19

2016 FINANCIAL RESULTS March 15, 2017 MAIRE TECNIMONT - 2016 FINANCIAL RESULTS

2016 FINANCIAL RESULTS

March 15, 2017

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

DISCLAIMER

This document has been prepared by Maire Tecnimont S.p.A. (the “Company”) solely for use in the presentation of its financial results.

This document does not constitute or form part of any offer or invitation to sell, or any solicitation to purchase any shares in the Company.

The information contained and the opinions expressed in this document have not been independently verified. In particular, this document may contain forward-looking statements that are based on current estimates and assumptions made by the management of the Company to the best of its knowledge. Such forward-looking statements are subject to risks and uncertainties, the non-occurrence or occurrence of which could cause the actual results – including the financial condition and profitability of the Group – to differ materially from or be more negative than those expressed or implied by such forward-looking statements. This also applies to the forward-looking estimates and forecasts derived from third-party studies. Consequently, neither the Company nor its management can give any assurance regarding the future accuracy of the estimates of future performance set forth in this document or the actual occurrence of the predicted developments.

Dario Michelangeli, as Executive for Financial Reporting, declares - in accordance with paragraph 2, Article 154-bis of Legislative Decree No. 58/1998 (“Consolidated Finance Act”) - that the accounting information included in this presentation corresponds to the underlying accounting records.

The data and information contained in this document are subject to variations and integrations. Although the Company reserves the right to make such variations and integrations when it deems necessary or appropriate, the Company assumes no affirmative disclosure obligation to make such variations and integrations.

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

2

KEY MESSAGES

• Strong growth in Consolidated Revenues, EBITDA and Net Income

− Revenues: €2.4bn (+45.9%)

− EBITDA: €160.0m (+22.3%)

− Net Income: €85.3m (+94.8%)

• Steady marginality throughout 2016

− EBITDA Margin: 6.6%

• Dividends 2016: €28.4m (+97%)

• Significant deleverage

− NFP: €42.8m (vs. €125.6m as of 31/12/15)

• Solid order intake supported by increasing commercial pipeline

− Order Intake of €1.8bn

− Commercial pipeline of €31.5bn (+€2.9bn vs. 31/12/15)

3

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

KEY CONSOLIDATED FINANCIALS (€M)

130.8

160.0

2015 2016

1,669.6

2,435.4

2015 2016

43.8

85.3

2015 2016

126.2

184.7

Dec '15 Dec '16

125.6

42.8

Dec '15 Dec '16

Revenues EBITDA Net Income

NFP Net Worth

4

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

+45.9% +22.3% +94.8%

+€58.5m- €82.8 m

SUMMARY

1. Operational Performance Pierroberto Folgiero, CEO

2. Financial Results

Alessandro Bernini, CFO

3. Looking Ahead

Pierroberto Folgiero, CEO

2016 ORDER INTAKE

Name Client Country Business Type Value (€m)

Liwa Plastic Complex ORPIC Oman Petrochemical EPC 786

Pengerang Integrated

ComplexPetronas Malaysia Petrochemical EPC 308

Clean Fuel ProjectPetro

RabighSaudi Arabia Oil & Gas EPC 134

SumgayitSOCAR

PolymerAzerbaijan Petrochemical EPC 111

Wind Farm Utility Mexico Renewable Energy EPC 84

Others Various Various O&G/Petchem/Fertilizers E/EP 354

Total €1.8bn

6

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

BACKLOG

4,545

6,4556,065

406

438

451

31/12/14 31/12/15 31/12/16

TE&C Infrastructure

6,893

6,516

29%

39%

16%

13%

3%

Europe

Middle East

Others

Asia

Africa

Backlog by Geography(December 2016)

A Well Diversified Backlog that Provides a Solid Base to Future Revenues

Backlog by Business Unit(€m, 31/12/14-31/12/16)

7

TE&C

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

4,951

BACKLOG ANALYSIS – TE&C BUSINESS UNIT

Good mix between E, EP, and EPC Excellent cover for increasing revenues

Book to Bill Ratio* (31/12/14-31/12/16)

3.1

4.2

2.7

31/12/14 31/12/15 31/12/16

126 80

846 681

5,4835,304

31/12/15 31/12/16

E EP EPC

6,4556,065

972 761

Backlog by Type (€m, 31/12/15-31/12/16)

*Defined as the ratio between Backlog and LTM Revenues

*Defined as the ratio between Backlog and LTM Revenues8

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

OUTLOOK ON COMMERCIAL ACTIVITY (TE&C)

