40

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED 1 DAVID BURIK [email protected] APRIL 6, 2016 2016 HEALTH SYSTEM “CONSUMERISM” CHECKLIST

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED1

DAVID BURIK

APRIL 6, 2016

2016 HEALTH SYSTEM

“CONSUMERISM” CHECKLIST

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED2 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED2

1

2

3

Do trends in “major industries with highest

employment” matter?

Can a typical Health System C Suite trust their

gut when it comes to consumer behavior?

Do you think UBER may have greater impact on

your health system beyond getting patients to the

hospitals?

Let’s triangulate on our topic through the discussion of three questions

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED3 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED3

Q1 DO TRENDS IN MAJOR INDUSTRIES WITH HIGHEST

EMPLOYMENT MATTER?

MAJOR INDUSTRIES WITH HIGHEST EMPLOYMENT, BY STATE - 1990

http://www.bls.gov/opub/ted/2014/ted_20140728.htm

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED4 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED4

MAJOR INDUSTRIES WITH HIGHEST EMPLOYMENT, BY

STATE - 1992

http://www.bls.gov/opub/ted/2014/ted_20140728.htm

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED5 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED5

MAJOR INDUSTRIES WITH HIGHEST EMPLOYMENT, BY

STATE - 2002

http://www.bls.gov/opub/ted/2014/ted_20140728.htm

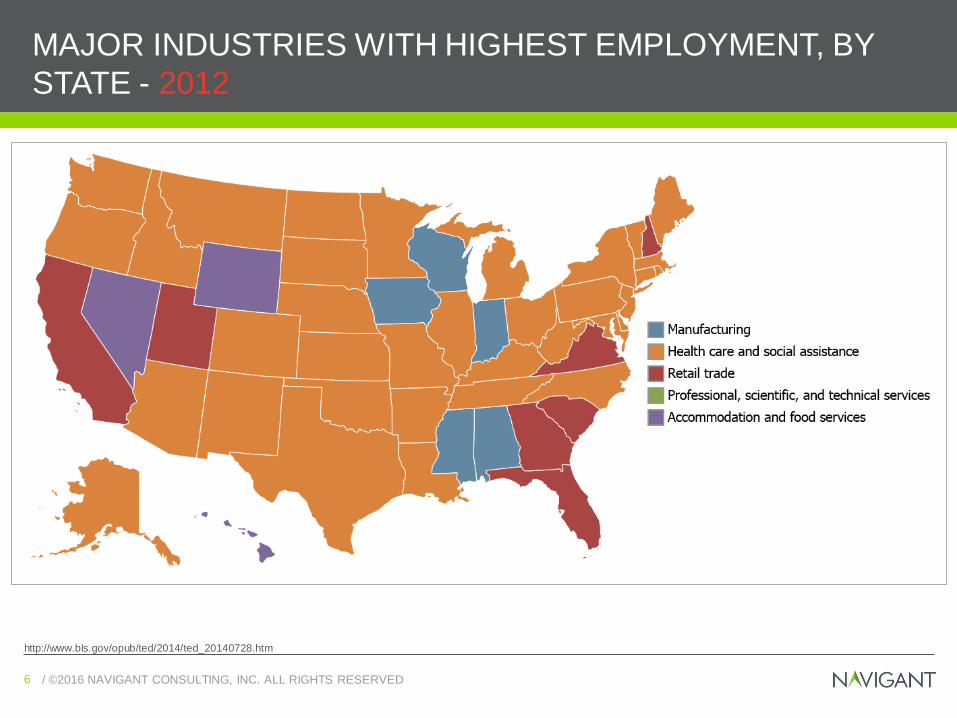

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED6 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED6

MAJOR INDUSTRIES WITH HIGHEST EMPLOYMENT, BY

STATE - 2012

http://www.bls.gov/opub/ted/2014/ted_20140728.htm

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED7 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED7

WHAT ARE THE RAMIFICATIONS OF THIS SITUATION?

Over the long haul, can a service sector be funded at richer levels than the sectors

it serves?

Requires increasing government subsidy or increasing proportion of

household income

Commercial insurance and cross subsidy was built on the back of solid, well paid,

benefit-rich manufacturing jobs. That foundation appears greatly diminished.

How can state and local governments continue to have their largest employers NOT

pay taxes?

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED8 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED8

Q2 CAN A TYPICAL HEALTH SYSTEM C SUITE TRUST THEIR

GUT WHEN IT COMES TO CONSUMER BEHAVIOR?

How many of you drive

Toyota Camry

Toyota Corolla

Honda Accord

Nissan Altima

Honda Civic

Ford Fusion

Hyundai Elantra

http://www.caranddriver.com/flipbook/10-most-cars-here-are-the-bestselling-cars-in-america-for-2015

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED9 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED9

Q3 DO YOU THINK UBER MAY HAVE GREATER IMPACT ON YOUR

HEALTH SYSTEM BEYOND GETTING PATIENTS TO THE HOSPITAL?

Page 9

Interface Companies Are The Fastest Growing, Most Profitable Companies In History

“Own” valuable customer relationships

Low operating costs

Exploit “market inefficiency”

Used with permission from Dave Johnson 4sight Health

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED10 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED10

LIKE MANY DISRUPTIVE INNOVATIONS, INTERFACE

COMPANIES ARE SLOW TO TACKLE US HEALTHCARE

But recognize private equity abounds to fund companies like:

Ignore vs make vs buy-

These firms typically seek to

serve nationally. Can you

compete with a home grown

app serving only your region?

Should you partner? Invest?

http://www.beckershospitalreview.com/hospital-management-administration/25-disruptive-healthcare-companies-to-watch.html

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED11 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED11

US CONSUMERS, IF GIVEN THE OPPORTUNITY…

Will interface companies,

exchanges, Medicaid managed

care, Medicare Advantage put

this information in usable forms

for consumers at the

time of purchase?

1

2

… generally respond to

price and quality data /

perception

… generally respond to

a favorable experience

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED12 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED12

Sources: See Navigant’s Retail Health Issue Brief

RETAIL HEALTH IS A $900 BILLION SECTOR AND GROWING

Cost

Accessibility

Transparency

Lifestyle

Industry Acceptance

+67% Deductible

increase 2010-2015

$4.4bAnnual savings,

shifting 27% ER

visits to clinics

Convenient locations, online

scheduling, walk-in visits

Pricing is transparent and simple

Whole-person wellness is mainstream

http://kff.org/report-section/ehbs-2015-summary-of-findings/

http://content.healthaffairs.org/content/29/9/1630.full

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED13 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED13

ARE THERE CONTRARIANS HERE AMONG US?

• First $ coverage is coming back!

