128

2017 Annual Report Sydbank Group

2017 Annual ReportSydbank Group

2 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 3

A highly satisfactory result ensures a record-high dividend per share and a new share buyback programme of DKK 500m. Total distribution represents 83% of profit for the year after tax.

Sydbank’s 2017 financial statements show a profit before tax

of DKK 1,956m compared with DKK 1,869m in 2016. The

improvement is due to a reversal of impairment charges and

very satisfactory investment portfolio earnings. Profit before

tax equals a return of 16.8% p.a. on average shareholders’

equity. The profit exceeds the expectations presented in the

2016 financial statements.

Profit for the year represents DKK 1,531m against DKK

1,472m in 2016, equal to a return on average shareholders’

equity of 13.1% after tax.

CEO Karen Frøsig comments on the year’s result: - As a result of the negative interest rate environment combi-ned with fierce competition in the sector, the Group’s net inte-rest income continues to be under pressure. I am therefore very happy that we have succeeded in holding total core income at the same level as in 2016, which is in no small part thanks to the efforts of Sydbank’s many competent employees.

Chairman of Sydbank’s Board of Directors Torben Nielsen ela-borates:- We have generated a return of 13.1% on shareholders’ equity in a highly competitive market and ensured a record-high divi-dend per share as well as the launch of a new share buyback programme of DKK 500m. After a total distribution of DKK 1,266m, the Bank will continue to be highly capitalised.

2017 highlights• A 1% decrease in total income

• A 2% rise in costs (core earnings)

• A reversal of DKK 51m in impairment charges

• A rise in core earnings of DKK 56m to DKK 1,814m

• Investment portfolio earnings of DKK 182m

• Bank loans and advances of DKK 64.3bn

• Deposits of DKK 82.7bn

• A capital ratio of 20.8%, including a Common Equity Tier 1

capital ratio of 17.3%

• A proposed dividend of DKK 11.31 per share.

Outlook for 2018Limited growth is projected for the Danish economy in 2018.

Total income is expected to be on a par with the income

generated in 2017.

Costs (core earnings) are projected to rise slightly in 2018.

Impairment charges for 2018 are forecast to be at a low level.

The uncertainty surrounding price developments in the

agricultural sector may however affect impairment charges.

Non-recurring costs are expected to represent around DKK

75m.

In 2017 very satisfactory investment portfolio earnings and the reversal of impairment charges had a positive effect on profit for the year. However we cannot be sure that this will be the case also in 2018.As a result profit after tax of DKK 1,200-1,400m is projected for 2018.

The outlook is subject to uncertainty and depends among other

things on macroeconomic factors.

4 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 5

Contents

The 2017 Annual Report is available in Danish at sydbank.dk/regnskab and in English at sydbank.com.In case of doubt the Danish version will apply.

Financial Review

Highlights .......................................................................................................................................................................................................................................................6

Group Financial Highlights .....................................................................................................................................................................................................................8

Summary .......................................................................................................................................................................................................................................................9

Performance in 2017 ............................................................................................................................................................................................................................12

Capital Management .............................................................................................................................................................................................................................22

Investor Relations ....................................................................................................................................................................................................................................24

Mission Statement and Business Goals .........................................................................................................................................................................................25

Organisation and Corporate Governance ......................................................................................................................................................................................30

Corporate Social Responsibility .........................................................................................................................................................................................................36

Financial Statements

Financial Statements - contents .......................................................................................................................................................................................................41

Income Statement ...................................................................................................................................................................................................................................42

Statement of Comprehensive Income ............................................................................................................................................................................................42

Balance Sheet ...........................................................................................................................................................................................................................................43

Statement of Changes in Equity .......................................................................................................................................................................................................44

Cash Flow Statement ............................................................................................................................................................................................................................46

Notes ............................................................................................................................................................................................................................................................47

Statements and Reports

Management Statement ...................................................................................................................................................................................................................110

Auditors’ Reports ..................................................................................................................................................................................................................................112

Management, Organisation etc

Notice Convening the Annual General Meeting ......................................................................................................................................................................116

Board of Directors ...............................................................................................................................................................................................................................118

Group Executive Management.......................................................................................................................................................................................................124

Organisation ...........................................................................................................................................................................................................................................126

6 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

A highly satisfactory result ensures a record-high dividend per share and a new share buyback programme

Record-high dividend per share (DKK 11.31 per share)

We build on relationships

Market shares

50% 33%

Dividend

Meetings with adviser Online meetings with adviser

Corporate (SME) Retail

Share buyback766 DKKm

114,000 15,000

13% 6%

500 DKKm

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 7 Å r s r a p p o r t 2 0 1 6 / S Y D B A N K

Profit for the year

1,531DKKm

(+4%)

Return on shareholders’ equity

13.1%

Core income

4,167DKKm(-1%)

Impairment charges forloans and advances

(51)DKKm

Customer satisfaction

4th 5th

Corporate Retail(among the 6 largest banks)

Costs (core earnings)

2,637DKKm(+2%)

Bank loans and advances

64.3DKKbn

Dividend of DKK 11.31per share

50% of profit for the year

8 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Group Financial Highlights

2017 2016Index 17/16 2015 2014 2013

Income statement (DKKm)Core income 4,167 4,198 99 4,329 4,319 4,058

Trading income 233 237 98 215 196 229

Total income 4,400 4,435 99 4,544 4,515 4,287Costs, core earnings 2,637 2,590 102 2,675 2,619 2,514

Core earnings before impairment 1,763 1,845 96 1,869 1,896 1,773Impairment of loans and advances etc (51) 87 - 316 707 1,861

Core earnings 1,814 1,758 103 1,553 1,189 (88)Investment portfolio earnings 182 104 175 (80) 76 319

Profit before non-recurring items 1,996 1,862 107 1,473 1,265 231Non-recurring items, net (40) 7 - - 64 (60)

Profit before tax 1,956 1,869 105 1,473 1,329 171Tax 425 397 107 325 277 (16)

Profit for the year 1,531 1,472 104 1,148 1,052 187

Balance sheet highlights (DKKbn)Loans and advances at amortised cost 64.3 77.2 83 74.3 68.5 66.6

Loans and advances at fair value 5.2 6.1 85 10.2 6.9 4.9

Deposits and other debt 82.7 81.1 102 79.9 73.9 70.0

Bonds issued at amortised cost 3.7 3.7 100 3.7 3.7 6.5

Subordinated capital 1.9 2.1 90 2.1 1.4 1.8

Shareholders’ equity 11.9 11.8 101 11.4 11.3 10.2

Total assets 138.5 146.7 94 142.7 152.3 147.9

Financial ratios per share (DKK per share of DKK 10) EPS Basic 22.4 20.9 15.8 14.3 2.5EPS Diluted 22.4 20.9 15.8 14.3 2.5Share price at year-end 249.9 219.2 221.8 190.2 144.0Book value 178.3 169.2 160.2 154.2 139.7Share price/book value 1.40 1.30 1.38 1.23 1.03Average number of shares outstanding (in millions) 68.4 70.4 72.5 73.3 73.4Proposed dividend 11.31 10.46 11.12 7.08 -

Other financial ratios and key figuresCommon Equity Tier 1 capital ratio 17.3 16.1 14.5 13.9 13.4Tier 1 capital ratio 17.7 17.4 15.9 15.5 15.3Capital ratio 20.8 19.2 17.6 16.0 15.7Pre-tax profit as % of average shareholders’ equity 16.8 16.6 13.3 12.4 1.6

Post-tax profit as % of average shareholders’ equity 13.1 13.1 10.2 9.6 1.8Costs (core earnings) as % of total income 59.9 58.4 58.9 58.0 58.6Return on assets (%) 1.07 1.02 0.78 0.70 0.12Interest rate risk 0.8 1.6 2.8 0.0 0.6Foreign exchange position 1.2 2.2 2.2 1.8 2.1Foreign exchange risk 0.0 0.0 0.0 0.0 0.0Loans and advances relative to deposits 0.6 0.8 0.8 0.8 0.8Loans and advances relative to shareholders’ equity 5.4 6.6 6.5 6.1 6.5Growth in loans and advances for the year (16.7) 3.9 8.5 2.8 (2.3)Excess cover relative to statutory liquidity requirements (section 152 of the Danish Financial Business Act) 232.1 186.5 166.8 142.2 179.8Total large exposures 0.0 0.0 0.0 0.0 25.8Accumulated impairment ratio 3.6 3.6 4.7 5.1 5.4Impairment ratio for the year (0.1) 0.1 0.4 0.8 2.3Number of full-time staff at year-end 2,064 2,037 101 2,044 2,101 2,231Financial ratio definitions on page 94.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 9

Summary

A highly satisfactory result ensures a record-high dividend per share and a new share buyback programme of DKK 500m. Total distribution represents 83% of profit for the year after tax.

Sydbank’s 2017 financial statements show a profit before tax

of DKK 1,956m compared with DKK 1,869m in 2016. The

improvement is due to a reversal of impairment charges and

very satisfactory investment portfolio earnings. Profit before

tax equals a return of 16.8% p.a. on average shareholders’

equity. The profit exceeds the expectations presented in the

2016 financial statements.

