robustness and guarantee of services will be decisive to make applications run.

A problem is that people interested in applying satellite navigation need reliable information on the Galileo time schedule.

IP/A/STOA/WS/2006-007 Page 11 of 73 PE 375.883

3.6 Presentation by Stephan Sassen (TeleOP)

TeleOp is one of the eight shareholders of the concessionaire.

The private side of the PPP will have to establish the Galileo Operating Company (GOC). GOC will be financed by sponsors via equity as well as by lenders. GOC has to make contracts with service providers, has to guarantee services and performance of the system. With regard to discussions on the need for a PPP it has to be taken into account that this would not be feasible under a public procurement scheme.

The procurement of the system done by GOC comprises three main tasks: 1. Launch services (together with Arianespace), 2. Infrastructure deployment (together with Galielo Industries); 3. Operation and maintenance. The procurement pillars will be covered by the eight companies of the consortium in a kind of division of responsibilities (see slide “Galieleo Concession Structure”).

The Head of Terms (a kind of pre-contract) will be finalised end of this year. The concession contract will be roughly around 10,000 pages long. Beyond that there are a couple of hundred subcontracts to be prepared in order to implement the deployment and the operation of the infrastructure. Every change in the “hinge” (the concession contract) will have implications for subcontracting. It is therefore essential that from a certain point in the negotiations (which is now) the main boundary conditions have to be fixed. Negotiations are now well on the way to the Head of Terms, which will allow industry to go into more detail with regard to the necessary subcontracts.

Galileo with a relatively low € 7 billion of costs during the whole concession period, should always be seen together with the expected yearly turnaround of a couple of hundred billions in the applications market. Industry still believes that the benefit is in the applications sector. The “space companies” now involved in the development of the infrastructure will be a minority when the system is running. “Galileo” will then be made up by application and service providers.

Regarding revenue mechanisms: It is not a single revenue mechanism that forms the basis of the Galileo business. The consortium expects and has to develop several sources for revenues. Regulated applications have to be done together with the public side. A couple of services will be purely commercial. On other services the public will be the exclusive customer. There is support from the Commission that also third countries can make a contract with the concessionaire on the provision of regional services. The concession bidder is planning for a complex revenue structure - therefore discussions with GJU on who should bear the risk associated with revenue streams are difficult. However, a reasonable scheme for allocation of risks has now been achieved. It still requires a couple of innovative ideas on industries’ side: open service authentication is one key word; here industry probably can link some royalties to the chipsets combined with service guarantees.

Concession negotiations are on risk sharing. One problem is that the concessionaire has to take over an infrastructure that has already been developed by a third party (ESA). This is in a way like taking over a black box. Industry has to make service level commitments before they have the opportunity to really test the infrastructure.

IP/A/STOA/WS/2006-007 Page 12 of 73 PE 375.883

The IOV period (testing) is running until 2009, the concession contract has to be signed in 2007 already. That is why the contract has to have some provisions on responsibilities on IOV performance.

Provisions for the case of termination of the contract and compensation are a sensitive problem: What happens if something goes wrong in the concession, which cannot be excluded for 20 years? A good contract has to take care of this.

Replenishment of the system will be necessary and has to be provided for by industry. However, industry would like to see ESA on board for support.

Third party liability: Industry can cover this only to a certain extent. The public sector has to step in for unexpected issues not covered by insurances.

Challenges of the near future are connected to the following phases of “hand over”:

Hand over from GJU to GSA: continuity with regard to the concession process has to be provided for.

Handover from ESA to GOC (infrastructure): There are no direct contract relations between ESA and the concessionaire so far, but GOC is expected to take over a 1.5 billion € infrastructure from ESA. There should be a contractual relation to regulate this transfer after completion of the IOV.

EGNOS hand-over. EGNOS has a couple of investors and stakeholders. The relations of the partners involved in EGNOS to the GOC have to be clarified.

3.7 Discussion (II)

Questions:

What are the possibilities to support the application of Galileo by legal regulations?

