38

©2008 Pearson Prentice Hall. All rights reserved. 5-1 Short-Term Investments & Receivables Chapter 5

©2008 Pearson Prentice Hall. All rights reserved.

5-1

Short-Term Investments & Receivables

Chapter 5

©2008 Pearson Prentice Hall. All rights reserved.

5-2

Learning Objective 1

Account for short-term investments

©2008 Pearson Prentice Hall. All rights reserved.

5-3

Accounting for Short-Term Investments

• Also called marketable securities

• Held for one year or less

• Most liquid asset other than cash

• Placed into three categories:

Trading Investments

Available-for-Sale

Held-to-Maturity

©2008 Pearson Prentice Hall. All rights reserved.

5-4

Trading Investments

• Held for short time and then sold Gain or loss recorded

• Dividend revenue may also be received

• At year-end, trading investments are adjusted to equal their market value Results in an unrealized gain or loss

Selling price > cost = Gain Selling price < cost = Loss

©2008 Pearson Prentice Hall. All rights reserved.

5-5

Unrealized Gains & Losses

• Difference between market price and cost of investment at year-end

• Unrealized – investment has not been sold

Market price > cost =

Unrealized gain

Market price < cost =

Unrealized loss

©2008 Pearson Prentice Hall. All rights reserved.

5-6

Realized vs. Unrealized

Realized• Investment sold to

third party• Gain or loss =

difference between selling price and cost

• Word “realized” usually dropped from title

Unrealized • Company still owns

investment• Gain or loss =

difference between market value and cost

• Word “unrealized” is kept in account title

©2008 Pearson Prentice Hall. All rights reserved.

5-7

Entries to Adjust to Market

JOURNAL

Date Accounts Debit Credit

Short-term investments $$$

Unrealized gain on investments $$$

Adjusted investment to market value (when greater than cost)

Unrealized loss on investments $$$

Short-term investments $$$

Adjusted investment to market value (when less than cost)

©2008 Pearson Prentice Hall. All rights reserved.

5-8

Reporting on Financial Statements

Balance Sheet• Trading Investment

Reported at current market value

Listed directly under “cash” in the current asset section

Income Statement• Gains and losses

From sales of investments

• Investment revenue From dividends or

interest earned

• Unrealized gain or loss From entry to adjust to

market value

©2008 Pearson Prentice Hall. All rights reserved.

5-9

E5-18

JOURNAL

Date Accounts Debit Credit

Nov 6 Trading investment $35,000

Cash $35,000

Nov 27 Cash $850

Dividend revenue $850

©2008 Pearson Prentice Hall. All rights reserved.

5-10

E5-18

JOURNAL

Date Accounts Debit Credit

12-31 Unrealized loss _______

Trading Investments ________

What would be the amount of the

unrealized loss?

Compute the difference between the cost and

market value.

©2008 Pearson Prentice Hall. All rights reserved.

5-11

E5-18

JOURNAL

Date Accounts Debit Credit

1-11 Cash $36,000

Trading Investments $33,000

Gain on sale of investments $3,000

©2008 Pearson Prentice Hall. All rights reserved.

5-12

Receivables

• Monetary claims against others

• Third most liquid asset

• Accounts Receivable Amounts owed by customers for selling goods

or services

• Notes Receivable Lending money to outsiders More formal than accounts receivable

©2008 Pearson Prentice Hall. All rights reserved.

5-13

Learning Objective 2

Apply internal controls to receivables

©2008 Pearson Prentice Hall. All rights reserved.

5-14

Internal Control over Cash Collections on Account

• Separate cash-handling from cash-accounting duties

• Cash-handling One person receives customer checks and

makes deposits

• Cash-accounting Another person makes entries to customer

accounts

©2008 Pearson Prentice Hall. All rights reserved.

5-15

Accounting for Uncollectible Receivables

• Extending credit to customers bears some risk

• Risk: Some customers do not pay the amount owed

• Cost: Uncollectible accounts

©2008 Pearson Prentice Hall. All rights reserved.

5-16

Learning Objective 3

Use the allowance method for uncollectible receivables

©2008 Pearson Prentice Hall. All rights reserved.

5-17

Allowance Method

• Amount of uncollectible accounts is estimated

• An expense is recorded as part of the adjusting process

• A contra-asset is recorded that reduces accounts receivable on the balance sheet

A contra-asset is always pairedwith an asset and reduces

its balance

©2008 Pearson Prentice Hall. All rights reserved.

5-18

Entry to Record Uncollectible accounts

JOURNAL

Date Accounts Debit Credit

Uncollectible accounts expense

Allowance for uncollectible accounts

Goes on theIncome Statement

Goes on the Balance Sheet netted with accounts receivable

©2008 Pearson Prentice Hall. All rights reserved.

5-19

Balance Sheet

Current assets:

Accounts receivable $$,$$$

Less: Allowance for

Uncollectible Accounts ( $,$$$)

Accounts receivable, net $$,$$$

Accounts receivable, net $$,$$$

OR

©2008 Pearson Prentice Hall. All rights reserved.

