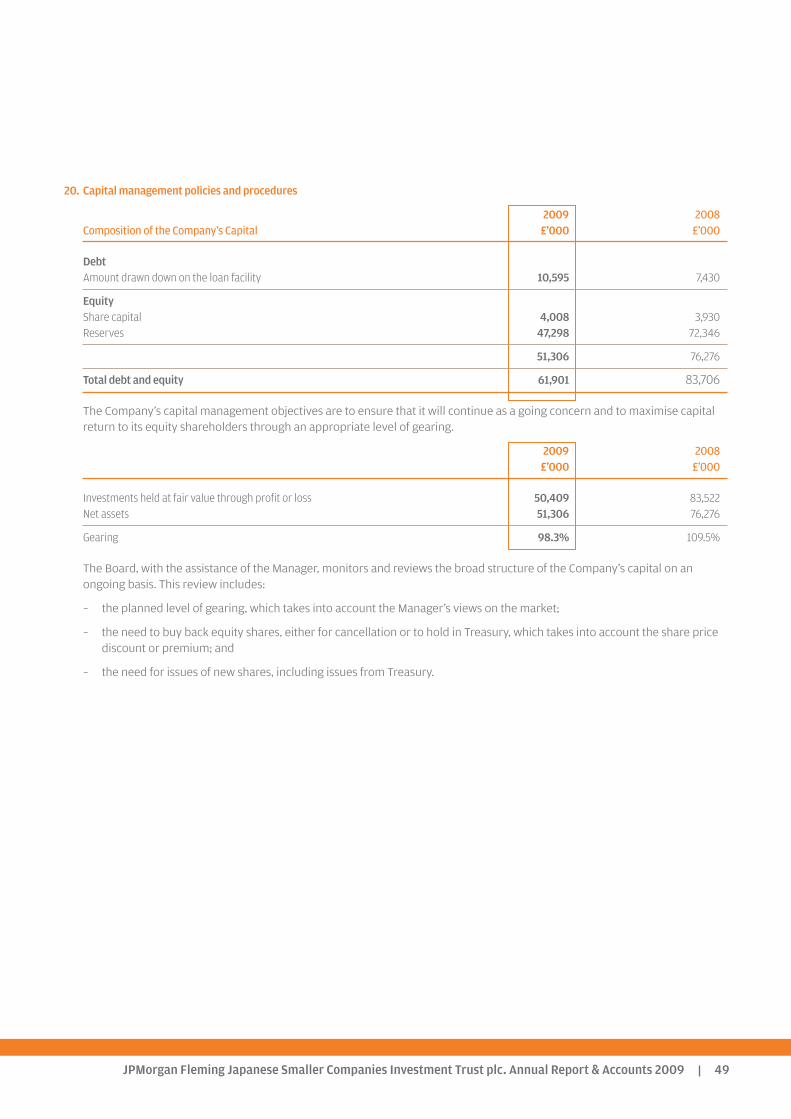

60

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc Annual Report & Accounts for the year ended 31st March 2009 Annual Report 09

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc

Annual Report & Accounts for the year ended 31st March 2009

Annual Report09

Features

Contents

About the Company

1 Financial Results2 Chairman’s Statement

Investment Review

5 Investment Managers’ Report8 Summary of Results9 Performance10 Five Year Financial Record11 Ten Largest Investments12 Sector Analysis13 List of Investments

Directors’ Report

15 Board of Directors16 Directors’ Report23 Corporate Governance

Accounts

27 Directors’ Remuneration Report28 Directors’ Responsibilities in Respect

of the Accounts29 Independent Auditors’ Report31 Income Statement32 Reconciliation of Movements in

Shareholders’ Funds33 Balance Sheet34 Cash Flow Statement35 Notes to the Accounts

Shareholder Information

50 Information about the Company51 Shareholder Analyses 53 Notice of Meeting56 Glossary of Terms

Objective

Long term capital growth through investment in small and medium sized Japanesecompanies.

Investment Policies

- To maintain a portfolio almost wholly invested in Japan.- To restrict the Company’s investment universe to all Japanese quoted companies

excluding the largest 200 measured by market capitalisation.- To utilise borrowings to enhance shareholder returns.- To operate a gearing policy for the Company to within a range of 90% to 120%

invested.- To invest no more than 15% of gross assets in other UK listed investment companies

(including investment trusts).

Further details on investment policies and risk management are given in theDirectors’ Report on page 16.

Benchmark

S&P/Citigroup Japan Extended Market Index (Total Return Net) in sterling terms.Comparison of the Company’s performance is made with the benchmark as stated.

Capital Structure

The Company has an authorised share capital of 100,000,000 Ordinary shares of10p each (of which 39,309,423 were in issue as at 31st March 2009, including 396,000shares held in Treasury) and 10,000,000 Subscription shares of 1p each (of which7,798,873 were in issue as at 31st March 2009).

Management Company

The Company employs JF Asset Management Limited (‘JFAM’) to manage its assetsand JPMorgan Asset Management (UK) Limited (‘JPMAM’) as Secretary.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 1

Financial ResultsTotal Returns (capital plus income)

–35

–30

–25

–20

–15

–10

–5

0

JPMFJSC IT**Peer Group6Jasdaq5TSE25MSJSCI*5Benchmark4

–2.4 –2.9–4.8

–8.8

–31.0–32.2

Japanese Smaller Companies Indices(returns for the year ended 31st March 2009)

–34.4%Return to shareholders1

(2008: –33.9%)

–32.2%Return on net assets2,3

(2008: –28.1%)

–2.4%Benchmark return4

(2008: –19.1%)

* Morgan Stanley Japanese Small Cap Index.

**JPMorgan Fleming Japanese Smaller Companies Investment Trust plc.

A glossary of terms and definitions is provided on page 56.

1Source: Morningstar/J.P. Morgan.2Source: J.P. Morgan.3Assumes that the 396,000 shares held in Treasury at 31st March 2009 were reissued in accordance with the Board’spolicy on the reissuance of Treasury shares.

4Source: Datastream. The Company’s benchmark is the S&P/Citigroup Japan Extended Market Index (Total Return Net)in sterling terms.5Source: Bloomberg.6Japanese smaller companies sector median. Source: Fundamental Data.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 20092

Chairman’s Statement

Investment Performance

Performance for the year to 31st March 2009 was very poor. The Company’s totalreturn on net assets fell 32.2%, which, when compared to a fall of 2.4% in theCompany’s benchmark, the S&P/Citigroup Japan Extended Market Index (TotalReturn Net) in sterling terms, reveals an underperformance of 29.8%. That theCompany’s peer group of comparator funds also performed poorly is of no greatcomfort. Nor is the fact that the market environment was difficult. This is a deeplydisappointing outcome, especially when the Company has seen underperformance inthe previous two financial years. Your Board is extremely concerned to ensure thatthis pattern of underachievement does not continue.

The Investment Managers, both last year and before, have sought to build a portfolioof generally well managed, financially secure companies with comparatively strongoperating performances. Growth companies such as these are invariably the choiceof other active foreign investors, too. When such investors seek to reduce theirpositions in the smaller companies section of the Japanese market, voluntarily orotherwise, it is just these types of stocks which experience persistent selling pressure.During recent past periods of poor market conditions in Japan, growth stocks havesuffered exceptional down-gradings as a consequence, notwithstanding theirgenerally robust operating results. Compared with such unwanted volatility, ourinvestigations show that a large proportion of the shares in our benchmark index aremade up of illiquid stocks which appear not to have traded in any meaningful wayand have not fallen as far as those growth stocks favoured by our own and otheroverseas managers.

Looking ahead, there are increasing signs of a better market outlook which leads usto believe that we should continue with our market positioning and not be temptedto change tack now. The Company’s net asset value has risen in both April and Mayand has outperformed the benchmark. We have a good degree of confidence that theCompany can begin to rebuild its longer term record.

The Investment Managers’ Report on pages 5 to 7 gives a more detailed review of theCompany’s performance and future outlook.

Gearing

The Company has a yen 2.5 billion credit facility with ING Bank which gives theinvestment managers the ability to gear tactically. The facility is due to expire on 28thAugust 2009 and is in the process of being renewed. The Board has given theinvestment managers the flexibility to set gearing within the range of 90% to 120%invested. During the year the investment managers operated between a gearingrange of 98% and 110% and at the time of writing the Company was 118% geared.