• Folks don’t want to use their handhelds

for something like healthcare!

• People do not shop on price for their

healthcare or health insurance

• That healthy lifestyle stuff is a fad for

the privileged few!

• Payers and employers are starting to

see the benefit of shouldering double

digit health insurance expense

increases

• You just can’t measure good

healthcare!

Samuel Brannon“The real money’s in

the shovels, not the gold”

San Francisco, 1849

Copernicus“It’s the Sun I tell you"

King Camp Gillette“Sell the razors cheap

and the blades dear”

Henry Ford“The airplane takes

off against the wind,

and not with it”

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED14 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED14

SO LET’S DRIVE DEEPER INTO THE NEW HEALTH CARE

“CONSUMERISM” FROM A PRAGMATIC PERSPECTIVE

Section

1Section

2Section

3

Managed care is embracing Medicare and

Medicaid and is intending greater consolidation

than providers

Medical consumers have skin in the game, but

there are conflicting signals of the impact of that

Primary care is the focus of great innovation

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED15 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED15

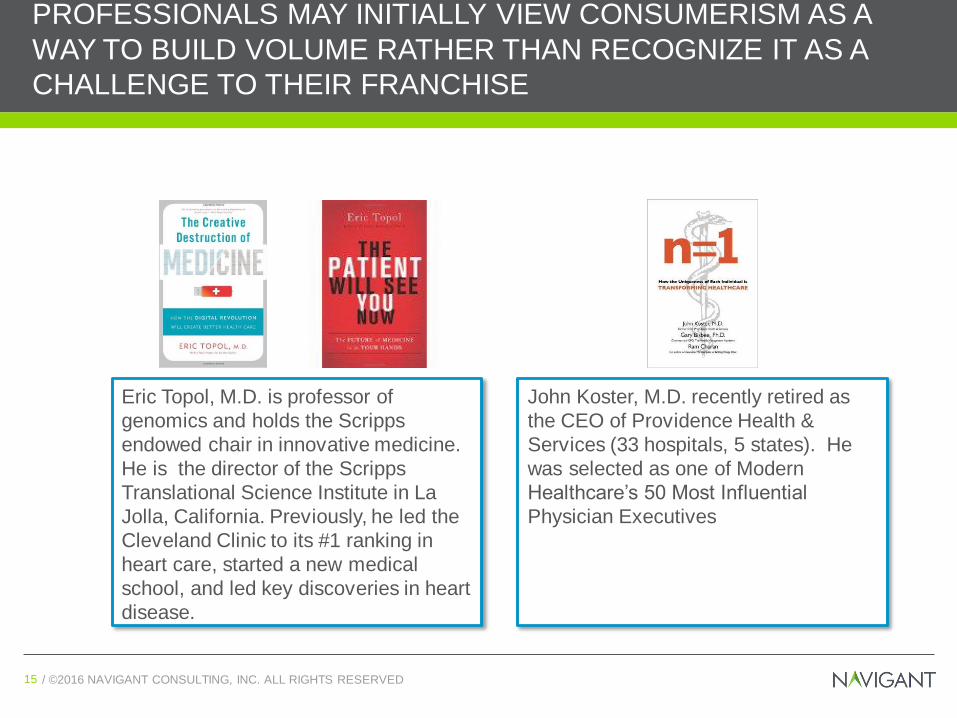

PROFESSIONALS MAY INITIALLY VIEW CONSUMERISM AS A

WAY TO BUILD VOLUME RATHER THAN RECOGNIZE IT AS A

CHALLENGE TO THEIR FRANCHISE

Eric Topol, M.D. is professor of

genomics and holds the Scripps

endowed chair in innovative medicine.

He is the director of the Scripps

Translational Science Institute in La

Jolla, California. Previously, he led the

Cleveland Clinic to its #1 ranking in

heart care, started a new medical

school, and led key discoveries in heart

disease.

John Koster, M.D. recently retired as

the CEO of Providence Health &

Services (33 hospitals, 5 states). He

was selected as one of Modern

Healthcare’s 50 Most Influential

Physician Executives

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED16 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED16

Sources: See Navigant’s Retail Health Issue Brief

9 IMPACT ZONES OF RETAIL HEALTH

• Preference

Driven Tests &

Procedures

• Fitness & Health

Coaching

• Probiotics &

Nutrition

• Complementary

Health

• Medication &

Vitamins

• Core:

Information &

Social Networks

• Retail Primary

Care

• Individual

Insurance

• Payment

Services

• Personalized

Diagnostics

Today’s Focus

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED17 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED17

MANAGED CARE IS TAKING OVER GOVERNMENT-FUNDED

HEALTHCARE

Medicaid Managed Care Today: A Most Unlikely “Market Maker”

Data as of September 2015

http://kff.org/other/state-indicator/medicaid-enrollment-by-mco/#

State Medicaid MCOTotal Medicaid

MCO Enrollment

Arizona 11 Plans 1,461,410

California 22 Plans 9,866,313

Florida 18 Plans 3,071,647

Hawaii 5 Plans 338,477

Illinois 12 Plans 1,592,118

Indiana 3 Plans 1,006,759

Kentucky 5 Plans 1,153,063

Louisiana 5 Plans 975,289

Massachusetts 6 Plans 841,361

Michigan 12 Plans 1,610,382

Minnesota 9 Plans 758,054

Mississippi 2 Plans 498,108

Missouri 3 Plans 444,526

New Mexico 4 Plans 649,606

New York 24 Plans 4,665,309

Ohio 5 Plans 2,337,645

Oregon 16 Plans 948,388

Pennsylvania 9 Plans 2,076,361

South Carolina 7 Plans 697,378

Tennessee 4 Plans 1,460,130

Texas 19 Plans 3,499,476

Washington 6 Plans 1,379,840

West Virginia 4 Plans 364,481

Wisconsin 20 Plans 755,261

24 States

&

42.5 million

Enrollees

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED18 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED18

MEDICARE IS SERIOUS ABOUT THE VALUE TRANSITION

January 26, 2015 HHS announced explicit goals for alternative payment models

and value-based payments

In March 2016, it reached the 30% APM goal - - nearly 1 year ahead of schedule

http://www.hhs.gov/about/news/2016/03/03/hhs-reaches-goal-tying-30-percent-medicare-payments-quality-ahead-schedule.html

2014($362 B)

2015($380 B)

2016(Est. $386 B)

2018(Est. $401 B)

FFS Actual

(%)

FFS Actual

($)

FFS Actual

(%)

FFS Actual

($)

FFS Goal

(%)

FFS Goal

($)

FFS Goal

(%)

FFS Goal

($)

Using

Alternative

Payment

Models

20% $72 B 30% $117 B 30% $116 B 50% $201 B

FFS

Payments

with Quality

Component

80% $290 B N/A N/A 85% $328 B 90% $361 B

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED19 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED19

NATIONAL PAYER LANDSCAPE COULD CHANGE

DRAMATICALLY

“Anthem Raises Offer for Cigna; Aetna

Bids for Humana”

June 2015 -- ….Anthem Inc. taking its $47.5 billion bid to buy Cigna in a

contentious move that shows the pressure the big health insurers are under to

quickly find merger partners.

