56

2010 Analyst Day Chicago, June 2 & 3 2010 Analyst Day Chicago, June 2 & 3 Paul Spence Global Service Lines: Push for Growth

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Paul Spence

Global Service Lines: Push for Growth

2

Together. Free your energies 2010 Capgemini Analyst Day

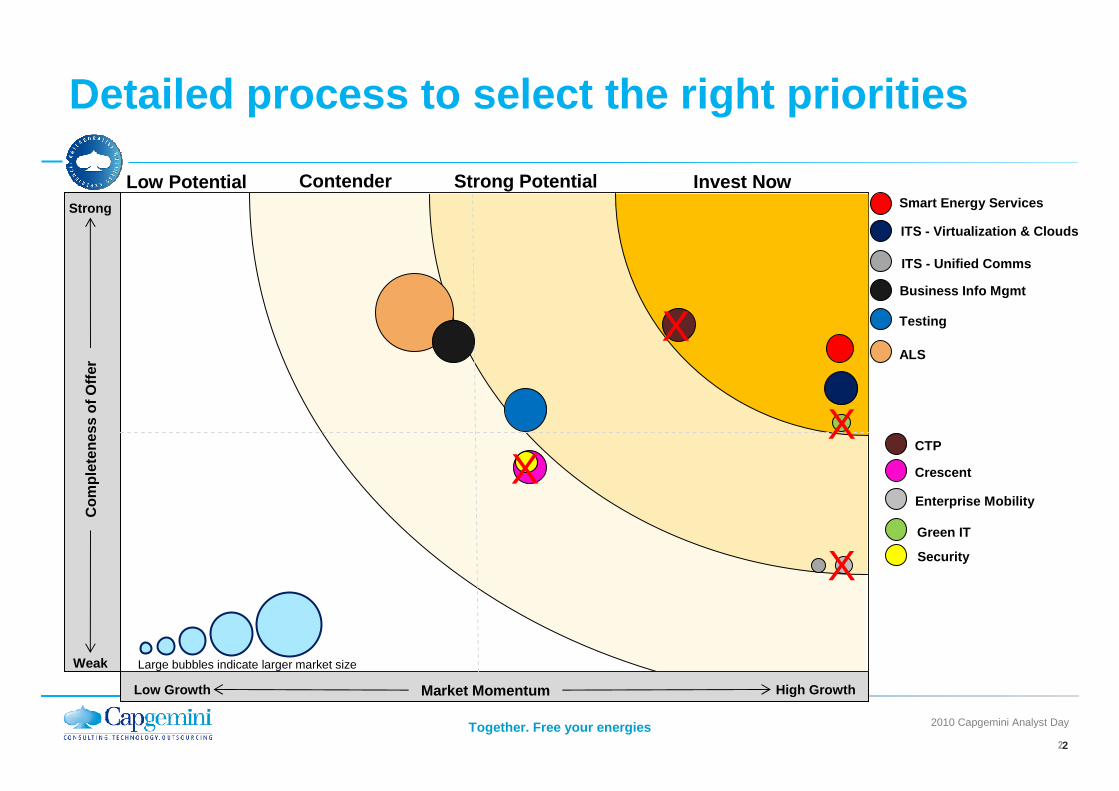

Detailed process to select the right priorities

2

Smart Energy Services

Testing

ALS

Market Momentum High GrowthLow Growth

Com

plet

enes

s of

Offe

r

Strong

Weak

Invest NowLow Potential Contender Strong Potential

Enterprise Mobility

ITS - Unified Comms

Green IT

Security

ITS - Virtualization & Clouds

Business Info Mgmt

Large bubbles indicate larger market size

CTP

Crescent

X

XX

X

3

Together. Free your energies 2010 Capgemini Analyst Day

First five months highly encouraging

� Financially• Roughly 1/3 of bookings• Roughly 1/4 of Revenue• CM Several points above rest of business

� Operationally• Several points better win rates in CC and TS businesses • Faster way for OS to win new work • Shifting of Alliance role and focus

� But…• Requiring intensified recruitment to optimise results• Requiring increased reskilling of work force

Shifting portfolio from geographic fragmentation to un ified global capability

4

Together. Free your energies 2010 Capgemini Analyst Day

Strong base to evolve business models and innovate

� ALS – Catchup with industry, then surpass with a twist

� TST – Industry best processes w/ consolidated delivery

� BIM – From data to information to sector solutions

� ITS – Technology change of XaaS and unified comms

� SES – MBS with monitored investment and risk

On track for above market growth AND improved margins for the five GSL’s

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Nicolas Dufourcq

BaU Lean Supply Chain Update for Tech Day

6

Together. Free your energies 2010 Capgemini Analyst Day

Lean is essentially about “eliminating waste” and focuses on delivering maximum value to the customer

Lean’s origins lie in the Toyota production system developed by Taiichi Ohno in the 1950s

‘Lean Thinking’ has successfully transformed many co mpanies,giving them a greater focus on performance and cust omer requirements

‘Lean Thinking’ has successfully transformed many co mpanies,giving them a greater focus on performance and cust omer requirements

C. R. Allen, 1919C. R. Allen, 1919C. R. Allen, 1919C. R. Allen, 1919

T. OhnoT. OhnoT. OhnoT. Ohno

TWI, 1940TWI, 1940TWI, 1940TWI, 1940

S. ShingoS. ShingoS. ShingoS. Shingo

MMééthodesthodesjaponaisesjaponaisesMMééthodesthodesjaponaisesjaponaises

TPS HouseTPS House, Cho, 70, Cho, 70’’ssTPS HouseTPS House, Cho, 70, Cho, 70’’ss

S. Toyoda, 1890S. Toyoda, 1890’’ssS. Toyoda, 1890S. Toyoda, 1890’’ss

E. DemingE. DemingE. DemingE. Deming

J. JuranJ. JuranJ. JuranJ. Juran

K. Ishikawa, 60K. Ishikawa, 60’’ssK. Ishikawa, 60K. Ishikawa, 60’’ss

J. Womack & D. JonesJ. Womack & D. JonesJ. Womack & D. JonesJ. Womack & D. Jones

«« LeanLean »»

Jidoka

Jidoka

QualitQualit éé

JITJITKaizenKaizen

C. R. Allen, 1919C. R. Allen, 1919C. R. Allen, 1919C. R. Allen, 1919

T. OhnoT. OhnoT. OhnoT. Ohno

TWI, 1940TWI, 1940TWI, 1940TWI, 1940

S. ShingoS. ShingoS. ShingoS. Shingo

MMééthodesthodesjaponaisesjaponaisesMMééthodesthodesjaponaisesjaponaises

TPS HouseTPS House, Cho, 70, Cho, 70’’ssTPS HouseTPS House, Cho, 70, Cho, 70’’ss

S. Toyoda, 1890S. Toyoda, 1890’’ssS. Toyoda, 1890S. Toyoda, 1890’’ss

E. DemingE. DemingE. DemingE. Deming

J. JuranJ. JuranJ. JuranJ. Juran

K. Ishikawa, 60K. Ishikawa, 60’’ssK. Ishikawa, 60K. Ishikawa, 60’’ss

J. Womack & D. JonesJ. Womack & D. JonesJ. Womack & D. JonesJ. Womack & D. Jones

«« LeanLean »»

Jidoka

Jidoka

QualitQualit éé

JITJITKaizenKaizen

The five principles of Lean

1. Define what is of value to the customer

2. Create a continuous flow of value to the customer, eliminate waste and complexity

3. Link the flow of value directly to customer demand

4. Empower employees to manage the process, and make them accountable for improvement

5. Maintain a strong focus on continuous improvement

Waste is ‘anything that consumes time & resources, but does not contribute to satisfying customer needs, or something that the cu stomer will not pay for’

Waste is ‘anything that consumes time & resources, but does not contribute to satisfying customer needs, or something that the cu stomer will not pay for’

7

Together. Free your energies 2010 Capgemini Analyst Day

Waiting for previous processes to finish. Waiting for material to arrive.

