107

The Economy is Safe, But a Wild Ride Ahead Stephen Slifer NumberNomics www.NumberNomics.com

| Date post: | 13-Jul-2015 |

| Category: |

Real Estate |

| Upload: | charleston-trident-association-of-realtors |

| View: | 815 times |

| Download: | 0 times |

The Economy is Safe,But a Wild Ride Ahead

Stephen SliferNumberNomicswww.NumberNomics.com

The Highlights

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

2. Housing. Shift from owning to renting.

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

2. Housing. Shift from owning to renting.

3. Labor Market. On a roll.

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

2. Housing. Shift from owning to renting.

3. Labor Market. On a roll.

4. Inflation about to rise. Sea change in oil market.

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

2. Housing. Shift from owning to renting.

3. Labor Market. On a roll.

4. Inflation about to rise. Sea change in oil market.

5. Rates to rise by midyear. Fundamental shift by Fed.

The Highlights1. GDP growth moderate: 2.8% -- 2014; 3.4% -- 2015.

2. Housing. Shift from owning to renting.

3. Labor Market. On a roll.

4. Inflation about to rise. Sea change in oil market.

5. Rates to rise by midyear. Fundamental shift by Fed.

6. No recession until 2018 at the earliest.

Consumption60%

Government15.0%

Trade10.0%

Investment15%

GDP Components

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

Jan

20

07

Ap

r 2

00

7

Jul 2

00

7

Oct

20

07

Jan

20

08

Ap

r 2

00

8

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

00

9

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

01

0

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

01

1

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

01

2

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

01

3

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

01

4

Jul 2

01

4

Oct

20

14

Jan

20

15

Consumer Sentiment

Recession

Confidence is at its highest level for the cycle.

That confidence is justified.

$40.0

$45.0

$50.0

$55.0

$60.0

$65.0

$70.0

$75.0

$80.0Consumer Net Worth

Consumer net worth is at a record highlevel which is 20% higher than its prior peakand is growing at a double-digit pace.

It is being driven by a combination ofa rising stock market and increases in home prices.

600

800

1000

1200

1400

1600

1800

2000 S&P 500The stock market is close to a record high level.

The stock market gains reflect a steadyincrease in corporate profits.

10

30

50

70

90

110

130

Jan2000

Jan2001

Jan2002

Jan2003

Jan2004

Jan2005

Jan2006

Jan2007

Jan2008

Jan2009

Jan2010

Jan2011

Jan2012

Jan2013

Jan2014

Jan2015

P/E Ratio -- S&P 500

The relationship between stock pricesand earnings is roughly in line withits average for the past 15 years.

It is hard to argue that the stock market issignificantly overvalued.

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

-2.7%

-1.7%

-0.7%

0.3%

1.3%

2.3%

Home Prices

Year-Over-Year (R)

Case Shiller Home Price Index

Home prices continue to climb which furtherbolsters net worth.

14.5

15.0

15.5

16.0

16.5

17.0

17.5

18.0

18.5

Financial Obligations Ratio

Trend

Consumer debt in relation to income isthe lowest it has been since the 1980’s.

We have the ability to pick up the paceof spending if they choose to do so.

2.9

3.9

4.9

5.9

6.9

7.9

8.9

9.9

10.9

Jan

-90

Oct

-90

Jul-

91

Ap

r-9

2

Jan

-93

Oct

-93

Jul-

94

Ap

r-9

5

Jan

-96

Oct

-96

Jul-

97

Ap

r-9

8

Jan

-99

Oct

-99

Jul-

00

Ap

r-0

1

Jan

-02

Oct

-02

Jul-

03

Ap

r-0

4

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

30-year Mortgage Rate

While 30-year mortgage rates have risen almost 0.5% sinceJune 2013 to 4.0% they are essentially the lowest rates in 50 years.

-900

-700

-500

-300

-100

100

300

500

Jan

-05

Ap

r-0

5

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Private Employment

Private Employ.

3-mo. average

Jobs rising by 275 thousand per month.

As good as it gets.

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Unemployment Rate

Full Employment

The unemployment rate has fallento 5.6% which was much more quicklythan anyone expected.

$2.00

$2.50

$3.00

$3.50

$4.00

Gasoline Prices

Gasoline prices have declined by 33% sincelat summer.

The money saved can be spent on othergoods and services.

1. Stock market climb boosts confidence.

2. Net worth is at a record high level.

3. Debt burden is quite comfortable.

4. Jobs growth is robust.

5. Unemployment rate low.

6. Gas prices have fallen dramatically.

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

Consumption spending

Year-over-Year

Consumption Spending (%)

For all of these reasons we expect consumerspending to pick up to 3.0% in 2015.

What is the Outlook for Housing?

500

700

900

1100

1300

1500

1700

1900

Jan 2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015

Housing Starts

Trend

Housing StartsWe need 1.3 million new homes or apartmentseach year to keep pace with population.

Builders are only providing about1.0 million.

Demand continues to outpace supply.

Starts should climb to 1.3 million by endof this year.

