30

2009 First half financials and strategy update September 2009

2009 First half financials

and strategy update

September 2009

2

• Recent market trends and the performance of Virbac

• 2009 first half consolidated financials

• Growth levers and 2009 outlook

Agenda

32,5%32,9%

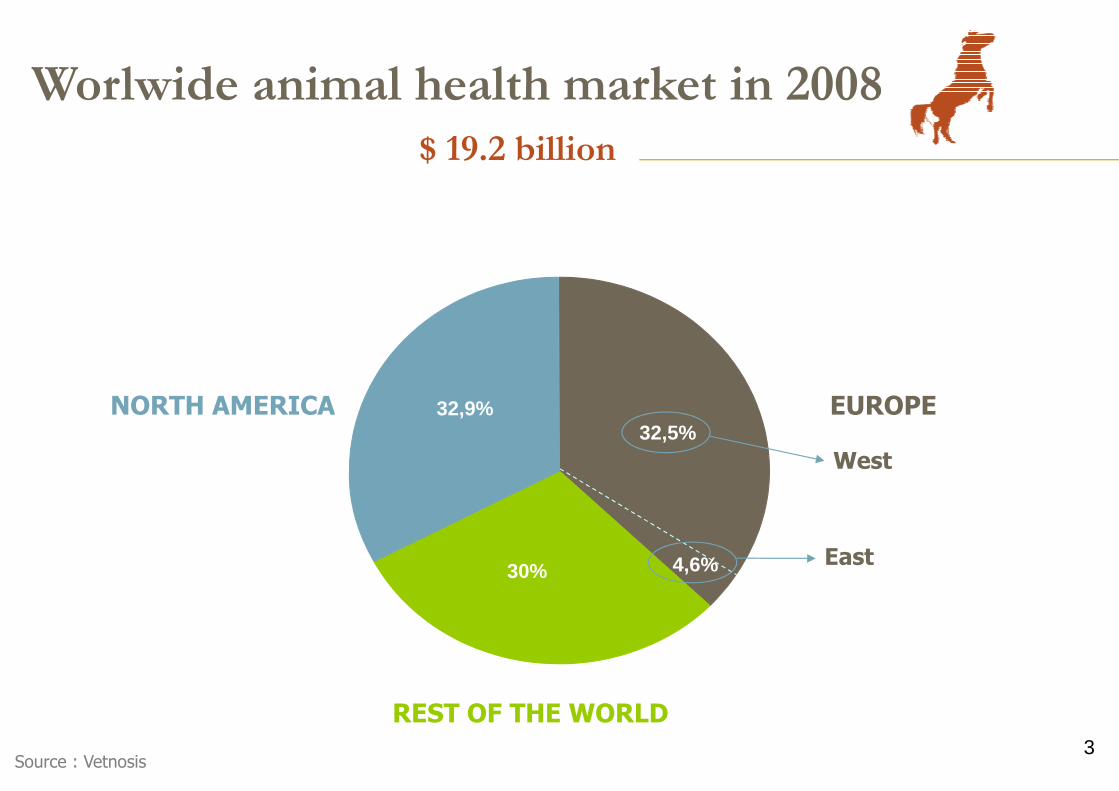

