13

Spin-Off Research Joe Cornell, CFA “Breaking Up is Good To Do” The ABC’s of Spin-Offs

Spin-Off Research

Joe Cornell, CFA

“Breaking Up is Good To Do”

The ABC’s of Spin-Offs

Why Spin-Off?

• Spin-Offs are a source of significant market

outperformance for investors

• Spin-Offs often result in a higher aggregate

value for the constituent pieces

• Studies conducted by a range of researchers,

from Penn State to McKinsey have

documented that spin-offs, on average,

outperform market indexes

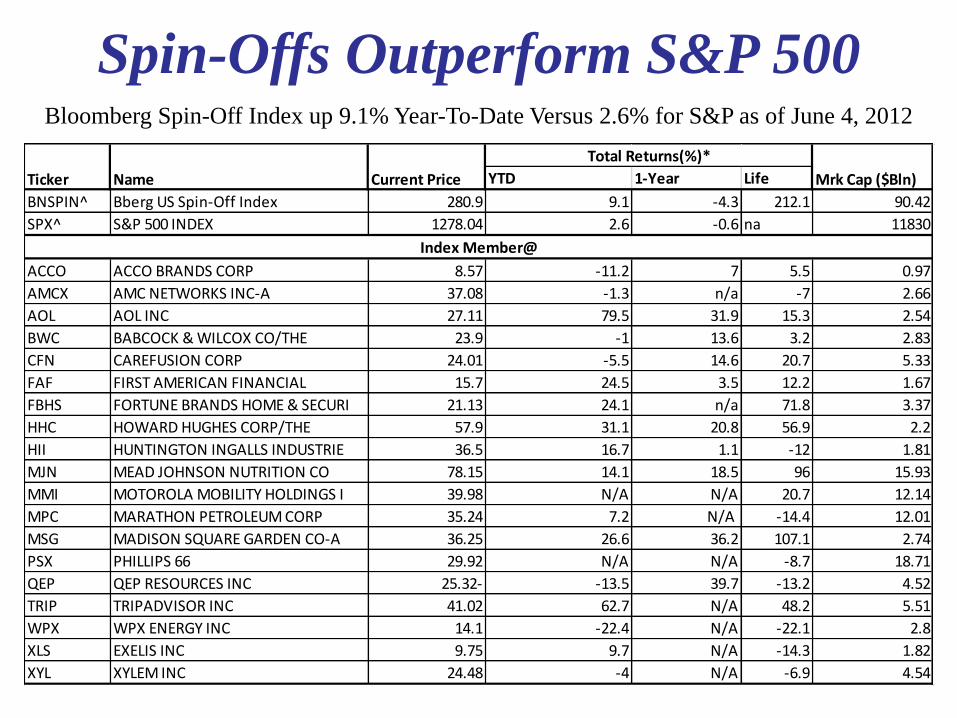

Spin-Offs Outperform S&P 500 Bloomberg Spin-Off Index up 9.1% Year-To-Date Versus 2.6% for S&P as of June 4, 2012