In which way will the concession process continue when GJU ceases its activities by the end of 2006?

In the PriceWaterhouseCoopers study on the Galileo business plan royalties from Intellectual Property Rights on the Galileo chipset have been regarded as being a main source of revenues for the concessionaire. Is this still valid?

Paul Verhoef: There is exploration taking place on how applications can be supported by actions of the public sector both at EU, national and local level. These actions are multiple, including possibly some elements of regulation. The results will be presented in a Green Paper. There are many examples. However, the use of Galileo cannot simply be stipulated (there are international trade commitments; the principle of technological neutrality has to be obeyed). There is a strong recommendation for the use of satellite navigation in the Directive on electronic fee collection (transport). There are, however, considerable difficulties with Member States with regard to agreements on a European standard for fee collection. Member States are inclined to first look on how they can do it on a national basis, and eventually they will talk on how to make this interoperable on a European level.

IP/A/STOA/WS/2006-007 Page 13 of 73 PE 375.883

Mark Dumville: Train control as an example of how to support areas of application by regulation: As part of the European rail traffic management system industry has provided plans for a general architecture for train management but then it is left to the individual companies to develop their own best technical solution. By this a high technological standard can be achieved.

Stephan Sassen: There are problems to raise revenues from IPR related royalties. The technical development is running fast; i.e. IPRs which have been established now may no longer be valuable five years from now. There are ways to circumvent IPRs.

The concessionaire conclusion is: IPRs are a questionable source of revenues. Therefore the concessionaire puts much effort in developing a portfolio of products (currently 21) to back up the revenue stream.

Rainer Grohe: GJU has not given up the idea of commercialising IPR. PriceWaterhouseCoopers has been asked to review their study and to re-evaluate the relevance of IPRs. The agreement with the US on interoperability of the open signal implies that there will be a joint receiver (for GPS and Galileo). The US will not ask for a fee. Therefore it is decisive with respect to royalties and fees that Galileo proves to provide added value for fees connected with the chipset. One important feature is the authentication of the signal, which can be protected by IPR. It would however be risky to rely on IPR alone.

With regard to the handover from GJU to GSA: Both sides have committed to hand over after completion of the HoT. The transfer includes that the core team from GJU moves over to GSA. This is a prerequisite for a smooth transfer and guarantees continuity in the concession process. GSA is already involved in the current negotiations.

Pedro Pedreira (Director of GSA): On the way from the HoT to a fully fledged contract there is much negotiation needed. The stability of the negotiation team is provided for. The hand-over from GJU to GSA will not cause a slow-down in the negotiation process.

IP/A/STOA/WS/2006-007 Page 14 of 73 PE 375.883

4. Background Paper Prepared for the Workshop

Perspectives of the European Galileo Satellite Navigation System and its Applications

Background document for the STOA Workshop "Perspectives of the European Galileo Satellite Navigation System and its Applications" 13 September 2006, 14:30-18:30 Room ASP 5 G-3, European Parliament, Brussels The workshop is part of the project “Galileo Applications” commissioned by STOA and carried out by ETAG

IP/A/STOA/WS/2006-007 Page 15 of 73 PE 375.883

Preface This paper has been produced to give background information and input for the STOA-Workshop “Perspectives of the European Galileo Satellite Navigation System and its Applications” (13 September 2006, European Parliament).

The paper draws to a great extent on answers to a questionnaire on the current status and perspectives of the Galileo programme developed by the author and sent to a selected group of experts. The author would like to thank the following persons for their support:

Mark Dumville, NSL

Paul Flament, DG TREN

Rafael Lucas-Rodriguez, ESA

Hans Marchlewski, GJU

Stefan Sassen, TeleOp

Martin-Ulrich Ripple, EADS

The opinions expressed in this document do not necessarily represent the position of the above mentioned experts.