Worlwide animal health market in 2008$ 19.2 billion

EUROPE

REST OF THE WORLD

NORTH AMERICA

4,6%30%

West

East

Source : Vetnosis3

4

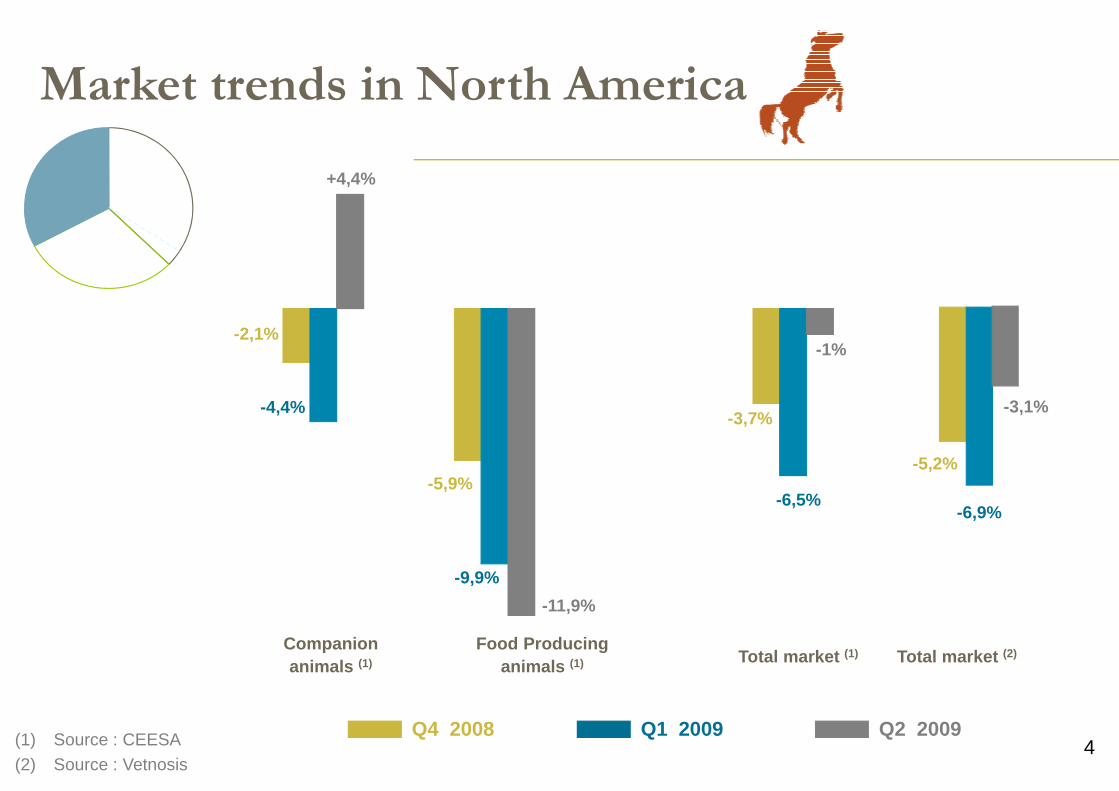

Market trends in North America

Companionanimals (1)

Food Producinganimals (1) Total market (1) Total market (2)