Corporate Governance

The Company operates in accordance with corporate governance best practice andthe Board is committed to high standards of corporate governance applicable underthe Combined Code and the ‘Association of Investment Companies’ (‘AIC’) Code ofCorporate Governance for Investment Trusts. Comprehensive compliance statementscan be found in the Corporate Governance section of this report on pages 23 to 26.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 3

In January 2009, the Nomination Committee of the Board met and carried out anevaluation of the Directors, the Chairman, the Board itself and its Committees, theresults of which were satisfactory. The Board takes this review seriously and viewsit as an effective means of evaluating the ongoing efficacy of the Board.

Review of Services Provided by the Manager

During the year, the Board carried out a formal review of the investmentmanagement, company secretarial, administrative and marketing services providedby the Manager, JF Asset Management (‘JFAM’) and the Company Secretary,J.P. Morgan Asset Management (‘JPMAM’). The review encompassed the investmentperformance record, management processes, investment style, resources and riskcontrol mechanisms as well as noting the Company’s performance against its peers,performance against the benchmark, discount to net asset value, performanceattribution and total expense ratio. Despite the recent poor performance, the Boardconcluded that the continued appointment of the Manager and Company Secretaryis in the best interests of shareholders as a whole. Details of the Company’sManagement Agreements with JFAM and JPMAM can be found on page 19.

Subscription Shares

Following the passing of all the resolutions proposed at the Company’s GeneralMeeting held on 2nd March 2009 the Company issued 7,798,873 Subscription shareson 5th March 2009 as a bonus issue to the Ordinary shareholders on the basis of oneSubscription share for every five Ordinary shares held. Each Subscription shareconfers the right (but not the obligation) to subscribe for one Ordinary share on anybusiness day during the period from 1st April 2009 to 31st March 2014 (both datesinclusive) when the rights under the Subscription shares will lapse.

At the time of writing, the Company has issued 10,639 Ordinary shares following theconversion of Subscription shares into Ordinaries, amounting to proceeds of £14,363.Further details of the Subscription shares, including the bonus cost for the calculationof taxation, can be found on page 18 of this report and on the Company’s website atwww.jpmfjapanesesmallercompanies.co.uk

Share Issues and Repurchases

At the General Meeting held on 2nd March 2009, shareholders also gave the Boardauthority to repurchase up to 14.99% of the Company’s Ordinary and Subscriptionshare capital for cancellation. As previously stated, repurchases will only be made inthe market at prices below the prevailing net asset value per share. Repurchases ofSubscription shares will be made at the discretion of the Board and only when marketconditions are appropriate.

At the Annual General Meeting in 2008, shareholders gave the Board authority toallot up to 10% of the Company’s Ordinary share capital and to re-issue Treasuryshares at a discount to NAV, subject to certain limits and restrictions.

Since the share repurchase and issuance authorities were granted, the Companyhas repurchased a total of 396,000 Ordinary shares into Treasury for a totalconsideration of £492,000. The Company has not issued any new Ordinary sharesunder this authority nor issued any shares out of Treasury.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 20094

The Board believes that the ability to issue new Ordinary shares, repurchase Ordinaryand Subscription shares for cancellation and to hold and reissue Ordinary sharesfrom Treasury, is in the interests of shareholders in assisting the Company inmanaging any imbalance between the supply and demand for the Company’s sharesand in reducing the volatility of the discount. Accordingly, the Board will be seekingshareholders’ approval to renew these authorities at this year’s Annual GeneralMeeting. The Board is aware that the authority to reissue shares out of Treasury ata discount to NAV continues to be a controversial matter for certain groups ofshareholders and, in view of this, it will apply certain limits and restrictions. Shareswill only be reissued out of Treasury at a discount narrower than the weightedaverage of those currently held in Treasury, and the aggregate dilution associatedwith any re-issuance from Treasury will not exceed 0.5% of the net asset value overthe one year period of the authority. Furthermore, shares issued out of Treasury willbe limited to 5% of the total Ordinary shares in issue. This, in the Board’s view,represents a balanced and considered approach to this matter.

Board of Directors

During the year, the Directors appointed Robert White to the Board as anindependent Non-Executive Director of the Company. Robert has already madesignificant contributions to the Board’s deliberations and I am confident that he willcontinue to add value. In accordance with the terms of the Combined Code, havingbeen appointed during the year, Robert will retire and stand for election at theforthcoming Annual General Meeting.

In accordance with the Company’s Articles of Association, Chris Russell will retireby rotation at the forthcoming Annual General Meeting and offers himself forre-election. The Nomination Committee has met to consider the attributes andcontributions of Chris and, following this review, has no hesitation in recommendinghis re-election at the forthcoming Annual General Meeting.

Annual General Meeting

This year’s Annual General Meeting will be held at The Armourers’ Hall, 81 ColemanStreet, London EC2R 5BJ on Wednesday 22nd July 2009 at 11.30 a.m. In addition tothe formal proceedings, the investment managers will review the past year andcomment on the outlook for the current year. I look forward to seeing as many of youas possible at the meeting. If you have any detailed questions, you may wish to raisethese in advance with the Company Secretary at Finsbury Dials, 20 Finsbury Street,London EC2Y 9AQ or via the Company’s website. Shareholders who are unable toattend the Annual General Meeting in person are encouraged to use their proxyvotes. Shareholders who hold their shares through CREST are able to lodge theirproxy votes electronically. More details are given in the notes to the Notice of Meetingon page 55.

Alan CliftonChairman 17th June 2009

Chairman’s Statement continued

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 5

Investment Managers’ Report

The year to 31st March 2009 was an exceptionally challenging one, marred by theglobal financial crisis and a slump in domestic demand in Japan. At the start of ourfinancial year we believed that Japanese smaller companies already looked goodvalue in that they were trading at close to their underlying net asset values. Theperiod ended, however, with those same companies trading 40% lower – a recordlow level – and typically at around 60% of their attributable net worth. What was analready cheaply priced asset class became extremely cheap. Institutional investorswere major sellers of smaller company stocks throughout the year as they shranktheir appetite for risk taking. This heavy selling resulted in many widely held stocksbeing amongst the very worst performers regardless of valuation or business quality.We believe that this leaves the Japanese smaller companies market looking moreattractive than at any time since the 2002/3 trough and this is especially the casewhere good companies have been pushed down excessively by heavy sellingpressure.

In the dire investing environment of last year investors focused on company balancesheets. However, as the global situation stabilises, we expect that the focus will returnto companies medium term earnings prospects. It is for this forward lookingenvironment that we have positioned the portfolio. Having endured the forced sellingand drawn out de-rating of many of our portfolio holdings over the last few years, webelieve that we should now begin to enjoy the benefits of those – often long held –investments.

Our performance was extremely disappointing. Smaller company fund managersacross the board suffered compared to the benchmark index. You may, rightly,wonder why fund managers have struggled quite so much. One of the major driversof this performance relates to investment flows. Fund managers deliberately seek outattractive places to invest money: companies with strong business models; highprofitability; and attractive valuations. However, when markets suffer aggressiveoutflows, as Japanese smaller companies have over the past year, investors can onlysell what they own, not what they want to. Last year, especially, amongst the veryworst performing factors associated with stock price performance were high businessquality, profitability and cheap earnings. However, the single worst performing factorwas a high level of institutional ownership. These factors together reflect theconcerted and prolonged selling of those fundamentally attractive businesses. Clearlyfor managers focusing on profitable and attractive businesses at cheap prices it was aperfect storm as these growth businesses normally trade at a premium to the rest ofthe market but as a result of this exceptionally aggressive de-rating process they nowstand at a discount of 50%. This reflects an extreme divergence from the average andthe first time in 45 years that a very substantial discount for future growth exists.These stocks have become not just cheap but generationally cheap.

Over the long term, cheaply priced stocks based on earnings in Japan have steadilyoutperformed albeit with periods of sharp underperformance. During the mostrecent recovery phase the best performing factor in 2003 was low earnings basedvaluation measures; in 2004 it was low earnings based valuation, and in 2005 it waslow earnings valuation. The positive return was more than 30% annually. This is invery stark contrast to the latest year. Just as these measures have led the marketdown this year, we expect them to generate strong returns going forwards. Priorperiods, where cheaply priced stocks have lagged sharply, have tended to last at leasttwo years so the recent bear market is in line with that period. The forced liquidation

David Mitchinson

Nicholas Weindling

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 20096

of stock and record cheapness combined with their prolonged weakness suggest thatthis is the time to be actively seeking out and investing in those highly attractivebusinesses with cheaply priced earnings. We anticipate that as investors regain theirconfidence they will look at earnings streams more favourably again and reverse thehistoric cheapness. We have used the distress selling as an opportunity to increaseweightings and to bargain hunt very attractive stocks.