Anthem has offered $184 a share in cash and stock for Cigna. Cigna said it rejected

the offer, calling it “inadequate and not in the best interests of Cigna’s shareholders.”

A key point of contention involves who would run the combined firm.

Anthem’s pursuit of Cigna comes as Cigna as well as Aetna size up Humana, which

has privately offered itself for sale. Aetna in the past few days made a takeover

proposal to Humana, which has a market value of $30 billion, said people familiar

with the overture. UnitedHealth Group Inc., meanwhile, recently made a takeover

approach to Aetna.

The five big managed-care companies are jockeying for deals that will enable them to

become more efficient and better respond to changes in the health-care landscape in

the U.S. brought on by the Affordable Care Act and other developments. Analysts say

it is likely regulators will allow only one or two such combinations, so the firms are

racing to be the first ones to find merger partners.

Sources: “Anthem Raises Offer for Cigna; Aetna Bids for Humana” June 21, 2015, WSJ.

Consolidation of National Payer Entities Will Impact Many Markets

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED20 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED20

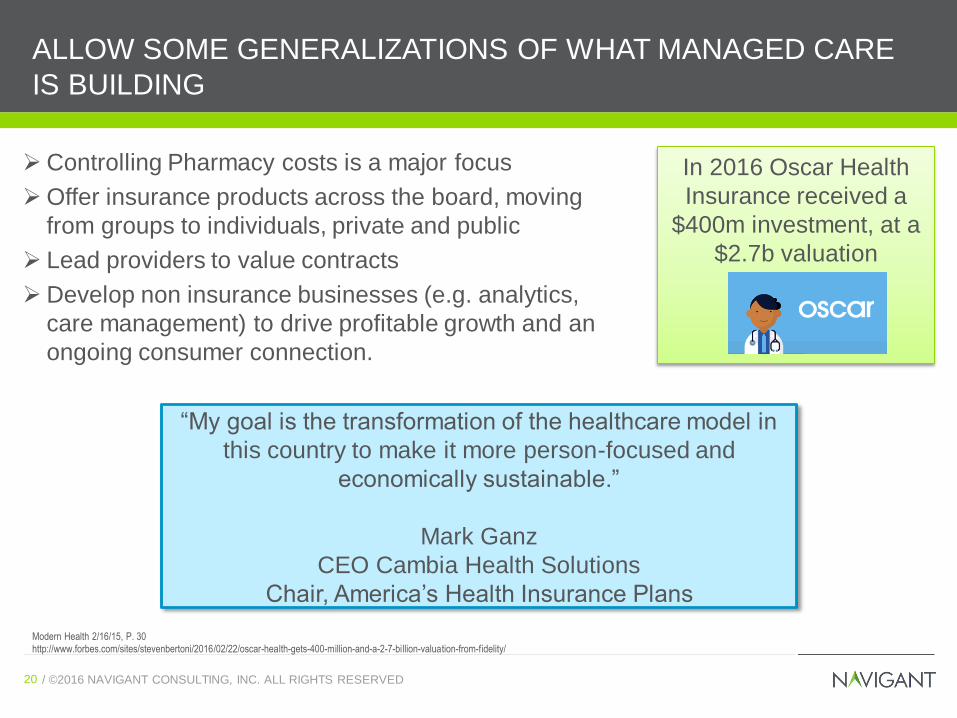

ALLOW SOME GENERALIZATIONS OF WHAT MANAGED CARE

IS BUILDING

Controlling Pharmacy costs is a major focus

Offer insurance products across the board, moving

from groups to individuals, private and public

Lead providers to value contracts

Develop non insurance businesses (e.g. analytics,

care management) to drive profitable growth and an

ongoing consumer connection.

“My goal is the transformation of the healthcare model in

this country to make it more person-focused and

economically sustainable.”

Mark Ganz

CEO Cambia Health Solutions

Chair, America’s Health Insurance Plans

Modern Health 2/16/15, P. 30

http://www.forbes.com/sites/stevenbertoni/2016/02/22/oscar-health-gets-400-million-and-a-2-7-billion-valuation-from-fidelity/

In 2016 Oscar Health

Insurance received a

$400m investment, at a

$2.7b valuation

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED21 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED21

MEDICAL CONSUMERS HAVE SKIN IN THE GAME, BUT THEY

DON’T KNOW WHAT TO DO

Number on exchanges and split gold/bronze, etc.

Interest in private exchanges is growing, by end of 2015, 3% of large employers will provide

their active employees with health insurance through a private exchange while 35% said

they are considering doing so for 2016 or beyond.

o Meantime, 14% of respondents are partnering with a private exchange for their retirees, an

increase from 10% last year. Another 7% are planning to move retirees to private exchanges next

year.

Marketplace Enrollees by Metal Level

https://www.businessgrouphealth.org/pressroom/pressRelease.cfm?ID=234

https://aspe.hhs.gov/sites/default/files/pdf/187866/Finalenrollment2016.pdf

https://aspe.hhs.gov/sites/default/files/pdf/83656/ib_2015mar_enrollment.pdf

https://aspe.hhs.gov/sites/default/files/pdf/76876/ib_2014Apr_enrollment.pdf

Total

Enrollees

Bronze

Plans

Silver

Plans

Gold

Plans

Platinum

Plans

Catastrophic

Plans

2016 12,681,874 23% 68% 6% 2% 1%

2015 11,688,074 22% 67% 7% 3% 1%

2014 8,019,763 20% 65% 9% 5% 2%

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED22 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED22

Sources: See Navigant’s Retail Health Issue Brief

441

2007 2009 2011 2013 2015

FOR MANY HOSPITALS, RETAIL CLINICS ARE THE TIP OF

CONSUMER ICEBERG

2,150 Retail

Clinics 10.5m retail clinic

visits

2% of primary care

encounters

100 partnerships

between retail clinics

and health systems

linking care settings,

expanding after-hours

care options and

providing patients with

alternatives to

emergency departments

Trends

https://newsroom.accenture.com/news/number-of-us-retail-health-clinics-will-surpass-2800-by-2017-accenture-forecasts.htm and

http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2015/rwjf419415

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED23 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED23