(1) Source : CEESA(2) Source : Vetnosis

Q4 2008 Q1 2009 Q2 2009

-2,1%

-5,9%

-3,7%-4,4%

-9,9%

-6,5%

+4,4%

-11,9%

-1%

-5,2%

-6,9%

-3,1%

5

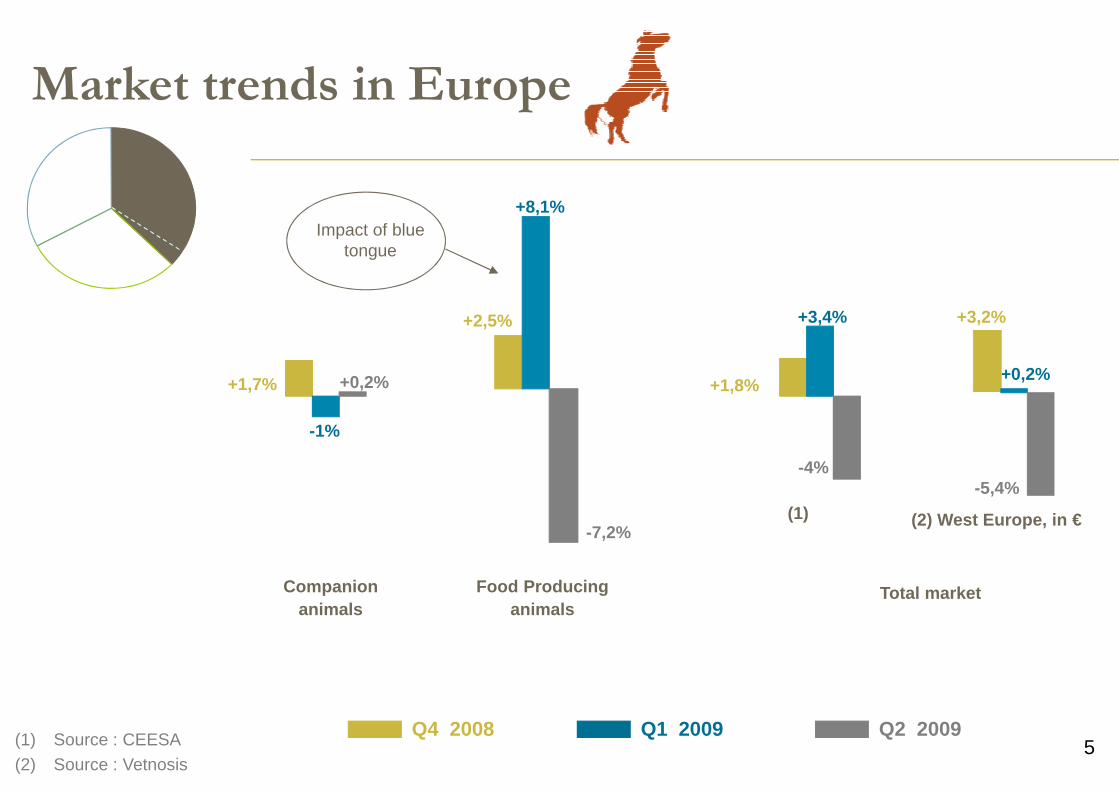

Market trends in Europe

(1) Source : CEESA(2) Source : Vetnosis

Q4 2008 Q1 2009 Q2 2009

Companionanimals

Food Producinganimals

Total market

(1) (2) West Europe, in €

+1,7%

+8,1%

+1,8%

-1%

+2,5% +3,4%

Impact of blue tongue

-7,2%

-4%

+0,2%

+3,2%

+0,2%

-5,4%

6

Virbac’s turnover in the first half of 2009(225,5 M€, + 6,6%*)

125,7 M€

35,7 M€

64,1 M€

North America(+ 0,5%)

Europe(+8,1%)

Rest of the world(+7,5%)

* All percentages of variance are at constant exchange rates

7

Virbac performance in North AmericaFirst half of 2009

47,4 M$

84 %

16%

Ethical(+12,0%)

OTC,3rd party

Manufacturing(-36,5%)

49 %

51 %

* All percentages of variance are at constant exchange rates

Heartworms(+26,4%)

Other ranges(+1,2%)

39,8 M$

47,4 M$+ 0,5 %

8

Virbac performance in EuropeFirst half of 2009

* All percentages of variance are at constant exchange rates

125,7 M€+ 8,1%

80,7 M€+ 2,0%

45,0 M€+ 19,1%

Ex Schering& Pharmalett

France

Rest of Europe

4,7 M€Products launched in

the last 12 months

76 M€- 5,0%All other products

7,4 M€

13,5 M€- 5,3%

24,1 M€+3,3%

Companion Animals

Food Producing Animals

9

Virbac performance in the rest of the world first half of 2009

+ 5% / + 15% > +15%Growth *

Turnover

10 / 15 M€Australia All others

combinedIndia

South Africa

4 / 10 M€MexicoBrazil

Japon

< - 5% - 5% / + 5%

+ 8.4% OVERALL

* Constant exchange rates

64.1 M€

+7.5%

10

• Recent market trends and the performance of Virbac

• 2009 first half consolidated financials

• Growth levers and 2009 outlook

Agenda

11

• Good increase of sales despite the market slow down :

+6,6 % at constant exchange rates / +3,1% organic

• Contribution of 2008 acquisitions in line with expectations

• Gross margin level maintained in spite of the decline of certain currencies (£, …)

• Cost control ; selective increase in R&D (USA) and marketing-sales (launches of

new products) :

� evolution of the operating profit in line with sales, excluding one-time items

� One-time items : industrial restructurings in 2009 vs. exceptional profits in 2008

• Improvement of cash generation (cash-flow, working capital) and slight seasonal increase of debt

2009 First half highlights

12

Consolidated sales30.06.2009

Consolidated sales 225.5 211.8 +6.4%

- Exchange rate impact vs. 2008 0.2

Consolidated sales at constant rates 225.7 211.8 +6.6%

- Change of perimeter (7.4) (0.2)

