29

© 2015 Environmental Risk Communications, Inc. Contact: John Rosengard (415) 336-5085 www.erci.com 2014 10K Reports on Environmental Liabilities - Trends March 2015

| Date post: | 27-Jul-2015 |

| Category: |

Environment |

| Upload: | john-rosengard |

| View: | 67 times |

| Download: | 3 times |

© 2015 Environmental Risk Communications, Inc.

Contact:

John Rosengard(415) 336-5085

www.erci.com

2014 10K Reports on EnvironmentalLiabilities - Trends

March 2015

© 2015 Environmental Risk Communications, Inc.

Outline for Today’s Webinar

Speaker’s Bio and Elevator Speech

Why Are Liability Disclosures Necessary?

What Will We See in Case Studies

Case Studies

ERCI Observations

Q&A

© 2015 Environmental Risk Communications, Inc.

Speaker Background: John Rosengard

Wrote Defender™ liability forecasting software package

Environmental remediation liabilities (ASC 410-30) Asset retirement obligations (ASC 410-20) Due diligence on acquisitions and divestitures Watch list for future reserve increases (sites &

portfolios) Decision analysis on individual sites Pollution remediation obligations (GASB49) Counterparty (PRP) default tracking

We support Corporate remediation groups PRP groups Port authorities The engineering/consulting and legal partners Their internal and external auditors

MBA, Northwestern; BS, Georgetown

John RosengardPresident & CEO, [email protected], CA

© 2015 Environmental Risk Communications, Inc.

Elevator Speech: 2014 10-K Review

ERCI internal R&D project; publicly-disclosed data only; 21 US-based companies, seven industries, 1995 to present.

ERCI Findings:

1. disclosures are not universal

2. divergence on form and substance

3. 17 of 18 companies show growing environmental liabilities from 1995 to 2015.

3.a More sites, more regulations, more assets.

3.b Plus…failed cleanups, reopeners, bankrupt PRPs.

4. ARO disclosure only improved after 2001’s FAS143 release

5. All 21 companies say they use “fair value measurement”…only metals/mining companies say they apply FVM to environmental liabilities

© 2015 Environmental Risk Communications, Inc.

Why Are Liability Disclosures Necessary?

Help a reasonable investor make better decisionsComply with GAAP:

FASB: ASC 410-20 [ARO], 410-30 [ERL], 440, 450, 460, 820 GASB: GASB Statements 18, 49, 72 IASB: IAS 37, IFRS 13 SEC Regulation S-K (17 CFR 210 to 230) Securities Act (1933) Securities Exchange Act (1934) Sarbanes-Oxley Act (2002) Dodd-Frank Act (2010): Title IX, Subtitle I PCAOB AU 336 (2011+) PCAOB Audit Standards 5, 12, 15 (2011+) ASTM E2137-06 Standard Guide for Estimating Monetary Costs and

Liabilities for Environmental Matters (2002, updated 2011) ASTM E2173-07 Standard Guide for Disclosure of Environmental

Liabilities (2002, updated 2011)

© 2015 Environmental Risk Communications, Inc.

Are Liability Disclosures Useful?

What an investor wants to know about environmental liabilities: Are the liability values true (ERL, ARO)?

Any recent or proposed acquisitions that can trigger surprises?

For operating facilities, will an industry downturn or contraction lead to more liabilities?

If we exit a business, are we ready? For divested facilities, can any come back to

us? Are the reserves trending up, down, or

sideways? Do we differ substantially from our peer

companies? Why?

Recognition

Measurement

Presentation

Disclosure

Elements of Financial

Statements

Investor only sees this

© 2015 Environmental Risk Communications, Inc.

FASB: Where Do Disclosures Fit In?

Source: FASB Statement of Financial Accounting Concepts No. 8, September 2010

Enhancing Qualitative

CharacteristicsFundamental Qualitative

Characteristics

Objective of Financial Reporting

Information

Useful to Decisions

Relevant

Predictive value

Confirmatory value

Faithful Representation

Complete

Neutral

Free from error

Elements of Financial

Statements

Comparability

Verifiability

Timeliness

Understandability

Recognition

Measurement

Presentation

Disclosure

Cost Constraint

Materiality Constraint

GAAP Conceptual Framework

© 2015 Environmental Risk Communications, Inc.