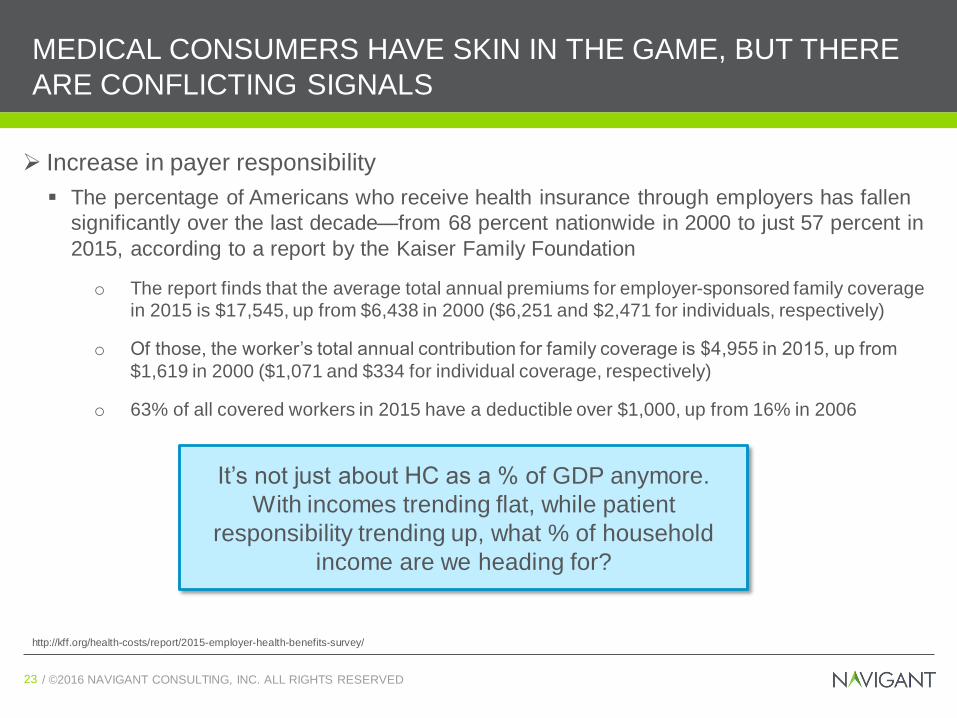

MEDICAL CONSUMERS HAVE SKIN IN THE GAME, BUT THERE

ARE CONFLICTING SIGNALS

Increase in payer responsibility

The percentage of Americans who receive health insurance through employers has fallen

significantly over the last decade—from 68 percent nationwide in 2000 to just 57 percent in

2015, according to a report by the Kaiser Family Foundation

o The report finds that the average total annual premiums for employer-sponsored family coverage

in 2015 is $17,545, up from $6,438 in 2000 ($6,251 and $2,471 for individuals, respectively)

o Of those, the worker’s total annual contribution for family coverage is $4,955 in 2015, up from

$1,619 in 2000 ($1,071 and $334 for individual coverage, respectively)

o 63% of all covered workers in 2015 have a deductible over $1,000, up from 16% in 2006

http://kff.org/health-costs/report/2015-employer-health-benefits-survey/

It’s not just about HC as a % of GDP anymore.

With incomes trending flat, while patient

responsibility trending up, what % of household

income are we heading for?

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED24 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED24

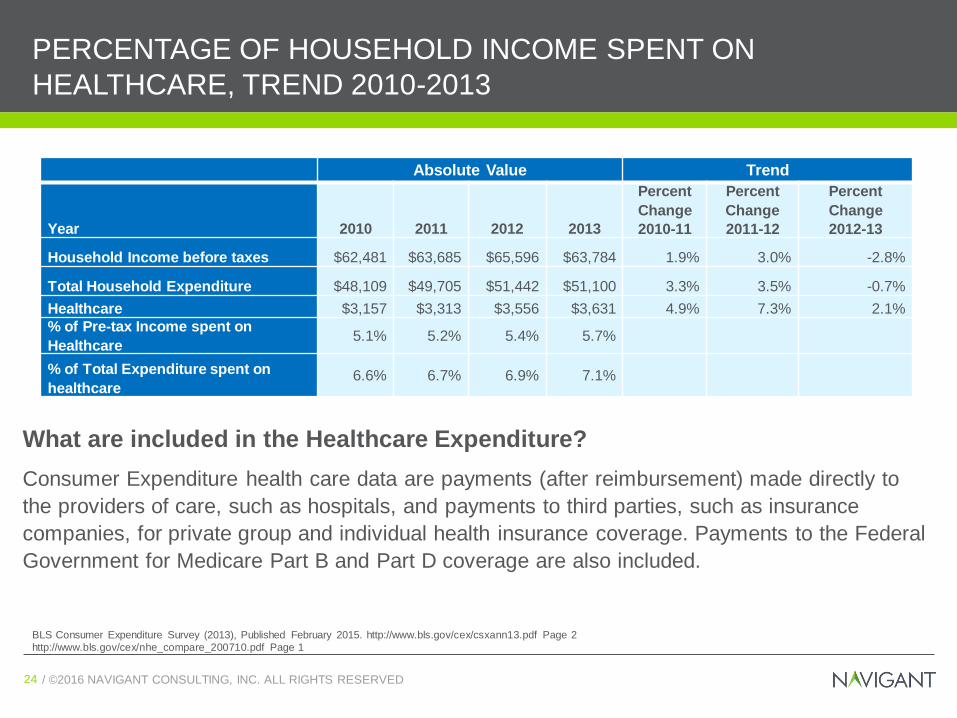

PERCENTAGE OF HOUSEHOLD INCOME SPENT ON

HEALTHCARE, TREND 2010-2013

What are included in the Healthcare Expenditure?

Consumer Expenditure health care data are payments (after reimbursement) made directly to

the providers of care, such as hospitals, and payments to third parties, such as insurance

companies, for private group and individual health insurance coverage. Payments to the Federal

Government for Medicare Part B and Part D coverage are also included.