Consolidated sales, pro-forma

at constant exchange rates 218.3 211.6 +3.1%

2008 Var. %2009Million euros

13

Quarterly growth of sales30.06.2009 *

3%

1%

0%

First half +3.1%

Q1 Q2

+3.3%

+3.0%

2%

109.0 M€ 116.5 M€

4%

5%

* Pro forma sales, excluding impact of exchange rates and acquisitions

14

France 45.7 45.7 0.1% 0.1%Europe outside France 80.0 71.7 11.5% 13.1%North America 35.7 31.0 15.2% 0.5%Latin America 13.6 13.6 0.4% 12.0%Africa & Middle East 11.6 11.5 1.1% 4.2%Asia 26.2 22.1 18.2% 17.3%Pacific 12.6 16.1 -22.1% -10.2%

TOTAL 225.5 211.8 6.4% 6.6%

2008 Variation %2009Million eurosVar. Tx

Constants

Consolidated sales first half 2009Geographical breakdown

15

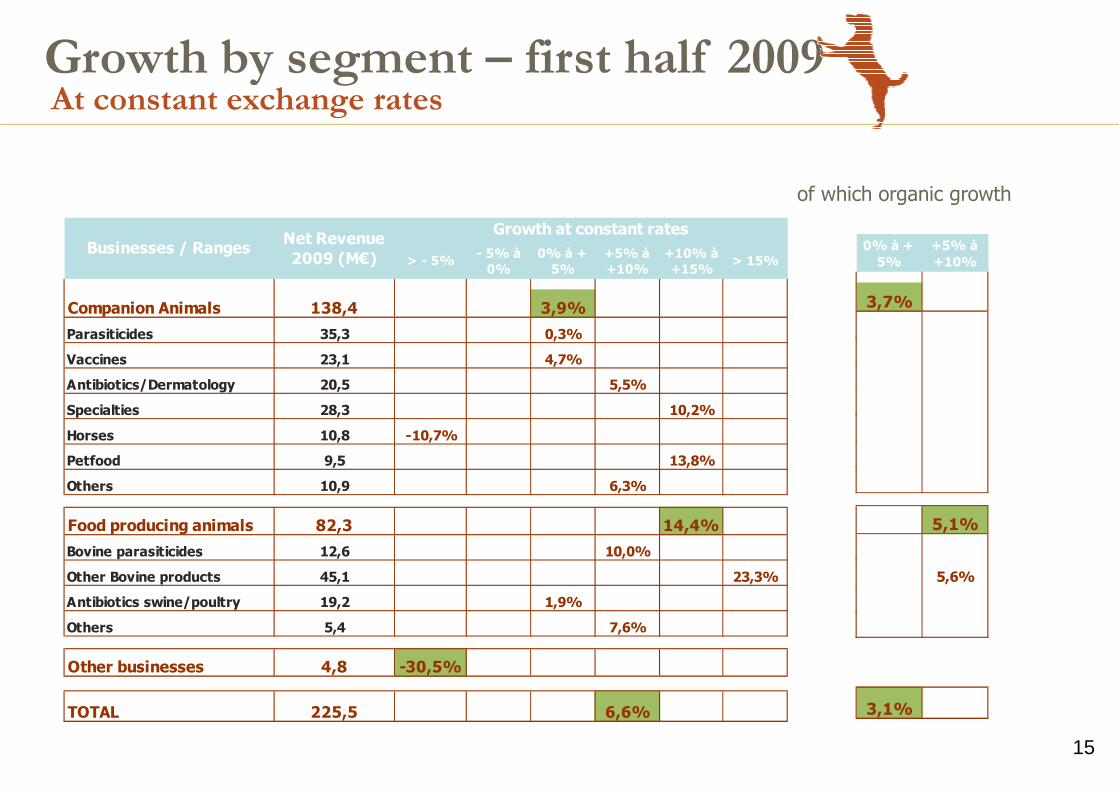

Growth by segment – first half 2009At constant exchange rates

> - 5%- 5% à

0%0% à +

5%+5% à +10%

+10% à +15%

> 15%

Companion Animals 138,4 3,9%

Parasiticides 35,3 0,3%

Vaccines 23,1 4,7%

Antibiotics/Dermatology 20,5 5,5%

Specialties 28,3 10,2%

Horses 10,8 -10,7%

Petfood 9,5 13,8%

Others 10,9 6,3%

Food producing animals 82,3 14,4%

Bovine parasiticides 12,6 10,0%

Other Bovine products 45,1 23,3%

Antibiotics swine/poultry 19,2 1,9%

Others 5,4 7,6%

Other businesses 4,8 -30,5%

TOTAL 225,5 6,6%

Businesses / RangesGrowth at constant rates

Net Revenue 2009 (M€)

