23

2015 Q2 INVESTOR PRESENTATION ODEON & UCI CINEMAS GROUP 27 August 2015

| Date post: | 19-Jun-2018 |

| Category: |

Documents |

| Upload: | nguyenngoc |

| View: | 213 times |

| Download: | 0 times |

2015 Q2 INVESTOR

PRESENTATION

ODEON & UCI CINEMAS GROUP 27 August 2015

ODEON & UCI CINEMAS GROUP

IMPORTANT INFORMATION

DISCLAIMER

THIS DOCUMENT HAS BEEN PREPARED BY ODEON & UCI FINCO PLC (“ODEON”). BY REVIEWING THIS DOCUMENT OR PARTICIPATING IN THE CONFERENCE CALL THAT PRESENTS IT, YOU AGREE TO BE BOUND BY THE FOLLOWING CONDITIONS.

THIS DOCUMENT IS FOR INFORMATION PURPOSES ONLY AND DOES NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY SECURITIES IN ODEON. FURTHERMORE, IT DOES NOT CONSTITUTE A RECOMMENDATION BY ODEON OR ANY OTHER PARTY TO SELL OR BUY SECURITIES IN ODEON OR ANY OTHER SECURITIES. ALL WRITTEN OR ORAL FORWARD-LOOKING STATEMENTS ATTRIBUTABLE TO ODEON OR PERSONS ACTING ON THEIR BEHALF ARE QUALIFIED IN THEIR ENTIRETY BY THESE CAUTIONARY STATEMENTS.

Unaudited Information

This document contains financial

information regarding ODEON and its

fellow subsidiaries (the “Group”). Such

financial information may not have been

audited, reviewed or verified by any

independent accounting firm. The inclusion

of such financial information in this

document or any related presentation

should not be regarded as a representation

or warranty by ODEON, any of its

respective affiliates, advisors or

representatives or any other person as to

the accuracy or completeness of such

information’s portrayal of the financial

condition or results of operations by the

Group.

Non-GAAP information

We have presented certain non-GAAP

information in this document. As used in

this document, this information includes

‘‘EBITDA’’, which represents earnings

before interest, tax, depreciation,

amortisation, exceptional items and

strategic costs. Our management believes

that EBITDA is meaningful for investors

because it provides an analysis of our

operating results, profitability and ability to

service debt and because EBITDA is used

by our chief operating decision makers to

track our business evolution, establish

operational and strategic targets and make

important business decisions. In addition,

we believe that EBITDA is a measure

commonly used by investors and other

interested parties in our industry.

Forward-Looking Statements

This document includes forward-looking

statements. When used in this document,

the words “anticipate”, “believe”,

“estimate”, “forecast”, “expect”, “intend”,

“plan” and “project” and similar

expressions, as they relate to ODEON, its

management or third parties, identify

forward-looking statements. Forward-

looking statements include statements

regarding ODEON’s business strategy,

financial condition, results of operations,

and market data, as well as any other

statements that are not historical facts.

These statements reflect beliefs of

ODEON’s management, as well as

assumptions made by its management and

information currently available to ODEON.

Although ODEON believes that these

beliefs and assumptions are reasonable,

the statements are subject to numerous

factors, risks and uncertainties that could

cause actual outcomes and results to be

materially different from those projected.

These factors, risks and uncertainties

expressly qualify all subsequent oral and

written forward- looking statements

attributable to ODEON or persons acting

on its behalf.

2

2015 Q2 INVESTOR PRESENTATION

27 August 2015

ODEON & UCI CINEMAS GROUP

AGENDA

1 2015 Q2 and H1 highlights

2 Q2 markets & films

3 Future film slate

4 Strategic progress

5 Financial highlights

6 Current trading and outlook

7 Q&A

Paul Donovan

Group Chief

Executive Officer

Mark Way

Group Chief

Financial Officer

Ian Shepherd

Group Chief

Commercial Officer

2015 Q2 INVESTOR PRESENTATION

27 August 2015

3

2015 Q2 AND H1 HIGHLIGHTS

1

ODEON & UCI CINEMAS GROUP

Q2 HIGHLIGHTS CAPITALISING ON A STRONG MARKET

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Market Attendance1 up 9.2% - Strong performance of the Top 3 films

(Jurassic World, Fast & Furious 7 and

Avengers: The Age of Ultron )