Production of parts without a customer order.

Time spent making defecting products that can not be accepted by the customer.

Excessive human / equipment effort – poor layout and process design.

Adding to a part something that is not required by the customer.

Raw Material / WIP / Finished goods – tied up capital.

Moving parts from one location to another without adding value.

Waiting

Over Production

Rework

Motion

Over Processing

Inventory

Transportation

Toyota identified 7 Wastes, which are relevant to most business environments

The identification and elimination of waste is fund amental to Lean – reducing costs and increasing profit. Other benefits are de rived from waste elimination…

The identification and elimination of waste is fund amental to Lean – reducing costs and increasing profit. Other benefits are de rived from waste elimination…

Toyota Examples�Testing team waiting for code to arrive

�Unassigned capacity between projects

�Waiting for responses from offshore teams

�Detailed reports that no-one reads

�Develop exceeding scope of contract

�Poor trained people

�Late test execution in development process

�Searching for files

�Resources switched within different tasks

�Repeated data entry in different environments

�Non-actionable supporting tools

�Huge ticket backlog

�Large number of features waiting for batch release

�Meeting in different sites

�Multiple handoff in ticket management

Service Examples

8

Together. Free your energies 2010 Capgemini Analyst Day

Lean is potentially a powerful change process

Lean means:1. A new way of designing and implementing

standards and methods2. A major change in the way we work in the field

and with our clients

Findings in engagements

Improvementactions

BU MgmtDelivery managers

Lean CA

Continuous improvement

Sta

ndar

d w

ays

of

wor

king

Lean

beh

avio

urs

Process performance

� Rapid performance monitoring and problem solving - Visual Management using daily white board meetings

� Seamless model with offshore - important transfers of responsibility

People

� Behaviours, efficiency and performance tightly connected to the customer

� A strong focus on our global and local management

� People listening, coaching and adopting the standard toolset

� Additional soft skills ‘à la Genesis’

Lean growth

� Snowballing network of Manager Champions and CAs, on and offshore

� Continuous Improvement ethos facilitated with a central full time officer

9

Together. Free your energies 2010 Capgemini Analyst Day

BeLean® unlocks a new entrepreneurial spirit withbroad benefits

A performance-driven company with continuous improv ement behaviours consistent with our DNA

A performance-driven company with continuous improv ement behaviours consistent with our DNA

BeLean®Value Proposition : Market share BD costs GOP

Hard benefits� Increased CM by eliminating waste� Lower ADRC through more offshoring� Improved topline through:

– Increased non-compete business with customers

– Re-invested saved time in intimacy building or higher margin work

� Improved effort estimation, leading to an increased win rate

Soft benefits� Improved relationship with offshore � More positive industrialization message� Lower regretted attrition by improved day-to-

day performance coaching� More ingrained performance culture in the

field from bottom-up� Clearer rallying point : “BeLean!”

10

Together. Free your energies 2010 Capgemini Analyst Day

We will apply BeLean® to the 4 main categories of business model in the Group

� BPO� IM� ALS (AO, TS+, Frames)� Testing

� ERPs inst/roll-out (SAP, Oracle, MS)

� Domain « template solution » (Crescent, CTP/Mobistar…)

� BI, Agile SOA/CSD � Responsibility business

Run

Transform

Established

In Progress

11

Together. Free your energies 2010 Capgemini Analyst Day

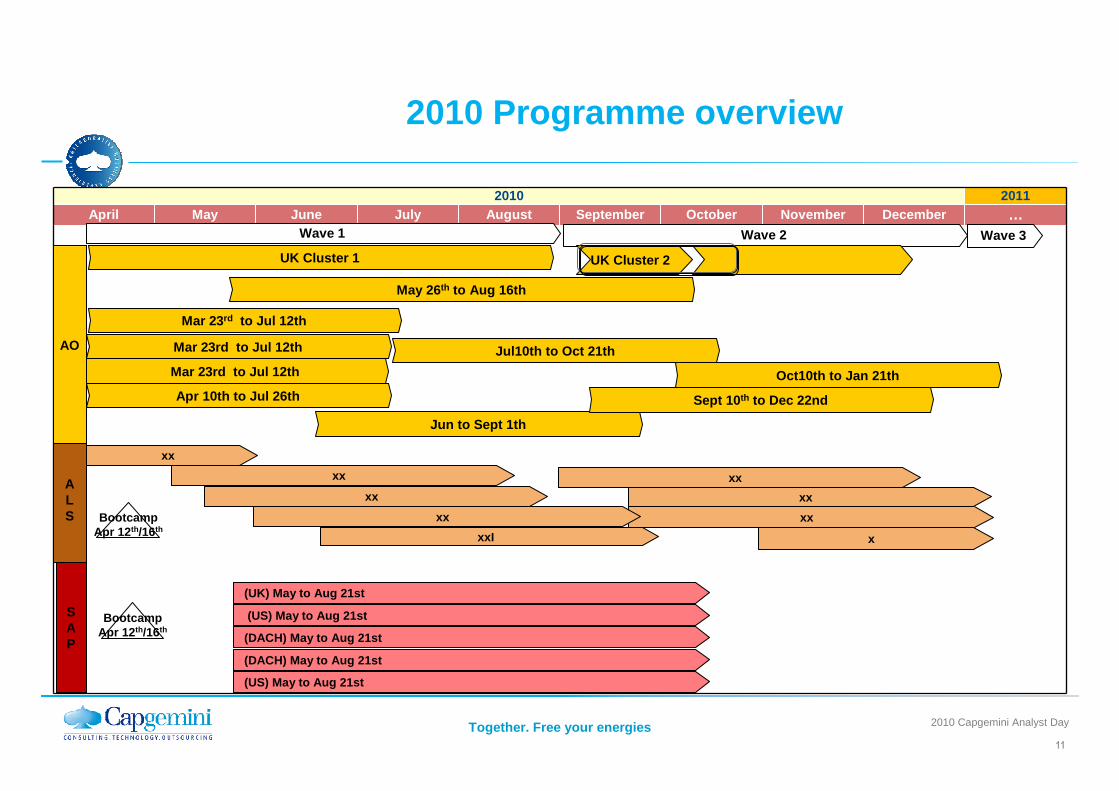

2010 Programme overview

2010 2011April May June July August September October November December …

Wave 1 Wave 2 Wave 3

ALS

SAP

xx

(UK) May to Aug 21st

UK Cluster 1 UK Cluster 2

May 26th to Aug 16th

Mar 23rd to Jul 12th

Mar 23rd to Jul 12th

Mar 23rd to Jul 12th

Apr 10th to Jul 26th

Jul10th to Oct 21th

Oct10th to Jan 21th

Jun to Sept 1th

Sept 10 th to Dec 22nd

xx

xx

xx

x

xx

BootcampApr 12 th/16th

BootcampApr 12 th/16th

xxI

xx

xx

(DACH) May to Aug 21st

(DACH) May to Aug 21st

AO

(US) May to Aug 21st

(US) May to Aug 21st

12

Together. Free your energies 2010 Capgemini Analyst Day

Focus Example findings

Inefficient resource on-boarding

10% productivity loss due to 23+ days delay in on-boarding

Offshore resource utilization 28% idle time for offshore resources

Low use of rightshoring Only 19% FTEs offshore

Manual testing70% of test steps could be automated for Regression and Negative testing