IP/A/STOA/WS/2006-007 Page 16 of 73 PE 375.883

Contents 1- Introduction 2- The Galileo Programme 3- Galileo and GNSS 4- Galileo Services, Applications, and Markets 5- Galileo Business Case 6- Legal Aspects 7- Questions for the Workshop 8- Related Documents

IP/A/STOA/WS/2006-007 Page 17 of 73 PE 375.883

Note for the reader: The following pages do not claim to provide a validated assessment of the perspectives of the Galileo Programme. This report is - apart from a description of the major features of the programme - meant to illustrate different opinions and statements, which play a role in discussions about the programme and which have been drawn from the documents listed in the annex and from input provided by an expert questionnaire. It is the objective of the workshop to clarify the validity of different statements and to provide the latest, up-to-date view on the Galileo programme and its perspectives.

1. Introduction

The Galileo Programme is a joint initiative of the European Community and the European Space Agency to provide Europe with its own independent global satellite navigation system. The Galileo satellite system will allow users to pinpoint their location at any time to a high degree of accuracy. The system is meant to ensure Europe’s competitiveness in a global market in satellite navigation products and services. It is planned to be interoperable with the existing global satellite navigation system GPS (USA). It is regarded as being Galileo’s advantages compared with GPS to provide for a high level of accuracy and to be under civilian control. When fully deployed, Galileo will consist of a constellation of 30 satellites in 3 orbits, the signal will be worldwide available with high integrity and authentication.

The range of commercial applications of satellite navigation systems is broad and so is the expected market potential of Galileo: It can offer applications, products and services for use in transport, telecommunications, fisheries and agriculture, civil protection, building, environmental protection and others. The biggest market is estimated to be services for transport (electronic charging, route guidance, fleet management, Advanced Driving Assistant Systems) and for private mobile phone applications (e.g. location based information services). The economic potential of the Galileo system, the perspectives for European industry to take a good share of the developing global market for satellite based navigation services as well as for the related upstream industries appear to be extraordinary. Due to remaining uncertainties and economic risks it is a subject for discussion to what extent the impressive range of possible applications will be realised and will be commercially successful.

2. The Galileo Programme

The EU and the European Space Agency agreed in 2003 on the scope and the budget of the Galileo programme. In the same year the partners founded a private company, Galileo Joint Undertaking (GJU), which is responsible for managing the Galileo system during its development phase. This phase includes the launching of two test satellites (in 2005/2006), 4 Galileo satellites and related ground segments and is funded by ESA and the EU together with approx. 1.5 billion €. Main contractor is Galileo Industries.

One of the main tasks of GJU is to manage the programmes development phase and carry out the procedure to select the future concessionaire. For this purpose a call for tenders for a private partner responsible for developing and operating Galileo on the basis of a concession scheme was launched in 2004. Negotiations by GJU regarding the concession with a consortium of private companies comprising the main actors in European space and satellite navigation industry are currently running.

IP/A/STOA/WS/2006-007 Page 18 of 73 PE 375.883

Purpose is to conclude the major items by the end of this year, financial close and signature of the contract are scheduled for the second half of 2007.

At the core of the development phase is the In Orbit Validation (IOV) of the Galileo satellite system. This includes the launching and testing of the first 4 Galileo satellites together with the set up and testing of the most important ground segments. According to the Galileo Mission High Level Definition Paper of the EC (2002) the IOV originally was scheduled to be finished by the end of 2005. It is now scheduled to be completed by the end of 2008.

At the end of 2006 GJU will be closed and the Galileo Supervising Authority (GSA) will take over the remaining tasks. The director of GSA was appointed in 2005. The authority is currently being built up and will be the owner of the Galileo system. GSA as the owner of the satellite system will control the fulfilment of the contract with the private partner.

The deployment phase now scheduled to be completed by 2010 (originally 2007) will include the completion of the full set up of 30 satellites and ground control centres in Germany and Italy. It is planned that 2/3 of estimated total costs (2.3 billion €) will be covered by the private concessionaire. The concessionaire is expected to develop and exploit the commercial use of Galileo. It is planned that private suppliers for Galileo services and for end devices will have to pay royalties and fees to the concessionaire. Revenues from these sources should also cover estimated costs of 220 Mio p.a. for replenishment and maintenance of the system after its completion in 2010.