Commercial Activity (€bn, Dec ’13-Dec ‘16)

9.512.0

17.9 19.04.3

7.4

6.2 5.5

5.2

6.6

4.57.0

Dec '13 Dec '14 Dec '15 Dec '16

Prospect, Prequalification & Pre-Tendering Tendering Tendered

28.6

26.0

19.0

31.5

Our Commercial Pipeline Has Been Increasing since 2013

9

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

&

COMMERCIAL ACTIVITY’S GEOGRAPHICAL BREAKDOWN (TE&C)*

North and CentralAmericaPOLYOLEFIN

South AmericaGAS TREATMENT

POLYOLEFIN AfricaFERTILIZER

POLYOLEFIN

GAS TREATMENT

REFINERY

Middle EastFERTILIZER

POLYOLEFIN

GAS TREATMENT

REFINERY

AsiaFERTILIZER

POLYOLEFIN

GAS TREATMENT

C.I.S.FERTILIZER

POLYOLEFIN

GAS TREATMENT

REFINERYEuropePOLYOLEFIN

REFINERY

Our commercial activity continues to be very focused on implementing our current strategic approach

*Figures include prospect prequalification and pre-tendering, tendering, and tendered

10

€1.3bn

€1.6bn

€0.5bn

€9.2bn

€8.8bn

€6.5bn

€3.6bn

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

SUMMARY

1. Operational Performance

Pierroberto Folgiero, CEO

2. Financial Results Alessandro Bernini, CFO

3. Looking Ahead

Pierroberto Folgiero, CEO

CONSOLIDATED INCOME STATEMENT

€m 2015 2016 ∆%

Revenues 1,669.6 2,435.4 45.9%

Business Profit 211.2 241.2 14.2%

G&A (73.9) (76.2) 3.1%

R&D (6.4) (5.0) (21.9%)

EBITDA 130.8 160.0 22.3%

EBITDA % 7.8% 6.6%

EBIT 115.4 152.6 32.2%

Net Financial Charges (37.8) (18.8) (50.3%)

Profit Before Taxes 77.6 133.8 72.4%

Tax Provision (33.8) (48.5)

Effective Tax Rate 43.6% 36.3%

Net Income 43.8 85.3 94.8%

12MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

NET FINANCIAL POSITION AND CASH FLOW BRIDGE

125.6

20.6

18.8 42.8

Net Debt

Dec-2015

Operating

Cash Flows

Forex Dividends Capex Net Financial

Charges

Net Debt

Dec-2016

14.416.3

152.9

Cash Flow Bridge (€m)

11.9 28.2

73.175.1

40.6

-60.5

Net Bank DebtConv. BondDerivatives

Dec 2015 Dec 2016

-82.8

Net Financial Position (€m)

13

125.642.8

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

SUMMARY

1. Operational Performance

Pierroberto Folgiero, CEO

2. Financial Results

Alessandro Bernini, CFO

3. Looking Ahead Pierroberto Folgiero, CEO

GLOBAL & TECHNOLOGICAL LEADERSHIP

163

30%

Ammonia and Urea Plants

Market share in polyolefin plants

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

completed since 1924

40%Market share in

LDPE plants

PETROCHEMICALS FERTILIZERS

Well rooted technology orientation: market leader (#1)

for installed capacity

WORLD CLASS TRACK RECORD

in Large Gas Treatment Plants and Refinery

Process Units

OIL & GAS

WELL RECOGNIZED LEADERSHIP

in Licensing hydrogen technology and in licensing Sulphur Recovery and Tail Gas Treatment Technology

* Data are based on corporate analysis

54%Market share in

licensing urea plants technology

(#1 worldwide)*

34%Market share

in licensing urea granulation technology

(#2 worldwide)*

62 Polyethylene Plants

117 Polypropylene Plants

Since 1970

+1,100Individual Patents

Strong commitment to technology development

230Hydrogen and Sulphur Recovery

Unit Projects completed

Since 1971

15

OUR OPERATIONS ARE DRIVEN BY POSITIVE BUSINESS TRENDS

• Gas monetization: Cheap feedstock supports owner’s investment attractiveness

• Strong demand for plastics-based products

• Gas monetization

• Demography and agricultural modernization driving long term

demand for nitrogen-based fertilizers

• Technology barriers

• Midstream Oil and Gas Treatment

• Refining: Revamping & Capacity upgrade

• Integration between petchem and refining

16

FERTILIZERS

PETCHEM

OIL & GAS

MA

IRE

TE

CN

IMO

NT

–20

16 F

INA

NC

IAL

RE

SU

LTS

MAIRE TECNIMONT HAS BEEN OUTPERFORMING THE SECTOR

Maire Tecnimont’s Relative Performance, 6/20/14 – 3/13/17

Maire Tecnimont BEUOILS Index WTI Future

Correlation Coefficient MT – BEUOILS = — 0.26 MT – WTI Future = — 0.35 BEUOILS – WTI Future= + 0.97