Missed CR revenue 36 CRs (worth €50K) unbilled to client in current phase

Re-use of standard tools

~3 days spent by 30% of project team members creating templates for project use

Focus Example findings

Inefficient resource on-boarding

10% productivity loss due to 23+ days delay in on-boarding

Offshore resource utilization 28% idle time for offshore resources

Low use of rightshoring Only 19% FTEs offshore

Manual testing70% of test steps could be automated for Regression and Negative testing

Missed CR revenue 36 CRs (worth €50K) unbilled to client in current phase

Re-use of standard tools

~3 days spent by 30% of project team members creating templates for project use

Our first Lean pilots in AO, ALS & Package deployme nt demonstrated that significant capacity release is

achievable in our business by adopting Lean princip les

Focus Example findings

Root Cause Analysis 0% proactive analysis on P3 and P4 incidents

Incident Management 20% of tickets return to user for more information

Change management 14 duplicate entries of data across 4 systems for a client CR

Change Management

100% of non-financial data fixes require same approval as full system deployment

Time Management 100% of support staff spend 1hr/week ensuring that data in Clarity and DTX match

Transition Management

6.5 days per month spent by Transition managers chasing project managers for plans/documentation

Focus Example findings

Root Cause Analysis 0% proactive analysis on P3 and P4 incidents

Incident Management 20% of tickets return to user for more information

Change management 14 duplicate entries of data across 4 systems for a client CR

Change Management

100% of non-financial data fixes require same approval as full system deployment

Time Management 100% of support staff spend 1hr/week ensuring that data in Clarity and DTX match

Transition Management

6.5 days per month spent by Transition managers chasing project managers for plans/documentation

� Pilots proved that significant capacity release is possible through the Lean approach

� At December ASEs, SMEsconfirm that over 50% of pilot findings are scalable

� Sustainability is achieved by changing behaviours and installing robust performance management systems

13

Together. Free your energies 2010 Capgemini Analyst Day

12 Month FTE capacity saving

Right first time (Offshore)

Root Cause Analysis & FMA (Offshore)

Knowledge Management (Offshore)

0.15

1.4

0.4

Root Cause Analysis & FMA (Onshore Service Desk)

1

Knowledge Transfer (On & Offshore)

TBD

Cashable

Re-investmen

t of capacity

into account

Opportunity Area Potential benefits

Total 3.65 FTE

% Capacity Release:

13.5%* out of 27FTE

in scope

Other solution activities (Onshore service desk)

0.7*

0% Scalable

100% Scalable

Pilot themes

Theme is only local

Don’t know

% Potential benefit for AO SupportBenefits (AO Support)

by end 2011

Capacity Release (FTEs)

% Capacity Release *

7.6

16.0%

6.8

33.0Problem Mgt

Knowledge Mgt (Incident)

Shift left (Incident) 3.4

Opportunity Area

Potential Benefits

(Hours per day)

Total Capacity Release

57.2

2.4

2.3DTX/Clarity - NOE Lite

DTX/Clarity - Plan Mgt

Application release window

0.7

Testing environment 4.1

2.6

0.4Test team KT

Change Mgt

1.5Batching of data fixes

Current FTEs 47.5

Cost/benefit – 36% ROI in Year 1

Str eams

1%

1 0%

1 .5FTE

6%

21%

3 FTE

11% 1.5 FTE 27% 3 FTE+

Improve employee w orking condi tions

Cr eate a mor e f lexible o rganisa t ionBreak the silos (horizontal tr aining)Strengthen employee ski lls (vertical tra ining )

Crea te a more effective organisationMonito r and control pro duction tightly Improve project govern ance

Implement best prac tices and rationa lise production too ls

Standardise and propagate best practices amongthe teamsRational ise the produ ction tools Revise the reso urce estimatio n models

Improve client relations to reduce reworkincluding improvement of the bi ll ing process

+ +

Mo ra le

ARE A PO TE NTIAL BE NEFI TS

TOTAL (% Benefits) +O ps MgtOps M gt

HighLow

2

6

8

3

7

4

5

1

S TRE AMS

Already decided & planned to

rem ove 10 FTE in the next 5 week s

(according to the training sessions)

Managem en t

O pe ra t ion s

O pe rat ion s

Benefits summary pilot 1Benefits summary pilot 1

Benefits summary pilot 2Benefits summary pilot 2

Benefits summary pilot 3Benefits summary pilot 3

Pilot teams and technical experts were broughttogether, and confirmed that over 50% of the

pilot findings were common/ scalable

14

Together. Free your energies 2010 Capgemini Analyst Day

Summary

� BeLean® is a bottom-up approach which delivers sustainable improvements by changing behaviours at all levels

� Our BaU programme has proved that substantial capacity release is possible in ‘Run’ environments (AM/ADM)

� We are in the process of mobilising the management levels to sponsor, support and drive realization of benefits

� Lean is potentially a powerful change process

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Salil Parekh

The next frontier:Offshore for growth

16

Together. Free your energies 2010 Capgemini Analyst Day

� Serve 900 clients from offshore

� Deploy 32,000professionals in low-cost delivery centers

� Growing at 32% offshore penetration

INDIA

20,50022,00025,000

EASTERN EUROPE

3,7004,1004,200

CHINA

1,0001,2001,200

LATIN AMERICA

1,2001,8502,300

MOROCCO

220260260

Red 2008 headcountBlack 2009 headcount Blue 2010 headcount (est.)

PHILIPPINES

Offshore has becomea core engine of our business

NEW!

17

Together. Free your energies 2010 Capgemini Analyst Day

What we learned during the slowdown

� Learning from our Financial Services, North America, and Australia businesses, we saw a segment of the market that we needed to play a larger part in: the offshore-driven market

� Clients are asking for more direct relationships with their teams offshore —for current business and for new sales and innovation

� Large clients are consolidating and focusing their vendor lists

� Fixed price delivery requires more cohesive onshore-offshore teams and processes

� As we move toward a greater proportion of our staff based in emerging markets, we need to actively manage cultural evolution within Capgemini, for performance and competitiveness

18

Together. Free your energies 2010 Capgemini Analyst Day

� Position our services more competitively

� Realize that depth of domain expertise is as critical as scale

� Leverage offshore as the ‘pivot point’ for delivering innovation

� Get onto client framework deals

� Develop joint onshore-offshore delivery programs

� Apply cultural awareness and commitment as a competitive edge

The next step of our transformation attempts to address these issues

19

Together. Free your energies 2010 Capgemini Analyst Day

Beyond price, we are managing customer-focused innovation in three ways:

LEAN

AGILEVIRTUALREALITY

If the price is right…

…then, if we demonstrate a world-beating solution…

…we earn the opportunity tooffer a winning deal

Price is a rite of passage, but customers also want deep expertise and innovative solutions

POSITION COMPETITIVELY

PRICEPOINT

COMPELLINGSOLUTION

VALUE& DEAL

DEPTH OF DOMAIN EXPERTISE AS CRITICAL AS SCALE

CoEs SOLUTION AREASCOMMUNITIES

VISUALISATION

CLOUDCOMPUTING

20

Together. Free your energies 2010 Capgemini Analyst Day

Offshore distributes local innovations globally and helps break into new markets

OFFSHORE GROWSOFFSHORE AS ‘PIVOT POINT’

FOR INNOVATION

Offshore serves as the coordination point for gathering leading solutions from one BU and launching them into all.