3. Galileo and GNSS

Galileo is designed to be interoperable with the existing American satellite system GPS but will as well be an independent European contribution to the world wide satellite navigation system GNSS (Global Navigation Satellite System). EGNOS, the European Geostationary Navigation Overlay Service, which commenced to provide signals in 2005, will be operated in conjunction with Galileo.

GLONASS The Russian GLONASS satellite system initiated by the Soviet armed forces was planned to reach its full constellation of 24 satellites in 1995. Partly due to short life span of satellites the originally planned full constellation has never been realised. However, the Russian Government has initiated a programme of replenishment and modernisation of the system. The current constellation of 17 satellites includes 4 satellites of the modified GLONASS-M design (longer life span, additional civil ranging code). GLONASS-K satellites with enhanced features are currently under development and the launch of the first of 27 satellites is planned for 2008.

GPS The GPS system was developed by the US Department of Defense (DoD) and is currently managed by the GPS Joint Program Office (JPO). The JPO aims to ensure the system is continuously available, originally for the US and allied military users. From the beginning of the 1990s however a degraded signal for open use was provided. GPS so far is the system applied for navigation and positioning all over the world and the main supplier for increasing civilian demands for the continuous provision of position, navigation and timing services. Whereas the basic system has changed very little, there have been a series of improvements of services for the civil user community.

IP/A/STOA/WS/2006-007 Page 19 of 73 PE 375.883

In 1998, the addition of a second civilian GPS signal to improve accuracy and reliability for civilian users was announced and in 2000 the degradation of the standard positioning service was removed. By this the performance of GPS has been improved to accuracy levels that proved to be acceptable for consumer applications with noticeable effects for the application market.

The GPS modernisation period has begun with the launch of the first of eight modified Block IIR satellites (Block-IIR-M) in September 2005. It is planned to successively improve the GPS service in terms of accuracy, availability and integrity of the signal. The first GPS Block IIF satellites are scheduled to be launched in 2006/2007 and will provide a signal with higher signal power and wider bandwidth. Final operational capability for the currently developed GPS III satellite system is anticipated after 2015.

EGNOS The European Geostationary Navigation Overlay Service (EGNOS) is a regional European Satellite Based Augmentation System (SBAS) designed for transmitting a signal containing information on the reliability and accuracy of the positioning signals sent out by GPS. Comparable regional augmentation systems are ready or under construction in Japan, the U.S and India. EGNOS is regarded as being both “… a precursor to Galileo and (as) an instrument enabling Galileo to penetrate rapidly the market for satellite radio-navigation services” (EU Council Conclusions of 5 June 2003, cf. GJU n.d., p. 3). EGNOS will provide an Open Service for free, a commercial service and a safety of life service with very high accuracy of positioning for application in aviation, maritime, rail and road navigation. EGNOS will allow for accuracy of positioning up to 1-3 meters and will provide an integrity signal when the quality of the signal is low. These are features also regarded as main advantages of Galileo.

EGNOS consists of 34 ground based Ranging and Integrity Monitoring Stations (RIMS) receiving GPS signals and three geosynchronous satellites. Initial operations of EGNOS commenced during 2005 and it is expected that the open service will become available during 2006 with full EGNOS operations, including the safety of life service, expected to start during 2007. It is planned that until 2008 EGNOS will be made available for other regions of the world.

Galileo From the start of the Galileo programme it has been held to be a decisive advantage of Galileo as a new system to deliver a more accurate and reliable signal than the older GPS. Galileo is planned to offer instantaneous positioning services at the metre level, as a result of better clocks, dual frequency and enhanced navigation algorithms. Apart from that Galileo will provide an integrity signal, which informs users about the reliability of the provided signal. It is also expected that signal authentication of satellite navigation systems will be required for many services in order to ensure that the source of the satellite signaling is not from a simulator but genuine. Galileo is planned to provide authentication of the delivered signals for several services, where authentication is crucial for financial (e.g. toll collection) or security reasons (Pozzobon et al. 2004).