- Weak Q2 last year, impacted by FIFA

World Cup

- Regional variations - i.e. Spain’s

Fiesta del Cine ran in May 2015 vs

March 2014

ODEON & UCI Paid Attendance

up 15.9% - Strategic actions contributing to

positive market share trends;

- Market share1 increased +1.3% pts

vs. 2014

Retail revenue2 up 23.9% - Driven by Group-wide retail and

product training initiatives

Total Revenue2 growth of 22.6%

EBITDA2 up by £12.0m on prior

year

1 At constant territory weighting and includes all territories

2 At constant FX rate

Q2

2015

Q2

2014

Vs LY

Fav/(Adv)

Market Weighted Attendance1 (m) 9.2%

Odeon & UCI Paid Attendance (m) 19.6 16.9 15.9%

Total Market Attendance Share1 19.6% 18.3% 1.3% pts

Retail Revenue2 (£m) 41.1 33.2 23.9%

Total Revenue2 (£m) 164.8 134.4 22.6%

EBITDA2 (£m) 12.9 0.9 1,313%

Average Ticket Price1,2 (£)(ATP) 5.69 5.44 4.6%

Retail Revenue Per Head1,2 (£)(RPH) 2.10 2.03 3.4%

5

ODEON & UCI CINEMAS GROUP

H1 HIGHLIGHTS CONTINUING TO OUTPERFORM

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Market Attendance1 up 7.3% - Driven by a strong slate (including

Jurassic World, Fifty Shades of Grey,

Fast & Furious 7 and Honig im Kopf)

ODEON & UCI Paid Attendance

up 13.8% - Outperformed market growth in both

quarters

- Market share up +1.1% pts vs. 2014

Retail Revenue2 up by 19.4%

Total Revenue2 grew by 17.1%

due to: - Improved market volumes

- Strategic actions across business

EBITDA2 more than doubled to

£37.3m

1 At constant territory weighting and includes all territories

2 At constant FX rate

H1

2015

H1

2014

Vs LY

Fav/(Adv)

Market Weighted Attendance1 (m) 7.3%

Odeon & UCI Paid Attendance (m) 42.9 37.7 13.8%

Total Market Attendance Share1 19.2% 18.1% 1.1% pts

Retail Revenue2 (£m) 85.0 71.1 19.4%

Total Revenue2 (£m) 348.7 297.7 17.1%

EBITDA2 (£m) 37.3 18.4 102.1%

Average Ticket Price1,2 (£)(ATP) 5.53 5.43 1.8%

Retail Revenue Per Head1,2 (£)(RPH) 1.98 1.93 2.5%

6

Q2 MARKETS AND FILMS

2

ODEON & UCI CINEMAS GROUP

UK & IRELAND Q2 MARKET ATTENDANCE UP 13%

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Total Market Attendance up 13%; Total Market GBOR grew