Innovation in Cloud services, SaaS, BIM, SmartX and others will continue to make us popular as an expert provider of leading solutions.

!

!!

!

!!

THAT WAS THEN (2007)

� Services unit of a large French telco

� Single project. Early stages of offshore usage.

THIS IS NOW (2010)

� € 20m across multiple projects during last three years and extended for additional three years.

� Offshore leverage over 80% across multiple projects. Some projects at 100% offshore leverage.

� End to end delivery managed offshore

OUR APPROACH

� Focus on understanding business requirements.

� Mutualized team and flexible staffing across multiple projects.

� End to end responsibility of customer relationship

21

Together. Free your energies 2010 Capgemini Analyst Day

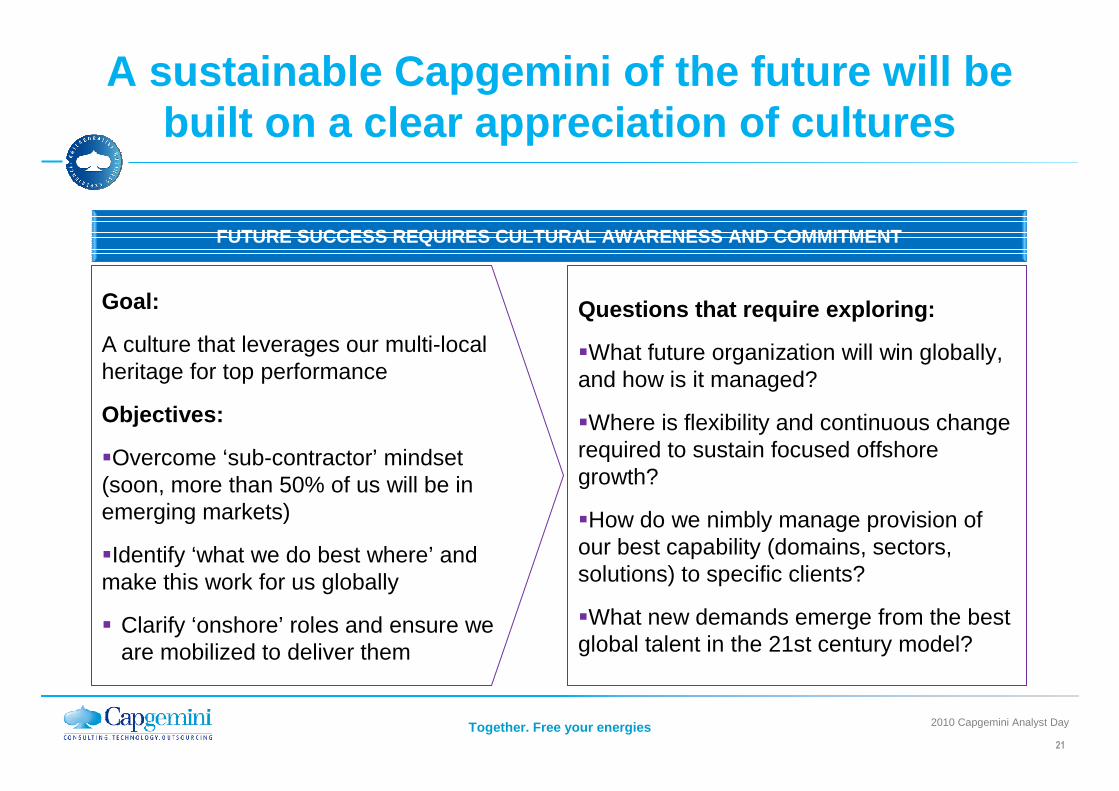

A sustainable Capgemini of the future will be built on a clear appreciation of cultures

FUTURE SUCCESS REQUIRES CULTURAL AWARENESS AND COMM ITMENT

Questions that require exploring:

�What future organization will win globally, and how is it managed?

�Where is flexibility and continuous change required to sustain focused offshore growth?

�How do we nimbly manage provision of our best capability (domains, sectors, solutions) to specific clients?

�What new demands emerge from the best global talent in the 21st century model?

Goal:

A culture that leverages our multi-local heritage for top performance

Objectives:

�Overcome ‘sub-contractor’ mindset (soon, more than 50% of us will be in emerging markets)

