26

2012 SPECIAL REPORT: LUXURY AUTOMOTIVE OUTLOOK FEATURING THE FORBES INSIGHTS LUXURY CAR BUZZ INDEX

2012 Special report: Luxury Automotive outLookFeAturing the Forbes insights Luxury CAr buzz index

ContentsIntroduction ............................................................................................................... 2

A Focus Group With Wine .................................................................................. 3

Boosting Brands in a Sluggish Economy .......................................................4

The Regional Reality ..............................................................................................4

The Forbes Insights Luxury Car Buzz Index ................................................. 6

So What’s in a Name? ......................................................................................... 10

The BIG Picture .......................................................................................................12

Democratizing Luxury. ........................................................................................ 14

The Truth About Affluence ................................................................................16

What’s Next for American Luxury?. ................................................................ 17

Even More of an Underdog ................................................................................19

A View From the Top. ...........................................................................................21

The New Contender .............................................................................................22

Conclusion ...............................................................................................................23

Appendix: Luxury Car Buzz Index Methodology .....................................24

2 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

introduCtionThree years after a market cataclysm vaporized real estate and stock values, luxury automakers are still grappling

with the consequences. In 2008, wealth plummeted $11.2 trillion compared with the year before—the biggest annual

decline in household net worth since the Federal Reserve began keeping quarterly records in 1952.

With less wealth to go around, the def-inition of luxury is changing, and by extension, so must the companies that sell high-end cars. The go-go days of surpassing the Joneses are gone. These are sober times. And yet Baby Boomers, who are nearing or transitioning to retirement, still crave the trappings of wealth. Meanwhile, so do their chil-

dren. Generation Y was raised in heady times, when Viking ovens, Sub-Zero refrigerators and 50-inch flat screens were the norm. Bigger was better. More wasn’t enough. They grew up ensconced in a premium lifestyle and now expect that for themselves. Yet they’re broke: Unemployment among Generation Y is more than 13% by some estimates.

Thus, the story of how luxury car companies are rein-venting themselves in the wake of this great recession has become a tale of two generations—wooing the Boomers and priming Gen Y’ers for future purchases. That’s why blue-blood brands like Mercedes-Benz are seeking a more youthful image and formerly conservative Lexus is jazz-ing up its cars like never before. Doing so appeals not only to Gen Y’ers, but also to Boomers, who are young at heart and would rather globetrot than retire to gated communi-ties and games of shuffleboard.

Audi, meanwhile, the up-and-coming alternative lux-ury brand, has shored up so much clout over the past five years that the average transaction price for one of its vehi-cles has jumped $5,000. The underdog is overachieving.

In fact, in the midst of economic uncertainty and a painfully slow recovery, the auto industry has been bounc-ing back from the depths of 2009, and the thirst for luxury remains powerful. In 2011, Audi and Mercedes posted their highest sales ever. BMW had such a strong year that it knocked Lexus off the top spot to become the best-selling luxury brand in the U.S.

What all of this shows is how topsy-turvy things are right now.

The Forbes Insights Luxury Automotive Outlook Special Report takes an inside look at the struggles and triumphs of luxury automakers through the eyes of chief

marketers and general managers. Their commentary sketches out a roadmap for where brands are headed, while data from BIGinsight, a consumer insight resource based in Worthington, Ohio, paints a detailed picture of how consumers regard them right now, as well as what those consumers intend to do—and buy—over the next six months. Together, the two give unparalleled insight into a market overcoming turmoil.

Using data from BIGinsight, Forbes Insights has devised a Luxury Car Buzz Index to rank the leading lux-ury automotive brands based on a composite score that measures customer satisfaction and loyalty, car owners’ propensity to recommend their brand to others, and the effectiveness of marketing efforts in both traditional and digital media, as well as the impact of digital word-of-mouth through social media and blogs. The Buzz Index distills all these factors into a snapshot of luxury brand performance. (See Figure 2, page 6, for the full ranking and Appendix, page 24, for the complete methodology.)

The Luxury Car Buzz Index distills a

snapshot of luxury brand performance.

CoPyRIGhT © 2012 ForbeS inSightS | 3

A FoCus group With WineOne of Beth Tyler’s most memorable experiences involv-ing Lexus has more to do with spiced lamb than her beloved LS 460.

The Japanese luxury automaker recently selected Tyler to host a dinner at her Annapolis, Md., home. Professional chef Todd Gray, who owns Equinox restaurant in Washington, D.C., spent hours in her kitchen cook-ing a six-course meal for the gathering of 12.

“The food was out-of-this-world fabulous. One of the courses was chestnuts. I never had a chestnut in my life,” says Tyler, a real estate agent at Long & Foster in Annapolis.

Mark Templin, group vice president and general manager of Lexus, joined Tyler, her husband, and eight of their friends for the din-ner. Nancy Hubbell, Lexus prest ige communicat ions manager, also attended, tweeting the dinner conversation as it unfolded to more than 250,000 Twitter followers.

It was the sixth event of its kind for Lexus in a little over a year, all held in key luxury-car markets—Beverly Hills, Chicago, Miami, San Francisco, among others. “It’s a focus group, but it’s a focus group with wine,” Templin says.

The dinners aren’t about selling cars or pitching the brand. They’re a chance for Templin to get inside the heads of car buyers and learn things like the fact that several people at the dinner, including Tyler’s husband, think that signing the paperwork for a new car shouldn’t

take more than 15 minutes. “No one wants to sit at the dealership for hours and get up-sold,” Tyler says.

Interesting opinions often come to light at the dinner table. “The best comment we’ve had yet was from a woman who bought a Land Rover,” Templin says. “She said, ‘It’s like a bad boyfriend: He treats you terribly, but he looks so good,’” referring to the SUV’s notorious reputa-tion for being unreliable.

The fact that Templin, a top Lexus executive, is tak-ing time to dine with random luxury-car buyers is remark-able on many levels. But what

it perhaps shows most clearly is how car companies are taking drastic measures to change their image and the way they conduct business.

The dinners aren’t about selling cars or pitching the brand. They’re a chance

to get inside the heads of car buyers.

4 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

the regionAL reALity

When it comes to luxury car sales, there’s no such thing as Anytown, U.S.A. Consumer data from BIGinsight reveals significant regional differences in the popularity of some luxury car brands. Figure 1 illustrates this with a few select-ed brands and markets, summing up the first and second choices being considered by consumers who plan to buy a vehicle in the next six months. (The table uses June and December data averaged together, both to eliminate any seasonal effects and to maximize the sample size.)

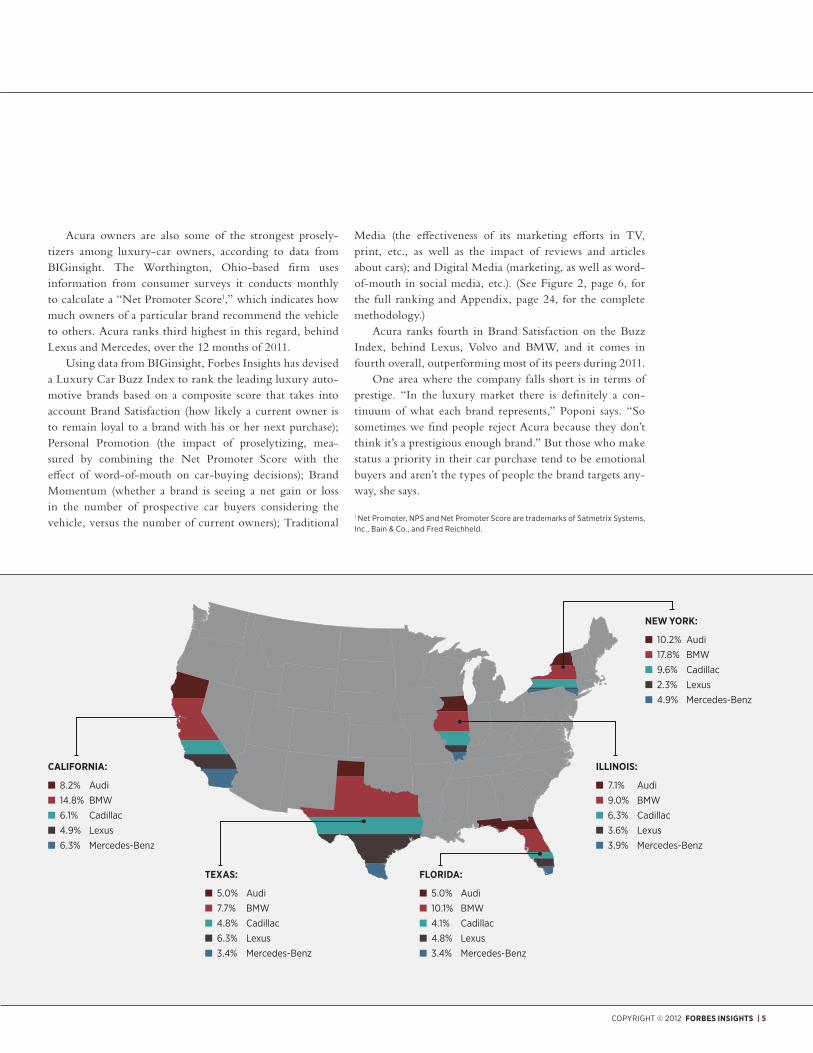

Audi, for instance, is more than twice as popular in New york as in Texas or Florida. Cadillac is more than twice as popular in New york as in Florida. BMW is roughly twice as popular in New york and California as in Texas, and Lexus is almost three times more popular in Texas than in New york. Mercedes is almost twice as popular in California as in Florida or Texas.

Figure 1: Planning to Buy/Lease: What make of vehicle are you considering? First choice plus second choice:

United StateS:

n 5.6% Audi

n 10.2% BMW

n 5.5% Cadillac

n 4.0% Lexus

n 3.6% Mercedes-Benz

Source: BIGinsight Media Behaviors & Influence™ (MBI™) Survey, June and December 2011

boosting brAnds in A sLuggish eConomy

Luxury isn’t what it used to be. People no longer flaunt wealth the way they did before the market crash of 2008, says Vicki Poponi, assistant vice president of product planning for Honda and Acura. Many simply can’t afford to any longer. But even those who can are refraining, out of respect for the many whose lives are in turmoil.