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

Jan

20

09

Mar

20

09

May

20

09

Jul 2

00

9

Sep

20

09

No

v 2

00

9

Jan

20

10

Mar

20

10

May

20

10

Jul 2

01

0

Sep

20

10

No

v 2

01

0

Jan

20

11

Mar

20

11

May

20

11

Jul 2

01

1

Sep

20

11

No

v 2

01

1

Jan

20

12

Mar

20

12

May

20

12

Jul 2

01

2

Sep

20

12

No

v 2

01

2

Jan

20

13

Mar

20

13

May

20

13

Jul 2

01

3

Sep

20

13

No

v 2

01

3

Jan

20

14

Mar

20

14

May

20

14

Jul 2

01

4

Sep

20

14

No

v 2

01

4

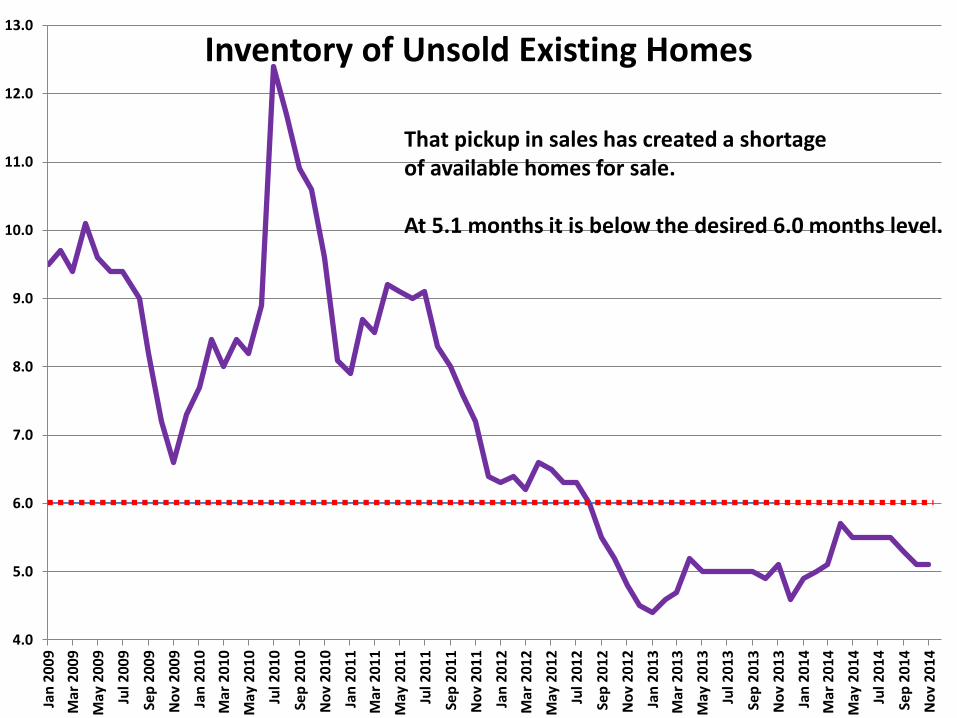

Inventory of Unsold Existing Homes

That pickup in sales has created a shortageof available homes for sale.

At 5.1 months it is below the desired 6.0 months level.

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

1980:Q1 1985:Q1 1990:Q1 1995:Q1 2000:Q1 2005:Q1 2010:Q1

Homeownership Rates

Even though the demand for homes has beenstrong, homeownership has been fallingfor a decade. Why?

It rose dramatically in the mid-1990’s.in response to the “Affordable HousingAct”.

When the bubble burst many peoplelost their homes and were forcedto rent.

$20,000

$70,000

$120,000

$170,000

$220,000

$270,000

Jan 1970 Jan 1975 Jan 1980 Jan 1985 Jan 1990 Jan 1995 Jan 2000 Jan 2005 Jan 2010

New Home Prices

Home prices had been rising steadily since the 1970’s

A sure bet. You could not lose.

But “The Great Recession people learned that housingIs not a sure bet. Home prices can also fall.

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

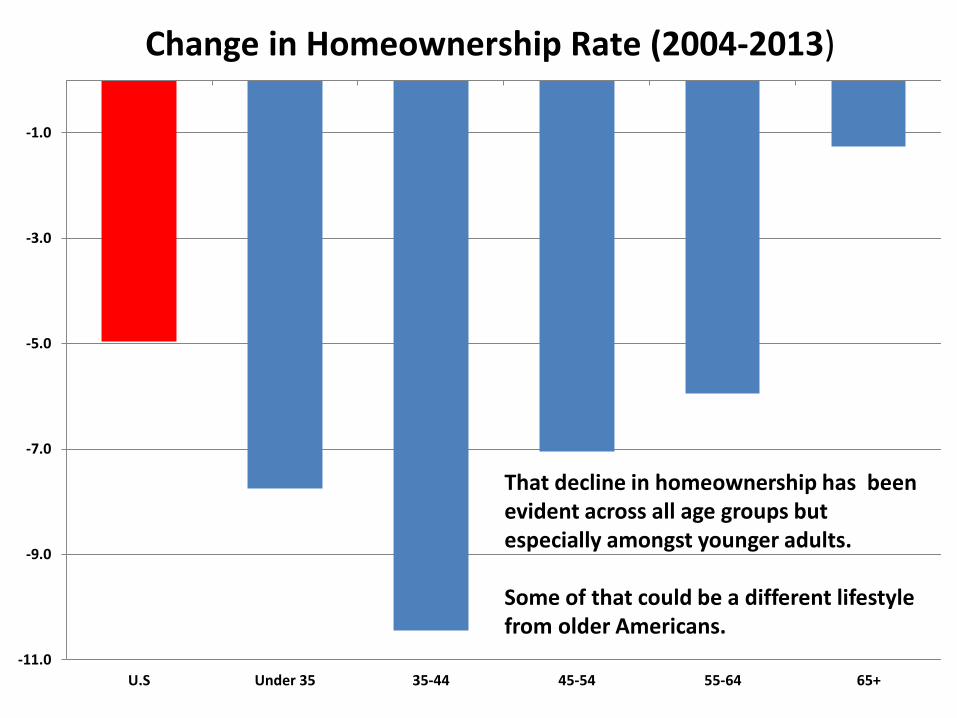

U.S Under 35 35-44 45-54 55-64 65+

Change in Homeownership Rate (2004-2013)

That decline in homeownership has beenevident across all age groups butespecially amongst younger adults.