�Identify ‘what we do best where’ and make this work for us globally

� Clarify ‘onshore’ roles and ensure we are mobilized to deliver them

22

Together. Free your energies 2010 Capgemini Analyst Day

We are growing…

...through bringing new innovation to our customers

We are stretching margins…

…bringing more offshore capability into our propositions

We are unifying delivery…

…by cross-fertilizing capability through transversal offerings

KEY INITIATIVES

� Joint account management

� Framework penetration

� Rapid lead generation

� Large deal teams

KEY INITIATIVES

� Low-cost deployment

� Fixed-price delivery

� Competitive pricing

KEY INITIATIVES

� Centres of excellence

� OneTeam delivery

� Customer visit experience

We are driving the transformation via a set of initiatives for growth and margin

GROWTH

CUSTOMER MARKETS INDIA & OFFSHORE

MARGINS

23

Together. Free your energies 2010 Capgemini Analyst Day

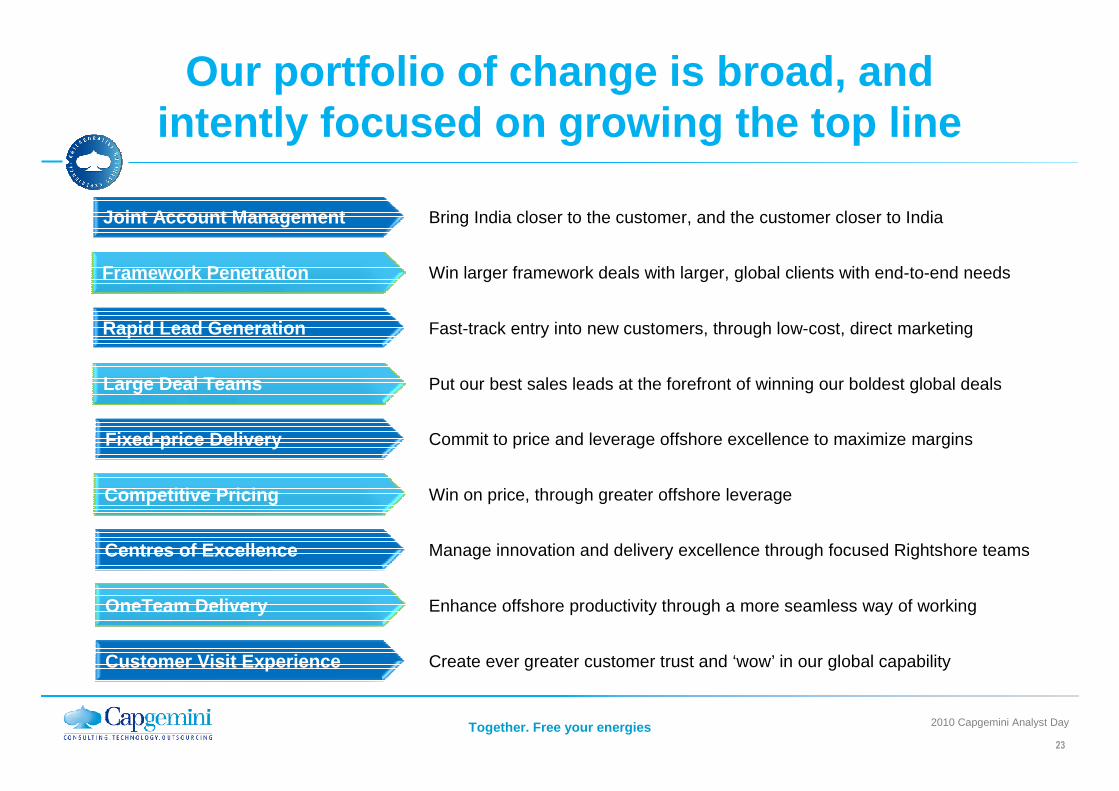

Our portfolio of change is broad, and intently focused on growing the top line

Joint Account Management

Framework Penetration

Rapid Lead Generation

Large Deal Teams

Fixed-price Delivery

Competitive Pricing

Centres of Excellence

OneTeam Delivery

Bring India closer to the customer, and the customer closer to India

Win larger framework deals with larger, global clients with end-to-end needs

Fast-track entry into new customers, through low-cost, direct marketing

Put our best sales leads at the forefront of winning our boldest global deals

Commit to price and leverage offshore excellence to maximize margins

Win on price, through greater offshore leverage

Manage innovation and delivery excellence through focused Rightshore teams

Enhance offshore productivity through a more seamless way of working

Customer Visit Experience Create ever greater customer trust and ‘wow’ in our global capability

24

Together. Free your energies 2010 Capgemini Analyst Day

The program puts offshore onto the front lines of our go-to-market strategy

LOCAL DELIVERY OF GLOBAL DESIGNS

TS NA

TS UK

OS

...

GROUP STRATEGY & DIRECTION

BEST PRACTICE ‘DRAG & DROP’

RADICALRIGHTSHORE

� Offshore and India have increasing impact on the shape of Group strategy

� Business units are ‘upping their game’ through adoption of our best ways of working, coordinated and distributed by an India core team

� Global improvements are accelerated through immediate duplication of our best ways of working, across all business units

25

Together. Free your energies 2010 Capgemini Analyst Day

The program is re-designingthe way we work in certain areas

WE ARE CREATING SPACE TO DELIVER OUR E2E CAPABILITY

WE ARE GROWINGA SUSTAINBLE REVENUE BASE

WE ARE MORE COMPETITIVE

COMPETITIVE PRICING

� Stronger price challenge

� Global standards

� Better leverage

JOINT ACCOUNT MGMT

� Improved client intimacy

� Clearer accountability

� More account talent

FRAMEWORK PENETRATION

� Greater market visibility

� Deeper relationships

� Global process live

� Regular flow of deals

� Ruthless price challenge –focused on offshore blend

� 34 accounts agreed

� Global model live

� Joint teams mobilised

� New managers on board

� Account team training underway

� 16 accounts agreed

� Global standards defined

� Framework pursuit teams mobilised

� Framework core team leading from offshore

26

Together. Free your energies 2010 Capgemini Analyst Day

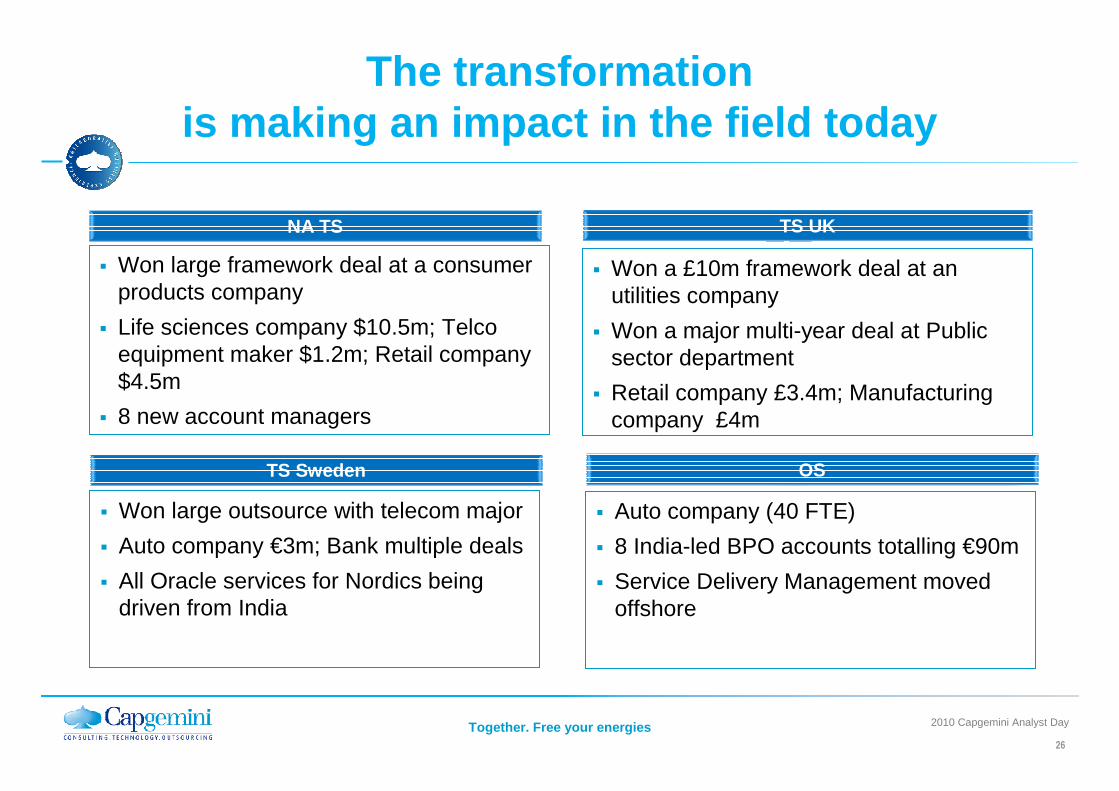

The transformationis making an impact in the field today

NA TS

� Won large framework deal at a consumer products company

� Life sciences company $10.5m; Telco equipment maker $1.2m; Retail company $4.5m

� 8 new account managers

TS UK

TS Sweden OS

� Won large outsource with telecom major

� Auto company €3m; Bank multiple deals

� All Oracle services for Nordics being driven from India

� Won a £10m framework deal at an utilities company

� Won a major multi-year deal at Public sector department

� Retail company £3.4m; Manufacturing company £4m

� Auto company (40 FTE)

� 8 India-led BPO accounts totalling €90m

� Service Delivery Management moved offshore

27

Together. Free your energies 2010 Capgemini Analyst Day

� Faster growth: 3 points of extra growth where program initiatives are deployed in the field

� Stronger intimacy and stickiness with clients: via joint account management and framework deals

� Access to larger, global clients: by becoming more competitive, but with depth of expertise and innovation

Where does that take us …

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Andy Mulholland

Innovation; Business and Technology Change

The Innovation question is; Not what is the role of the IT departmentbut what is the role ofTechnology within the Enterprise

29

Together. Free your energies 2010 Capgemini Analyst Day

Our Clients’ agenda? Moving back to Growth!