“We were wondering whether it was going to be a permanent change or not,” she says. “At Acura, we believe it is. We

believe there’s a significant value shift in the luxury buyer.”The reason is simple: People are happier, according

to a 2009 wealth study by the Harrison Group. It tracked people’s attitudes after the market crash of 2008 and found that, even though times were harder and money was tighter, many were actually more content with their lives.

“Basically, the happiness quotient went up huge,”

Poponi says. “It’s completely paradoxical: Everybody thinks they have less money, they’re spending less money, but all of a sudden they’re happier. Our hypothesis is, everybody got off this rat race of chasing the Joneses. It just made people happier—you didn’t have the stress of look-ing at what somebody else had and you didn’t.”

The shift in sentiment plays to Acura’s strengths. The company embodies “smart luxury,” Poponi says, offering a good value relative to more expensive European luxury cars, and reliability that saves hassle by avoiding repairs. “People need time given back to them. It’s really sort of like the last luxury,” she says.

Acura buyers are more rational than emotional when it comes to their car purchases. They have a longer list of requirements than those who buy other brands, and they are looking to get the most value for their money, Poponi says. “They’re not cheap. They’re smart, savvy, maybe a little smug, looking around at all the research, seeing that they’re the most informed in their product choices.”

“People need time given back to them. It’s really

the last luxury.”

—Vicki poponi Assistant Vice President of

Product Planning for Honda and Acura uSA

CoPyRIGhT © 2012 ForbeS inSightS | 5

illinoiS:

n 7.1% Audi

n 9.0% BMW

n 6.3% Cadillac

n 3.6% Lexus

n 3.9% Mercedes-Benz

caliFornia:

n 8.2% Audi

n 14.8% BMW

n 6.1% Cadillac

n 4.9% Lexus

n 6.3% Mercedes-Benz

texaS:

n 5.0% Audi

n 7.7% BMW

n 4.8% Cadillac

n 6.3% Lexus

n 3.4% Mercedes-Benz

new York:

n 10.2% Audi

n 17.8% BMW

n 9.6% Cadillac

n 2.3% Lexus

n 4.9% Mercedes-Benz

Florida:

n 5.0% Audi

n 10.1% BMW

n 4.1% Cadillac

n 4.8% Lexus

n 3.4% Mercedes-Benz

Acura owners are also some of the strongest prosely-tizers among luxury-car owners, according to data from BIGinsight. The Worthington, Ohio-based firm uses information from consumer surveys it conducts monthly to calculate a “Net Promoter Score1,” which indicates how much owners of a particular brand recommend the vehicle to others. Acura ranks third highest in this regard, behind Lexus and Mercedes, over the 12 months of 2011.

Using data from BIGinsight, Forbes Insights has devised a Luxury Car Buzz Index to rank the leading luxury auto-motive brands based on a composite score that takes into account Brand Satisfaction (how likely a current owner is to remain loyal to a brand with his or her next purchase); Personal Promotion (the impact of proselytizing, mea-sured by combining the Net Promoter Score with the effect of word-of-mouth on car-buying decisions); Brand Momentum (whether a brand is seeing a net gain or loss in the number of prospective car buyers considering the vehicle, versus the number of current owners); Traditional

Media (the effectiveness of its marketing efforts in TV, print, etc., as well as the impact of reviews and articles about cars); and Digital Media (marketing, as well as word-of-mouth in social media, etc.). (See Figure 2, page 6, for the full ranking and Appendix, page 24, for the complete methodology.)

Acura ranks fourth in Brand Satisfaction on the Buzz Index, behind Lexus, Volvo and BMW, and it comes in fourth overall, outperforming most of its peers during 2011.

One area where the company falls short is in terms of prestige. “In the luxury market there is definitely a con-tinuum of what each brand represents,” Poponi says. “So sometimes we find people reject Acura because they don’t think it’s a prestigious enough brand.” But those who make status a priority in their car purchase tend to be emotional buyers and aren’t the types of people the brand targets any-way, she says.

1 Net Promoter, NPS and Net Promoter Score are trademarks of Satmetrix Systems, Inc., Bain & Co., and Fred Reichheld.

6 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

Forbes insights

Luxury CAr buzz indexThe Forbes Insights Luxury Car Buzz Index uses exclusive, forward-

looking data on consumer intentions provided by BIGinsight to assess

the industry’s prospects for the next six months, with a special focus

on the luxury car segment. The data used to calculate the Index derives

from two extensive consumer surveys conducted on a regular basis.

BIGinsight’s monthly Consumer Survey, which has a 10-year history,

includes a total monthly sample of more than 8,000 respondents and

produces a uniquely powerful database, more highly predictive of

consumers’ actions than backward-looking data on past sales. The

Media Behaviors & Influence™ Study polls some 25,000-plus respon-

dents and is conducted twice a year, in June and December.

CoPyRIGhT © 2012 ForbeS inSightS | 7

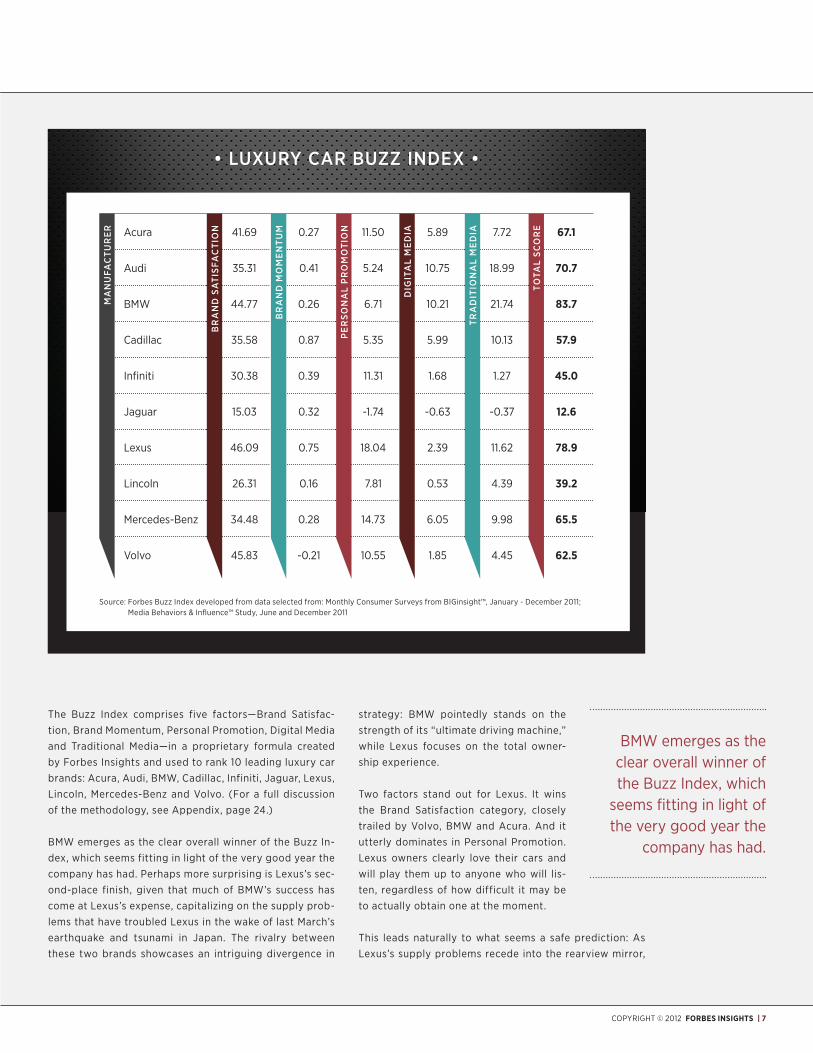

The Buzz Index comprises five factors—Brand Satisfac-tion, Brand Momentum, Personal Promotion, Digital Media and Traditional Media—in a proprietary formula created by Forbes Insights and used to rank 10 leading luxury car brands: Acura, Audi, BMW, Cadillac, Infiniti, Jaguar, Lexus, Lincoln, Mercedes-Benz and Volvo. (For a full discussion of the methodology, see Appendix, page 24.)

BMW emerges as the clear overall winner of the Buzz In-dex, which seems fitting in light of the very good year the company has had. Perhaps more surprising is Lexus’s sec-ond-place finish, given that much of BMW’s success has come at Lexus’s expense, capitalizing on the supply prob-lems that have troubled Lexus in the wake of last March’s earthquake and tsunami in Japan. The rivalry between these two brands showcases an intriguing divergence in

strategy: BMW pointedly stands on the strength of its “ultimate driving machine,” while Lexus focuses on the total owner-ship experience.

Two factors stand out for Lexus. It wins the Brand Satisfaction category, closely trailed by Volvo, BMW and Acura. And it utterly dominates in Personal Promotion. Lexus owners clearly love their cars and will play them up to anyone who will lis-ten, regardless of how difficult it may be to actually obtain one at the moment.

This leads naturally to what seems a safe prediction: As Lexus’s supply problems recede into the rearview mirror,

• Luxury Car Buzz Index •

Acura 41.69 0.27 11.50 5.89 7.72 67.1

Audi 35.31 0.41 5.24 10.75 18.99 70.7

BMW 44.77 0.26 6.71 10.21 21.74 83.7

Cadillac 35.58 0.87 5.35 5.99 10.13 57.9

Infiniti 30.38 0.39 11.31 1.68 1.27 45.0

Jaguar 15.03 0.32 -1.74 -0.63 -0.37 12.6

Lexus 46.09 0.75 18.04 2.39 11.62 78.9

Lincoln 26.31 0.16 7.81 0.53 4.39 39.2

Mercedes-Benz 34.48 0.28 14.73 6.05 9.98 65.5

Volvo 45.83 -0.21 10.55 1.85 4.45 62.5

Source: Forbes Buzz Index developed from data selected from: Monthly Consumer Surveys from BIGinsight™, January - December 2011; Media Behaviors & Influence™ Study, June and December 2011

Ma

nu

faC

tu

re

r

Br

an

d S

atI

Sfa

CtI

on

Br

an

d M

oM

en

tu

M

Pe

rSo

na

L P

ro

Mo

tIo

n

dIg

Ita

L M

ed

Ia

tra

dIt

Ion

aL

Me

dIa

tota

L SC

or

e

BMW emerges as the clear overall winner of the Buzz Index, which

seems fitting in light of the very good year the

company has had.

