2006 Full Year Roadshow This presentation may contain forward-looking statements, including ‘forward-looking statements’ within the meaning of the United States Private Securities Litigation Reform Act of 1995. These forward-looking statements are based upon current expectations and assumptions regarding anticipated developments and other factors affecting the Group. They are not historical facts, nor are they guarantees of future performance. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements. Further details of potential risks and uncertainties affecting the Group are described in the Group’s filings with the London Stock Exchange, Euronext Amsterdam and the US Securities and Exchange Commission, including the Annual Report & Accounts on Form 20-F. These forward-looking statements speak only as of the date of this presentation. Handout version

Transcript

0

2006 Full Year Roadshow

This presentation may contain forward-looking statements, including ‘forward-looking statements’ within the meaning of the United States Private Securities Litigation Reform Act of 1995. These forward-looking statements are based upon current expectations and assumptions regarding anticipated developments and other factors affecting the Group. They are not historical facts, nor are they guarantees of future performance. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements. Further details of potential risks and uncertainties affecting the Group are described in the Group’s filings with the London Stock Exchange, Euronext Amsterdam and the US Securities and Exchange Commission, including the Annual Report & Accounts on Form 20-F. These forward-looking statements speak only as of the date of this presentation.

Handout version

jennifer.hogan

Rectangle

1

59Small&Mighty30Agenda for 2007

60Idea! from family Goodness

29

28

27

26

25

24

23

22

21

20

19

18

17

16

15

14

13

12

11

8

7

6

5

4

3

2

Frusi

Dove Pro.Age

Ponds Age Miracle

New for 2007

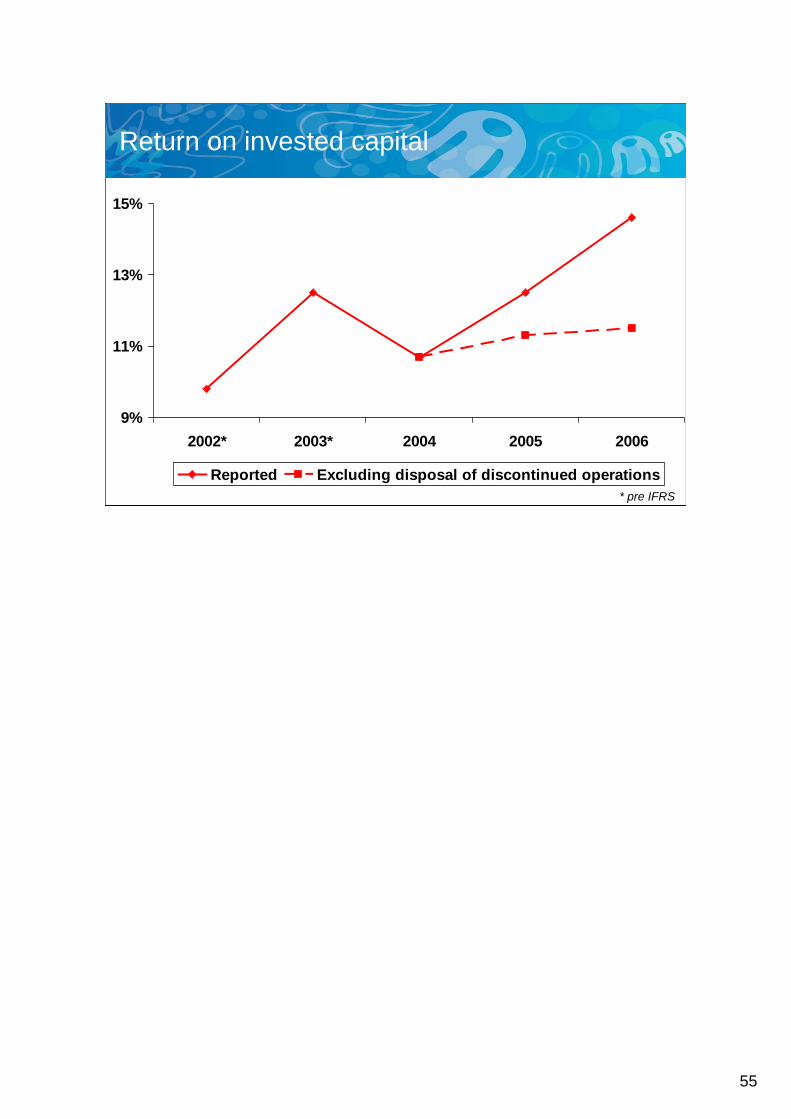

Return on invested capital

Cash flow

Tax rate development

Commodity costs

Q4 operating margin

Operating margin

Key financials

2006 Financials

AdeZ

Lipton Tea Can Do That

Slim.Fast

Ice Cream and Beverages

Heart Health

Wishbone salad spritzers

Knorr bouillon

Savoury, Dressings and Spreads

Actigel tablets

Domestos with C-Tac

Home Care

Dove Summer Glow

Sunsilk North America

Dove Clear

Personal Care

Drivers of growth in 2006

55Progress on One Unilever

Delayered, simpler, more effective

57Simplification saves money