Since GPS has been and is successively modernised in the course of replenishment it has been regarded decisive for Galileo to become operable in due time before GPS III will have reached technical standards comparable to Galileo. The US programme for expanding and modernizing GPS can be regarded as being for a great part triggered by Europe’s Galileo-Initiative.

IP/A/STOA/WS/2006-007 Page 20 of 73 PE 375.883

It is now expected that in terms of accuracy GPS III and Galileo will be comparable by 2015. In this respect it might be a point for discussion to what extent a delayed operability of Galileo could be detrimental to Galileo’s success in the international market for satellite navigation.

After the successful agreement between the EU and the US on the cooperation of GPS and Galileo (in June 2004), however, the development of Galileo must not be regarded as being competitive to GPS since both systems may benefit from each other. Signals sent out by Galileo and GPS are compatible to each other. Combined Galileo and GPS constellation may be even more attractive for end users and be able to prompt the establishment of new markets. This leads to the assumption that in the future all users will look for a combined use of GPS and Galileo signals.

Apart from synergies of GPS and Galileo it is seen as being a major advantage of Galileo that it will provide additional value via the global integrity signal.

Another important argument which was made at least at the beginning of the Galileo programme for the launching of a separate global Satellite navigation system has been the need for independence of the US. As has happened during the first Gulf war the U.S. in case of a crisis situation may decide to encrypt the GPS signal or otherwise disable civilian use of the signal. Apart from political and military reasons this uncertainty regarding the continuous provision of the positioning signal has been regarded as a major barrier for the development of application markets.

Last but not least launching of an own European satellite navigation system with global availability is regarded as an indispensable precondition for assuring a leading position of European satellite and downstream industries in the expanding global market for navigation, positioning and timing devices and related services.

4. Galileo Services, Applications and Markets

When fully deployed and operable each of the 30 Galileo satellites will transmit 10 navigation signals. Galileo will offer 5 distinct services (ref. ESA 2006):

Public Regulated Service (PRS) The relevant signals will be encrypted and will only be available for use by public authorities for applications in the context of law enforcement, emergency services, European or national security etc.

Search & Rescue (SAR) This service is used for the global reception and handling of distress messages, which will allow for near real time reception of messages and precise location of alerts.

Open Service (OS) This service will be free of charge and used for mass-market timing and positioning applications. It will not offer integrity information and no service guarantee.

IP/A/STOA/WS/2006-007 Page 21 of 73 PE 375.883

Safety of Life Service (SoL) This service is for use in safety critical navigation purposes in transport (aviation, maritime, rail, car). Other than the OS the SoL will provide integrity information (timely warnings when the system fails to meet margins of accuracy). The Service has to be certified by applying organisations - such as e.g. the International Civil Aviation Organisation (ICAO).

Commercial Service (CS) This service is planned to provide higher performance than the OS and will be offered on payment of a fee. Providers of application services will have to buy the right to use two additional signals protected by encryption from the Galileo operator.

Applications

There are an immense number of possible applications that are expected to be either improved and expanded or newly developed and commercially supplied in the future on the basis of the increased performance and security of navigation data provided by Galileo. Applications e.g. comprise: Network synchronization for power generation and distribution, precision agriculture, environmental monitoring, disaster monitoring and prediction, data encryption for e-commerce, construction side management and logistics, navigation assistance for people with disabilities, localisation of emergency calls and many others.

The most promising areas of applications and market development are supposed to be services for transport and the integration of Galileo navigation chipsets into mobile phones allowing for so called Location Based Services (LBS).

Due to its high level of accuracy Galileo is expected to participate to a great extent in the evolving market for new services in the transport domain - e.g. car navigation systems with additional features such as information about the traffic situation and other (e.g. tourist) information related to the current position of the user. An important future market is seen in traffic telematics: The Galileo signal can be used for fleet management as well as (together with other sensors) for so called Advanced Driver Assistance Systems allowing for autopilot-like support of the driver. More in a short term perspective are plans to allow for improved road charging systems (e.g. in urban areas) via extended use of positioning and route determination by the use of satellite navigation signals.

