42

2010 Interim Results July 2010

2010 Interim ResultsJuly 2010

Agenda

Business review and outlook

Financial results

Q&A

Highlights

Revenues up 33% to £46.2m (2009: £34.6m)

Signals/Illumination Revenue up by 23% to £26.1m :

Obstruction products up 60% to £4.9m

Lighting products up 60% to £4.0m

Operating profit £5.3m (2009:£0.6m)

Underlying EPS 10.8p (2009:1.0p)

Interim Dividend 2.8pence (2009: 2.3pence)

Half year Revenues

2010 2009

Total Revenue £46.2m £34.6m

Signals/Illumination £26.1m £21.2m

Electromagnetic Components £7.5m £5.4m

Indication Components £12.5m £8.0m

Contribution Margins

2010 2009

Signals/Illumination 42.0% 35.5%

Electromagnetic Components 18.3% 24.9%

Indication Components 54.6% 49.2%

Indication Components

Revenues up over 50% versus 2009

Inventory replenishment in H1

Some softness anticipated in H2

Shortages in the general electronics component market starting

to affect customer schedules

Fundamentals of the business unchanged

Margins solid

Demand driven by Servers, Storage, Cellular Infrastructure and

Networking/Internet

Electromagnetic Components

Revenues up £2.1m (40%) versus 2009

200 amp Disconnect still showing growth

Traditional business continues recovery

Prospects for Disconnect still promising but on thin margins

Smart Metering starting to proliferate throughout the world

Major new customer in US market

Signals/Illumination

2010 2009

Revenue: £25.6m £21.2m

Traffic £12.8m £11.2m

Obstruction £4.9m £3.0m

Transportation £4.4m £4.5m

Lighting £4.0m £2.5m

Signals - Traffic

US traffic continues steady with little big contract activity

Strong European performance

UK market performs well

Margins improved

Market showing some nervousness for second half

€750m potential market

More than 15million lights still to replace

50W halogen lamps (1yr life)

vs.

8W Dialight LED lamps (5yr life)

European growth opportunity

Signals - Obstruction

Continued strong growth

Wind Turbine Market in US quite soft

White Strobe showing outstanding growth

H1 shipments almost equal to full year 2009

New “single level” strobe shipping

Previously announced contracts shipping in volume

BTI acquisition on plan

• White LED Strobe replaces over 80,000 conventional strobes in the US alone

• Potential 10 year lamp life

• Over 95% still to be converted

• Wind turbines forecasted to produce up to 35% of Europe’s electricity by 2030

Potential market over $250m

for strobes alone

Dialight LED

Dual Beacon

Xenon Strobe

Telecom • Broadcast • Wind Turbines • Tall Structures

Obstruction Lighting growth potential

Illumination

Revenues up 60%

Industrial White Lighting sales in H1 2010 almost as twice those

in full year 2009

Safesite High Bay continues early success in multiple

applications

Strong paybacks with Dialight LED Lights

Multiple customers

Pipeline of new products

White Light Strategy

Type Efficiency

lm/W

Life -hours

x1000

Cost Per

lumen $

Colour

Rendering Ra

High Pressure

Sodium

60 -120 10 - 20 0.0004 30

Ceramic Metal

Halide

60 -100 6 -12 0.0010 70 - 95

Fluorescent 40 -100 6 - 45 0.0005 60 - 90

Halogen & Tungsten 8 -22 2 - 10 0.0002 100

Cool white LED

6000k

90 -130 50 0.015 70

Warm white LED

3000k

20 - 50 50 0.04 75 -90

How do LEDs compare to the competition?

LED Technology Roadmap

Why LEDs?