Absolute Value Trend

Year 2010 2011 2012 2013

Percent

Change

2010-11

Percent

Change

2011-12

Percent

Change

2012-13

Household Income before taxes $62,481 $63,685 $65,596 $63,784 1.9% 3.0% -2.8%

Total Household Expenditure $48,109 $49,705 $51,442 $51,100 3.3% 3.5% -0.7%

Healthcare $3,157 $3,313 $3,556 $3,631 4.9% 7.3% 2.1%

% of Pre-tax Income spent on

Healthcare 5.1% 5.2% 5.4% 5.7%

% of Total Expenditure spent on

healthcare6.6% 6.7% 6.9% 7.1%

BLS Consumer Expenditure Survey (2013), Published February 2015. http://www.bls.gov/cex/csxann13.pdf Page 2

http://www.bls.gov/cex/nhe_compare_200710.pdf Page 1

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED25 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED25

Sources: See Navigant’s Retail Health Issue Brief

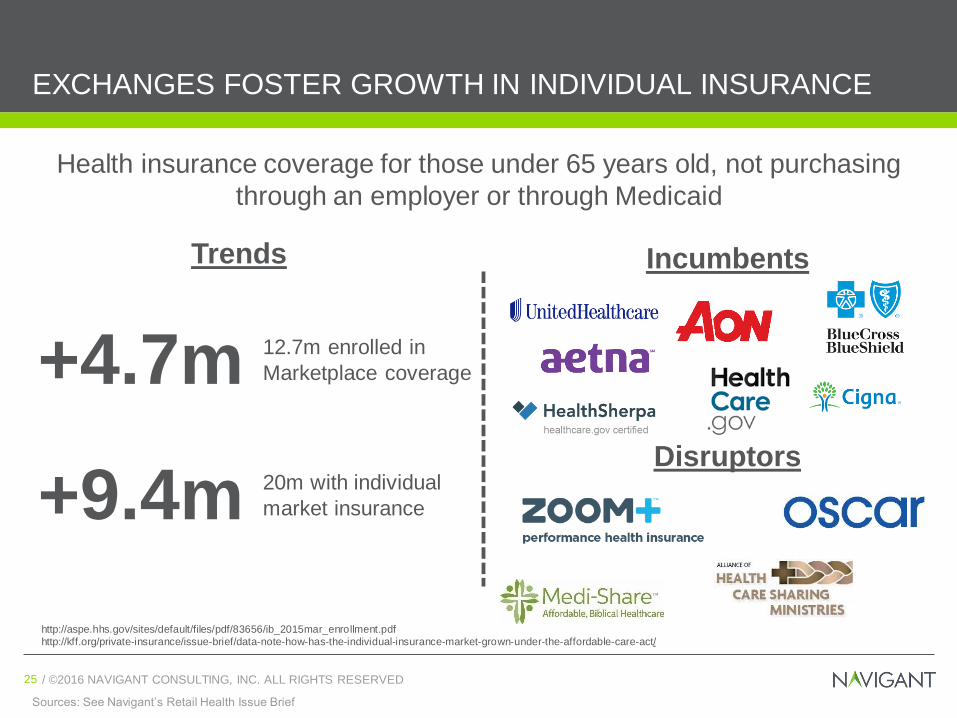

EXCHANGES FOSTER GROWTH IN INDIVIDUAL INSURANCE

Health insurance coverage for those under 65 years old, not purchasing

through an employer or through Medicaid

Trends

+4.7m 12.7m enrolled in

Marketplace coverage

+9.4m 20m with individual

market insurance

Incumbents

Disruptors

http://aspe.hhs.gov/sites/default/files/pdf/83656/ib_2015mar_enrollment.pdf

http://kff.org/private-insurance/issue-brief/data-note-how-has-the-individual-insurance-market-grown-under-the-affordable-care-act/

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED26 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED26

Sources: See Navigant’s Retail Health Issue Brief

HIGH DEDUCTIBLES FOSTER GROWTH IN PAYMENT SERVICES

The institutional structures through which patients finance their care

Trends

+6m 43m Americans with

medical debt

+5m27m Americans

contacted by a

collections agency

+22%51% uninsured have

trouble paying medical

bills vs 29% insured

Incumbents

Disruptors

http://www.consumerfinance.gov/newsroom/cfpb-takes-action-against-medical-debt-collector/

http://www.commonwealthfund.org/~/media/files/publications/issue-brief/2015/jan/1800_collins_biennial_survey_brief.pdf?la=en

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED27 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED27

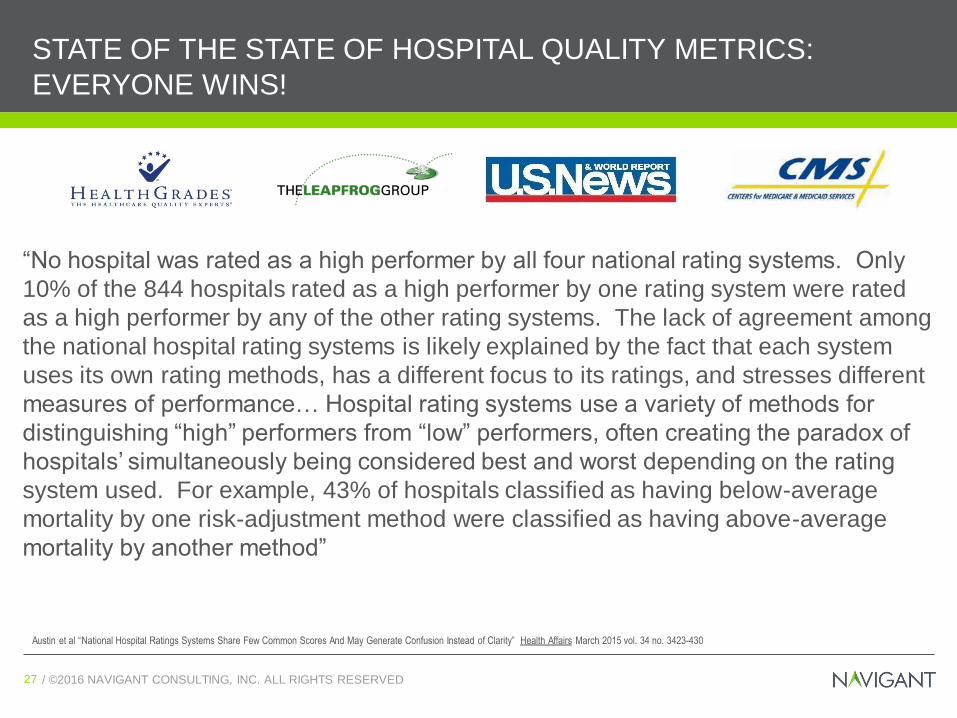

STATE OF THE STATE OF HOSPITAL QUALITY METRICS:

EVERYONE WINS!