YTD 1-Year Life

BNSPIN^ Bberg US Spin-Off Index 280.9 9.1 -4.3 212.1 90.42

SPX^ S&P 500 INDEX 1278.04 2.6 -0.6 na 11830

ACCO ACCO BRANDS CORP 8.57 -11.2 7 5.5 0.97

AMCX AMC NETWORKS INC-A 37.08 -1.3 n/a -7 2.66

AOL AOL INC 27.11 79.5 31.9 15.3 2.54

BWC BABCOCK & WILCOX CO/THE 23.9 -1 13.6 3.2 2.83

CFN CAREFUSION CORP 24.01 -5.5 14.6 20.7 5.33

FAF FIRST AMERICAN FINANCIAL 15.7 24.5 3.5 12.2 1.67

FBHS FORTUNE BRANDS HOME & SECURI 21.13 24.1 n/a 71.8 3.37

HHC HOWARD HUGHES CORP/THE 57.9 31.1 20.8 56.9 2.2

HII HUNTINGTON INGALLS INDUSTRIE 36.5 16.7 1.1 -12 1.81

MJN MEAD JOHNSON NUTRITION CO 78.15 14.1 18.5 96 15.93

MMI MOTOROLA MOBILITY HOLDINGS I 39.98 N/A N/A 20.7 12.14

MPC MARATHON PETROLEUM CORP 35.24 7.2 N/A -14.4 12.01

MSG MADISON SQUARE GARDEN CO-A 36.25 26.6 36.2 107.1 2.74

PSX PHILLIPS 66 29.92 N/A N/A -8.7 18.71

QEP QEP RESOURCES INC 25.32- -13.5 39.7 -13.2 4.52

TRIP TRIPADVISOR INC 41.02 62.7 N/A 48.2 5.51

WPX WPX ENERGY INC 14.1 -22.4 N/A -22.1 2.8

XLS EXELIS INC 9.75 9.7 N/A -14.3 1.82

XYL XYLEM INC 24.48 -4 N/A -6.9 4.54

Total Returns(%)*

Index Member@

Ticker Name Current Price Mrk Cap ($Bln)

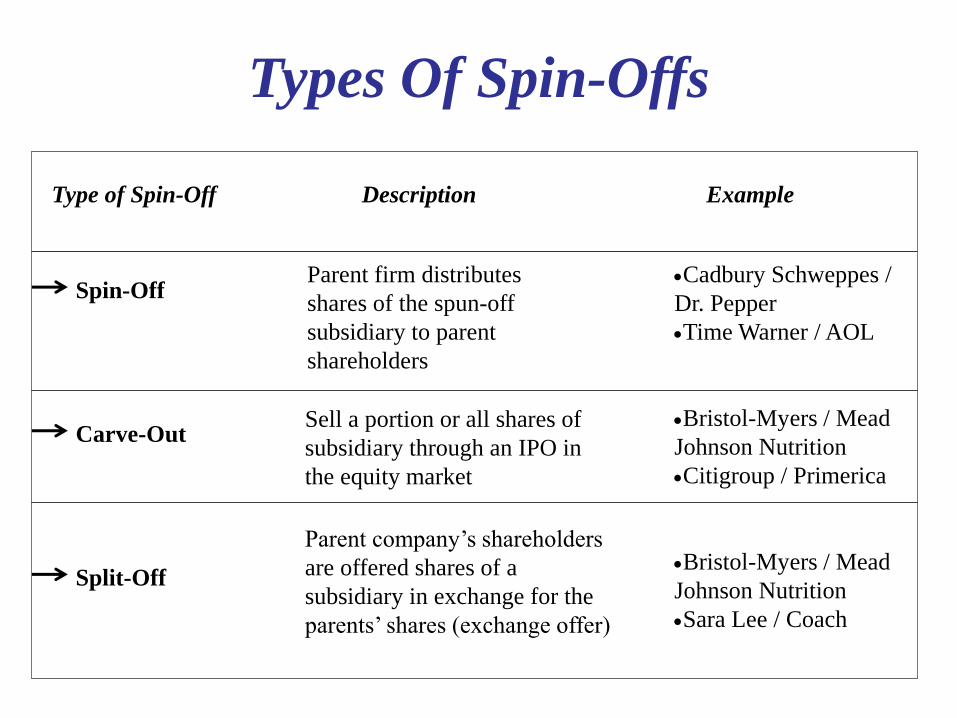

Types Of Spin-Offs

Type of Spin-Off

Spin-Off

Carve-Out

Split-Off

Description Example

Parent firm distributes

shares of the spun-off

subsidiary to parent

shareholders

Cadbury Schweppes /

Dr. Pepper

Time Warner / AOL

Bristol-Myers / Mead

Johnson Nutrition

Citigroup / Primerica

Bristol-Myers / Mead

Johnson Nutrition

Sara Lee / Coach

Sell a portion or all shares of

subsidiary through an IPO in

the equity market

Parent company’s shareholders

are offered shares of a

subsidiary in exchange for the

parents’ shares (exchange offer)

Spin-Off

• A parent distributes the stock of a subsidiary in

the form of a dividend

• Following the distribution, the stockholders hold

stock of the parent and the stock of the company

that was spun off

• Two independent companies exist where before

there was only one

• A spin-off effectively removes the parent from

management and control of the subsidiary

• Pure spins are tax efficient

Carve-Out

• Parent company sells some or all of the stock of

a subsidiary to the public in an IPO

• The carve-out may pay a portion of the IPO

proceeds to its parent

• Parent companies sometimes link subsidiary

IPOs and Spin-Offs (two step spin)

