80

A NNUAL R EPORT 2008

A N N U A L R E P O R T

2 0 0 8

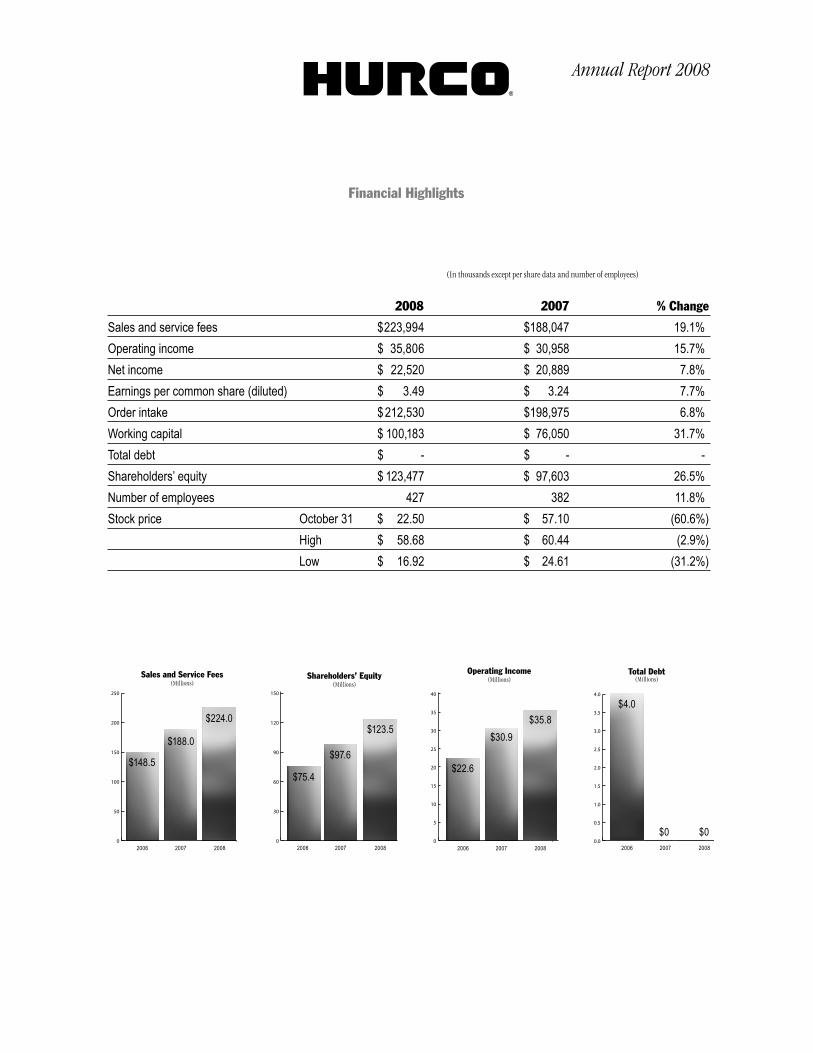

Financial Highlights

(In thousands except per share data and number of employees)

2008 2007 % Change

Sales and service fees $223,994 $188,047 19.1%Operating income $ 35,806 $ 30,958 15.7%Net income $ 22,520 $ 20,889 7.8%Earnings per common share (diluted) $ 3.49 $ 3.24 7.7%Order intake $ 212,530 $198,975 6.8%Working capital $ 100,183 $ 76,050 31.7%Total debt $ - $ - -Shareholders’ equity $ 123,477 $ 97,603 26.5%Number of employees 427 382 11.8%Stock price October 31 $ 22.50 $ 57.10 (60.6%) High $ 58.68 $ 60.44 (2.9%) Low $ 16.92 $ 24.61 (31.2%)

Annual Report 2008

Shareholders’ Equity(Millions)

$123.5

$97.6

2006 2007 2008

$75.4

0

30

60

90

120

150

Sales and Service Fees(Millions)

$148.5

$188.0

$224.0

2006 2007 20080

50

100

150

200

250

Operating Income(Millions)

$30.9$35.8

2006 2007 2008

$22.6

0

5

10

15

20

25

30

35

40

$0

Total Debt (Millions)

$4.0

2006 2007 2008

$00.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Report to Shareholders

While we are pleased to report another record breaking year for 2008, our elation is tempered by the global economic downturn that has affected our customers who serve a variety of industries, such as automotive, aerospace, energy, medical device, etc. This year’s revenues of $223,994,000, refl ect a 19% increase compared to 2007. Our fi scally conservative, Midwestern culture and commitment to strategic planning has led to a strong cash position that will help Hurco endure this economic downturn. We continue to reinvest in the business through product and technology innovation that yields measurable productivity benefi ts for our customers.

In 2008, we simultaneously introduced a record number of new products at the International Manufacturing Technology Show held in Chicago in September. Of the 14 new products we introduced, the investment we made in large machining centers, multi-axis machining centers, and complementary software features warrants special emphasis. We also held the offi cial grand opening ceremony of Hurco India at the Chennai technical center to showcase Hurco products and technology for this key market. To support effi cient manufacturing of our newest large machining centers, we opened a second plant at Hurco Manufacturing Limited (HML) and continue to reap the benefi ts of an effi cient global supply chain. The agility of our supply chain and manufacturing processes is an integral part of our success because we are able to effi ciently develop and manufacture new products and continually identify cost containment opportunities.

CustomersWhile our customers throughout the world are experiencing the strain from economic uncertainty, the ingenuity of small business owners and their resiliency should not be underestimated. At Hurco, we view our customers as collaborative partners and our goal is to develop technology and products that perpetuate productivity and profi tability for their businesses. Investment in relevant technology is the most expedient way for these customers to gain the speed and fl exibility they need to succeed. Responding to our customers’ need to compete drives product innovation at Hurco. Therefore, our investment in developing advanced technology and machines that yield increased productivity, such as our multi-axis products and new multi-tasking machines, is an important part of serving our customers who must continuously fi nd ways to stay competitive.

Core CompetenciesOur core competencies include software and product innovation, effi cient manufacturing, and targeted expansion in emerging markets. Even though we are considered a manufacturing company, it is our technology that sets us apart. In 2008, we saw the fruition of massive product and technology development efforts we undertook in previous years with the introduction of a record number of new machines and new software products. Additionally, all of our product development efforts generated more new patents for us to add to the Hurco intellectual property portfolio. As for targeted expansion in emerging markets, we continued to establish relationships throughout India and successfully opened our technical center in Chennai as planned.

Profi tabilityIn addition to record sales fi gures for 2008, Hurco recorded net income of $22.5 million ($3.49/share), which is a $1.6 million, or 8%, increase compared to 2007. Other key fi nancial data include Shareholders’ Equity of $123.5 million, an increase of $25.8 million compared to 2007, and Operating Income of $35.8 million, a 15.7% increase from 2007.

Going Forward 2009In 2009, we will carefully continue our strategic expansion throughout the world including emerging markets, such as Indonesia, Korea, South Africa, and Vietnam. We also plan to devote more resources in Spain and Turkey to further develop these markets. Although these individual markets are modest compared to the global market, they are important for future growth and can be developed effi ciently by existing subsidiaries without the need to devote signifi cant resources.

The investment we have made in new products will allow our sales organizations more opportunities to serve existing customers and to meet the needs of new customers, especially those customers who need machines that can produce large parts and molds for the aerospace and energy sectors. Worldwide, our total solutions control and software features continue to yield premium benefi ts for all markets and user-levels.

We want to thank our shareholders for their continued support. We also want to thank our employees for their dedication and strong work ethic. We especially want to thank our loyal customers and welcome our new customers to Hurco. We look forward to growing with you and continuing to provide you with the most innovative, user-friendly machine tools in the world.

