51

Jointly published by Roland Berger and BitAuto November, 2015 2015 Chinese auto consumer insights

Jointly published by Roland Berger and BitAuto

November, 2015

2015 Chinese auto consumer insights

With an obvious sales slowdown in 2015, China's auto market is entering a more mature stage of development, and it is of great

importance to maximize future opportunities in the auto sales market. Carmakers and dealers must precisely identify and deeply

understand trends in customer demands and strategic layout to take a leadership position in the coming period of fierce competition.

Bitauto and Roland Berger have combined big data capabilities with industry insight and research expertise to examine and analyze auto

market trends in 2015.

Research background

Report objectives

1. To clearly identify present consumer trends, this report will fully interpret Bitauto's data on consumer preferences in China's auto

market over the past year in order to help auto clients enjoy a bird's eye view of changes in consumers' auto-purchasing demands.

2. This report provides insight into changes in the auto consumption structure, traditional consumer groups and traditional brand user

groups. Leveraging Roland Berger's experience and insights as well as Bitauto's big data resources, this report presents a clear view of

China's complex and disordered auto market from multiple perspectives and sets concrete reference points by which the industry can

understand consumers.

Introduction

Through our deep investigation of online auto purchasing behavior in China (via Bitauto's big data resources and indices), we aim to

analyze consumers' preferences when making auto purchases, consumer group makeup and other major trends auto consumption.

Data is sourced from the Bitauto index (which is based on big data collected by Bitauto). The Bitauto index is informed by analysis of auto

consumption data on browsing, searches and orders from Bitauto's website and over 500 other media partners. It integrates auto sales

data from authoritative sources to objectively and comprehensively reflect behavioral trends among Chinese auto consumers and

consumption activities throughout China's auto market. The report aims to provide carmakers, dealers and other auto industry operators

with objective, precise, effective and sustained data services to inform marketing strategy.

Methodology

Auto sales slow in 2015; market nears maturity after rapid growth

2000 and before

2001-2004 2005-2007 2012-2014 2015 and

after

Demand primarily from

the public sector

First car purchases for families in 1st-

tier cities

First car purchases for

families in 2nd- & 3rd-tier cities

Nation-wide consumption;

increased trade-ins

2008-2011

First car purchases for

families in 4th- & 5th-tier cities and rural areas

Market saturation drives emergence

of market sub-segments

Infancy

Broad overview of sales growth in China's auto market

CAGR: 40%

Taking off

Rapid growth

Maturity

CAGR: 33%

CAGR: 20% CAGR: 7% or lower

Source(s): Joint Advisory Committee of China Passenger Car Market sales figures; Roland Berger research

Introduction

Past and present market situation:

• Uneven consumption across

regional/urban-rural lines

• Auto industry developments

occur relatively quickly

• Overlapping increases in

consumption growth overlaps

and replaces previous growth

• Consumer divisions in market

sub-segments are complicated

Future market situation:

• Increasing market saturation

• Influence of mobile internet

• Transformation in the auto

industry toward further

integration

• New opportunities as the auto

market is adjusted

Given the complex and rapidly-changing consumption environment,

industry players must capitalize on future market opportunities

Introduction

Insights into

China's auto

consumers

Contents

• Trends in Chinese auto consumer preferences

• Trends in the makeup of Chinese auto consumers

• Six types of Chinese auto consumers

• Customer profiles for representative auto brands in

China

Trends in Chinese auto

consumer preferences

1

Pricing preferences:

Growing market share for

entry-level economy

models and enhanced mid-

to-high-end models Vehicle type preferences:

SUVs are still key

drivers of growth,

while the market share of

sedans continues to slide

Country of origin preferences:

Powered by both products and marketing,

independent brands are seeing gradual and

sustained growth

Urban preferences:

Auto consumption is becoming

more widespread; distribution

in 4th- and 5th-tier cities

growing noticeably

Regional preferences:

Sales volume is still

concentrated in the East,

but growth is speeding

up in central-

western China

Trends in Chinese auto consumer preferences

Pricing preferences: Growing market share for entry-level economy

models and enhanced mid-to-high-end models

Trends in Chinese auto consumer preferences

National sales volume of models in different price ranges

Economical choices for first car purchases

Better quality , mainstream positioning

Status symbol, trade-up vehicle 10% 6%

13% 8%

8% 14%

36% 32%

15% 21%

17% 18%

2014 2015*

<80K

80-120K

120-180K

180-250K

250-400K

>400K

C

120-180K

>180,000

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

Cars under 120K

+7% in

sales volume

2015 sales volume growth for two market sub-segments:

Cars from 180-250K

+6% in

sales volume

Vehicle type preferences: SUVs and MPV retain popularity, squeezing out

sedans, especially A-class models National sales volume of different vehicle types