What Does ERCI See in 10-K Reports?

Minimal metrics: accrued, spent, balance for 2-3 years

Cautionary statements, policy statements

Jargon

“Charged to expense”…means “reserve increase”

“Accretion”…means rolling the present value forward a year

Reductive reasoning/oversimplification (“Reserve minus spending equals remaining liability; we always get exactly 100 cents of value for all spending”)

Recursive reasoning (“the reserve balance is the liability; the liability is the reserve”)

Inductive reasoning (“CERCLA and RCRA cause our liabilities; without notice of violation, liability is therefore zero”)

© 2015 Environmental Risk Communications, Inc.

Detailed vs. Minimal Disclosure

Chevron 2014 10-KExcerpts

The company records asset retirement obligations when there is a legal obligation associated with the retirement of long-lived assets and the liability can be reasonably estimated. These asset retirement obligations include costs related to environmental issues. The liability balance of approximately $15.1 billion for asset retirement obligations at year-end 2014 related primarily to upstream properties. For the company’s other ongoing operating assets, such as refineries and chemicals facilities, no provisions are made for exit or cleanup costs that may be required when such assets reach the end of their useful lives unless a decision to sell or otherwise abandon the facility has been made, as the indeterminate settlement dates for the asset retirements prevent estimation of the fair value of the asset retirement obligation. Refer to the discussion below for additional information on environmental matters and their impact on Chevron, and on the company's 2014 environmental expenditures. Refer to Note 23 on pages FS-57 through FS-59 for additional discussion of environmental remediation provisions and year-end reserves. Refer also to Note 24 on page FS-59 for additional discussion of the company's asset retirement obligations.

General Electric2014 10-KExcerpts

Our operations, like operations of other companies engaged in similar businesses, involve the use, disposal and cleanup of substances regulated under environmental protection laws. We are involved in a number of remediation actions to clean up hazardous wastes as required by federal and state laws. Such statutes require that responsible parties fund remediation actions regardless of fault, legality of original disposal or ownership of a disposal site. Expenditures for site remediation actions amounted to approximately $0.4 billion in each of the years 2014, 2013 and 2012. We presently expect that such remediation actions will require average annual expenditures of about $0.4 billion in 2015 and $0.3 billion in 2016.

We are involved in numerous remediation actions to clean up hazardous wastes as required by federal and state laws. Liabilities for remediation costs exclude possible insurance recoveries and, when dates and amounts of such costs are not known, are not discounted. When there appears to be a range of possible costs with equal likelihood, liabilities are based on the low end of such range. It is reasonably possible that our environmental remediation exposure will exceed amounts accrued. However, due to uncertainties about the status of laws, regulations, technology and information related to individual sites, such amounts are not reasonably estimable. Total reserves related to environmental remediation and asbestos claims, were $2,182 million at Dec 31, 2014.

Environmental Remediation Reserves 2014 2013 2012

Balance at January 1 $ 1,456 $ 1,403 $ 1,404

Net Additions $ 636 $ 488 $ 428

Expenditures $ (409) $ (435) $ (429)

Balance at December 31 $ 1,683 $ 1,456 $ 1,403

Asset Retirement Obligations 2014 2013 2012

Balance at January 1 $ 14,298 $ 13,271 $ 12,767

Liabilities incurred $ 133 $ 59 $ 133

Liabilities settled $ (1,291) $ (907) $ (966)

Accretion expense $ 882 $ 627 $ 629

Revisions in estimated cash f low s $ 1,031 $ 1,248 $ 708

Balance at December 31 $ 15,053 $ 14,298 $ 13,271

© 2015 Environmental Risk Communications, Inc.

