83

2017 Investment Community Meeting September 7, 2017

2017Investment Community MeetingSeptember 7, 2017

©20

17 M

aste

rcar

d.

Agenda7:30 a.m. Registration 10:30 a.m. International Markets

Ann Cairns

8:30 a.m. WelcomeWarren Kneeshaw

10:40 a.m. Europe Panel DiscussionAnn Cairns, Javier Perez, Mark Barnett, Carlo Enrico

8:35 a.m. Our Strategy AdvancesAjay Banga

11:05 a.m. Emerging MarketsLing Hai, Ari Sarker, Gilberto Caldart

8:50 a.m. Global Products:Powering Choice and ConvenienceMichael Miebach

11:20 a.m. Financial PerspectiveMartina Hund-Mejean

9:15 a.m. Addressing Digital OpportunitiesGarry Lyons

11:35 a.m. Q&A Session

9:35 a.m. Securing and Advancing CommerceAjay Bhalla

9:45 a.m. North American MarketsCraig Vosburg

10:10 a.m. Break

©20

17 M

aste

rcar

d.

Forward looking statements

Today’s presentation may contain, in addition to historical information, forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

These forward-looking statements are based on our current assumptions, expectations and projections about future events which reflect the best judgment of management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by our comments today. You should review and consider the information contained in our filings with the SEC regarding these risks and uncertainties.

Mastercard disclaims any obligation to publicly update or revise any forward-looking statements or information provided during today’s presentations.

Any non-GAAP information contained in today’s presentations is reconciled to its GAAP equivalent in the appendices at the end of this presentation.

2017 Investment Community Meeting

Our Strategy AdvancesAjay BangaPresident and Chief Executive Officer

©20

17 M

aste

rcar

d.

2012 2013 2014 2015 2016 2017YTD

Net Revenue 13%

EPS 19%

Creating shareholder value

Total Shareholder Return1

Jan 1, 2012 - Aug 31, 2017

Currency-Neutral5-Year CAGR%2

1 Source: Factset. 2 Note: See Appendix A for non-GAAP reconciliation.

-25%

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%269%

MastercardS&P 500S&P 500 Info Tech

121%

168%

©20

17 M

aste

rcar

d.

Our strategy advances

Enabled by Brand, Data, Technology and People

GROWCore Business

• Consumer Credit• Debit• Commercial• Prepaid• Physical-Digital

Convergence

DIVERSIFYCustomers & Geographies

• Merchants• Businesses• Governments• Financial Inclusion• New Markets

• Advisors• Safety & Security• Loyalty & Rewards• Processing• Fast ACH

BUILDNew Businesses

©20

17 M

aste

rcar

d.

Shift to card Real-time payments and Fast ACH

Consulting, data analytics,fraud and loyalty solutions Automated services, ACH services

Digital payments, QR codes Artificial Intelligence, IoT-based payments

POS and online focused Protecting data across all devicesand channels

Digital players, telcos, startups Emerging market and social media players

Financial inclusion, interchange regulation, domestic schemes

New domestic schemes,increasing regulatory actions

Rapidly evolving payments landscape

Acceleration ofElectronic Payments

Evolution ofTechnology

Security andCybersecurity Threats

Regulatory Interestand Nationalism

Demand forAdjacent Services

New Entrants

Current trends Emerging trends

©20

17 M

aste

rcar

d.

202

225

60

49

114

17

58

11

86

PCE B2B P2P/B2C TOTAL

Market size by payment flowVolume in $ Trillions

Carded ACH Cash & Check

Expanded capabilities increasing our opportunity...more than

4x 90%

10%

$451 $120 $60 $2251,2

Note: Figures may not sum due to rounding. 1 Includes approximately $4 trillion in non-purchase personal consumption. 2 Includes non-PCE card spend.Sources: 2016 – Oxford Economics, Euromonitor International, Kaiser Associates, McKinsey Payment Data; Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Delivering value through services

Card orAccount-basedsolutions

DataAnalytics

Advisors

Processing

Labs asa Service

Safety &Security

Loyalty& Rewards Driving Our

Core Business

Delivering Differentiation

WinningDeals

©20

17 M

aste

rcar

d.

Closing thoughts

Significant untapped opportunity ahead of us

Executing our strategyaround the world

Buildingnew capabilitiesanddifferentiatingwith services

Anticipating market and technology trends

Addressing nationalism, regulatory risks andcompetitive disruption

Well-positionedfor continuedlong-term growth

2017 Investment Community Meeting

Global Products:Powering Choice andConvenienceMichael MiebachChief Product Officer

©20

17 M

aste

rcar

d.

Our product strategy – powering choice and convenience

Who What How

Consumers

Partners

World Class Brand

Value-Added Services

Differentiated Products Seamless, Digitized Technology

Every Device an Acceptance Device

Multi-Rail Network

Grow, Diversify, Build

©20

17 M

aste

rcar

d.