14% 11%

39% 35%

12% 11%

4% 3%

24% 29%

8% 9%

2014 2015*

MPV

SUV

Mid-

size/large*

Mid-size

Compact

Subcompact*

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

* including luxury and sports cars

*Including microcars

Driven by growth in low-end cars; future growth to be slow as already close to hitting the ceiling

Meets dual needs for practicality and individuality; will still enjoy the favor of consumers in the short term

The mainstream choice for many years; will increasingly be divided into sub-segments in the future

MPVs

SUVs

Compact

cars

Trends in Chinese auto consumer preferences

Country of origin preferences: Independent domestic brands are taking off

and winning market share; Japanese brands remain strong National sales volume by cars' country of origin

30% 34%

19% 19%

21% 19%

14% 13%

10% 8%

7% 6%

2014 2015*

Europe/other

Korea

USA

Germany

Japan

China

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

Share decreased slightly across the board

Continuous innovation and effort in the areas of

appearance, technology and marketing have

resulted in significant growth

Due to strategic variety of vehicle types, growth is stronger than that of German, US or jointly invested brands

Independent brands

Japanese brands

Other foreign-invested brands

Trends in Chinese auto consumer preferences

Crossover structure: Self-owned SUV brands are growing rapidly in low-end markets; foreign-invested SUV brands are seeing significant market penetration in mid- to high-end markets

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015) *foreign brands include jointly invested brands and imports

Self-owned MPV brands

Foreign-invested SUV brands

Self-owned sedan brands

Foreign-invested MPVbrands

Self-owned SUV brands

Foreign-invested sedan brands

Trends in Chinese auto consumer preferences

Foreign-invested SUVs penetrate lower-end markets

Self-owned SUV brands break into mid-to-higher-end markets

33% 44%

3%

2014

12%

2015

<RMB 80,000 RMB 80-120K RMB 120-180K RMB 180-250K

Self-owned

SUV and

MPV brands

show

significant

growth

6%

2014

28%

38%

18%

4%

2015

36%

Self-owned

SUV brands

show

significant

growth

76%

2014

83%

13%

2015

10% 3%

52%

2014 2015

4%

44%

Foreign-

invested

SUVs increase

market share

Self-owned SUV brands break into higher-end markets

49% 33.4% 34% 29%

40% 47%

5% 9% 3% 2%

15% 10%

8% 6%

16% 16%

27% 27%

22% 23%

26% 28%

2014 2015*

5th tier

4th tier

3rd tier

2nd tier

1st tier

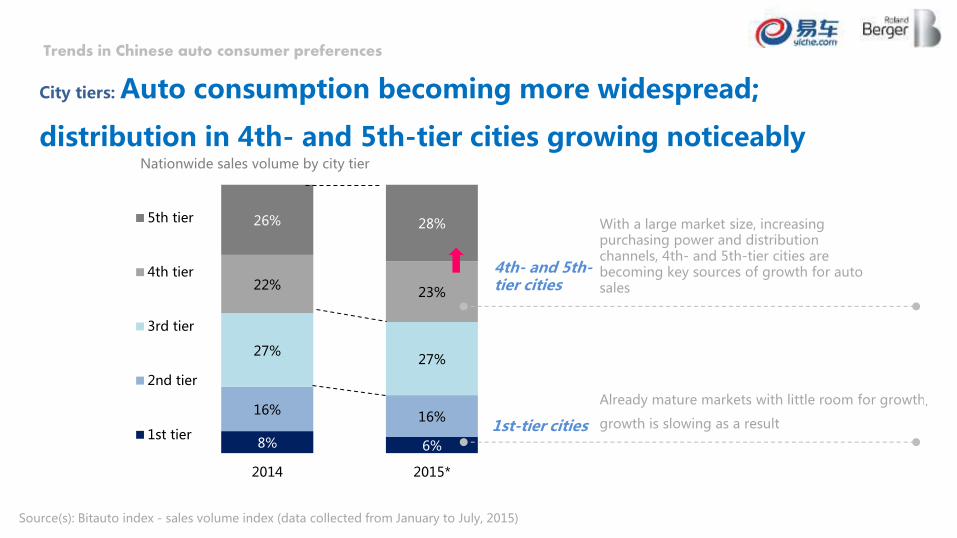

City tiers: Auto consumption becoming more widespread;

distribution in 4th- and 5th-tier cities growing noticeably

Nationwide sales volume by city tier

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

With a large market size, increasing purchasing power and distribution channels, 4th- and 5th-tier cities are becoming key sources of growth for auto sales

Already mature markets with little room for growth;

growth is slowing as a result 1st-tier cities

4th- and 5th-tier cities

Trends in Chinese auto consumer preferences

City tiers: Distribution of vehicles under RMB 180K moving toward

4th- and 5th-tier cities Sales volume of vehicles at different price points in different city tiers