Profit for the year after tax represents DKK 1,531m against

DKK 1,472m in 2016, equal to a return on average

shareholders’ equity of 13.1%.

The 3-year plan “Blue growth”The plan for the 3-year period 2016-2018 is named “Blue

growth”. The plan must ensure that the positive development in

the Group’s profitability is sustained.

Blue growth – financial targets • Realise a return on shareholders’ equity of a minimum of

12% after tax or be in the top 3 of the 6 largest banks

• Maintain top 3 ranking among the 6 largest banks in terms

of customer satisfaction.

Status – targets

Target Objective Status at 31 December 2017 Comment

Return on shareholders’ equityafter tax

Over 12%* 13.1% Progressing as planned

Customer satisfaction- Corporate

Top 3** 4th - Aalund Not met in 2017

Customer satisfaction- Retail

Top 3** 5th - EPSI Not met in 2017

Common Equity Tier 1 capital ratio Around 14.0% 17.3% Met from Q3 2013

Capital ratio Around 18.0% 20.8% Met from Q1 2015

Dividend30-50% of profit for the year after tax

50% of profit after tax(proposed)

Met in 2017(proposed dividend)

* or top 3 ranking among the 6 largest banks

** among the 6 largest banks

among the 6 largest banks

* or top 3 ranking amongthe 6 largest banks

Return on shareholders’ equity

12%

Top 3Customer satisfaction

after tax*

Targets - Blue growth

10 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Results for 2017As a result of the negative interest rate environment combined

with fierce competition in the sector, the Group’s net interest

income remains under pressure. Net interest income has

decreased by DKK 330m or 14% to DKK 1,993m. DKK 129m

of the decline is attributable to the effects of the amended

funding agreement concerning mortgage-like loans. The

funding agreement was changed from an offsetting model

according to which the Bank covers losses as regards the entire

loan to a guarantee model according to which the Bank

provides a guarantee for the part of the loan in the LTV range

of 60-80%. As a consequence of the amendment of the

agreement, funded mortgage-like loans will not be recognised

in the balance sheet in future and income will be recognised as

mortgage credit income.

Mortgage credit income has increased by DKK 175m or 44%

compared with 2016.

Other core income has risen by DKK 124m or 8% compared

with 2016.

Total core income has decreased by DKK 31m or 1% compared

with 2016.

Trading income has dropped by DKK 4m or 2% compared with

2016.

Total income has declined by DKK 35m or 1% compared with

2016.

Costs (core earnings) have increased by DKK 47m or 2%

compared with 2016. The increase is a consequence of general

pay rises for the financial sector and a payroll tax increase of

0.5 percentage points.

The Group’s impairment charges for loans and advances

constitute an income of DKK 51m in 2017.

Core earnings have increased by DKK 56m to DKK 1,814m

compared with DKK 1,758m in 2016. The improvement is

attributable to the decrease in impairment charges for loans

and advances.

Together the Group’s position-taking and liquidity handling

generated investment portfolio earnings of DKK 182m in 2017

compared with DKK 104m in 2016.

Profit before tax rose to DKK 1,956m in 2017 compared to

DKK 1,869m in 2016. Tax has been calculated at DKK 425m.

Profit for the year amounts to DKK 1,531m compared with

DKK 1,472m in 2016.

Bank loans and advances decreased by DKK 12.9bn in 2017.

DKK 10.0bn of the decline is attributable to funded mortgage-

like loans no longer being recognised in the balance sheet.

Return on shareholders’ equity before and after tax constitutes

16.8% and 13.1% respectively against 16.6% and 13.1% in

2016.

Earnings per share has increased to DKK 22.4 from DKK 20.9

in 2016.

During the year shareholders’ equity grew by DKK 169m to

DKK 11,926m.

Less the proposed dividend, the Common Equity Tier 1 capital

ratio and the capital ratio stand at 17.3% and 20.8%

respectively at year-end 2017 compared to 16.1% and 19.2%

at year-end 2016.

At 31 December 2017 the individual solvency need

represented 11.0% (2016: 10.2%).

Total credit intermediationIn addition to traditional bank loans and advances the Group

arranges for mortgage loans from Totalkredit and DLR Kredit.

The Group’s total credit intermediation comprises bank loans

and advances, mortgage-like loans funded by Totalkredit as well

as mortgage loans arranged through Totalkredit and DLR Kredit

respectively. At 31 December 2017 credit intermediation totalled

DKK 144.0bn – a drop of DKK 3.9bn compared with year-end

2016.

Total credit intermediation

Group – year-end (DKKbn) 2017 2016

Bank loans and advances 64.3 77.2

Funded mortgage-like loans 10.0 -

Arranged mortgage loans – Totalkredit 58.0 58.3

Arranged mortgage loans – DLR 11.7 12.4

Total 144.0 147.9

SIFISydbank has been designated as a SIFI (systemically important

financial institution) in Denmark. As a result the Bank is subject

to an additional buffer requirement of 0.6% as regards

Common Equity Tier 1 capital in 2017. The requirement will

gradually rise to 1.0% in 2019.

Summary

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 11

Capital targetsThe Group’s capital targets have been raised to a Common

Equity Tier 1 capital ratio of around 14.0% and a capital ratio

of around 18.0%. Before the change the capital targets were a

Common Equity Tier 1 capital ratio of around 13.5% and a

capital ratio of around 17.0%.

Proposed dividend for 2017The Board of Directors proposes – in compliance with the Bank’s

dividend policy – that a dividend of DKK 11.31 per share, equal to

50% of the Group’s profit after tax, be distributed and that DKK

10m be donated to the sponsorship fund Sydbank Fonden.

No dividend will be distributed as regards the shares acquired in

connection with the share buyback programme completed in

2017.

Share buyback in 2018Following distribution of the proposed dividend, the capital

ratios will remain above the capital targets. As a result the

Board of Directors has resolved to implement a share buyback

totalling DKK 500m in 2018.

The Group will continue to be highly capitalised after the

proposed dividend distribution and the share buyback.

Outlook for 2018Limited growth is projected for the Danish economy in 2018.

Total income is expected to be on a par with the income

generated in 2017.

Costs (core earnings) are projected to rise slightly in 2018.

Impairment charges for 2018 are forecast to be at a low level.

The uncertainty surrounding price developments in the

agricultural sector may however affect impairment charges.

Non-recurring costs are expected to represent around DKK

75m.

In 2017 very satisfactory investment portfolio earnings and the reversal of impairment charges had a positive effect on pro-fit for the year. However we cannot be sure that this will be the case also in 2018.As a result profit after tax of DKK 1,200-1,400m is projected for 2018.

The outlook is subject to uncertainty and depends among

other things on macroeconomic factors.

12 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Performance in 2017

The Sydbank Group has recorded a profit before tax of DKK

1,956m (2016: DKK 1,869m). The performance exceeds the

expectations at the beginning of the year. Profit before tax

equals a return of 16.8% p.a. on average shareholders’ equity.

Profit for the year represents DKK 1,531m against DKK

1,472m in 2016, equal to a return on average shareholders’

equity of 13.1% after tax.

The financial statements are characterised by the following:

2017• A 1% decrease in total income

• A 2% increase in costs (core earnings)

• A reversal of DKK 51m in impairment charges

• A rise in core earnings of DKK 56m to DKK 1,814m

• Investment portfolio earnings of DKK 182m

• Bank loans and advances of DKK 64.3bn (2016: DKK 77.2bn)

• Deposits of DKK 82.7bn (2016: DKK 81.1bn)

• A capital ratio of 20.8%, including a Common Equity Tier 1

capital ratio of 17.3%

• A proposed dividend of DKK 11.31 per share.

Q4• Impairment charges for loans and advances constitute an

income of DKK 13m

• Profit for the period amounts to DKK 327m.

Income statement

Group (DKKm) 2017 2016

Core income 4,167 4,198

Trading income 233 237

Total income 4,400 4,435

Costs, core earnings 2,637 2,590

Core earnings before impairment 1,763 1,845

Impairment of loans and advances etc (51) 87

Core earnings 1,814 1,758

Investment portfolio earnings 182 104

Profit before non-recurring items 1,996 1,862

Non-recurring items, net (40) 7

Profit before tax 1,956 1,869

Tax 425 397

Profit for the year 1,531 1,472

Core incomeTotal core income has declined by DKK 31m to DKK 4,167m.

As a result of the negative interest rate environment combined

with fierce competition in the sector, the Group’s net interest

income remains under pressure. Net interest income has

decreased by DKK 330m or 14% to DKK 1,993m. DKK 129m

of the decline is attributable to the effects of the amended

funding agreement concerning mortgage-like loans. The fund-

ing agreement was changed from an offsetting model accord-

ing to which the Bank covers losses as regards the entire loan

to a guarantee model according to which the Bank provides a

guarantee for the part of the loan in the LTV range of 60-80%.

