41

2016 First Quarter revenue 21 April 2016 2020 Full-year results February 17, 2021

2016

First Quarter

revenue

21 April 2016 2020 Full-year results

February 17, 2021

DISCLAIMER

This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction.

Certain information contained in this document may include projections and forecasts. They express objectives based on current assessments and

estimates of the Group’s executive management which are subject to numerous factors, risks and uncertainties. Consequently, reported figures and

assessments may differ significantly from projected figures. The following factors among others set out in the Universal Registration Document (Document

d’Enregistrement Universel) filed with the French Financial Markets Authority (Autorité des Marchés Financiers - AMF) on March 26, 2020 which is

available on Kering’s website at www.kering.com may cause actual figures to differ materially from projected figures: any unfavourable development

affecting consumer spending in the activities of the Group in France and abroad, notably for products and services sold by our Luxury brands, the events,

crises, fears, and resulting costs of complying with environmental, health and safety regulations and all other regulations with which Group companies are

required to comply; the competitive situation on each of our markets; exchange rate and other risks related to international activities; risks arising from

current or future litigation. Kering gives no commitment to updating and/or revising and/or commenting any projections and forecasts, or their impact on the

results and perspectives of the Group, which may be contained in this presentation.

The information contained in this document has been selected by the Group’s executive management to present Kering’s FY2020 results. This document

has not been independently verified. Kering makes no representation or undertaking as to the accuracy or completeness of such information. None of the

Kering or any of its affiliates representatives shall bear any liability (in negligence or otherwise) for any loss arising from any use of this presentation or its

contents or otherwise arising in connection with this presentation.

IN NO WAY DOES KERING ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION

PROVIDED IN THIS PRESENTATION. INFORMATION IN THIS PRESENTATION, INCLUDING FORECAST FINANCIAL INFORMATION, SHOULD NOT BE

CONSIDERED AS ADVICE OR A RECOMMENDATION TO INVESTORS OR POTENTIAL INVESTORS IN RELATION TO HOLDING, PURCHASING OR

SELLING SECURITIES OR OTHER FINANCIAL PRODUCTS OR INSTRUMENTS AND DOES NOT TAKE INTO ACCOUNT YOUR PARTICULAR

INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR NEEDS. BEFORE ACTING ON ANY INFORMATION YOU SHOULD CONSIDER THE

APPROPRIATENESS OF THE INFORMATION HAVING REGARD TO THESE MATTERS, ANY RELEVANT OFFER DOCUMENT AND IN PARTICULAR,

YOU SHOULD SEEK INDEPENDENT FINANCIAL ADVICE. ALL SECURITIES AND FINANCIAL PRODUCT OR INSTRUMENT TRANSACTIONS INVOLVE

RISKS, WHICH INCLUDE (AMONG OTHERS) THE RISK OF ADVERSE OR UNANTICIPATED MARKET, FINANCIAL OR POLITICAL DEVELOPMENTS

AND, IN INTERNATIONAL TRANSACTIONS, CURRENCY RISK. READERS ARE ADVISED TO REVIEW THE COMPANY’S UNIVERSAL REGISTRATION

DOCUMENT AND THE COMPANY'S APPLICABLE AMF FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISION.

INTRODUCTION

FRANÇ OIS-HENRI PINAULT

CHAIRMAN & CEO

4

2020 FULL-YEAR RESULTS

A YEAR OF

YIELDING RESILIENT

FINANCIAL PERFORMANCES

REINFORCING OUR VISION

OF LUXURY

CONFIRMING OUR STRATEGY

& BUSINESS MODEL

READY TO COME OUT OF THE CRISIS WITH STRENGTHENED POSITIONS

TO LEVERAGE THE REBOUND AND MAXIMIZE BRAND POTENTIAL

DISRUPTION

INTRODUCTION

February 17, 2021

ANALYSIS OF RESULTS

JEAN-MARC DUPLAIX

GROUP CHIEF F INANCIAL OFFICER

6

RESILIENCE THANKS TO SCALE & AGILITY

Western Europe

28% (-28%)

North America

21% (-8%)

Asia Pacific

38% (-7%)

RoW

6% (-16%)

Japan

7% (-29%)

€3,135m

-34.4% vs. last year

EBIT margin: 23.9%

FCF AND NET DEBT (€m)

• Group CAPEX: €787m, 6.0% of revenue

• Strong FCF +38% YoY: €2,105m, WCR tightly managed with inventories undercontrol

• Net debt down at €2.1bn (excl.leaseliabilities)

€13,100m

-17.5% reported

-16.4% comparable*

o/w Q4 -5% comparable

GROUP REVENUE (€m)

As a % of FY20 revenue and (% comparable growth)

NET DEBTFCF FROM OPERATIONS

• Balancing profitability protection & investment priorities

• Solid H2 margin: Luxury Houses at 30.7%

• Yielding resilient FY EBIT margin

GROUP RECURRING OPERATING INCOME (€m)

7,6385,378

8,246

7,722

FY19 FY20

H2

H1

15,884

FY20FY19

1,521

2,105

YE 19 YE 20

2,812

2,149

13,100

-30.1% comp

-3.2% comp

* At constant scope and exchange rates

2,253952

2,525

2,183

FY19 FY20

H2

H1

4,778

3,135

28.3% margin

17.7% margin

30.6% margin

29.5% margin

February 17, 2021

7

OVERVIEW

-19%

-42%

0% -3%

Q1 Q2 Q3 Q4

12%

42%

5% 10%

Q1 Q2 Q3 Q4

WHOLESALE AND OTHER (COMPARABLE)RETAIL (COMPARABLE)