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

3% 1% 5% 3% 7% 5% 11% 10% 15% 14% 17% 16% 10% 10%

15% 14%

18% 17%

18% 17% 20% 21%

21% 21% 25% 24%

28% 28%

28% 28%

27% 27%

27% 28% 29% 30% 28%

28%

24% 25%

21% 23%

19% 20%

17% 18% 15% 16%

34% 38% 28% 31% 25% 28% 25% 26%

20% 20% 17% 16%

2014年 2015年

*

2014年 2015年

*

2014年 2015年

*

2014年 2015年

*

2014年 2015年

*

2014年 2015年

*

8万以下 8-12万 12-18万 18-25万 25-40万 40万以上

五级

四级

三级

二级

一级

<80K 80-120K 120-180K 180-250K

250-400K

>400K

Trends in Chinese auto consumer preferences

Regional preferences: Auto sales are concentrated in the east, but sales are rising in the central-west and demand growth is expected

Source(s): Bitauto sales volume index; Roland Berger analysis

In coastal regions and

provinces with high-ranking

GDP, demand for vehicles

remains strong

Central-western regions

contribute around 22% of

national auto sales, but the

average growth rate is higher

than in the east区

Economic downturn or slow

markets has resulted in minimal

growth or negative growth

2015 national passenger vehicle sales volume mapped by major provinces in each region

Trends in Chinese auto consumer preferences

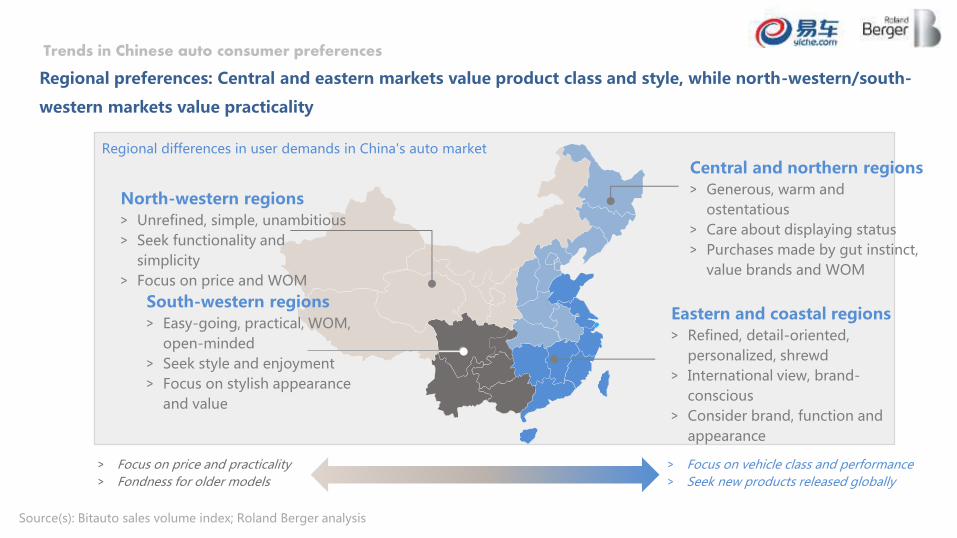

Regional preferences: Central and eastern markets value product class and style, while north-western/south-

western markets value practicality

Source(s): Bitauto sales volume index; Roland Berger analysis

> Focus on vehicle class and performance

> Seek new products released globally

> Focus on price and practicality

> Fondness for older models

Central and northern regions > Generous, warm and

ostentatious

> Care about displaying status

> Purchases made by gut instinct,

value brands and WOM

Eastern and coastal regions > Refined, detail-oriented,

personalized, shrewd

> International view, brand-

conscious

> Consider brand, function and

appearance

South-western regions > Easy-going, practical, WOM,

open-minded

> Seek style and enjoyment

> Focus on stylish appearance

and value

North-western regions > Unrefined, simple, unambitious

> Seek functionality and

simplicity

> Focus on price and WOM

Regional differences in user demands in China's auto market

Trends in Chinese auto consumer preferences

Regional preferences: Northern consumers focus on public opinion, eastern on brands and western on

functionality

Source(s): Bitauto sales volume index; Roland Berger analysis

Central and northern

Eastern and coastal Southwest

Northwest

Vehicle models typically bought by consumers in each region

Average price: RMB 178K

Touran Excelle

MINI

BMW 5 Series

EMGRAND EC7

Representative vehicle models:

Average price: RMB 168K

Satigar Lavida

Jetta

Xuanyi

Avante

Representative vehicle models:

Average price: RMB 160K

Refine S3

Wuling Hongguang Haval H6

Santana

Sportage

Representative vehicle models:

Average price: RMB 164K

科鲁兹三厢 Wuling Hongguang

HavalH6

ChangAn Honor

Bao Jun730

Representative vehicle models:

*classic models were defined as those with the highest sales volume in a given region

Trends in Chinese auto consumer preferences

Trends in the makeup of

Chinese auto consumers

2

Rising purchasing

power of women

Activating demand

in lower-tier cities

Youth trend

orientation

Trend 1

Youth trend orientation

80s and 90s-generation consumers are gradually becoming the main force for the future auto market