After enduring a three year bear market it is worth reviewing where we stand onwhat makes Japanese smaller companies perform. The smaller company market inJapan is driven by two concurrent cycles: economic and valuation. These conspire tocreate a volatile asset class where deviations from intrinsic value can be profound.Currently, we are at the lowest ebb of the economic cycle. The overleveragedfinancial system drove industrial production down exceptionally sharply last year. Inthe fourth quarter of 2008 Japanese industrial production fell at an annualised rateof 30%. Our meetings with companies suggest a steady improvement in conditionssince February. Companies exposed to Chinese and Indian demand are faringespecially well. Given these circumstances we expect a continued improvement in theeconomy, though the recovery path is likely to be bumpy.

The second cyclical component is a valuation cycle. Whichever smaller companyindex we look at we can see that the valuations reached in the last year are atunprecedented low levels. Since the market bottom we have seen a moderaterecovery but that still leaves many companies trading at, or below, previous marketbottom valuation levels. The smaller company market currently offers outstandingvalue for investors based on extremely low price to book and price to earningsmeasures. Taking both the depressed state of the economy and valuations together,provides a very substantial scope for stock performance to improve as the economybegins to recover. It is this factor that lies behind our optimism on the smallercompany market outlook.

Over the last few months we have gradually repositioned the portfolio to benefit froma recovering market. We are continuing to emphasise companies that we believe cangrow their business scale over the medium term in a profitable way. Currently thesestocks are very out of favour with investors. The dire economy has also pushed somecompanies to seriously restructure their businesses and in many cases the difficultiesof one business unit have hidden the strong performance of other divisions – oftencausing a large mispricing in the stock. Additionally, we have been increasing theholdings in companies that will benefit from the recovering economy and market.This repositioning has been funded by reducing healthcare and defensive stockholdings which we expect will underperform in a better market environment. Finally,we have also increased the gearing of the Company to reflect our positive outlook.

As an example of the type of company we have been investing in we would highlightlogistics company Trancom. This company has steadily grown from yen 12 billion insales 10 years ago to more than yen 65 billion today. Profits have grown alongsidethis as the company has rolled out its logistics business to more customers. Thestable customer base includes many food companies, whilst the economic crisis hasspurred many other companies to look for ways to reduce their distribution costs;new customers are joining at a rapid rate. Despite the long track record of profits and

Investment Managers’ Reportcontinued

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 7

sales increases, Trancom trades on a below market rating of a six times price toearnings ratio this year. This strikes us as being much too low for such a stronglymanaged and profitable business.

Another company example would be Yokogawa Electric. We have followed thebusiness for some time but only recently felt that the timing was right to invest. Thecompany has a globally competitive industrial controls business that is especiallystrong in China and the Middle East and a very weak semiconductor testing business.The management team was slow to realise that the semiconductor business had lostcompetitiveness and it has suffered very high losses for the past few years. Thisdivision is finally being closed and the remaining control business trades on less thana quarter of the valuation of global competitors. For us, the valuation gap isenormously attractive. Not only will the losses from semiconductors drop away butthe company will also be able to put all of its energy into the successful, high profitcore business.

Our final company example is Japan’s only listed securities exchange – OsakaSecurities Exchange. This company is the centre for trading in the Nikkei 225 futurescontract but has expanded the product line up to include exchange traded options,mini-futures, and Exchange Traded Funds. Last year it acquired the Jasdaq marketand will integrate that with its own stock trading business. This should produce a veryquick payback given the huge cost savings that can be made. The depressed marketlevel means that both futures and stock trading levels are currently low; any increasein stock trading activity will flow directly to their bottom line. This is a market play butis outstandingly well placed to benefit from a recovery in the Japanese stock market.

The last few years have been undeniably challenging for Japanese smallercompanies. A combination of steady de-rating, accompanied by a domesticslowdown and then a major global financial crisis have pushed smaller companies torecord lows. The economy has also struggled. These two factors are now beginning toreverse as the economy gradually recovers and the extremely cheap valuations ofmany smaller companies attract investors’ attention. Within the portfolio we havebegun to position ourselves more positively using the opportunity of cheap prices tobuild weightings in attractive businesses; exploiting the large mispricing of somerestructuring firms and running some long held successful companies that have beenvictims of the long bear market but are now poised to recover very strongly.

David MitchinsonNicholas WeindlingInvestment Managers 17th June 2009

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 20098

2009 2008

Total Returns for the year ended 31st March

Return to shareholders1 –34.4% –33.9%Return on net assets2 –32.2% –28.1%Benchmark return3 –2.4% –19.1%

Net Asset Value, Share Price and Discount at 31st March % change

Shareholders’ funds (£’000) 51,306 76,276 –32.7Net asset value per share 131.8p 194.0p –32.1Net asset value per share assuming reissuance of Treasury shares4 131.6p 194.0p –32.2Ordinary share price 108.5p 169.5p –36.0Discount of share price to net asset value assuming reissuance of

Treasury shares 17.6% 12.6%Ordinary shares in issue 39,309,4235 39,309,423Subscription share price 13.5p —Subscription shares in issue 7,798,873 —

Revenue for the year ended 31st March

Gross revenue return (£’000) 1,421 1,404 +1.2Net loss attributable to shareholders (£’000) (385) (508)Loss per share (0.98)p (1.29)p

Actual Gearing Factor at 31st March6 98.3% 109.5%

Total Expense Ratio (‘TER’)7 1.99% 1.80%

A glossary of terms and definitions is provided on page 56.

1Source: Morningstar/J.P. Morgan.2Source: J.P. Morgan.3Source: Datastream. 4Source: Net asset value assuming the 396,000 shares held in Treasury at 31st March 2009 were reissued in accordance with the Board’s policy on the reissuance of Treasury shares. 5Includes 396,000 shares held in Treasury (2008: nil).6Actual gearing represents investments expressed as a percentage of shareholders’ funds.7Management fees and all other operating expenses, excluding interest and subscription share costs, expressed as a percentage of the average of the opening and closing net assets.Further details are given in the glossary of terms and definitions on page 56.

Summary of Results

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 9

Performance

Five Year PerformanceFigures have been rebased to 100 at 31st March 2004

Source: Standard & Poor’s – www.funds.morningstar.com/Fundamental Data – www.funddata.com/Datastream.

JPMorgan Fleming Japanese Smaller Companies – Ordinary share price

JPMorgan Fleming Japanese Smaller Companies – Net asset value

Benchmark

0

50

100

150

200

200920082007200620052004

Performance Relative to BenchmarkFigures have been rebased to 100 at 31st March 2004

Source: Standard & Poor’s – www.funds.morningstar.com/Fundamental Data – www.funddata.com/Datastream.

JPMorgan Fleming Japanese Smaller Companies – Ordinary share price

JPMorgan Fleming Japanese Smaller Companies – Net asset value

Benchmark

40

60

80

100

120

200920082007200620052004

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200910

As at 31st March 2004 2005 2006 2007 2008 2009

Total assets less current liabilities (£m) 123.3 103.4 160.0 106.3 76.3 51.3

Net asset value per share (p) 273.9 249.9 405.9 269.7 194.0 131.8

Ordinary share price (p) 252.0 227.0 387.5 256.5 169.5 108.5

Discount of Ordinary shares (%)1 8.0 9.2 4.5 4.9 12.6 17.6

Actual gearing factor (%) 114.0 98.2 115.9 115.7 109.5 98.3

Subscription share price — — — — — 13.5

Year ended 31st March

Revenue attributable to shareholders (£’000) 974 1,023 1,266 1,447 1,404 1,421

Loss per Ordinary share (p) (2.11) (1.89) (1.61) (2.14) (1.29) (0.98)

Total expense ratio (%)2 1.58 1.56 1.46 1.54 1.80 1.99

Rebased to 100 at 31st March 2004

Ordinary share price total return3 100.0 90.1 153.8 101.8 67.7 43.3

Net asset value total return4 100.0 91.2 149.0 99.0 72.0 48.8

Benchmark5 100.0 103.9 150.6 121.7 98.0 95.6

A glossary of terms and definitions is provided on page 56.

1Assumes that shares held in Treasury were issued in accordance with the Board’s policy on the reissuance of Treasury shares. 2Management fees and all other operating expenses, excluding interest and subscription share costs, expressed as a percentage of the average of the opening and closing net assets.3Source: Morningstar.4Source: J.P. Morgan.5Source: Datastream.

Five Year Financial Record

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 11

2009 2008Valuation Valuation

Company and Japanese Company Code Sector £’000 %1 £’000 %

Moshi Moshi Hotline (4708) Services 2,104 3.4 2,658 3.2Provides marketing services utilising telephone, fax and electronic mail. TheCompany, an affiliate of Mitsui & Co., also provides customer services, marketresearch and sales promotion services for businesses.