Michael DoarChairman and Chief Executive Offi cer

James D. FabrisPresident and Chief Operations Offi cer

HURCO COMPANIES, INC.ELEVEN-YEAR SELECTED FINANCIAL DATA

(In thousands except per share data and number of employees)

For the Fiscal Year Ended 2008 2007 2006 Sales and service fees $223,994 $188,047 $148,517 Cost of sales and service (1) $ 141,377 $116,965 $ 95,192 Operating expenses (SG&A) $ 46,811 $ 40,124 $ 30,697 Restructuring and other expenses, net $ - $ - $ - Operating income (loss) $ 35,806 $ 30,958 $ 22,628 License fee income, net $ - $ - $ - Other income (expense) $ (1,640) $ 1,807 $ 486 Income before taxes $ 34,166 $ 32,765 $ 23,114 Income tax expense (benefi t) (2) $ 11,646 $ 11,876 $ 7,635 Net income (loss) $ 22,520 $ 20,889 $ 15,479

Average shares outstanding - Basic 6,415 6,382 6,317 Diluted/Primary 6,444 6,440 6,397 Earnings per share Basic $ 3.51 $ 3.27 $ 2.45 Diluted/Primary $ 3.49 $ 3.24 $ 2.42 Capital expenditures $ 5,514 $ 4,510 $ 3,301 Depreciation and amortization $ 3,023 $ 2,106 $ 1,504 EBITDA $ 37,252 $ 35,072 $ 24,977 EBITDA, excluding license fees and restructuring charge $ 37,252 $ 35,072 $ 24,977 Gross profi t margin % 36.9% 37.8% 35.9% Operating income as % of sales 16.0% 16.5% 15.2% Net return on sales 10.1% 11.1% 10.4% Return on average equity 20.4% 24.2% 23.0% Stock price range High $ 58.68 $ 60.44 $ 37.47 Low $ 16.92 $ 24.61 $ 17.74

At Fiscal Year End 2008 2007 2006 Working capital $ 100,183 $ 76,050 $ 59,094 Current ratio 2.96 2.20 2.33 Total assets $ 177,444 $163,781 $125,545 Total debt $ - $ - $ 4,010 Shareholders’ equity $ 123,477 $ 97,603 $ 75,375 Total debt to capitalization % - - 5.1% Shareholders’ equity per share (3) $ 19.16 $ 15.16 $ 11.78 Net operating assets per $ revenue (4) $ .404 $ 0.308 $ 0.334 Number of employees 427 382 320

Annual Report 2008

Certain prior year amounts have been reclassifi ed to conform to the current year presentation.

(1) Cost of Sales in fi scal 2002 includes restructuring write-downs of inventory of $1.1 million.

(2) Fiscal 2005 includes an approximate $2.3 million benefi t from the reduction of valuation allowances on our deferred tax assets.

(3) Based on shares outstanding at fi scal year end - diluted

(4) Excluding cash, short-term investments, and debt.

2005 2004 2003 2002 2001 2000 1999 1998$125,509 $99,572 $75,532 $70,486 $92,267 $96,204 $88,238 $93,422$ 82,951 $69,274 $54,710 $55,240 $69,005 $70,827 $64,064 $65,483$ 26,057 $21,401 $18,749 $19,658 $24,040 $23,538 $ 21,259 $21,786$ - $ 465 $ (124) $ 2,755 $ 143 $ 300 $ (103) $ 1,162$ 16,501 $ 8,432 $ 2,197 $ (7,167) $ (921) $ 1,539 $ 3,018 $ 4,991$ - $ - $ - $ 163 $ 723 $ 5,365 $ 304 $ 6,974$ (419) $ (864) $ (777) $ (670) $ (622) $ (1,298) $ (1,268) $ (777)$ 16,082 $ 7,568 $ 1,420 $ (7,674) $ (820) $ 5,606 $ 2,054 $11,188$ (361) $ 1,299 $ 958 $ 589 $ 777 $ 571 $ 252 $ 1,934$ 16,443 $ 6,269 $ 462 $(8,263) $ (1,597) $ 5,035 $ 1,802 $ 9,254

6,171 5,784 5,582 5,583 5,670 5,952 5,980 6,4986,336 6,026 5,582 5,583 5,670 6,020 6,061 6,670

$ 2.66 $ 1.08 $ 0.08 $ (1.48) $ (0.28) $ 0.85 $ 0.30 $ 1.42 $ 2.60 $ 1.04 $ 0.08 $ (1.48) $ (0.28) $ 0.84 $ 0.30 $ 1.39 $ 3,040 $ 2,052 $ 1,215 $ 1,716 $ 1,918 $ 1,899 $ 2,157 $ 2,328 $ 1,331 $ 1,223 $ 1,429 $ 1,929 $ 2,196 $ 2,519 $ 2,428 $ 2,138 $ 17,768 $ 9,259 $ 3,507 $ (5,111) $ 2,166 $ 9,064 $ 5,775 $14,202 $ 17,768 $ 9,724 $ 3,383 $(2,519) $ 1,586 $ 3,999 $ 5,368 $ 8,390

33.9% 30.4% 27.6% 21.6% 25.2% 26.4% 27.4% 29.9% 13.1% 8.5% 2.9% (10.2%) (1.0%) 1.6% 3.4% 5.3% 13.1% 6.3% 0.6% (11.7%) (1.7%) 5.2% 2.0% 9.9% 33.8% 18.7% 1.6% (26.0%) (4.3%) 13.4% 4.9% 27.4%

$ 20.00 $ 17.37 $ 3.15 $ 3.35 $ 4.19 $ 5.88 $ 6.63 $ 9.25 $ 10.25 $ 2.52 $ 1.30 $ 1.45 $ 2.08 $ 3.00 $ 3.38 $ 6.25

2005 2004 2003 2002 2001 2000 1999 1998$ 43,057 $26,347 $22,236 $20,350 $31,293 $26,071 $33,276 $29,349

2.40 1.87 2.10 1.96 2.72 2.13 2.70 2.14 $ 94,114 $73,446 $57,958 $ 57,152 $66,217 $65,024 $ 69,632 $71,696 $ 4,136 $ 4,600 $ 9,222 $ 8,885 $12,000 $ 3,736 $ 14,172 $ 8,358 $ 58,944 $38,455 $28,741 $28,017 $35,468 $38,891 $ 36,148 $ 37,740

6.6% 10.7% 24.3% 24.1% 25.3% 8.8% 28.2% 18.1%$ 9.30 $ 6.38 $ 5.15 $ 5.02 $ 6.26 $ 6.46 $ 5.96 $ 5.66 $ 0.363 $ 0.347 $ 0.424 $ 0.462 $ 0.476 $ 0.408 $ 0.531 $ 0.458

284 250 232 240 277 293 280 306

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K (Mark One)

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended October 31, 2008 or

Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from _________ to _________.

Commission File No. 0-9143

HURCO COMPANIES, INC. (Exact name of registrant as specified in its charter)

Indiana 35-1150732 (State or other jurisdiction of (I.R.S. Employer Identification Number) incorporation or organization) One Technology Way Indianapolis, Indiana 46268 (Address of principal executive offices) (Zip code)

Registrant’s telephone number, including area code (317) 293-5309 Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: Common Stock, No Par Value (Title of Class) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X ] Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d). Yes [ ] No [X ] Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to the filing requirements for at least the past 90 days. Yes [X ] No [ ] Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non- accelerated filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act. Large accelerated filer [ ] Accelerated filer [ X ] Non-accelerated filer [ ] Smaller Reporting Company [ ] (Do not check if a smaller reporting company) Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X ] The aggregate market value of the registrant’s voting stock held by non-affiliates as of April 30, 2008 (the last day of our most recently completed second quarter) was $294,011,000. The number of shares of the registrant’s common stock outstanding as of January 7, 2009 was 6,420,851. DOCUMENTS INCORPORATED BY REFERENCE: Portions of the registrant’s Proxy Statement for its 2009 Annual Meeting of Shareholders (Part III).

1

Disclosure Concerning Forward-looking Statements Certain statements made in this annual report on form 10-K may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These factors include the risks identified in Item 1A.