Orientation toward youth trends is driving the restructuring of auto brands, more focus on youth-oriented products and upgrades to consumer experiences

Young consumers' purchasing decisions consider price as well as individuality; economically positioned compact cars are the most popular among them

Increased division of young consumer groups into sub-segments and clearly differentiated options

Young consumers, age 30 and younger, are gradually becoming

the main force in China's auto market

Trends in the makeup of Chinese auto consumers

21% 16% 17%

17%

14% 14%

17%

15% 15%

20%

19% 18%

20%

21% 23%

6% 14% 13%

26-30

<25

2015.1-7 2014 2013

>45

41-45

36-40

31-35

Changes in the ages of auto consumers in China

26%

74% > Peak consumption period passed: The market has already entered a period of relative maturity and slower growth

> Awaiting a boost from upgrades: The demand for trade-ins and upgrades hasn't entirely hit the market yet; market sub-segments are expected to particularly benefit from this additional demand

> Mentality of younger consumers: Cars not viewed as much as "major assets," but more as "ordinary commodities"; car ownership ages are becoming lower

> Young consumers' purchasing power: They have purchasing power and they value individualized experiences

36%

64%

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

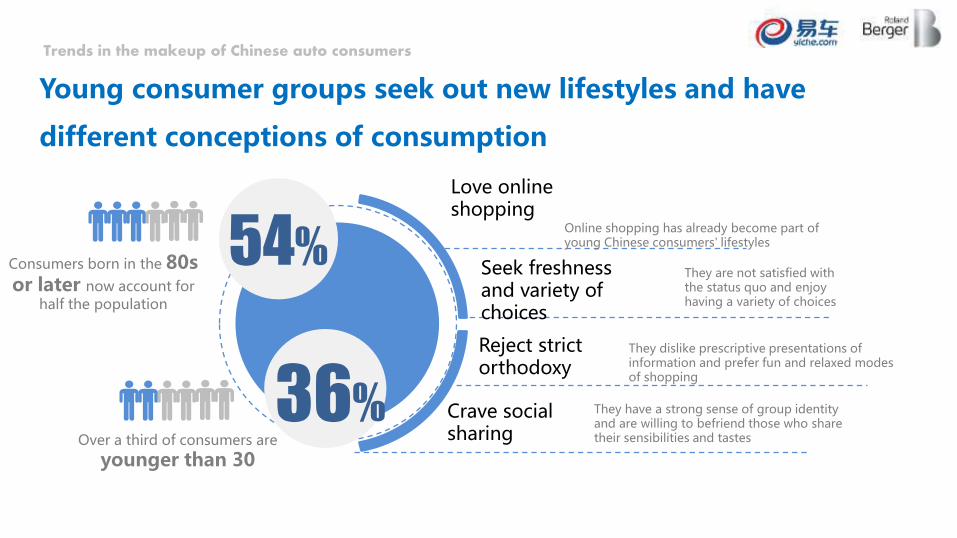

Young consumer groups seek out new lifestyles and have

different conceptions of consumption

Trends in the makeup of Chinese auto consumers

Consumers born in the 80s or later now account for

half the population

54%

36% Over a third of consumers are

younger than 30

Online shopping has already become part of young Chinese consumers' lifestyles

Love online shopping

Seek freshness and variety of choices

Reject strict orthodoxy

Crave social sharing

They dislike prescriptive presentations of information and prefer fun and relaxed modes of shopping

They are not satisfied with the status quo and enjoy having a variety of choices

They have a strong sense of group identity and are willing to befriend those who share their sensibilities and tastes

The youth trend in consumers is driving a rethinking of auto

brands, products and strategic layout

Trends in the makeup of Chinese auto consumers

80s- and 90s-generation consumers

Individuality

Fashion

80s- and 90s-generation consumers are

individualists; a car is not just a means

of transportation, but also a means of

fashionably expressing one's identity

Sportiness

60s- and 70s-generation consumers

Status symbol

Comfort

60s-generation consumers are utilitarian

consumers; a car is just a means of transportation

70s-generation consumers are status-seekers; a

car is a status symbol

Durability

Youth orientation is driving the industry to provide more individualized, "smarter" and multidimensional consumer experiences

Trends in the makeup of Chinese auto consumers

Source(s): Roland Berger research

> Comprehensive car-lifestyle experience – Individualization and convenience – Car ownership community network – Integration and transformation of car travel

> High-quality products – Vehicle exterior design – Quality and safety

> Individualized service – Key-customer relationship maintenance – Vehicle customization

> Professional service – Professional sales and after-sales staff – One-time repair success

> One-stop service – Second-hand vehicle services – Auto insurance and financing services

Trends in the changing demands for the consumer experience:

新兴需求

70s- and 80s-generation consumers

Consumers born between '85 and '90

90s-generation consumers

60s- and 70s-generation consumers

60s-generation consumers

Young consumers look for attractive pricing and individualization,

so economical, compact cars are their favorites

Trends in the makeup of Chinese auto consumers

Source(s): Bitauto index - sales volume index (data collected from January to July, 2015)

Pricing of cars purchased by consumers of different ages

Vehicle types purchased by consumers of different ages

Young consumer groups are undergoing further segmentation

and show clear differentiation in preferences

Trends in the makeup of Chinese auto consumers

Vehicle price points considered by young consumers is different professions (TGI index)

a

b

d

Sales/service/tech support

Computing/IT/information

Manufacture/operations/purchasing/logistics

HR/administrative/executive management

Advertising/marketing/media

Accounting/finance/banking/insurance

Architecture/real estate Consulting/legal/education/ research Service industry

Public sector/translation/ other Bio/pharmaceuticals/medical/nursing

Professional

elites

Rising

talent

Balanced

professions

Concrete

professions

Professions with clear purpose

<80K 80-150K 150-250K 250-400K >400K

c

e

122 89 81 99 118

87 96 109 134 129

88 101 117 105 103

116 108 72 72 68

75 96 155 104 102

Source(s): Bitauto user data (the above TGI took consumers below 30 as the base, assigning a base number of 100)

Trend 2

Rising purchasing power of women

China's female auto consumers are a rapidly growing demographic that makes up one third of the market and is expected to grow further in the future

Compared to male consumers, female consumers pay more attention to exterior aesthetics, brand, quality, safety and comfort

The pursuit and preservation of youth is never-ending for female consumers, so the trend of youthfulness in the auto sector is a driving force for female consumers

72%

54% 55%

29% 46% 45%

China's female auto consumers are rapidly growing demographic, make up one third of the market and are expected to grow further in the future

Trends in the makeup of Chinese auto consumers

Source(s): Bitauto index - sales volume index; Roland Berger research

The rapid rise of female consumers in China and their increasing share of the consumer market

But there is still a gap with mature markets and China's female auto consumers still have room for further growth

320

267227

187

144125

2011 2013 2015 2014 2012 2010

Newly registered female car owners [10,000]

Composition of carbuyers:

North America

China

Male

Europe

Female Percent of

female car

owners

17%

Percent of

female car

owners

29%

2010

2015

Female vehicle choices tend to be based on personal feeling, aesthetics, quality and comfort

Trends in the makeup of Chinese auto consumers

Source(s): Roland Berger research

Demands and preferences of female consumers

"I go for the best-looking cars in the best colors. Stylish design is also a

must."

"The most important things are safety and ease of driving"

"Good brands offer more security and

have better design"

"It's best if the car comes with a variety of entertainment systems and features including speakers and automatic parking"

Style and aesthetics

Safety and comfort

Brand Electronic entertainment

24.2%

38.4%

15.0%

12.7%8.0%

8.0%

18.5%

20.9%

16.6%25.1%

13% 10%

36%35%

12%10%

29%

30%

10%

14%22%

19%

21%

34%

31%

13%12%

12%8%

8% 6%

Compared to men, female car owners have higher demands for

vehicle class, appearance and brand

Trends in the makeup of Chinese auto consumers

80-120K

250-400K

180-250K

<80K

120-180K

>400K

Male car owners

Female car owners

Mid-size

Subcompact

SUV

MPV

Mid-size/large

3% 3%

5%

Compact

Male car owners

Female car owners

Japan

Other

China

USA

Korea

France

Germany

3.4%

3.6%

Male car owners

Female car owners

Prices paid by car owners: Vehicle classes chosen: Countries of origin chosen:

Female auto consumers: favor higher-class models

Seek style and attractive designs

Prefer foreign- owned brands

Source(s): Bitauto index - sales volume index

A youthful orientation is the key to unlocking the female auto

consumer market

Trends in the makeup of Chinese auto consumers

Source(s): Bitauto index - sales volume index

57% 54% 44% 43% 41%

43% 46% 56% 57% 59%

12万以下 12-18万 18-25万 25-40万 40万以上

Purchases of cars at different price points by male consumers above or below 35

65% 64% 57% 54% 51%

35% 36% 43% 46% 49%

12万以下 12-18万 18-25万 25-40万 40万以上

Purchases of cars at different price points by female consumers above or below 35

Under 35

Above 35

数据范围:2014年全国已购车用户

• Among auto sales to male customers, low-to-mid-end cars are primarily sold to young men, while high-end cars are primarily sold to older men

• However, among auto sales to female customers, women from the 80s generation or younger are the primary purchasers of cars over 400K;

aligning with female consumers' desire for youthfulness is critical to success

Trend 3

Activation of market demand in lower-tier cities With China's urbanization and market saturation in highly developed cities, the shift of more sales to

lower-tier cities is inevitable

Auto consumption demand lower-tier cities is gradually rising and contributing a larger share of China's overall auto sales