GMO Internet (9449) Information and 1,435 2.3 1,917 2.3Provides server rental services and internet domain name Communicationregistration services. The Company’s services include internet infrastructureservices and internet advertising services via electronic mails.

Osaka Securities Exchange (8697)2 Other Financing 1,424 2.3 1,350 1.6Provides and operates a market place for the trading of equities, Businessfutures and options. The Company manages the trading, as well as administerslisted stocks and registered members.

Disco (6146)2 Machinery 1,403 2.3 — —Manufactures abrasive and precision industrial machinery for cutting and grindingpurposes. The Company’s products are applied in the semiconductor, electronicsand construction industries for producing consumer goods such as personalcomputers, digital cameras, video game systems and Digital Video Disc (DVD)players.

Nitori Co (9843)2 Retail Trade 1,361 2.2 1,126 1.3Is based in Hokkando and operates a furniture retail chain. The Company sellsliving room furniture, storage furniture, dining furniture, office furniture, beds andinterior goods. Nitori also sells original brand and imported merchandise.

Aeon Delight (9787) Services 1,360 2.2 3,201 3.8Is a building maintenance company. The Company provides services such ascleaning, security and equipment management for buildings.

Towa Pharmaceutical (4553)2 Pharmaceuticals 1,329 2.1 — —Produces generic drugs mainly for the elderly. The Company also wholesalesmedicine and medical products of other pharmaceuticals.

Trancom (9058)2 Warehouse & 1,293 2.1 1,457 1.7Provides freight transportation services in the Tokai region. The Harbour TransportationCompany transports products for Sharp Corp., other consumer electronics makersand cosmetic and food producers. Trancom also operates warehousing businessand offers distribution information services.

Gree (3632)2 Information and 1,283 2.1 — —Operates a Social Network Service for PC and mobile users. The website Communicationprovides online communities and games to its members. The Company also sellsadvertising space through adveritising agencies.

EPS (4282)2 Services 1,182 2.0 1,101 1.3Provides clinical testing services to contract research organisations who are in thepharmaceutical industry in Japan. The Company’s services range from planning,monitoring and analysing study and clinical testing for development of new drugs.EPS also develops systems and provides data management as well as patentregistration.

Total3 14,174 23.0

1Based on total assets less current liabilities of £61.9m (2008: £83.7m) other than loan balances falling due within one year.2Not included in the ten largest investments as at 31st March 2008.3As at 31st March 2008, the value of the ten largest investments amounted to £24.5m representing 29.2% of total assets less current liabilities other than loan balances falling duewithin one year.

Ten Largest InvestmentsYear ended 31st March

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200912

31st March 20091 31st March 2008Portfolio Benchmark Portfolio Benchmark

% % % %

Services 14.0 4.5 14.4 4.8Retail Trade 11.8 8.8 10.4 7.4Information & Communication 11.3 4.7 15.1 3.9Machinery 7.5 6.4 5.1 7.8Real Estate 4.5 5.7 1.2 7.2Pharmaceuticals 4.5 2.9 5.3 2.7Other Financing Business 3.7 1.2 1.8 1.7Foods 3.4 5.3 — 5.7Land Transportation 3.2 3.0 1.6 2.2Metal Products 2.2 1.8 — 1.3Warehouse & Harbour Transportation 2.1 0.7 1.9 1.3Nonferrous Metals 1.9 1.7 — 1.7Construction 1.7 5.1 8.5 3.5Glass & Ceramics Products 1.7 1.4 0.4 1.8Transportation Equipment 1.4 2.5 4.9 3.1Electric Appliances 1.4 7.8 6.2 9.0Wholesale Trade 1.4 5.3 10.2 4.5Iron & Steel 1.3 1.7 — 2.8Precision Instruments 0.7 0.9 — 1.3Securities & Commodity Futures 0.7 1.3 — 1.0Chemicals 0.7 7.7 7.6 8.2Other Products 0.3 2.6 0.3 2.4Banks — 10.7 3.0 8.5Textiles & Apparels — 2.6 1.9 2.4Pulp & Paper — 1.1 — 0.6Rubber Products — 0.7 — 0.9Fishery Agriculture & Forestry — 0.7 — 0.5Electric Power & Gas — 0.6 — 0.7Marine Transportation — 0.3 — 0.5Mining — 0.1 — 0.1Oil & Coal — 0.1 — 0.1Insurance — 0.1 — 0.4Net current assets 18.6 — 0.2 —

Total 100.0 100.0 100.0 100.0

1Based on total assets less current liabilities of £61.9m (2008: £83.7m) other than loan balances falling due within one year.

Sector Analysis

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 13

ValuationCompany and Japanese Company Code £’000

ServicesMoshi Moshi Hotline (4708) 2,104Aeon Delight (9787) 1,360EPS (4282) 1,182Pacific Golf Group (2466) 967Kakaku.com (2371) 907Nichii Gakkan (9792) 875Daiseki (9793) 511Prestige International (4290) 445Cmic (2309) 169Outsourcing (2427) 155

Total Services 8,675

Retail TradeNitori Co (9843) 1,361Toridoll (3397) 1,147Ozeki (7617) 930Point (2685) 825ABC-Mart (2670) 806K’s Holdings (8282) 634Sugi (7649) 453Growell Holdings (3141) 356Okuwa (8217) 332Cosmos Pharmaceutical (3349) 225Daikokutenbussan (2791) 108Chimney (3362) 91Ain Pharmaciez (9627) 60

Total Retail Trade 7,328

Information & CommunicationGMO Internet (9449) 1,435Gree (3632) 1,283IT Holdings (3626) 863Access (4813) 854Digital Garage (4819) 759Hikari Tsushin (9435) 641Eacess (9427) 605GameOn (3812) 337Digital Arts (2326) 148Hudson Soft (4822) 74

Total Information & Communication 6,999

ValuationCompany and Japanese Company Code £’000

MachineryDisco (6146) 1,403Shinkawa (6274) 964NTN (6472) 606Nippon Pillar Packing (6490) 573Mars Engineering (6419) 294Nippon Thompson (6480) 277Amada (6113) 256Union Tool (6278) 251

Total Machinery 4,624

Real EstateTokyo Tatemono (8804) 820Japan Prime Realty Investment (8955) 569Global One Real Estate Investment (8958) 434Japan Excellent (8987) 410Sankei Building (8809) 409Kenedix Realty Investment Trust (8972) 135

Total Real Estate 2,777

PharmaceuticalsTowa Pharmaceutical (4553) 1,329Kissei Pharmaceutical (4547) 733Nichi-Iko Pharmaceutical (4541) 558Fuji Pharma (4554) 145

Total Pharmaceuticals 2,765

Other Financing BusinessOsaka Securities Exchange (8697) 1,424Japan Securities Finance (8511) 730Osaka Securities Finance (8512) 154

Total Other Financing Business 2,308

FoodsToyo Suisan Kaisha (2875) 873Snow Brand Milk Products (2262) 755Oenon (2533) 487

Total Foods 2,115

List of Investmentsat 31st March 2009

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200914

ValuationCompany and Japanese Company Code £’000

Land TransportationHamakyorex (9037) 978Seino (9076) 591Hitachi Transport System (9086) 412

Total Land Transportation 1,981

Metal ProductsMimasu Semiconductor Industry (8155) 1,031Sumco (3436) 360

Total Metal Products 1,391

Warehouse & Harbour TransportationTrancom (9058) 1,293

Total Warehouse & Harbour Transportation 1,293

Nonferrous MetalsFurukawa Electric (5801) 548Toho Zinc (5707) 545Hitachi Cable (5812) 89

Total Nonferrous Metals 1,182

ConstructionKyowa Exeo (1951) 576Taihei Dengyo Kaisha (1968) 487

Total Construction 1,063

Glass & Ceramics ProductsTaiheiyo Cement (5233) 1,052

Total Glass & Ceramics Products 1,052

Transportation EquipmentShowa Aircraft Industry (7404) 886

Total Transportation Equipment 886

ValuationCompany and Japanese Company Code £’000

Electric AppliancesFunai Electric (6839) 744Axell (6730) 141

Total Electric Appliances 885

Wholesale TradeAutobacs Seven (9832) 848

Total Wholesale Trade 848

Iron & SteelHitachi Metals (5486) 786

Total Iron & Steel 786

Precision InstrumentsAsahi Intecc (7747) 374Noritsu Koki (7744) 49

Total Precision Instruments 423

Securities & Commodity FuturesKabu.com Securities (8703) 417

Total Securities & Commodity Futures 417

ChemicalsMiraial (4238) 411

Total Chemicals 411

Other ProductsPigeon (7956) 200

Total Other Products 200

Total Portfolio 50,409

The portfolio comprises all equity investments.