Some of that could be a different lifestylefrom older Americans.

600

650

700

750

800

850

900

Au

g 2

009

Oct

20

09

Dec

20

09

Feb

20

10

Ap

r 2

010

Jun

20

10

Au

g 2

010

Oct

20

10

Dec

20

10

Feb

20

11

Ap

r 2

011

Jun

20

11

Au

g 2

011

Oct

20

11

Dec

20

11

Feb

20

12

Ap

r 2

012

Jun

20

12

Au

g 2

012

Oct

20

12

Dec

20

12

Feb

20

13

Ap

r 2

013

Jun

20

13

Au

g 2

013

Oct

20

13

Dec

20

13

Feb

20

14

Ap

r 2

014

Jun

20

14

Au

g 2

014

Oct

20

14

Monthly Payment RequiredSince early 2013 home prices have climbed and rates have risen:

Down payment has increased from $34,0000 to $42,000Monthly payments have risen from $600 to $825.

Younger borrowers, particularly ones with student debt,are having a hard time qualifying for a mortgage.

4.5

5.5

6.5

7.5

8.5

9.5

10.5Rental Vacancy Rate

As a result, they are turning to rentals.

The rental vacancy rate is the lowestit has been in 20 years.

525

725

925

1125

1325

1525

1725

1925

Jan 2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015

Housing Starts

Trend

Housing Starts

Starts should climb to 1.3 million by endof next year.

But multi-family starts will climb farmore rapidly than single-family.

50

150

250

350

450

550

650

750

850Ja

n 2

00

8

Jul 2

00

8

Jan

20

09

Jul 2

00

9

Jan

20

10

Jul 2

01

0

Jan

20

11

Jul 2

01

1

Jan

20

12

Jul 2

01

2

Jan

20

13

Jul 2

01

3

Jan

20

14

Jul 2

01

4

Jan

20

15

Jul 2

01

5

Single Family

Multi-family

Single vs. Multi-Family Starts

Single-family starts will grow at about a 20% pace

Multi-family starts will climb at about a 45% pace.

Let’s Talk Jobs

-900

-700

-500

-300

-100

100

300

500

Jan

-05

Ap

r-0

5

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Private Employment

Private Employ.

3-mo. average

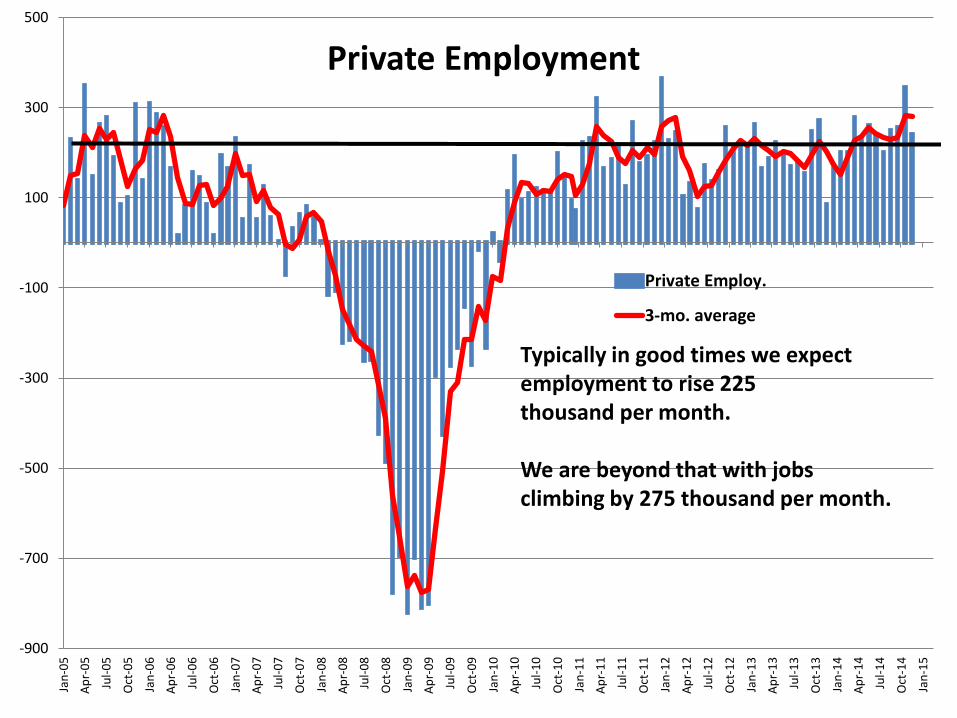

Typically in good times we expectemployment to rise 225thousand per month.

We are beyond that with jobs climbing by 275 thousand per month.