78% 22%

-16%

INCL. E-COMMERCE UP 67%,

REACHING 13% OF RETAIL SALES

-17%

WHOLESALE

-29%

ROYALTIES & OTHER

%

OF WW STORES CLOSED

-7%

-48%

-5% -12%

Q1 Q2 Q3 Q4

REVENUE

LUXURY HOUSES FY20 REVENUE BY CHANNEL

February 17, 2021

LUXURY HOUSES

FOCUS ON RETAIL

WESTERN

EUROPE-14%

-66%

-41% -40% -41%

Q1 Q2 Q3 Q4 FY

-7%

-49%

+44%

+13%0%

-17%

-62%

-23%-10%

-28%

Q1 Q2 Q3 Q4 FY

-30%-12%

+18% +17%

-2%

Q1 Q2 Q3 Q4 FY

-9%

-70%

+20%+8%

-13%

BY REGION (COMPARABLE GROWTH)

NORTH

AMERICA

JAPAN

ASIA

PACIFIC

ROW

8February 17, 2021

+42%

+89% +89%

+35%

Western Europe North America APAC Japan

9

LUXURY HOUSES

DIGITAL PENETRATION CONTINUING TO RISE

IN ALL REGIONS

INCREASED PENETRATION

E-COMMERCE COMPARABLE REVENUE GROWTH E-COMMERCE REVENUE AS A % OF RETAIL SALES

FY 2020 E-COMMERCE COMPARABLE REVENUE GROWTH E-COMMERCE REVENUE AS A % OF RETAIL SALES

ONLINE ACCELERATION

+21%

+72%

+102%

+72%

Q1 20 Q2 20 Q3 20 Q4 20

7%

13%

FY 2019 FY 2020

9%

13%

3% 3%

22%24%

6% 6%

Western Europe North America APAC Japan

FY 2019 FY 2020

February 17, 2021

10

GUCCI

BUILDING SUSTAINABLE GROWTH

• H2 revenue trend improving

– Q4 reta i l -7%, dr ivers unchanged. 9 net s tore c losures in quar ter and 4 in FY

– W holesale rat ional izat ion ongoing

• Cost discipline and brand reinvestment: H2 EBIT margin 38.6%

• CAPEX adapted to the environment and project prioritization

Asia

Pacific

2020Royalties

and others

Japan

-8%

Wholesale2019 Western

Europe

RoWNorth

America

9,628

-47% 0% -32%-26%

-33%

7,441

-29%

Retail (87% of sales): -19% In €m 2020 2019 Change

Revenue

% comparable

7,441 9,628 -22.7%

-21.5%

Recurring operating income

Margin (%)

2,615

35.1%

3,947

41.0%

-33.8%

-5.9pt

Gross CAPEX

As % of revenue

206

2.8%

337

3.5%

-39.0%

-0.7pt

-45% +13% -20% +8% -2% -31% -3%of which Q4 20

comp growthTOTAL

-10%

REVENUE CHANGE BY REGION AND CHANNEL

(in €m, and comparable growth in %)

FULL-YEAR KEY FIGURES

February 17, 2021

11

SAINT LAURENT

-2%-20%

1,744

2,049

-34% -2% +1%-14%

-24%

In €m 2020 2019 Change

Revenue

% comparable

1,744 2,049 -14.9%

-13.8%

Recurring operating income

Margin (%)

400

22.9%

562

27.4%

-28.9%

-4.5pt

Gross CAPEX

As % of revenue

53

3.0%

98

4.8%

-46.2%

-1.8pt

DEMONSTRATING RESILIENCE AND POTENTIAL

• FY20 revenue decline limited to H1 with H2 at +2% comp

– Q4 reta i l +5%; wholesale down on scheduled later Spr ing shipments and s tar t of rat ional izat ion

– Successful W inter 20 col lec t ion, cont inued development in APAC

– Fast-growing e-commerce fur ther propel led by m igrat ion on fu l ly owned plat form in Q4

• Pursuing ambitious growth investment plans (communications, store expansion)

• CAPEX dedicated to footprint expansion with a focus on Mainland China and Korea

REVENUE CHANGE BY REGION AND CHANNEL

(in €m, and comparable growth in %)