List of Investments continued

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 15

Board of Directors

Alan Clifton (Chairman of the Board and the Nomination Committee)

A Director since March 2003 and appointed Chairman in June 2003.

He is Chairman of Schroder UK Growth Fund plc and a Director of several other investment companies.From 1990 until 2001 he was Managing Director of Morley Fund Management, the asset managementarm of Aviva plc, the UK’s largest insurance group.

John Gibbon (Chairman of the Audit Committee)

A Director since March 2003.

He is Chairman of BDT Invest Funds plc. He was Chief Investment Officer of BAE SYSTEMS Pension Fundfrom 1983 to 2001 and is now an advisor to a number of pension funds and charities.

Bernard Grigsby

A Director since August 2003.

He has more than 30 years experience in investment banking and international capital markets and is currentlythe principal of Rockbridge Advisors, a private advisory and consulting practice. Prior to retiring from the SwissRe Group in December 2005, he was Chief Executive Officer of Swiss Re’s Capital Management & Advisorydivision in London from 2001 to 2004, becoming Vice Chairman in 2004. He serves on a variety of boards andadvisory committees, including the Board of Trustees of Washington & Lee University, and the Boards of LIM-Asia Multi-Strategy Fund, various funds managed by Tudor Investment Corp, VinaCapital Vietnam OpportunityFund, and Corney & Barrow Group Ltd.

Chris Russell

A Director since January 2006.

He is a Non-Executive Director of a number of listed and unlisted investment and financial servicecompanies in the UK, Guernsey, US and Asia. These include London listed Candover plc and the New Yorklisted Korea Fund Inc. He is currently a Director of the Association of Investment Companies and anassociate of GaveKal Research in Hong Kong. He was formerly Head of Overseas Businesses at GartmoreInvestment Management plc which included Gartmore’s two businesses in Japan. From 1990-1997 he was aDirector of the Jardine Fleming Group in Asia after being Head of Research and of International Broking forJF Securities in Tokyo.

Robert White

A Director since October 2008.

He is currently a Partner of Oldfield Partners LLP, responsible for their Japanese investments. He hasinvestment experience in the Japanese market spanning more than 30 years during which time, interalia, he was Senior Representative of Warburg Investment Manager Japan Limited, President of INVESCOMIM Asset Management (Japan) Limited and a Partner of Dalton Strategic Partnership LLP.

All Directors are members of the Audit and Nomination Committees and are considered independent of theManager.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200916

The Directors present their report for the year ended31st March 2009.

Business Review

Business of the CompanyThe Company carries on business as an investment trust andwas approved by HM Revenue & Customs as an investmenttrust in accordance with Section 842 of the Income andCorporation Taxes Act 1988 for the year ended 31st March2008. This is subject to review, should there be any subsequentenquiry under Corporation Tax Self Assessment. In the opinionof the Directors, the Company has subsequently conducted itsaffairs so that it should continue to qualify. The Company willcontinue to seek approval under Section 842 of the Incomeand Corporation Taxes Act 1988 each year.

The Company is an investment company within the meaning ofSection 833 of the Companies Act 2006. The Company is not aclose company for taxation purposes.

A review of the Company’s activities and prospects is given inthe Chairman’s Statement on pages 2 to 4, and in theInvestment Managers’ Report on pages 5 to 7.

ObjectiveThe Company’s objective is to achieve long term capital growththrough investments in small and medium sized Japanesecompanies.

Investment Policies and Risk ManagementIn order to achieve its investment objective and to seek tomanage risk, the Company invests in a diversified portfolio ofinvestments in the stock markets of Japan, emphasising capitalgrowth rather than income. The Company’s investmentuniverse is restricted to all Japanese quoted companiesexcluding the largest 200 measured by market capitalisation,at the time of investment.

The Company manages liquidity and borrowings with the aimof increasing returns to shareholders. The assets are managedby two Investment Managers based in Tokyo, supported by a 16strong Japanese equity team.

The Board has set no minimum or maximum limit on thenumber of investments in the portfolio but in the year underreview, the number of investments ranged between 63 to 86.

It should be noted that the Company invests in smallercompanies which tend to be more volatile than largercompanies and the Company’s shares should thereforebe regarded as greater than average risk.

Investment Restrictions and Guidelines The Board seeks to manage the Company’s risk by imposingvarious limits and restrictions:

• As an investment trust, the Company cannot invest morethan 15% of its assets in any one investment, at the time ofacquisition.

• The Company will not invest more than 5% of its totalassets in any one individual stock at the time of acquisition.

• The Company’s gearing policy is to operate within a rangeof 90%-120% invested in normal market conditions.

• All currency hedging transactions are subject to the priorapproval of the Board. The Company did not enter any sucharrangements during the year.

These limits and restrictions may be varied by the Board at anytime at its discretion. Compliance with the Board’s investmentrestrictions and guidelines is monitored continuously by theManager and is reported to the Board on a monthly basis.

PerformanceIn the year to 31st March 2009, the Company produced a totalloss to shareholders of 34.4% and a total loss on net assetsof 32.2%. This compares with the loss on the Company’sbenchmark index of 2.4%. As at 31st March 2009, the valueof the Company’s investment portfolio was £50.4 million.The Investment Managers’ Report on pages 5 to 7 includes areview of developments during the year as well as informationon investment activity within the Company’s portfolio.

Total Return, Revenue and Dividends Total gross loss for the year amounted to £22,672,000 (2008:loss of £27,922,000) and distributable revenue after deductinginterest, administrative expenses and taxation amounted to adeficit of £385,000 (2008: deficit of £508,000).

Key Performance Indicators (‘KPIs’) The Board uses a number of financial KPIs to monitor andassess the performance of the Company. The principal KPIs are:

Directors’ Report

• Performance against the Company’s peers The principal objective is to achieve capital growth.The Board monitors performance relative to both thebenchmark and a broad range of competitor funds.

• Performance against the benchmark index Another KPI is the Company’s performance against itsbenchmark index.

Performance Relative to Benchmark IndexFigures have been rebased to 100 at 31st March 2004

Source: Standard & Poor’s – www.funds.morningstar.com/Fundamental Data – www.funddata.com

JPMorgan Fleming Japanese Smaller Companies – Ordinary Share price

JPMorgan Fleming Japanese Smaller Companies – Net asset value

The benchmark is represented by the grey horizontal line

Five Year PerformanceFigures have been rebased to 100 at 31st March 2004

Source: Standard & Poor’s – www.funds.morningstar.com/Fundamental Data – www.funddata.com

JPMorgan Fleming Japanese Smaller Companies – Ordinary Share price

JPMorgan Fleming Japanese Smaller Companies – Net asset value

Benchmark

• Discount to net asset value (‘NAV’)The Board has a share repurchase programme which seeks

to address imbalances in supply of and demand for theCompany’s shares within the market. This minimises thevolatility and absolute level of the discount to NAV at whichthe Company’s shares trade in relation to its peers in thesector. In the year to 31st March 2009, the shares tradedbetween a discount of 4.4% and 27.0%.

Discount Performance

Source: Datastream (month end date)

JPMorgan Fleming Japanese Smaller Companies – Discount

• Performance attribution The purpose of performance attribution analysis is toassess how the Company achieved its performance relativeto its benchmark index, i.e. to understand the impact onthe Company’s relative performance of the variouscomponents such as asset allocation and stock selection.

• Total expense ratio (‘TER’)The TER represents management fees and all otheroperating expenses excluding interest and subscriptionshare costs, expressed as a percentage of the average ofthe opening and closing net assets. The TER for the yearended 31st March 2009 was 1.99% (2008: 1.80%). TheBoard reviews the TER of the Company regularly. On anannual basis it compares its TER against other companieswith similar investment objectives and policies.

Share CapitalThe Company has the authority both to purchase shares in themarket for cancellation and to issue new shares for cash. Inaddition, the Company has authority to repurchase shares intoTreasury and to reissue shares out of Treasury at a discount toNAV, subject to limits and restrictions, as authorised byshareholders at the 2008 Annual General Meeting.

During the year, the Company repurchased a total of 396,000Ordinary shares of 10p each, into Treasury, for a totalconsideration of £492,000. The Company did not issue any

–30

–25

–20

–15

–10

–5

0

Mar-09Jan-09Nov-08Sep-08Jul-08May-08Mar-08

0

50

100

150

200

200920082007200620052004

40

60

80

100

120

200920082007200620052004

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 17

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200918

Directors’ Report continued

Ordinary shares during the year nor issue any Ordinary sharesout of Treasury. Resolutions to renew the authority to issuenew shares for cash, to reissue shares out of Treasury at adiscount to NAV and to purchase shares for cancellation aredue to be put to shareholders at the forthcoming AnnualGeneral Meeting. The full text of these resolutions is set out inthe Notice of Meeting on pages 53 and 54.