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Unemployment Rate

Full Employment

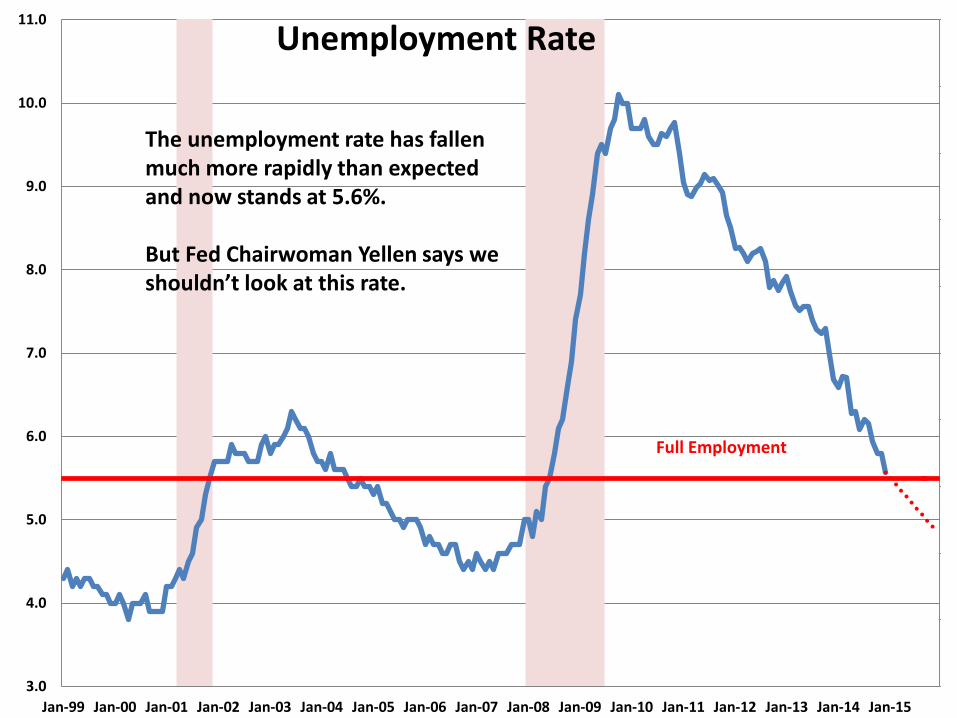

The unemployment rate has fallenmuch more rapidly than expectedand now stands at 5.6%.

But Fed Chairwoman Yellen says weshouldn’t look at this rate.

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

Jan 1970 Jan 1973 Jan 1976 Jan 1979 Jan 1982 Jan 1985Jan 1988 Jan 1991 Jan 1994 Jan 1997 Jan 2000 Jan 2003 Jan 2006 Jan 2009 Jan 2012 Jan 2015

Participation Rate

She claims that the unemployment rate isbiased downwards because a growing numberof “discouraged workers” have given upup looking for a job and are no longer“participating” in the labor force.

But that is not entirely accurate.

200

400

600

800

1000

1200

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

Discouraged Workers

The number of “discouragedworkers” is getting smaller, not bigger.

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

Jan 1970 Jan 1973 Jan 1976 Jan 1979 Jan 1982 Jan 1985Jan 1988 Jan 1991 Jan 1994 Jan 1997 Jan 2000 Jan 2003 Jan 2006 Jan 2009 Jan 2012 Jan 2015

Participation Rate

Furthermore, the decline in the participationrate began in 2000 – long before the recessionbegan.

Something else is happening.

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

Jan 1970 Jan 1973 Jan 1976 Jan 1979 Jan 1982 Jan 1985Jan 1988 Jan 1991 Jan 1994 Jan 1997 Jan 2000 Jan 2003 Jan 2006 Jan 2009 Jan 2012 Jan 2015

Participation Rate

The participation rate rose in the 1970-1980’sas the baby boomers entered the labor force.

As the baby boomers retire the participation ratewill continue to decline (2011-2029).

About 2/3 of the recent drop is attributable tobaby boomers and is simply a function of demographics.

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Broad vs. Official Unemployment RateYellen says we are supposed to be watchingthe broad unemployment rate because it includesboth unemployed workers and those who are“underemployed” .

Underemployed workers include :Ones who have given up looking for a job,Ones who are working part time but wouldlike a full time position.

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Broad vs. Official Unemployment Rate

The broad rate is always much higher thanthe official rate. It is a different measure.It averages 80% higher than the official rate.

If full employment for the official rate is 5.5%then full employment for the broad measureshould be about 10.0%.

The broad rate today is 11.2%.

200

400

600

800

1000

1200

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

Discouraged Workers

Going forward the number of “discouragedworkers” will keep getting smaller, not bigger.

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

19.5%

20.0%

20.5%

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

Part Time -- % Total

As the economy gathers momentumsome of those time workers will likelybe offered full time positions.

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Broad vs. Official Unemployment Rate

Full Employment

Full Employment

By mid-2015 both unemploymentrates will be close to full employment.