58Changing culture and behaviour

61

54Simplification

53Brilliant consumer marketing

52Winning with customers

51Building capabilities

50Bigger, better innovation

49Better category strategies

Clear, distinct, complementary roles

47Unilever’s organisation

46Reshaping the portfolio – disposals

45The relentless rollout of Dirt Is Good

44Priorities driving growth

43Sales in D&E markets

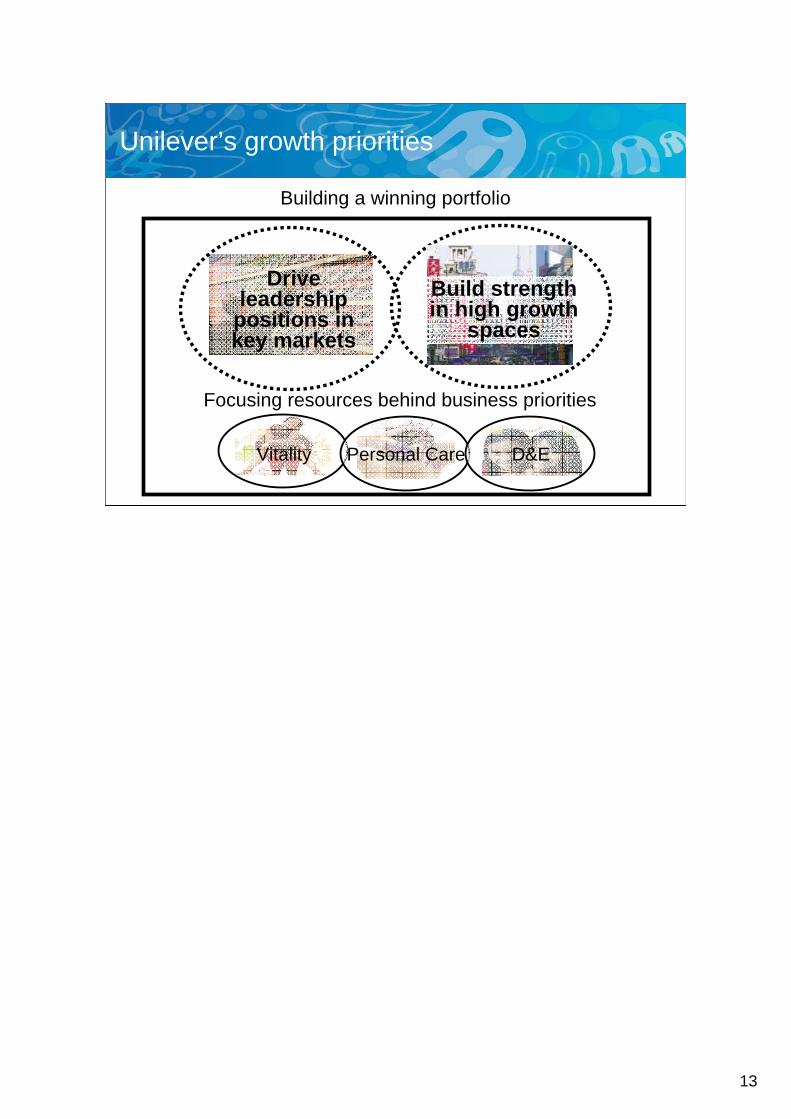

42Unilever’s growth priorities

41Our portfolio

40Building blocks of change

39Strategy – change – performance

38Our long term ambition

372007 Outlook

36Uses of cash

35Drivers of EPS growth

34Operating margin

33Broad-based growth

Consistent growth

Unilever’s 2006 Results

2

Consistent growth

0%

1%

2%

3%

4%

5%

6%

2002

2003

2004

2005

2006

Q1 2

005*

Q2 2

005

Q3 2

005

Q4 2

005*

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

* Days adjusted

Underlying sales growth

jennifer.hogan

Rectangle

3

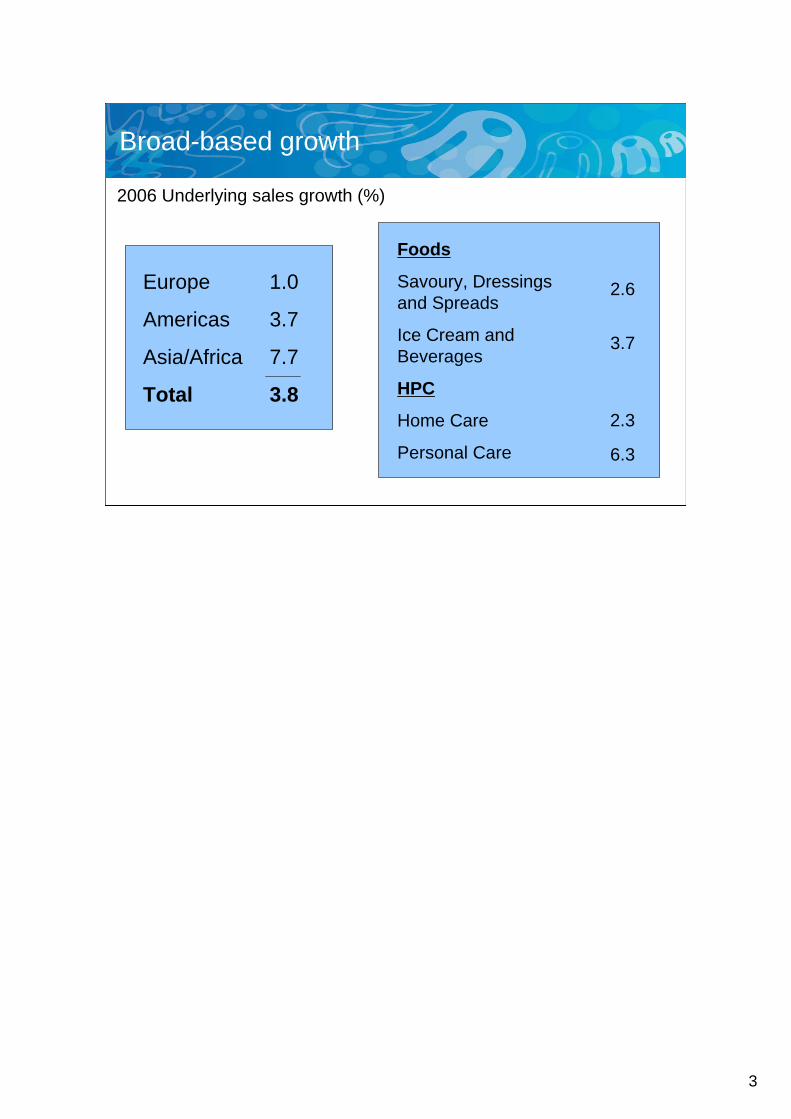

Broad-based growth

Europe

Americas

Asia/Africa

Total

1.0

3.7

7.7

3.8

Foods

Savoury, Dressings and Spreads

Ice Cream and Beverages

HPC

Home Care

Personal Care

2.6

3.7

2.3

6.3

2006 Underlying sales growth (%)

jennifer.hogan

Rectangle

4

Operating margin

Including:

Key drivers:

(0.3)%A&P

(0.3)%Change before these items

2.3%Savings

(2.3)%Cost/price/mix

(0.1)%-0.1%- Q2 2005: property sale

0.7%0.7%-- Q4 2006: US health care, UK pensions

0.2%(1.3)%(1.5)%- RDIs

0.4%13.6%13.2%Operating margin

Change20062005

jennifer.hogan

Rectangle

5

Drivers of 2006 EPS growth

Operating profit 7

Interest and pensions financing 4JVs and associates 2Tax rate 4Preference share provision (6)

EPS growth from continuing operations 11

Discontinued operations 16

Total EPS growth 27

(%)

jennifer.hogan

Rectangle

6

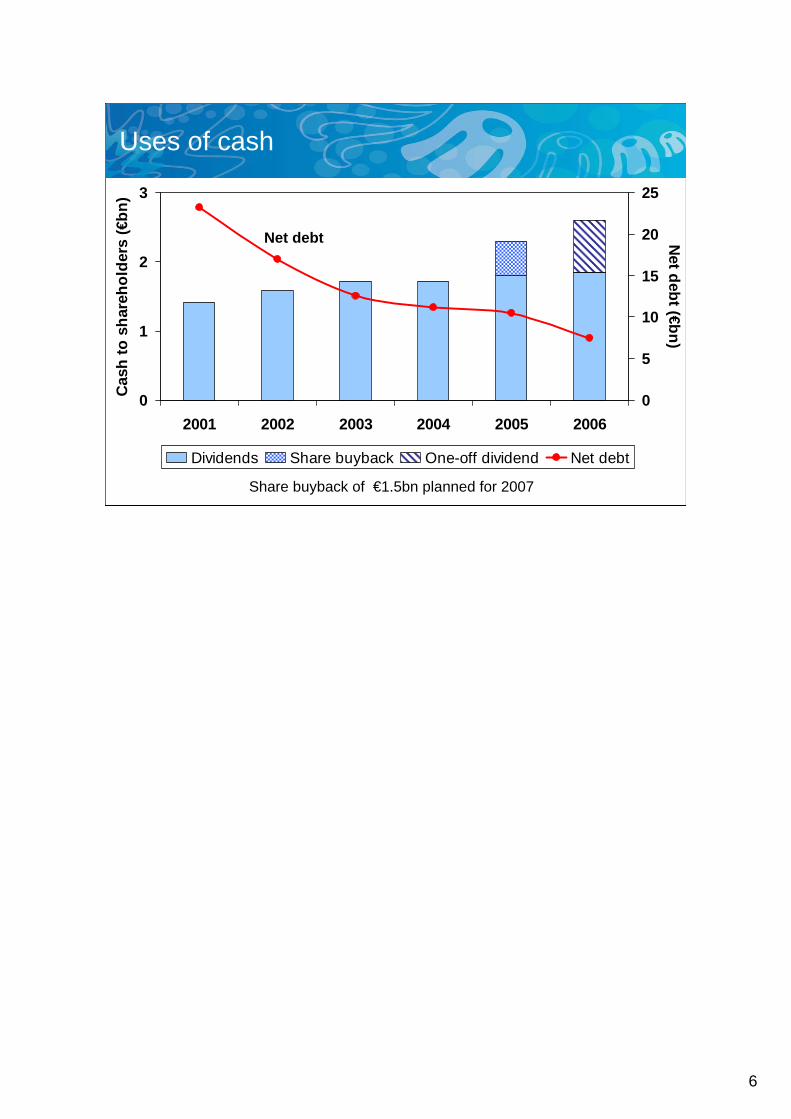

Uses of cash

0

1

2

3

2001 2002 2003 2004 2005 2006

Cas

h to

sha

reho

lder

s (€

bn)

0

5

10

15

20

25

Net debt (€bn)

Dividends Share buyback One-off dividend Net debt

Net debt

Share buyback of €1.5bn planned for 2007

7

Outlook 2007

• Little change to the business environment

• Underlying sales growth within 3-5% range

• Commodity cost increases easing

• Operating margin above 13.6%

• Restructuring in the 50 -100bps range

jennifer.hogan

Rectangle

8

Long term targets:

FCF €25-30bn during 2005-2010

Improved ROIC

Through:

Underlying sales growth of 3-5% pa

Operating margin in excess of 15% by 2010 after normal restructuring

Improved capital and tax efficiency

Overarching ambition remains top one-third TSR

Our long term ambition

jennifer.hogan

Rectangle

9

10

Strategy

Performance

Change

jennifer.hogan

Rectangle

11

Building blocks of change

• A strategy for growth - concentrating resources behind growth opportunities

Big brands, global resourcesWeak brands, managed locally

jennifer.hogan

Rectangle

21

Bigger, better innovation

Fewer, bigger innovation projects in the funnel

jennifer.hogan

Rectangle

22

Building capabilities

Firstchoice for our

customers

Shopper and

customer solutions

Every day great

execution

CustomerService

Excellence

World Class Customer

Development

Winningat Point of Purchase

BuildingBrandsThrough

Customers

Strategic Investing

For Growth

Firstchoice for our

consumersEvery day

great execution

Innovation capability

improvements

World Class

Brands

IntegratedBrand

Communication

Brand activation capability

Brand Planning Toolset

Unique and relevant

innovation

RegionsWin With Customers

CategoriesBrilliant Consumer

Marketing

jennifer.hogan

Rectangle

23

Winning with customers – unique store reach

jennifer.hogan

Rectangle

24

Brilliant consumer marketing

Winner of 37 Lions at the 2006 Cannes International Advertising Festival

jennifer.hogan

Rectangle

25

Simplification

600

700

800

900

1000

1100

1200

2004 2005 2006

Top management numbers

c. 30% headcount reduction

jennifer.hogan

Rectangle

26

0% 20% 40% 60% 80% 100%

Regional sharedservices

Back officeintegration

One sales force

Single head office

One top team

Completed Announced

Progress on One Unilever – Top 20 countries

jennifer.hogan

Rectangle

27

Delayered, simpler, more effective

20062004

One Unilever in China

c.10% growth c. 30% growth

Unilever Ice Cream China

Unilever Foods China

Unilever HPC China

HPC Division

Foods Category

Unilever China

HPC Category

President Asia/Africa

Foods Division

Foods Asia Business

Group

HPC Asia Business

Group

jennifer.hogan

Rectangle

28

Simplification saves money

0100200300400500600700800900

1000

Q1 Q2 Q3 Q4

€m

Procurement One Unilever and other

2006 Cumulative savings

jennifer.hogan

Rectangle

29

Changing culture and behaviour

• Global mindset

• Real accountability

• External orientation

• Action not debate

• Team alignment

• Build talent

jennifer.hogan

Rectangle

30

Agenda for 2007

Grow• Competitively – to gain market share

• Profitably – better margin development, further simplification

• Consistently

jennifer.hogan

Rectangle

31

32

Drivers of growth in 2006

jennifer.hogan

Rectangle

33

Personal Care

6.3%6.3%USG

20062005

jennifer.hogan

Rectangle

34

A patented combination of translucent anti-perspirant ingredients that are unbeatable against white marks, while delivering protection and a light, fresh fragrance.