8 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

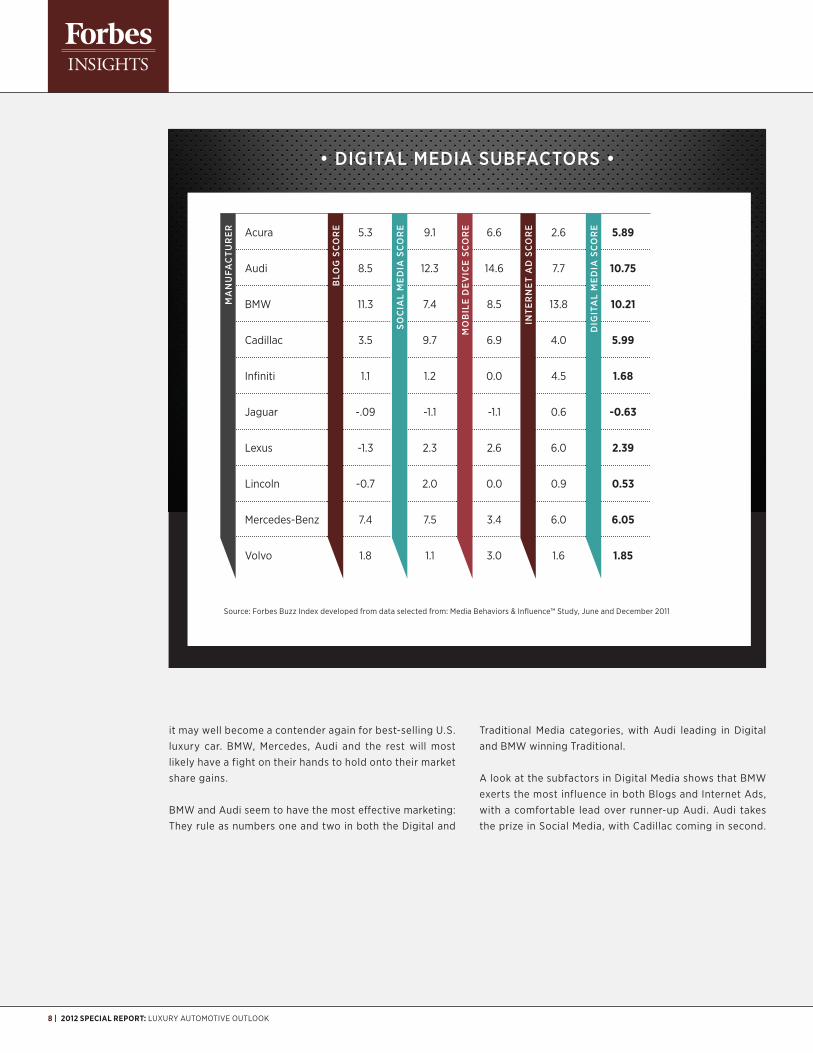

• dIgItaL MedIa SuBfaCtorS •

Acura 5.3 9.1 6.6 2.6 5.89

Audi 8.5 12.3 14.6 7.7 10.75

BMW 11.3 7.4 8.5 13.8 10.21

Cadillac 3.5 9.7 6.9 4.0 5.99

Infiniti 1.1 1.2 0.0 4.5 1.68

Jaguar -.09 -1.1 -1.1 0.6 -0.63

Lexus -1.3 2.3 2.6 6.0 2.39

Lincoln -0.7 2.0 0.0 0.9 0.53

Mercedes-Benz 7.4 7.5 3.4 6.0 6.05

Volvo 1.8 1.1 3.0 1.6 1.85

Source: Forbes Buzz Index developed from data selected from: Media Behaviors & Influence™ Study, June and December 2011

it may well become a contender again for best-selling U.S. luxury car. BMW, Mercedes, Audi and the rest will most likely have a fight on their hands to hold onto their market share gains.

BMW and Audi seem to have the most effective marketing: They rule as numbers one and two in both the Digital and

Traditional Media categories, with Audi leading in Digital and BMW winning Traditional.

A look at the subfactors in Digital Media shows that BMW exerts the most influence in both Blogs and Internet Ads, with a comfortable lead over runner-up Audi. Audi takes the prize in Social Media, with Cadillac coming in second.

Ma

nu

faC

tu

re

r

BLo

g S

Co

re

SoC

IaL

Me

dIa

SC

or

e

Mo

BIL

e d

ev

ICe

SCo

re

Inte

rn

et

ad

SC

or

e

dIg

Ita

L M

ed

Ia S

Co

re

CoPyRIGhT © 2012 ForbeS inSightS | 9

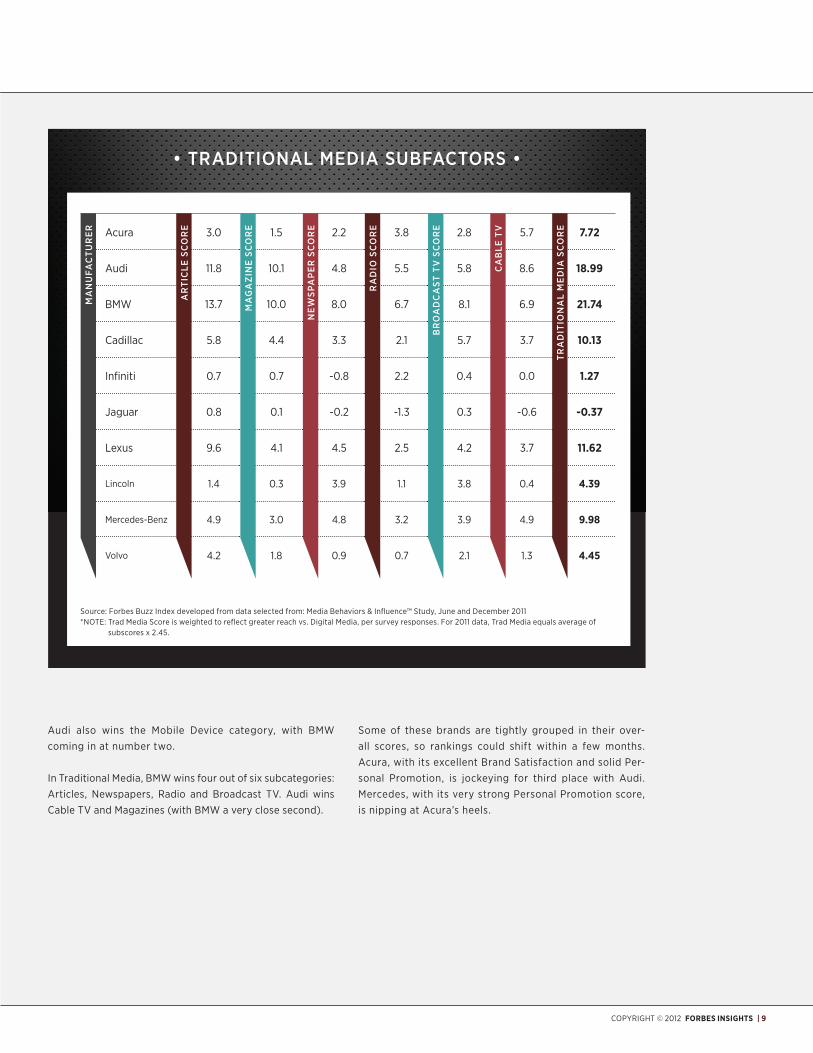

• tradItIonaL MedIa SuBfaCtorS •

Acura 3.0 1.5 2.2 3.8 2.8 5.7 7.72

Audi 11.8 10.1 4.8 5.5 5.8 8.6 18.99

BMW 13.7 10.0 8.0 6.7 8.1 6.9 21.74

Cadillac 5.8 4.4 3.3 2.1 5.7 3.7 10.13

Infiniti 0.7 0.7 -0.8 2.2 0.4 0.0 1.27

Jaguar 0.8 0.1 -0.2 -1.3 0.3 -0.6 -0.37

Lexus 9.6 4.1 4.5 2.5 4.2 3.7 11.62

Lincoln 1.4 0.3 3.9 1.1 3.8 0.4 4.39

Mercedes-Benz 4.9 3.0 4.8 3.2 3.9 4.9 9.98

Volvo 4.2 1.8 0.9 0.7 2.1 1.3 4.45

Source: Forbes Buzz Index developed from data selected from: Media Behaviors & Influence™ Study, June and December 2011 * NoTE: Trad Media Score is weighted to reflect greater reach vs. Digital Media, per survey responses. For 2011 data, Trad Media equals average of

subscores x 2.45.

Ma

nu

faC

tu

re

r

ar

tIC

Le S

Co

re

tra

dIt

Ion

aL

Me

dIa

SC

or

e

Ma

ga

zIn

e SC

or

e

ne

wS

PaP

er

SC

or

e

ra

dIo

SC

or

e

Br

oa

dC

aS

t t

v S

Co

re

Ca

BLe

tv

Audi also wins the Mobile Device category, with BMW coming in at number two.

In Traditional Media, BMW wins four out of six subcategories: Articles, Newspapers, Radio and Broadcast TV. Audi wins Cable TV and Magazines (with BMW a very close second).

Some of these brands are tightly grouped in their over-all scores, so rankings could shift within a few months. Acura, with its excellent Brand Satisfaction and solid Per-sonal Promotion, is jockeying for third place with Audi. Mercedes, with its very strong Personal Promotion score, is nipping at Acura’s heels.