Most auto sales in lower-tier cities are to first-time buyers; consumers tend to be more rational, cautious, practical and economically minded

At the same time, lower-tier cities are also a critical market for luxury cars and are expected to continue to grow steadily in that area

The shift in auto sales volume to lower-tier cities is inevitable

Trends in the makeup of Chinese auto consumers

Source(s): Roland Berger research

Drivers of auto sales growth in lower-tier cities:

Saturation of 1st-and 2nd- tier

markets and a shift of market focus

Purchasing restriction

policies have not yet been

implemented in 3rd- and 4th-tier

cities

Relatively low inventory in 3rd- and

4th-tier cities

A rise in expendable income in

3rd- and 4th-tier cities

Urbanization has increased

urban populations

Rural 14%

4th tier 31%

3rd tier 24%

2nd tier 16%

1st tier

14%

9%

14%

30%

2nd tier

1st tier

3rd tier

Rural 9%

4th tier 38%

Current car-owner market composition:

Expectations for market composition in the coming year:

70%

77%

Note: Beijing, Shanghai, Guangzhou and Shenzhen are classified as 1st-tier cities; provincial capitals and economic hubs are classified as 2nd-tier cities; prefecture-level cites as 3rd-tier cities, and county-level cities as 4th-tier cities

Market share of lower-tier cities

Market share of lower-tier cities

35% 22%

18%

22%

13% 15%

9% 7%

19% 27%

低线城市 发达城市

德系

法系

韩系

美系

日系

中国

其他

12% 7%

36%

32%

10% 15%

2% 6%

29% 32%

11% 7%

低线城市 发达城市

MPV

SUV

中大型车

中型车

紧凑型

小型车

Compared to developed cities, consumers in lower-tier cities rational, cautious, practical and economically minded

Trends in the makeup of Chinese auto consumers

Source(s): Bitauto sales volume index

Note: "Developed cities" are defined as 1st- and 2nd-tier cities; lower-tier cities are defined as 3rd- and 4th-tier cities

20% 9%

23%

16%

32%

31%

10%

14%

9%

16%

6% 13%

低线城市 发达城市

40万及以

上 25-40万

18-25万

12-18万

8-12万

8万以下

250-400K

180-250K

>400K

80-120K

<80K

120-180K Mid-size

Subcompact

SUV

MPV

Mid-size/large

Compact

Japan

Other

China

USA

Korea

France

Germany

Prices paid by car owners: Vehicle classes chosen: Countries of origin chosen:

Consumers in lower-tier cities primarily buy mid-to-low-end vehicle models

MPVs and subcompact cars are favored

Self-owned brands enjoy a competitive edge

Developed cities

Lower-tier cities

Developed cities

Lower-tier cities

Developed cities

Lower-tier cities

Lower-tier cities are also major markets for luxury cars, an area which is expected see continue steady growth

Trends in the makeup of Chinese auto consumers

Source(s): Bitauto sales volume index

Developed cities

2015

62%

38% 40%

2012

59%

41%

2011

58%

42%

2010

54%

46%

2014

61%

39%

2013

60%

Regional sales volume in China's luxury auto market by region

2010-2015 CAGR: 25%

Lower-tier cities

Sales and

distribution

channels of luxury

car OEMs shifting

to lower-tier cities

Even with the

large base market

in lower-tier cities,

there is still space

for more growth

in demand

2010-2015 CAGR: 31%

Note: Luxury cars here are defined by brand, including BMW, Audi, Mercedes-Benz, Infiniti, Acura, Land Rover, Volvo, Lexus, etc., but not sports cars

Note: "Developed cities" are defined as 1st- and 2nd-tier cities; lower-tier cities are defined as 3rd- and 4th-tier cities

Six types of Chinese auto

consumers

3

Analysis of data collected via the Bitauto network, interpreting

representative consumer groups in China's auto market

Computation and cluster analysis of data reveals representative

consumer groups

Population characteristics

Survey of vehicle type preferences

Car ownership situation

Hobbies and interests

Regional characteristics

Source(s): Bitauto platform user cookies and orders (PC+mobile), January-August, 2015

Cost-conscious young men

• Young, mid-to-low

income

• Utilitarian, simple

demands

• Favors economical

sedans

Men whose careers are taking off

• Mid aged, mid-level salary

• 2nd/3rd-tier city, office job

• Traditional, conservative

• Seeks quality and

practicality

Mature, wealthy men

• Older and successful

• 1st and 2nd tier cities

• Favor high-end brands

and models

Fun-loving small-town guys • 3rd/4th-tier city, low

income

• Young, fun-loving,

sporty

• Favors domestic

SUVs and MPVs

Mature, knowledge-able women

• Older, financially

successful

• Seeks quality and

enjoyment

• Favors mid-to-high-

end foreign cars

Fun-loving female youth

• Fashionable, mid-to-low

income

• Seeks individuality and

variety of choices

• Favors economical

Chinese/Japanese cars

Based on big data gathered by Bitauto, Roland Berger identified each group's characteristics and auto purchasing preferences through cluster analysis of Chinese auto customers and extrapolating those characteristics to define six consumer types