Whereas the aforementioned applications are offered in the frame of the open or the commercial service, other safety relevant applications in maritime and air navigation are emerging from the safety of life service. Navigation assistance in air flight is seen as becoming crucial since the number of air flights and the frequency of starts and landings is increasing rapidly. The process of certification for EGNOS (as a precursor for Galileo) for aircraft navigation is currently running. Satellite navigation is growing in importance for use in maritime navigation as well. Possible applications include locating traps and nets in fishing, fleet management and cargo monitoring, locating and handling of containers in harbours and others.

Galileo is supposed to trigger new developments in the probably most important consumer technology market of recent years, the mobile phone market, by making new Location Based Services available. The market for mobile phones in Europe and US is near to saturation but innovation cycles are quite short and the market will continue to grow in Asia (especially China).

IP/A/STOA/WS/2006-007 Page 22 of 73 PE 375.883

The inclusion of GNSS chipsets for navigation in mobile phones offers the possibility for new services. Mobile phones may deliver information (e.g. for leisure activities) directly to mobile phone users according to their current location or may supply localisation of the caller in case of emergency calls (E112 in Europe). GNSS may also support network related services where knowledge of user position improves communication services. The integration of GPS/GNSS into mobile phones is developing rather slowly so far in Europe, whereas in Japan and the US first services have been offered.

Markets

Given the recent development of the market for GPS as well as figures from market forecasts, perspectives for Galileo applications appear to be promising.

The GNSS related turnover passed from 10 billion € in 2001, to almost 60 billion € in 2005 (COM 2006). The increase is mainly linked to services associated with hand-held devices and road navigation devices.

The gross turnover for satellite navigation products has been forecasted to increase from 23 billion € in 2004 to 180 billion € by 2020 (GJU 2005).

The recent market development is supposed to indicate a move from a professional niche market for GNSS to a mass market. The initial GPS receiver concept, based on a standalone device with a simple man-machine interface aimed to trace waypoints has been replaced by a variety of different solutions and sophisticated all-in-one hand-held navigation system with a colour display, accurate and complete cartography stored on memory of some GByte, 3D maps visualisation, sophisticated algorithms to optimise the route computation for cars, bicycles and pedestrian and traffic information. Also Personal Digital Assistants (PDA) and smart phones might be equipped with Bluetooth GPS receivers. The integration of satellite navigation in mobile phones has started.

The involved actors ESA, EC, GJU have launched projects for exploring markets, raising awareness among possible service providers and manufactures of GNSS devices and have invested in fostering research and development activities for a broad range of applications in the context of 5th and 6th FP. Twelve projects for different user communities are being funded in the 6th FP to perform an assessment for the applications in each sector for technical, business, regulations and standards point of view. These projects, currently running, represent the European platform to discuss the best exploitation of EGNOS/Galileo for the various sectors: location based services, road, rail, aviation, maritime, multi-modal transport, energy, survey and civil engineering, agriculture, science, emergency and cultural assets (for an overview see GJU webpage, www.galileoju.com).

In order to provide for access to the world wide market for satellite navigation cooperation agreements for Galileo have been signed with several countries - among them China (participating with 280 mill. €) and Israel (18 mill. €). Ongoing activities of GJU to expand international cooperation for the use of EGNOS/Galileo are focussing on Africa and Latin America. International cooperation can be regarded as being vital for Galileo to be established as a globally applied system. The significance of GNSS technology is becoming increasingly understood and appreciated by governments around the world.

IP/A/STOA/WS/2006-007 Page 23 of 73 PE 375.883

It has been reported that India and China (despite its involvement in Galileo) are considering to launch their own satellite navigation systems.

EGNOS - about to be fully operable in the near future – has been referred to as a door opener for Galileo. It has been stated that the majority of receivers sold on the European market today are already “EGNOS-compatible”. Since EGNOS system receivers are already for sale EGNOS is supposed to help to establish confidence for the user equipment and applications service providers.