0% à + 5%

+5% à +10%

3,7%

5,1%

5,6%

3,1%

of which organic growth

16

Consolidated profit & loss statement30.06.2009

Net Sales 225.5 100 211.8 100 +6.4%

Margin on material cost 153.0 67.9 144.0 68.0 +6.3%

Net operating expenses 126.3 56.0 119.0 56.2 +6.2%

One-time expenses or revenues (1) 1.9 (1.0)

Operating profit from ordinary activities 24.8 11.0 26.0 12.3 -4.7%

Non recurring expenses - 0.1

Operating profit 24.8 11.0 25.9 12.2 -4.4%

Net financial expenses 1.6 1.8

Income before tax 23.2 10.3 24.1 11.4 -3.4%

Income tax expense 7.3 7.4

Net profit of consolidated entities 15.9 7.1 16.6 7.8 -4.2%

Minority interests 0.4 0.4

Net loss – Group’s Share 15.5 6.9 16.2 7.6 -4.3%

2008 %% % Var.2009Million euros

(1) cost of industrial restructuring in 2009

capital gain and output of 2008 litigations

17

2009 OPERATING PROFIT - RECURRING 24.8

2008 OPERATING PROFIT - RECURRING 26.0

Main positive variances 5.6

- USA excluding R&D 3.6- India 1.0- South Africa 1.0

M€

Main negative variances (3.9)

- Europe (1.4)

- Australia (1.1)

- Global R&D expenses (0.9)

- Others (0.5)

One-time items (2.9)

30.06.2009

Operating profit – main evolutions

- 2008 exceptional profits (capital gain and output of litigation) (1.0)- Cost of 2009 industrial restructurings (1.9)

18

2009 OPERATING PROFIT – RECURRING 26.7 -1.9 24.8

% of sales 11,8% 11,0%

Excluding One-time Totalone-time items items

2008 OPERATING PROFIT - RECURRING 25.0 1.0 26.0

% of sales 11,8% 12,3%

Margin 7.1 7.1

- Increase of gross margin from the business 7.1

-Improvement of gross margin rate -

Operating expenses -5.4 -2.9 -8.3

-Commercial and distribution expenses (2.8)

-Research, Development and Licensing expenses (0.9)

-Administrative expenses (0.6)

-Others (1.1)

M€

30.06.2009

Operating profit – main evolutions(2/2)

19

30.06.2009Evolution of cash-flow

RecurringOperating cash-flow (EBIT DA)

Net cash-flow

31,4 32,2

21,8

25 +14.7%

+2.7%

30

30.06.08

25

20

15

10

5

0

30.06.09

35M€

21,8

25

20

Cash-flow statement

Cash-flow 25.0 Tangible assets 9.8

Sale of assets (net) 0.1 Intangible assets 0.6

Decrease of treasury shares 1.1 Operating working capital 5.7

Other assets and liabilities 13.9

Miscellaneous 0.4

Total sources of funds 26.2 Total uses of funds 30.4

Decrease of net debt 4.2

30.06.2009 (M€)*

Sources of funds Uses of funds

* million euros in average exchange rates

21

30.06.08 30.06.09 30.06.08 30.06.09

INVESTED CAPITAL CAPITAL EMPLOYED

253.7

295.2

Shareholder’s equity

Minority interests +LT reserves

Net financial debt

Working capital

Fixed assets

253.7

295.2

Balance sheet analysis

43.4

210.3 243.1

52.1

180.6

14.3

58.8 (1)

208.6

17.1

69.5

30.06.2009

+16.4%

(1) 30.06.2008 = before the acquisition of the Schering-Plough products (25.4 M€)