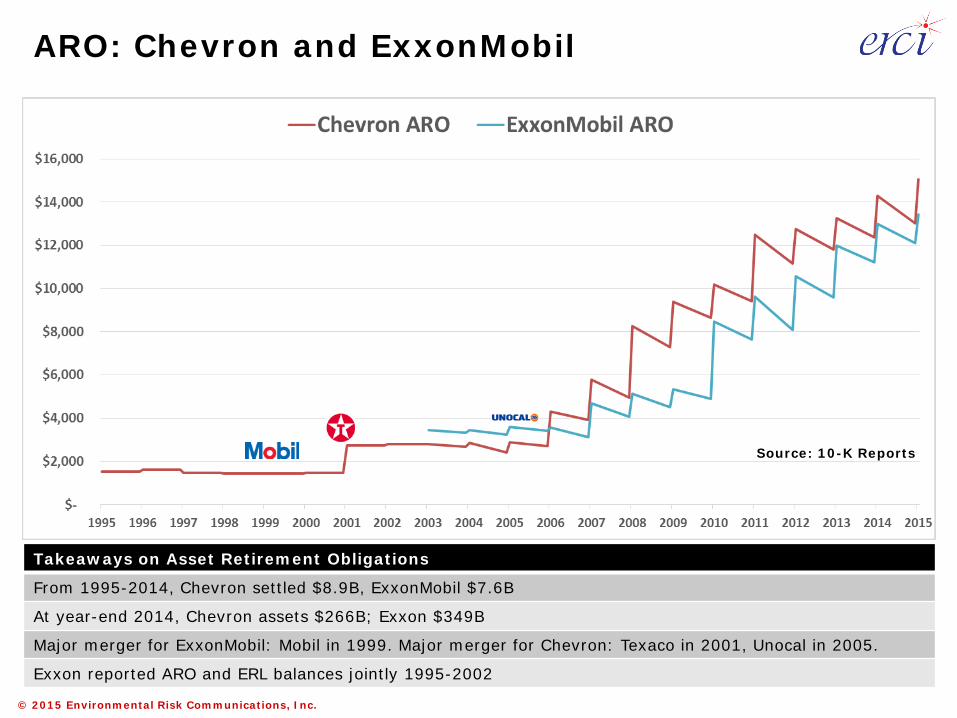

Source: 10-K Reports

Case Studies: Chevron and ExxonMobil

Takeaways on Environmental Remediation Liabilities

From 1995-2014, Chevron spent $6.5B, ExxonMobil $6.4B

At year-end 2014, Chevron assets $266B; Exxon $349B

Major merger for ExxonMobil: Mobil in 1999. Major merger for Chevron: Texaco in 2001, Unocal in 2005.

Exxon reported ARO and ERL balances jointly 1995-2002

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ARO: Chevron and ExxonMobil

Takeaways on Asset Retirement Obligations

From 1995-2014, Chevron settled $8.9B, ExxonMobil $7.6B

At year-end 2014, Chevron assets $266B; Exxon $349B

Major merger for ExxonMobil: Mobil in 1999. Major merger for Chevron: Texaco in 2001, Unocal in 2005.

Exxon reported ARO and ERL balances jointly 1995-2002

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Honeywell and Boeing

Takeaways on Environmental Remediation Liabilities

From 2006-2014, Honeywell spent $2.6B, Boeing $1B

At year-end 2014, Honeywell assets $45B; Boeing $99B

Major merger for Honeywell: AlliedSignal in 1999. Major merger for Boeing: McDonnell Douglas in 1997.

Boeing did not disclose environmental remediation liabilities before 2006.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Dow and DuPont

Takeaways on Environmental Remediation Liabilities

From 1995-2014, Dow spent $2.4B, DuPont $1.5B

At year-end 2014, Dow assets $69B; DuPont $50B

Major Dow mergers: Union Carbide in 2001, Rohm and Haas in 2009.

Major DuPont divestiture: Conoco 1998.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Valero and Tesoro

Takeaways on Environmental Remediation Liabilities

From 1995-2014, Valero spent $526M, Tesoro $303M

At year-end 2014, Valero assets $46B; Tesoro $17B

Major Valero mergers: UDS in 2001, Premcor in 2005.

Major Tesoro acquisitions: six refineries 1998-2013.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Duke, PG&E and Exelon

Takeaways on Environmental Remediation Liabilities

From 2010-2014, Duke increased reserves by $140M, PG&E $368M, Exelon $164M; no spend disclosed.