As a consequence of the amendment of the agreement, funded

mortgage-like loans will not be recognised in the balance sheet

in future and income will be recognised as mortgage credit

income.

Net income from the cooperation with Totalkredit represents

DKK 420m (2016: DKK 291m) after a set-off of loss of DKK

27m (2016: DKK 23m). The cooperation with DLR Kredit has

generated an income of DKK 152m (2016: DKK 107m).

Compared to 2016 mortgage credit income has gone up by a

total of DKK 175m to DKK 575m – an increase of 44%. DKK

113m of the DKK 175m increase is attributable to funded

mortgage-like loans.

Income from remortgaging and loan fees has risen by DKK 63m

to DKK 133m compared to 2016 – a rise of 90%.

Commission and brokerage income has gone up by DKK 11m

to DKK 365m – an increase of 3% compared to 2016.

Income from asset management has climbed by DKK 44m to

DKK 264m – a rise of 20% compared with 2016. DKK 14m of

the income is attributable to performance-related fees.

The remaining income components have risen by DKK 6m

compared to 2016, equal to 1%.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 13

Core income

Group (DKKm) 2017 2016

Net interest etc 1,993 2,323

Mortgage credit 575 400

Payment services 202 199

Remortgaging and loan fees 133 70

Commission and brokerage 365 354

Commission etc investment funds and pooled pension plans 388 381

Asset management 264 220

Custory account fees 69 71

Other operating income 178 180

Total 4,167 4,198

Trading incomeCompared with 2016 trading income has decreased by DKK

4m to DKK 233m and is composed as follows in terms of busi-

ness units:

Trading income

Group (DKKm) 2017 2016Fixed Income 143 135

Equities 58 65

Money Market and Foreign Exchange 32 37

Total 233 237

Fixed Income has generated an income of DKK 143m, an

increase of DKK 8m compared with 2016. A high level of activi-

ty was recorded in Fixed Income in 2017.

Equities has recorded an income of DKK 58m, a fall of DKK 7m

compared to 2016.

Money Market and Foreign Exchange has generated an income

of DKK 32m, a decrease of DKK 5m compared with 2016.

Costs and depreciationThe Group’s costs and depreciation totalled DKK 2,684m, equal

to an increase of DKK 63m compared with 2016.

Costs (core earnings) represent DKK 2,637m compared with

DKK 2,590m in 2016. The increase is a consequence of general

pay rises for the financial sector and a payroll tax increase of 0.5

percentage points.

At year-end 2017 the Group’s staff numbered 2,064 (full-time

equivalent).

Costs and depreciation

Group (DKKm) 2017 2016

Staff costs 1,561 1,519

Other administrative expenses 976 968

Amortisation/depreciation and impairment of intangible assets and property, plant and equipment 122 115

Other operating expenses 25 19

Total 2,684 2,621Distributed as follows:

Costs, core earnings 2,637 2,590

Costs, investment portfolio earnings 7 7

Non-recurring costs 40 24

In connection with the opening of the new regional head office

in Odense, the number of branches was reduced by 2 in 2017,

bringing the number of branches to 62 in Denmark and 3 in

Germany.

Core earnings before impairment of loans and advancesCore earnings before impairment charges for loans and advanc-

es represent DKK 1,763m – a decrease of DKK 82m compared

with 2016.

Impairment of loans and advances etcImpairment charges for loans and advances represent an

income of DKK 51m compared with an expense of DKK 87m in

2016, equal to a fall of DKK 138m.

Impairment charges for the year by industry

Group (DKKm) 2017 2016

Agriculture etc 4 231

Trade 65 14

Real property (53) (40)

Other corporate lending 133 37

Total corporate 149 242

Retail (95) (38)

Total individual impairment charges 54 204

Collective impairment charges (105) (117)

Total impairment charges (51) 87

In 2017 collective impairment charges fell by DKK 105m

(2016: DKK 117m). Collective impairment charges constitute

DKK 75m at 31 December 2017. They were positively affected

by the reduction in collective impairment charges for agricultural

exposures of DKK 75m in 2017 (2016: reduction of DKK 75m).

14 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

In 2017 the agricultural sector saw a considerable improvement

in earnings compared to the period from 2014 to 2016.

However the sector continues to be characterised by an overall

large debt burden.

Lower earnings are expected in the agricultural sector for 2018

as a consequence of expectations of lower settlement prices.

Reference is made to the separate publication Credit Risk 2017

for further elaboration.

At year-end 2017 the impairment ratio for the year represents

minus 0.08% relative to bank loans and advances and minus

0.06% relative to bank loans and advances and guarantees. At

year-end 2017 accumulated impairment and provisions

amount to DKK 2,887m (2016: DKK 3,289m).

Individually impaired bank loans and advances

DKKm

6,000

4,000

2,000

0

%

8.0

6.0

4.0

2.0

0.0

Impaired bank loans and advancesIndividual impairment charges for bank loans and advancesImpaired bank loans and advances, netImpaired bank loans and advances as % of bank loans and advances

Q1

16

Q2

16

Q3

16

Q4

16

Q1

17

Q2

17

Q3

17

Q4

17

During the year impaired bank loans and advances before

impairment charges declined by DKK 471m to DKK 4,391m

(2016: DKK 4,862m). During the same period individually

impaired bank loans and advances after impairment charges

decreased by DKK 126m, equal to 6%. Impairment charges for

bank loans and advances subject to individual impairment rep-

resent 54.2% (2016: 56.1%).

Individually impaired bank loans and advances

Group (DKKm) 2017 2016Non-defaulted bank loans and advances 3,468 3,637

Defaulted bank loans and advances 923 1,225

Impaired bank loans and advances 4,391 4,862

Impairment charges for bank loans and advances subject to individual impairment 2,381 2,726

Impaired bank loans and advances after impairment charges 2,010 2,136

Impaired bank loans and advances as % of bank loans and advances before impairment charges 6.6 6.1

Impairment charges as % of bank loans and advances before impairment charges 3.6 3.4

Impaired as % of impaired bank loans and advances 54.2 56.1

Impairment charges as % of defaulted bank loans and advances 258.0 222.5

The figure below shows the breakdown of impaired bank loans

and advances in terms of defaulted bank loans and advances

and non-defaulted bank loans and advances. The bulk of

impaired bank loans and advances concern non-defaulted bank

loans and advances.

Breakdown of impaired bank loans and advances

DKKm

6,000

4,000

2,000

0

Defaulted bank loans and advances Non-defaulted bank loans and advances

4,515

1,708 1,665 1,603 1,225 1,246 1,144 1,030 923

4,546 4,346 3,637 3,369 3,412 3,364 3,468

Q1

16

Q1

17

Q2

16

Q2

17

Q3

16

Q3

17

Q4

16

Q4

17

Defaulted bank loans and advances declined by DKK 302m in

2017 and non-defaulted bank loans and advances decreased

by DKK 169m. The considerable drop in impaired bank loans

and advances of DKK 1,087m in Q4 2016 is attributable to a

decrease in impaired loans and advances as regards agricultural

exposures of DKK 879m. The decline regarding agricultural

exposures is primarily a consequence of the conversion of the

debt concerning 48 agricultural exposures to subordinated loan

capital in Q4 2106. The subordinated loan capital has been

written off for accounting purposes.

Performance in 2017

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 15

Core earnings Core earnings for 2017 represent DKK 1,814m – an increase of

DKK 56m compared with 2016.

Investment portfolio earningsTogether the Group’s position-taking and liquidity handling

generated earnings of DKK 182m in 2017 compared with DKK

104m in 2016.

Investment portfolio earnings

Group (DKKm) 2017 2016Position-taking 118 100

Liquidity generation and liquidity reserves 52 9

Strategic positions 19 2

Costs (7) (7)

Total 182 104

The satisfactory result for 2017 is a consequence of the excess

yield on Danish mortgage bonds relative to the risk-free inter-

est rate, a narrowing of the credit spreads on mortgage bonds

as well as gains on interest rate fluctuations – notably in the

early months of the year.

At year-end 2017 the interest rate risk is composed so that the

Group will profit from an interest rate increase.

Margin expenses as regards the Group’s senior issues are

included under liquidity generation and liquidity reserves and

represent DKK 21m in 2017 compared to DKK 35m in 2016.

Non-recurring items, netNon-recurring items etc total an expense of DKK 40m compared

with a net income of DKK 7m in 2016. The item consists of pro-

cess digitization costs related to Blue growth as well as the estab-

lishment of a new mortgage platform. In 2016 this item included

one-off income of DKK 31m concerning the adjustment of the

purchase sum from the sale of the shares in Nets Holding in 2014

as well as process optimisation costs of DKK 24m.

Profit for the yearProfit before tax amounts to DKK 1,956m (2016: DKK

1,869m). Tax represents DKK 425m (2016: DKK 397m), equiv-

alent to an effective tax rate of 21.7%. Profit for the year

amounts to DKK 1,531m (2016: DKK 1,472m).

Return Return on shareholders’ equity before and after tax constitutes

16.8% and 13.1% respectively against 16.6% and 13.1% in

2016. Earnings per share has increased to DKK 22.4 from DKK

20.9 in 2016.