10 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

so WhAt’s in A nAme?One brand that does command a lot of clout is Mercedes-Benz. Yet when looking at Brand Satisfaction, the German automaker scores seventh out of the 10 brands ranked in the Buzz Index.

That’s because it has been working through some qual-ity issues, according to BIGinsight data. “As we look at reasons that survey respon-dents chose a car, in late 2009 and 2010, Mercedes was experiencing some qual-ity and style problems,” says Roger Saunders, manag-ing director, Prosper Group of Companies at BIGinsight. “They were capturing peo-ple because of financing deals, old cars dying, high mileage. Now they are capturing them based on style, added features and quality. This quality issue was driving people away from Mercedes in the later portion of 2009. They appear to have turned the corner in the con-sumers’ mind.”

Mercedes’s Brand Satisfaction and Personal Promotion scores have both been moving up over the past six months. U.S. sales in 2011 were up 17.5% over 2010 to a total of 264,460 vehicles, an all-time record for the brand.

Up until a few years ago, Mercedes was the automotive icon for the established wealthy elite. But that is chang-ing, thanks to the Baby Boomers. “This sort of elitist kind of luxury is really a notion that’s going by the wayside,” says Steve Cannon, who in January was appointed presi-dent and CEO of Mercedes-Benz USA. He was previously vice president of marketing.

That’s because most wealth in the U.S. is generated by entrepreneurs. “It’s made wealth, not inherited wealth,” he says, and these entrepreneurs “bring a middle-class men-tality to their wealth.”

Another sociological trend shifting Mercedes’s brand focus is the fact that Baby Boomers are not slow-ing down as they approach retirement. “Look at most of them, they’re going to keel over in the gym somewhere, as opposed to nursing homes,” Cannon says. “They’re rede-fining old age; that’s why we say things like 70 is the new 60. So they’re still youthful, they’re not going quietly into the night.”

Couple that with the fact that their kids—Generation Y—will eventually be the next Mercedes-Benz buy-ers and it’s clear why the company has been creating cars with more dynamic and youthful designs in recent years. In 2011, the company launched six new products, the most it has ever debuted in a single year. Half are what

Cannon calls “halo” cars—like the SLS AMG Roadster and SLK convertible—which sell in relatively small num-bers but bolster the company’s image with their high perfor-mance and desirability. The other three are big sellers: the all-new C-Class coupe, and a redesigned C-Class sedan and M-Class crossover.

To promote these new vehicles, Mercedes has been running edgier ads. Cannon is proud of them. He gets visibly excited showing a television spot, called “Unchained,” on his iPad. In it, a C-Class sedan with

chains attached to its rear doors accelerates away; the chains are anchored to the ground and rip the rear doors off to reveal the new C-Class coupe.

“The C-Class is our entry price point,” Cannon says, “so if we’re going to start building bridges with younger consumers as they start to move into our consideration set, that’s the right vehicle to do it. We wouldn’t be edgy and kind of push the needle with something like the S-Class, because it’s our flagship.”

At the same time, Mercedes is also playing up its heritage in advertising. It celebrated 125 years in 2011 and has several TV spots that star classic Mercedes vehicles. “Heritage plays really well with Gen Y’ers,” Cannon says.

A spot that ran during the Super Bowl celebrating 125 years shows dozens of Mercedes cars, old and new, flock-ing of their own volition to an aircraft hangar where the company’s new line of vehicles is on display. Janice Joplin’s song “Mercedes-Benz” plays on the stereo of a classic SL convertible. “It gives me chills,” Cannon says. “I watch it whenever I need to get charged up.”

His job is a balancing act: planting seeds in the minds of future customers while still targeting existing ones.

“This sort of elitist kind of luxury is really a notion that’s going by the wayside.”

—SteVe cannon president and ceo, Mercedes-benz USa

CoPyRIGhT © 2012 ForbeS inSightS | 11

“Because those are who I’m going to get measured on: sales that we make this year, not bridges that I build for 10 years from now,” he says.

Marketing efforts seem to be paying off. The fact that Mercedes—or any other automaker for that matter—can appeal to both Baby Boomers and Generation Y simulta-neously is serendipitous. There’s usually a generation gap getting in the way.

“With Boomers and the Silent Generation, who were their parents, there was a lot of like, ‘I want to make the world a different place; I’m not listening to you; I’m doing something completely radical,’” Acura’s Poponi says. “Whereas Gen Y and the Boomers, they’re friends—they’re much more simpatico.”

Boomers have made a point of being as connected to their kids as they can be. “The Baby Boomers are involved parents that maybe their parents weren’t. They’re abso-lutely hands-on,” Cannon says. “They’re often called ‘helicopter parents’ because they kind of hover around their kids and circle and make sure that they get every-thing right and they’re given a trophy at the end.”

As much as Boomers and Gen Y’ers may get along famously, BIGinsight’s December 2011 Consumer Survey does highlight some attitudinal differences among gen-erations. For example, the younger the respondent, the more likely he/she is to feel confident of a strong econ-omy in the next six months (Figure 5). Forty percent of Gen Y’ers said they were confident/very confident. In contrast, 31.7% of Generation X respondents expressed confident/very confident views, while only 20.9% of the Boomers were confident/very confident, about half as many as Gen Y.

Younger respondents are also much more likely to agree with the statement “Live for today because tomorrow is so uncertain,” and they are much more fashion-oriented than older consumers (Figure 6).

0% 30% 60%

n Gen y n Gen x n Boomers

FigUre 5: Which one of the following best describes your feelings about chances for a strong economy during the next 6 months?

Very confident

Confident

Little confidence

No confidence

9.5

30.5

49.0

11.0

7.9

23.8

51.1

17.2

2.9

18.0

52.7

26.4

0% 30% 60%

n Gen y n Gen x n Boomers

FigUre 6: Which statement best applies to your feelings about fashion:

Newest trends and styles are important to me

I prefer a traditional conservative look

Fashion is less important than value and comfort to me

36.2

27.1

36.7

29.0

32.8

38.2

9.4

37.9

52.7

Source: Monthly Consumer Survey from BIGinsight™, December 2011 Total Adult Respondents 18+ 8,402

totaL BooMer aduLtS 2,891

totaL generatIon x aduLtS 1,835

totaL generatIon y aduLtS 2,123

12 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

the big piCture

Data from BIGinsight can provide per-spective on the outlook for the forest, not just the trees. Figure 7 below graphs the percentage of affluent consumers (household income $100,000 or more) who plan to purchase a vehicle in the next six months. one can readily see the big dips of 2009 and early 2010, as well as the drop in July/August 2011 amid the uncertainty of the debt ceiling debate and the U.S. credit downgrade. Just as clear is the overall trend line, which has moved

steadily upward for the past three years. Given that the data looks ahead six months, that steady trend line bodes well for the industry.

Figure 8 below underlines that rosy forecast: It graphs the percentage of those affluent prospective purchasers who intend to buy a car in the most expensive category (over $40,000). once again, the trend line cuts through the noisy clutter of month-to-month fluctuations, revealing a steady, continuing upward trend—encouraging news for the next six months.

FigUre 7: HH Income $100,000+

Dec ‘08 Jun ‘09 Dec ‘09 Jun ‘10 Dec ‘10 Jun ‘11 Dec ‘11

25%

20%

15%

10%

5%

0%

yes (Planning to Buy Car/Truck)

Linear Trend Line

FigUre 8: HH Income $100,000+

40%

35%

30%

25%

20%

15%

10%

5%

0%Dec ‘08 Jun ‘09 Dec ‘09 Jun ‘10 Dec ‘10 Jun ‘11 Dec ‘11

over $40,000 (Price Range for a Car to Buy)

Linear Trend Line

CoPyRIGhT © 2012 ForbeS inSightS | 13

Source: Monthly Consumer Survey from BIGinsight™

FigUre 10: Planning to Buy Car/Truck

16%

14%

12%

10%

8%

6%

4%

2%

0%Dec ‘08 Jun ‘09 Dec ‘09 Jun ‘10 Dec ‘10 Jun ‘11 Dec ‘11

FigUre 9: Aggregate Luxury Demand (1st and 2nd Choice)

All hh Income Levels Considering Luxury Brand

Linear Trend Line

All hh Income Levels

Linear Trend Line

20%

15%

10%

Jan ‘11 Feb ‘11 Mar ‘11 Apr ‘11 May ‘11 Jun ‘11 Jul ‘11 Aug ‘11 Sep ‘11 Oct ‘11 Nov ‘11 Dec ‘11

Figure 9 below provides yet another way of looking at the market: It shows aggregate luxury car demand throughout 2011 (demand for all 10 luxury brands ranked in the Buzz Index) by graphing the percentage of all prospective pur-chasers (all incomes) who said they were considering any of these brands as either first or second choice.

This trend line also shows a steady rise. The prediction of growing luxury car sales implicit in the first half of this chart was borne out by events in the latter half of 2011. The second half of this chart signals strong results continuing through the first half of 2012.

And finally, stepping away from the luxury category for a mo-ment provides a look at prospects for the auto industry as a whole. Figure 10 graphs the percentage of the total popula-tion with an intent to buy a vehicle over the next six months. Although the starting and ending points on the chart are not as high as with affluent consumers (Figure 7), and the trend line is not as steep, the overall direction remains relentlessly upward, predicting further growth for the next six months.

14 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

demoCrAtizing LuxuryLexus’s Templin says he believes buyers are gravitating more toward luxury these days—not just for cars, but for everything from clothing to household appliances.

He attributes this trend to “the democratization of luxury.”

The father of three—ages 22, 20 and 15—says chil-dren like his grew up during an economic boom, and pre-mium goods are the stuff of ordinary life to them. “I think there’s a whole genera-tion that wants to have those things,” he says.

He mentions the two Sub-Zero refrigerators and the restaurant-quality, six-burner stove in his kitchen, for exam-ple. To the young Templins, this is standard, because they’ve never known anything else. “They don’t want the Sears Kenmore stuff I grew up with,” Templin says.