At year-end 2014, Duke assets $80B; PG&E $60B, Exelon $87B.

Major Duke mergers: Cinergy in 2005, Progress in 2012.

Exelon mergers: Unicom in 1999, Constellation in 2012, Pepco Holdings is pending. PG&E had no mergers.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K ReportsARO: Duke, PG&E and Exelon

Takeaways on Asset Retirement Obligations

Each of the three displayed have nuclear decommissioning funds

At year-end 2014, Duke assets $80B; PG&E $60B, Exelon $87B.

Major Duke mergers: Cinergy in 2005, Progress in 2012. Exelon mergers: Unicom in 1999, Constellation in 2012, Pepco Holdings is pending. PG&E had no mergers.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Republic Services & Waste Mgmt

Takeaways on Environmental Remediation Liabilities

From 2002-2014, Republic spent $558M, Waste Management spent $458M.

At year-end 2014, Republic assets $20B; Waste Management $21B.

Major Republic events: IPO in 1998, Allied merger in 2008. Waste Management mergers: USA Waste in 1998.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ARO: Republic Services & Waste Mgmt

Takeaways on Asset Retirement Obligations

From 2002-2014, Republic settled $637M of their AROs, Waste Management settled $938M.

At year-end 2014, Republic assets $20B; Waste Management $21B.

FASB 143 covering asset retirement obligations took effect after June 2002.

Numbers above exclude financial guarantees and financial assurance to State and Federal Agencies

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: KinderMorgan & Enterprise Products

Takeaways on Environmental Remediation Liabilities

From 2002-2014, KinderMorgan spent an undisclosed amount, Enterprise Products spent over $88M.

At year-end 2014, KinderMorgan assets $83B; Enterprise Products $47B.

Major KinderMorgan events: El Paso merger in 2012.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ARO: KinderMorgan & Enterprise Products

Takeaways on Asset Retirement Obligations

From 2002-2014, KinderMorgan settled $30M of their AROs, Enterprise Products settled $90M.

At year-end 2014, KinderMorgan assets $83B; Enterprise Products $47B.

Major KinderMorgan events: El Paso merger in 2012.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ERL: Newmont, Freeport and Alcoa

Takeaways on Environmental Remediation Liabilities

From 1995-2014, Newmont spent $334M, Freeport $949M and Alcoa spent $920M.

At year-end 2014, Newmont had $25B of assets, Freeport $59B, and Alcoa $37B.

Over 1995-2014, Newmont completed six mergers/acquisitions. Freeport acquired Phelps Dodge (2007), Plains E&P (2013) and McMoRan Exploration (2013). Alcoa acquired Reynolds in 2000.

© 2015 Environmental Risk Communications, Inc.

Source: 10-K Reports

ARO: Newmont, Freeport and Alcoa

Takeaways on Asset Retirement Obligations

From 2002-2014, Newmont settled $738M of their AROs, Freeport $560M, and Alcoa $635M.

At year-end 2014, Newmont had $25B of assets, Freeport $59B, and Alcoa $37B.

Over 1995-2014, Newmont completed six mergers/acquisitions. Freeport acquired Phelps Dodge (2007), Plains E&P (2013) and McMoRan Exploration (2013). Alcoa acquired Reynolds in 2000.

Numbers above exclude financial guarantees and financial assurance to State and Federal Agencies

© 2015 Environmental Risk Communications, Inc.

Chevron

ExxonMobil Honeywell

Boeing

Dow

DuPont

Valero

Tesoro

Duke Republic Services

Waste Management

Enterprise Products

0

2

4

6

8

10

12

2010 2011 2012 2013 2014

How Long Will an ERL Balance Last?YE

ARS

Takeaway: this is the price of using “probable and reasonably estimable”: no reliable or consistent duration

© 2015 Environmental Risk Communications, Inc.

Chevron

ExxonMobil Honeywell

Boeing

Dow

DuPont

Valero

Tesoro

Duke PG&E

Exelon

Republic Services

Kinder Morgan

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2010 2011 2012 2013 2014

Will Environmental Reserve Increases End?an

nual

res

erve

incr

ease

Takeaway: not in the near future….

© 2015 Environmental Risk Communications, Inc.