PART I Item 1. BUSINESS General Hurco Companies, Inc. is an industrial technology company. We design, manufacture and sell computerized machine tools, consisting primarily of vertical machining centers (mills) and turning centers (lathes), to companies in the metal working industry through a worldwide sales, service and distribution network. Although our computer control systems and software products are proprietary, they predominantly use industry standard personal computer components. Our computer control systems and software products are primarily sold as integral components of our computerized machine tool products. As used in this report, the words “we”, “us” and “our” refer to Hurco Companies, Inc. and its consolidated subsidiaries. Since our founding in 1968, we have been a leader in the introduction of interactive computer control systems that automate manufacturing processes and improve productivity in the metal parts manufacturing industry. Hurco pioneered the application of microprocessor technology and conversational programming software for use in machine tools. We have concentrated on designing “user-friendly” computer control systems that can be operated by both skilled and unskilled machine tool operators and yet are capable of instructing a machine to perform complex tasks. The combination of microprocessor technology and patented interactive, conversational programming software in our computer control systems enables operators on the production floor to quickly and easily create a program for machining a particular part from a blueprint or computer-aided design file and immediately begin machining that part. Our executive offices and principal design and engineering operations are headquartered in Indianapolis, Indiana. Sales, application engineering and service subsidiaries are located in Mississauga, Canada; Shanghai, China; High Wycombe, England; Paris, France; Munich, Germany; Chennai, India; Milan, Italy; and Singapore, along with manufacturing operations in Taiwan and China. Products are sold through independent agents and distributors in North America, Europe and Asia. We also have direct sales forces in Canada, France, Germany, Italy, Singapore and the United Kingdom. Distribution facilities are located in Los Angeles, California, Venlo, the Netherlands, and Singapore. In August, we held the official grand opening ceremony for our newest sales, application engineering and service subsidiary, Hurco India, Ltd. The event was held at our Technical Center in Chennai and was an opportunity to illustrate the capabilities of Hurco technology and machining centers to this growing market. Hurco machine tools are advantageous to customers in India because the user-friendly control and conversational programming enables machine shop owners to hire workers with less technical skill sets. Our strategy is to design, manufacture and sell to the global metalworking market a comprehensive line of computerized machine tools that incorporate our proprietary, interactive computer control technology. Our technology is designed to enhance the machine tool user's productivity through ease of operation and higher levels of machine performance (speed, accuracy and surface finish quality). We use an open system software architecture that permits our computer control systems and software to be produced and employed using standard PC hardware. We have emphasized a “user-friendly” design that employs both interactive conversational and graphical programming software. Each year we have expanded our product offering to meet customer needs, which has led us to design and manufacture more complex machining

2

centers with advanced capabilities. We bring a disciplined approach to strategically enter new geographic markets, as appropriate. Our introduction of new, technologically advanced products, combined with our expansion into new markets, has resulted in our significant growth over the last several years. In addition to this strong organic growth, we have the capability to pursue opportunistic acquisitions that are consistent with our strategic focus on expanding our product line and entering new markets. At present, we are not engaged in negotiations, and have no current plans, for any acquisitions. Industry

Machine tool products are considered capital goods, which makes them part of an industry that has historically been highly cyclical.

Although, industry association data for the U.S. machine tool market is available, that market accounts for only 9% of worldwide consumption. Reports available for the U.S. machine tool market include:

• United States Machine Tool Consumption – generated by the Association for Manufacturing Technology and American Machine Tool Distributor Association, this report includes metal cutting machines of all types and sizes, including segments in which we do not compete

• Purchasing Manager’s Index - developed by the Institute for Supply Management and reports activity levels in U.S. manufacturing plants that purchase machine tools

• Capacity Utilization of Manufacturing Companies – issued by the Federal Reserve Board

A limited amount of information for foreign markets is available, and different reporting methodologies are used by various countries. Machine tool consumption data published by Gardner Publications, Inc., calculates machine tool consumption annually by country. It is important to note that data for foreign countries is based on government reports that may lag six to twelve months and therefore is unreliable for forecasting purposes.

Demand for capital equipment can fluctuate during periods of changing economic conditions. Manufacturers and suppliers of capital goods, such as Hurco, are often the first to experience these changes in demand. Additionally, since our order backlog is approximately 45 days, it is difficult to estimate demand with any reasonable certainty. Therefore, we do not have the benefit of relying on the common leading indicators that are available to many other industries for market analysis and forecasting purposes.

Products

Our core products consist of general purpose computerized machine tools for the metal cutting industry. These are, principally, vertical machining centers (mills) and turning centers (lathes), with which our proprietary software and computer control systems are fully integrated. We also produce computer control systems and related software for press brake applications that are sold as retrofit units for installation on existing or new press brake machines. Additionally, we produce and distribute software options, control upgrades, hardware accessories, and replacement parts for our machine tool product lines and we provide operator training and support services to our customers.

3

The following table sets forth the contribution of each of our product groups to our total sales and service fees during each of the past three fiscal years: Net Sales and Service Fees by Product Category(Dollars in thousands) Year ended October 31,

2008 2007 2006 Continuing Products and Services Computerized Machine Tools $199,238 89.0% $165,832 88.2% $128,946 86.8% Computer Control Systems and Software * 5,678 2.5% 5,291 2.8%

4,694 3.2%

Service Parts 13,240 5.9% 12,096 6.4% 10,494 7.0% Service Fees 5,838 2.6% 4,828 2.6% 4,383 3.0% Total $223,994 100% $188,047 100% $148,517 100% * Amounts shown do not include computer control systems sold as integrated components of computerized machine

tools. Computerized Machine Tools – Machining and Turning Centers We design, manufacture and sell computerized machine tools equipped with a fully integrated interactive computer control system that features our WinMax® software. Our computer control system enables a machine tool operator to create complex two-dimensional or three-dimensional machining programs directly from an engineering drawing or computer aided design geometry file. An operator with little or no machine tool programming experience can successfully create a program with minimal training and begin machining the part in a short period of time. The control features an operator console with a liquid crystal display (LCD), and incorporates an upgradeable personal computer (PC) platform using a Pentium®* class processor with solid rendering graphical programming. In addition, WinMax® has a Windows®** based operating system to enable users to improve shop floor flexibility and software productivity. In the intensely competitive global manufacturing marketplace, increases in productivity are being derived from control and software technologies. Companies using computer controlled machine tools are better able to:

• maximize the efficiency of their human resources • continue to expand their capability to make more advanced and complex parts from a wide range

of materials using multiple processes • maintain the ability to incorporate fast moving changes in technology into their operations to

keep their competitive edge • continue to integrate themselves into the global supply chain of their customers by supporting

small to medium lot sizes for “just in time” initiatives

Our Windows®** based control facilitates our ability to meet these customer needs. Companies are finding that the familiar Windows®** operating system coupled with the Hurco conversational style of program creation means that their operators are capable of creating and editing part-making programs without incurring the incremental overhead of specialized computer aided design and computer aided manufacturing programmers. With the ability to transfer most computer aided design data directly into a Hurco program, programming time becomes minutes instead of hours. Products today are being designed to meet the demand for machining complex parts with greater part accuracies. Our proprietary controls with WinMax® software and Pentium®* processors efficiently handle the large amounts of data these complex part-making programs require, which enables our customers to create parts with superb accuracy at world-class speeds. We continue to add technology to our control design as it becomes available. Our offering of machining centers, currently equipped with either a twin touch-screen console or a single touch-screen console, consists of the following six product lines:

4

VM Product Line The VM product line consists of moderately priced vertical machining centers for the entry-level market. Their design premise of a machining center with a large work cube and a small footprint optimizes the use of available floor space. The VM line consists of five models in three sizes with X-axis (horizontal) travels of 26, 40, and 50 inches. The base prices of the VM machines range from $40,000 to $80,000. VMX Product Line The VMX product line consists of higher performing vertical machining centers aimed at manufacturers that require greater part accuracy. It is our flagship series of machining centers. The VMX line consists of 14 models in seven sizes with X-axis travels of 24, 30, 40, 50, 60, 64, and 84 inches. The base prices of VMX machines range from $50,000 to $200,000. Five-Axis Product Line The five-axis product line is targeted at manufacturers seeking to produce complex multi-sided parts in a single setup. Machines in this product line can yield significant productivity gains for operations that previously processed each side of a part individually. Due to market demand for increased processing efficiency, we focused on five-axis technology in 2008 and introduced four new five-axis machining centers in September. In total, we now have six Hurco five-axis machining centers to offer customers. The base prices of the five-axis machines range from $100,000 to $180,000. TM/TMM Product Line Since its introduction in fiscal 2005, we have continued to expand the TM turning center (horizontal slant-bed lathe) product line. The TM series is designed for entry-level job shops and contract manufacturers seeking efficient processing of small to medium lot sizes. The TM is offered in three models with chucks of 6, 8, and 10 inches respectively. In September 2006, we further enhanced the capability of the TM turning centers with the addition of “live” or motorized tooling on the lathe turret. Designated as the TMM product line, these machines allow our customers to complete a number of secondary milling, drilling and tapping operations, while the part is still held in the chuck after the turning operations are complete. This ability to “mill/turn” or “multi-task” on the same machine in a single setup can provide significant productivity gains. Two TMM models with this capability are being offered. The base prices of the TM/TMM machines range from $40,000 to $85,000. TMX Product Line Introduced in September 2008, the TMX product line consists of high performance turning centers. There are three TMX models, all with chucks of 8 inches, but two of the models are equipped with an additional axis and motorized live tooling, and one of those models has an additional spindle. The base prices of TMX turning centers range from $80,000 to $180,000. Specialty Product Lines Two new specialty products were introduced in September 2008: the dual-column machining center and the zone machining center. Both of these machines are designed to facilitate production of large parts and molds. The horizontal machining center is also included in this category as it facilitates efficient and accurate machining of complex production parts. The base prices of these machines range from $235,000 to $350,000. *Pentium® is a registered trademark of Intel Corporation. **Windows® is a registered trademark of Microsoft Corporation.