• Long Life

• High Efficiency

• Shock & Vibration

• Extreme Climates

• Zero Maintenance

• Precise Optical Control

• Instant Light

• Switching Cycles

• Improved Visibility

=Superior Cost

of

Ownership

2010 Global Projection: $75 billion

Residential

23% Industrial

7%

Outdoor

17%Commercial

21%

Portable

18%

Parts &

Accessories

14%

Source: Freedonia

Lighting Market Segments

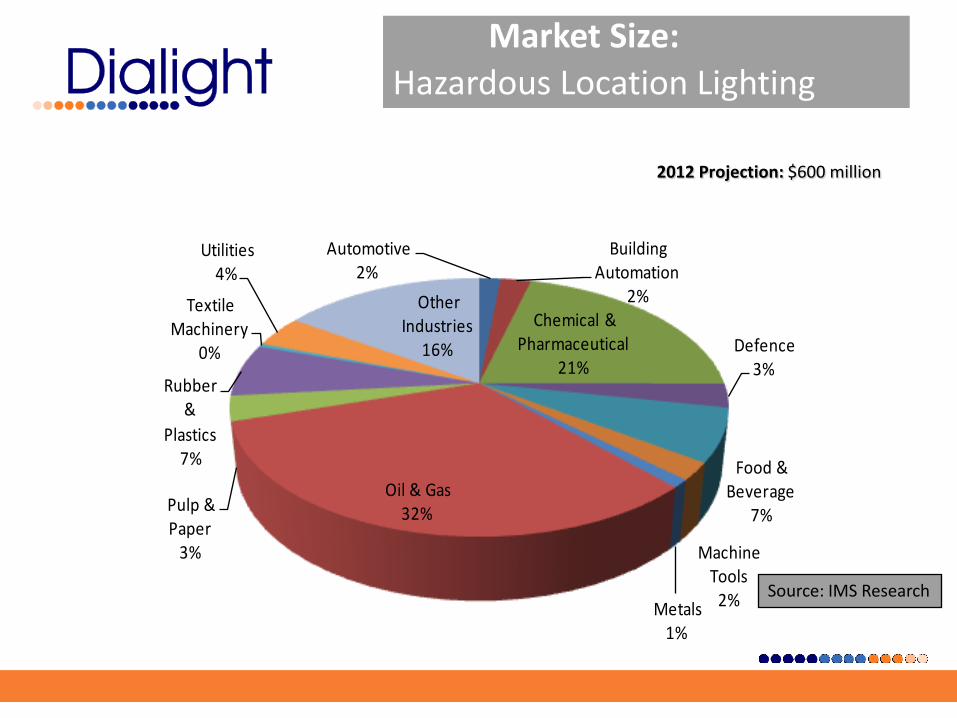

Automotive 2%

Building Automation

2%Chemical &

Pharmaceutical 21%

Defence 3%

Food & Beverage

7%

Machine Tools

2%Metals 1%

Oil & Gas 32%Pulp &

Paper 3%

Rubber &

Plastics 7%

Textile Machinery

0%

Utilities 4%

Other Industries

16%

Source: IMS Research

Market Size:

Hazardous Location Lighting

2012 Projection: $600 million

Dialight LED Lighting

Product Portfolio

HZC / STW Area LightPower Consumption: 100WReplaces: 250W HIDEnergy Savings: 40%Typical Payback: 2-4 years

Wallpack / BulkheadPower Consumption: 22WReplaces: 70W HIDEnergy Savings: 70%Typical Payback: 2-4 years

RTO Area LightPower Consumption: 9WReplaces: 65W IncanEnergy Savings: 75 – 85%Typical Payback: 1-3 years

FRT Linear FixturePower Consumption: 30WReplaces: 35W FluorEnergy Savings: 25%Typical Payback: 4-6 years

Linear FixturePower Consumption: 100WReplaces: 200W FluorEnergy Savings: 50%Typical Payback: < 2 years

High BayPower Consumption: 150WReplaces: 400W HIDEnergy Savings: 65%Typical Payback: 1-3 years

LPK Linear FixturePower Consumption: 72WReplaces: 100W FluorEnergy Savings: 30%Typical Payback: 3-5 years