Asia

Pacific

2020Royalties

and others

Japan Wholesale2019 Western

Europe

RoWNorth

America

-31% +19% +4% +30% +26% -14% -8%of which Q4 20

comp growthTOTAL

+1%

Retail (69% of sales): -13%

February 17, 2021

FULL-YEAR KEY FIGURES

12

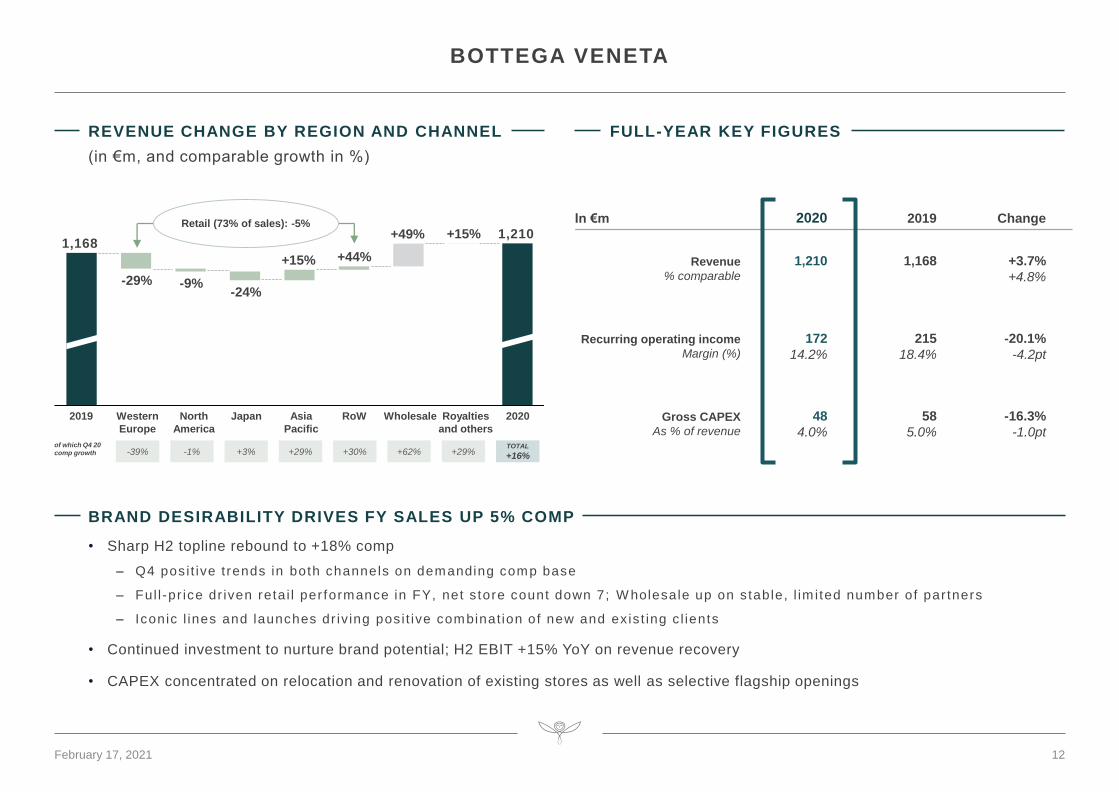

BOTTEGA VENETA

+49%1,168

-29% -9%-24%

+15% +44%

+15% 1,210

In €m 2020 2019 Change

Revenue

% comparable

1,210 1,168 +3.7%

+4.8%

Recurring operating income

Margin (%)

172

14.2%

215

18.4%

-20.1%

-4.2pt

Gross CAPEX

As % of revenue

48

4.0%

58

5.0%

-16.3%

-1.0pt

BRAND DESIRABILITY DRIVES FY SALES UP 5% COMP

• Sharp H2 topline rebound to +18% comp

– Q4 pos i t ive t rends in both channels on demanding comp base

– Ful l -pr ice dr iven reta i l per formance in FY, net s tore count down 7; W holesale up on s table, l im i ted number of par tners

– Iconic l ines and launches dr iv ing pos i t ive combinat ion of new and ex is t ing c l ients

• Continued investment to nurture brand potential; H2 EBIT +15% YoY on revenue recovery

• CAPEX concentrated on relocation and renovation of existing stores as well as selective flagship openings

REVENUE CHANGE BY REGION AND CHANNEL

(in €m, and comparable growth in %)