Sydbank – the parentThe Bank’s total income before costs and impairment charges

for loans and advances represents DKK 4,510m (2016: DKK

4,489m). The income includes the consolidated loss on hold-

ings in associates and subsidiaries of DKK 26m (2016: profit of

DKK 71m).

Total costs including non-recurring costs of DKK 40m (2016:

DKK 24m) constitute DKK 2,608m (2016: DKK 2,552m).

A reversal of impairment charges for bank loans and advances

of DKK 51m (2016: impairment charge of DKK 87m) has been

recorded.

Pre-tax profit amounts to DKK 1,947m (2016: DKK 1,839m).

SubsidiariesProfit after tax of the subsidiaries represents minus DKK 12m

(2016: DKK 76m).

Group – Q4 2017The Group’s profit before tax for the quarter represents DKK

412m. Tax represents DKK 85m and profit for the period

amounts to DKK 327m.

Compared with Q3 2017 profit before tax shows:

• a core income of DKK 1,038m (Q3: DKK 1,036m)

• a trading income of DKK 36m (Q3: DKK 58m)

• costs (core earnings) of DKK 645m (Q3: DKK 623m)

• impairment charges for loans and advances of minus DKK 13m

(Q3: minus DKK 29m)

• investment portfolio earnings of minus DKK 13m (Q3: DKK 8m).

16 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Performance in 2017

Profit for the period

Group (DKKm) Q4 2017 Q3 2017 Q2 2017 Q1 2017 Q4 2016Core income 1,038 1,036 1,040 1,053 1,067

Trading income 36 58 46 93 49

Total income 1,074 1,094 1,086 1,146 1,116

Costs, core earnings 645 623 678 691 632

Core earnings before impairment 429 471 408 455 484

Impairment of loans and advances etc (13) (29) (20) 11 (27)

Core earnings 442 500 428 444 511

Investment portfolio earnings (13) 8 51 136 63

Profit before non-recurring items 429 508 479 580 574

Non-recurring items, net (17) (11) (6) (6) (14)

Profit before tax 412 497 473 574 560

Tax 85 109 104 127 116

Profit for the period 327 388 369 447 444

Total assetsThe Group’s total assets made up DKK 138.5bn at year-end

2017 against DKK 146.7bn at year-end 2016.

Assets

Group – year-end (DKKbn) 2017 2016

Amounts owed by credit institutions etc 14.6 9.0

Loans and advances at fair value (reverse transactions) 5.2 6.1

Loans and advances at amortised cost(bank loans and advances) 64.3 77.2

Securities and holdings etc 28.1 28.3

Assets related to pooled plans 16.5 13.8

Other assets etc 9.8 12.3

Total 138.5 146.7

The Group’s bank loans and advances total DKK 64.3bn.

Compared to 2016 this constitutes a decrease of DKK 12.9bn.

DKK 10.0bn of the decline is attributable to funded mortgage-

like loans no longer being recognised in the balance sheet.

Corporate lending has declined by DKK 0.7bn and retail lending

has decreased by DKK 1.9bn when the effects of the amended

funding agreement are taken into account.

Shareholders’ equity and liabilities

Group – year-end (DKKbn) 2017 2016

Amounts owed to credit institutions etc 6.0 17.6

Deposits and other debt 82.7 81.1

Deposits in pooled plans 16.5 13.8

Bonds issued 3.7 3.7

Other liabilities etc 15.4 16.2

Provisions 0.4 0.4

Subordinated capital 1.9 2.1

Shareholders’ equity 11.9 11.8

Total 138.5 146.7

Amounts owed to credit institutions etc represent DKK 6.0bn, a

decrease of DKK 11.6bn compared to 2016. One reason for

this is that the funding agreement concerning mortgage-like

loans was changed effective 1 January 2017 after which date

the funding of mortgage-like loans is no longer recognised in

the balance sheet. The funding represented DKK 5.3bn at year-

end 2016 and was included in “Amounts owed to credit

institutions etc”.

The Group’s deposits make up DKK 82.7bn. This is an increase

of DKK 1.6bn compared to 2016. Deposits have increased due

to a rise in time deposits of DKK 2.7bn, a rise in demand deposits

of DKK 2.0bn, a decrease in deposits at notice of DKK 2.7bn and

a decrease of DKK 0.4bn regarding special categories of deposits.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 17

The Sydbank share

Number 2017 2016

Average number of shares outstanding 68,364,550 70,392,671

Number of shares outstanding at year-end 66,900,704 69,501,452

Number of shares issued at year-end 70,361,174 72,240,199

Share capitalAs a result of a capital reduction implemented in 2017 the

share capital has declined from DKK 722,401,990 at year-end

2016 to DKK 703,611,740 at year-end 2017.

The number of shares outstanding has decreased from

69,501,452 (96.21%) at the end of 2016 to 66,900,704

(95.08%) at the end of 2017. The book value of the Sydbank

share represents 178.3 (2016: 169.2). At year-end 2017 the

closing price of the Sydbank share stood at 249.9 and the share

price/book value at 1.40.

Shareholders’ equityAt year-end 2017 shareholders’ equity constitutes DKK

11,926m – an increase of DKK 169m since the beginning of

the year. The change comprises an addition from profit for the

year of DKK 1,531m, net purchases of own shares of DKK

642m as well as dividend distribution etc of DKK 720m.

CapitalThe Bank issued Tier 2 capital worth EUR 75m on 2 November

2017. The issue is a 12-year issue with a first call option after 7

years.

The Bank has prepaid Additional Tier 1 capital of EUR 100m

and DKK 85m. The prepayments were made on 25 April 2017

and 15 May 2017 respectively.

The Bank implemented a share buyback programme of DKK

664m in 2017. The share buyback commenced on 2 March

2017 and was completed on 29 December 2017. 2,690,220

shares were repurchased.

The share buyback is part of the capital adjustment to optimise

the capital structure in accordance with the Group’s capital

policy.

In 2018 the Bank will continue to optimise the capital structure,

possibly by issuing subordinated capital and consequently the

possibilities for issuing subordinated capital in the market are

monitored on an ongoing basis.

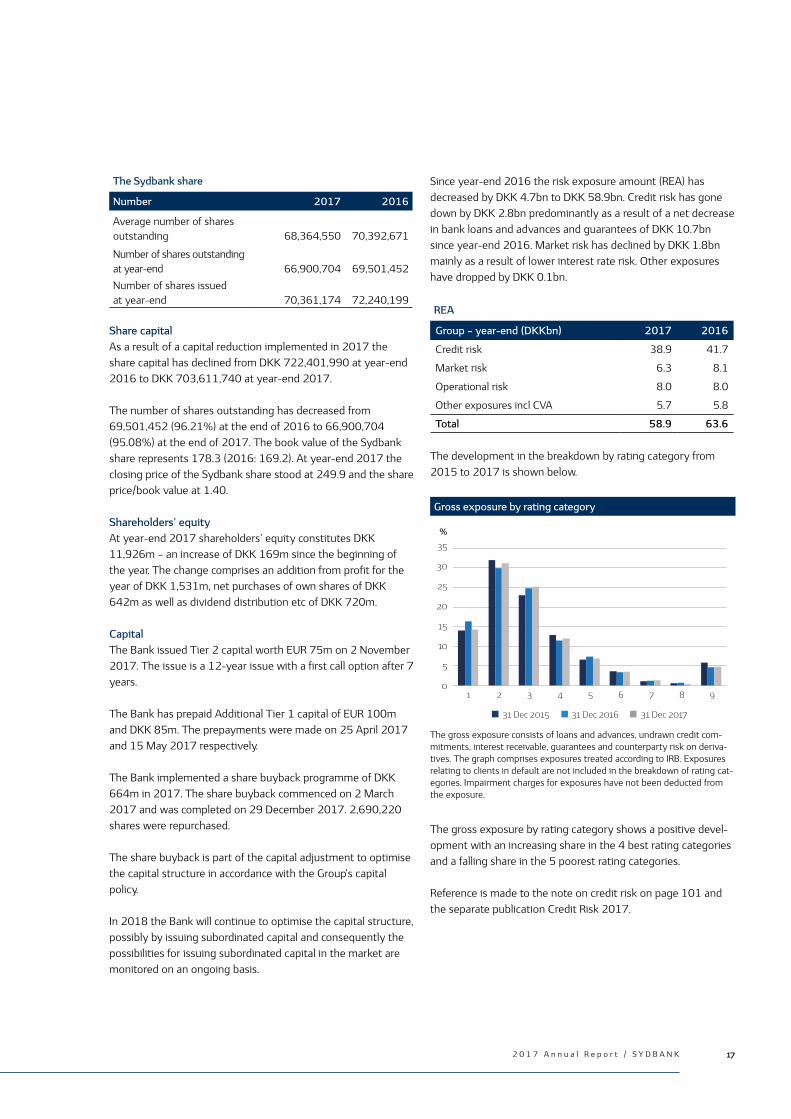

Since year-end 2016 the risk exposure amount (REA) has

decreased by DKK 4.7bn to DKK 58.9bn. Credit risk has gone

down by DKK 2.8bn predominantly as a result of a net decrease

in bank loans and advances and guarantees of DKK 10.7bn

since year-end 2016. Market risk has declined by DKK 1.8bn

mainly as a result of lower interest rate risk. Other exposures

have dropped by DKK 0.1bn.