Source and copyright by Peter Evans-Greenwood, Unic o pty

Value Creating

ExternalWeb & Clouds

InternalEnterprise IT

operations

sales support

billing & collectionstraditionalbusiness intelligence

Focused and strong signals

Mixed and weak signals Realtime analysis

of opportunities

Cost Driven

EventsTransactions

30

Together. Free your energies 2010 Capgemini Analyst Day

New Business Models built on Technology & Services

31

Together. Free your energies 2010 Capgemini Analyst Day

Technology is used every where in the business

Internal External

People

Applications Computers

Web Services

32

Together. Free your energies 2010 Capgemini Analyst Day

Now put the Business and Technology Together …

Internal External

Cost

Value

SupportingPeople and Expertise

SupportingComputers

andSystems

33

Together. Free your energies 2010 Capgemini Analyst Day

The focus for the Breakout sessions;

Internal External

Cost

Value Supporting

People and Expertise

SupportingComputers

andSystems

Business InformationManagement

A roadmap from TraditionalBI to Realtime Data Analysis

Infostructure TechnologyServices

Moving to improve IT flexibility & change the delivery model

Smart BusinessUtilities

Creating new markets and Value through technology

34

Together. Free your energies 2010 Capgemini Analyst Day

Business Collaborative Innovationits part of the Capgemini Collaborative Business Exp erience!

Three unique methods;

� TechnoVision – the Capgemini approach to enable an Enterprise to understand how technology will impact its business both beneficially and adversely to be able to define and focus on crucial actions.

� RApid INnovation, RAIN – Capgemini working in partnership with Intel Capital to bring the capabilities of more than 300 advanced technology companies into our clients requirements to provide defined requirements and benefits specifications for new projects.

� Rapid Design & Visualisation, RDV, – the Capgemini method for capturing requirements as visual prototypes so ‘agile’ and iterative builds can be used to provide high value leading edge business solutions with immediate delivered benefits.

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Cyril Garcia

Winning position in a new market

36

Together. Free your energies 2010 Capgemini Analyst Day

• Reality of ‘Cloud’ offerings: external storage, processing and connectivity options at unit and usage costing

• Data generation continues to explode: analytics, BI, manipulation personal data management tools grow as a result, in memory

• Security

• Globalisation: international regulation, globalised markets and organisation structures continue apace

Techno evolutions feed a disruptive world

Virtualizedeconomy

Virtualizedeconomy A world of

citiesA world of

cities

Business decision

making shifts east

Business decision

making shifts east

A sustainablegrowth

A sustainablegrowth

37

Together. Free your energies 2010 Capgemini Analyst Day

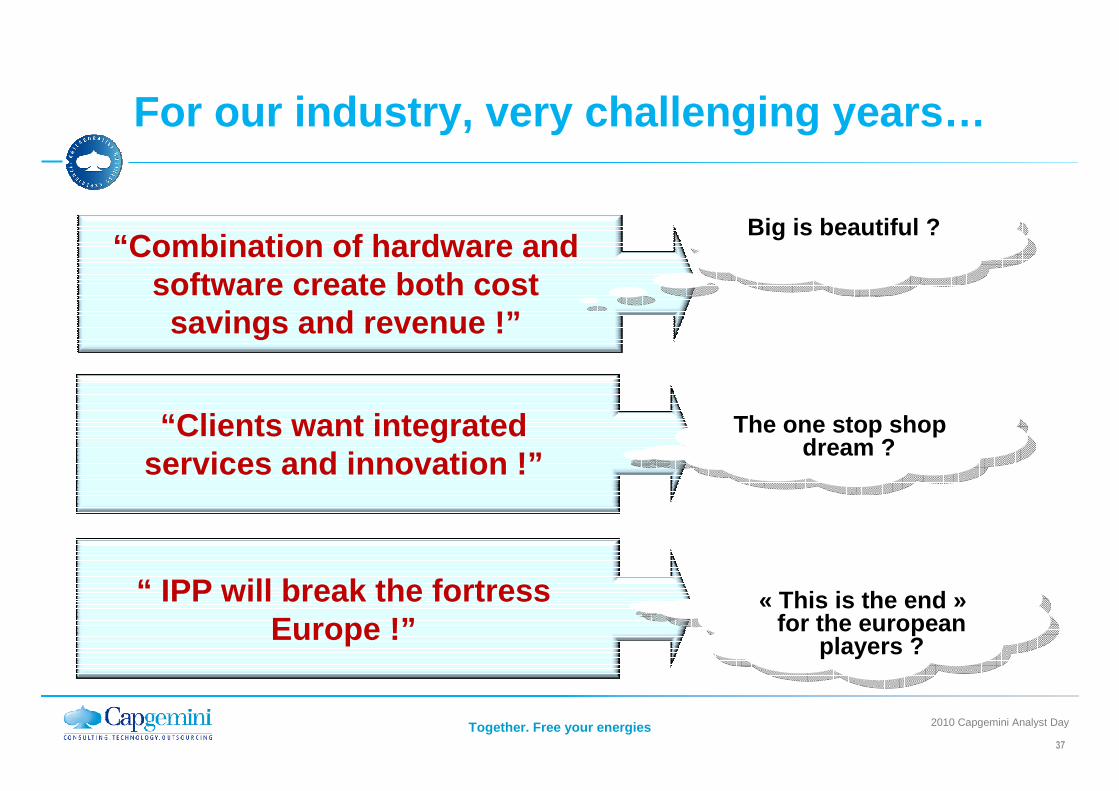

For our industry, very challenging years…

“Combination of hardware and software create both cost

savings and revenue !”

“Clients want integrated services and innovation !”

“ IPP will break the fortress Europe !”

Big is beautiful ?Big is beautiful ?

The one stop shop dream ?

The one stop shop dream ?

« This is the end »for the european

players ?

« This is the end »for the european

players ?

38

Together. Free your energies 2010 Capgemini Analyst Day

Thanks to our I 3 program we are now positioned as a global leader

3

Global reach

Strong brand

Leader in chosen segments

Above market growth

Strong sales coverage

Balance sheet to invest

Differentiated IP

Lean cost structure

AccentureHPIBM Capgemini

39

Together. Free your energies 2010 Capgemini Analyst Day

Global and country managed accounts

We are starting a journey far more complex, which mobilizes the group

Manage the portfolio

Rebalance geographies

Invest in new offerings

Capgemini

Become strategic for clients

Streamline cost structure

Competition

Acquisition

Business analyticsCloud computingSmarter gridCloud

Diamond clientsSales coverage

BRIC, Mexico, South Korea,China

Leaner cost structureLayoffs plan

Latam, APAC, India, Eastern Europe

ITS & CloudBIMSmart energy

Application lifecycle servicesTesting services

RightshoreIndia enabled transformationLean

40

Together. Free your energies 2010 Capgemini Analyst Day

Back Office industrialization will share the stage with technology

drivers

Growth

Time

Business maintenance and BO industrialization

New custom softwares

New custom softwares

Disperseddevice

systems

Disperseddevice

systems

Systems of systems

Systems of systems

2010/2011 ?