• Parent would typically sell less than 20% Of

subsidiary to the public and then distribute the

balance of the stock to their shareholders in a

tax-free distribution (Example: Bristol-Myers

Squibb / Mead Johnson Nutrition)

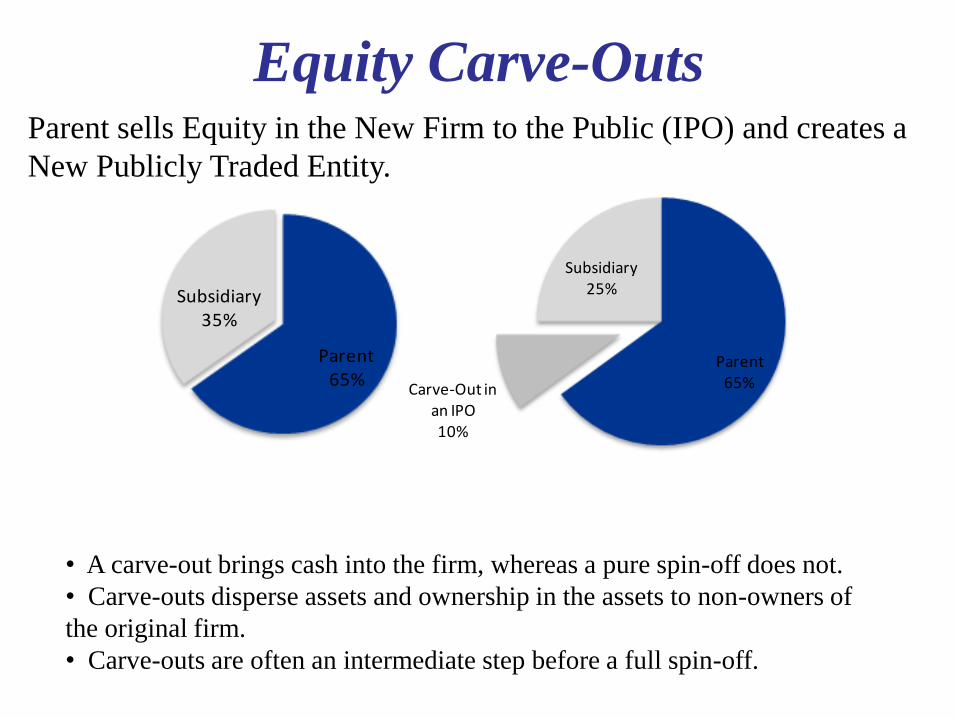

Equity Carve-Outs Parent sells Equity in the New Firm to the Public (IPO) and creates a

New Publicly Traded Entity.

Parent65%Carve-Out in

an IPO10%

Subsidiary25%

Parent65%

Subsidiary35%

• A carve-out brings cash into the firm, whereas a pure spin-off does not.

• Carve-outs disperse assets and ownership in the assets to non-owners of

the original firm.

• Carve-outs are often an intermediate step before a full spin-off.

Split-Offs

• In a split-off, the investor must decide between the new company and the parent.

• Holders of the parent company stock must choose to continue owning stock in the parent or, instead, exchange some or all of the parent stock for stock in the spin-off.

• The parent offers its existing shareholders stock in the subsidiary in exchange for shares in the parent company.

• If the parent distributes 80% of the subsidiary stock, the split is tax-free. What’s more, in an effort to induce enough shareholders to swap stock, investors are offered shares in the subsidiary that are worth more than the shares being returned to the parent company. This offered “premium” explains why split-offs are often oversubscribed.