Dove Clear

jennifer.hogan

Rectangle

35

$200m national launch of the brand to solve your hair dramas

Sunsilk North America

jennifer.hogan

Rectangle

36

A light moisturising body lotion, with a

unique combination of special Dove

moisturisersand a hint of self

tan

Dove Summer Glow

jennifer.hogan

Rectangle

37

2.3%2.4%USG

20062005

Home Care

jennifer.hogan

Rectangle

38

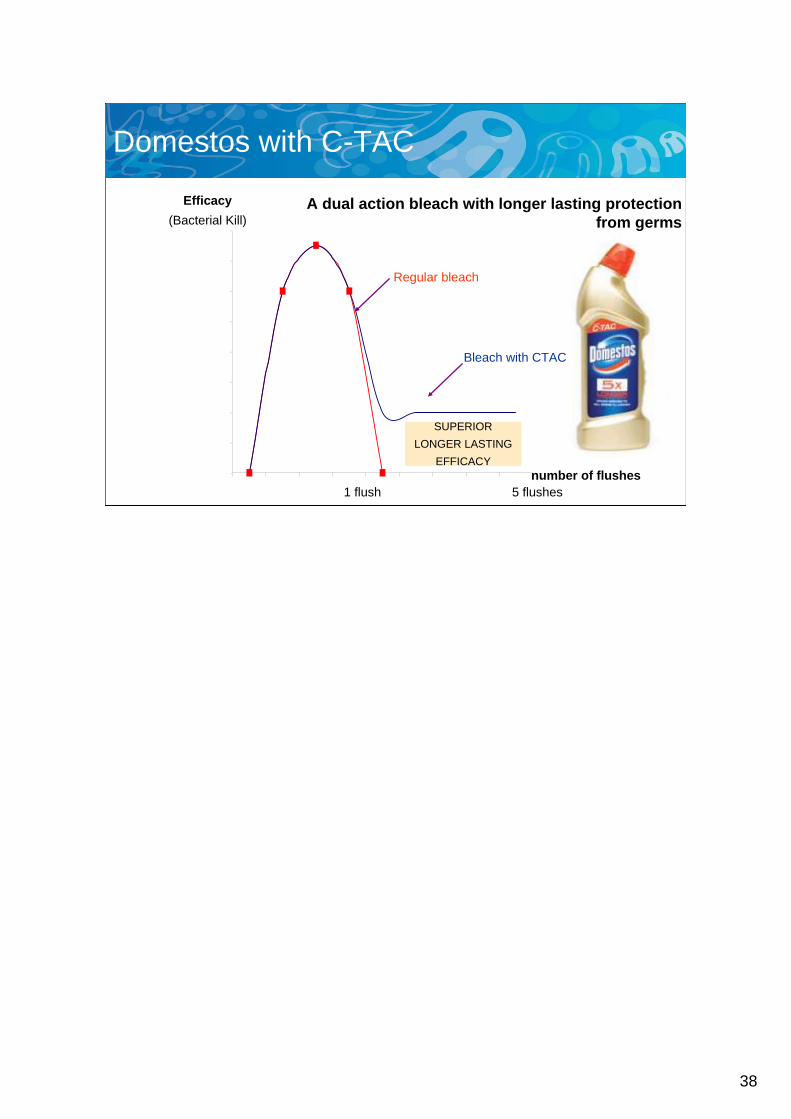

Domestos with C-TAC

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

number of flushes

Efficacy(Bacterial Kill)

SUPERIOR LONGER LASTING

EFFICACY

Regular bleach

Bleach with CTAC

1 flush 5 flushes

A dual action bleach with longer lasting protection from germs

jennifer.hogan

Rectangle

39

Laundry tablets with a unique gel layer containing pre-treating agents that tackle even the toughest stains

Dirt Is Good Actigel tablets

jennifer.hogan

Rectangle

40

2.6%2.2%USG

20062005

Savoury, Dressings and Spreads

jennifer.hogan

Rectangle

41

A range of bouillons with carefully selected ingredients.

Because good food deserves Knorr

Knorr bouillon

jennifer.hogan

Rectangle

42

Salad dressings in breakthrough easy-to-use spray bottles to control the amount of dressing added to salads, with one calorie per spray

Wishbone salad spritzers

jennifer.hogan

Rectangle

43

Omega 3 plusPacked with more omega 3

than any other spread or minidrink

pro.activSpreads, milk, yoghurt and mini-drinks clinically proven to lower cholesterol