“No hospital was rated as a high performer by all four national rating systems. Only

10% of the 844 hospitals rated as a high performer by one rating system were rated

as a high performer by any of the other rating systems. The lack of agreement among

the national hospital rating systems is likely explained by the fact that each system

uses its own rating methods, has a different focus to its ratings, and stresses different

measures of performance… Hospital rating systems use a variety of methods for

distinguishing “high” performers from “low” performers, often creating the paradox of

hospitals’ simultaneously being considered best and worst depending on the rating

system used. For example, 43% of hospitals classified as having below-average

mortality by one risk-adjustment method were classified as having above-average

mortality by another method”

Austin et al “National Hospital Ratings Systems Share Few Common Scores And May Generate Confusion Instead of Clarity” Health Affairs March 2015 vol. 34 no. 3423-430

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED28 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED28

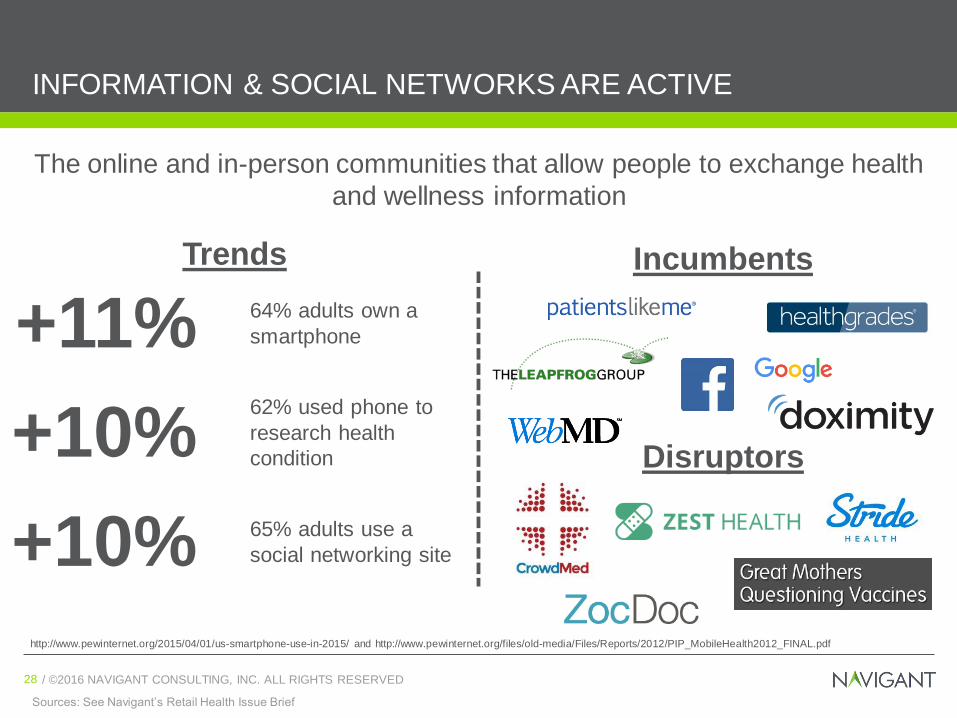

Sources: See Navigant’s Retail Health Issue Brief

INFORMATION & SOCIAL NETWORKS ARE ACTIVE

The online and in-person communities that allow people to exchange health

and wellness information

Trends

+11% 64% adults own a

smartphone

+10%62% used phone to

research health

condition

+10% 65% adults use a

social networking site

Incumbents

Disruptors

http://www.pewinternet.org/2015/04/01/us-smartphone-use-in-2015/ and http://www.pewinternet.org/files/old-media/Files/Reports/2012/PIP_MobileHealth2012_FINAL.pdf

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED29 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED29

PRIMARY CARE INNOVATION:

MEDICAL HOME IS BECOMING ESTABLISHED FOR PATIENTS

NEEDING MUCH CARE

“The PCMH is a model of primary care in which a team of clinicians offers

accessible first-contact care that is personalized, coordinated and comprehensive

and meets most or all of a person's health care needs, including behavioral health”

Rapid adoption of an innovation

http://www.ncqa.org/Portals/0/Events/BehindtheEnhancements_FINAL.pdf

http://www.ncqa.org/Portals/0/Programs/Recognition/PCMH/PCMH-2014_Brochure-web-1.pdf

2013

44 States

20.76 million patients

34,492 clinicians

6,762 sites

2009

18 States

4.95 million patients

1,976 clinicians

383 sites

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED30 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED30

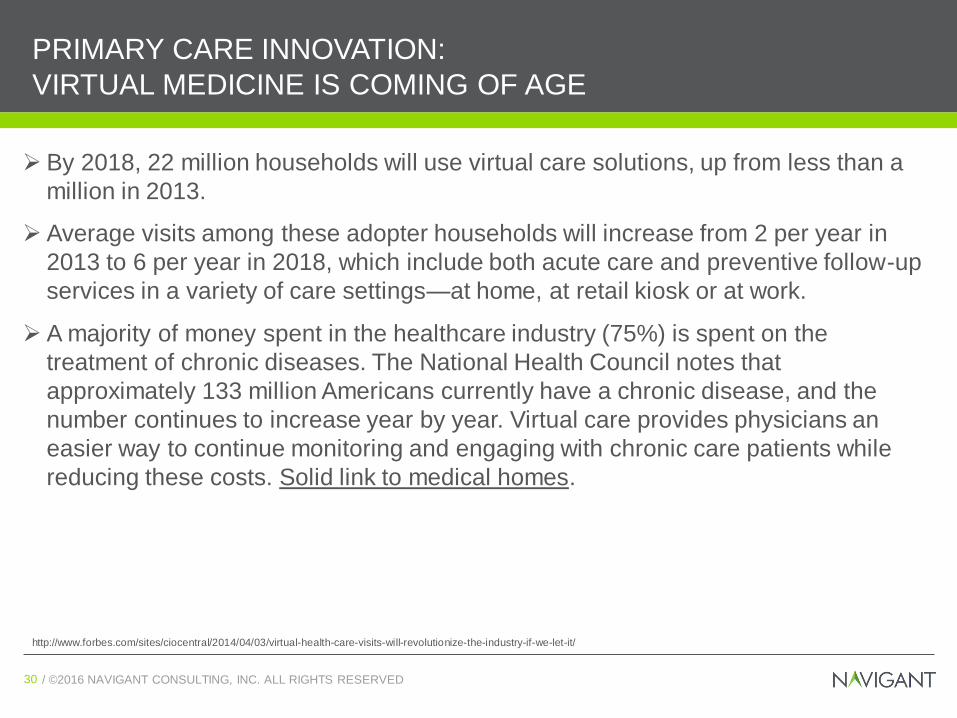

PRIMARY CARE INNOVATION:

VIRTUAL MEDICINE IS COMING OF AGE

By 2018, 22 million households will use virtual care solutions, up from less than a

million in 2013.

Average visits among these adopter households will increase from 2 per year in

2013 to 6 per year in 2018, which include both acute care and preventive follow-up

services in a variety of care settings—at home, at retail kiosk or at work.