He casts this desire to buy luxury as being practi-cal, more so than splurging. “In the old days, you’d buy something that was less money, but you’d have to buy it more frequently,” he says. “Over time, people have come to the realization they’d rather have a premium brand and hold on to it lon-ger, versus replacing that GE or that Sears Kenmore.”

Still, he does not expect sales of luxury cars to go gangbusters. He projects that luxury could rise from 11% of overall car sales to 13%. “It’ll probably not reach 15%, because there is a price fac-tor,” he says.

Competition in the luxury segment is heating up along with demand. Because of this, Templin says, sales wil l be fragmented among more manufacturers. So even though Lexus expects its own sales volume to increase, it most l ikely wil l have a smaller share of the market.

That’s a dramatic shift from a few years ago, when the luxury automotive sector had its own version of the Big Three.

“Everybody wants a piece of this growing mar-ket,” Templin says. “So even though we will grow, and Mercedes will grow, and BMW will grow, our shares

probably won’t be as big as they were back in 2007, because there were really only three players in the entire market then.”

Key to Lexus’s strategy is the ownership experience. While a brand like BMW focuses on positioning its cars as the “ultimate driv-ing machines,” Lexus puts as much emphasis on the expe-rience of owning its cars as it does the cars themselves.

It seems to be working. Lexus ranks highest among luxury brands in satisfaction with the process of buying a new vehicle, according to the J.D. Power and Associates 2011 Sales Satisfaction Index Study. Cadillac and Mercedes-Benz rank second and third, respectively.

Tyler, who hosted the Lexus dinner in her home, says she had never thought about the actual experi-ence of owning her “ruby red” LS 460 luxury sedan that “was sitting there spar-kling, calling my name” at Sheehy Lexus of Annapolis.

But sure enough, she thinks her experience with Lexus has been exceptional.

In fact, Tyler goes to the dealer once or twice a week to have her car washed for free— “well, you tell a real estate agent ‘car wash,’ I’m there”—and sometimes brings a coworker to have lunch at the dealership’s cafe, which makes a killer chicken salad sandwich.

“If it weren’t a great experience, if everyone wasn’t so nice, if the place wasn’t so clean and bright, I wouldn’t go

“Everybody wants a piece of this growing market.

So even though we will grow, and Mercedes will grow, and BMW will grow, our shares probably won’t be as big as

they were back in 2007, because there were really only three players in the

entire market then.”

—Mark teMplin group Vice president and

general Manager, lexus USa

CoPyRIGhT © 2012 ForbeS inSightS | 15

to lunch there every week,” Tyler says. “I’d just slam in to get my car washed and leave; or maybe I’d go to the normal car wash. But it feels good.”

The dinner she hosted in her home was no differ-ent—five-star all the way, from setup to service to the food and wine, she says. Tyler was chosen to host the dinner because she participates in a group called the Lexus Advisory Board, which answers online surveys the company conducts periodically. Lexus keeps in reg-ular email contact with about 30,000 customers who participate on the advisory board. When it’s time to schedule a new dinner, they ask for volunteers and pick based on their location and the layout of their home, among other factors.

The dinners operate under what Templin calls a “truth serum” theme. “I’m not trying to sell them a car—that’s not what it’s about,” he says. “We want open, candid conversation.”

Tyler was instructed not to invite a bunch of Lexus owners. “They said, ‘Basically, we don’t want a Lexus love fest.’ So only one other person [at the dinner] owns a Lexus car, currently,” she says. “We had a diehard Cadillac couple. Two people have Mini Cooper convert-ibles, one couple is both Mercedes.”

Mercedes uses online communities similar to Lexus’s Advisory Board to get feedback directly from consum-ers on the Web. One is called Mercedes-Benz Advisors and consists of typical Mercedes owners. Another group, called Gen Benzers, is younger. “They’re 20-somethings, they’re Gen Y’ers,” Cannon says. “Only about a quar-ter of them are actual Mercedes-Benz owners, the rest of them aren’t in our consuming demographic. But they are our Gen Y sounding board. There’s about 500 of them at any given time.”

It was through their feedback that he discovered that imagery surrounding the company’s heritage and histori-cal footage would appeal to that age group.

Last year was a tough one for Lexus, in terms of sales. It ended 2011 having sold 13.7% fewer cars in the U.S. than it did in 2010. As was the case with Acura, which saw annual sales decline 8%, the natural disasters that pounded Japan in 2011 had a huge impact on produc-tion capacity.

16 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

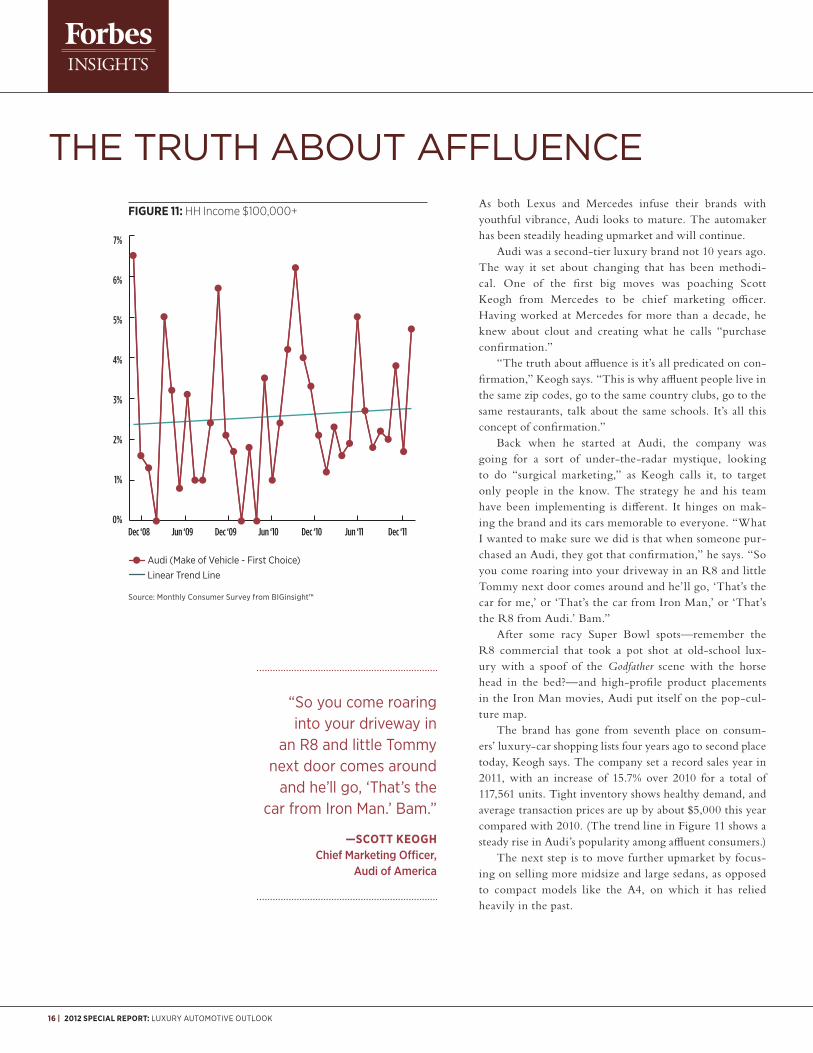

the truth About AFFLuenCeAs both Lexus and Mercedes infuse their brands with youthful vibrance, Audi looks to mature. The automaker has been steadily heading upmarket and will continue.

Audi was a second-tier luxury brand not 10 years ago. The way it set about changing that has been methodi-cal. One of the first big moves was poaching Scott Keogh from Mercedes to be chief marketing officer. Having worked at Mercedes for more than a decade, he knew about clout and creating what he calls “purchase confirmation.”

“The truth about affluence is it’s all predicated on con-firmation,” Keogh says. “This is why affluent people live in the same zip codes, go to the same country clubs, go to the same restaurants, talk about the same schools. It’s all this concept of confirmation.”

Back when he started at Audi, the company was going for a sort of under-the-radar mystique, looking to do “surgical marketing,” as Keogh calls it, to target only people in the know. The strategy he and his team have been implementing is different. It hinges on mak-ing the brand and its cars memorable to everyone. “What I wanted to make sure we did is that when someone pur-chased an Audi, they got that confirmation,” he says. “So you come roaring into your driveway in an R8 and little Tommy next door comes around and he’ll go, ‘That’s the car for me,’ or ‘That’s the car from Iron Man,’ or ‘That’s the R8 from Audi.’ Bam.”

After some racy Super Bowl spots—remember the R8 commercial that took a pot shot at old-school lux-ury with a spoof of the Godfather scene with the horse head in the bed?—and high-profile product placements in the Iron Man movies, Audi put itself on the pop-cul-ture map.

The brand has gone from seventh place on consum-ers’ luxury-car shopping lists four years ago to second place today, Keogh says. The company set a record sales year in 2011, with an increase of 15.7% over 2010 for a total of 117,561 units. Tight inventory shows healthy demand, and average transaction prices are up by about $5,000 this year compared with 2010. (The trend line in Figure 11 shows a steady rise in Audi’s popularity among affluent consumers.)

The next step is to move further upmarket by focus-ing on selling more midsize and large sedans, as opposed to compact models like the A4, on which it has relied heavily in the past.

FigUre 11: HH Income $100,000+

7%

6%

5%

4%

3%

2%

1%

0%Dec ‘08 Jun ‘09 Dec ‘09 Jun ‘10 Dec ‘10 Jun ‘11 Dec ‘11

Source: Monthly Consumer Survey from BIGinsight™

Audi (Make of Vehicle - First Choice)

Linear Trend Line

“So you come roaring into your driveway in

an R8 and little Tommy next door comes around

and he’ll go, ‘That’s the car from Iron Man.’ Bam.”

—Scott keogh Chief Marketing officer,

Audi of America

CoPyRIGhT © 2012 ForbeS inSightS | 17

WhAt’s next For AmeriCAn Luxury?Having successfully climbed its way up the luxury-car lad-der, Audi has created room for a new challenger: Cadillac.