Tipping point

41

Together. Free your energies 2010 Capgemini Analyst Day

Clients are starting to adopt these drivers

CustomedServices

Shared resources

IP

Infrastructure

End-to-endservices

Flexibility

Saas+BPO

Service platform

Interaction platform

Xaas

42

Together. Free your energies 2010 Capgemini Analyst Day

These technology drivers are accelerating with diff erent impact on industries

GOV TME

Risks & regulation

Online 2.0

Rail network management

PLM

Consolidation

Customer lifecycle

management

Emerging markets

Customer analytics

Multi-channel

Billing & customer

information systems

New entrants

Smart meters & smart grid

E-border

eHealth

Tax systems

Billing

Smartphones

Digital media

Level of change

Security systems

Network engineering &

field management

ConsolidationStandardization

Diversification

Consolidation

Retail EUC FS ServicesManufacturing

Long term growthCapgemini has some strong positions and consulting favors business alignment

43

Together. Free your energies 2010 Capgemini Analyst Day

Clients are expecting new business models

Businesses

Models

OLD NEW

OLD

NEW

Complex systemsComplex systems

TransactionsAas

TransactionsAas

Interaction servicesInteraction services

End-to-end IT

applications

End-to-end IT

structure

performance

End-to-end

business

outsourcing

44

Together. Free your energies 2010 Capgemini Analyst Day

How to win positions in this new market

Businesses

EconomicModels

OLD NEW

OLD

NEW

TECHPLATFORMTECHPLATFORM

SECTOR KNOWLEDGESECTOR KNOWLEDGE

INVESTMENTSINVESTMENTS

BI, SES, Alliances…BI, SES,

Alliances…

FS, Telco,PS,EUFS, Telco,PS,EU

Alliances, IP, COEs

Alliances, IP, COEs

45

Together. Free your energies 2010 Capgemini Analyst Day

This may trigger a new IT role where intelligence a nd services will be key differentiators

AggregatedCloud services

AlliancesPartners

Bundling BPO + Software platform

TechnologyBusiness

IntelligenceService

Integrator andOperator

Complex customsoftwares

Security SLAs

Sector expertises

Partner resources

Eveything as A service Own resources

2010 Analyst DayChicago, June 2 & 3

2010 Analyst DayChicago, June 2 & 3

Paul Hermelin

Meeting the challenge of market disruptions

47

Together. Free your energies 2010 Capgemini Analyst Day

Some areas of our portfolio are getting hot

Pipeline growth

ALS

BIM

TST

SES

ITS

CC

Sogeti

SCM

CRM

FS

Gov US

Manufacturing

NA

Nordics

APAC

Eastern Europe Utilities

Offerings Disciplines Geographies Sectors

BPO

48

Together. Free your energies 2010 Capgemini Analyst Day

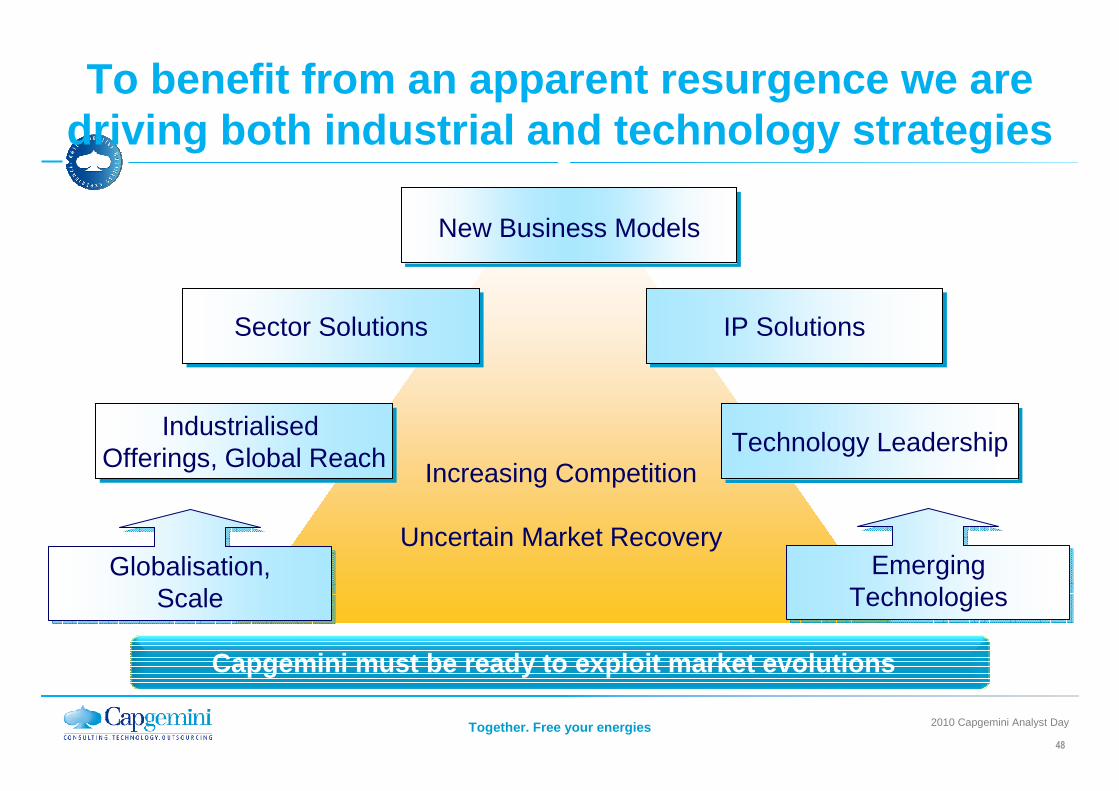

To benefit from an apparent resurgence we are driving both industrial and technology strategies

Capgemini must be ready to exploit market evolutions

New Business Models

Increasing Competition

Uncertain Market RecoveryGlobalisation,

ScaleGlobalisation,

ScaleEmerging

TechnologiesEmerging

Technologies

IP SolutionsIP Solutions

Technology LeadershipTechnology Leadership

Sector SolutionsSector Solutions

Industrialised Offerings, Global Reach

Industrialised Offerings, Global Reach

49

Together. Free your energies 2010 Capgemini Analyst Day

Global delivery will be a strong differentiator in a thawing market

Offshore is rebounding…

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 Q1'10

Offshore headcount growth q/q

Capgemini Accenture Wipro (IT svces)

Capgemini has taken early steps and will keep its fo cus

…a driver we embrace

9 000

20 00025 300 28 000

36 000

2006 2007 2008 2009 2010

Offshore headcount

Subcontractormodel

�Volume driven

�Pure delivery�Onshore

responsibility

One teammodel

�Shared KPIs�Client exposure�Sales support� Innovation�Shared

responsibility

Kanbay

Empoweredmodel

�Shared client ownership

�Full responsibility

�Transversal expertise

�Most competitive pricing

50

Together. Free your energies 2010 Capgemini Analyst Day

Technology drivers are accelerating

Networked devices

Consumer technology

& Webservices

Capgemini builds on strong assets: Alliances, Techno logy Culture, Management Talent and a true Entrepreneurial Mindset