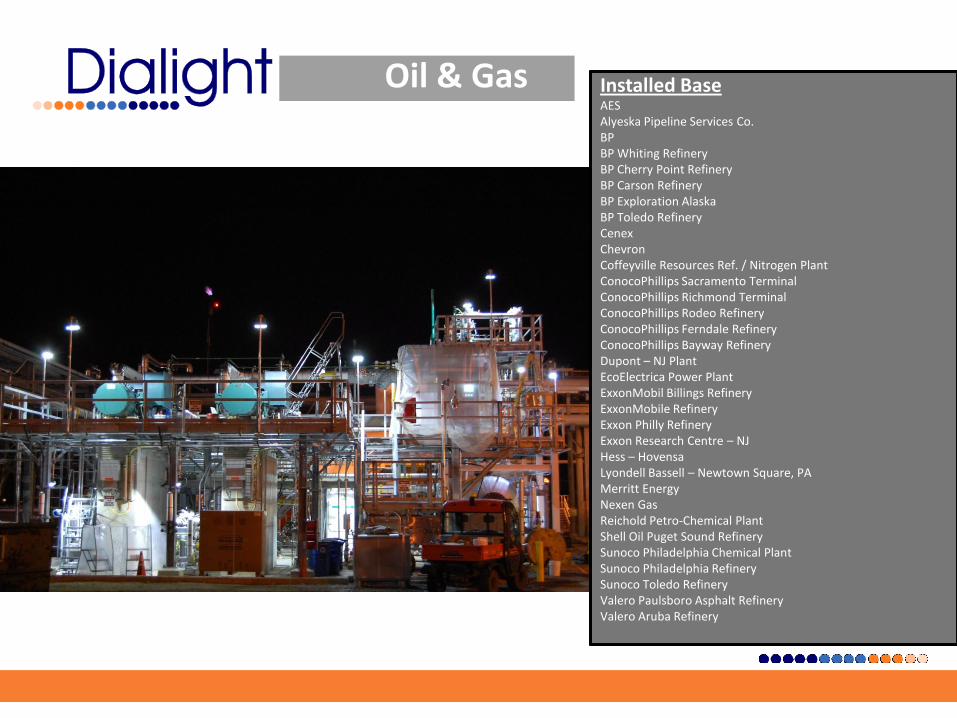

Installed BaseArkema ChemicalsDegussa Engineered CarbDow ChemicalDow CorningFMC AlcoyFormosa PlasticGreat Salk Lake MineralsIndolex Chemical Co.ISP ChemicalsLubrizol PainsevilleLyondell Bassell Oxbow Carbon & MineralsOxy ChemicalRain CII Carbon LLCRed Cedar GatheringReichhold ChemicalsRohm HaasSaint Gobain PlasticsSartomerSasol North AmericaSolvay ChemicalsSun ProductsTamecoThatcher Chemical

Chemical & Petrochemical

Oil & Gas Installed BaseAESAlyeska Pipeline Services Co.BPBP Whiting RefineryBP Cherry Point RefineryBP Carson RefineryBP Exploration AlaskaBP Toledo RefineryCenexChevronCoffeyville Resources Ref. / Nitrogen PlantConocoPhillips Sacramento TerminalConocoPhillips Richmond TerminalConocoPhillips Rodeo RefineryConocoPhillips Ferndale RefineryConocoPhillips Bayway RefineryDupont – NJ PlantEcoElectrica Power PlantExxonMobil Billings RefineryExxonMobile RefineryExxon Philly RefineryExxon Research Centre – NJHess – HovensaLyondell Bassell – Newtown Square, PAMerritt EnergyNexen GasReichold Petro-Chemical PlantShell Oil Puget Sound RefinerySunoco Philadelphia Chemical PlantSunoco Philadelphia RefinerySunoco Toledo RefineryValero Paulsboro Asphalt RefineryValero Aruba Refinery

Water, Sewage & Wastewater Treatment

Installed BaseCity of Philadelphia, Water Dept

City of Reno, NV

Dip Abitibi Bowater

Excel Energy

Henkel

Idaho Power

LA Water & Power

Passaic Valley Sewage

Offshore Technology

Installed BaseBP

Pioneer Drilling Co.

Pride International

Rain CII Carbon LLC

Sasol North America

Pharmaceuticals

Installed BaseBaxter

Baxter Caribe Inc.

Merck & Co. – VA plant

Proctor & Gamble

Pfyzer Puerto Rico

Mining ApplicationsInstalled BaseAntelope Coal Mine

Arch Black Thunder Coal Mine

Climax Molybdenum Henderson Mine

Coal Peers

Henderson Mine

Jacobs Ranch Mine

Kiewit Buckskin Mining

Mississippi Phosphates Corp.