Asia

Pacific

2020Royalties

and others

Japan Wholesale2019 Western

Europe

RoWNorth

America

-39% -1% +3% +29% +30% +62% +29%of which Q4 20

comp growthTOTAL

+16%

Retail (73% of sales): -5%

February 17, 2021

FULL-YEAR KEY FIGURES

13

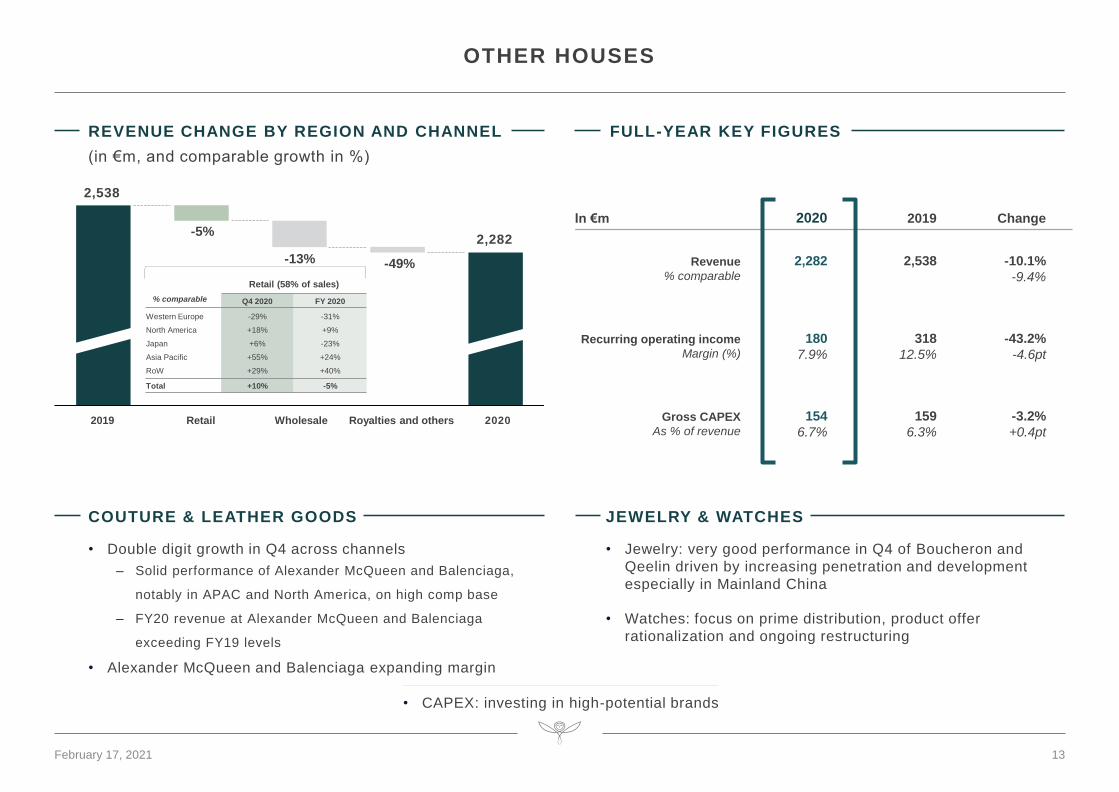

OTHER HOUSES

COUTURE & LEATHER GOODS

• Double digit growth in Q4 across channels

– Solid performance of Alexander McQueen and Balenciaga,

notably in APAC and North America, on high comp base

– FY20 revenue at Alexander McQueen and Balenciaga

exceeding FY19 levels

• Alexander McQueen and Balenciaga expanding margin

Royalties and othersRetail2019 2020Wholesale

-49%

2,538

-5%

-13%

2,282

JEWELRY & WATCHES

• Jewelry: very good performance in Q4 of Boucheron and

Qeelin driven by increasing penetration and development

especially in Mainland China

• Watches: focus on prime distribution, product offer

rationalization and ongoing restructuring

In €m 2020 2019 Change

Revenue

% comparable

2,282 2,538 -10.1%

-9.4%

Recurring operating income

Margin (%)

180

7.9%

318

12.5%

-43.2%

-4.6pt

Gross CAPEX

As % of revenue

154

6.7%

159

6.3%

-3.2%

+0.4pt

• CAPEX: investing in high-potential brands

REVENUE CHANGE BY REGION AND CHANNEL

(in €m, and comparable growth in %)

% comparable

Retail (58% of sales)

Q4 2020 FY 2020

Western Europe

North America

Japan

Asia Pacific

RoW

-29%

+18%

+6%

+55%

+29%

-31%

+9%

-23%

+24%

+40%

Total +10% -5%

February 17, 2021

FULL-YEAR KEY FIGURES

24

14

CORPORATE & OTHER

In €m 2020 2019

Recurring operating income

Underlying result

Corporate Long-term incentive plan

(232)

(185)

(47)

(264)

(196)

(68)

Gross CAPEX 326 304

REVENUE REBOUND IN H2 AND EBIT CONTRIBUTION IMPROVING

• Kering Eyewear revenue improving in H2

– Fur ther extens ion of brand por t fol io wi th the addi t ion of Chloé and Dunhi l l , SS 2021 f i rs t co l lec t ion avai lable s ince January

– Launch of F lagship s tore on Tmal l to fur ther establ ish Ker ing Eyewear on Chinese market

• Strict discipline on corporate costs, Kering Eyewear EBIT contribution increasing

• CAPEX driven by continued investment in logistics & technology

Royalties and

intragroup

eliminations

487

FY20 Total

Corporate

and Other

FY20 Kering

Eyewear

total sales

Other revenueFY20 Kering

Eyewear

consolidated

sales

423

FY19 Total

Corporate

and Other

-88

399

501

-15% comp

-18% comp

REVENUE CHANGE BY REGION AND CHANNEL

(in €m, and comparable growth in %)