Outliers during the past twenty years: Only DuPont reduced their environmental liability balance Only Chevron notes the use of counterparty risk data in

forecasts Fair value is not being applied to ERLs…yet. Reserves and AROs are typically replenished (annually) at

rates from 80-120% of current year spending. Anecdotal justification for reserve increases:

Existing sites progressing from study to remedial design, then to remediation to OM&M (including five-year reviews)

New sites, AOCs, pathways (NPL listing, litigation, contractual, counterparty default, vapor intrusion)

Acquisitions initially adding their environmental reserves Acquisitions later “trued up” with acquirer’s policies PRPs defaulting on their allocations Changing cleanup goals

ERCI Observations

© 2015 Environmental Risk Communications, Inc.

If the ERLs were $439M annuities paying $79.6M/yr, they would be yielding 18% (!).

Use a lower discount rate instead, the liability shifts up:

Takeaway: “probably and reasonably estimable” liability balances are not consistent with PV of historical spend

Takeaway: adjust for inflation, distortion worsens

Are Reserve Balances Too Low?

Discount rate justification Discount rate Liability Value“probable and reasonably estimable”

$79.6M/$439M= 18.13%

$439M

NYSE – Price/Earnings Multiplier of 19 (March 2015)

5.27% $1,511M

DuPont pension plan (2014) 4.55% $1,749MDuPont’s cost of LT debt (2015) 2.43% $3,276M

DuPont 2010-2014 1995-2014ERL Spending/year $79.6M $75.4MERL Balance (avg) $439M $422MShelf life (years) =439/79.6 = 5.5 =422/75.4 = 5.6

© 2015 Environmental Risk Communications, Inc.

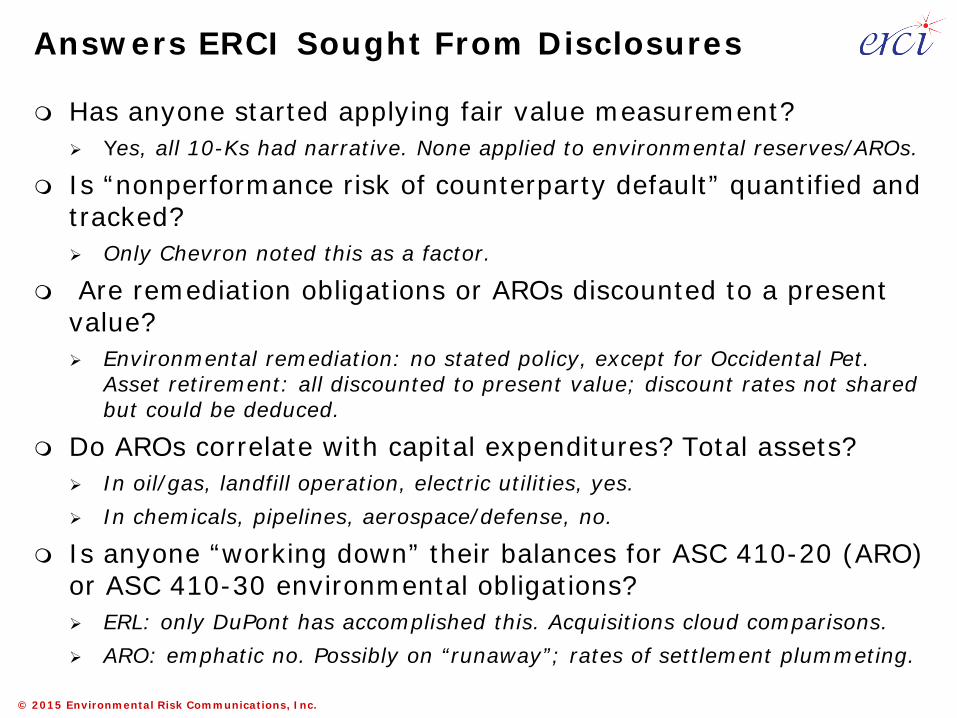

Has anyone started applying fair value measurement? Yes, all 10-Ks had narrative. None applied to environmental reserves/AROs.

Is “nonperformance risk of counterparty default” quantified and tracked? Only Chevron noted this as a factor.