by 22%

- Jurassic World significantly outperformed; the first film ever to take

over $500m globally on opening weekend

- Unique marketing and CRM campaigns for ODEON customers

£17.3m

£17.3m

£38.4m

£48.3m

£51.2m

5

4

3

2

1

Jurassic World

X-Men: Days of Future Past

Avengers: The Age of Ultron

The Amazing Spider-Man 2

Fast & Furious 7

Godzilla

Pitch Perfect 2

Maleficent

Mad Max: Fury Road

Bad Neighbours

Q2 2015 GBOR

Q2 2014 GBOR

8

ODEON & UCI CINEMAS GROUP

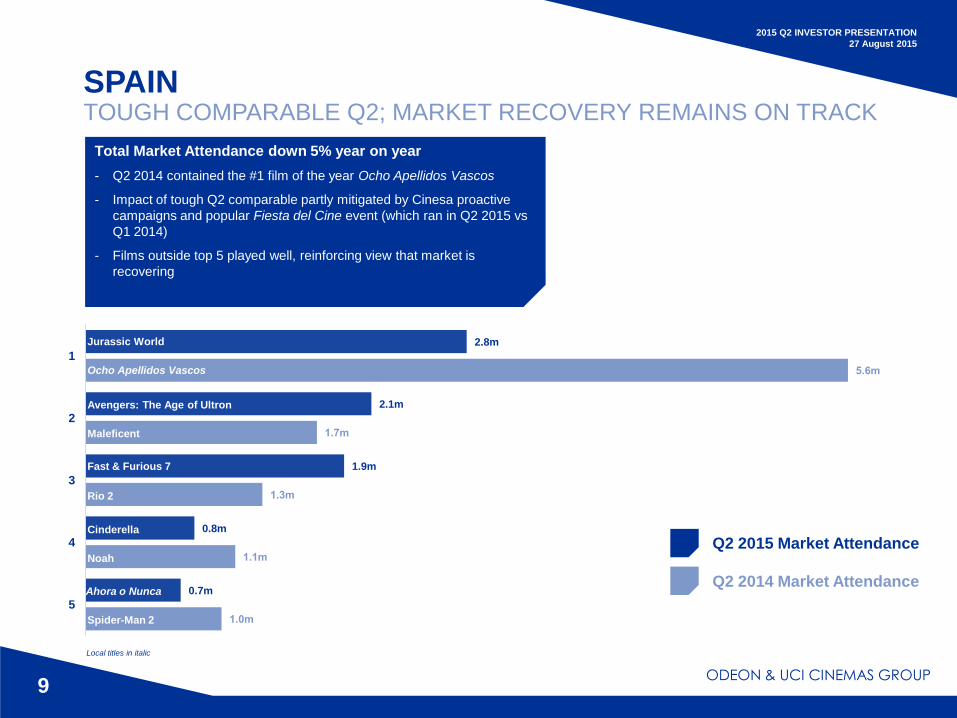

SPAIN TOUGH COMPARABLE Q2; MARKET RECOVERY REMAINS ON TRACK

2015 Q2 INVESTOR PRESENTATION

27 August 2015

0.7m

0.8m

1.9m

2.1m

2.8m

5

4

3

2

1

Jurassic World

Ocho Apellidos Vascos

Avengers: The Age of Ultron

Maleficent

Fast & Furious 7

Rio 2

Cinderella

Noah

Ahora o Nunca

Spider-Man 2

Q2 2015 Market Attendance

Q2 2014 Market Attendance

9

Total Market Attendance down 5% year on year

- Q2 2014 contained the #1 film of the year Ocho Apellidos Vascos

- Impact of tough Q2 comparable partly mitigated by Cinesa proactive

campaigns and popular Fiesta del Cine event (which ran in Q2 2015 vs

Q1 2014)

- Films outside top 5 played well, reinforcing view that market is

recovering

Local titles in italic

ODEON & UCI CINEMAS GROUP

GERMANY Q2 TOTAL MARKET UP 19%

2015 Q2 INVESTOR PRESENTATION

27 August 2015

1.1m

1.3m

2.4m

3.0m

3.9m

5

4

3

2

1

Fast & Furious 7

Rio 2

Jurassic World

Bad Neighbours

Avengers: The Age of Ultron

The Lego Movie

Pitch Perfect 2

The Other Woman

Der Nanny

Maleficent

Q2 2015 Market Attendance

Q2 2014 Market Attendance

10

Total Market Attendance up 19%

- Very strong top 3 titles

- Successful new retail combo offers and pricing mechanics

implemented by UCI Kinowelt team

Local titles in italic

ODEON & UCI CINEMAS GROUP

ITALY STRONG Q2 MARKET GROWTH DRIVEN BY TOP 3

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Total Market Attendance grew 3%

- Strong Top 3

- Popular new popcorn offer and “superticket” promotion implemented

in UCI Italy

0.7m

1.0m

1.9m

2.5m

2.9m

5

4

3

2

1

Fast & Furious 7

Maleficent

Avengers: The Age of Ultron

The Amazing Spider-Man 2

Jurassic World

Noah

Youth

X-Men: Days of Future Past

Se Dio Vuole

Rio 2

11

Local titles in italic

Q2 2015 Market Attendance

Q2 2014 Market Attendance

ODEON & UCI CINEMAS GROUP

Inside Out

Terminator Genisys

Mission: Impossible – Rogue Nation

Ant-Man

Man from U.N.C.L.E.

Spectre

The Hunger Games: Mockingjay – Part 2

Star Wars Episode VII – The Force Awakens

Fack ju Göhte 2

Ocho Apellidos Catalanes

STRONG FILM SLATE CONTINUES IN H2 2015

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Q3 Q4

12

ODEON & UCI CINEMAS GROUP

Finding Dory Independence Day: Resurgence

Fantastic Beasts and Where to Find Them The Secret Life of Pets

X-Men: Apocalypse Star Wars: Rogue One

Ice Age 5 Batman v Superman: Dawn of Justice

Alice Through the Looking Glass Zootopia

Captain America: Civil War Ghostbusters 3

2016 FILM SLATE LOOKS PROMISING

2015 Q2 INVESTOR PRESENTATION

27 August 2015

2016

13

ODEON & UCI CINEMAS GROUP

CONTINUED PROGRESS WITH STRATEGIC CHANGES

2015 Q2 INVESTOR PRESENTATION

27 August 2015

More targeted marketing activity alongside strategic promotions and

pricing

- New local marketing plans in key sites

- Further development of customer segmentation and targeted

activity

- Strategic pricing concepts trialled across all territories

Group-wide focus on delivering better guest experience in all

cinemas

- Net Promoter Score reporting now active in all territories

- Cinema team restructure in UK; savings reinvested in guest

experience

Improved digital offering

- First full quarter following removal of UK online booking fee

- Development of social media activity, including:

• Instagram launch in UK

• Mobile app in Italy

New retail initiatives and training

- Retail sales training delivered around the Group

- Successful trials of new combos, ticket bundles and products

Increased colleague engagement and training processes

- Further investment in engagement and communication

14

FINANCIAL HIGHLIGHTS

MARK WAY CFO

5

ODEON & UCI CINEMAS GROUP

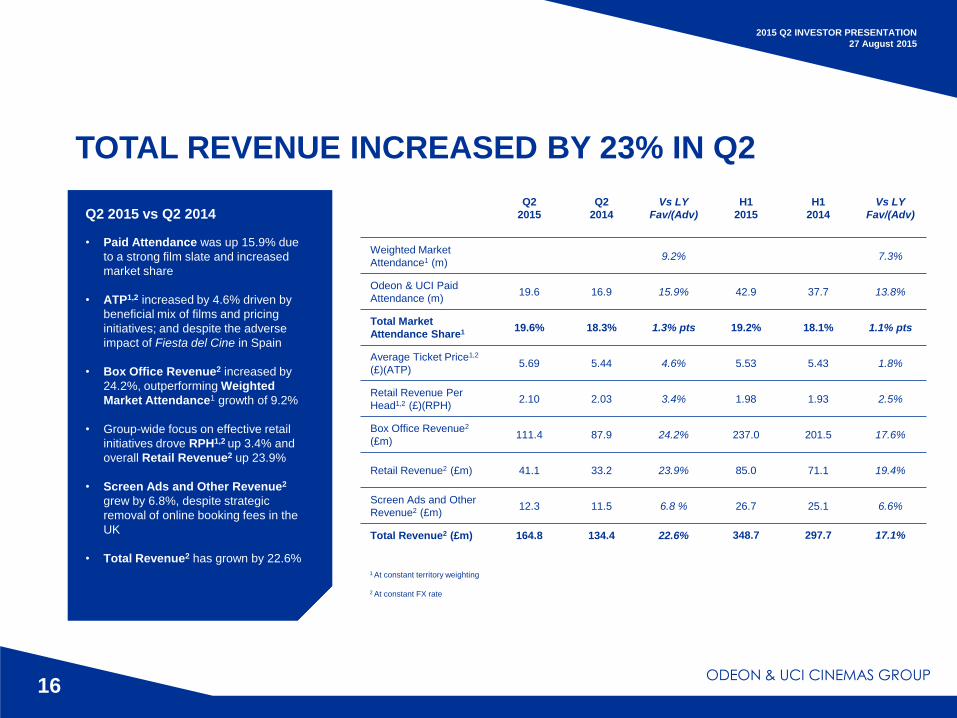

TOTAL REVENUE INCREASED BY 23% IN Q2

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Q2 2015 vs Q2 2014

• Paid Attendance was up 15.9% due

to a strong film slate and increased

market share

• ATP1,2 increased by 4.6% driven by

beneficial mix of films and pricing

initiatives; and despite the adverse

impact of Fiesta del Cine in Spain

• Box Office Revenue2 increased by

24.2%, outperforming Weighted

Market Attendance1 growth of 9.2%

• Group-wide focus on effective retail

initiatives drove RPH1,2 up 3.4% and

overall Retail Revenue2 up 23.9%

• Screen Ads and Other Revenue2

grew by 6.8%, despite strategic

removal of online booking fees in the

UK

• Total Revenue2 has grown by 22.6% 1 At constant territory weighting

2 At constant FX rate

Q2

2015

Q2

2014

Vs LY

Fav/(Adv)

H1

2015

H1

2014

Vs LY

Fav/(Adv)