Our Stock is Not Correlated to the Oil Price

20

40

60

80

100

120

140

Jun-14

Jul-14

Aug-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

17

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

Mar-17

Source: Bloomberg. BEUOILS Index Components: Subsea 7, Saipem, Petrofac, John Wood Group, SBM, Amec FW, TGS

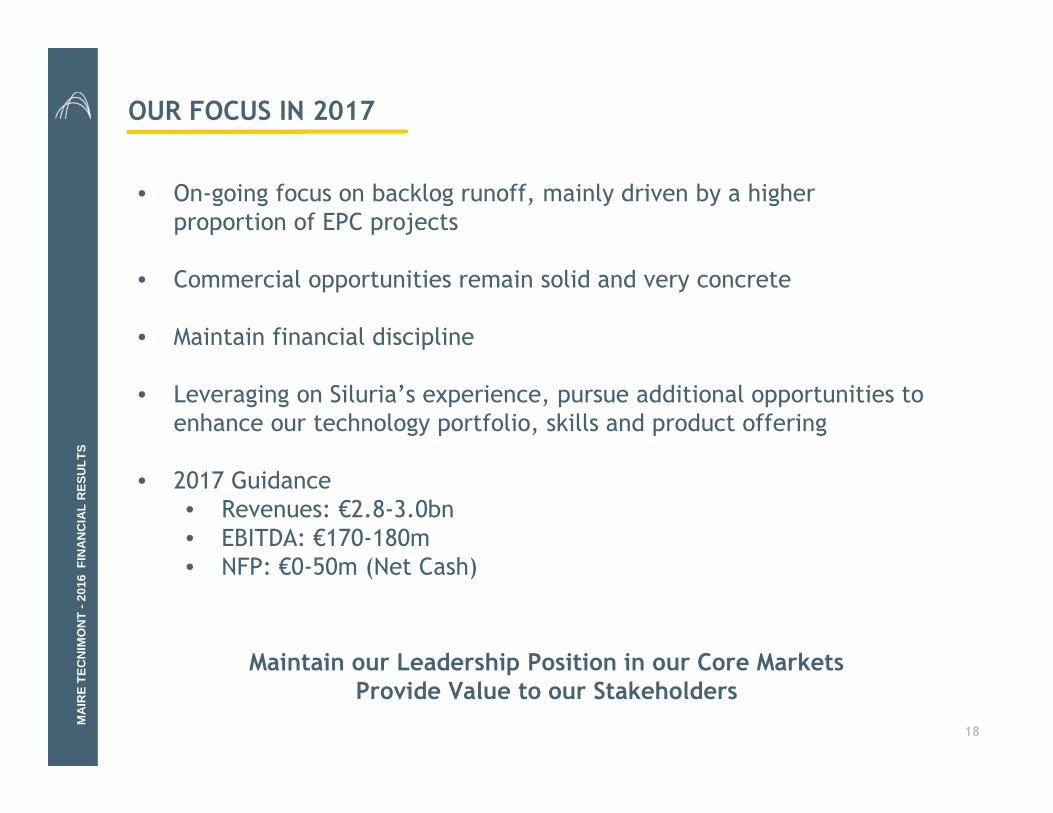

OUR FOCUS IN 2017

• On-going focus on backlog runoff, mainly driven by a higher

proportion of EPC projects

• Commercial opportunities remain solid and very concrete

• Maintain financial discipline

• Leveraging on Siluria’s experience, pursue additional opportunities to

enhance our technology portfolio, skills and product offering

• 2017 Guidance

• Revenues: €2.8-3.0bn

• EBITDA: €170-180m

• NFP: €0-50m (Net Cash)

18

Maintain our Leadership Position in our Core MarketsProvide Value to our Stakeholders

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS

Maire Tecnimont Group’s Headquarters

Via Gaetano De Castillia, 6A

20124 Milan

www.mairetecnimont.com

Investor Relations T +39 02 6313-7823 02 [email protected]

MA

IRE

TE

CN

IMO

NT

-20

16 F

INA

NC

IAL

RE

SU

LTS