5

Computer Control Systems and Software The following machine tool computer control systems and software products are sold directly to end-users and/or to original equipment manufacturers. Autobend® Autobend® computer control systems are applied to metal bending press brake machines that form parts from sheet metal and steel plate. They consist of a microprocessor-based computer control and back gauge (an automated gauging system that determines where the bend will be made). We have manufactured and sold the Autobend® product line since 1968. We currently market two models of our Autobend® computer control systems for press brake machines, in combination with six different back gauges, through distributors to end-users as retrofit units for installation on existing or new press brake machines, as well as to original equipment manufacturers and importers. Software Products In addition to our standard computer control features, we offer software option products for two-dimensional and three-dimensional programming. These products are sold to users of our computerized machine tools equipped with our twin touch-screen or single touch-screen consoles featuring WinMax® control software. The options include: Swept Surface, SelectSurface Finish Quality (SFQ), DXF Transfer, UltiNetTM, UltiPocketTM, Conversational Part and Tool Probing, Advanced Verification Graphics, and Simultaneous Five-Axis Contouring. Our Swept Surface software option simplifies programming of 3D contours and significantly reduces programming time. SelectSurface Finish Quality (SFQ) lets the customer control surface finish quality and run time in one easy step. The DXF Transfer software option can substantially increase operator productivity because it eliminates manual data entry of part features by transferring AutoCADTM drawing files directly into the Hurco computer control or into our desktop programming software, WinMax® Desktop. UltiNet™ is a networking software option used by our customers to transfer part design and manufacturing information to computerized machine tools at high speeds and to network computerized machine tools within the customer's manufacturing facility. UltiPocketTM automatically calculates the tool path around islands, eliminating the arduous task of plotting these shapes. Islands can also be rotated, scaled and repeated. Conversational Part and Tool Probing options permit the computerized dimensional measurement of machined parts and the associated cutting tools. This “on-machine” technique improves the throughput of the measurement process when compared to traditional “off-machine” approaches. The Advanced Verification Graphics feature significantly reduces both scrap and programming time because it provides customers with a three-dimensional solid rendering of the part, including dynamic rotation. This feature allows a customer to view the rendered part from any angle without needing to redraw it. Simultaneous five-axis contouring software enables a five-axis machine to command motion concurrently on all axes. This allows the user to create continuous tool-paths along complex geometries with only a single machine/part setup, providing increased productivity along with the performance benefits of using shorter cutting tools. The sale of simultaneous five-axis contouring software is subject to governmental licensing.

6

Parts and Service Our service organization provides installation, warranty, operator training and customer support for our products on a worldwide basis. In the United States, our principal distributors have primary responsibility for machine installation and warranty service and support for product sales. Our service organization also sells software options, computer control upgrades, accessories and replacement parts for our products. Our after-sales parts and service business strengthens our customer relationships and provides continuous information concerning the evolving requirements of end-users. Manufacturing Our computerized metal cutting machine tools are manufactured to our specifications primarily by our wholly owned subsidiary in Taiwan, Hurco Manufacturing Limited (HML). This subsidiary has increased our overall capacity and reduced our dependence on other manufacturers. HML conducts final assembly operations and is supported by a network of contract suppliers of components and sub-assemblies who manufacture components for our products in accordance with our proprietary designs, quality standards and cost specifications. This has enabled us to lower our production costs, reduce our working capital per sales dollar and increase our worldwide manufacturing capacity without significant incremental investment in capital equipment or personnel. In 2006, we opened a new manufacturing facility in Ningbo, China, that focuses on the machining of castings and components to support HML’s production in Taiwan. In the future, we can expand the Ningbo facility to include sub-assembly operations. Eventually, we expect that machines designed specifically for the Chinese market will be produced at the Ningbo facility. We have a contract manufacturing agreement for computer control systems with Hurco Automation, Ltd., a Taiwanese company in which we have a 35% ownership interest. This company produces all of our computer control systems to our specifications, sources industry standard computer components and our proprietary parts, performs final assembly and conducts test operations. We work closely with our subsidiaries, key component suppliers and our minority-owned affiliate to ensure that their production capacity will be sufficient to meet the projected demand for our machine tool products. Many of the key components used in our machines can be sourced from multiple suppliers. However, any prolonged interruption of operations or significant reduction in the capacity or performance capability at either of our Taiwanese manufacturing facilities, or at any of our key component suppliers, could have a material adverse effect on our operations. Marketing and Distribution We sell our products through more than 100 independent agents and distributors throughout North America, Europe and Asia. Although some distributors carry competitive products, Hurco is the primary line for the majority of our distributors globally. We also have direct sales personnel in Canada, France, Germany, Italy, Singapore and the United Kingdom, which are among the world's principal machine tool consuming markets. Approximately 91% of the worldwide demand for computerized machine tools and computer control systems is outside the United States. In fiscal 2008, more than 75% of our revenues were from overseas customers. No single end-user or distributor of our products accounted for more than 5% of our total sales and service fees. The end-users of our products are precision tool, die and mold manufacturers, independent metal parts manufacturers, and specialized production application or prototype departments within large manufacturing companies. Industries served include aerospace, defense, medical equipment, energy, automotive/transportation, electronics and computer equipment.

7

We also sell our Autobend® computer control systems to original equipment manufacturers of new metal fabrication machine tools who integrate them with their own products prior to the sale of those products to their own customers, to retrofitters of used metal fabrication machine tools who integrate them with those machines as part of the retrofitting operation, and to end-users who have an installed base of metal fabrication machine tools, either with or without related computer control systems. Demand We believe that advances in industrial technology and the related demand for automated process improvements drive demand for our products. Other factors affecting demand include:

• the need to continuously improve productivity and shorten cycle time • an aging machine tool installed base that will require replacement with more advanced and

efficient technology created by shorter product life cycles • the industrial development of emerging markets in Asia and Eastern Europe • the declining supply of skilled machinists

Demand for our products is also highly dependent upon economic conditions and the general level of business confidence, as well as such factors as production capacity utilization and changes in governmental policies regarding tariffs, corporate taxation, and other investment incentives. By marketing and distributing our products on a worldwide basis, we seek to reduce the impact of adverse changes in economic conditions that might occur in a particular geographic region. For additional information regarding current economic conditions and their impact on our results of operation and financial condition, refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. Competition We compete with many other machine tool producers in the United States and foreign countries. Most of our competitors are larger and have greater financial resources than our company. In the United States and European metal cutting markets, major competitors include Haas Automation, Inc., Daewoo, Miltronics, Deckel Maho Gildemeister Group (DMG), Hardinge Inc. and MAG Industrial Automation Systems. There are also a large number of other foreign manufacturers, including Okuma Machinery Works Ltd., Mori Seiki Co., Ltd., Mazak and Matsuura Machinery Corporation. We strive to compete effectively by incorporating into our products unique, patented software and other proprietary features that offer enhanced productivity, technological capabilities and ease of use. We offer our products in a range of prices and capabilities to target a broad potential market. We also believe that our competitiveness is aided by our reputation for reliability and quality, our strong international sales and distribution organization, and our extensive customer service organization. Intellectual Property We consider our products to be proprietary. Various features of our control systems and machine tools employ technologies covered by patents that are material to our business. We also own additional patents covering new technologies that we have acquired or developed, and that we are planning to incorporate into our control systems in the future.