REA

Group – year-end (DKKbn) 2017 2016

Credit risk 38.9 41.7

Market risk 6.3 8.1

Operational risk 8.0 8.0

Other exposures incl CVA 5.7 5.8

Total 58.9 63.6

The development in the breakdown by rating category from

2015 to 2017 is shown below.

Gross exposure by rating category

%

35

30

25

20

15

10

5

01

31 Dec 2015 31 Dec 2016 31 Dec 2017

2 3 4 5 6 7 8 9

The gross exposure consists of loans and advances, undrawn credit com-mitments, interest receivable, guarantees and counterparty risk on deriva-tives. The graph comprises exposures treated according to IRB. Exposures relating to clients in default are not included in the breakdown of rating cat-egories. Impairment charges for exposures have not been deducted from the exposure.

The gross exposure by rating category shows a positive devel-

opment with an increasing share in the 4 best rating categories

and a falling share in the 5 poorest rating categories.

Reference is made to the note on credit risk on page 101 and

the separate publication Credit Risk 2017.

18 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Performance in 2017

Solvency

Group - year-end (DKKm) 2017 2016

REA 58,889 63,607

Common Equity Tier 1 capital 10,167 10,213

Tier 1 capital 10,446 11,044

Total capital 12,240 12,242

Common Equity Tier 1 capital ratio 17.3 16.1

Tier 1 capital ratio 17.7 17.4

Capital ratio 20.8 19.2

At year-end 2017 the Common Equity Tier 1 capital ratio and

the capital ratio stand at 17.3% and 20.8% respectively com-

pared to 16.1% and 19.2% at year-end 2016.

In 2017 the capital ratio was positively affected by profit for the

year (+2.4 percentage points), the issue of new Tier 2 capital

(+0.9 percentage points) and the reduction in risk exposure

(+1.5 percentage points) and negatively affected by the pro-

posed dividend (-1.2 percentage points), the completed share

buyback programme (-1.0 percentage points), the repayment of

Additional Tier 1 capital (-0.8 percentage points) and other ele-

ments (-0.2 percentage points).

Capital ratio in 2017

Capital ratioat 1 Jan 2017

Share buybackDKK 664m

Repayment of Additional Tier 1 capital

Issue ofTier 2 capital

Profit

19.2

1.0

0.8

0.9

2.4

1.2

1.5

20.8

0.2

Proposed dividend 2017

Decline inrisk exposure

Capital ratioat 31 Dec 2017

Increase Decrease

17.0 18.0 19.0 20.0 21.0

Deductions etc

At 31 December 2017 the individual solvency need

represented 11.0% (2016: 10.2%).

Solvency of the parentAt year-end 2017 the Common Equity Tier 1 capital ratio and

the capital ratio stand at 16.7% and 20.1% respectively.

Advanced IRB – corporate exposuresToday Sydbank applies the advanced IRB approach to calculate

the capital requirement as regards retail exposures and the

foundation IRB approach to calculate the capital requirement as

regards corporate exposures.

Sydbank is working on a project with the aim of gaining approv-

al to apply the advanced IRB approach to calculate the capital

requirement as regards corporate exposures. The objective is to

gain approval in 2019.

Capital policyThe Group’s capital policy consistently supports the Group’s

strategy and at the same time takes into account Sydbank’s sta-

tus as a SIFI as well as full implementation of capital regulations.

The Group’s capital targets have been raised and the current

targets are a Common Equity Tier 1 capital ratio of around

14.0% (previously: 13.5%) and a capital ratio of around 18.0%

(previously: 17.0%). The capital targets have been set to ensure

that the Group complies with all capital requirements, including

buffer requirements, once these have been fully implemented.

Reference is made to Capital Management on page 22.

Dividend policyThe Group’s dividend policy must contribute to creating long-

term shareholder value. The objective is to distribute 30-50%

of profit for the year after tax while taking into account growth

plans and capital policy.

Interest rate risk etcThe Group’s interest rate risk represents minus DKK 86m at 31

December 2017 (2016: DKK 177m). As a result the Group will

profit from an interest rate increase.

The Group’s exchange rate risk continues to be very low and its

equity risk modest as regards its trading portfolio.

Funding and liquidityThe guidelines for calculating the Liquidity Coverage Ratio –

LCR – specify a run-off of exposures, while taking into account

counterparties, funding size, hedging and duration.

Consequently the most stable deposits are favoured relative to

large deposits, in particular large deposits from business enter-

prises and financial counterparties.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 19

As a SIFI in Denmark, Sydbank must fully meet the LCR. The

Group’s LCR constituted 176% at 31 December 2017 (2016:

166%).

The Group has met the LCR requirement of 100% throughout

the year and as can be seen its excess cover is significant at 31

December 2017.

Joint funding The Bank’s agreement on joint funding with Totalkredit was

changed effective 1 January 2017. The agreement was changed

from an offsetting model according to which the Bank covers

losses as regards the entire loan to a guarantee model according

to which the Bank provides a guarantee for the part of the loans

in the LTV range of 60-80%. The Group no longer has a credit

risk as regards the part of the loan in the LTV range of 0-60%.

As a consequence of the amendment of the agreement, funded

mortgage-like loans are no longer recognised in the Group’s bal-

ance sheet.

At 31 December 2017 funded mortgage-like loans amount to

DKK 10.0bn (31 December 2016: DKK 5.3bn). Had the agree-

ment been effective as of 31 December 2016, bank loans and

advances would have been recognised at DKK 5.3bn less at this

date and the Bank would instead have registered guarantees for

DKK 1.2bn as regards the guarantee amount in the range of

60-80%. At the beginning of 2018 funded mortgage-like loans

represent DKK 10.9bn.

Accounting estimatesEstimates in relation to the measurement of assets and liabili-

ties are based on assumptions considered reasonable by man-

agement but which by their nature are uncertain. They may

prove to be incomplete or inaccurate as a result of develop-

ments differing from projections, in the external environment in

which the Group operates or in other respects relating to cus-

tomers or business relations.

RatingMoody’s most recent rating of Sydbank:

Outlook: Positive

Long-term deposit: A3

Baseline credit assessment: Baa1

Senior unsecured: Baa1

Short-term deposit: P-2.

ShareholdersIn 2017 the Sydbank share yielded a return of 14% (2016:

minus 1%) as a result of the increase in the share price during

the year. Moreover dividend distribution represented DKK

10.46 per share. Consequently the total return in 2017 repre-

sented 19% (2016: 4%).

The Board of Directors will propose to the AGM that 50% of the

Group’s profit after tax, equal to a dividend of DKK 11.31 per

share, be distributed and that DKK 10m be donated to the

sponsorship fund Sydbank Fonden.

Supervisory DiamondThe Supervisory Diamond sets up a number of benchmarks to

indicate banking activities that initially should be regarded as

involving a higher risk. Any breach of the Supervisory Diamond

is subject to reactions by the Danish FSA.

The calculations at the end of 2017 are shown below:

Supervisory Diamond benchmarks

Group 2017 2016

Sum of large exposures < 125% 0 0

Lending growth < 20% annually (17) 4

Commercial property exposure < 25% 8 9

Funding ratio < 1 0.69 0.80

Excess cover relative to statutory liquidity requirement > 50%(section 152 of the Danish Financial Business Act) 232 186

At 31 December 2017 the Group as well as the parent comply

with all the benchmarks of the Supervisory Diamond.

Leverage ratioThe CRR/CRD IV rules require credit institutions to calculate,

report, monitor and disclose their leverage ratio, which is defined

as Tier 1 capital as a percentage of total exposures. The

European Commission’s proposal for a revision of CRR includes

a proposal to introduce a minimum leverage ratio requirement

of 3%.

The Group’s leverage ratio stood at 6.9% at 31 December 2017

(2016: 7.0%) taking into account the transitional rules.

Assuming fully loaded Tier 1 capital under CRR/CRD IV without

any refinancing of non-eligible Additional Tier 1 capital, the lever-

age ratio would be 6.7% (2016: 6.5%).

The introduction of a minimum leverage ratio requirement is not

expected to be of significance to the Group.

20 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Performance in 2017

SIFISydbank has been designated as a SIFI in Denmark and in 2017

there is an additional buffer requirement of 0.6% as regards

Common Equity Tier 1 capital. The requirement will gradually

rise to 1% in 2019. The intention is to bring Danish SIFI capital

requirements on a par with the requirements in other compara-

ble European countries.

IFRS 9With IFRS 9, which came into force on 1 January 2018, a new

impairment model has been introduced according to which

impairment charges must be recognised for all loans and

advances and guarantees on the basis of expected losses.