1.5

2.0

2.5

3.0

3.5

4.0

Jan

20

07

Ap

r 2

007

Jul 2

00

7

Oct

20

07

Jan

20

08

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

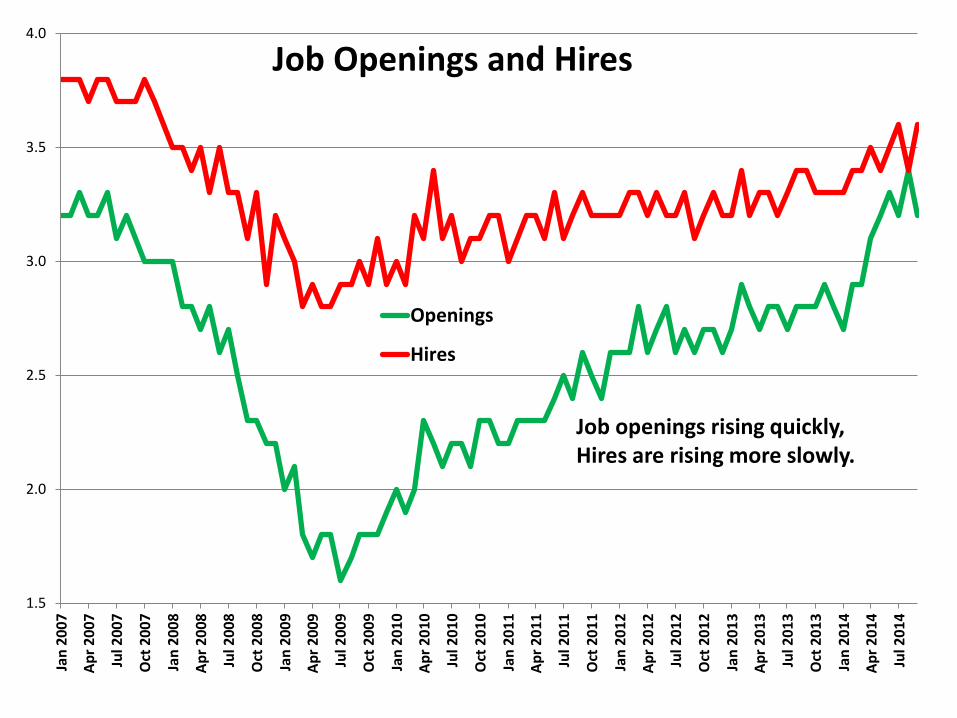

Job Openings and Hires

Openings

Hires

Job openings rising quickly,Hires are rising more slowly.

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

Dec 2000Dec 2001Dec 2002Dec 2003Dec 2004Dec 2005Dec 2006Dec 2007Dec 2008Dec 2009Dec 2010Dec 2011Dec 2012Dec 2013

Openings /Hires Ratio

Plenty of jobs out there. Workers do not have the skills required for the jobs that are available.

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

Dec 2000Dec 2001Dec 2002Dec 2003Dec 2004Dec 2005Dec 2006Dec 2007Dec 2008Dec 2009Dec 2010Dec 2011Dec 2012Dec 2013

Openings /Hires Ratio

That is why the long-term unemployed workers, part timers, and young adultsare having such a hard time.

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

Dec 2000Dec 2001Dec 2002Dec 2003Dec 2004Dec 2005Dec 2006Dec 2007Dec 2008Dec 2009Dec 2010Dec 2011Dec 2012Dec 2013

Openings /Hires Ratio

Our colleges and universities are trying to fill that gap.Businesses can help by offering internships and training programs.

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0% Hourly Earnings

Many complain that the jobs being created are alllow paying jobs in food & beverage and retail.

Hourly earnings are growing at a 2.0% rate.

But earnings growth is biased downwards as the baby boomers retire.

Replace someone making $40/hr with someonemaking $15/hr the average declines.

Consumption60%

Government15.0%

Trade10.0%

Investment15%

GDP Components

49

52

55

58

61

64

U.S. CEO Confidence

Like consumers CEO’s remaindecidedly upbeat and for goodreason.

-35.0%

-15.0%

5.0%

25.0%

45.0%

65.0%

85.0%

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

20

0…

20

0…

20

0…

20

0…

20

0…

20

0…

20

0…

20

0…

20

0…

20

0…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

20

1…

Corporate Profits w/o IVA and CC

Corporations are not onlymaking record profits, profits are rising at a10% pace.

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Corporate Bond Rates

Aaa

Baa

Corporate borrowing rates are as lowas they have been anytime in the past50 years.

Low rates allow firms to re-finance debtwhich lowers costs and increases profit.

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

Jan

20

10

Ap

r 2

01

0

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

01

1

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

01

2

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

01

3

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

01

4

Jul 2

01

4

Oct

20

14

C & I Loans (L)

Year-Over-Year (R)

C & I Loans (%)

Credit is readily available.

Bank loans to businesses have surged.They have grown at a 12.7% pace in the past year.

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

20

07

-Q1

20

07

-Q2

20

07

-Q3

20

07

-Q4

20

08

-Q1

20

08

-Q2

20

08

-Q3

20

08

-Q4

20

09

-Q1

20

09

-Q2

20

09

-Q3

20

09

-Q4

20

10

-Q1

20

10

-Q2

20

10

-Q3

20

10

-Q4

20

11

-Q1

20

11

-Q2

20

11

-Q3

20

11

-Q4

20

12

-Q1

20

12

-Q2

20

12

-Q3

20

12

-Q4

20

13

-Q1

20

13

-Q2

20

13

-Q3

20

13

-Q4

20

14

-Q1

20

14

-Q2

20

14

-Q3

20

14

-Q4

Corporate Cash / Assets (%)

Firms have plenty of cash availablefor investment and are finallyputting it to work.

64

66

68

70

72

74

76

78

80

82

Jan1999

Jan2000

Jan2001

Jan2002

Jan2003

Jan2004

Jan2005

Jan2006

Jan2007

Jan2008

Jan2009

Jan2010

Jan2011

Jan2012

Jan2013

Jan2014

Capacity Utilization

Factory utilization rates have climbed to a pointwhere firms need additional plant capacity andneed to implement new technology.