The ongoing certification process for EGNOS to enter into the safety of life services (especially in aviation) is held to pave the way for Galileo, since the implementation period for this particular market has long lead times.

Thus the potential of the Galileo system, the perspectives for European industry to take a good share of the developing global market for satellite based navigation services as well as for the related downstream industries appear to be extraordinary. There are however remaining uncertainties and risks regarding the development of technical specifications for commercial applications, consumer acceptance of services and necessary standardisation of technical parameters. It remains questionable to what extent the impressive range of possible applications will be realised and will be commercially successful and triggering of value added application markets will be the major challenge for the future Galileo Operating Company.

The difficulties to establish the market for the UMTS standard in mobile phone communication is a recent example for imponderability of market development for high tech consumer applications. The market in Europe so far did not evolve as positively as foreseen by past market analysis studies. User acceptance of Location Based Service varies from country to country. Trials made by a few mobile phone operators in Europe have not (yet) been successful, while it is reported that LBS markets in Korea and Japan are evolving rapidly.

Problems for Galileo to establish new services might be as follows: The development of Galileo related services will take time and may gain momentum only when the full capacity of the satellite system is realised, since many new and value added applications and services expected to be instigated by Galileo are dependent on new additional features which distinguish Galileo from current GPS. For a new application to succeed many preconditions must be fulfilled. Receiver technology must be at hand to affordable prices, the content for services must be provided (e.g. digital maps, databases). The maturity and economical affordability of the receiver technology, signals and services may have to be standardised and interoperable with other systems, a particular regulatory frame may be affordable to instigate new applications and some applications involve a certification by users and/or public authorities. The more complex and interactive an application is the more efforts for technical and content optimisation are necessary to meet customer needs.

5. Galileo Business Case - Revenues and Risks

The core of the commercial operation of Galileo is the Public-Private Partnership (PPP) which is based on a concession scheme that has been adopted as the business model for the Galileo project. The consortium of companies currently negotiating the contract for the PPP has been set up after the two original main competitors merged and offered a joint bid in June 2005 (Aena, Alcatel, EADS Space, Finmeccanica, Hispasat, Inmarsat, Thales, TeleOp and others).

IP/A/STOA/WS/2006-007 Page 24 of 73 PE 375.883

This has been welcomed by GJU as being helpful to reduce costs for the public partner and improve perspectives of the Galileo business case.

The private partner, the concessionaire, is charged with the responsibility to finance, operate, maintain, replenish and develop the system in exchange for the right to develop market revenues for a specified period of time.

The PPP is scheduled to start with the procurement of the deployment phase and will run for 20 years. The private partner is expected to cover 2/3 of the costs for deployment of the system.

Achievable Revenues for this period of time have been estimated at 9.3 billion €. The associated costs of the programme are estimated at 7 billion €. Given the complex technical structures to be developed as well as the above mentioned imponderability in market development these estimates unavoidably are subject to a high degree of uncertainty (Recent reports indicate the development phase of Galileo has already seen costs exceeded by € 400 mill. on top of the 1.1 billion € originally earmarked).

Studies on the business plan for Galileo carried out on behalf of the EC in 2001 and 2003 (PricewaterhouseCoopers) identified two main sources of revenue for the Galileo Operating Company (GOC) which are regarded as forming the financial backbone of the PPP: payments from service providers for making the signal available to them and their customers (for Galileo’s Commercial Services with an encrypted signal) and – most important source of revenue - royalties from Intellectual Property Rights.

The GOC will be the only entity entitled to exploit IPR provided by the public sector e.g. by creating revenues through licence fees for Galileo chipsets to be implemented in receivers. This should constitute a flow of revenue from the sale of Galileo enabled receivers, by charging royalties or a license fee paid to GOC by receiver manufacturers. The ability to derive revenues from the chipset royalties has been held to be crucial particularly in the early years of Galileo since “… it is not until applications are well established in the user market that the GOC benefits from a meaningful level of service revenue” (PricewaterhouseCoopers 2001, p. 20). According to GJU this expectation is still valid. However, partly due to the EU/USA agreement on cooperation in satellite navigation, difficulties to assess the actual potential for Galileo to gain revenue from royalties seem to be relevant.