Heart Health

jennifer.hogan

Rectangle

44

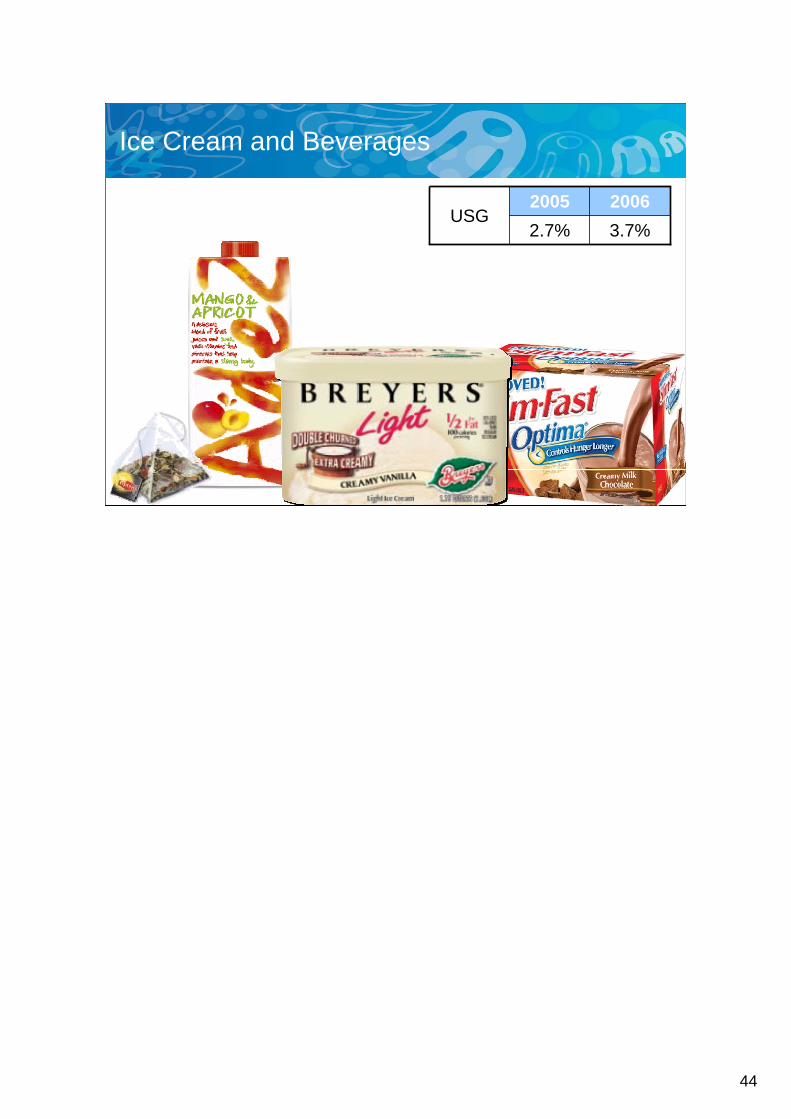

3.7%2.7%USG

20062005

Ice Cream and Beverages

jennifer.hogan

Rectangle

45

New improved Slim.Fast: delays the absorption of fat in the gut resulting in stronger ‘satisfaction signals’ to the brain, making you

feel fuller for longer

jennifer.hogan

Rectangle

46

Lipton’s unique combination of health benefits, with antioxidants to fight free radicals

Lipton Tea Can Do That

jennifer.hogan

Rectangle

47

AdeZ - a Healthy Drink that combines the Goodness of Soya with the Refreshment ,Taste & Health from Fruit Juice!

*Before restructuring, disposals and impairments and 2006 gains on US health care and UK pensions

and 2005 profit on office sale

jennifer.hogan

Rectangle

50

Operating margin

Including:

Key drivers:

(0.3)%A&P

(0.3)%Change before these items

2.3%Savings

(2.3)%Cost/price/mix

(0.1)%-0.1%- Q2 2005: property sale

0.7%0.7%-- Q4 2006: US health care, UK pensions

0.2%(1.3)%(1.5)%- RDIs

0.4%13.6%13.2%Operating margin

Change20062005

jennifer.hogan

Rectangle

51

Q4 Operating margin

Including

0.1%Change before these items

2.7%2.7%-- Q4 2006: US health care, UK pensions

(2.3)%(4.3)%(2.0)%- RDIs

0.5%10.9%10.4%Operating margin

Change20062005

Features:• Commodity cost inflation• A&P 0.5% lower – different phasing to last year• Investment in market research and development • Continued contribution from savings