between spouses• Partial exclusion for health, job, unforeseen

circumstances• Months of use/24 months x maximum

exclusion• Nonqualified use—partial exclusion

8-6

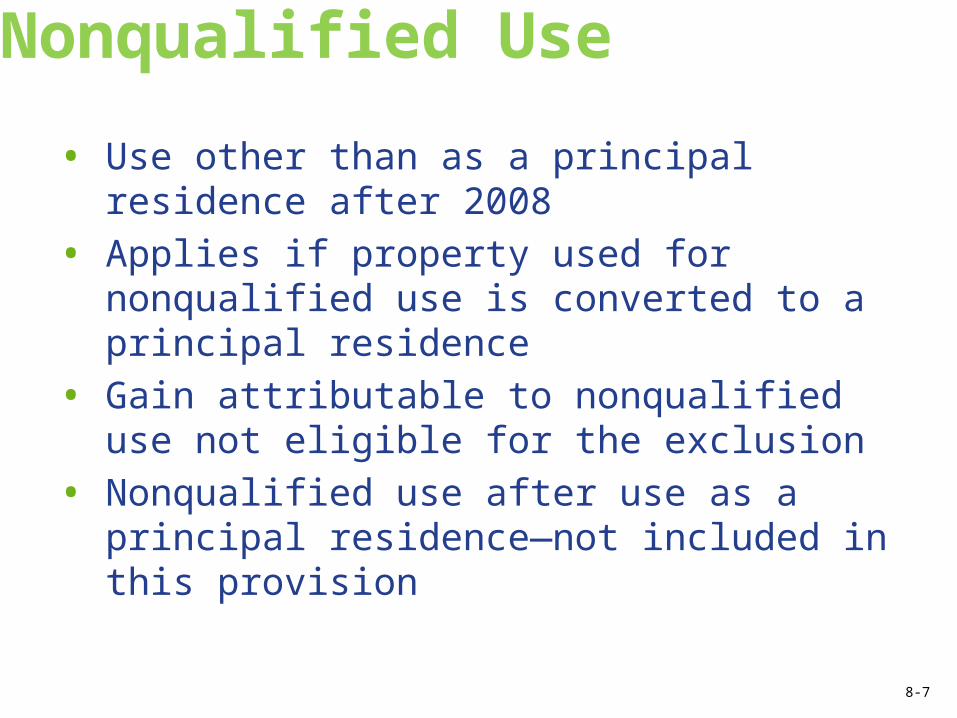

Nonqualified Use

• Use other than as a principal residence after 2008

• Applies if property used for nonqualified use is converted to a principal residence

• Gain attributable to nonqualified use not eligible for the exclusion

• Nonqualified use after use as a principal residence—not included in this provision

8-7

Review Question 1

In a like-kind exchange, a lossa. may be recognized within certain

limitations.b. may be recognized without limitation.c. may be recognized only by the

taxpayer who pays boot.d. may not be recognized.

8-8

Review Question 2

The substitute basis of a qualifying asset received in a like-kind exchange is the asset’sa. basis reduced by the gain realized but

not recognized.b. basis increased by the gain realized

but not recognized.c. fair market value reduced by the gain

realized but not recognized.d. fair market value increased by the gain

realized but not recognized.

8-9

Review Question 3

In January of 1995, Jim Johnson, then age 57, sold his principal residence in Seattle and took advantage of the once-in-a-lifetime exclusion available under Section 121. At that time, the maximum exclusion was $125,000. He excluded his entire gain on the sale, which was $100,000. Later that year, he purchased a new residence in Denver that he used as his principal residence. Earlier this year, he sold the Denver residence for a realized gain of $300,000.What is the maximum amount of gain, if any, that Jim may exclude under Section 121?a. $0b. $25,000c. $250,000

8-10

Review Question 4

Mary Falcon is a single taxpayer. On January 1, 2014, she received a gift from her mother of a house that immediately became her principal residence. On January 1, 2015, she sold this home for a realized gain of $133,000. She sold the home because she received a job promotion and was transferred to a new location out of state.What is the maximum amount of gain, if any, that may be excluded under Section 121?a. $0b. $66,500c. $125,000d. $133,000

8-11

Review Question 5

Which one of the following may qualify as a like-kind exchange?a. a heifer exchanged for a bullb. an apartment building located in Miami

exchanged for an apartment building located in Mexico City

c. farming equipment exchanged for farmland

d. a shopping center exchanged for farmland

8-12

Review Question 6

Bob is involved in a like-kind exchange. In the exchange, he assumes a mortgage of $15,000, is relieved of a mortgage of $26,000, and receives $7,000 in cash. How much boot did Bob receive in the transaction?a. $7,000b. $11,000c. $18,000d. $33,000

8-13

Review Question 7

Robert McCallum has a truck that he uses to make deliveries for his business. The truck has a fair market value of $21,000 and an adjusted basis of $10,000. Robert still owes $9,000 on the truck. Pasqual Mendez has offered to trade his truck for Robert’s truck in an even trade, taking over payments on Robert’s truck. Pasqual’s truck has a fair market value of $12,000 and an adjusted basis of $10,000.What is the amount of Robert’s basis in the acquired property?a. $9,000b. $10,000c. $11,000d. $21,000