26

2010 Budget: Presentation National Treasury February 2010

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | christopher-robbins |

| View: | 215 times |

| Download: | 1 times |

2010 Budget:Presentation

National TreasuryFebruary 2010

Five key messages of the budget

• Our country needs a united effort, drawing in business, labour and community organisations to map out a path to boost growth, raise employment and reduce poverty

• Today, we table important elements of a new growth path, including proposals to raise employment

• We will carefully and gradually reduce the budget deficit to more sustainable levels

• We are not increasing the tax burden this year

• We are taking firm steps to improve the quality of spending and reduce corruption

2

Key aspects of a new growth path that supports faster growth and job creation

• A concerted effort to reduce joblessness among young people

• Support for labour-intensive industries through industrial policy interventions, skills development, public employment programmes and a rural development strategy

• Sustaining high levels of public and private investment and raising our savings level

• Keeping inflation low, striving for a stable and competitive exchange rate, and providing a buffer against global volatility

• Improving the performance and effectiveness of the state, especially the provision of quality education and training at all levels

• Reforms to increase inclusion and participation in the labour market, alongside efforts to improve competition in product markets

• Raising productivity and competitiveness, opening up the economy to investment and trade opportunities that can boost exports.

3

The macroeconomic forecast

• Growth projections revised higher to 2.3% in 2010 rising to 3.6% in 2012• Recovery supported by improved global environment, rising investment

spending, government consumption, gradual rise in household spending

4

Macroeconomic projections, 2006 – 2012Calendar year 2006 2007 2008 2009 2010 2011 2012

Actual Estimate Forecast

Percentage change unless otherwise indicated

Final household consumption 8.3 5.5 2.4 -3.5 0.9 2.6 2.9

Final government consumption 4.9 4.7 4.9 5.7 4.7 4.1 3.6

Gross fixed capital formation 12.1 14.2 11.7 4.0 5.8 7.8 8.7

Gross domestic expenditure 8.6 6.4 3.3 -1.9 3.1 3.5 3.8

Exports 7.5 5.9 2.4 -20.2 3.8 3.9 5.4

Imports 18.3 9.0 1.4 -18.3 6.8 4.9 5.6

Real GDP growth 5.6 5.5 3.7 -1.8 2.3 3.2 3.6

GDP inflation 6.5 8.2 9.2 7.4 6.6 7.3 6.5

GDP at current prices (R billion) 1 767 2 017 2 284 2 407 2 626 2 908 3 211

Headline CPI inflation 3.2 6.1 9.9 7.1 5.8 6.1 5.9

Current account balance (% of GDP) -5.3 -7.2 -7.1 -4.3 -4.9 -5.3 -5.8

Risks to recovery

• Global risks

– Premature removal of fiscal and monetary policy stimuli

– Impact of high debt burdens on growth and inflation

– Overheating of Chinese economy and lower commodity prices

– Impact of large capital flows to emerging markets on asset prices and exchange rates

– Lack of reform in global financial system leading to “business as usual” approach and re-emergence of bubbles

• Domestic risks

– Slower recovery in employment, credit extension and household spending

– Impact of increase in electricity prices on growth and inflation

– Low productivity growth and a stronger real exchange rate constraining competitiveness of exports

5

Improved outlook for global growth

• The IMF expects world growth to recover to 3.9% in 2010 and 4.3% in 2011

• Emerging markets grow strongly driven by China, India and Brazil

• Higher growth supports commodity prices and SA’s terms of trade

• Risks from weak labour market and growing debt burdens in developed countries

IMF growth forecast, by region

6

IMF growth forecast2010 2011

World 3.9 4.3

US 2.7 2.4

Euro area 1.0 1.6

UK 1.3 2.7

Japan 1.7 2.2

China 10.0 9.7

India 7.7 7.8

South Africa 2.3 3.2 2

3

4

5

6

7

Per

cent

age

chan

ge

2010 2011

Signs of economic recovery in South Africa

• A range of indicators point to recovery:

– The leading indicator up 14.6% between March and November 2009

– Improvement in manufacturing and mining output

– PMI rose to 53.6 in January 2010

– Manufacturing capacity utilisation above 80% in the fourth quarter

– New car sales up 15.4% y-o-y in January 2010

– House prices are rising

– 89 000 jobs created in the fourth quarter

Components of the Purchasing Managers Index

Mining, manufacturing & electricity output

7

70

80

90

100

110

120

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Mining output

Manufacturing output

Electricity output

Inde

x 20

05=1

00 (t

hree

mon

ths

mov

ing

aver

age)

20

30

40

50

60

70

80

2005

2006

2007

2008

2009

2010

Diff

usio

n in

dex

(sea

sona

lly a

djus

ted)

a

a

Total PMIPMI-Expected business conditions PMI - Inventories

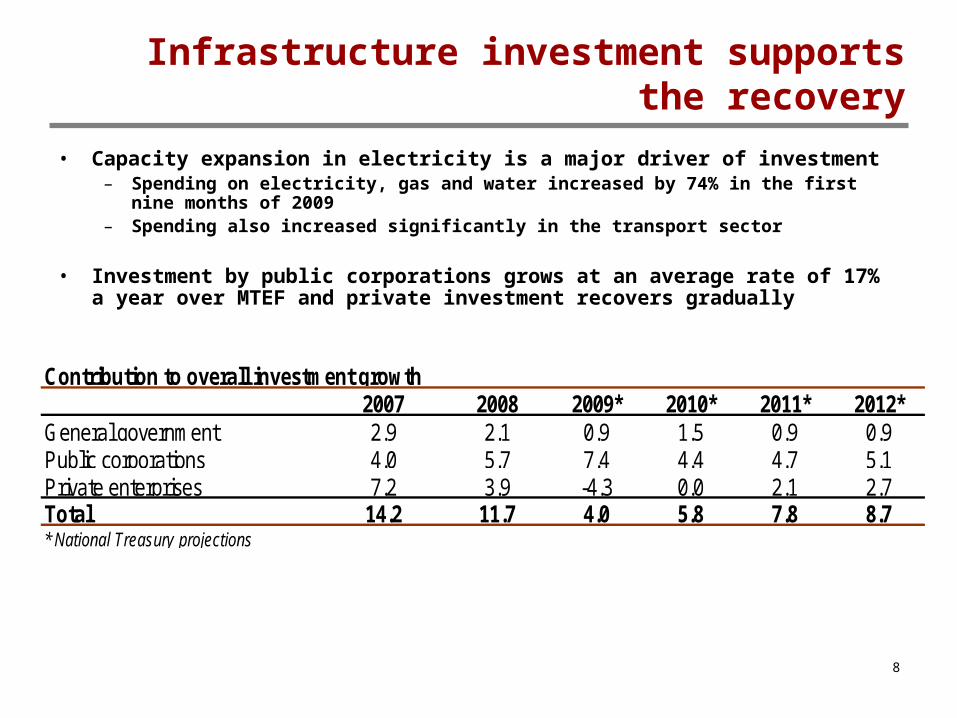

Infrastructure investment supports the recovery

• Capacity expansion in electricity is a major driver of investment– Spending on electricity, gas and water increased by 74% in the first nine months of

2009– Spending also increased significantly in the transport sector

• Investment by public corporations grows at an average rate of 17% a year over MTEF and private investment recovers gradually

8

Contribution to overall investment growth2007 2008 2009* 2010* 2011* 2012*

General government 2.9 2.1 0.9 1.5 0.9 0.9Public corporations 4.0 5.7 7.4 4.4 4.7 5.1Private enterprises 7.2 3.9 -4.3 0.0 2.1 2.7Total 14.2 11.7 4.0 5.8 7.8 8.7* National Treasury projections