Mountain Coal West Elk Mine

Oxbow Carbon and Minerals

Peabody Twenty Mile Mine

Peabody Caballo Coal Mine

PCS Phosphate

Pilbara Iron

Red Path Mining

Rio Tinto Antelope Mine

Rio Tinto Cordero Rojo Mine

Rio Tinto Kennecott Copper Mine

Rio Tinto Kayenta Mine

Teck-Cominko Pogo Mine

Unico Mining

Western Energy Rose Bud Mine

Westmore Coal - Abasaloka Mine

Power Generation & Utilities

Installed BaseAnderson Merrit Energy

Chamming Electric Montana Power (PPL) Colstrip Power Plant

Chesapeake Energy PNM NM

Coalstrip – PA Light Public Service New Mexico

Colorado Springs Utilities Portland General Electric

Connectiz Rocky Mountain Power Hunter Station

Coteau Rocky Mountain Power Huntingdon Plant

Covanta Energy – DE Plant Rohr

DTE Energy Rytway

Energy Nuclear – River Bend Station Sebago

Enogex Spectra Energy

Envirolight Snowey Hydro

Eraring Energy Southwest Generation

Farmington, NM Tucson Electric Power

Great River Energy Wiliams Energy Gas Plant

Idaho Power Corporation Wisconsin Power & Light

IES Utilities, Inc OGS Xcel Energy

Kaneka Eperan

Kapar Energy

Line Power

Midwest Generation

Warehouse ApplicationsInstalled Base3E - Electrical Eng & Equipment Co. Noctur

Anderson Rittenhouse Electric

Archer Daniels Midland Corp. Rockline Industries

Aisin – Japan SEPTA

Automation & Electronics Steffen Inc.

The Baltimore Sun TECOT Dover Branch Transfers

Buckman Labs Timken David SIPE

City of Toronto Vektra Electric

Concord Phillips Wichita

Conectiv Edgemoor

DOT Warehouse

DTE Energy-St. Clair PP

Eco Lighting Services & Tech

FedEx

Galavan Industries

Glenadale Complex

Henrico County

Huntsmann

I/O Solutions & Controls

Jesco

John Deere

KEW Incorporated C/O Gerrie

Klockner Pentaplast

Lafarge

Medsafe Warehouse

Meng Xue Song

Mozel Inc.

Noctur

Manufacturing Applications

And Processing Plants

Installed BaseADM Corn ProcessingAlcoa PPG

Allsteel Panel Proctor & Gamble

Anderson Auto Rockline Industries

Arbiti Bowater Sherman Alumina

Bar-S Foods SSAB Steel Alabama Inc.

Cargill Swann

Davisco Int’l Temple Island

DMI Industries Tyson Foods

Flexicon Inc Van Meter Industrial

Frontline Int.

Galvin

General Machinery

Graphic Packaging Int’l

GS Dunn

Hatfield Quality Meats

Heinz

Holcium USA

Huntingdon Alloys

Industrial Automation Controls

John Deere

Kapstone Kraft Paper Co

Kellogg’s

Metal Container

Michigan Sugar

Nestle-Stouffee Frozen Foods

Noranda Alumina

Pilkington North America

Potato Factory

Case Study:

Baxter Pharmaceuticals

Project Overview

(50) 250W HID vs. (40) 100W LED

$6,000 (34,000 kWh) Energy Savings / yr

$35,000 Lifetime Maintenance Savings

30 tons CO2 Reduced

Payback = 23 Months

Case Study:

Rockline Industries

Project Overview

(140) 400W Metal Halide vs. (140) 150W LED

$16,000 (144,000 kWh) Energy Savings / yr

$77,500 Lifetime Maintenance Savings

124 tons of CO2 Reduced

Rebate Incentive: $48,000 ($342 per fixture)

Payback: < 9 Months (with rebate)

Case Study:

Frontline International

Project Overview

(59) 400W HID vs. (59) 150W LED

$18,000 (123,486 kWh) Energy Savings / yr

$30,000 Lifetime Maintenance Savings

106 tons of CO2 Reduced

Payback = 13 Months

Case Study:

G.S. Dunn

Project Overview

(18) 450W HID vs. (18) 150W LED

$3,000 (22,000 kWh) Energy Savings / yr

$8,000 Lifetime Maintenance Savings

25 Tons of CO2 Reduced

Payback = 2 years

Outlook

Group shows continued excellent prospects for Revenue Growth and Profitability

Signals/Illumination demonstrating strong growth and margins

Improved LED efficiency and cost is moving the adoption point

Pipeline of new and improved White Lighting products

Reengineering and cost reduction programmes continue to drive profits in Signals/Illumination

LED Indication anticipated H2 softness but still a strong profit and cash generator for the full year

Prospects for Disconnect improved with the addition of a new US customer, albeit on thin margins

George RalphFinance Director

Summary Profit & Loss Account

2010 £M 2009 £M

Revenue 46.2 34.6

Gross Profit 12.6 7.0

Gross Profit % 27.3 20.2

Overhead costs (7.3) (6.4)

Operating profit 5.3 0.6

Net financing cost (0.1) (0.1)