Under the existing rules impairment charges are recognised

only when there is objective evidence of impairment.

Under IFRS 9 exposures are divided into 3 groups for calculat-

ing impairment and classified into different stages (1, 2 or 3),

depending on the risk of credit loss. The staging assessment

and the calculation of expected loss will to a large extent be

based on the Group’s existing rating models and credit manage-

ment.

Based on the Danish FSA’s national guidelines concerning

impairment charges in accordance with IFRS 9 impairment

charges are expected to increase by around DKK 200m at 1

January 2018.

In general the projected increase in the Group’s impairment

charges will reduce the Group’s shareholders’ equity and will

consequently have a corresponding negative impact on regula-

tory capital. To counter an unintended impact on regulatory

capital and hence banks’ possibilities of supporting lending, a

transitional arrangement has been adopted so that any adverse

impact from the new impairment model will be phased in over a

number of years. Sydbank has decided to apply the transitional

rules.

Bank Recovery and Resolution DirectiveThe directive, including the bail-in provisions, was implemented

in Danish law on 1 June 2015. According to legislation each

credit institution must meet a minimum requirement for eligible

liabilities (MREL). The Danish FSA has been authorised to set

the requirement for Sydbank.

Uncertainty continues to surround the deadline for compliance

with the minimum requirement. The final minimum requirement

may affect the Group’s capital and funding structure.

The general resolution principle for SIFIs is that it should be

possible to restructure them and send them back to the market

with adequate capitalisation to ensure market confidence. In

accordance with this principle the MREL for SIFIs is expected to

be set at 2 times the total capital requirement. It is expected

that the MREL will have to be met with convertible instruments

(“contractual bail-in”).

The Danish FSA will have discussions with the industry on

phase-in and the specific requirements regarding capital that

can be used to comply with the MREL. The discussions will take

into consideration international developments in the area.

During 2018 the Danish FSA is expected to set the MREL for

the Group effective as of 1 January 2019.

The establishment of a resolution fund began in 2015. Credit

institutions must make contributions to the fund according to

their relative size and risk in Denmark. The resolution fund must

be established and have assets at its disposal equal to at least

1% of the covered deposits of all Danish credit institutions by

31 December 2024.

The Group’s contribution to the resolution fund for 2017 repre-

sents DKK 18m.

Basel IVOn 7 December 2017 the Basel Committee on Banking

Supervision (BCBS) published its recommendations for a num-

ber of changes to the calculation of the capital requirements for

credit institutions. These recommendations are also known as

Basel IV. Among other things, Basel IV proposes to constrain

the use of internal models and introduce a permanent floor for

the risk exposure amount.

The recommendations are expected to have a limited impact on

the Group’s capital.

The recommendations must be implemented in the EU before

they will apply to Danish institutions. The Group is following

developments closely. At present the extent of the changes in

relation to the Basel Committee’s recommendations when

implemented into EU regulation is unknown. The effective date

is expected to be 1 January 2022 on which date the floor

requirement is also expected to be implemented, starting at

50% and gradually increasing until finally reaching 72.5% at 1

January 2027.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 21

Outlook for 2018Limited growth is projected for the Danish economy in 2018.

Total income is expected to be on a par with the income

generated in 2017.

Costs (core earnings) are projected to rise slightly in 2018.

Impairment charges for 2018 are forecast to be at a low level.

The uncertainty surrounding price developments in the

agricultural sector may however affect impairment charges.

Non-recurring costs are expected to represent around DKK

75m.

In 2017 very satisfactory investment portfolio earnings and the reversal of impairment charges had a positive effect on profit for the year. However we cannot be sure that this will be the case also in 2018.As a result profit after tax of DKK 1,200-1,400m is projected for 2018.

The outlook is subject to uncertainty and depends among

other things on macroeconomic factors.

22 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Capital Management

The Group’s capital management ensures efficient deployment

of capital relative to the Group’s overall capital targets. The

Group’s risk profile is determined on the basis of the capital

targets which ensure first and foremost that there is adequate

capital to meet the Group’s growth expectations and cover

fluctuations in the risks assumed by the Group.

The Group applies internal ratings based approaches to manage

the credit risk of the Group’s corporate and retail client

portfolios. The Group applies the advanced IRB approach as

regards retail clients and the foundation IRB approach as

regards corporate clients to determine the Group’s capital

requirements.

The Group applies the Standardised Approach to credit risk in

relation to exposures to governments and credit institutions.

Further details, also concerning the risk exposure amount

(REA), capital information and capital ratios, are found in note 3.

The Group’s capital management focuses on 4 capital elements:

minimum capital, adequate total capital, capital requirements

including buffers and total capital.

Capital and solvency and capital requirements

% of REA31 Dec

2017Fully

loaded*Capital and solvency

Common Equity Tier 1 capital ratio 17.3 17.3

Capital ratio 20.8 20.8

Capital requirements (incl buffers)**Total capital requirement 12.9 14.5

CET1 capital requirement 8.0 9.7

- of which countercyclical capital buffer 0.0 0.0

- of which capital conservation buffer 1.3 2.5

- of which SIFI buffer 0.6 1.0

Excess capitalCommon Equity Tier 1 capital 9.3 7.6

Total capital 7.9 6.3

* Based on fully loaded CRR/CRD IV rules and requirements.** The total capital requirement consists of an individual solvency need

and a combined buffer requirement. The fully loaded countercyclical capital buffer is based on the national buffer rate as at 31 December 2017.

Minimum capital represents the necessary capital in compliance

with CRR and adequate total capital is the Group’s determination

of the capital sufficient to protect depositors against loss under

the prevailing economic conditions. The solvency need is

defined as adequate total capital in percentage terms of the risk

exposure amount.

The capital requirement including buffers is based on the

solvency need to which a combined buffer requirement is

added. The combined buffer requirement for the Group

constitutes 1.9% at 31 December 2017. When fully loaded the

combined buffer requirement will represent 3.5% bringing the

fully loaded CET1 capital ratio requirement to 9.7%.

In December 2017 the Systemic Risk Council recommended

that a countercyclical buffer rate of 0.5% be set in Denmark

effective 31 March 2019. If a countercyclical capital buffer is

implemented in Denmark the Group’s fully loaded CET1 capital

ratio requirement will go up by approx 0.4 percentage points.

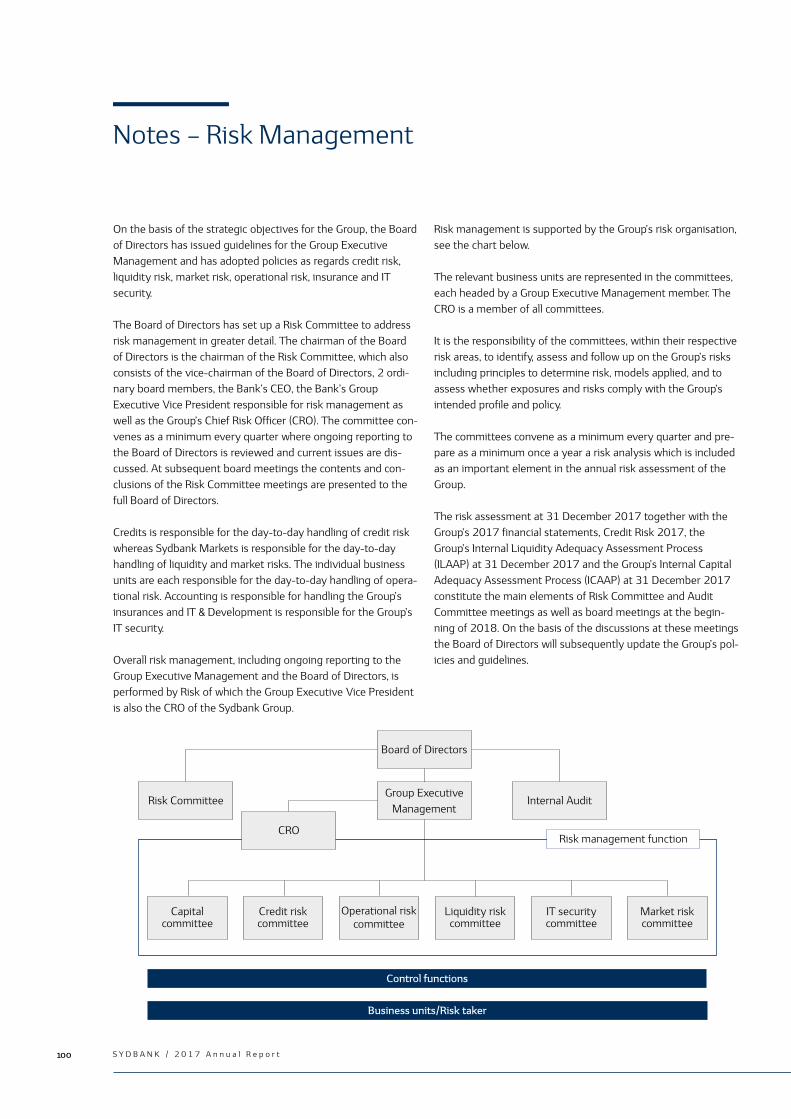

The committees in the Group’s risk organisation report directly

to the Group Executive Management. The committees identify,

monitor and assess risks within the individual risk areas and

ensure that models and principles are formulated to calculate

risks. The committees ensure that the Bank’s business units

proactively carry out their operations and analyse identified

risks. The Group’s Chief Risk Officer is a member of all

committees, see Risk Management on page 100.