6 types of Chinese auto consumers

1 2

3 4

6

5

Mature, wealthy men: Have high purchasing power, show flexibility in brand choices and favor mid-sized-and-large SUVs

Six types of Chinese auto consumers

High-end consumers that love SUVs

1

SUVs

91%

MPVs

6% Luxury

cars*

3%

80-

150K

14%

150-

250K

12% 250-

400K

51%

400K-1

million

22%

Classic models

Share of vehicles bought at different

prices [%]

Share of vehicles types bought [%]

CR-V & XR-V

RAV4

Escape

ix35

Envision

Touran & Tiguan

Sportage

Compass Q5 & Q7

Variety of brands shows flexibility

Source(s): Bitauto big data; Roland Berger research

*Luxury cars include sports cars

Men whose careers are taking off: Appreciate the VW aesthetic,

are moderate consumers, and are loyal to German brands

Six types of Chinese auto consumers

2

Source(s): Bitauto big data; Roland Berger research

Compact

54% Subcom

pact

13%

Mid-size

25%

Large

7%

German

y

67%

Korea

24%

France

法国

8%

Preference for sedans, especially three-box sedans

Share of vehicles types bought [%]

Breakdown by country of origin [%]

Note: 87% of the models chosen by consumers in this group are three-box sedans

Jetta

Satigar

Lavida

Magotan

Bora

Passat

POLO Golf

A4L A6L

Avante Verna

Classic models

Widespread popularity of German cars

Cost-conscious young men: Seek value above all else; they favor

economical, practical and popular compact cars

Six types of Chinese auto consumers

3

Source(s): Bitauto big data; Roland Berger research

They favor economical Chinese, Japanese and American sedans

Classic models

The top-three most popular compact sedans

Japan

39%

China

31%

USA

25%

Other

5%

Compac

t cars

60%

Subcom

pact

cars

14%

Mid-

size

18%

Mid-size

and

large

4%

Micro-

cars

4%

Share of vehicles types bought [%]

Breakdown by country of origin

[%]

BYD Surui

Chevrolet Malibu

Toyota Carola

SUV

72%

MPV

26%

Other

2% >150K

1%

80-150K

44% <80K

55%

Fun-loving small-town guys: Seek individuality despite small

budget; love domestic SUVs and MPVs

Six types of Chinese auto consumers

4

Source(s): Bitauto big data; Roland Berger research

Seeking individuality despite limited budget

Classic brands

Almost entirely domestic brands

Share of vehicles bought at different

prices [%]

Share of vehicles types bought [%]

Brand German

y

52% Korea

19%

Japan

13%

France

7%

USA

8% Subcom

pact

9%

Compac

t 34%

Mid-size

13%

Mid

size/

large 5%

MPVs

3%

SUVs

36%

Mature, knowledge-able women: Purchasing power + taste =

fans of German cars, especially mid/high-end sedans and SUVs

Six types of Chinese auto consumers

5

Source(s): Bitauto big data; Roland Berger research

Favor mid/high-end sedans and SUVs

Classic brands

Taste and individuality

Share of vehicles types bought [%]

Breakdown by country of origin [%]

VolkswagenSatigar

VolkswagenTougar

AudiA4L

BMW 3 Series

Audi Q5

Quality

Taste

Economical

Fun-loving female youth: Putting cost-effectiveness first and

individuality second, they like many diverse brands and models

Six types of Chinese auto consumers

6

Source(s): Bitauto big data; Roland Berger research

Favor economical sedans and SUVs

Classic brands

Cost-effectiveness and individuality

Share of vehicles bought at different

prices [%]

Breakdown by country of origin [%]

Individuality

Casual

<80K

49% 80-150K

38%

150-

250K

9%

>250K

3%

China中

国

57%

Japan

24%

USA

15%

Other

4% HavalH6

Bao Jun730

CS35/75

Changan Ford Escort

Toyota Carola

Customer profiles for

representative auto brands in

China

4

Analysis of big data on car buyers reveals three major categories of auto brand consumers with clearly defined characteristics

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

BMW

Audi

Mercedes-Benz Porsche

Haval

BYD

Changan

Volkswagen

Toyota

Honda

Ford

Hyundai Chevrolet

Buick

Luxury brands Mid-range jointly owned brands Self-owned domestic brands

• The following brands define three types of auto consumers: 4 luxury brands, 7 mid-range jointly owned brands

and 3 self-owned domestic brands

• The 14 brands listed here make up the majority market share of China's auto sales volume and the connected

consumer groups exhibit clear characteristics

A brand consumer profile can be sketched by combining information such as population characteristics, interests, region, predicted purchases, etc.