5-20

Methods to Estimate Uncollectibles

Percent-of-sales• Expense is estimated

based on credit sales• Income Statement

approach

Aging-of-receivables• Accounts receivable

analyzed based on how long outstanding

• Balance Sheet approach

©2008 Pearson Prentice Hall. All rights reserved.

5-21

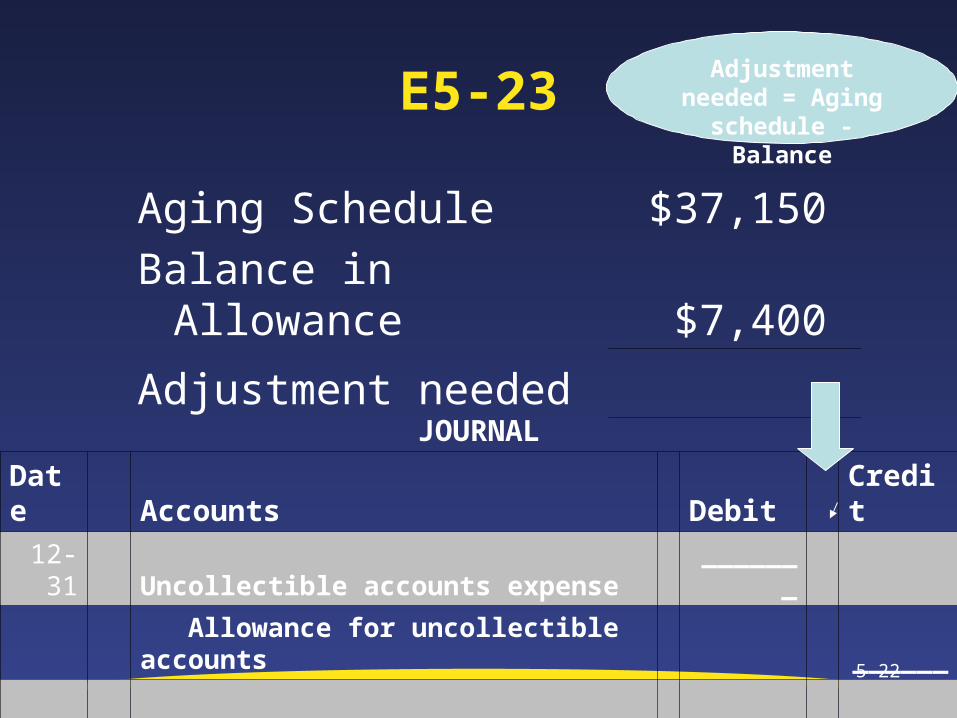

E5-23

Age of Accounts

1 - 30 Days 31 - 60 Days 61 - 90 Days Over 90 Days

$ 110,000 $ 60,000 $ 50,000 $ 15,000

0.5% 1% 60% 40%

$ 550 $ 600 $ 30,000 $ 6,000

$37,150

©2008 Pearson Prentice Hall. All rights reserved.

5-22

E5-23

Aging Schedule $37,150

Balance in Allowance $7,400

Adjustment needed

JOURNAL

Date Accounts Debit Credit

12-31 Uncollectible accounts expense _______

Allowance for uncollectible accounts ______

Adjustment needed = Aging schedule -

Balance

©2008 Pearson Prentice Hall. All rights reserved.

5-23

E5-23

Allowance for Uncollectible Accounts

$7,400 Balance before adjustment

$37,150 Balance per aging schedule

$29,750Adjusting entry

©2008 Pearson Prentice Hall. All rights reserved.

5-24

Uncollectible Accounts Methods

Percent-of-Sales Aging-of-Receivables

Adjust Allowance for Uncollectible Accounts

Adjust Allowance for Uncollectible Accounts

BY TO

The Amount of UNCOLLECTIBLE ACCOUNT

EXPENSE

The Amount of UNCOLLECTIBLE ACCOUNTS

RECEIVABLE

©2008 Pearson Prentice Hall. All rights reserved.

5-25

Writing Off a Specific Account

• The allowance is used to absorb specific accounts that are determined to uncollectible

• When it’s determined a customer cannot pay, the following entry is made:

JOURNAL

Date Accounts Debit Credit

Allowance for uncollectible accounts $$$$

Accounts receivable $$$$

©2008 Pearson Prentice Hall. All rights reserved.

5-26

Direct Write-Off Method

• Less preferable than allowance method Does not match expenses with revenues Accounts Receivable overstated

• Uncollectible Accounts Expense used for write offs

• No Allowance for Uncollectible Accounts

©2008 Pearson Prentice Hall. All rights reserved.

5-27

Accounts Receivable

Sales on account Payments on account

Uncollectible accounts written off

©2008 Pearson Prentice Hall. All rights reserved.