A risk assessment is carried out annually to determine the

Group’s risk profile. The Board of Directors considers the

assessment and determines the adequate total capital and the

individual solvency need in continuation of this assessment.

The adequate total capital is determined on the basis of the

Danish FSA approach (8+). A proposal for the determination of

the adequate total capital is prepared by Risk and is presented

to the Group Executive Management. The Board of Directors

discusses and determines the adequate total capital on the

basis of this proposal.

The proposal is based on the capital adequacy rules (Pillar I)

with add-ons for any risks deemed not to be sufficiently

covered under Pillar I. At year-end 2017 add-ons were allocated

in relation to credit risk, market risk and operational risk.

The models used to calculate the Pillar I capital requirement are

described in detail in note 3.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K 23

The adequate total capital/solvency need can be broken down

as follows:

Adequate total capital/solvency need

DKKm% of REA

Credit risk 4,547 7.7

Market risk 600 1.0

Operational risk 892 1.5

Other exposures 456 0.8

Adequate total capital/solvency need 6,495 11.0

Other exposures include property, plant and equipment and the

Group’s equity investments.

Total capital is the actual capital that the Group has at its

disposal.

Based on the adequate total capital the Group’s capital

structure can be specified as follows at 31 December 2017:

Capital structure

DKKm% of REA

Adequate total capital/solvency need 6,495 11.0

Combined buffer requirement 1,089 1.9

Capital requirement inclcombined buffer requirement 7,584 12.9

Excess capital 4,656 7.9

Total capital 12,240 20.8

Stress testing is another important element when determining

the adequate total capital.

The object of stress testing is to assess the impact of adverse

events on capital needed and income. Stress test calculations

show the impact for the coming years in given economic

scenarios.

At 31 December 2017 the Group has based its stress test

calculations on the following macroeconomic scenarios:

Base case scenario which reflects the Group’s forecast of

developments in the economy.

Mild recession which reflects deteriorated economic conditions

compared with the base case scenario. Annualised GDP is

expected to develop positively in 2018 and 2019.

Unemployment will remain at its current level in 2018 and 2019.

Global crisis which reflects that the Danish economy will be hit

by 2 blows: a domestic blow where confidence among Danish

consumers and businesses will weaken significantly and a

foreign blow where the international economy will be hit by a

new cyclical downturn. This scenario resembles a very deep

recession and in terms of GDP it is on a par with the recession

during the period 2008-2009. Unemployment will increase

substantially. GDP developments will be negative in 2018 and

2019 and house prices will drop sharply during the same

period.

Lending freeze which reflects a scenario resembling the global

crisis scenario. However Danish households and consumers will

be more reluctant to borrow money. This can be construed as a

more severe domestic blow to the Danish economy. The

recession will be slightly deeper than in the global crisis scenario.

Deflation which reflects that inflation will continue to decrease

in Denmark and the euro area leading to deflation where the

overall level of prices will drop. Compared with the global crisis

scenario, Denmark will see more significant declines in prices

and lending.

Interest rate increase which reflects a steep rise in oil prices. In

the light of sharply rising inflation the central banks in USA and

the euro area will hike interest rates considerably. Danish

economic growth will come to a standstill, unemployment will

rise slightly and property prices and lending will decline.

Debt crisis which could reflect Greece abandoning the euro,

prompting renewed uncertainty as regards other debt-ridden

euro area countries. Another scenario could be the bank crisis

or the political instability in Italy having a severe adverse impact

on the Italian economy. Both scenarios involve a setback for

Europe’s economy and investors fleeing from debt-ridden

countries. Danish economic growth will be slightly negative and

unemployment will be higher than in the mild recession

scenario. At the same time Denmark, via its status as a safe

haven, will attract foreign capital, which will push interest rates

lower than in the base case scenario.

The scenarios and their relevance are subject to ongoing

assessment and the scenarios are approved by management as

the basis for further stress test calculations. The impacts of the

scenarios are included in the assessment of the adequate total

capital. The stress tests conducted show that the Group is

adequately capitalised.

Throughout 2017 the Group has fully complied with external as

well as internal capital requirements.

24 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

To support its strategic goals the Group ensures that stakehold-

ers receive accurate and complete information. This is done by

targeting investor communication according to best practice

and by maintaining a high degree of professionalism.

The Group strengthens and expands relations with investors

and analysts by conducting roadshows when its financial state-

ments are published.

In addition management interacts with analysts, shareholders

and potential investors at a number of seminars and conferenc-

es where current issues concerning Sydbank are presented and

discussed.

In 2017 Sydbank held approximately 150 meetings with inves-

tors in Western Europe and USA.

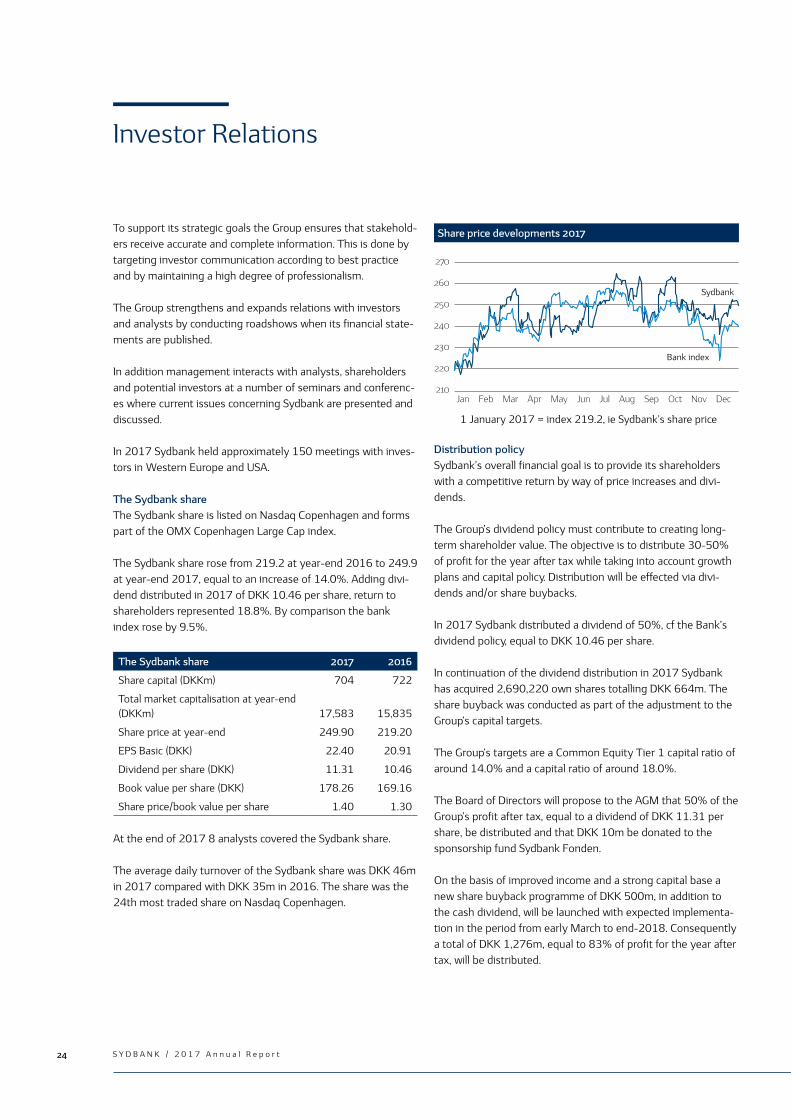

The Sydbank share The Sydbank share is listed on Nasdaq Copenhagen and forms

part of the OMX Copenhagen Large Cap index.

The Sydbank share rose from 219.2 at year-end 2016 to 249.9

at year-end 2017, equal to an increase of 14.0%. Adding divi-

dend distributed in 2017 of DKK 10.46 per share, return to

shareholders represented 18.8%. By comparison the bank

index rose by 9.5%.

The Sydbank share 2017 2016

Share capital (DKKm) 704 722

Total market capitalisation at year-end (DKKm) 17,583 15,835

Share price at year-end 249.90 219.20

EPS Basic (DKK) 22.40 20.91

Dividend per share (DKK) 11.31 10.46

Book value per share (DKK) 178.26 169.16

Share price/book value per share 1.40 1.30

At the end of 2017 8 analysts covered the Sydbank share.

The average daily turnover of the Sydbank share was DKK 46m

in 2017 compared with DKK 35m in 2016. The share was the

24th most traded share on Nasdaq Copenhagen.

Share price developments 2017

Distribution policySydbank’s overall financial goal is to provide its shareholders

with a competitive return by way of price increases and divi-

dends.