Addressing the employment challenge

9

• Employment growth is likely to be weak in the short-term

• The economy must grow faster and raise the absorptive capacity

• The employment challenge demands a comprehensive policy framework

• Improving education is a key priority in the long-term

• Our approach to employment creation includes:

– Measures to encourage industries and services that have significant jobs potential

– Stepped up implementation of the expanded public works programme

– Investment in further education and skills development

– Encouragement of small business development and entrepreneurship

– A new focus on promoting youth employment

Employment scenarios

10

Scenario planning – 2010-2019

• Moderate recovery will create about 1 million jobs in the next 5 years

• The economy must grow faster and labour absorption need to be higher

• If growth averages 6% over 2015-19 then employment will be 1.3 million higher than if the economy grows at 3.5%.

Employment scenarios, 2010 - 2019

2010 – 2014 2015 – 2019 2010 – 2014 2015 – 2019 2014 2019

Scenario A 3.2 3.5 1 085 1 274 22.6 19.8

Scenario B 3.4 4.0 1 147 1 470 22.2 18.5

Scenario C 3.5 4.5 1 189 1 667 22.0 17.2

Scenario D 3.7 6.0 1 251 2 266 21.7 13.8

1. The scenarios project growth of 1% per year for the working age population and hold the labour force participation rate

constant at 55%.

Growth (%) Change in employment (thousands)

Unemployment rate (%)

Youth unemployment is the priority

11

• Young people tend to be unemployed for a long time before finding a job leaving them vulnerable to future unemployment and lower wages

• A wage subsidy will create an incentive to hire young and inexperienced workers

• The aim is to raise youth employment by 500 000 by 2013

• A discussion document with further details will be tabled by the end of March

48.2

28.5

13.5

24.3

0

10

20

30

40

50

60

18-24

25-34 35

+

Averag

e

Age group

unem

ploy

men

t rat

e (p

er c

ent)

Consolidated government fiscal framework

• Countercyclical fiscal policy has enabled continued spending on strategic priorities as weak economic activity has reduced revenue

• Government has increased debt to sustain spending• Over the MTEF, the consolidated government deficit is projected to recover from

7.3% of GDP in 2009/10 to 4.1% by 2012/13• Lower deficit due to increased revenue as economy recovers and slower growth

in non-interest spending

12

Budget 2010: Consolidated Government Budget Framework2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

R million / per cent Estimate

Revenue 627 669 689 671 657 552 738 404 827 742 922 278

per cent GDP 30.2% 29.7% 26.8% 27.3% 27.9% 28.0%

Expenditure 593 269 713 890 835 324 906 964 977 361 1 058 622

per cent GDP 28.5% 30.8% 34.1% 33.6% 32.9% 32.1%

Budget balance 34 400 - 24 219 - 177 773 - 168 560 - 149 619 - 136 344

per cent GDP 1.7% -1.0% -7.3% -6.2% -5.0% -4.1%

Projections

Debt and interest costs

• National net loan debt is forecast to increase from 22.7% in 2008/09 to 39.8% of GDP by 2012/13

• Interest costs are the fastest growing area of spending over the MTEF and rise to 3.2% of GDP by 2012/13

• To support fiscal sustainability, government will need to reduce borrowing and debt as the economy recovers

• If revenue does not recover sufficiently, tax rates will need to be adjusted and the tax base broadened, and growth in expenditure moderated further

13-6

-3

0

3

6

9

12

15

18

Average 2005/06 - 2008/09 Average 2009/10 - 2012/13

Av

era

ge

re

al

gro

wth

Debt service costsCompensation of employeesTransfers to householdsCapitalOther current spend

Real growth in areas of expenditure, 2005/06 – 2012/13

Fiscal sustainability – the primary balance

• Non-interest spending rose strongly during the economic boom supported by robust revenue growth

• Revenues are currently insufficient to cover non-interest spending and interest payments, but will rise as economy recovers

• In addition, real growth in non-interest spending moderates to only 1% on average over the MTEF to stabilise debt