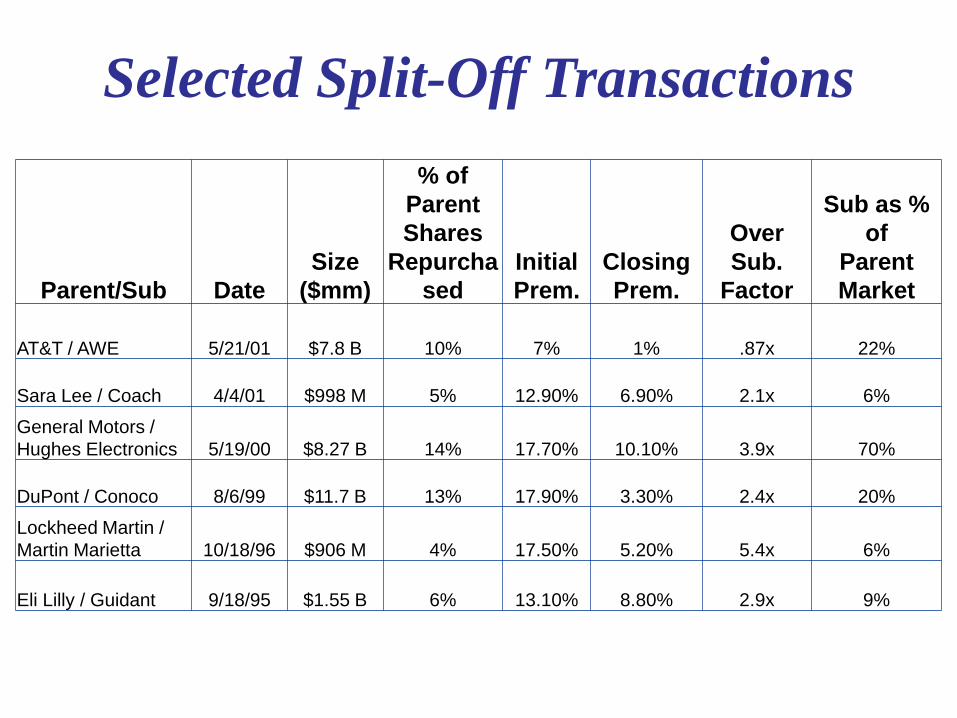

Selected Split-Off Transactions

Parent/Sub Date

Size

($mm)

% of

Parent

Shares

Repurcha

sed

Initial

Prem.

Closing

Prem.

Over

Sub.