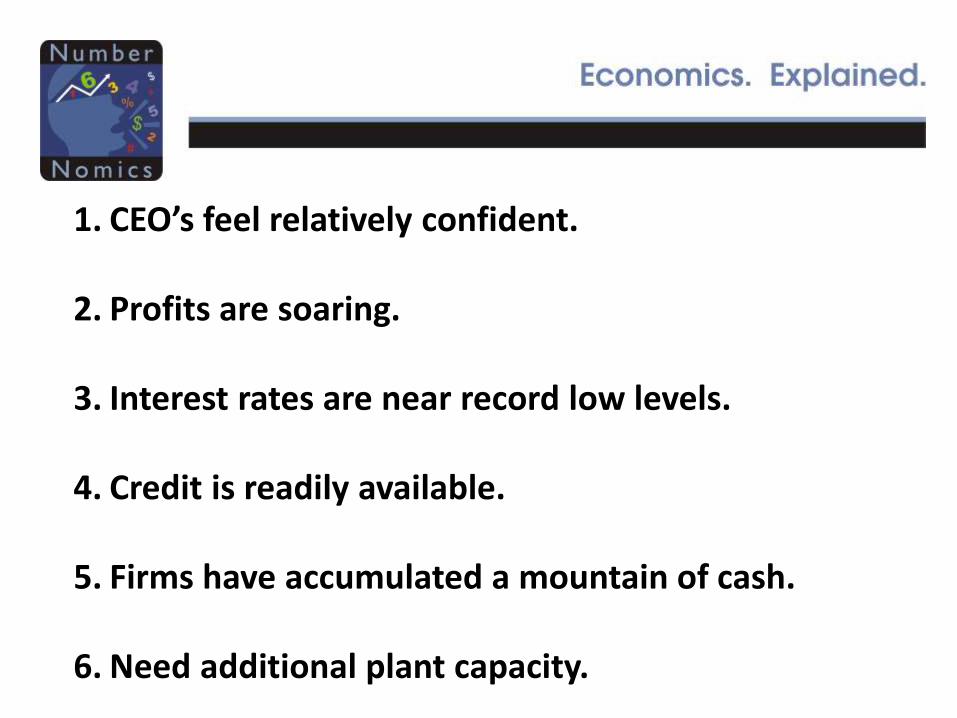

1. CEO’s feel relatively confident.

2. Profits are soaring.

3. Interest rates are near record low levels.

4. Credit is readily available.

5. Firms have accumulated a mountain of cash.

6. Need additional plant capacity.

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

Nonresidential Invest.

Year-over-year

Nonresidential Investment

Given the above we expect nonresidentialinvestment to pick up to about 7.6%in 2015.

Nanotechnology, biotechnology, robotics, the cloud, aps, 3-D printing are all drivinggrowth in earnings and the need to invest.

Consumption60%

Government15.0%

Trade10.0%

Investment15%

GDP Components

-470

-450

-430

-410

-390

-370

-350

-3302

01

1q

1

20

11

q3

20

12

q1

20

12

q3

20

13

q1

20

13

q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

Net Exports

The trade deficit has been steadily shrinking.

It is all oil related and has been caused byimprovements in technology –Fracturing and horizontal drilling.

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015

Oil Exports -- 2005 $

Oil production has increased 80% in past 7 years.

Oil exports have quadrupled from $2.0 billionto $8.0 billion.

15,500

16,500

17,500

18,500

19,500

20,500

21,500

22,500

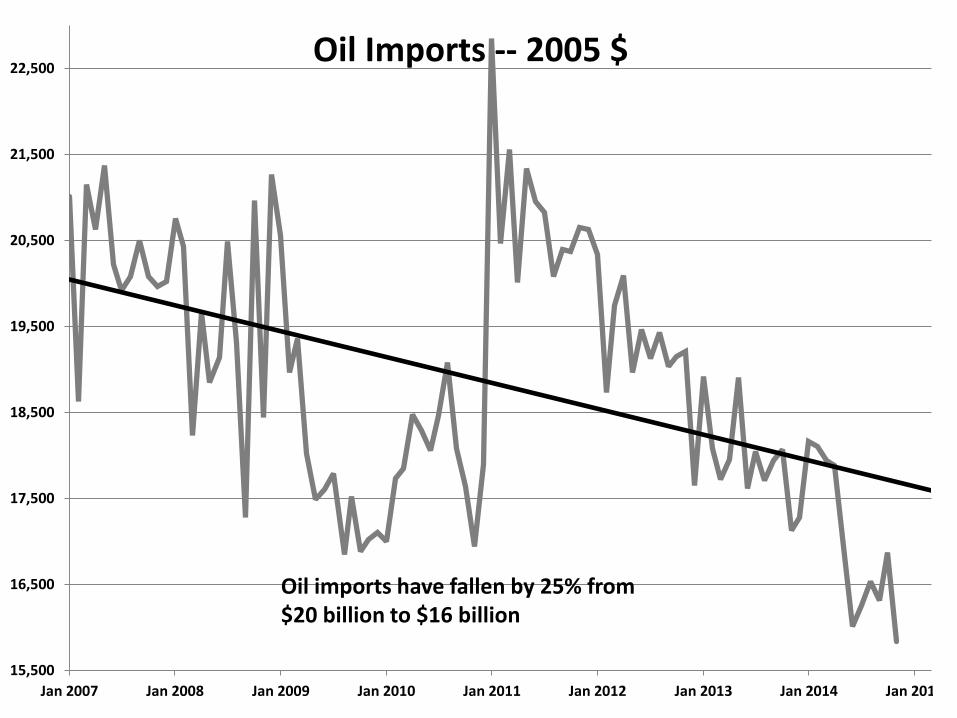

Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015

Oil Imports -- 2005 $

Oil imports have fallen by 25% from $20 billion to $16 billion

-19,000

-17,000

-15,000

-13,000

-11,000

-9,000

-7,000

Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014 Jan 2015

Oil Trade Deficit -- 2005 $

The trade deficit for oil has shrunk from $18 billion to $8 billion.

The U.S. will be a net exporter of oil by the end of this decade.