• This reduces the primary balance from -5% of GDP in 2009/10 to -1% in 2012/13

14

20

22

24

26

28

30

32

Per

cen

t of G

DP

Non-interest expenditure

Budget revenue

Fiscal sustainability – debt

• Countercyclical fiscal stance enabled government to meet its expenditure commitments during the recession

• The shortfall between revenue and expenditure has been financed by debt leading to higher debt-service costs over the MTEF

• Forecasts indicate the debt ratio will peak between 43% and 48% of GDP in 2015/16, before gradually declining over the longer term

• As the economy recovers government will act to reduce borrowing and pay down debt

Long-term forecast of national government debt, % of GDP

Possible debt outcomes, % of GDP, 2015/2016

15

0

5

10

15

20

25

30

35

40

45

50

Per

cent

age

of G

DP

0

5

10

15

20

25

30

35

Less than33%

33 - 38% 38 - 43% 43 - 48% 48 - 53% 53 - 58% More than58%

Debt to GDP, 2015/16

Prob

abili

ty (p

er c

ent)

Fiscal sustainability – how does SA compare?

• Countries with high levels of debt tend to grow more slowly

• Several countries are facing the real threat of default, making international markets particularly nervous about sovereign debt accumulation

• A credible strategy to reduce debt over the medium term supports fiscal sustainability and reduces pressure on South Africa’s credit rating

Selected forecasts, real growth and average government debt to GDP, 2009 – 2014

16

01234Average real GDP growth, 2009 - 2014

0 20 40 60 80 100 120 140

Chile

Thailand

SA

Turkey

Brazil

Ireland

Spain

Portugal

UK

Greece

Average government debt to GDP, 2009 - 2014

Public sector infrastructure spending

• Public sector spending on infrastructure remains strong over the MTEF helping to raise South Africa’s future growth potential

• R846 billion will be spent over the MTEF period

– Non-financial public enterprises to spend R454 billion (53.7% of total spend)

– Provinces and municipalities continue to be significant drivers of infrastructure spending due to capacity expansion in transport, housing, water & sanitation, hospital revitalisation and social infrastructure

17

Public sector infrastructure expenditure and estimates, 2006/07 – 2012/132008/09 2009/10 2010/11 2011/12 2012/13

R millionOutcome

Revisedestimate

Medium-term estimates

Consolidated government 48 606 58 426 63 645 72 812 80 310

Percentage of GDP 2.1% 2.4% 2.4% 2.5% 2.4%

General government 93 125 109 657 114 889 134 650 142 447

Percentage of GDP 4.0% 4.5% 4.3% 4.5% 4.3%

Non-financial public enterprises 103 322 125 504 147 025 148 665 157 970

Percentage of GDP 4.5% 5.1% 5.4% 5.0% 4.8%

Total 196 447 235 161 261 914 283 315 300 417

Main tax proposals: 2010/11

• Individuals:

– Personal income tax relief amounting to R6.5 billion

– Higher monthly cap for medical scheme contributions

– Tax-free interest income threshold raised

– Reforms to travel allowances take effect from 1 March 2010

• Businesses:

– Further closure of tax loopholes

– Promotion of South Africa as gateway into Africa by relaxing rules governing corporate headquarters

• Reduced interest charges and penalties for voluntary disclosures by non-complaint of taxpayers

• Environmental fiscal reforms:

– CO2 motor vehicle emission tax simplified and delayed until 1 Sep 2010

– Carbon tax discussion document to be released for comment by mid 2010

• Increases in excise duties and fuel taxes:

– Road Accident Fund (RAF) and general fuel levy, including a levy to contribute towards the construction of a new pipeline