8

Research and Development

In the fiscal years set forth below, non-capitalized research and development expenditures for new products and significant product improvements and expenditures related to software development projects that were capitalized were as follows (in thousands):

Fiscal Year

Non-capitalizedresearch and development

Capitalized software

development

2008 $ 3,000 $ 900 2007 3,100 1,200 2006 2,500 2,100

Employees We had approximately 430 full-time employees at the end of fiscal 2008, none of whom were covered by a collective-bargaining agreement or represented by a union. We have experienced no employee-generated work stoppages or disruptions and we consider our employee relations to be satisfactory. Geographic Areas Financial information about geographic areas in which we sell our products is set forth in Note 15 of Notes to Consolidated Financial Statements. The risks of doing business on a global basis are set forth in Item 1A. Risk Factors below. Backlog For information on orders and backlog, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. Availability of Reports and Other Information Our website is www.hurco.com. We make available on this website, free of charge, access to our annual, quarterly and current reports and other documents filed by us with the Securities and Exchange Commission (SEC) as soon as reasonably practical after the filing date. These reports can also be obtained at the SEC’s Public Reference Room at 100 F Street, NE Washington, DC 20549. Item 1A. RISK FACTORS In this section we describe what we believe to be the material risks related to our business. The risks and uncertainties described below or elsewhere in this report are not the only ones to which we are exposed. Additional risks and uncertainties not presently known and/or risks we currently deem immaterial may also adversely affect our business and operations. If any of the developments included in the following risks were to occur, our business, financial condition, results of operations, cash flows or prospects could be materially adversely affected. The current global economic crisis is adversely affecting overall demand and our customers’ ability to purchase our products and services. The current global economic crisis has severely impacted banks and other lenders, limiting the ability of many businesses to access the credit markets. As a result of the credit crisis and the overall decline in economic activity, the ability of our customers to purchase our products and services has been adversely affected, the initial impact of which was reflected in our results for the fourth quarter of fiscal 2008. An

9

overall decline in economic activity may also have an adverse affect on our customers and distributors ability to pay us for the products they purchased. A prolonged recession or further decline in the global economy will materially adversely affect our results of operations and financial condition. For additional information regarding current economic conditions and their impact on our results of operations and financial condition, refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. The cyclical nature of our business causes fluctuations in our operating results. The machine tool industry is highly cyclical and changes in demand can occur abruptly in the geographic markets we serve. As a result of this cyclicality, we have experienced significant fluctuations in our sales, which, in periods of reduced demand have adversely affected our results of operations and financial condition. Our international operations pose additional risks that may adversely impact sales and earnings. During the fiscal year ended October 31, 2008, more than 75% of our revenues were derived from sales to customers located outside the United States. We also have manufacturing facilities and assets located outside of the United States. These international operations are subject to a number of risks, including:

• trade barriers • regional economic uncertainty • differing labor regulation • risk of governmental expropriation • domestic and foreign customs and tariffs • current and changing regulatory environments affecting the importation and exportation of

products and raw materials • difficulty in obtaining distribution support • difficulty in staffing and managing widespread operations • differences in the availability and terms of financing • political instability and unrest • risks of changes in taxes • tax implications from repatriation of funds

Quotas, tariffs, taxes or other trade barriers could require us to change manufacturing sources, reduce prices, increase spending on marketing or product development, withdraw from or not enter certain markets or otherwise take actions that could be adverse to us. Also, in some foreign jurisdictions, we may be subject to laws limiting the right and ability of entities organized or operating therein to pay dividends or remit earnings to affiliated companies unless specified conditions are met. These factors may adversely affect our future operating results. All of our products are shipped from our manufacturing facility in Taiwan from the Port of Taichung to three ports of destination: Los Angeles, California, Venlo, the Netherlands, and Singapore. Changes in customs requirements, as a result of national security or other constraints put upon these ports, may also have an adverse impact on our results of operations.

We depend on limited sources for our products. Our wholly owned subsidiary in Taiwan, Hurco Manufacturing Ltd. (HML), produces all of our machine tools. Any interruption in manufacturing at HML would have a material adverse effect on our results of operations and financial condition. Interruption in manufacturing at HML could result from a change in the political environment in Taiwan or a natural disaster, such as an earthquake, typhoon, or tsunami. Any interruption with one of our key component suppliers may also have a material adverse effect on our results of operations and financial condition.

10

Fluctuations in the exchange rates between the U.S. Dollar and any of several foreign currencies can increase our costs or decrease our revenues. Our international sales divisions generate more than 75% of our revenues, which are received in several foreign currencies, primarily the Euro and Pound Sterling. Therefore, our results of operations and financial condition are affected by fluctuations in exchange rates between these currencies and the U.S. Dollar, both for purposes of actual conversion and for financial reporting purposes. In addition, payments for components incorporated into our products are made in the New Taiwan Dollar. We hedge our foreign currency exposure with the purchase of forward exchange contracts. Hedge contracts only mitigate the impact of changes in foreign currency rates that occur during the term of the related hedge contract period. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 1 of Notes to Consolidated Financial Statements for the impact of translation of foreign currencies and hedging on the consolidated financial statements. Our competitive position and prospects for growth may be diminished if we are unable to develop and introduce new and enhanced products on a timely basis that are accepted in the market. The machine tool industry is subject to technological change, evolving industry standards, changing customer requirements, and improvements in and expansion of product offerings. Our ability to anticipate changes in technology, industry standards, customers’ requirements and competitors’ product offerings and to develop and introduce new and enhanced products on a timely basis that are accepted in the market, will be significant factors in maintaining and improving our competitive position and growth prospects. If the technologies or standards used in our products become obsolete or fail to gain widespread commercial acceptance, our business would be materially adversely affected. Although we believe that we have the technological capabilities to remain competitive, developments by others may render our products or technologies obsolete or noncompetitive. We compete with larger companies that have greater financial resources, and our business could be harmed by competitors’ actions. The markets in which our products are sold are extremely competitive and highly fragmented. In marketing our products, we compete with other manufacturers in terms of quality, reliability, price, value, delivery time, service and technological characteristics. We compete with a number of U.S., European and Asian competitors, most of which are larger, have substantially greater financial resources and are supported by governmental or financial institution subsidies. While we believe our product lines compete effectively, our financial resources are limited compared to those of most of our competitors, making it challenging to remain competitive. Fluctuation of the price of raw materials, especially steel and iron, could adversely affect our sales, costs and profitability. We manufacture products with a high iron and steel content for which worldwide prices can change significantly. The availability and price for these and other raw materials are subject to volatility due to worldwide supply and demand forces, speculative actions, inventory levels, exchange rates, production costs and anticipated or perceived shortages. In some cases, those cost increases can be passed on to customers in the form of price increases; in other cases they cannot. If the prices of raw materials increase and we are not able to charge our customers higher prices to compensate, it would adversely affect our results of operations. Due to future changes in technology, changes in market demand, or changes in market expectations, portions of our inventory may become obsolete or excess. The technology within our products changes and generally new versions of machines are brought to market in three to five year cycles. The phasing out of an old product involves estimating the amount of inventory to hold to satisfy the final demand for those machines and to satisfy future repair part needs. Based on changing customer demand and expectations of delivery times for repair parts, we may find that

11

we have either obsolete or excess inventory on hand. Because of unforeseen future changes in technology, market demand or competition, we might have to write off unusable inventory, which would adversely affect our results of operations. We may make acquisitions that could disrupt our operations and harm our operating results. Although we are not currently engaged in negotiations, and have no current plans for any acquisitions, we may seek to expand our product offerings or the markets we serve by acquiring other companies, product lines, technologies and personnel. Acquisitions involve numerous risks, including the following:

• difficulties integrating the operations, technologies, products, and personnel of the acquired companies

• diversion of management’s attention from normal daily operations of the business • potential difficulties completing projects associated with in-process research and development • difficulties entering markets in which we have no or limited prior experience, especially when

competitors in such markets have stronger market positions • initial dependence on unfamiliar supply chains or relatively small supply partners • insufficient revenues to offset increased expenses associated with acquisitions • the potential loss of key employees of the acquired companies

Acquisitions may also cause us to:

• issue common stock that would dilute our current shareholders’ percentage ownership • assume liabilities • record goodwill and non-amortizable intangible assets that will be subject to impairment testing

on a regular basis and potential periodic impairment charges • incur amortization expenses related to certain intangible assets • incur large and immediate write-offs, and restructuring and other related expenses • become subject to litigation

Mergers and acquisitions are inherently risky. No assurance can be given that our acquisitions will be successful. Further, no assurance can be given that acquisitions will not adversely affect our business, operating results, or financial condition. Failure to manage and successfully integrate acquisitions could harm our business and operating results in a material way. Even when an acquired company has already developed and marketed products, there can be no assurance that product enhancements will be made in a timely manner or that pre-acquisition due diligence will identify all possible issues that might arise with respect to such products. Risks related to new product development also apply to acquisitions. For additional information, please see the risk factor above entitled, “Due to future changes in technology, changes in market demand, or changes in market expectations, portions of our inventory may become obsolete or excess.” Intangible or other assets may become impaired, requiring us to record a significant charge to earnings. Under U.S. Generally Accepted Accounting Principles, we review our assets for impairment when events or changes in circumstances indicate the carrying value may not be recoverable. Intangible assets and our investment accounted for under the equity method are required to be tested for impairment at least annually. We could be required to record a significant charge to earnings in our financial statements for the period in which any impairment of these assets is determined, which would adversely affect our results of operations for that period.

12

Our continued success depends on our ability to protect our intellectual property. Our future success depends in part upon our ability to protect our intellectual property. We rely principally on nondisclosure agreements, other contractual arrangements, trade secret law, trademark and patent law, to protect our intellectual property. However, these measures may be inadequate to protect our intellectual property from infringement by others or prevent misappropriation of our proprietary rights. In addition, the laws of some foreign countries do not protect proprietary rights to the same extent as do U.S. laws. Our inability to protect our proprietary information and enforce our intellectual property rights through infringement proceedings could have a material adverse effect on our business, financial condition and results of operations. The unplanned loss of current members of our senior management team and other key personnel may adversely affect our operating results. The unexpected loss of senior management or other key personnel could impair our ability to carry out our business plan. We believe that our future success will depend in part on our ability to attract and retain highly skilled and qualified personnel. The loss of senior management or other key personnel may adversely affect our operating results as we incur costs to replace the departed personnel and potentially lose opportunities in the transition of important job functions. Item 1B. UNRESOLVED STAFF COMMENTS None.

13

Item 2. PROPERTIES The following table sets forth the location, size and principal use of each of our facilities:

Location Square Footage Principal Uses Indianapolis, Indiana 165,000 (1) Corporate headquarters, design and

engineering, product testing, sales and marketing, application engineering and customer service

Los Angeles, California 13,000 Warehouse, distribution, sales, application

engineering and customer service Dexter, Michigan 3,000 Sales, design engineering, product testing

and customer service Mississauga, Canada

3,600 Sales, application engineering andcustomer service

High Wycombe, England 12,000 Sales, application engineering and

customer service Paris, France 9,700 Sales, application engineering and

customer service Munich, and Rodermark, Germany

26,000 Sales, application engineering andcustomer service

Milan and Venice, Italy 13,000 Sales, application engineering and

customer service Singapore 9,300 Sales, application engineering and

customer service Shanghai, China 8,000 Sales, application engineering and

customer service Guangzhou, China 2,400 Sales, application engineering and

customer service Chennai, India 5,400 Sales, application engineering and

customer service Liegnitz, Poland 2,900 Sales, application engineering and

customer service Taichung, Taiwan 221,000 Manufacturing Ningbo, China 34,000 Manufacturing (1) Approximately 50,000 square feet is leased to a third-party under a lease, which expires April 30, 2010.

We own the Indianapolis facility and lease all other facilities. The leases have terms expiring at various dates ranging from September 2009 to May 2017. We believe that all of our facilities are well maintained and are adequate for our needs now and in the foreseeable future. We do not believe that we would experience any difficulty in replacing any of the present facilities if any of our leases were not renewed at expiration.

14

Item 3. LEGAL PROCEEDINGS

We are involved in various claims and lawsuits arising in the normal course of business. We do not expect any of these claims, individually or in the aggregate, to have a material adverse effect on our financial position or results of operations. Item 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS None. Executive Officers of the Registrant Executive officers are elected each year by the Board of Directors at the first board meeting following the Annual Meeting of Shareholders to serve during the ensuing year and until their respective successors are elected and qualified. There are no family relationships between any of our executive officers or between any of them and any of the members of the Board of Directors. The following information sets forth as of October 31, 2008, the name of each executive officer and his or her age, tenure as an officer, principal occupation and business experience for the last five years: Name Age Position(s) with the CompanyMichael Doar 53 Chairman of the Board and Chief Executive Officer James D. Fabris 57 President and Chief Operating OfficerJohn G. Oblazney 40 Vice President, Secretary, Treasurer and Chief Financial OfficerSonja K. McClelland 37 Corporate Controller, Assistant Secretary

Michael Doar was elected Chairman of the Board and Chief Executive Officer on November 14, 2001. Mr. Doar had held various management positions with Ingersoll Milling Machine Company from 1989 until 2001. Mr. Doar has been a director of Hurco since 2000. James D. Fabris was elected President and Chief Operating Officer on November 14, 2001. Mr. Fabris served as Executive Vice President - Operations from November 1997 until his current appointment and previously served as a Vice President of Hurco since February 1995. John G. Oblazney was elected Vice President, Secretary, Treasurer and Chief Financial Officer in September 2006. Prior to joining us, Mr. Oblazney served as the Chief Financial Officer of Carrier Corporation’s Light Commercial Business, a division of United Technologies Corporation, since December 2005. Prior to that, Mr. Oblazney served in various other financial positions with Carrier Corporation from 2000 to 2005. Prior to joining Carrier Corporation, Mr. Oblazney was employed for six years with Cooper Industries and employed three years by an international public accounting firm. Sonja K. McClelland has been employed by Hurco since September 1996 and was elected Corporate Controller, Assistant Secretary in November 2004. Ms. McClelland served as Corporate Accounting Manager from September 1996 to 1999, then as Division Controller for Hurco USA from September 1999 to November 2004. Prior to joining Hurco, Ms. McClelland was employed for three years by an international public accounting firm.

15

PART II Item 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES Our common stock is traded on the Nasdaq Global Select Market under the symbol “HURC”. The following table sets forth the high and low sale prices of the shares of our common stock for the periods indicated, as reported by the Nasdaq Global Select Market. 2008 2007Fiscal Quarter Ended: High Low High Low January 31 .............................................. $58.68 $30.24 $33.18 $24.61 April 30.................................................. 52.12 33.41 47.86 33.07 July 31 ................................................... 49.30 23.11 56.28 39.12 October 31 ............................................. 38.24 16.92 60.44 39.77 At January 7, 2009, the closing price of our common stock on the Nasdaq Global Select Market was $14.76. We do not currently pay dividends on our common stock and intend to continue to retain earnings for working capital, and capital expenditures. There were186 holders of record of our common stock as of January 7, 2009. During the period covered by this report, we did not sell any equity securities that were not registered under the Securities Act of 1933, as amended. The disclosure under the caption “Equity Compensation Plan Information” is included in Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