Are remediation obligations or AROs discounted to a present value? Environmental remediation: no stated policy, except for Occidental Pet.

Asset retirement: all discounted to present value; discount rates not shared but could be deduced.

Do AROs correlate with capital expenditures? Total assets? In oil/gas, landfill operation, electric utilities, yes. In chemicals, pipelines, aerospace/defense, no.

Is anyone “working down” their balances for ASC 410-20 (ARO) or ASC 410-30 environmental obligations? ERL: only DuPont has accomplished this. Acquisitions cloud comparisons. ARO: emphatic no. Possibly on “runaway”; rates of settlement plummeting.

Answers ERCI Sought From Disclosures

© 2015 Environmental Risk Communications, Inc.

Resources to Read

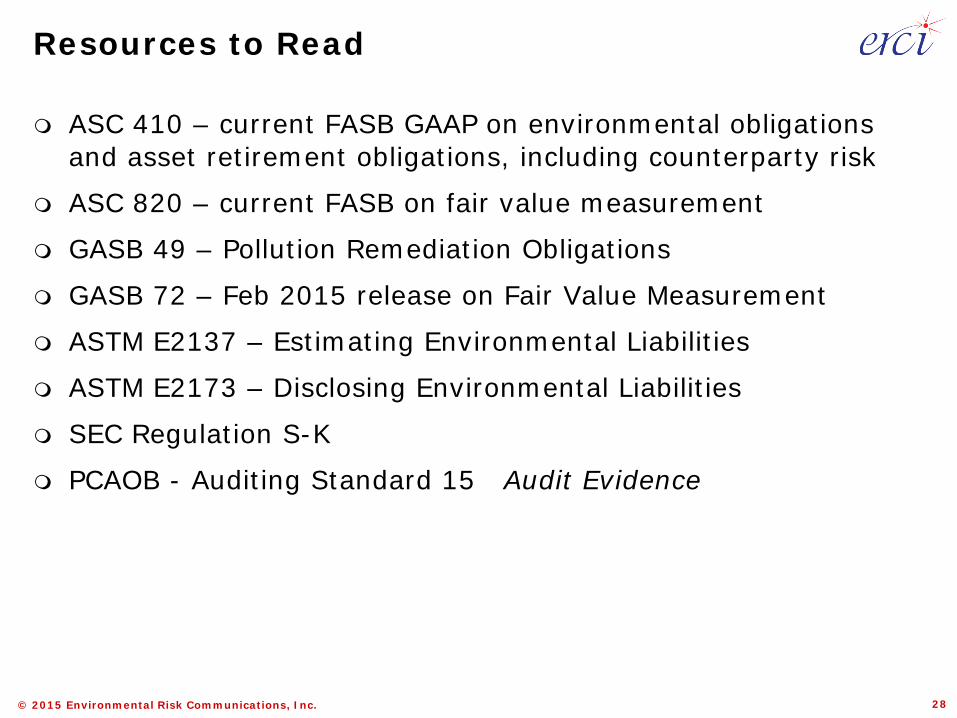

ASC 410 – current FASB GAAP on environmental obligations and asset retirement obligations, including counterparty risk

ASC 820 – current FASB on fair value measurement

GASB 49 – Pollution Remediation Obligations

GASB 72 – Feb 2015 release on Fair Value Measurement

ASTM E2137 – Estimating Environmental Liabilities

ASTM E2173 – Disclosing Environmental Liabilities

SEC Regulation S-K

PCAOB - Auditing Standard 15 Audit Evidence

28

© 2015 Environmental Risk Communications, Inc.

Next Steps

Website: www.erci.com

LinkedIn Group – webinar announcements

YouTube page – select webinar recordings

Email [email protected] or call me at (415) 336-5085 PDF of this presentation (original PPTX format on request)

March 2015 webinars on Managing Nonperformance Risk of Environmental Counterparties Obstacles to Recognizing and Measuring Environmental Liabilities

April 2015 webinars on Estimating and Disclosing Environmental Liabilities Auditor’s Tough Questions on Environmental Liabilities Calculating Counterparty Risk on Environmental Liabilities

29