Weighted Market

Attendance1 (m) 9.2% 7.3%

Odeon & UCI Paid

Attendance (m) 19.6 16.9 15.9% 42.9 37.7 13.8%

Total Market

Attendance Share1 19.6% 18.3% 1.3% pts 19.2% 18.1% 1.1% pts

Average Ticket Price1,2

(£)(ATP) 5.69 5.44 4.6% 5.53 5.43 1.8%

Retail Revenue Per

Head1,2 (£)(RPH) 2.10 2.03 3.4% 1.98 1.93 2.5%

Box Office Revenue2

(£m) 111.4 87.9 24.2% 237.0 201.5 17.6%

Retail Revenue2 (£m) 41.1 33.2 23.9% 85.0 71.1 19.4%

Screen Ads and Other

Revenue2 (£m) 12.3 11.5 6.8 % 26.7 25.1 6.6%

Total Revenue2 (£m)

164.8 134.4 22.6% 348.7 297.7 17.1%

16

ODEON & UCI CINEMAS GROUP

Q2 2015 vs Q2 2014

• Gross Profit Margin1 fell by (1.5%)

pts, in line with expectations, due to a

better film slate (resulting in higher

film hire charges) and product mix

• Operating Costs (excluding rent) as

a % of Total Revenue1 improved

year on year by 3.8% pts

• Rent1 costs reduced by 3.9% as a

result of successful negotiations with

landlords

• EBITDA1 increased by £12.0m driven

by a significant improvement in

market attendance, higher market

share, improved ATP & RPH and

ongoing cost control

EBITDA1 INCREASED BY £12M IN Q2

2015 Q2 INVESTOR PRESENTATION

27 August 2015

1 At constant FX rate

Q2

2015

Q2

2014

Vs LY

Fav/(Adv)

H1

2015

H1

2014

Vs LY

Fav/(Adv)

Gross Profit1 (£m) 103.9 86.7 19.8% 222.4 194.0 14.6%

Gross Profit Margin1 63.0% 64.5% (1.5%) pts 63.8% 65.2% (1.4%) pts

Operating Costs

(excluding rent)1 (£m) 61.8 55.4 (11.4%) 125.1 114.6 (9.2%)