Smart X

Smart energy

Smart transport

Cloud

Cloud services

IaasGreen IT

Virtualization

Collaboration

Social CRMMarketing

Social web

MobilityApps

MCommerce

In-memory

BI & analytics

Real-Time

Portals

Maturity

51

Together. Free your energies 2010 Capgemini Analyst Day

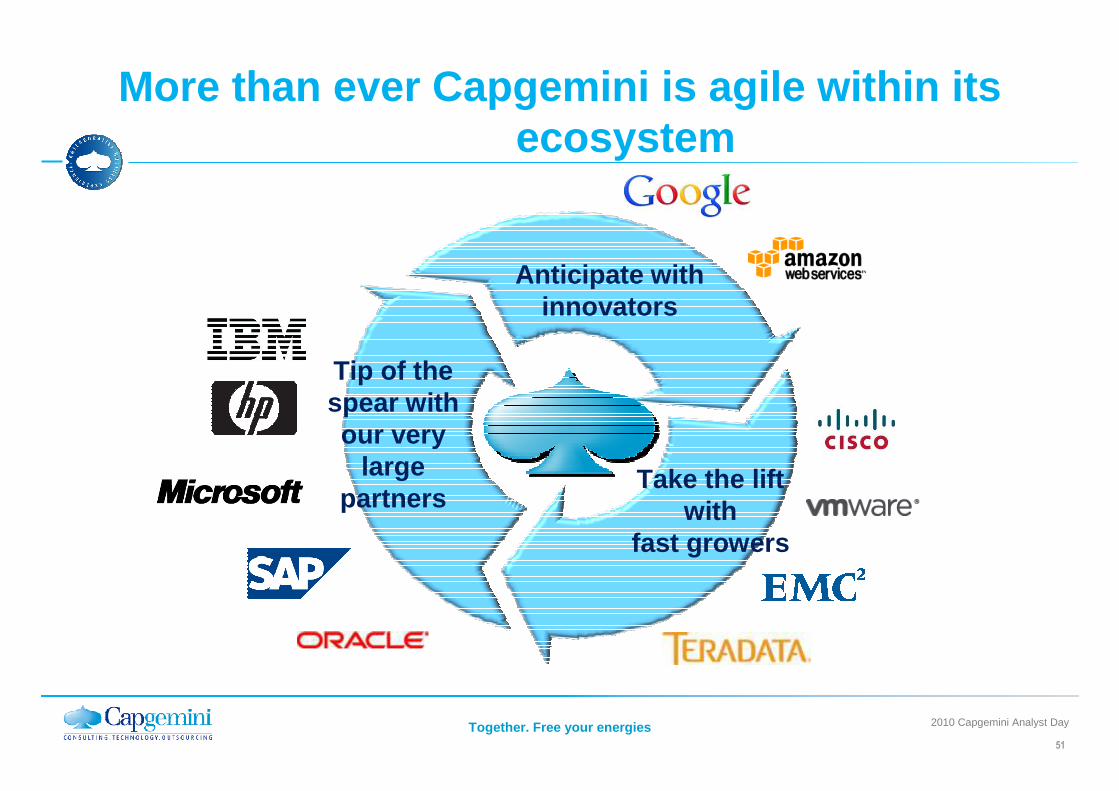

More than ever Capgemini is agile within its ecosystem

Tip of the spear with our very

large partners

Take the lift with

fast growers

Anticipate withinnovators

52

Together. Free your energies 2010 Capgemini Analyst Day

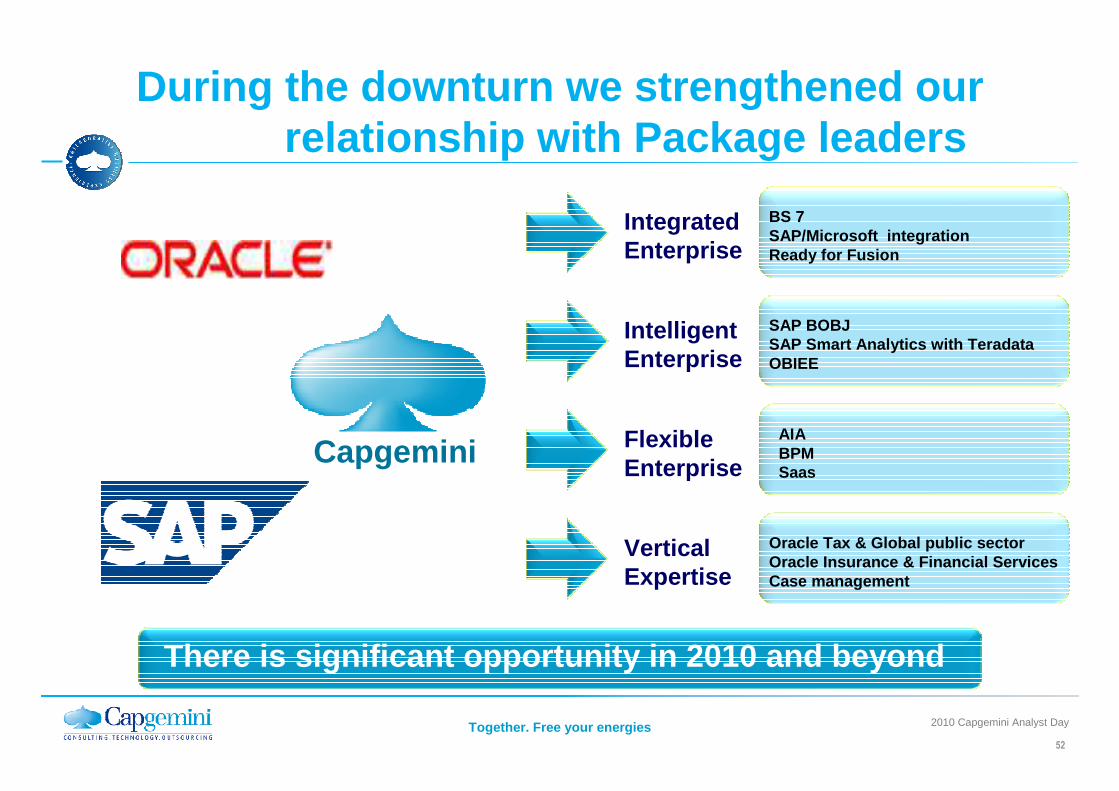

During the downturn we strengthened our relationship with Package leaders

Capgemini

Integrated Enterprise

BS 7SAP/Microsoft integrationReady for Fusion

Intelligent Enterprise

SAP BOBJSAP Smart Analytics with TeradataOBIEE

Flexible Enterprise

AIABPMSaas

VerticalExpertise

Oracle Tax & Global public sectorOracle Insurance & Financial ServicesCase management

There is significant opportunity in 2010 and beyond

53

Together. Free your energies 2010 Capgemini Analyst Day

Capgemini is broadening our traditional Alliances with Channel-based Strategic Selling

Regular Engagement

• Deal Driven Partnering

• Skills, Certification, Resources

• Geographic co-ordination

• Account Teams

• Sales Teams

Regular Engagement

• Deal Driven Partnering

• Skills, Certification, Resources

• Geographic co-ordination

• Account Teams

• Sales Teams

Differentiated Partnerships• IP accelerators support Partner Technical

Solutions

• Co-owned IP for sector-specific applications

• Joint GTM leveraging Partners’geographic sales teams

• Solution Specific CoEs

Differentiated Partnerships• IP accelerators support Partner Technical

Solutions

• Co-owned IP for sector-specific applications

• Joint GTM leveraging Partners’geographic sales teams

• Solution Specific CoEs

Alliances Channels

Our value proposition is to integrate and support

Focus: De-risking DeliveryFocus: De-risking Delivery Focus: Pipeline GrowthFocus: Pipeline Growth

54

Together. Free your energies 2010 Capgemini Analyst Day

We are changing to build our leadership position

Global reach

Strong brand

Leader in chosen segments

Above market growth

Strong sales coverage

Balance sheet to invest

Differentiated IP

Lean cost structure

� Renewed offshore drivers� Lean supply chain� Portfolio management

� Emerging markets� New business models� Differentiated IP

Capgemini’s current position

Strengthen Core

Business

New Growth

Initiatives

55

Together. Free your energies 2010 Capgemini Analyst Day

Our acquisition program is aligned

Expand

Consolidate

Long Term Short Term

IBX

China

US portfolio

Smart X RevenueSynergies

Offensive

Defensive

CostSynergies

56

Together. Free your energies 2010 Capgemini Analyst Day

We now are facing new challenges for 2013

Business partner

Global

Local

Businesstechnology Tech integrator

Proximity

Intimacy Rightshore

IndependentIndustrializedBuild & Operate

Reactive Pervasive

New modelsSector expertiseConsulting