A much larger portion of our energy needs will beproduced domestically .

Far less reliant on OPEC sources to satisfy oil needs.

By 2020 the U.S. will surpass Saudi Arabia and Russia to become the world’s largest oil producer.

Biggest losers – Venezuela, Iran, Russia.

-470

-450

-430

-410

-390

-370

-350

-3302

01

1q

1

20

11

q3

20

12

q1

20

12

q3

20

13

q1

20

13

q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

Net Exports

Given these developments in the oil market, the trade deficit will continue to shrink.

Consumption60%

Government15.0%

Trade10.0%

Investment15%

GDP Components

-17.0%

-12.0%

-7.0%

-2.0%

3.0%

8.0%

13.0%

Federal Government

Year-over-year

Federal Government

Federal government spending -- defensespending in particular -- has been fallingfor the past two years because the U.S. is winding down of two wars.

Cuts in defense spending are over.

Consumption60%

Government15.0%

Trade10.0%

Investment15%

GDP Components

2014-2015 Forecasts2013 2014 2015

GDP 3.1% 2.8% 3.4%Unemploy. Rate 6.7% 5.6% 4.9%Inflation Rate 1.5% 1.8% 2.8%Fed Funds Rate 0.1% 0.1% 1.4%10-year Note 2.9% 2.2% 2.7%30-year Mortgage 4.3% 3.9% 4.5%

How About Inflation?

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Jan

20

07

Ap

r 2

007

Jul 2

00

7

Oct

20

07

Jan

20

08

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Oct

20

14

CPIEx Food & Energy

CPI

The CPI has slowed to 1.3% because of oil.

The core CPI is currently quite subdued at 1.7%.

Inflation is poised to accelerate. Here’s why.

$2.30

$2.50

$2.70

$2.90

$3.10

$3.30

$3.50

$3.70

$3.90

$4.10 Gasoline Prices

Gasoline prices are very seasonal.

Always decline from early summer through mid-November,Then rise from December through June.

Gasoline prices should climb to about $3.00 by June.

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%Ja

n 2

007

Ap

r 2

007

Jul 2

007

Oct

20

07

Jan

20

08

Ap

r 2

008

Jul 2

008

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

009

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

010

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

011

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

012

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

013

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

014

Oct

20

14

Shelter -- Rent

The shortage of available housing Is pushing up rents.

They are currently rising at 3.0% pace.

Rents are 1/3 of the entire CPI.

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Broad vs. Official Unemployment Rate

Full Employment

Full Employment

As the unemployment rate approachesfull employment wages will begin to rise.

A big deal. Wages represent 2/3 of a firm’s total cost.

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Employment Cost IndexEmploy. Cost Index

Year-over-Year

In fact, labor costs are alreadybeginning to accelerate.

Have picked up from 1.8% to 2.3%and are poised to go higher.

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Jan

20

07

Ap

r 2

007

Jul 2

00

7

Oct

20

07

Jan

20

08

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Oct

20

14

Jan

20

15

Ap

r 2

015

Jul 2

01

5

Oct

20

15

CPIEx Food & Energy

CPI -- Projected

It is quite easy to expect the CPI to be 2.8% by the end of this year.

2014-2015 Forecasts2013 2014 2015

GDP 3.1% 2.8% 3.4%Unemploy. Rate 6.7% 5.6% 4.9%Inflation Rate 1.5% 1.8% 2.8%Fed Funds Rate 0.1% 0.1% 1.4%10-year Note 2.9% 2.2% 2.7%30-year Mortgage 4.3% 3.9% 4.5%

What About the Fed?

The Fed Should Raise Rates by June

Rates Will Rise Slowly Thereafter

But the Fed Will Completely Change

The Way It Conducts Policy

0

1

2

3

4

5

6

7

8

Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Fed Funds RatePrior to 2008 the Fed focused entirely on short rates.

By December 2008 that rate had dropped to 0%.The economy was still in trouble.The Fed had to do something else.

1.50

2.50

3.50

4.50

5.50

6.50

7.50

8.50

Jan

-00

Jun

-00

No

v-0

0

Ap

r-0

1

Sep

-01

Feb

-02

Jul-

02

Dec

-02

May

-03

Oct

-03

Mar

-04

Au

g-0

4

Jan

-05

Jun

-05

No

v-0

5

Ap

r-0

6

Sep

-06

Feb

-07

Jul-

07

Dec

-07

May

-08

Oct

-08

Mar

-09

Au

g-0

9

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

Dec

-12

May

-13

Oct

-13

Mar

-14

Au

g-1

4

10-year Treasury and Mortgage Rates

10-year Treasury Note

30-year mortgages

The Fed switched its focus to long rates.The idea was to stimulate the housing sector.

Mortgage rates fell from 5.5% to 3.5%.

0

500

1,000

1,500

2,000

2,500Ja

n 2

00

8

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Excess Reserves

The Fed would buy a bond andpay for it by putting money in a bank’s checking account at the Fed whichis called a “reserves” account.

Excess reserves have climbed from $2 billionIn 2008 to $2.7 trillion currently.

Excess reserves represent the supply of fundsavailable to the banking system to lend.

0

500

1,000

1,500

2,000

2,500Ja

n 2

00

8

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Excess Reserves

Monetary Policy Prior to 2008:

If banks have $2.0 billion of excess reservesand the Fed sells $4.0 billion of securities,banks have to borrow $2.0 billion from the Fed.

Went from a situation where there weretoo many reserves in the system to a shortage.

0

500

1,000

1,500

2,000

2,500Ja

n 2

00

8

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Excess Reserves

But today excess reserves are not $2 billionthey are $2.7 trillion.