Profit before tax 5.2 0.5

Tax (1.8) (0.2)

Profit from cont. ops 3.4 0.3

Exceptional profit - 2.0

Retained profit 3.4 2.3

Taxation

Effective tax rate in 2010 forecast at 36.0%

Effective tax rate in FY 2009 was 37.7%

Issues being addressed

Profits in high tax locations

Historic unrelievable UK losses

Dividends and Earnings Per Share

2010 2009

Interim dividend per share 2.8p 2.3p

Basic EPS 10.8p 7.3p

Dividend cover 3.9 times 3.2 times

Adjusted EPS 10.8p 1.0p

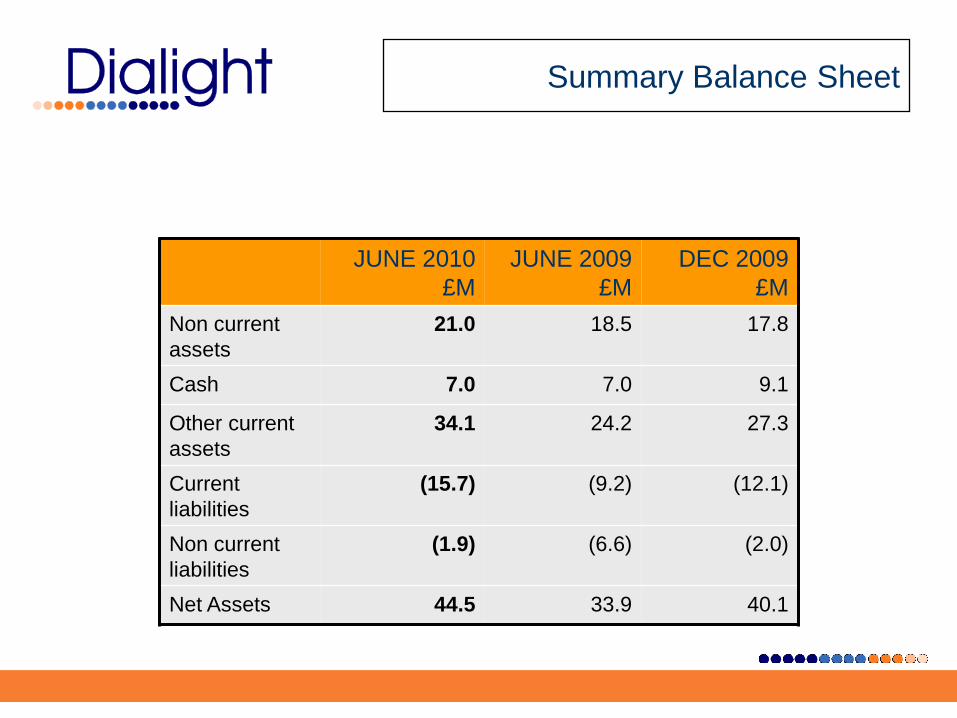

Summary Balance Sheet

JUNE 2010

£M

JUNE 2009

£M

DEC 2009

£M

Non current

assets

21.0 18.5 17.8

Cash 7.0 7.0 9.1

Other current

assets

34.1 24.2 27.3

Current

liabilities

(15.7) (9.2) (12.1)

Non current

liabilities

(1.9) (6.6) (2.0)

Net Assets 44.5 33.9 40.1

Summarised Cash flow

2010£M 2009£M

Operating cash 6.7 2.1

Working capital (2.5) 3.7

Cash from operations 4.2 5.8

Tax/financing (1.6) (0.4)

Investing activities (3.7) (0.9)

Financing activities (1.4) (1.2)

Change in net cash (2.5) 3.3

Working capital / Cash flow

Working capital requirements increased due to growth in

business.

Inventory – strategic purchasing to protect growth

Small improvement in receivables days outstanding compared

with year end.

Improvement in payables days outstanding compared with year

end

Cash - Continuing strong operating cash flow. Debt free balance

sheet

Outlook

Group shows continued excellent prospects for Revenue Growth and Profitability

Signals/Illumination demonstrating strong growth and margins

Improved LED efficiency and cost is moving the adoption point

Pipeline of new and improved White Lighting products

Reengineering and cost reduction programmes continue to drive profits in Signals/Illumination

LED Indication anticipated H2 softness but still a strong profit and cash generator for the full year

Prospects for Disconnect improved with the addition of a new US customer, albeit on thin margins