February 17, 2021

FULL-YEAR KEY FIGURES

15

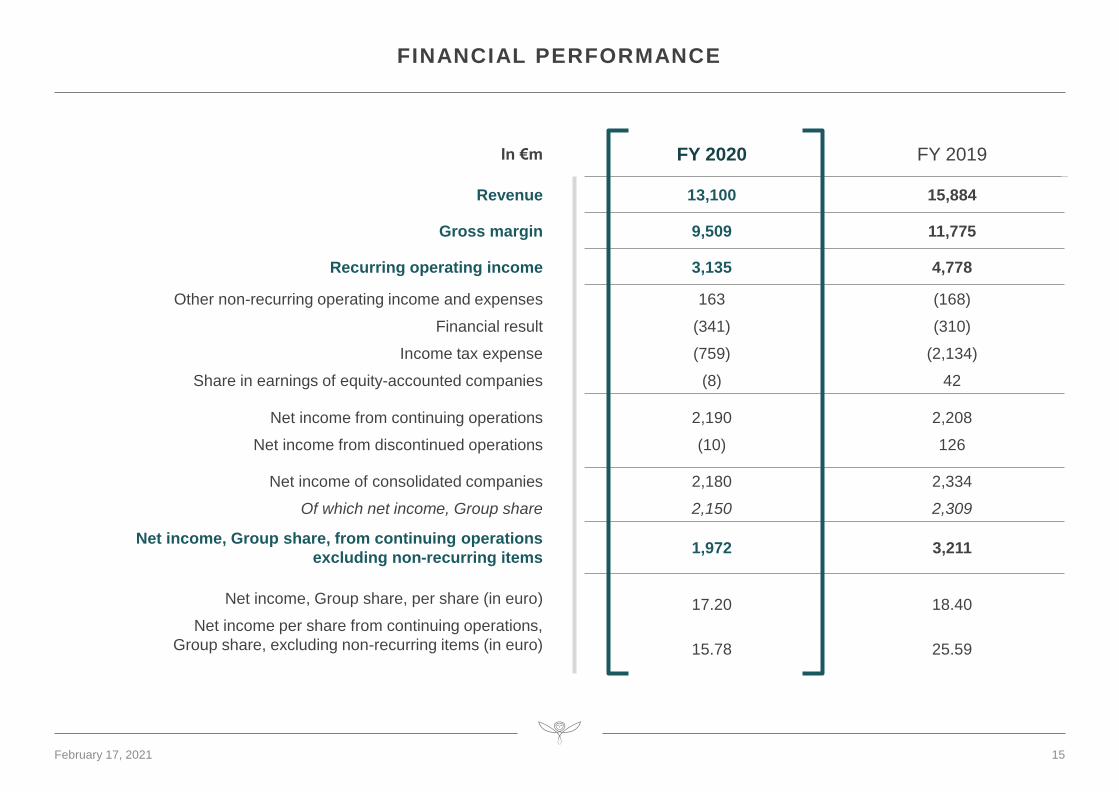

FINANCIAL PERFORMANCE

In €m FY 2020 FY 2019

Revenue 13,100 15,884

Gross margin 9,509 11,775

Recurring operating income 3,135 4,778

Other non-recurring operating income and expenses

Financial result

Income tax expense

Share in earnings of equity-accounted companies

163

(341)

(759)

(8)

(168)

(310)

(2,134)

42

Net income from continuing operations

Net income from discontinued operations

2,190

(10)

2,208

126

Net income of consolidated companies

Of which net income, Group share

2,180

2,150

2,334

2,309

Net income, Group share, from continuing operations

excluding non-recurring items 1,972 3,211

Net income, Group share, per share (in euro)

Net income per share from continuing operations,

Group share, excluding non-recurring items (in euro)

17.20

15.78

18.40

25.59

February 17, 2021

In €m FY 2020 FY 2019

Cash flow before taxes, dividends and interests

Change in working capital requirement

Income tax paid

4,280

45

(1,436)

5,936

(557)

(2,903)

Net cash flow from operating activities 2,889 2,476

Acquisition of fixed operating assets, net (784) (955)

Free cash flow from operations 2,105 1,521

16

FREE CASH FLOW FROM OPERATIONS

February 17, 2021

17

CAPITAL EMPLOYED AND OPERATING WORKING CAPITAL

EQUITY

€12,035M

NETDEBT

€2,149M

INVENTORIES

€2,846M

RECEIVABLES

€824M

DEBT-TO-EQUITY RATIO

17.8%

CAPITAL EMPLOYED

€14,184M

OPERATING WORKING CAP

€3,004M22.9%*

PAYABLES

€666M

* of FY20 group revenue

February 17, 2021

FY 2020 NET DEBT BRIDGE

18

CHANGE IN NET FINANCIAL DEBT

16754

900

1,009

-32

Net debt at

December

31, 2019

FCF from

operations

Dividend paid Disposal of

5.83% of Puma

Net financial

investments

and other

Net interest paid

and dividends

received

Acquisition of

Kering shares

Lease

repayment and

related interests

Net debt at

December

31, 2020

2,812

-2,105

-656

2,149

In €m and Net Debt / EBITDA ratio

February 17, 2021

0.5x

0.5x

STRENGTHENED POSITIONS TO LEVERAGE THE REBOUND

FRANÇOIS-HENRI PINAULT CHAIRMAN & CEO

JEAN-FRANÇOIS PALUS GROUP MANAGING DIRECTOR

A DEMAND-DRIVEN

SUPPLY CHAIN

OMNICHANNEL

AS A MUST

NUMEROUS

TOUCHPOINTS

NEW TECHNOLOGIES

20

KERING IS WELL POSITIONED TO LEVERAGE THE NEW LUXURY ENVIRONMENT

WE CARE,

WE COLLABORATE,

WE CREATE

WE INCREASE

CONTROL OVER

DISTRIBUTION

WE INVESTIN GROWTH PLATFORMS

OUR BRANDS DEPLOY INNOVATIVE MARKET

APPROACHES

YOUNG AND GLOBAL

CONSUMERS

INCREASED DEMAND

FOR TRANSPARENCY

ACCELERATING TRENDS COMFORTING OUR STRATEGY

February 17, 2021

21

PROGRESSING ON OUR SUSTAINABILITY COMMITMENTS

• 29% reduction in our environmental footprint (EP&L intensity 2015-19)