Subscription SharesFollowing the passing of all the resolutions proposed at theCompany’s General Meeting held on 2nd March 2009 theCompany issued 7,798,873 Subscription shares on 5th March2009 as a bonus issue to the Ordinary shareholders on thebasis of one Subscription share for every five Ordinary sharesheld. Each Subscription share confers the right (but not theobligation) to subscribe for one Ordinary share on any businessday during the period from 1st April 2009 to 31st March 2014(both dates inclusive) when the rights under the Subscriptionshares will lapse. The conversion prices of the Subscriptionshares, calculated as at the close of business on 27th February2009 and based on the Company’s net asset value of 133.53pence, per share are as follows:

• If exercised between 1st April 2009 and 31st March 2010,135 pence;

• If exercised between 1st April 2010 and 31st March 2012, 147pence; and

• If exercised between 1st April 2012 and 31st March 2014, 174pence.

Since the year end and at the time of writing, the Company hasissued 10,639 Ordinary shares following the conversion ofSubscription shares into Ordinaries, amounting to proceeds of£14,363. Following these conversions the Company’s issuedshare capital consists of 39,320,062 Ordinary shares (of which396,000 are held in Treasury) and 7,788,234 Subscriptionshares.

For the purposes of UK taxation, the issue of Subscriptionshares is treated as a reorganisation of the Company’s sharecapital. Whereas such reorganisations do not trigger achargeable disposal for the purposes of the taxation ofcapital gains, they do require shareholders to reallocate thebase costs of their Ordinary shares between Ordinary sharesand Subscription shares received. At the close of business on5th March 2009 the middle market prices of the Company’sOrdinary shares and Subscription shares were as follows:

Ordinary shares 101.75p

Subscription shares 7p

Accordingly, an individual investor who, on 4th March 2009,held five Ordinary shares (or a multiple thereof) would havereceived a bonus issue of one Subscription share (or therelevant multiple thereof) and would apportion the base costof such holding 98.64% to the five Ordinary shares and 1.36%to the Subscription shares.

Principal RisksWith the assistance of the Manager, JF Asset ManagementLimited (‘JFAM’), and Secretary, JPMorgan Asset Management(UK) Limited (‘JPMAM’), the Board has drawn up a risk matrix,which identifies the key risks to the Company. These key risksfall broadly under the following categories:

• Investment and Strategy: An inappropriate investmentstrategy, for example excessive concentration ofinvestment, asset allocation or the level of gearing, maylead to under-performance against the Company’sbenchmark index and peer companies, which may result inthe Company’s shares trading on a wider discount. TheBoard manages these risks by diversification of investmentsthrough its investment restrictions and guidelines whichare monitored and reported on. JPMAM provides theDirectors with timely and accurate managementinformation, including performance data and attributionanalyses, revenue estimates, liquidity reports andshareholder analyses. The Board monitors theimplementation and results of the investment process withthe Investment Managers, who attend all Board meetings,and reviews data which shows statistical measures of theCompany’s risk profile. The Investment Managers employthe Company’s gearing tactically, within a strategic rangeset by the Board. In addition to regular Board meetings, theBoard visits the offices of JF Asset Management in Tokyo onan annual basis to discuss strategy.

• Discount: In order to manage the Company’s discount,which can be volatile, the Company operates a shareissuance and repurchase programme.

• Market: Market risk arises from fluctuations in the fair valueor future cash flows from the Company’s investments dueto changes in the market prices. It represents the potentialloss that the Company might suffer through holdinginvestments in the face of negative market movements. TheBoard considers asset allocation, stock selection and levelsof gearing on a regular basis and has set investmentrestrictions and guidelines, which are monitored andreported on by JPMAM. The Board monitors theimplementation and results of the investment process withthe Manager.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 19

• Accounting, Legal and Regulatory: In order to qualify asan investment trust, the Company must comply withSection 842 of the Income and Corporation Taxes Act1988 (‘Section 842’). Details of the Company’s approvalare given under “Business of the Company” on page 16.Should the Company breach Section 842, it may lose itsinvestment trust status and as a consequence gains withinthe Company’s portfolio would be subject to CorporationTax. The Section 842 qualification criteria are continuallymonitored by JPMAM and the results reported to theBoard each month. The Company must also comply withthe provisions of The Companies Act 1985 and 2006 and,since its shares are listed on the London Stock Exchange,the UKLA Listing Rules. A breach of the Companies Actscould result in the Company and/or the Directors beingfined or the subject of criminal proceedings. Breach of theUKLA Listing Rules may result in the Company’s sharesbeing suspended from listing which in turn would breachSection 842. The Board relies on the services of itsCompany Secretary, JPMAM, and its professional advisersto ensure compliance with The Companies Acts and TheUKLA Listing Rules.

• Corporate Governance and Shareholder Relations: Detailsof the Company’s compliance with Corporate Governancebest practice, including information on relations withshareholders, are set out in the Corporate Governancereport on pages 23 to 26.

• Operational: Loss of key staff by JFAM or JPMAM, such asthe investment managers, could affect the performance ofthe Company. Disruption to, or failure of, JFAM’s or JPMAM’saccounting, dealing or payments systems or the custodian’srecords may prevent accurate reporting and monitoring ofthe Company’s financial position. Details of how the Boardmonitors the services provided by JFAM, JPMAM and itsassociates and the key elements designed to provideeffective internal control are included within the InternalControl section of the Corporate Governance report onpage 25 and 26.

• Financial: The financial risks faced by the Company includemarket price risk, interest rate risk, foreign currency risk,liquidity risk, gearing and credit risk. Bank counterpartiesare subject to daily credit analysis by the Manager andregular consideration at meetings of the Board. In addition,the Board receives regular reports on the Manager’s

monitoring and mitigation of credit risks on sharetransactions carried out by the Company. Further detailsare disclosed in note 19 on pages 43 to 48.

• Political and Economic: Administrative risks, such as theimposition of restrictions on the free movement of capital.

Future Developments Clearly the future development of the Company is muchdependent upon the success of the Company’s investmentstrategy in light of economic and equity market developments;the Investment Managers discuss the outlook in their report onpages 5 to 7.

Management of the Company

The Manager of the Company is JFAM. JPMAM, the Londonbased Manager for the investment trust range of J.P. Morgan,acts as Secretary and provides administrative support.Investment advice is provided to JFAM by JF Investment Trustand Advisory Company Limited (‘JFITAC’) in Tokyo. JFAM andJPMAM are employed under a contract terminable on sixmonths’ notice, without penalty. If the Company wishes toterminate the contract on shorter notice, the balance ofremuneration is payable by way of compensation.

JFAM and JPMAM are wholly owned subsidiaries of J.P. MorganChase Bank which, through other subsidiaries, also providesbanking, dealing and custodian services to the Company.

The Board has evaluated the performance of the Manager andSecretary and confirms that it is satisfied that the continuingappointment of the Manager and Secretary is in the interestsof shareholders as a whole. In arriving at this view, the Boardconsidered the investment strategy and process of theManager and the support that the Company receives fromJFAM and JPMAM.

Management Fee

The management fee is charged at the rate of 1.25% per annumon the first £115 million of the Company’s gross assets and1% per annum on any amount exceeding £115 million of grossassets (save that in relation to cash and near cash assets above125% of net assets, a reduced fee of 0.25% per annum ispayable). A secretarial fee is paid to JPMAM out of thismanagement fee. If the Company invests in funds managed oradvised by JFAM or JPMAM or any of its associated companies,

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200920

Directors’ Report continued

those investments are excluded from the calculation andtherefore attract no additional fee.

Going Concern

The Directors believe that having considered the presentmarket uncertainties, the Company’s investment objective (seepage 16), risk management policies (see pages 43 to 48), capitalmanagement policies and procedures (see page 49), nature ofthe portfolio and expenditure projections, that the Companyhas adequate resources, an appropriate financial structure andsuitable management arrangements in place to continue inoperational existence for the foreseeable future. For thesereasons, they consider that there is reasonable evidence tocontinue to adopt the going concern basis in preparing theaccounts.

Payment Policy

It is the Company’s policy to obtain the best terms for allbusiness and therefore there are no standard payment terms.In general the Company agrees with its suppliers the terms onwhich business will take place and it is the Company’s policy toabide by these terms. As at 31st March 2009, the Company hadno outstanding trade creditors (2008: none).