With General Motors’ bankruptcy fading from mem-ory, Cadillac fills Audi’s spot as a key contender with top-tier brands and is wasting no time.

“Cadillac was, for the better part of the last century, the standard of the world,” says Don Butler, vice president of marketing at Cadillac. “That’s what we were known for. So we aspire to return to that.”

The company is counting on an all-new large sedan called the XTS, on sale in spring 2012, to help achieve that. It will have a new look, higher levels of craftsmanship and innovative technology. It will be the first model to feature the company’s new CUE interface, which takes an iPad approach to stereo, climate and navigation controls. A smaller sedan, the ATS, set to go on sale summer 2012, has

the unenviable task of trying to beat BMW’s new 3 Series, the leader in its segment.

Butler says these new Cadillacs aren’t for everyone. “I’m not going for broad acceptance, I’m going for that deep meaningful connection with a few customers. And if I get that deep meaningful connection with a few cus-tomers, then they will become ambassadors for the brand, and they will find like-minded customers and bring them along,” he says.

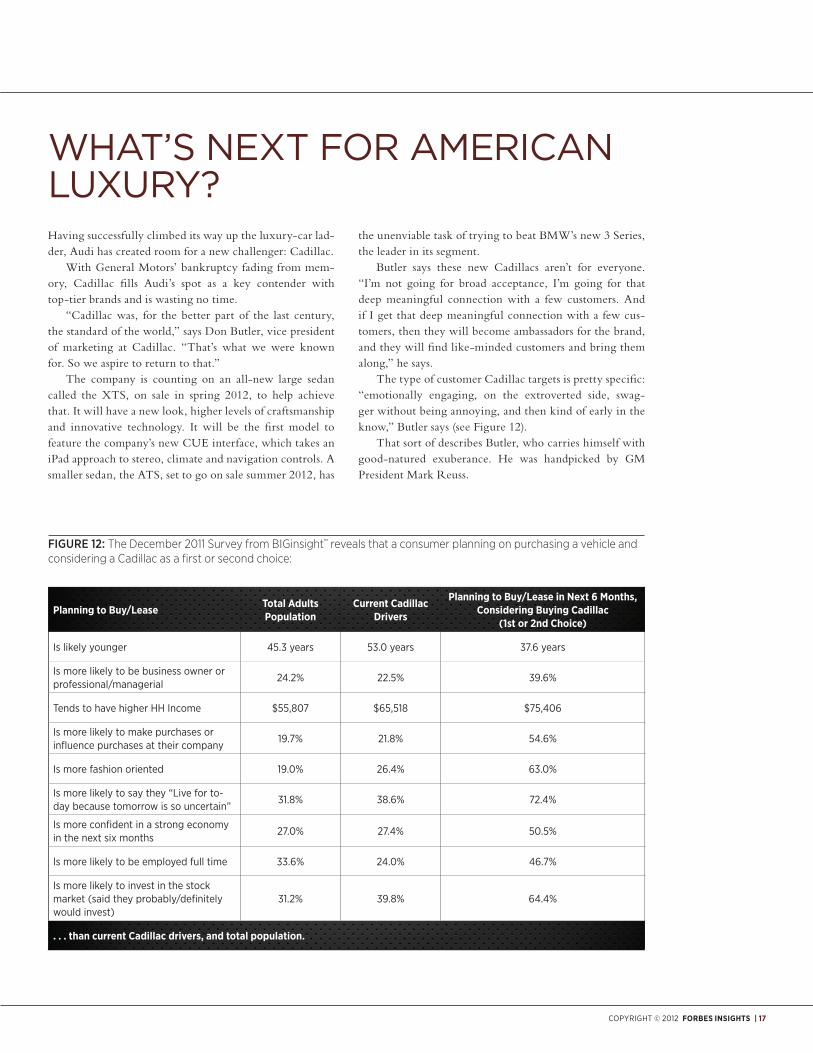

The type of customer Cadillac targets is pretty specific: “emotionally engaging, on the extroverted side, swag-ger without being annoying, and then kind of early in the know,” Butler says (see Figure 12).

That sort of describes Butler, who carries himself with good-natured exuberance. He was handpicked by GM President Mark Reuss.

planning to buy/lease total adults population

current cadillac drivers

planning to buy/lease in next 6 Months, considering buying cadillac

(1st or 2nd choice)

Is likely younger 45.3 years 53.0 years 37.6 years

Is more likely to be business owner or professional/managerial

24.2% 22.5% 39.6%

Tends to have higher hh Income $55,807 $65,518 $75,406

Is more likely to make purchases orinfluence purchases at their company

19.7% 21.8% 54.6%

Is more fashion oriented 19.0% 26.4% 63.0%

Is more likely to say they “Live for to-day because tomorrow is so uncertain”

31.8% 38.6% 72.4%

Is more confident in a strong economy in the next six months

27.0% 27.4% 50.5%

Is more likely to be employed full time 33.6% 24.0% 46.7%

Is more likely to invest in the stock market (said they probably/definitely would invest)

31.2% 39.8% 64.4%

. . . than current cadillac drivers, and total population.

Figure 12: The December 2011 Survey from BIGinsight™ reveals that a consumer planning on purchasing a vehicle and considering a Cadillac as a first or second choice:

18 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

Butler had left GM’s OnStar division at the end of 2009 to work at Inrix, a navigation and traffic services provider based in Kirkland, Wash. He ran into Reuss, who had just been named president that December, at the Detroit Metro airport. A couple phone calls and a few months later, Butler was heading up Cadillac marketing.

He was ecstatic. “It’s the tip of the spear for GM,” Butler says. “Definitely it’s been tarnished, but we’re pol-ishing it up, we’re making it brighter. So literally it’s this job that brought me back to the company.”

Getting to work with Reuss was key to persuad-ing Butler to jump back to GM after being gone only a few months. “The biggest factor was Mark [Reuss] him-self,” he says, “ just knowing him, knowing what he was about, knowing the way he approached things—kind of no nonsense, no politics, no b.s.”

Thanks to Reuss, the corporate culture at Cadillac is much more streamlined now, Butler says. He has enough autonomy to push through important ideas quickly, like featuring the company’s high-performance V-series vehi-cles prominently in advertising for the first time ever. Niche models like the CTS-V were kept out of the mix previously because Cadillac sells only about 6,000 a year in North America.

“Typically, the practice is, don’t advertise against them, we don’t want to burden them with ad dollars because we sell so few,” Butler says. “And for me, I was like, ‘Are you kidding me? We build the world’s fastest production sedan? Let’s tell people about it.’ Let’s show that—guess what—in this area, we are the standard of the world.”

That’s how a 30-second television spot titled “Bellissimo” came about. It shows a bright red Ferrari 458 chasing a Cadillac CTS-V coupe. The upshot is that Ferrari borrowed Magnetic Ride Control suspension tech-nology from the Cadillac.

The company is also conducting “V Labs” at five different racetracks around the country to put people behind the wheel of a CTS-V—particularly those who drive competing Audi, BMW or Mercedes AMG cars.

“The surprise and the shock when they see that we are better than a BMW M5—it’s just kind of like, ‘Whoa,’” Butler says.

On a broader scale, the company is improving its deal-erships. Facilities are being upgraded to a new high-end look, but more importantly, Cadillac has partnered with Ritz-Carlton to train employees on how to create a five-star experience. It’s a lot of change, but dealers seem to be on board. In the most recent National Automobile Dealers Association annual ranking of what dealer bod-ies think of manufacturers, Cadillac came in ninth out of 33, compared with 24th in 2009.

“There’s a huge amount of respect for Cadillac,” Butler says. “But for a lot of people, that respect is analogous to, I respect and I love my grand-dad, but I don’t want to hang out with him all the time. So the challenge that I have is,

how do I take that residual positive sentiment and make it relevant for today’s buyer?”

Overall sales for the brand were up 3.7% in 2011. Factor out fleet sales to rental and limo companies, and the sales increase more than triples to 10.5% over the previous year. The Cadillac SRX crossover was particularly hot in 2011, with double-digit sales increases.

“We build the world’s fastest production sedan? Let’s tell people about it. Let’s show that—guess

what—in this area, we are the standard of the world.”

—don bUtler Vice president of Marketing, cadillac

CoPyRIGhT © 2012 ForbeS inSightS | 19

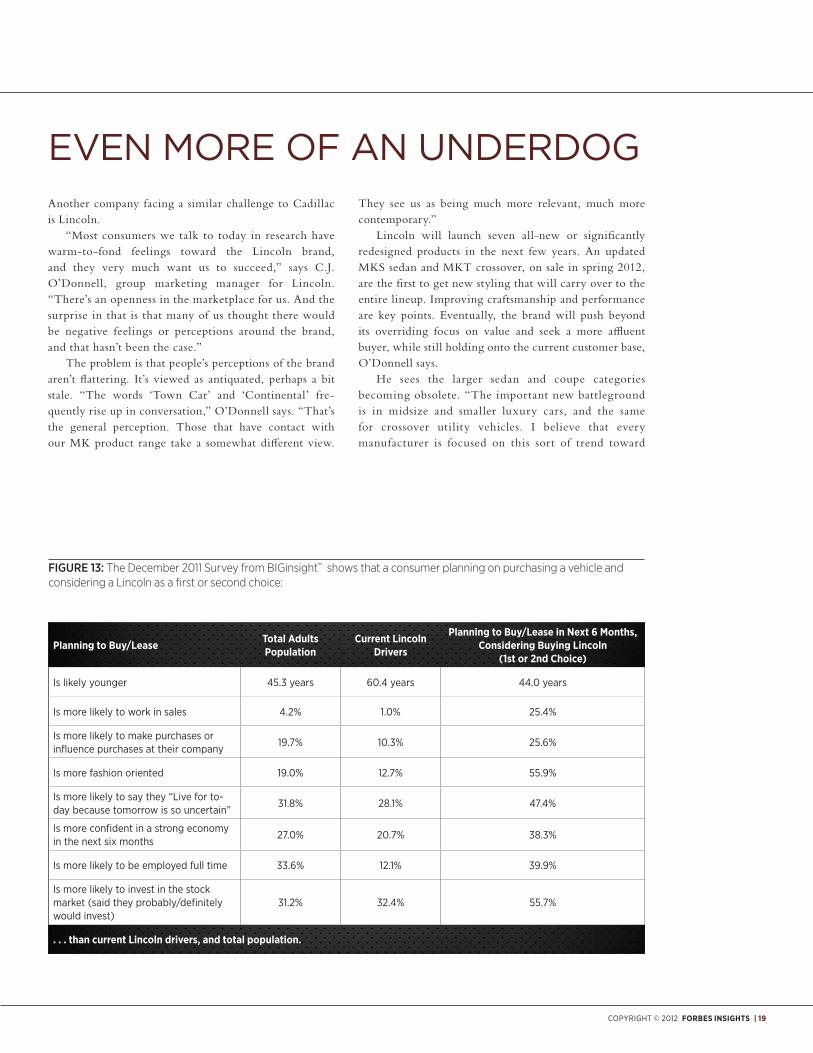

even more oF An underdogAnother company facing a similar challenge to Cadillac is Lincoln.