• 91% traceability for our key raw materials

• Biodiversity commitments to protect 2 million hectares (6x our total land footprint)

• Fashion Pact commitments: 3 pillars, 7 key objectives

• 55% women managers within the Group

• D&I committees in each house/entity with Management Committee sponsors

• Fully mobilized against Covid-19 pandemic: financial donations, ensuring safety and well-being of our employees worldwide, supporting our suppliers

• Anti-domestic violence policy to protect women and families

• New collections from recycled or sustainably sourced materials: Gucci Off the Grid, Balenciaga Archetypes

• Adherence to the “Vision of a circular economy for fashion” of the Ellen MacArthur Foundation

• New business models

2021• CONTINUED TRANSPARENCY WITH STAKEHOLDERS

• EXTENSION OF OUR ENVIRONMENTAL FOOTPRINT TO THE CONSUMER USE AND END-OF-LIFE PHASES OF OUR PRODUCTS

• ALIGNMENT OF OUR CLIMATE STRATEGY WITH THE 1.5° SCENARIO

CARE

COLLABORATE

CREATE

WE…

February 17, 2021

22

DEPLOYING INNOVATIVE MARKET APPROACHES

COLLECTIONS& PRODUCTS

• New calendars and Fashion Show expressions

• Adaptation of collections, phasing& merchandising structure

ASSETDIGITIZATION

• Design, prototyping, content

• Virtual Showrooms

CLIENTEXPERIENCE

• Immersive experiences: virtual fitting, Augmented Reality, gaming

• Pop up & pop in

• Clienteling actions & events

• Distant selling

• Personalized & localized CRM & AI programs

BRANDENGAGEMENT

• Increase brand visibility, nurture desirability on relevant platforms

& networks

• Adapted marketing & comms strategy, social commerce,

livestreaming

February 17, 2021

23

INCREASING CONTROL OVER DISTRIBUTION

• Wider range of services

• Improved depth and breadth of assortment

• Leveraging a single view of the client

OMNICHANNEL

February 17, 2021

STRATEGICWHOLESALE REDUCTION

• Beyond short-term impacts of Covid, notably Travel Retail

• Long-term strategy to reduce Wholesale through management

of orders, downsizing of number of doorsand retailization of offline and online partners

• Focus on brand.com

• Successful internalization ongoing

• Shift to e-concessions and opening of new e-concessions

FAST-GROWING

ONLINE RETAIL

RETAIL FOOTPRINT POTENTIAL

• # DOS at YE: 1,433 (+52 net)

• Constant assessment to identify new opportunities and adapt network

• # DOS roughly stable at Gucci & BV

• Large potential at YSL, AMQ, BAL & Boucheron

24

INVESTING IN GROWTH PLATFORMS

YE 2019New Wayne, NJ (USA) Distribution Center

PRODUCTION & MANUFACTURING

• Investing in production footprint in Italy to increase capacity and raise control over value chain

A DEMAND-DRIVEN SUPPLY CHAIN INFORMATION SYSTEMS

• AI powered models to improve short-term forecast and long-term demand planning: roll-out in regions and expansion to new product categories

• Logistics transformation program ongoing as planned

• Real-time access to a single sourceof data thanks to ERP rollout

• State-of-the art and integrated IT solutions

• Cybersecurity

2021-23 (tbc)APACand Middle-East

H1 2020Trecate (Italy) DC Phase I

Q3 2021Trecate (Italy) DC Phase II

2019-2021SAP rolloutin EMEA

2020-2022SAP rollout in AMER and APAC

February 17, 2021

STRONGCASH FLOW GENERATION

• Optimize Working Capital

• Pursue Group investments withCapex-to-sales ratioat c.6-7%

• Continued optimization of ROCE

UNCHANGED FINANCIAL PRIORITIES

BALANCEDCAPITALALLOCATION

• Consistent dividend policy

• Ability to seize M&A opportunities

• Agile in returning additional cashto shareholders

SUSTAINORGANIC GROWTH…

• Creative brands resonating with customers

• Market share gains

• Unleash potentialof our Houses according to their maturity level

… AT SOLID PROFITABILITY LEVEL

• Invest for growth: products, stores,client experience and engagement, talents, digital and omnichannel capabilities, communications