– Excise duties on alcoholic beverages and tobacco products18

Proposals on exchange control reforms

Banks• Implementation of the macro-prudential limit on banks• Foreign exposure limit will be 25% of total liabilities • The previous limit of 40% of liabilities was never implemented, the downward

adjustment is due to developments in global financial markets

Institutional investors • Updating Regulation 28 – technical amendments to allow investments in new

products and align with excon foreign investment limits • Private equity funds to obtain upfront approvals for up to a year for

investments in Africa

Exchange Control Modernisation • National Treasury to release a discussion document on modernisation of

exchange control legislation and approach towards inward and outward investments

19

Social security and health care financing

• The child support grant will be gradually extended to recipients’ 18th birthday while eligibility for the state old age pension will fall to 60 for men, the same age as for women

• Almost 14 million people now receive grants. Expenditure on grants is expected to be R85 billion this year; this equates to 3.5% of GDP

• The Unemployment Insurance Fund coped well with a sharp rise in the number of claimants

• Cabinet has approved the proposed transformation of the RAF into a no-fault road accident benefit scheme to improve the quality of benefits and reduce the leakage of funds to lawyers, minor claims and lengthy disputes

• The inter-Ministerial committee continues to work on social security reform, retirement industry reform, and proposals for National Health Insurance

20

Government spending and saving

• Spending growth moderates from 17.2%between 2006/07-2009/10 to 8.2% between 2009/10-2010/13

• Fiscal framework makes R86.7 billion available over MTEF plus savings of R25.6 billion that are added for reallocation to priorities = R112.2 billion

• Increased savings due to: – Decrease in spending on non-core goods and services, rescheduled

expenditure, lower overseas payments, reduced transfers to certain public entities, improved financial management, reduced expenditure on administration

• Major savings amounts are:– Defence and Military Veterans, R4.5 billion (A400M military aircraft contract

cancelled)– Correctional Services, R4.5 billion (rescheduled prison building plans)– Transport, R3.4 billion (including deferred public transport infrastructure

projects where planning and design have been delayed)– International Relations and Cooperation, R1.5 billion (revised foreign costs

and deferred construction of the Pan African Parliament building)– Social Development, R1.2 billion (rationalised social grant payments system)

21

Service delivery and outcomes

• Government is shifting to target outcomes in order to increase efficiency and improve performance to support inclusive development

• The focus on departmental outputs and activities has not resulted in the required step-change in service delivery

• 5 priorities in 2009 MTSF are unpacked into 12 measurable outcomes

• Over the next three years, expenditure is channeled towards 5 + 2 priority areas:

– Improving the quality of education– Upgrading health care– Promoting public safety– Supporting rural development– Creating decent jobs

– Building sustainable human settlements – Encouraging efficient local government