Directors

The Directors of the Company who held office at the end of theyear, together with their beneficial interests in the Company’sissued share capital, were:

31st March 1st April2009 2008

Ordinary Subscription OrdinaryDirectors Shares Shares Shares

Alan Clifton 10,000 2,000 10,000John Gibbon 5,000 1,000 5,000Bernard Grigsby 50,000 10,000 50,000Chris Russell 35,000 7,000 35,000Robert White1 5,000 1,000 —

1Appointed as a Director of the Company on 1st October 2008.

At the time of writing, no changes in the above holdings havebeen notified since the year end.

In accordance with the Company’s Articles of Association, theDirector retiring by rotation at the forthcoming Annual GeneralMeeting (‘AGM’) will be Chris Russell who, being eligible, offershimself for re-election by shareholders.

In accordance with the terms of the Combined Code, RobertWhite, having been appointed during the year, will retire andstand for election.

An insurance policy is maintained by the Company whichindemnifies the Directors of the Company against certainliabilities arising in the conduct of their duties. There is nocover against fraudulent or dishonest actions.

Disclosure of information to Auditors

In the case of each of the persons who are Directors of theCompany at the time when this report was approved:

(a) so far as each of the Directors is aware, there is no relevantaudit information of which the Company’s auditors areunaware, and

(b) each of the Directors has taken all the steps that he oughtto have taken as a Director in order to make himself awareof any relevant audit information and to establish that theCompany’s auditors are aware of that information.

The above confirmation is given and should be interpreted inaccordance with the provision of S234 ZA of the Companies Act1985.

Section 992 Companies Act 2006

The following disclosures are made in accordance with Section992 Companies Act 2006.

Capital StructureThe Company’s capital structure is summarised on the insidefront cover of this report.

Voting Rights in the Company’s sharesDetails of the voting rights in the Company’s shares as at thedate of this report are given in note 11 to the Notice of Meetingon page 55.

Notifiable Interests in the Company’s Voting RightsAt the date of this report, the following had declared anotifiable interest in the Company’s voting rights:

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 21

Shareholders Number of voting rights %

Lazard Asset Management LLC1 6,334,700 16.3Asset Value Investors1 5,145,579 13.2

Included within this is:British Empire Securities and

General Trust plc 2,887,809 7.4Midas Capital plc 2,880,000 7.4JPMorgan Asset Management (UK) Limited 2,575,006 6.61607 Capital Partners 2,046,495 5.3Legal & General Investment Management 1,588,524 4.1Wesleyan Assurance Society 1,183,500 3.0

1Non-beneficial.

The rules concerning the appointment and replacement ofDirectors, amendment of the Articles of Association andpowers to issue or repurchase the Company’s shares arecontained in the Articles of Association of the Company andthe Companies Acts 1985 and 2006.

There are no restrictions concerning the transfer of securitiesin the Company; no special rights with regard to controlattached to securities; no agreements between holders ofsecurities regarding their transfer known to the Company;no agreements which the Company is party to that affect itscontrol following a takeover bid; and no agreements betweenthe Company and its Directors concerning compensation forloss of office.

Independent Auditors

Deloitte LLP have expressed their willingness to continue inoffice as auditor to the Company and a resolution proposingtheir re-appointment and authorising the Directors todetermine their remuneration for the ensuing year will be putto shareholders at the Annual General Meeting.

Annual General Meeting

NOTE: THIS SECTION IS IMPORTANT AND REQUIRES YOURIMMEDIATE ATTENTION. If you are in any doubt as to the actionyou should take, you should seek your own personal financialadvice from your stockbroker, bank manager, solicitor or otherfinancial advisor authorised under the Financial Services andMarkets Act 2000.

Resolutions relating to the following items of special businesswill be proposed at the forthcoming Annual General Meeting:

(i) Authority to allot new shares for cash and disapply pre-emptionrights (Resolutions 6 and 7)

The Directors will seek renewal of the authority at the AGM toissue up to 3,932,006 new Ordinary shares for cash up toan aggregate nominal amount of £393,200, such amount beingequivalent to approximately 10% of the present issuedOrdinary share capital.

It is advantageous for the Company to be able to issue newshares to participants purchasing shares through the JPMAMsavings products and also to other investors when theDirectors consider that it is in the best interests of shareholdersto do so. Any such issues would only be made at prices greaterthan the NAV, thereby increasing the assets underlying eachshare and spreading the Company’s administrative expenses,other than the management fee which is charged on the valueof the Company’s net assets, over a greater number of shares.The issue proceeds would be available for investment in linewith the Company’s investment policies. The full text of theresolutions can be found in the Notice of Meeting on page 53.

(ii) Authority to repurchase the Company’s shares (resolution 8) The authority to repurchase up to 14.99% of the Company’sissued share capital, renewed by shareholders at a GeneralMeeting on 2nd March 2009, will expire on 31st January 2010unless renewed at the forthcoming Annual General Meeting.The Directors consider that the renewing of the authority is inthe interests of shareholders as a whole, as the repurchase ofshares at a discount to the underlying NAV enhances the NAVof the remaining shares.

The full text of the resolution is set out in the Notice of Meetingon pages 53 and 54. Repurchases will be made at the discretionof the Board, and will only be made in the market at pricesbelow the prevailing NAV per share as and when marketconditions are appropriate.

(iii) Treasury shares/disapplication of pre-emption rights(resolutions 9 and 10)

The Company is permitted to purchase up to 10% of its ownshares into Treasury (for sale or cancellation at a future date) asan alternative to immediate cancellation. The Board considersthat circumstances could arise in which it would be inshareholders’ interests for such powers to be exercised. This10% would form part of the 14.99% referred to in (ii) above.

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200922

The Board continues to believe that the effective use ofTreasury shares assists the Company in managing anyimbalance between supply and demand, thereby minimisingthe volatility and absolute level of the discount at which theCompany’s shares trade to their net asset value for the benefitof shareholders.

Accordingly, shareholders will also be asked at the AnnualGeneral Meeting to approve resolutions 9 and 10 whichwill allow the Company to sell shares from Treasury at adiscount to net asset value and disapply the statutorypre-emption rights respectively. This will enable the Companyto sell shares held in Treasury without having to first make apro rata offer to existing shareholders.

Should the resolutions be passed by shareholders, shareswould only be sold from Treasury when market demand isidentified and would be limited to 5% of the total Ordinaryshares in issue. This 5% would form part of the 10% issueauthority referred to in (i) above. Sales would only be made at adiscount narrower than the weighted average discount of theshares held in Treasury at that time. This process ensures thatthe enhancement in net asset value associated with sharepurchases exceeds the dilution in net asset value associatedwith the sale of Treasury shares at a discount.

The Board is mindful that shareholders may be concernedabout the dilution in net asset value associated with the sale ofTreasury shares at a discount. It is therefore proposed that thesale of shares from Treasury at a discount be limited so that inthe year to the Company’s 2010 Annual General Meeting, theaggregate dilution in net asset value per share arising on suchsales does not exceed 0.70 pence per Ordinary share, beingapproximately 0.5% of the net asset value per Ordinary shareat 31st March 2009. The full text of the resolutions can be foundin the Notice of Meeting on page 54.

Recommendation

The Board considers that resolutions 6 to 10 are likely topromote the success of the Company and are in the bestinterests of the Company and its shareholders as a whole.The Directors unanimously recommend that you vote in favourof the resolutions as they intend to do in respect of their ownbeneficial holdings which amount in aggregate to 105,000shares with voting rights representing approximately 0.3% ofthe voting rights of the Company.

By order of the Board Andrew Norman, for and on behalf of JPMorgan Asset Management (UK) Limited, Secretary 17th June 2009

Directors’ Report continued

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 23

Compliance

The Company is committed to high standards of corporategovernance. This statement, together with the Directors’Responsibilities in Respect of the Accounts on page 28indicates how the Company has applied the principles ofrecommended governance of the Financial Reporting CouncilCombined Code (the ‘Combined Code’) and the AIC’s Code ofCorporate Governance, (the ‘AIC Code’), which complementsthe Combined Code and provides a framework of best practicefor investment trusts.

The Board is responsible for ensuring the appropriate level ofcorporate governance and considers that the Company hascomplied with the best practice provisions of the CombinedCode, other than in respect of the provision relating to a SeniorIndependent Director, and the AIC Code throughout the yearunder review.