“Most consumers we talk to today in research have warm-to-fond feelings toward the Lincoln brand, and they very much want us to succeed,” says C.J. O’Donnell, group marketing manager for Lincoln. “There’s an openness in the marketplace for us. And the surprise in that is that many of us thought there would be negative feelings or perceptions around the brand, and that hasn’t been the case.”

The problem is that people’s perceptions of the brand aren’t flattering. It’s viewed as antiquated, perhaps a bit stale. “The words ‘Town Car’ and ‘Continental’ fre-quently rise up in conversation,” O’Donnell says. “That’s the general perception. Those that have contact with our MK product range take a somewhat different view.

They see us as being much more relevant, much more contemporary.”

Lincoln will launch seven all-new or significantly redesigned products in the next few years. An updated MKS sedan and MKT crossover, on sale in spring 2012, are the first to get new styling that will carry over to the entire lineup. Improving craftsmanship and performance are key points. Eventually, the brand will push beyond its overriding focus on value and seek a more affluent buyer, while still holding onto the current customer base, O’Donnell says.

He sees the larger sedan and coupe categories becoming obsolete. “The important new battleground is in midsize and smaller luxury cars, and the same for crossover utility vehicles. I believe that every manufacturer is focused on this sort of trend toward

planning to buy/lease total adults population

current lincoln drivers

planning to buy/lease in next 6 Months, considering buying lincoln

(1st or 2nd choice)

Is likely younger 45.3 years 60.4 years 44.0 years

Is more likely to work in sales 4.2% 1.0% 25.4%

Is more likely to make purchases orinfluence purchases at their company

19.7% 10.3% 25.6%

Is more fashion oriented 19.0% 12.7% 55.9%

Is more likely to say they “Live for to-day because tomorrow is so uncertain”

31.8% 28.1% 47.4%

Is more confident in a strong economy in the next six months

27.0% 20.7% 38.3%

Is more likely to be employed full time 33.6% 12.1% 39.9%

Is more likely to invest in the stock market (said they probably/definitely would invest)

31.2% 32.4% 55.7%

. . . than current lincoln drivers, and total population.

Figure 13: The December 2011 Survey from BIGinsight™ shows that a consumer planning on purchasing a vehicle and considering a Lincoln as a first or second choice:

20 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

downsizing and getting their mid- to small-package vehicles in a position where they’re seen as true luxury products,” he says.

O’Donnell is optimistic about the future for the company and is confi-dent of the team that has been built up at Lincoln over the past 20 months. He left Jaguar in May 2010 to join Lincoln. It has been a long, tough slog, he says. “We’ve put some hard hours in over this past year, and even though we’ve added to the team, we’re moving for-ward faster, but the workload hasn’t seemed to decrease.”

But there is a sense of a higher call-ing that keeps the team invigorated. “The fun part is that there’s a group of people here that feel part of something

really special. They joined up because they knew the work would be hard, they knew the payoff would be years out, and they come in every day and give me the energy to push on because they’re just so gassed by the concept of revitalizing Lincoln,” O’Donnell says.

At the dealership level, things are already looking up. Lincoln is the most improved luxury brand in terms of its dealership experience, according to the J.D. Power and Associates 2011 U.S. Sales Satisfaction Index, jumping to sixth place from ninth in 2010.

U.S. sales for the brand have been holding steady this year—down by only 0.7% through November. But O’Donnell says Lincoln is up more than 20% in key lux-ury markets. “The top 10 metro areas make up almost half of all the luxury sales in the country, and it’s in markets like that—like L.A., New York and Miami—where we’re making some really significant gains.”

“The important new battleground is in midsize

and smaller luxury cars, and the same for cross-

over utility vehicles. Every manufacturer is

focused on getting their mid- to small-package

vehicles seen as true luxury products.”

—c.J. o’donnell group Marketing Manager, Lincoln

CoPyRIGhT © 2012 ForbeS inSightS | 21

A vieW From the topOne company at the opposite end of the spectrum from Lincoln in terms of brand power is BMW. It scored the highest in the overall Buzz Index. Part of that is because the company focuses so keenly on conveying that its cars are “The Ultimate Driving Machine,” and actually backs it up with vehicles that truly are fun to drive.

Although 2011 turned out to be BMW’s second-best sales year in the U.S.—with 305,418 vehicles sold, for an increase of 14.9% over 2010—it still beat every other luxury automaker.

Ludwig Willisch, pres-ident and CEO of BMW North America, took over BMW NA in October from Jim O’Donnell, who is retir-ing. He spent the first several months getting his bear-ings. He’s new to the North American market, hav-ing most recently headed up BMW Group’s European sales region.

The biggest surprise so far has been finding out exactly how tough the competition is. “I have to say frankly, and I’ve been around quite a bit, I’ve not encountered any market that is as competitive as the U.S. market,” he says.

Willisch speaks of this not with concern, but with the same unflappable calm he brings to everything he does. Colleagues say it is one of his defining qualities. Another is the fact that he genuinely loves cars—so much so that part of him misses being president of BMW’s high-per-formance M division, which he was before becoming head of European sales in 2009. “I am a car guy, I really am. So I thought that was really the place to be and to stay,” he says.

Amid many new products, including the company’s most popular models, the 3 Series and 5 Series, next-gen-eration alternative propulsion has become a key priority, as previewed in two concept vehicles, the i3 electric car and i8 hybrid.

To play up fuel efficiency this prominently might seem incongruous for a brand so focused on high performance, but Willisch insists it’s not. “Fun-to-drive doesn’t have

anything to do with the technology of the powertrain, it’s simply the characteristics of the car itself.”

He also points out that efficiency and sustainabil-ity have long been a priority in other markets, where the company already offers smaller diesel engines, for exam-

ple. Plus, focusing on these attributes is critical if the brand is to remain relevant to Generation Y.

“We’re moving that way,” Willisch says. “Still having in mind that BMW will always stay the ultimate driving machine, but proving pretty soon that even with electro-mobility, even with hybrid technology, you will be able to provide the ultimate driv-ing machine.”

“I have to say frankly, and I’ve been around quite a bit,

I’ve not encountered any market that is as competitive

as the U.S. market.”

–lUdwig williSch president and ceo, bMw north america

22 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

the neW ContenderAs if the competition weren’t fierce enough for BMW and other luxury brands, a new contender has eyes on their territory: Hyundai Motor America. It would seem unlikely that a 47-year-old Korean manufacturer of budget-priced cars could compete with true luxury brands, but as we’ve already established, these are strange times.

“I think maybe it was being lucky, maybe it was being brilliant,” says Steve Shannon, Hyundai Motor America’s vice president of marketing. He’s talking about the company’s decision to push into the premium segment in the U.S. “Lucky in terms of being just when the market kind of took a dip a couple of years ago when the Equus was coming out.”

The Equus is Hyundai’s priciest car by far. The full-size sedan is loaded up

with a powerful V-8 and every conceivable luxury. It has a suggested starting price of $59,000—stratospheric for a company that has built its business on economy cars cost-ing less than $20,000.

Most of the 3,193 Equus sedans the company sold in 2011 were bought by people who already owned a Hyundai. In terms of luxury car trade-ins, the Lexus LS was the most frequent among Equus buyers, Shannon says. “No surprise, the character of the cars is similar. But what’s been exciting to see is a handful of BMW 7 Series, S-Class and Audi A8s, some E-Class” being traded for the Equus.

The Hyundai Equus was the highest-ranked large premium sedan in J.D. Power and Associates’ “2011 Automotive Performance, Execution and Layout Study,” which surveys owners and asks them to rank their vehi-cles on design, content and performance. In terms of resale value, Automotive Lease Guides rates the Equus the same three out of five stars as the BMW 5 Series, Lexus LS and Mercedes E-Class.

Still, with only 3,193 sales in 2011, Hyundai lags in brand clout. What it lacks in that regard, the company is trying to make up for in other ways. For instance, it offered a free iPad with the Equus sedan when it launched the 2011 Equus in December of 2010. Hyundai gave away 2,842 iPads in total and is no longer offering them.

A more lasting strategy falls in line with Acura’s focus on time as the ultimate luxury. “In the luxury space, there

was a kind of arms race to see who could have the best cappuccino machines and the most amount of marble and granite in their dealerships,” Shannon says. “But for Hyundai, we’re going to take the dealership even out of the equation. So if you want a test drive, we’ll bring you the car; if you want to buy one and get it serviced, we’ll come and get it for you. So that’s kind of a way of saying, ‘Okay, we may not be able to outdo Mercedes and Lexus selling $115,000 cars, so let’s come up with some really innovative ideas that help satisfy that luxury customer in a unique way.’”

The further downmarket from the Equus you go, the better the story gets for Hyundai. Sales of its mid-size Genesis premium sedan—with a starting price of $34,200—saw record sales in 2011, up 13% compared with 2010 for a total of 32,998. Its Elantra compact sedan, rede-signed for 2011, won the 2012 North American Car of the Year from an independent panel of 50 automotive journal-ists. Last and far from least, total sales for the company hit a record high of 645,691 units for 2011, up 20% from the year before.