Debt reductionoutside acquisitions:15 M€

M€

22

Balance sheet – financial ratios

H1 2008 2008.12 H1 2009

Net debt / Shareholder’s equity Group’s share

Net debt / Total equity + LT reserves

Net debt / Cash-flow

Net debt / EBIT DA

0.94

1.35

32.6 %

30.2 %

33.7%

31.2%

1.28

0.97 1.08

1.39

33.3 %

30.8 %

23

Shareholding

47,7%

50,9%

0,9%

0,5%

63,9%

34,9%

1,2%

Number of shares : 8 714 352Breakdown at 30 June 2009

In shares In voting rights

Dick Family

Dick Family

Others

Others

Treasury shares

Employees savings plan

Employees savings plan

EURONEXT : VIRP

Indices : SBF 250CAC MID 100

24

• Recent market trends and the performance of Virbac

• 2009 first half consolidated financials

• Growth levers and 2009 outlook

Agenda

25

Effipro / Fiproline

The Growth Levers

• Europe

� Launch, in almost all European countries in June 2009, with good results

� Difficulties in France linked to a quality defect of the Effipro spot-on pipette, that occurred in July and has been solved since

� Request for a variation of the Marketing Authorization by the French Agency. Marketing of Effipro spot-on stopped in France in July and unlikely to resume before 2010

• United States :

� Possible launch in 2011 (marketing authorization expected end of 2010 at federal level)

26

• Clinical studies :

� at 21 months : Efficacy statistically proven

� at 24 months (end of studies) : Results currently processed

CANILEISH Vaccine

• Marketing Authorization dossier to be filed in Q1 2010, in the likely event of a statistically proven efficacy at 24 months

• A small scale commercialization with a restricted status is possible in 2010

• Marketing at european level is conceivable in 2011, depending on the date of the Marketing Authorization and the scale up of production capacities.

27

• Latin America

• Eastern Europe

• Wyeth / Pfizer product portfolios

Acquisitions : ongoing projects

28

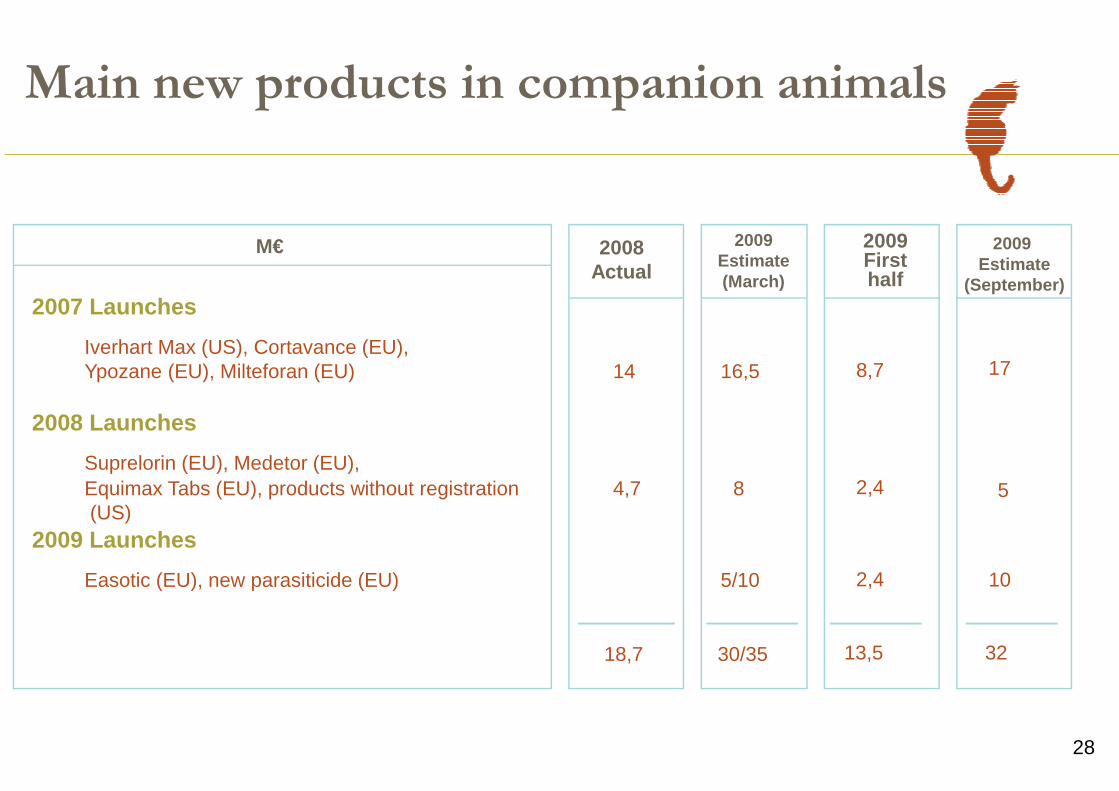

Main new products in companion animals

2008Actual

2009Estimate(March)