• Operating leverage thanks to optimizationof cost base relativeto scale

25February 17, 2021

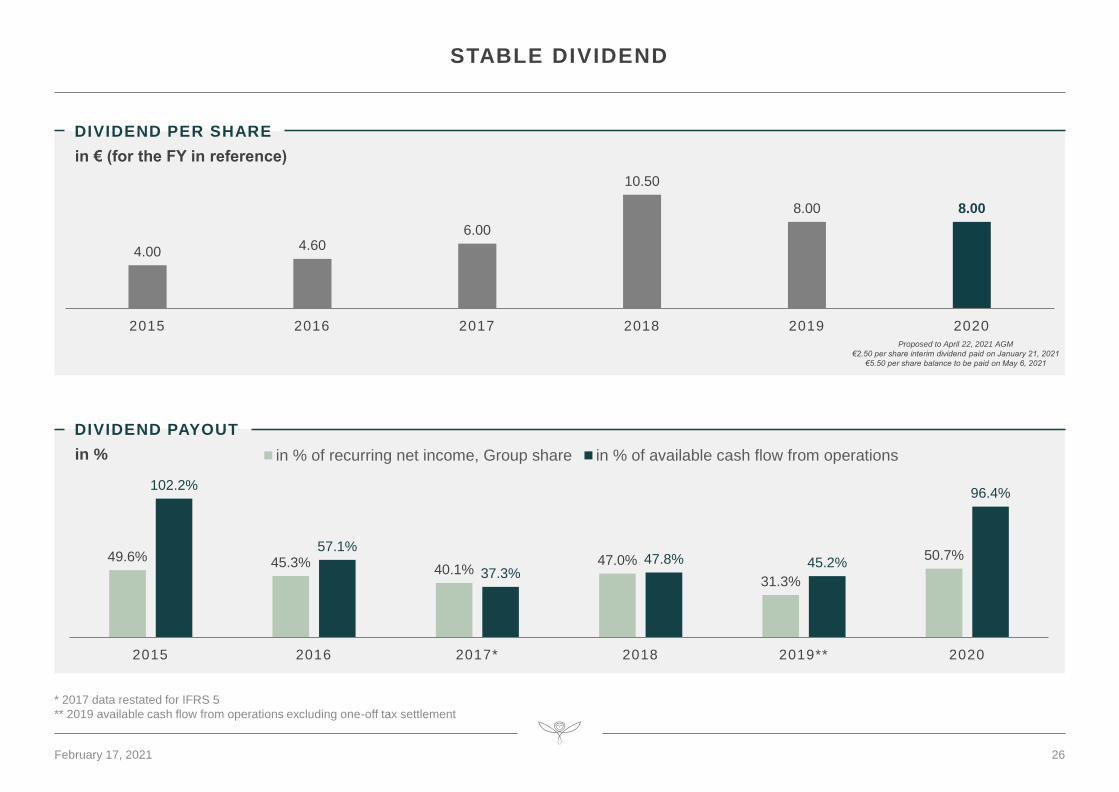

in %

DIVIDEND PAYOUT

in € (for the FY in reference)

DIVIDEND PER SHARE

STABLE DIVIDEND

4.00 4.606.00

10.50

8.00 8.00

2015 2016 2017 2018 2019 2020Proposed to April 22, 2021 AGM

€2.50 per share interim dividend paid on January 21, 2021

€5.50 per share balance to be paid on May 6, 2021

49.6% 45.3%40.1%

47.0%

31.3%

50.7%

102.2%

57.1%

37.3%47.8% 45.2%

96.4%

2015 2016 2017* 2018 2019** 2020

in % of recurring net income, Group share in % of available cash flow from operations

* 2017 data restated for IFRS 5

** 2019 available cash flow from operations excluding one-off tax settlement

26February 17, 2021

27

CONCLUSION

NURTURING

OUR CULTURE

OF INNOVATION,

CREATIVITY

AND CARING

FOCUS ON THE

EXECUTION OF

OUR STRATEGY

CONTINUING

TO INVEST

IN OUR

HOUSES AND

PLATFORMS

FURTHER

POTENTIAL &

OPPORTUNITIES

BACK ON

PROFITABLE

GROWTH

TRAJECTORY

HEALTHY

FINANCIAL

SITUATION

STRENGTHENED POSITIONS TO LEVERAGE THE REBOUND

February 17, 2021

Q&A

APPENDIX

30

REVENUE

Reported change

in €m FY 2020 FY 2019 €m %

Gucci

Saint Laurent

Bottega Veneta

Other Houses

7,440.6

1,744.4

1,210.3

2,281.3

9,628.4

2,049.1

1,167.6

2,537.5

(2,187.8)

(304.7)

+42.7

(256.2)