5-28

Allowance for Uncollectible Accounts

Uncollectible accounts written off

Uncollectible account adjustment

What is the normal balance of

the Allowance?

©2008 Pearson Prentice Hall. All rights reserved.

5-29

Learning Objective 4

Account for notes receivable

©2008 Pearson Prentice Hall. All rights reserved.

5-30

Notes Receivable Terms

• Creditor

• Debtor

• Interest

• Maturity Date

• Maturity Value

• Principal

• Term

Party to whom money is owed; lender

Date debtor must pay the note

Sum of principal and interest on note

Amount borrowed by debtor

Length of time money is borrowed

Party that owes money; borrower

Cost of borrowing money; percent

©2008 Pearson Prentice Hall. All rights reserved.

5-31

Accounting for Notes Receivable

• To record the receipt of a note receivable, the following entry is made:

JOURNAL

Date Accounts Debit Credit

Notes Receivable $$,$$$

Cash $$,$$$

©2008 Pearson Prentice Hall. All rights reserved.

5-32

Accounting for Notes Receivable

• Interest needs to be accrued on any note receivable outstanding at year end:

JOURNAL

Date Accounts Debit Credit

Interest receivable $$,$$$

Interest revenue $$,$$$

Interest is computed by the formula:Principal x rate x time

Time = date note issigned to end-of-year

©2008 Pearson Prentice Hall. All rights reserved.

5-33

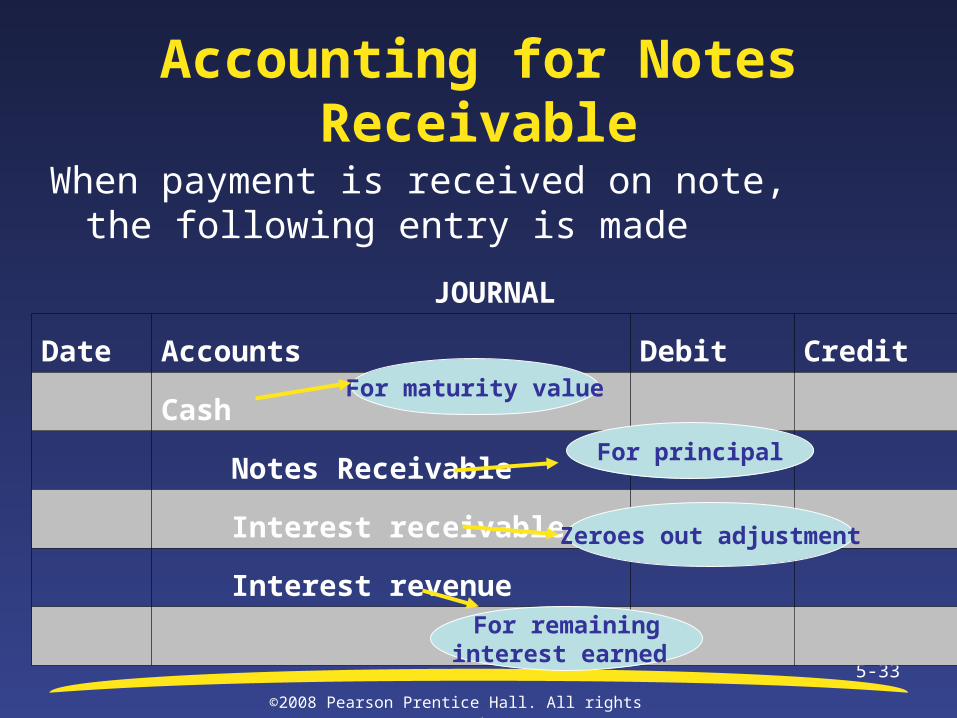

Accounting for Notes Receivable

When payment is received on note, the following entry is made

JOURNAL

Date Accounts Debit Credit

Cash

Notes Receivable

Interest receivable

Interest revenue

For maturity value

Zeroes out adjustment

For remaininginterest earned

For principal

©2008 Pearson Prentice Hall. All rights reserved.

5-34

Credit and Bank Card Sales

• Credit Cards American Express and Discover

• Bank Cards VISA and MasterCard

• Both charge the retailer a fee

©2008 Pearson Prentice Hall. All rights reserved.

5-35

Learning Objective 5

Use two new ratios to evaluate a business

©2008 Pearson Prentice Hall. All rights reserved.

5-36

Days’ Sales in Receivables

• How long it takes a company to collect its average amount of receivable

• Compute one day’s sales

• Days’ sales in receivables

Net Sales365 Days

Average receivables

One Day’s Sales

©2008 Pearson Prentice Hall. All rights reserved.

5-37

Acid-Test Ratio

• Also called quick ratio

• A more stringent measure of a company’s ability to pay its current liabilities

Cash + Short-term investments + net receivables

Total current liabilities

©2008 Pearson Prentice Hall. All rights reserved.

5-38

End of Chapter Five