16

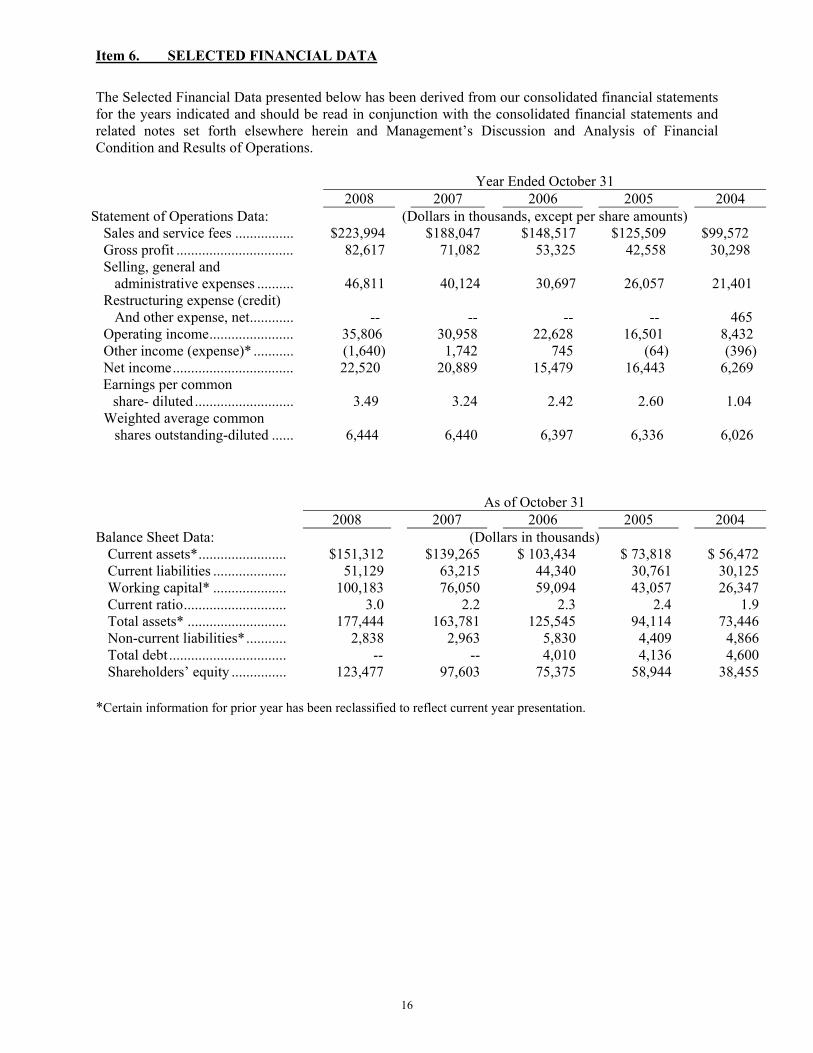

Item 6. SELECTED FINANCIAL DATA

The Selected Financial Data presented below has been derived from our consolidated financial statements for the years indicated and should be read in conjunction with the consolidated financial statements and related notes set forth elsewhere herein and Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Year Ended October 31 2008 2007 2006 2005 2004 Statement of Operations Data: (Dollars in thousands, except per share amounts) Sales and service fees ................ $223,994 $188,047 $148,517 $125,509 $99,572 Gross profit ................................ 82,617 71,082 53,325 42,558 30,298 Selling, general and administrative expenses ..........

46,811 40,124 30,697

26,057 21,401

Restructuring expense (credit) And other expense, net ............

-- -- --

--

465

Operating income ....................... 35,806 30,958 22,628 16,501 8,432 Other income (expense)* ........... (1,640) 1,742 745 (64) (396) Net income ................................. 22,520 20,889 15,479 16,443 6,269 Earnings per common share- diluted ...........................

3.49 3.24 2.42

2.60 1.04

Weighted average common shares outstanding-diluted ......

6,444 6,440 6,397

6,336 6,026

As of October 31 2008 2007 2006 2005 2004 Balance Sheet Data: (Dollars in thousands) Current assets* ........................ $151,312 $139,265 $ 103,434 $ 73,818 $ 56,472 Current liabilities .................... 51,129 63,215 44,340 30,761 30,125 Working capital* .................... 100,183 76,050 59,094 43,057 26,347 Current ratio ............................ 3.0 2.2 2.3 2.4 1.9 Total assets* ........................... 177,444 163,781 125,545 94,114 73,446 Non-current liabilities* ........... 2,838 2,963 5,830 4,409 4,866 Total debt ................................ -- -- 4,010 4,136 4,600 Shareholders’ equity ............... 123,477 97,603 75,375 58,944 38,455

*Certain information for prior year has been reclassified to reflect current year presentation.

17

Item 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS EXECUTIVE OVERVIEW Hurco Companies, Inc. is an industrial technology company operating in a single segment. We design and produce computerized machine tools, featuring our proprietary computer control systems and software, for sale through our own distribution network to the worldwide metal cutting market. We also provide software options, control upgrades, accessories and replacement parts for our products, as well as customer service and training support. The following overview is intended to provide a brief explanation of the principal factors that have contributed to our financial performance. This overview is intended to be read in conjunction with the more detailed information that follows and our audited financial statements that appear elsewhere in this report. The primary drivers of our operational performance in the past three years have been improved worldwide demand for our products, the increasing acceptance of our expanded product line and our success in selling and manufacturing outside of the United States. The market for machine tools is an international market. We have both significant foreign sales and manufacturing operations. During fiscal 2008, more than 75% of our revenues were attributable to customers located abroad. The percentage of revenues to customers located abroad has increased during the last fiscal year due in part to deterioration of the North American market for machine tool products, as well as the effect of a weaker U.S. Dollar when translating foreign sales to U.S. Dollars for financial reporting purposes. We sell our products through more than 100 independent agents and distributors in countries throughout North America, Europe and Asia. We also have our own direct sales and service organizations in Canada, France, Germany, Italy, Singapore and the United Kingdom. Our computerized metal cutting machine tools are manufactured in Taiwan to our specifications by our wholly owned subsidiary, Hurco Manufacturing Limited (HML). Our sales to foreign customers are denominated, and payments by those customers are made in the prevailing currencies—primarily the Euro and Pound Sterling—in the countries in which those customers are located, and our product costs are incurred and paid primarily in the New Taiwan Dollar and the U.S. Dollar. Changes in currency exchange rates may have a material effect on our operating results and consolidated balance sheets as reported under U.S. Generally Accepted Accounting Principles. For example, when a foreign currency increases in value relative to the U.S. Dollar, sales made (and expenses incurred) in that currency, when translated to U.S. Dollars for reporting in our financial statements, are higher than would be the case when that currency has a lower value relative to the U.S. Dollar. In our comparison of period-to-period results, we discuss not only the increases or decreases in those results as reported in our financial statements (which reflect translation to U.S. Dollars at exchange rates prevailing during the period covered by those financial statements), but also the effect that changes in exchange rates had on those results. For additional information on the impact of translation of foreign currencies and our hedging practices, see Note 1 of Notes to Consolidated Financial Statements. Our high levels of foreign manufacturing and sales also subject us to cash flow risks due to fluctuating currency exchange rates. We seek to mitigate those risks through the use of various derivative instruments – principally foreign currency forward exchange contracts. We experienced changes in material costs from inflation in fiscal 2008, which caused our gross margin to decline. While some material costs have recently declined, our production cycle of approximately six months requires us to establish material costs at the time a purchase order is accepted, when costs may have been higher. Government sources have confirmed that the U.S. economy has been in a recession since December 2007. We first experienced a decline in sales orders in our North American market during the first quarter of

18

fiscal 2008. The deterioration in that market continued and became more severe in subsequent quarters. During the second half of calendar year 2008, the recession became global in scope, impacting every market we serve and significantly affecting our sales and orders during the fourth fiscal quarter. Our sales in the fourth quarter of fiscal 2008 were 5.3% lower than in the corresponding quarter of fiscal 2007 and, most significantly, 17.2% below those of the third quarter of 2008. Similarly, our new orders in the fourth quarter of fiscal 2008 declined 27.0% from their level in the corresponding quarter of fiscal 2007 and 23.7% below the third quarter of fiscal 2008. Economic conditions have continued to worsen since the beginning of fiscal 2009. Many economists have indicated that the current deterioration in the global markets will remain or become more severe and continue for a prolonged period of time. During the fourth quarter, we implemented various initiatives to reduce expenses while staying committed to our strategic plan of product innovation and penetration of developing markets. We have also taken steps to reduce our inventories to reflect the decline in customer demand. Since our production lead time is approximately six months, the impact of reduced production levels on our inventories may take several quarters to be fully realized. We believe that, notwithstanding the severity of the current economic crisis, our company remains fundamentally stable. We have a broad product line due to recent new product introductions, no outstanding debt and a strong cash position. Results of Operations The following table presents, for the fiscal years indicated, selected items from the Consolidated Statements of Income expressed as a percentage of our worldwide sales and service fees and the year-to-year percentage changes in the dollar amounts of those items. Percentage of Revenues Year-to-Year % Change 2008 2007 2006 Increase (Decrease) ’08 vs. ’07 ’07 vs. ’06 Sales and service fees ........... 100.0% 100.0% 100.0% 19.1% 26.6% Gross profit .......................... 36.9% 37.8% 35.9% 16.2% 33.3% Selling, general and administrative expenses ....