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

Gender

Age Income

Education

Region

Interests & hobbies

Profession Consumption preferences

Lifestyle

Luxury brand consumers:

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

Audi

Senior executives

Audi

Traditional public and private sector executives

• Concentrated in the Yangtze river delta area

• Mostly high-income, highly educated men over the age of 50

• Pay attention to luxury cars; enjoy golf and travel

Golf

Travel Yangtze river delta

Most mature Public officials

Finance

Highly educated

Luxury autos

Audi

Mature conservative bosses

• Relatively mature and older

• Highly educated, high-income men make up the majority

• Many in finance and real estate

• Like to travel

Beijing

Shanghai

Travel South-west

High income Mature

Real estate

Highly educated

Finance

Audi

Racing

Fun-loving new rich

• Young & middle-aged high-income men are the majority

• More female owners than Audi or Mercedes-Benz

• Beijing and Pearl River Delta

• Follow racing and the stock market

Beijing

Travel

Pearl River Delta

Young & middle

aged New rich

Stocks

High income

Audi

Wine tasting

Stylish finance elites

• Young, high-income men make up the majority

• More female owners than Audi or Mercedes-Benz

• 1st- and 2nd-tier cities

• Many work in finance

• Broad interests, trendy

1st/2nd-tier

cities

Travel

Jiangsu, Zhejiang

Young 2nd hand

Finance

Trendy

Luxury autos

Mercedes-Benz BMW Porsche

Jointly invested brand consumers:

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

Audi

Northern upper-middle class

Audi

New metropolitan workforce

Audi

Coastal IT elites

• Young/middle aged and mainly middle income

• 1st-tier cities, Yangze River Delta

• Relatively high-end industries such as IT

• Interest in resold apartments and the stock market

Audi

Metropolitan families

• Concentrated in 2nd-tier cities

• Young/middle aged, more female owners, relatively highly educated

• Interested in fashion and shopping

• Pay attention to 2nd-hand cars

Buick

Audi

Real estate

• Middle aged, middle income

• Relatively highly educated

• Concentrated in BJ and TJ

• Wage earners from many different professions

• Enjoy reading and new cars

Novels

Family Middle income

Beijing Tianjin region

Office workers

Intellectual

New cars

Volkswagen Chevrolet

Middle income

Fashion Film fans

Eye candy 2nd/3rd-tier cities

Gaming

Young

• Young/middle aged and mainly middle income

• 2nd/3rd-tier cities

• Average education

• Enjoy films, gaming and fashion

Resold apartments

Stocks

undergrad Yangze River Delta

Relatively mature

1st-tier cities

IT guys

Upper-middle income

2nd-hand cars

Shopping

Women 2nd-tier cities

Relatively mature Real estate

Department stores

Highly educated

Ford

Jointly invested brand consumers:

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

Audi

Young urban office workers

Audi

Mature, middle class and in the South

Small city economical

utilitarians

• Young, middle income

• 2nd- and 3rd-tier cites

• Relatively low education

• Love online shopping

Audi

• Mostly young, mid/high income owners with average education

• 2nd- and 3rd-tier cites, esp. in the Pearl River Delta

• Sales, real estate and other mid-high professions

• Like football, manga, gaming

Young

Manga Pearl River Delta

Mid/high income Football

Office workers

Sales

Honda Toyota

Upper-middle income

Hotels Social media

Middle-aged/young Pearl River Delta

Wine tasting

Admin

• Middle-aged/young people slightly more mature than Honda owners, mid/high income, average education

• 1st- and 2nd-tier cites, esp. in the Pearl River Delta

• HR and administrative

• Like wine tasting, hotel travel

Low education

Upper-middle income 2nd- and 3rd-tier cites

Online shopping

Young

Hyundai

Gaming

Self-owned domestic brand consumers:

Customer profiles for representative auto brands in China

Source(s): Bitauto big data; Roland Berger research

Audi

Small city, struggling youth

Audi

Southwestern small-city

fun lovers

Small city middle-aged

business owner

• Older, more mature, mostly men

• 3rd/4th-tier cities

• Production, purchasing

• Lowest levels of education

• Enjoy drinking

Audi

• The youngest consumers

• Low education and income

• Work in mid-to-low-income industries

• Pay attention to new cars

• Read novels, love music

Different city tiers

New cars mid-to-low-income

The youngest

Service industry

Novels

Pop music

BYD Changan

Gaming

Sales, manufacture

Young/middle aged 3rd/4th-tier cities

Film

Southwest

• Young or middle aged, mid-to-low education and income

• 3rd/4th-tier cities, especially in the southeast

• Sales, manufacture

• Enjoy films, manga and gaming

Low education Older, more mature

Middle-aged men Purchasing

Alcohol

Haval

3rd/4th-tier cities low education

Business

Scan the QR code or seach for the public account "易车指数:" to access more research

results

To learn more about auto consumer market trends

follow the Bitauto Index below • Index.bitauto.com (Index rankings)

• datamodel.bitauto.com (the Index's public account) Thanks. The end.