It is regarded as being one of the most important tasks in the concession selection process to come up with a realistic assessment of opportunities to exploit IPR not only related to the Galileo chipset but also to EGNOS and Galileo System segments. Currently an IPR task force (EC, ESA, GJU) is occupied with the identification of solid and protectable IP in the domain of chipset and system functions in order to secure the opportunities emerging from the Research and Development activities (running e.g. under 6th FP) and from the Galileo infrastructure development.1

1 Arrangements to facilitate revenue generation for the concessionaire have been introduced by the GJU through contracts with the industrial teams who are generating Intellectual Property Rights within the Galileo projects funded under the 6th FP. These arrangements caused criticism from industry, especially concerning those projects that are funded at 50% and for those involving innovative SMEs.

IP/A/STOA/WS/2006-007 Page 25 of 73 PE 375.883

Difficulties to assess the opportunities to attain revenue from IPR have been reported as follows:

Strong competition is expected between chipset designers/manufacturers about the optimum chipset design providing most value added to the customers. To which extent the Galileo Operating Company will be able to influence and determine respective IPR depends on the detailed characteristics of the value chain, which can only be predicted with uncertainty.

Given the strong competition of manufacturers, costs are a sensitive success factor for the most important source of royalties, the Galileo Chipset. A royalty will be only acceptable provided that its level is not too high in comparison to a GPS-only product and that chipset manufacturers are charged the same fee. Currently royalties of 0.50 € are expected per chipset. A small change in the fee may play a very important role and it may represent the difference between failure and success. Slightly higher fees may easily stifle the market.

It is not certain that Galileo patent applications will lead to patents. Most of the patent applications were filed between 2002 and 2005 but it can take 5-7 years before a patent is granted by the patent office. The initial patent claims might as well be restricted or the patent office may refuse to grant the patent, and national courts might annul the patent in their territories.

It has also been argued that the charging of royalties is contradictory to the interoperability with GPS (which is free of royalties) and may be detrimental to Galileo’s position. Actually a royalty concept cannot be applied for the basic Open Service (due to agreement on interoperability with GPS). The royalty schemes will apply for value added by Galileo. This implies that it is vital for Galileo to actually prove that additional features and better performance are of added value for users. It will be a challenge for the Galileo Concessionaire to provide value added for regulated applications, where a high degree of positioning trustworthiness is legally required and higher revenue opportunities are given.

Due to the complexity and scope of the Galileo project the GOC will have to cope with a set of risks that have to be considered in developing the Galileo business case. According to the European Commission the following nine blocks of risks have been identified in the course of the concession negotiations (COM 2006, p. 3): cost overrun, construction, system performance, design, deployment, coverage of project risks, compensation in the event of termination of the project, refinancing.

It is/and will be the main subject of the currently running negotiations between GJU and the concessionaire to clarify the allocation of risks between the public and the private side of the PPP. The EC reports (June 2006) that whereas advances have been reached for seven areas of risk, the main differences concern the sharing of risks associated with system design and commercial revenue and market development (COM 2006).

According to the majority of experts the realisation of the Galileo programme is regarded as being indispensable in order to provide Europe with a satellite system which is independent and which opens the opportunity for European industry to play a major role in one of the most promising future markets.

IP/A/STOA/WS/2006-007 Page 26 of 73 PE 375.883

Some of them however are sceptical with regard to the PPP scheme, since the existing risks form too high a barrier for a private company to develop the Galileo business case. According to this position, Galileo – the satellite system and the ground segment – has to be regarded as basic infrastructure (like roads and railways) and is only feasible as an altogether publicly funded infrastructure project meant to open up opportunities for the private sector to utilise the system by developing applications and services.

6. Legal Aspects