20.9%

21.3%

20.7%

16.7%

30.7%

Operating income ................. 16.0% 16.5% 15.2% 15.7% 36.8% Other income (expense)* ..... (0.7%) 0.9% 0.5% (194.1%) 133.8% Net income ........................... 10.1% 11.1% 10.4% 7.8% 35.0% *Certain information for prior years has been reclassified to reflect current year presentation. Fiscal 2008 Compared to Fiscal 2007 Sales and Service Fees. Notwithstanding the severe decline in the fourth quarter of fiscal 2008, annual sales and service fees were the highest in our 40-year history, totaling $224.0 million, an increase of $35.9 million, or 19.1%, over fiscal 2007. Of this increase, $22.7 million was attributable to operational growth and approximately $13.2 million was due to the favorable effect of a weakening U.S. Dollar on currency translation. Computerized machine tool sales, which also were the highest in our history, totaled $199.2 million, an increase of 20.1% from the $165.8 million recorded in 2007, primarily driven by strong customer demand in European markets during the first nine months of the fiscal year, particularly for our higher end VMX product line.

19

Net Sales and Service Fees by Geographic Region The following table sets forth net sales and service fees by geographic region for the years ended October 31, 2008 and 2007 (in thousands): October 31, Increase (Decrease) 2008 2007 Amount % North America $ 48,373 21.6% $ 52,133 27.7% $ (3,760) (7.2%) Europe 163,807 73.1% 125,446 66.7% 38,361 30.6% Asia Pacific 11,814 5.3% 10,468 5.6% 1,346 12.9%

Total $223,994 100.0% $188,047 100.0% $ 35,947 19.1% In North America, sales and service fees decreased 7.2% as unit volumes decreased by 14.9% primarily in the second half of the year as a result of the global economic slowdown. This decrease in volume was partially offset by improved product mix. European sales and service fees increased by 30.6%, which includes a favorable impact due to changing currency rates of $12.4 million, or 9.9%. Unit sales increased by 11.5% in fiscal 2008 compared to fiscal 2007 as a result of a strong European market during the first three quarters of the fiscal year and continued expansion into eastern European markets. The remaining 9.2% of growth in European sales and service fees was primarily derived by continued demand for our higher end VMX product line. Sales and service fees in the Asia Pacific region increased by 12.9%, due to penetration into new markets along with the favorable impact of changes due to currency exchange rates of $778,000, or 7.4%. Net Sales and Service Fees by Product Category The following table sets forth net sales and service fees by product category for the years ended October 31, 2008 and 2007 (in thousands): October 31, Increase 2008 2007 Amount % Computerized Machine Tools $199,238 88.9% $165,832 88.2% $33,406 20.1% Service Fees, Parts and Other 24,756 11.1% 22,215 11.8% 2,541 11.4% Total $223,994 100.0% $188,047 100.0% $35,947 19.1%

Sales of computerized machine tools totaled $199.2 million in fiscal 2008, an increase of $33.4 million, or 20.1%, primarily driven by a strong European market and continued demand for our higher end VMX product line. Orders and Backlog. New order bookings in fiscal 2008, were $212.5 million, an increase of $13.6 million, or 6.8%, over the prior year. Orders for fiscal 2008 compared to fiscal 2007 were favorably affected by approximately $11.7 million, or 5.9%, due to changes in currency exchange rates. Unit orders increased 1.1% in Europe and decreased by 18.0% and 11.5% in North America and Asia Pacific, respectively. These order rates were significantly impacted by an overall fourth quarter decline in unit orders of 32.4%. Orders declined in all regions as our customers reacted to the sudden downturn in the markets they serve and limitations on their own ability to access the credit markets. Backlog was $15.7 million at October 31, 2008, compared to $29.4 million at October 31, 2007. We do not believe backlog is a useful measure of past performance or indicative of future performance. Backlog orders as of October 31, 2008 are expected to be fulfilled in fiscal 2009.

20

Gross Margin. Gross margin for fiscal 2008 was 36.9%, a decrease from the 37.8% margin realized in the corresponding 2007 period, reflecting the impact of higher material costs. Operating Expenses. Selling, general and administrative expenses for fiscal 2008 increased $6.7 million, or 16.7%, from those of fiscal 2007 and includes the unfavorable effect of currency translation of $2.2 million, or 5.6%. The remaining increase of $4.5 million was attributable to increased global sales and marketing expenditures, which include increased expenses for trade shows, European agent sales commissions and marketing expenses for expansion of sales into emerging markets. Operating Income. Operating income for fiscal 2008 totaled $35.8 million, or 16.0% of sales, compared to $31.0 million, or 16.5%, of sales, in fiscal 2007. The increase in operating income year-over-year primarily reflected growth in foreign sales and an improved product mix partially offset by higher material costs and operating expenses to support sales growth initiatives. Other Income (Expense). The decrease in other income of $3.4 million for fiscal 2008 compared to fiscal 2007 was primarily due to $2.3 million of currency exchange losses on inter-company receivables and payables denominated in foreign currencies, net of gains or losses on forward exchange contracts. Included in this decrease was approximately $220,000 of net losses related to cash flow hedges of forecasted inter-company sales and purchases that were de-designated as production levels steeply declined in the fourth quarter of fiscal 2008. Additionally, fiscal 2007 included income from our equity investment in a Taiwan contract manufacturer, which was sold during the fourth quarter of that year. Provision for Income Taxes. The effective tax rate for fiscal 2008 was 34.1%, compared to 36.2% for the same period in the prior year. The reduction in the effective tax rate was primarily due to the utilization of tax credits and tax rates of international jurisdictions that were less than U.S. statutory rates. Net Income. Net income for fiscal 2008 was $22.5 million, or $3.49 per share, which is an increase of 7.8% over fiscal 2007 net income of $20.9 million, or $3.24 per share. Fiscal 2007 Compared to Fiscal 2006 Sales and Service Fees. Sales and service fees for fiscal 2007 were $188.0 million, an increase of $39.5 million, or 26.6%, over fiscal 2006. Of this increase, $28.5 million was attributable to operational growth and approximately $11.0 million was due to the favorable effect of a weakening U.S. Dollar on currency translation. Computerized machine tool sales totaled $165.8 million, an increase of 28.6% from the $128.9 million recorded in 2006, primarily driven by strong worldwide demand for our products and an increase in the percentage of sales attributable to higher price machines as a result of our expanded product line. Net Sales and Service Fees by Geographic Region The following table sets forth net sales and service fees by geographic region for the years ended October 31, 2007 and 2006 (in thousands): October 31, Increase 2007 2006 Amount % North America $ 52,133 27.7% $ 50,563 34.0% $ 1,570 3.1% Europe 125,446 66.7% 87,735 59.1% 37,711 43.0% Asia Pacific 10,468 5.6% 10,219 6.9% 249 2.4%

Total $188,047 100.0% $148,517 100.0% $ 39,530 26.6% In North America, sales and service fees increased 3.1% primarily due to improved mix as unit sales volumes decreased by 4.7% a result of general weakening in demand for the domestic machine tool market.

21

European sales and service fees increased by 43.0%, which includes a favorable impact due to changing currency rates of $10.5 million, or 11.9%. Unit sales increased by 28.0% in fiscal 2007 compared to fiscal 2006 as a result of a strong European market and continued expansion into eastern European markets. The remaining 15.0% of growth in European sales and service fees was primarily derived by continued demand for our higher end VMX product line. Sales and service fees in the Asia Pacific region increased by 2.4%, due to increased volume of larger higher priced machines, partially offset by a 10.1% decline in overall unit volume. The effect of a weaker U.S. Dollar when translating foreign sales for financial reporting purposes had a favorable impact of approximately $539,000, or 5.3%, on this region’s sales comparison for the full year. Net Sales and Service Fees by Product Category The following table sets forth net sales and service fees by product category for the years ended October 31, 2007 and 2006 (in thousands): October 31, Increase 2007 2006 Amount % Computerized Machine Tools $165,832 88.2% $128,946 86.8% $36,886 28.6% Service Fees, Parts and Other 22,215 11.8% 19,571 13.2% 2,644 13.5% Total $188,047 100.0% $148,517 100.0% $39,530 26.6%