Factor

Sub as %

of

Parent

Market

AT&T / AWE 5/21/01 $7.8 B 10% 7% 1% .87x 22%

Sara Lee / Coach 4/4/01 $998 M 5% 12.90% 6.90% 2.1x 6%

General Motors /

Hughes Electronics 5/19/00 $8.27 B 14% 17.70% 10.10% 3.9x 70%

DuPont / Conoco 8/6/99 $11.7 B 13% 17.90% 3.30% 2.4x 20%

Lockheed Martin /

Martin Marietta 10/18/96 $906 M 4% 17.50% 5.20% 5.4x 6%

Eli Lilly / Guidant 9/18/95 $1.55 B 6% 13.10% 8.80% 2.9x 9%

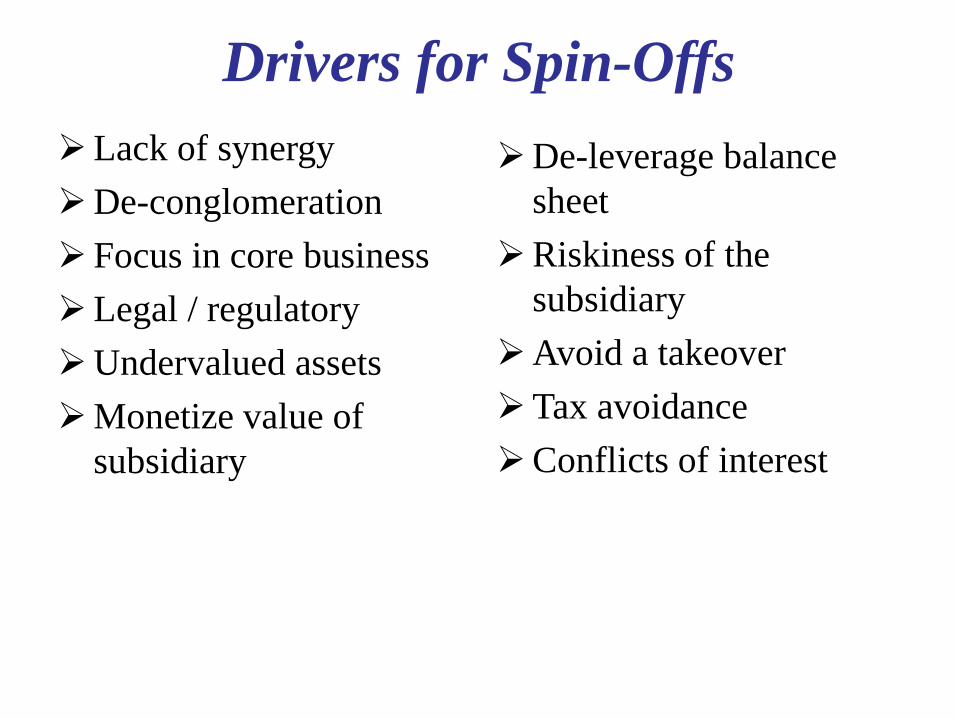

Drivers for Spin-Offs

Lack of synergy

De-conglomeration

Focus in core business

Legal / regulatory

Undervalued assets

Monetize value of

subsidiary

De-leverage balance

sheet

Riskiness of the

subsidiary

Avoid a takeover

Tax avoidance

Conflicts of interest

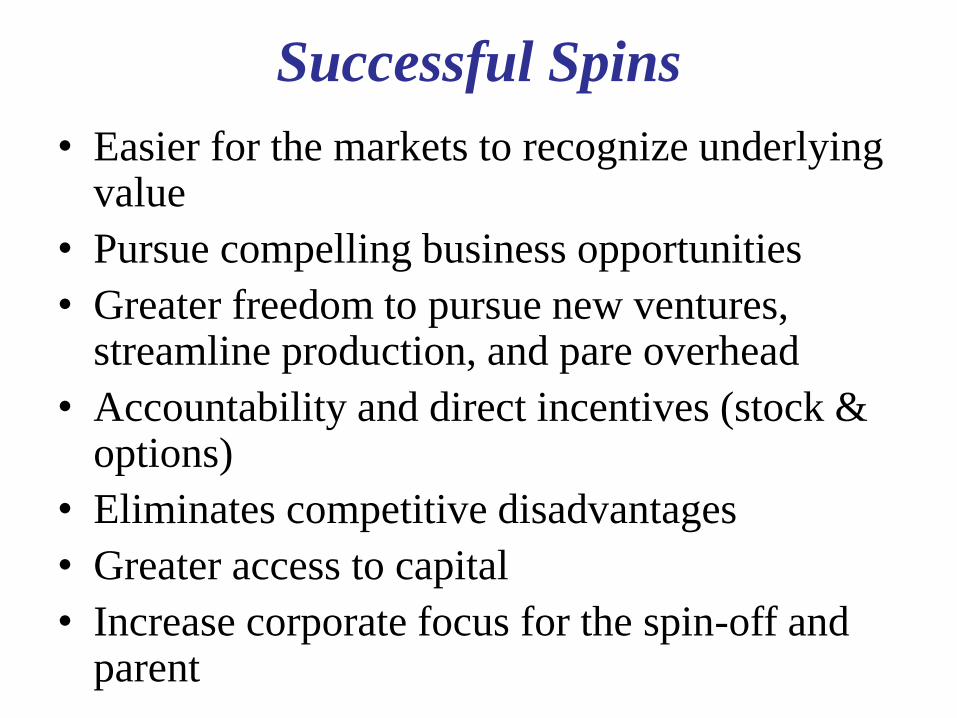

Successful Spins

• Easier for the markets to recognize underlying value

• Pursue compelling business opportunities

• Greater freedom to pursue new ventures, streamline production, and pare overhead

• Accountability and direct incentives (stock & options)