A majority of money spent in the healthcare industry (75%) is spent on the

treatment of chronic diseases. The National Health Council notes that

approximately 133 million Americans currently have a chronic disease, and the

number continues to increase year by year. Virtual care provides physicians an

easier way to continue monitoring and engaging with chronic care patients while

reducing these costs. Solid link to medical homes.

http://www.forbes.com/sites/ciocentral/2014/04/03/virtual-health-care-visits-will-revolutionize-the-industry-if-we-let-it/

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED31 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED31

Sources: See Navigant’s Retail Health Issue Brief

PERSONALIZED DIAGNOSTICS GROWING

Wearable devices, monitors, sensors, and patient-directed medical testing

are a solid link to medical homes

Trends

+46m 72m wearables shipped

worldwide

+$18b$60b targeted

therapeutics and

companion diagnostic

market (est.)

Incumbents

Disruptors

https://newsroom.accenture.com/news/number-of-us-retail-health-clinics-will-surpass-2800-by-2017-accenture-forecasts.htm and

http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2015/rwjf419415

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED32 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED32

IHA, one of Michigan’s most recognized multi-specialty physician groups, answers this

question by partnering with Zipnosis:

IHA, will soon launch a profoundly simple online diagnosis and treatment service for people

with straightforward health problems in the Michigan area. This service will connect patients

to IHA clinicians online to receive prompt, high-quality virtual care for common medical

conditions, such as sinus infections, female bladder infections, pink eye, colds and flu—all

for a flat fee payable online.

PRIMARY CARE INNOVATION:

WILL “TRADITIONAL” PROVIDERS (AND PAYERS) “OUT

ACCESS” RETAIL?

How can you give your patients convenient access to mainstream medicine?

• Founded in 2008

• “virtual care solution to empower health care systems with the technology and methodology

to launch their own virtual care service line”

• 90-Day Implementation Guaranteed

Your clinicians, your patients, your brand.

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED33 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED33

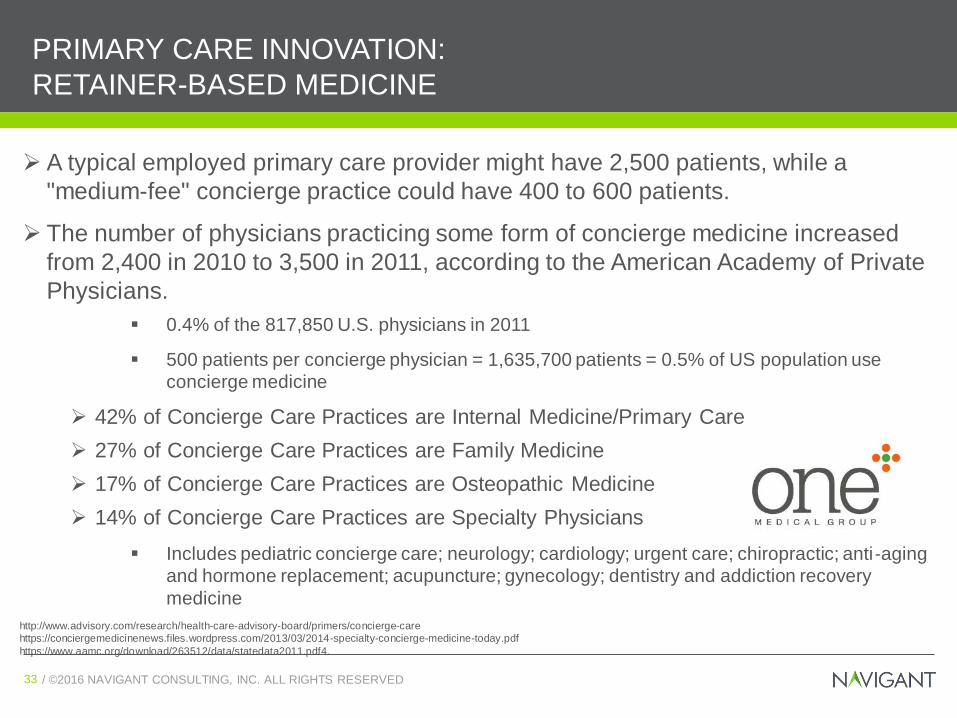

PRIMARY CARE INNOVATION:

RETAINER-BASED MEDICINE

A typical employed primary care provider might have 2,500 patients, while a

"medium-fee" concierge practice could have 400 to 600 patients.

The number of physicians practicing some form of concierge medicine increased

from 2,400 in 2010 to 3,500 in 2011, according to the American Academy of Private

Physicians.

0.4% of the 817,850 U.S. physicians in 2011

500 patients per concierge physician = 1,635,700 patients = 0.5% of US population use

concierge medicine

42% of Concierge Care Practices are Internal Medicine/Primary Care

27% of Concierge Care Practices are Family Medicine

17% of Concierge Care Practices are Osteopathic Medicine

14% of Concierge Care Practices are Specialty Physicians

Includes pediatric concierge care; neurology; cardiology; urgent care; chiropractic; anti-aging

and hormone replacement; acupuncture; gynecology; dentistry and addiction recovery

medicine

http://www.advisory.com/research/health-care-advisory-board/primers/concierge-care

https://conciergemedicinenews.files.wordpress.com/2013/03/2014-specialty-concierge-medicine-today.pdf

https://www.aamc.org/download/263512/data/statedata2011.pdf4.

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED34 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED34

A. Most of us started our careers in a world where integrated physicians were the EXCEPTION.

o Clinic club member

o Faculty practice plans

Independent physicians were the key for most health systems.

Successful management teams were effective in working with successful independent

physicians.

B. Then in the majority of markets albeit due to unique

market factors, physicians increasingly sought

an employment option; and health systems increasingly

became the chosen option. In a fee-for-service (Curve 1)

world, successful management teams were those that were

effective in getting physicians to sell their practices to their system.

C. Then the Curve 2, Value agenda emerged. This “shift upon shift”,

integrate with physicians while going from Curve 1 to Curve 2

is the Journey. Several clients have suggested that doing

both while doing an EHR install/refinement represents a third doll.

Completing these in a patient focused way becomes a fourth doll.