22

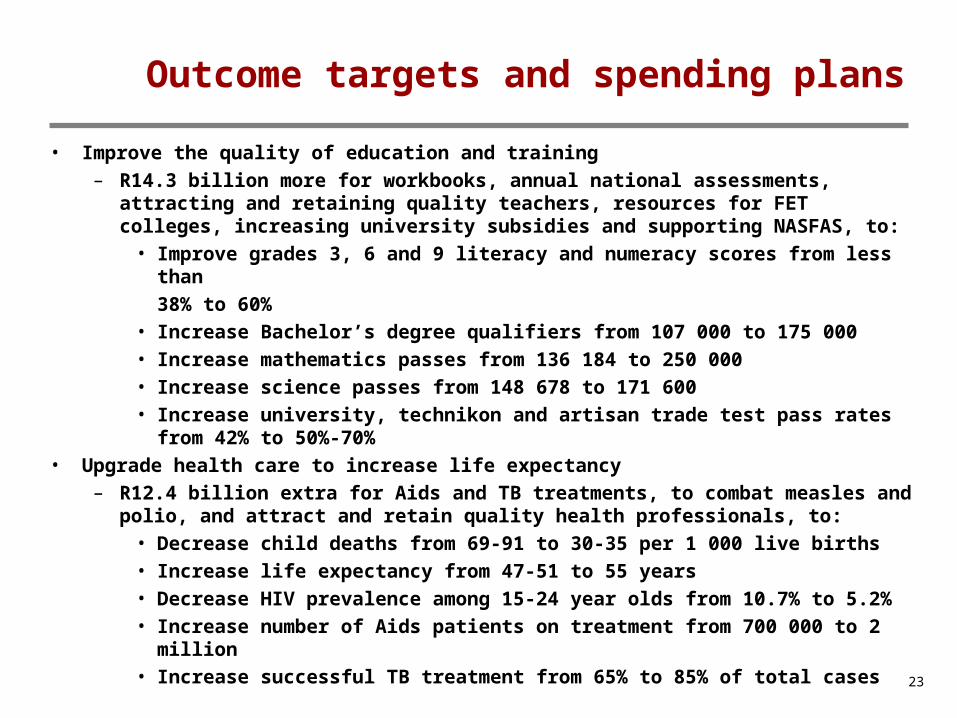

Outcome targets and spending plans

• Improve the quality of education and training– R14.3 billion more for workbooks, annual national assessments, attracting

and retaining quality teachers, resources for FET colleges, increasing university subsidies and supporting NASFAS, to:

• Improve grades 3, 6 and 9 literacy and numeracy scores from less than

38% to 60%• Increase Bachelor’s degree qualifiers from 107 000 to 175 000• Increase mathematics passes from 136 184 to 250 000• Increase science passes from 148 678 to 171 600• Increase university, technikon and artisan trade test pass rates from 42%

to 50%-70%• Upgrade health care to increase life expectancy

– R12.4 billion extra for Aids and TB treatments, to combat measles and polio, and attract and retain quality health professionals, to:

• Decrease child deaths from 69-91 to 30-35 per 1 000 live births• Increase life expectancy from 47-51 to 55 years• Decrease HIV prevalence among 15-24 year olds from 10.7% to 5.2%• Increase number of Aids patients on treatment from 700 000 to 2 million• Increase successful TB treatment from 65% to 85% of total cases 23

Outcome targets and spending plans

• Build a safe country– R1 billion more to fight organised crime, appoint more public defenders,

family advocates, family counsellors, sexual offences court officers, court clerks and to recruit additional personnel in detective services, crime intelligence and visible policing, to:

Increase contact crime detection rate from 52.5% to 57.5% Increase trio crime detection rate from 13.8% to 34% Decrease court case backlogs from 37 459 to 22 100 cases Increase the percentage of contact/trio crimes reported by victims/the

public from 48.9% to 60% Raise Corruption Perception Index Ranking from 160 to within the top 40

countries• Develop equitable and sustainable rural communities

– R2.4 billion extra for comprehensive rural development programme and the Land Bank, to:

Increase number of commercial farm holders from 780 000 to 800 000 Increase percentage of small farmers producing for sale from 4.1% to

10%

24

Outcome targets and spending plans

• Build a more inclusive economy, create jobs and develop network infrastructure – R10.8 billion extra for the second phase of EPWP, National Roads Agency

(coal haulage road network) and construction of fuel pipeline, to: Increase labour absorption rate from 43 to 45% Increase GDP per capita from R46 907 to R57 618 Achieve GDP growth average of 5% (2010-2014) Decrease level of income inequality, lowering Gini coefficient from 0.66 to

0.59 Increase the share of national income going to the poorest 40% of the

population• Ensure sustainable human settlements

– R1 billion more to integrated housing and human settlements development grant, to:

Decrease number of households with inadequate shelter from 1.1 million to 600 000

Increase number of new affordable rental units from 5 000 to 20 000 a year

Increase number of households with access to basic sanitation from 69 to 100%

– R1.2 billion on rural on-site water and sanitation

25

Conclusion

• Summary of the 5 key messages of the budget

• Raise economic growth and employment, and reduce poverty

• Proposals to raise employment, with a focus on the youth

• Reducing the budget deficit to more sustainable levels

• No tax increase in the tax burden

• Improving the quality of government spending

26