Iverhart Max (US), Cortavance (EU),Ypozane (EU), Milteforan (EU) 14 16,5

Suprelorin (EU), Medetor (EU),Equimax Tabs (EU), products without registration(US)

4,7 8

Easotic (EU), new parasiticide (EU) 5/10

18,7 30/35

M€ 2009First half

8,7

2,4

2,4

13,5

2009 Estimate

(September)

17

10

5

32

2007 Launches

2008 Launches

2009 Launches

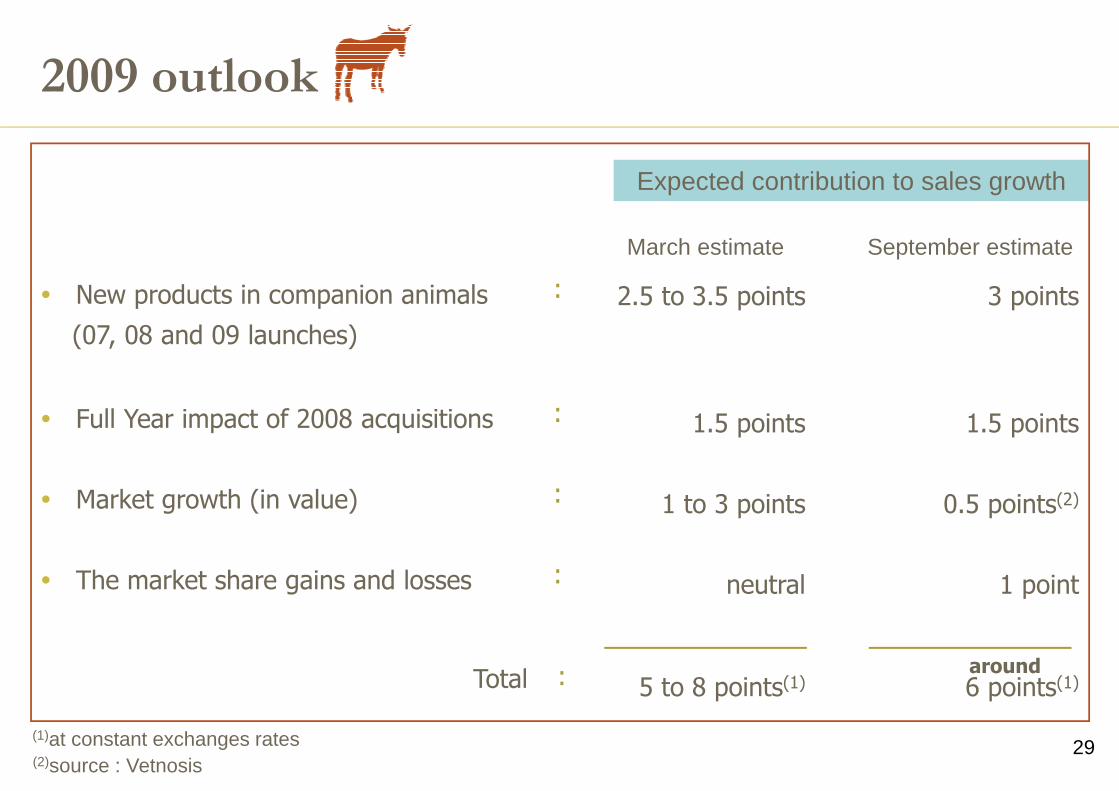

29

2.5 to 3.5 points

1.5 points

1 to 3 points

neutral

5 to 8 points(1)

2009 outlook

� New products in companion animals

(07, 08 and 09 launches)

� Full Year impact of 2008 acquisitions

� Market growth (in value)

� The market share gains and losses

:

:

:

:

:

Expected contribution to sales growth

(1)at constant exchanges rates

Total

3 points

1.5 points

0.5 points(2)

1 point

6 points(1)

March estimate September estimate

(2)source : Vetnosis

around

30

Thank you for your attention