-22.7%

-14.9%

+3.7%

-10.1%

Luxury – Total Houses 12,676.6 15,382.6 (2,706.0) -17.6%

Corporate & Other 423.6 500.9 (77.3) -15.4%

Kering 13,100.2 15,883.5 (2,783.3) -17.5%

February 17, 2021

Japan

7%

NUMBER OF DIRECTLY OPERATED STORES

y-o-y change

in €m % comparable % reported

Q1 20

Q2 20

Q3 20

Q4 20

3,066

2,110

3,600

3,901

-16.9%

-43.4%

-1.6%

-4.8%

-16.0%

-43.2%

-4.7%

-8.0%

31

LUXURY HOUSES

Revenue breakdown by region

Western Europe

27%

North America

21%

Asia Pacific

39%

RoW

6%

FY 2020 REVENUE€12,677m -17.6% REPORTED, -16.5% COMPARABLE

313229 228

663

324226 220

611

W es te rn Eu rope Nor th Amer i ca Japan Emerg ing marke ts

YE 2020: 1,433 YE 2019: 1,381

February 17, 2021

NUMBER OF DIRECTLY OPERATED STORES

Western Europe

22%

North America

22%

Japan

7%

Asia Pacific

44%

RoW

5%

FY 2020 REVENUE€7,441m -22.7% REPORTED, -21.5% COMPARABLE

105 9967

212

106 107

65

209

W es te rn Eu rope Nor th Amer i ca Japan Emerg ing marke ts

YE 2020: 483 YE 2019: 487

Revenue breakdown by region

y-o-y change

in €m % comparable % reported

Q1 20

Q2 20

Q3 20

Q4 20

1,804

1,268

2,088

2,281

-23.2%

-44.7%

-8.9%

-10.3%

-22.4%

-44.7%

-12.1%

-13.5%

32February 17, 2021

NUMBER OF DIRECTLY OPERATED STORES

Western Europe

32%

North America

25%

Japan

7%

Asia Pacific

30%

RoW

6%

FY 2020 REVENUE€1,744m -14.9% REPORTED, -13.8% COMPARABLE

47 4732

113

46 4331

102

W es te rn Eu rope Nor th Amer i ca Japan Emerg ing marke ts

YE 2020: 239 YE 2019: 222

Revenue breakdown by region

y-o-y change

in €m % comparable % reported

Q1 20

Q2 20

Q3 20

Q4 20

435

247

510

552

-13.8%

-48.4%

+3.9%

+0.5%

-12.6%

-48.2%

+0.8%

-3.0%

33February 17, 2021

NUMBER OF DIRECTLY OPERATED STORES

Western Europe

27%

North America

13%

Japan

11%

Asia Pacific

40%

RoW

9%

FY 2020 REVENUE€1,210m +3.7% REPORTED, +4.8% COMPARABLE

5435

50

122

60

3548

125

W es te rn Eu rope Nor th Amer i ca Japan Emerg ing marke ts

YE 2020: 261 YE 2019: 268

Revenue breakdown by region

y-o-y change

in €m % comparable % reported

Q1 20

Q2 20

Q3 20

Q4 20

274

229

332

375

+8.5%

-24.4%

+20.7%

+15.7%

+10.3%

-23.8%

+17.0%

+12.1%

34February 17, 2021

107

4879

216

112

4176

175

W es te rn Eu rope Nor th Amer i ca Japan Emerg ing marke ts

YE 2020: 450 YE 2019: 404

NUMBER OF DIRECTLY OPERATED STORES

Western Europe

41%

Japan

8%

Asia Pacific

28%

RoW

7%

35

OTHER HOUSES

FY 2020 REVENUE€2,282m -10.1% REPORTED, -9.4% COMPARABLE

Revenue breakdown by region

North America

16%

y-o-y change

in €m % comparable % reported

Q1 20

Q2 20

Q3 20

Q4 20

553

366

669

694

-5.4%

-44.0%

+11.7%

+1.7%

-4.1%

-43.6%

+9.3%

-1.0%

February 17, 2021

36

RECURRING OPERATING INCOME

in €m FY 2020 FY 2019 Reported change %

Gucci

Saint Laurent

Bottega Veneta

Other Houses

2,614.5

400.0

172.0

180.6

3,946.9

562.2

215.2

317.7

-33.8%

-28.9%

-20.1%

-43.2%

Luxury – Total Houses 3,367.1 5,042.0 -33.2%

Corporate & Other (231.9) (263.7) -12.1%

Kering 3,135.2 4,778.3 -34.4%

February 17, 2021

37

EBITDA

in €m FY 2020 FY 2019 Reported change %

Gucci

Saint Laurent

Bottega Veneta

Other Houses

3,224.9

589.9

333.6

457.2

4,463.6

733.7

374.3

550.0

-27.8%

-19.6%

-10.9%

-16.9%

Luxury – Total Houses 4,605.6 6,121.6 -24.8%

Corporate & Other (31.4) (98.0) -68.0%

Kering 4,574.2 6,023.6 -24.1%

EBITDA: defined as recurring operating income + net charges to depreciation, amortisation and provisions on non-current operating assets, recognised in recurring operating income

February 17, 2021

in €m FY 2020 FY 2019

Cost of net debt

Other financial income and expenses

(43.3)

(185.5)

(52.3)

(147.6)

Total Financial result (excluding leases) (228.8) (199.9)

Interest expense on lease liabilities (112.9) (109.6)

Financial result (341.7) (309.5)

38

FINANCIAL RESULT AND INCOME TAX

in €m FY 2020 FY 2019

Tax on recurring income

Tax on non-recurring items

Italian tax settlement

(784.2)

25.0

n.a.

(1,257.6)

27.9

(904.0)

Total tax charge (759.2) (2,133.7)

Effective tax rate 25.7% 49.6%

Tax rate on recurring income 28.1% 28.1%

February 17, 2021

39

BALANCE SHEET

Dec. 31, 2020 Dec. 31, 2019

Intangible Assets

RoU assets on lease contracts

Tangible Assets

Net other Non-current Assets (Liabilities)

Non-current lease Liabilities

Total net Non-current Assets (Liabilities)

Operating Working Capital

Net other Current Assets (Liabilities)

Current lease Liabilities

Total net Current Assets (Liabilities)

Net Assets held for sale

Provisions

9,438

3,957

2,670

1,170

(3,546)

13,689

3,004

(1,622)

(538)

843

1

(350)

9,787

4,247

2,619

1,231

(3,599)

14,285

3,146

(3,118)

(720)

(692)

5

(347)

Capital employed 14,184 13,251

Equity

Net Debt

12,035

2,149

10,439

2,812

Total Sources 14,184 13,251

In €m

February 17, 2021

Gucci • Saint Laurent • Bottega Veneta • Balenciaga • Alexander McQueen • Brioni

Boucheron • Pomellato • Dodo • Qeelin • Ulysse Nardin • Girard -Perregaux

Kering Eyewear