Operating Costs

(excluding rent) as a %

of Total Revenue1

37.5% 41.3% 3.8% pts 35.9% 38.5% 2.6% pts

EBITDAR1 (£m) 42.1 31.3 34.5% 97.3 79.4 22.5%

Rent1 (£m) 29.2 30.4 3.9% 60.0 61.0 1.6%

EBITDA1 (£m) 12.9 0.9 1,313.3% 37.3 18.4 102.1%

EBITDA1 Margin 7.8% 0.7% 7.1% pts 10.7% 6.2% 4.5% pts

17

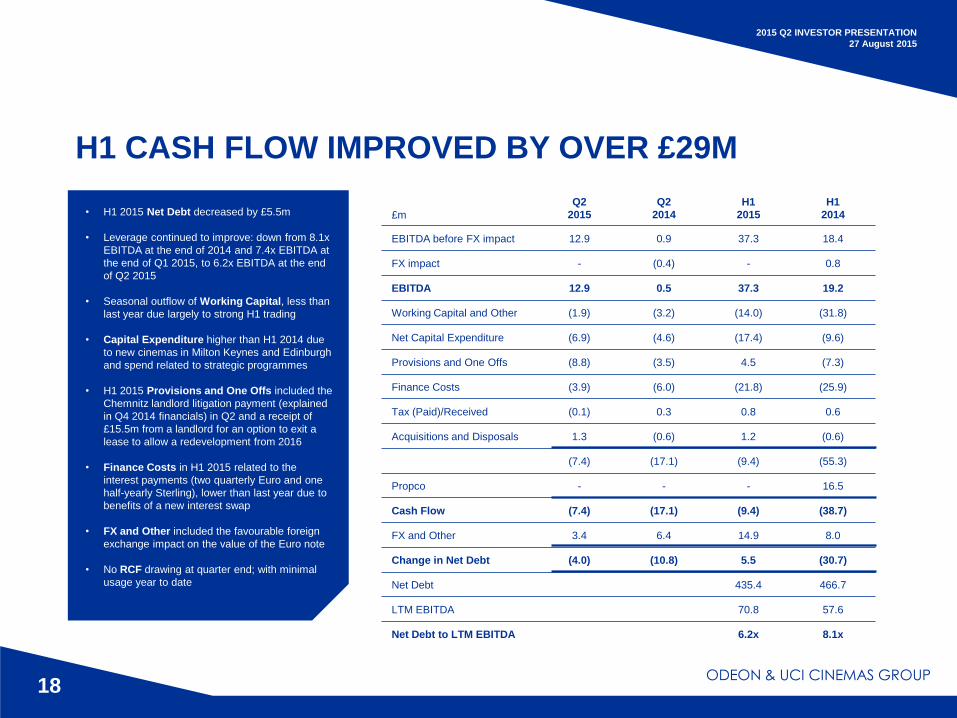

ODEON & UCI CINEMAS GROUP

• H1 2015 Net Debt decreased by £5.5m

• Leverage continued to improve: down from 8.1x

EBITDA at the end of 2014 and 7.4x EBITDA at

the end of Q1 2015, to 6.2x EBITDA at the end

of Q2 2015

• Seasonal outflow of Working Capital, less than

last year due largely to strong H1 trading

• Capital Expenditure higher than H1 2014 due

to new cinemas in Milton Keynes and Edinburgh

and spend related to strategic programmes

• H1 2015 Provisions and One Offs included the

Chemnitz landlord litigation payment (explained

in Q4 2014 financials) in Q2 and a receipt of

£15.5m from a landlord for an option to exit a

lease to allow a redevelopment from 2016

• Finance Costs in H1 2015 related to the

interest payments (two quarterly Euro and one

half-yearly Sterling), lower than last year due to

benefits of a new interest swap

• FX and Other included the favourable foreign

exchange impact on the value of the Euro note

• No RCF drawing at quarter end; with minimal

usage year to date

H1 CASH FLOW IMPROVED BY OVER £29M

2015 Q2 INVESTOR PRESENTATION

27 August 2015

£m

Q2

2015

Q2

2014

H1

2015

H1

2014

EBITDA before FX impact 12.9 0.9 37.3 18.4

FX impact - (0.4) - 0.8

EBITDA 12.9 0.5 37.3 19.2

Working Capital and Other (1.9) (3.2) (14.0) (31.8)

Net Capital Expenditure (6.9) (4.6) (17.4) (9.6)

Provisions and One Offs (8.8) (3.5) 4.5 (7.3)

Finance Costs (3.9) (6.0) (21.8) (25.9)

Tax (Paid)/Received (0.1) 0.3 0.8 0.6

Acquisitions and Disposals 1.3 (0.6) 1.2 (0.6)

(7.4) (17.1) (9.4) (55.3)

Propco - - - 16.5

Cash Flow (7.4) (17.1) (9.4) (38.7)

FX and Other 3.4 6.4 14.9 8.0

Change in Net Debt (4.0) (10.8) 5.5 (30.7)

Net Debt 435.4 466.7

LTM EBITDA 70.8 57.6

Net Debt to LTM EBITDA 6.2x 8.1x

18

CURRENT TRADING & OUTLOOK

PAUL DONOVAN CEO

6

ODEON & UCI CINEMAS GROUP

INVESTMENT FOR THE FUTURE

2015 Q2 INVESTOR PRESENTATION

27 August 2015

2015 capex in line with previous guidance

- New sites opened in H1 in Milton Keynes and Edinburgh

- New sites opening in H2 in Charlestown, Ireland; Marcianise and Bolzano in

Italy

- Refurbishing 25% sites in UK to improve guest experience and retail offer

Long term business development

- New sites signed for Orpington, UK (2016); Peterborough, UK (2017/18);

Mercedes Benz Arena, Berlin (2018); and Westfield, Milan (2018)

- Innovation Labs launched in London and Barcelona to develop ultimate

guest experience

- Unique partnership announced with National Film and Television School in

UK

20

ODEON & UCI CINEMAS GROUP

CURRENT TRADING AND OUTLOOK

2015 Q2 INVESTOR PRESENTATION

27 August 2015

Exciting film slate confirmed for H2

- Q3 looking better than last year, but not as strong as Q1 or Q2 2015

- Q4 film slate looks much stronger than last year:

• Return of proven Hollywood franchises such as Spectre, Hunger

Games and Star Wars

• Supported by local product such as Fack Ju Göhte 2 and Ocho

Apellidos Catalanes

- Market share continuing to track ahead of last year in Q3

- Ongoing investment in strategic initiatives to improve guest experience:

• UK site refurbishment & upgrades

• New digital infrastructure

• Retail enhancements

- Well positioned to deliver future growth

21

QUESTIONS

AND ANSWERS

7 Further questions can be addressed to:

Financial PR:

THANK YOU

ODEON & UCI CINEMAS GROUP