PRIMARY CARE INNOVATION:

PHYSICIANS AND HEALTH SYSTEMS ARE IN A COMPLEX

CHANGE ARENA

The architecture of physician organization is in a generational transition

Patient

FocusedCurve 2EHR Employment

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED35 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED35

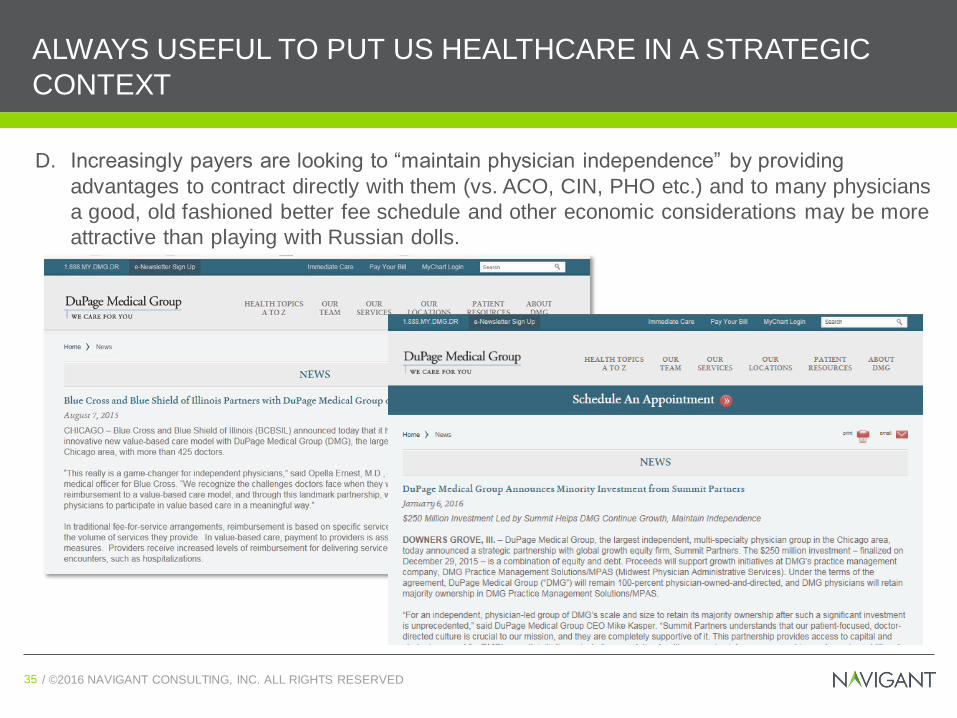

ALWAYS USEFUL TO PUT US HEALTHCARE IN A STRATEGIC

CONTEXT

D. Increasingly payers are looking to “maintain physician independence” by providing

advantages to contract directly with them (vs. ACO, CIN, PHO etc.) and to many physicians

a good, old fashioned better fee schedule and other economic considerations may be more

attractive than playing with Russian dolls.

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED36 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED36

CONSUMERISM IS NOT

Adding a patient hospitality layer to an ineffective & costly delivery system

Implementing an additional loss leader distribution systems to feed inpatient care

IT IS all about making care more accessible (ease of use, affordability) in a

sustainable business model with an ongoing consumer connection. Bear in mind that

at any given time, many of these consumers consider themselves healthy, even if they

regularly take meds requiring a prescription and physician visit.

Competition is at a new level: Who will succeed?

Ongoing

Consumer

Connection

Web/Cloud based

Retail-basedPayor based

Your Health System

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED37 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED37

QUESTIONS A DISCUSSION OF CONSUMERISM SHOULD

TRIGGER FOR A HEALTH SYSTEM

1. DO YOU HAVE A MARKET-LEADING PRIMARY CARE MODEL

1b. Are your PCPs generally an adequate “ongoing consumer connection”

1c. What is your system’s virtual care /

mHealth / retail approach?PCP

PCD

?

190M visits/month (more than physician visits)

Economist 10/17/15 p.74

1a. How many people in your community have a PCP?

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED38 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED38

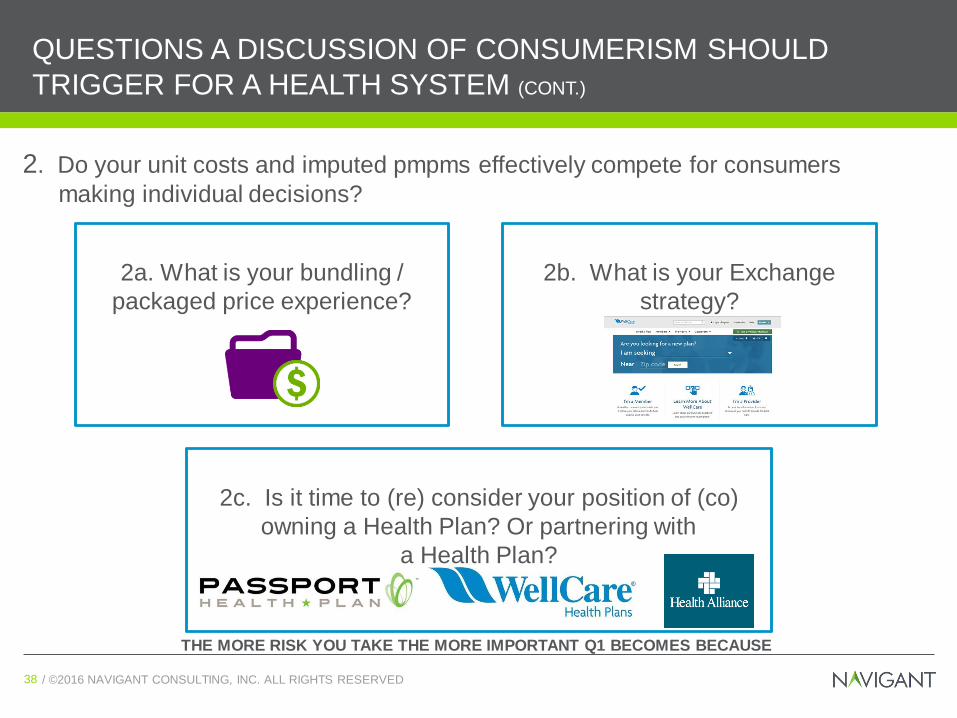

QUESTIONS A DISCUSSION OF CONSUMERISM SHOULD

TRIGGER FOR A HEALTH SYSTEM (CONT.)

2. Do your unit costs and imputed pmpms effectively compete for consumers

making individual decisions?

2a. What is your bundling /

packaged price experience?

2b. What is your Exchange

strategy?

2c. Is it time to (re) consider your position of (co)

owning a Health Plan? Or partnering with

a Health Plan?

THE MORE RISK YOU TAKE THE MORE IMPORTANT Q1 BECOMES BECAUSE

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED39 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED39

QUESTIONS A DISCUSSION OF CONSUMERISM SHOULD

TRIGGER FOR A HEALTH SYSTEM (CONT.)

3. What consumer segmentation work beyond “Payer Mix” is your health

system experienced with ? e.g.

CHRONICALLY

ILL

FOCUSED

FACTORYACTIVE &

HEALTHY

/ ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED40 / ©2016 NAVIGANT CONSULTING, INC. ALL RIGHTS RESERVED40

SUMMARY:

2016 HEALTH SYSTEM “CONSUMERISM” CHECKLIST

Market-leading Primary Care Model

Ongoing consumer connection

Bundling with service line plan behind it

Exchange strategy

Position on Health Plan ownership/partnership

Defined consumer segments being managed and reported against

Active Medical Home for the appropriate patients