Fed can not sell enough securities to createan actual shortage of reserves.

Something has to change.

Fortunately, the Fed has a plan.

0

500

1,000

1,500

2,000

2,500

3,000

Jan

20

08

Jun

20

08

No

v 2

00

8

Ap

r 2

009

Sep

20

09

Feb

20

10

Jul 2

01

0

Dec

20

10

May

20

11

Oct

20

11

Mar

20

12

Au

g 2

012

Jan

20

13

Jun

20

13

No

v 2

01

3

Ap

r 2

014

Sep

20

14

Feb

20

15

Jul 2

01

5

Dec

20

15

May

20

16

Oct

20

16

Mar

20

17

Au

g 2

017

Jan

20

18

Jun

20

18

No

v 2

01

8

Ap

r 2

019

Sep

20

19

Feb

20

20

Jul 2

02

0

Dec

20

20

Excess Reserves -- Projected

Fed is unwilling to sell securities.

But it will soon let them matureand not replace them.

That process will take until end of the decade.

What to do until then?

0

500

1,000

1,500

2,000

2,500Ja

n 2

00

8

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Excess Reserves

Today banks earn 0.25% on reserves they hold at the Fed.

But suppose the Fed pays them 4% on those reserves.

Banks would rather earn 4% risk free from the Fedthan to lend to you or me at, say 5%.

We higher the rate the Fed pays, the higher otherrates will be.

0

500

1,000

1,500

2,000

2,500Ja

n 2

00

8

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Excess Reserves

The reserves are still there, but they are effectively neutralized.

But will this work?

Will there be unintended consequences?

When Will the Fed Begin to Raise Rates?

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Broad vs. Official Unemployment Rate

Full Employment

Full Employment

The Fed has told us it won’t raise rates untilthe unemployment rate is close to full employment.

Should happen by mid-2015.

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Jan

20

07

Ap

r 2

007

Jul 2

00

7

Oct

20

07

Jan

20

08

Ap

r 2

008

Jul 2

00

8

Oct

20

08

Jan

20

09

Ap

r 2

009

Jul 2

00

9

Oct

20

09

Jan

20

10

Ap

r 2

010

Jul 2

01

0

Oct

20

10

Jan

20

11

Ap

r 2

011

Jul 2

01

1

Oct

20

11

Jan

20

12

Ap

r 2

012

Jul 2

01

2

Oct

20

12

Jan

20

13

Ap

r 2

013

Jul 2

01

3

Oct

20

13

Jan

20

14

Ap

r 2

014

Jul 2

01

4

Oct

20

14

Jan

20

15

Ap

r 2

015

Jul 2

01

5

Oct

20

15

CPIEx Food & Energy

CPI -- Projected

The Fed has told us it won’t raise rates untilthe inflation rate climbs to its 2.0% target.

Should happen by mid-2015.

0

1

2

3

4

5

6

7

8

9

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Fed Funds RateBoth conditions to raise rates will be met by June.

Thereafter the Fed will hike rates slowly.

It will take until mid-2017 for rates to be “neutral”.

0.0

5.0

10.0

15.0

20.0 Fed Funds Rate

The U.S. economy has never goneinto recession unless the funds ratehas been higher than “neutral”.

Earliest date for a recession? 2018?

In Conclusion

In Conclusion1. GDP growth solid at about 3.4%

In Conclusion1. GDP growth solid at about 3.4%

2. Unemployment rate will continue to drop.

In Conclusion1. GDP growth solid at about 3.4%

2. Unemployment rate will continue to drop.

3. Inflation will inch its way higher.

In Conclusion1. GDP growth solid at about 3.4%

2. Unemployment rate will continue to drop.

3. Inflation will inch its way higher.

4. Fed will begin to raise rates by midyear.

In Conclusion1. GDP growth solid at about 3.4%

2. Unemployment rate will continue to drop.

3. Inflation will inch its way higher.

4. Fed will begin to raise rates by midyear.

5. Stock market will continue to climb.

In Conclusion1. GDP growth solid at about 3.4%

2. Unemployment rate will continue to drop.

3. Inflation will inch its way higher.

4. Fed will begin to raise rates by midyear.

5. Stock market will continue to climb.

6. No recession for at least another three years.

2014-2015 Forecasts2013 2014 2015

GDP 3.1% 2.8% 3.4%Unemploy. Rate 6.7% 5.6% 4.9%Inflation Rate 1.5% 1.8% 2.8%Fed Funds Rate 0.1% 0.1% 1.4%10-year Note 2.9% 2.2% 2.7%30-year Mortgage 4.3% 3.9% 4.5%

But Volatility is Back!

But Volatility is Back!

1. Fed raising rates – 1st time in 8 years.

But Volatility is Back!

1. Fed raising rates – 1st time in 8 years.2. Fed policy is totally different.

But Volatility is Back!

1. Fed raising rates – 1st time in 8 years.2. Fed policy is totally different.3. Fed, Bank of England vs. ECB and BOJ.

But Volatility is Back!

1. Fed raising rates – 1st time in 8 years.2. Fed policy is totally different.3. Fed, Bank of England vs. ECB and BOJ.4. Oil market being transformed.

But Volatility is Back!

1. Fed raising rates – 1st time in 8 years.2. Fed policy is totally different.3. Fed, Bank of England vs. ECB and BOJ.4. Oil market being transformed.

Expect wild swings – stocks, bonds,currencies and commodities

Economy Good, but a Wild Ride!

Stephen SliferNumberNomicswww.NumberNomics.com