• Eliminates competitive disadvantages

• Greater access to capital

• Increase corporate focus for the spin-off and parent

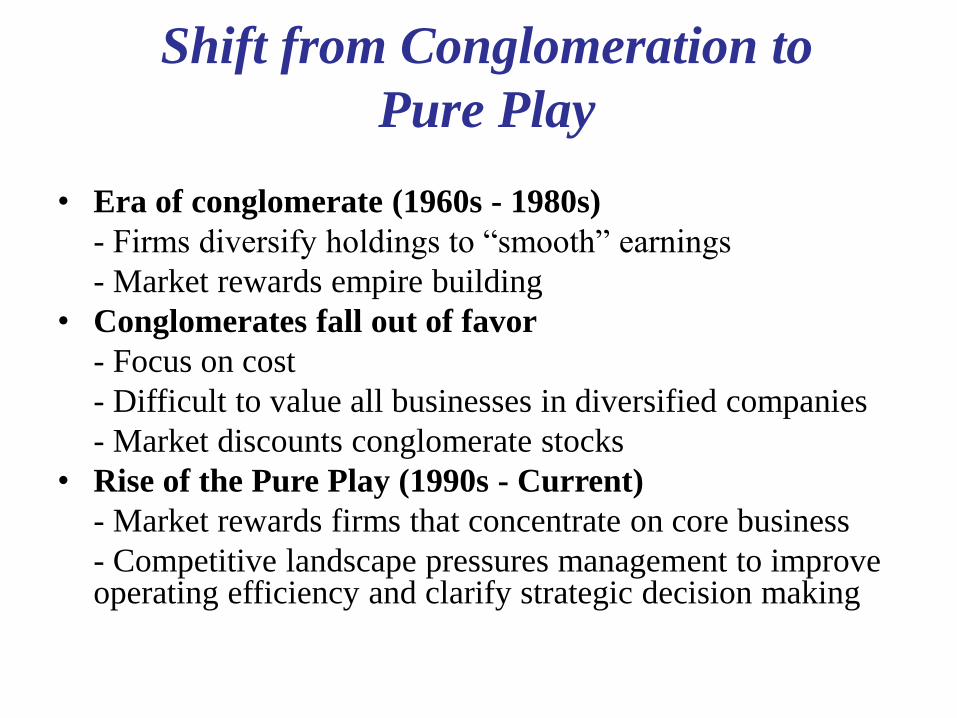

Shift from Conglomeration to

Pure Play

• Era of conglomerate (1960s - 1980s)

- Firms diversify holdings to “smooth” earnings

- Market rewards empire building

• Conglomerates fall out of favor

- Focus on cost

- Difficult to value all businesses in diversified companies

- Market discounts conglomerate stocks

• Rise of the Pure Play (1990s - Current)

- Market rewards firms that concentrate on core business

- Competitive landscape pressures management to improve operating efficiency and clarify strategic decision making

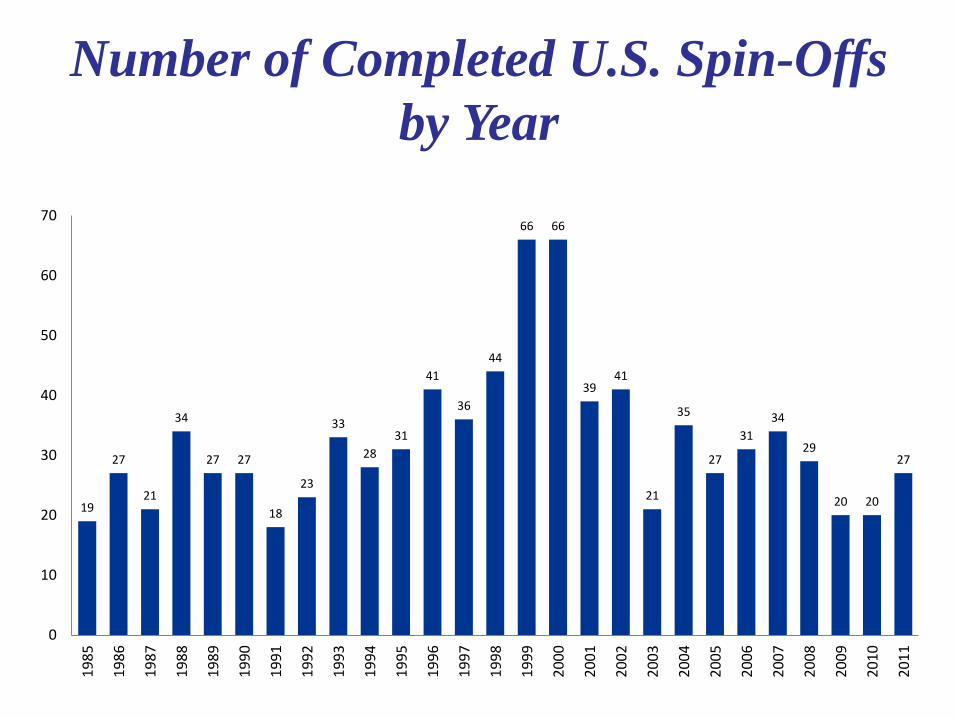

Number of Completed U.S. Spin-Offs

by Year

19

27

21

34

27 27

18

23

33

28

31

41

36

44

66 66

39 41

21

35

27

31

34

29

20 20

27

0

10

20

30

40

50

60

70

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11