So it’s clear that Hyundai has positive momentum. The question is: How well can it parlay that into suc-cess within the luxury-car market? On the one hand, the time seems right, with even affluent buyers looking to be more sensible and less showy. There’s also the trend toward democratizing luxury, as Lexus’s Templin called it, which plays to Hyundai’s strengths, too.

If anything, Hyundai’s efforts are just another exam-ple of how jumbled things are in the luxury market—so much so that even savvy customers like Tyler, the Lexus LS owner who hosted the dinner in her home, are con-founded. “You know, I’m not real sure what a luxury car is anymore when you can buy a $60,000 Hyundai,” she says.

“We’re going to take the dealership out of the equation. So if you want

a test drive, we’ll bring you the car; if you want

to buy one and get it serviced, we’ll come

and get it for you.”

—SteVe Shannon vice President of Marketing,

Hyundai Motor America

CoPyRIGhT © 2012 ForbeS inSightS | 23

To keep up with the latest consumer automotive trends and data,

visit BIginsight’s automotive InsightCenter™

www.autoinsightcenter.com/autoinfo/

ConCLusionBarring some cataclysmic event in the next several months, it seems wise to take consumers at their word as far

as their purchase plans. The data is signaling that the first half of 2012 will continue to be quite positive for the auto

market overall in the U.S., and especially rosy for the luxury sector.

The percentage of affluent consumers who say they intend to buy or lease a vehicle in the next six months continues to climb. Furthermore, the price range of the vehicle they plan to purchase is also rising on a steady upward trend.

As the Japanese automakers recover from their sup-ply problems, they may well win some market share back, especially Lexus, thanks largely to loyal customers. But BMW and Audi now dominate the marketing wars, and Mercedes seems to be on an upswing.

The U.S. luxury auto market is volatile and intensely competitive. With American brands busy reinventing themselves, and even newcomers like Hyundai edging into the luxury space, the overall shape of this sector by 2013 can barely be glimpsed through a (tinted) wind-shield darkly.

But overall, through midyear 2012 at least, the good times should continue to roll.

24 | 2012 Special report: LUxURy AUToMoTIVE oUTLook

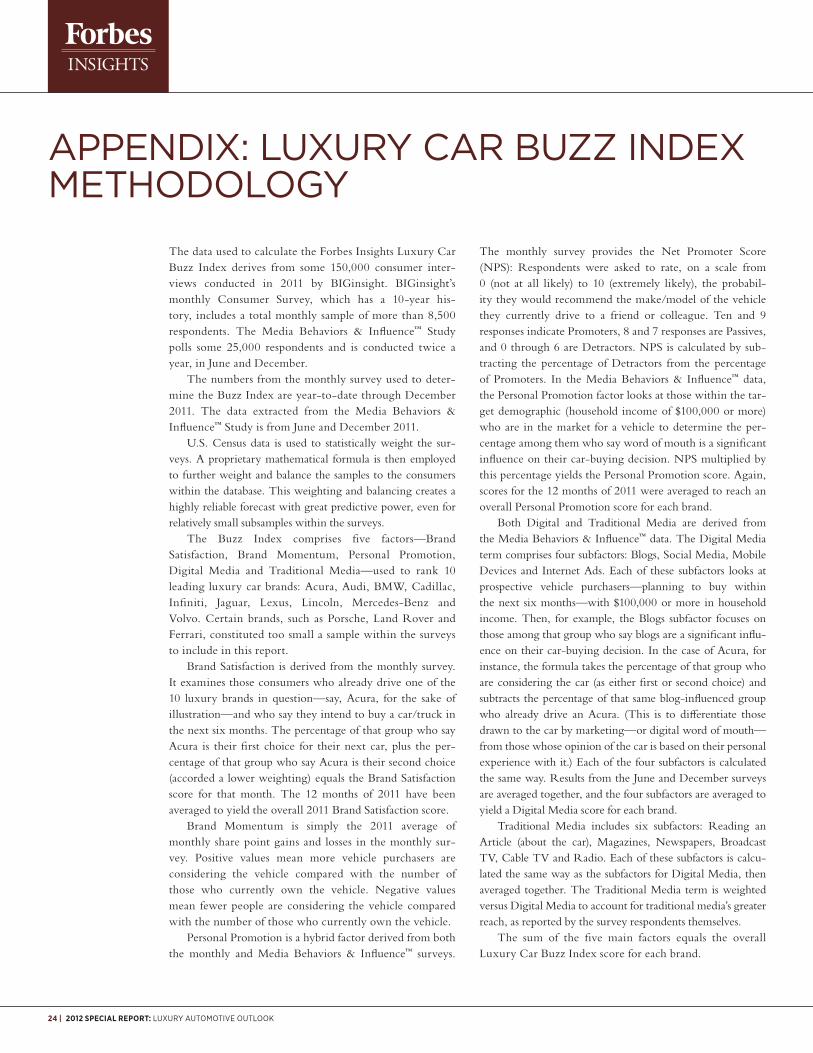

Appendix: Luxury CAr buzz index methodoLogy

The data used to calculate the Forbes Insights Luxury Car Buzz Index derives from some 150,000 consumer inter-views conducted in 2011 by BIGinsight. BIGinsight’s monthly Consumer Survey, which has a 10-year his-tory, includes a total monthly sample of more than 8,500 respondents. The Media Behaviors & Influence™ Study polls some 25,000 respondents and is conducted twice a year, in June and December.

The numbers from the monthly survey used to deter-mine the Buzz Index are year-to-date through December 2011. The data extracted from the Media Behaviors & Influence™ Study is from June and December 2011.

U.S. Census data is used to statistically weight the sur-veys. A proprietary mathematical formula is then employed to further weight and balance the samples to the consumers within the database. This weighting and balancing creates a highly reliable forecast with great predictive power, even for relatively small subsamples within the surveys.

The Buzz Index comprises five factors—Brand Satisfaction, Brand Momentum, Personal Promotion, Digital Media and Traditional Media—used to rank 10 leading luxury car brands: Acura, Audi, BMW, Cadillac, Infiniti, Jaguar, Lexus, Lincoln, Mercedes-Benz and Volvo. Certain brands, such as Porsche, Land Rover and Ferrari, constituted too small a sample within the surveys to include in this report.

Brand Satisfaction is derived from the monthly survey. It examines those consumers who already drive one of the 10 luxury brands in question—say, Acura, for the sake of illustration—and who say they intend to buy a car/truck in the next six months. The percentage of that group who say Acura is their first choice for their next car, plus the per-centage of that group who say Acura is their second choice (accorded a lower weighting) equals the Brand Satisfaction score for that month. The 12 months of 2011 have been averaged to yield the overall 2011 Brand Satisfaction score.

Brand Momentum is simply the 2011 average of monthly share point gains and losses in the monthly sur-vey. Positive values mean more vehicle purchasers are considering the vehicle compared with the number of those who currently own the vehicle. Negative values mean fewer people are considering the vehicle compared with the number of those who currently own the vehicle.

Personal Promotion is a hybrid factor derived from both the monthly and Media Behaviors & Influence™ surveys.

The monthly survey provides the Net Promoter Score (NPS): Respondents were asked to rate, on a scale from 0 (not at all likely) to 10 (extremely likely), the probabil-ity they would recommend the make/model of the vehicle they currently drive to a friend or colleague. Ten and 9 responses indicate Promoters, 8 and 7 responses are Passives, and 0 through 6 are Detractors. NPS is calculated by sub-tracting the percentage of Detractors from the percentage of Promoters. In the Media Behaviors & Influence™ data, the Personal Promotion factor looks at those within the tar-get demographic (household income of $100,000 or more) who are in the market for a vehicle to determine the per-centage among them who say word of mouth is a significant influence on their car-buying decision. NPS multiplied by this percentage yields the Personal Promotion score. Again, scores for the 12 months of 2011 were averaged to reach an overall Personal Promotion score for each brand.

Both Digital and Traditional Media are derived from the Media Behaviors & Influence™ data. The Digital Media term comprises four subfactors: Blogs, Social Media, Mobile Devices and Internet Ads. Each of these subfactors looks at prospective vehicle purchasers—planning to buy within the next six months—with $100,000 or more in household income. Then, for example, the Blogs subfactor focuses on those among that group who say blogs are a significant influ-ence on their car-buying decision. In the case of Acura, for instance, the formula takes the percentage of that group who are considering the car (as either first or second choice) and subtracts the percentage of that same blog-influenced group who already drive an Acura. (This is to differentiate those drawn to the car by marketing—or digital word of mouth—from those whose opinion of the car is based on their personal experience with it.) Each of the four subfactors is calculated the same way. Results from the June and December surveys are averaged together, and the four subfactors are averaged to yield a Digital Media score for each brand.

Traditional Media includes six subfactors: Reading an Article (about the car), Magazines, Newspapers, Broadcast TV, Cable TV and Radio. Each of these subfactors is calcu-lated the same way as the subfactors for Digital Media, then averaged together. The Traditional Media term is weighted versus Digital Media to account for traditional media’s greater reach, as reported by the survey respondents themselves.

The sum of the five main factors equals the overall Luxury Car Buzz Index score for each brand.

About Forbes insights

forbes Insights is the strategic research practice of forbes Media, publisher of forbes magazine and forbes.com. taking advantage of a proprietary database of senior-level executives in the forbes community, forbes Insights’ research covers a wide range of vital business issues, including: talent management; marketing; financial benchmarking; risk and regulation; small/midsize

business; and more.

Bruce rogers ChieF insights oFFiCer

Brenna Sniderman senior direCtor

Christiaan rizy direCtor

Hugo S. Moreno editoriAL direCtor

Matthew de Paula report Author

taryn Sefecka designer

60 Fifth Avenue, new york, ny 10011 | 212.367.2662 | www.forbes.com/forbesinsights