The Group’s dividend policy must contribute to creating long-

term shareholder value. The objective is to distribute 30-50%

of profit for the year after tax while taking into account growth

plans and capital policy. Distribution will be effected via divi-

dends and/or share buybacks.

In 2017 Sydbank distributed a dividend of 50%, cf the Bank’s

dividend policy, equal to DKK 10.46 per share.

In continuation of the dividend distribution in 2017 Sydbank

has acquired 2,690,220 own shares totalling DKK 664m. The

share buyback was conducted as part of the adjustment to the

Group’s capital targets.

The Group’s targets are a Common Equity Tier 1 capital ratio of

around 14.0% and a capital ratio of around 18.0%.

The Board of Directors will propose to the AGM that 50% of the

Group’s profit after tax, equal to a dividend of DKK 11.31 per

share, be distributed and that DKK 10m be donated to the

sponsorship fund Sydbank Fonden.

On the basis of improved income and a strong capital base a

new share buyback programme of DKK 500m, in addition to

the cash dividend, will be launched with expected implementa-

tion in the period from early March to end-2018. Consequently

a total of DKK 1,276m, equal to 83% of profit for the year after

tax, will be distributed.

Investor Relations

270

260

250

240

230

220

210

1 January 2017 = index 219.2, ie Sydbank’s share price

Sydbank

Bank index

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

252 0 1 7 A n n u a l R e p o r t / S Y D B A N K

AarhusRegion

14%

HerningRegion

9%Vejle

Region

13%

KoldingRegion

8% OdenseRegion

9%

NæstvedRegion

8%

CopenhagenRegion

14%

AabenraaRegion

14%

EsbjergRegion

11%

Geographical distribution of Sydbank’s business volume in Denmark

Mission Statement and Business Goals

Sydbank has a solid financial foundation that offers room for

more business with new customers as well as existing custom-

ers. Our growth will be built on a firm and sound footing.

Sydbank wishes to remain a bank operating on its own terms

and we aim to be the preferred business partner. We focus on

our own products but use business partners for a wide variety

of financial services, for instance mortgage credit, pension and

insurance.

As an advisory and service undertaking Sydbank’s primary

objective is to meet the financial requirements of its customers.

Sydbank achieves this objective by striving to be among the

absolute top performers in Denmark in terms of operating a

bank and providing advisory services to customers based on

their unique situation. As a nationwide bank Sydbank is present

in all parts of Denmark.

Sydbank’s business volume is evenly distributed across 9

Danish regions which form the basis of the direct advisory ser-

vices to the Bank’s customers. The total business volume con-

sists of loans and advances, deposits, guarantees and custody

accounts. Depending on customer segment and type of busi-

ness Sydbank has a market share of between 6 and 13%. The

Bank’s largest market share is within the SME segment.

Moreover Sydbank has 3 branches in Northern Germany and

together they constitute the Bank’s 10th region.

2 0 1 7 A n n u a l R e p o r t / S Y D B A N K

Sydbank’s business model

• Sydbank is a bank operating on its own terms.

• Sydbank is a competent and value-creating advisory

bank.

• Sydbank is a relationship bank and professional

relationships are the reason why we can create,

maintain and build on long-term customer relationships.

• We strive for simplicity in our work.

• Sydbank wants to be known for its belief that excellent

and committed employees are its most important asset.

26 S Y D B A N K / 2 0 1 7 A n n u a l R e p o r t

Values and attitudesSydbank’s interaction with its customers and other stakeholders

is based on a number of values and business principles and is

expressed in the statement: “Excellence and relationships create

value”. In addition the Bank’s stakeholder policy serves as a

guideline for its efforts in this respect.

Sydbank is convinced that the combination of excellent employ-

ees and good relationships creates value for customers – and the

Bank. Moreover Sydbank believes that strong relationships with

all stakeholders is an important business advantage. At Sydbank

we have a simple organisation to ensure high accessibility and

easy access to decisions so we can act quickly on behalf of our

customers and on our own behalf. Sydbank makes 3 promises –

to its customers, to its employees and to its shareholders.

Banking – pure and simple Sydbank’s mission is to be a bank that is close to its customers.

We are an advisory bank and find solutions where they are –

quickly and efficiently. Sydbank builds on relationships between

people. And we focus on what is important – banking and

sound business. Banking – pure and simple.

Sydbank is a bank for most people but not the same bank for

everyone. We serve our customers on the basis of their require-

ments and offer digital self-service solutions that enable cus-

tomers to carry out everyday banking transactions in an easy

and flexible manner. Sydbank provides the services in demand

by customers and sees technology as a way to bring us even

closer to customers.

Sydbank has a large number of online and digital solutions. In

NetBank and MobilBank customers can carry out their everyday

banking transactions whether they are corporate clients, Private

Banking clients or retail clients. For instance Sydbank offers

MobilBank Corporate and Online Banking, both of which are

fully integrated with the customer’s ERP systems. Sydbank is

also part of the MobilePay cooperation and part of the Bolighed

property portal.

Moreover customers can get in touch with Sydbank via the

branches in the Bank’s 9 Danish regions, its branches in

Germany and its specialist functions at the head office in

Aabenraa. Providing full service to all customers, the Danish

regions are organised in Corporate, Private Banking and Retail

sections and service the Bank’s branches.

Sydbank Direct is the Bank’s online advisory and service offer-

ing using a number of different channels. This enables custom-

ers to contact the Bank when and how it suits them best. In

addition Sydbank Direct has a special advisory department for

young customers aged between 18 and 29.

Sydbank Direct staff have a background in banking. The depart-

ment is open all weekdays between 8am and 8pm and is only

closed on public holidays, 24 and 31 December.

Customers As a large nationwide bank Sydbank has customers in all cate-

gories. Guided by Sydbank’s service philosophy “What can we

do for you”, the Bank wishes to increase the following customer

segments:

• Sound and well-run SMEs

• Retail clients with healthy finances

• Young customers undergoing education and training and

with a foreseeable potential

• Wealthy retail clients.

The Bank aims to have a diversified customer portfolio with only

few large exposures and diversification across industries corre-

sponding as far as possible to the Danish corporate structure.

CorporateSydbank aims to be the preferred business partner for SMEs

and prioritises building and maintaining value-creating relation-

ships with all corporate clients.

Consequently the Bank’s corporate clients receive advisory ser-

vices from a personal adviser who knows the individual enter-

prise and its situation. When needed the personal adviser

draws upon the expertise of the Bank’s many specialists in the

development of and the collaboration with the enterprise.

Sydbank is a full-scale corporate bank offering all financing solu-

tions tailored to the requirements of the individual enterprise.

Our corporate clients have access to efficient international com-

mercial banking services. Sydbank offers payment services and

Mission Statement and Business Goals

Sydbank’s stakeholder policy

• Sydbank will act as an open and credible

organisation proactively seeking dialogue with its

stakeholders and the surrounding community.

• Sydbank will treat its stakeholders responsibly,

properly and respectfully.

• Sydbank will base its decisions on dialogue with

significant stakeholders.

• Sydbank will communicate based on facts, in due

time, comprehensibly and precisely with relevant

stakeholders.

272 0 1 7 A n n u a l R e p o r t / S Y D B A N K

cash management solutions virtually worldwide. This is effected

through the Bank’s branches in Germany and the Connector banks.

As a rule corporate clients are served by one of the Bank’s

regional head offices or by special corporate branches. Sydbank

wishes primarily to have SMEs with growth potential as cus-

tomers. The enterprises must have a sound financial footing and

use the main part of the Bank’s palette of products and services.

Corporate clients are divided into 5 segments and are served by

the following entities:

• Corporate by Corporate Banking & Finance

• Corporate Large by the corporate centres

• Corporate Medium by the corporate departments

• Corporate Local by retail branches with corporate local

departments

• Agricultural clients by the agricultural centres.

Private BankingPrivate Banking at Sydbank strives to provide qualified advisory

services at all times. As a result the Bank focuses on long-term

relationships with each customer.

Within Private Banking Sydbank has a physical Private Banking

centre in each of the Bank’s 9 regions as well as 1 in Northern

Germany. Advisory services are provided by dedicated Private

Bankers who are are assisted by a team of experts tailored to

the specific requirements of the individual customer. The team

at the customer’s disposal provides advisory services on eg

investments, wealth management and current financial issues.

In addition special experts from the Bank’s central functions are

called upon as required.

Sydbank’s Private Banking concept is offered to wealthy retail

clients with investable assets or a household income above a

specified level. As an add-on to the Private Banking concept,

Sydbank offers its wealthiest customers Sydbank’s Private

Banking Elite.

The Private Banking concept consists of advisory services as

well as a range of benefits, thereby providing customers with

attractive terms regarding eg payment cards, insurance, invest-

ment products and related services as well as fees and charges.

For many years Sydbank has targeted the investment area and

the Bank has primarily focused on providing personal and indi-

vidual advisory services to its customers. The extent of invest-

ment advisory services depends in general on a customer’s

investment preferences.

RetailOur loyalty programme Sydbank Favorit is offered to retail cli-