Role of the Board

A management agreement between the Company, JFAM andJPMAM sets out the matters over which the Manager hasauthority. This includes management of the Company’s assetsand the provision of accounting, company secretarial,administration and some marketing services. The Companydelegates responsibility for voting investee shares to JPMAM.Details of JPMAM’s Voting Policy and Corporate GovernanceGuidelines are available from JPMAM on request or can beaccessed at www.jpmorganassetmanament.co.uk/institutional.Within the ‘Commentary & Analysis’ tab there is a section onCorporate Governance.

All other matters are reserved for the approval of the Board.A formal schedule of matters reserved to the Board fordecision has been approved. This includes determination andmonitoring of the Company’s investment objectives and policyand its future strategic direction, gearing policy, managementof the capital structure, appointment and removal of third partyservice providers, review of key investment and financial dataand the Company’s corporate governance and risk controlarrangements.

The Board has procedures in place to deal with potentialconflicts of interest and confirms that the procedures haveoperated effectively during the year under review.

The Board meets at least quarterly during the year andadditional meetings are arranged as necessary. Full and timely

information is provided to the Board to enable it to functioneffectively and to allow Directors to discharge theirresponsibilities.

There is an agreed procedure for Directors to take independentprofessional advice if necessary and at the Company’s expense.This is in addition to the access that every Director has to theadvice and services of the Company Secretary, JPMAM, whichis responsible to the Board for ensuring that Board proceduresare followed and that applicable rules and regulations arecomplied with.

Board Composition

The Board, chaired by Alan Clifton, consists of fivenon-executive Directors, all of whom are regarded bythe Board as independent, including the Chairman. TheDirectors have a breadth of investment, business and financialskills and experience relevant to the Company’s business andbrief biographical details of each Director are set out onpage 15.

A review of Board composition and balance is included as partof the annual performance evaluation of the Board. The Boardhas considered whether a Senior Independent Director shouldbe appointed and has concluded that, as the Board consistsentirely of Non-Executive Directors, this is unnecessary.

Tenure

Directors are initially appointed until the following AnnualGeneral Meeting when, under the Combined Code, it isrequired that they be elected by shareholders. Thereafter,a Director’s appointment will run for a term of three years.Subject to the performance evaluation carried out each year,the Board will agree whether it is appropriate for the Directorto seek an additional term. Any Director who has served for aperiod of more than nine years will submit himself for annualre-election thereafter.

The terms and conditions of Directors’ appointments are setout in formal letters of appointment, copies of which areavailable for inspection on request at the Company’s registeredoffice and at the Annual General Meeting.

The Board confirms that Chris Russell, who retires by rotationat this year’s Annual General Meeting, continues to be aneffective Director and demonstrates commitment to his role,and therefore recommends his re-election. Furthermore,

Corporate Governance

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 200924

Corporate Governance continued

having been appointed during the year, Robert White will retireand stand for election.

Meetings and Committees

The Board delegates certain responsibilities and functions toCommittees. All Directors are members of the Committees.

The table below details the number of Board, Audit Committeeand Nomination Committee meetings attended by eachDirector. During the year there were 7 Board meetings, whichincluded a private session of the Directors to evaluate theManager and an overseas visit to the offices of JF AssetManagement in Tokyo to discuss strategy, 2 Audit Committeemeetings and 3 Nomination Committee meetings.

Audit NominationBoard Committee Committee

Meetings Meetings MeetingsDirector Attended Attended Attended

Alan Clifton 7 2 3John Gibbon 7 2 3Bernard Grigsby 7 2 3Chris Russell 7 2 3Robert White1 3 1 1

1Appointed as a Director of the Company on 1st October 2008.

Training and Appraisal

On appointment, the Manager and Company Secretary provideall Directors with induction training. Thereafter regularbriefings are provided on changes in regulatory requirementsthat affect the Company and Directors. Directors areencouraged to attend industry and other seminars coveringissues and developments relevant to investment trusts.

The Board conducts a formal evaluation of the Manager, itsown performance and that of its Committees and individualDirectors. Questionnaires, drawn up by the Board, arecompleted by each Director. The responses are collated andthen discussed at a private meeting. The evaluationof individual Directors is led by the Chairman. The NominationCommittee evaluates the Chairman’s performance. The Boardas a whole evaluates the Manager, its own performance andthat of its Committees.

Board Committees

Nomination Committee The Nomination Committee, chaired by Alan Clifton, consists ofall of the Directors, and meets at least annually to ensure that

the Board has an appropriate balance of skills and experienceto carry out its fiduciary duties and to select and proposesuitable candidates for appointment when necessary. Varioussources, which may include the use of external searchconsultants, are used to ensure that a wide range of candidatesare considered.

The Committee undertakes an annual performance evaluation,as described above, to ensure that all members of the Boardhave devoted sufficient time and contributed adequately to thework of the Board. The Committee also reviews Directors’ feesand makes recommendations to the Board as and whenappropriate.

Audit Committee The Audit Committee, chaired by John Gibbon, consists of all ofthe Directors, and meets at least twice each year. The membersof the Committee consider that they have the requisite skillsand experience to fulfil the responsibilities of the Committee.Brief biographical details of each Director are set out onpage 15.

The Committee reviews the actions and judgements of theManager and Secretary in relation to the half year and annualaccounts and the Company’s compliance with the CombinedCode. It reviews the terms of the management agreementand examines the effectiveness of the Company’s internalcontrol systems, receives information from the Manager’sCompliance department and reviews the scope and results ofthe external audit, its cost effectiveness and theindependence and objectivity of the external auditors. In theDirectors’ opinion the auditors are considered independent.Representatives of the Company’s auditors attend theCommittee meeting at which the draft annual report andaccounts are considered.

The Directors’ statement on the Company’s system of internalcontrol is set out on pages 25 and 26.

Terms of ReferenceBoth the Nomination Committee and the Audit Committee havewritten terms of reference which define clearly their respectiveresponsibilities, copies of which are available on the Company’swebsite, on request at the Company’s registered office and atthe Annual General Meeting.

Relations with Shareholders

The Board regularly monitors the shareholder profile of theCompany. It aims to provide shareholders with a fullunderstanding of the Company’s activities and performanceand reports formally to shareholders quarterly each year by

JPMorgan Fleming Japanese Smaller Companies Investment Trust plc. Annual Report & Accounts 2009 25

way of the annual report and accounts, the half year financialreport and two interim management statements. This issupplemented by the daily publication, through the LondonStock Exchange, of the net asset value of the Company’s shares.

All shareholders have the opportunity, and are encouraged, toattend the Company’s Annual General Meeting at which theDirectors and representatives of the Manager and Secretaryare available in person to meet with shareholders and answerquestions. In addition, a presentation is given by theinvestment managers who review the Company’s performance.During the year the Company’s brokers, the investmentmanagers and the Secretary hold regular discussions withlarger shareholders. The Directors are made fully aware of theirviews. The Chairman and Directors make themselves availableas and when required to address shareholder queries andconsult major shareholders on an annual basis. The Directorsmay be contacted through the Secretary whose details areshown on page 50.

The Company’s Annual Report & Accounts is published in timeto give shareholders at least 20 working days’ notice of theAnnual General Meeting. Shareholders wishing to raisequestions in advance of the meeting are encouraged to submitquestions via the Company’s website or write to the CompanySecretary at the address shown on page 50 or via the website.

Details of the proxy voting position on each resolution will bepublished on the Company’s website shortly after the AnnualGeneral Meeting.

Internal Control

The Combined Code requires the Directors, at least annually,to review the effectiveness of the Company’s system of internalcontrol and to report to shareholders that they have done so.This encompasses a review of all controls which the Board hasidentified as including business, financial, operational,compliance and risk management.

The Directors are responsible for the Company’s systemof internal control which is designed to safeguard theCompany’s assets, maintain proper accounting records andensure that financial information used within the business,or published, is reliable. However, such a system can only bedesigned to manage rather than eliminate the risk of failureto achieve business objectives and therefore can only providereasonable, but not absolute, assurance against fraud, materialmis-statement or loss.

Since investment management, custody of assets and alladministrative services are provided to the Company by JFAM,

JPMAM and its associates, the Company’s system of internalcontrol mainly comprises monitoring the services providedby JFAM, JPMAM and its associates, including the operatingcontrols established by them, to ensure they meet theCompany’s business objectives. The Company does not havean internal audit function of its own, but relies on the internalaudit department of JFAM and JPMAM, which reports anymaterial failings or weaknesses. This arrangement is keptunder annual review. The key elements designed to provideeffective internal control are as follows:

Financial Reporting – Regular and comprehensive review bythe Board of key investment and financial data, includingmanagement accounts, revenue projections, analysis oftransactions and performance comparisons.

Management Agreement – Appointment of a Manager andcustodian are regulated by the Financial Services Authority(FSA), whose responsibilities are clearly defined in a writtenagreement.