Capturing more payment flows

Product Solutions

PCE B2B P2P / B2CPoint of

InteractionAccounts Payable

Consumer Cards (Credit, Debit, Prepaid)

Commercial Cards (SME, T&E, P-Card, Fleet)

Virtual Cards / Mastercard B2B Hub™

Mastercard Send™ / HomeSend

Fast ACH

Market Size* $45T $120T $60T

Opportunity$225T

Card Rails ACH / Fast ACH Rails

* Source: 2016 – Oxford Economics, Euromonitor, McKinsey Payment Data, Kaiser, Mastercard Estimates

©20

17 M

aste

rcar

d.

Delivering strong results and growth

Global1H 17 GDV*

Consumer Credit +7%

Consumer Debit +8%

Prepaid +15%

Commercial +15%

* Adjusted for the impact of recent EU regulatory changes (Article 8). See Appendix F

©20

17 M

aste

rcar

d.

Winning affluent credit around the world

Digital

Experiences over Things

Hyper-Personalized

Easy to Use

Personalized Benefits

Priceless Experiences and Luxury Properties

Digital by Default

Ease & Consistency

Affluent cards growing 5x faster than affluent segment*

Leading share ofaffluent spend in UK

Winning 9 out of 10 dealsin MEA

Affluent portfolio growing ~30% YoY in LAC

Expanding into India;Premium wins in China

Citi Prestige enhancementsin US

Evolving AffluentConsumer Expectations What We BringYielding Results

* Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Accelerating commercial growth into the B2B opportunitySizeable B2B opportunity Dual track approach

Global Commercial Flows ($T)

Point of Interaction

Accounts PayablePrimarily ACH and

check

Point of Interaction

Primarily card, check

and cash

20Total

20

100

120 SME

Accounts Payable

T&E

Purchasing

VirtualCards

MastercardSend

Mastercard B2B Hub™ Vocalink

Yielding Results

MA Commercial Card PV

20162013

+13% CAGR

the market

MA growth

Real-time payment certainty

Data and efficiency

significantly outpacing

Fleet

©20

17 M

aste

rcar

d.

Person

Government

Merchant

Business

Senders

Our network strategy – enabling all electronic payments

Receivers

Person

Government

Merchant

Business

All Electronic Rails

Value-Added Services

Differentiated Products

©20

17 M

aste

rcar

d.

Driving Fast ACH through Vocalink

Market leading provider of Fast ACH

Proven deployments in multiple markets

Extends Mastercard reach beyond cards

Well suited forAccounts Payable flows

Enhanced data & messaging capabilities

Faster, nearreal-time payments

Card Rails + Vocalink MA is a one-stop shop providing seamless,omni-channel, multi-payment support

Fast ACH features Competitively advantaged to succeed

©20

17 M

aste

rcar

d.

Our go-to-market approach with Fast ACH

Infrastructure

Scheme & Applications

Services

ACH operates atmultiple levels How will we play?

Strategically deploy and license

RetailPayments

BillPayments

Personal PaymentsB2B

FraudSolutions

DataAnalyticsConsulting

Underlying technology and rails

End user solutions built on Franchise rules and standards

Enhanced ACH capabilities

©20

17 M

aste

rcar

d.

Mastercard is at the forefront of acceptance growth

Every Device is an Acceptance Device…from Millions to Billions

Rails

Flows

Devices

Cards Emerging Technologies

Fast ACH

Person Merchant

GovernmentBusiness

More Merchants

More Acceptance

Merchants Beyond

Acceptance

Acceptance Beyond

Merchants

1

2

3

©20

17 M

aste

rcar

d.

DifferentiatedValue Propositions

Every Device an Acceptance Device

All Electronic Payments on All Rails

Cards ACH

Well positioned to capture more payment flows

2017 Investment Community Meeting

Addressing Digital OpportunitiesGarry LyonsChief Innovation Officer

©20

17 M

aste

rcar

d.

Increasingly connected world

Public-private partnerships

Advances in AI

Security and privacy top of mind

On-demand economy

Lines blurring between physical and digital

Pace of change

Urbanization and smarter cities

Focus on sustainability

Consumer expectations

…and it’s impacted by multiple trends

The digital shift is the biggest change inpayments since plastic cards

Digital commerce as share of retail payments

10% → 17%2016→2021

©20

17 M

aste

rcar

d.

Source: McKinsey study, excludes travel, 2017

©20

17 M

aste

rcar

d.

Our strategy – enable our customers and partners tobe at the forefront of digital payments

Identifying and experimenting with future technologies, start-ups & trends

Digitizing all forms of personal and business payments

Securingevery transaction

Delivering the best digital experience everywhere

Simplifyingaccess to, and integration of,our digital assets

Mastercard Digital Enablement Service,

Biometrics and Machine Learning

Mastercard Send

andand

©20

17 M

aste

rcar

d.

Delivering the best digital experience everywhereDriving the best-in-market digital payment service with Masterpass

90+ millionEnabled ‘Digital by Default’ accounts

Strong progress with customers in 2017

38Countries

140+Issuers live

Expanding acceptance with key merchants and partners

©20

17 M

aste

rcar

d.

Ghana

India

Kenya

Nigeria

Pakistan

Rwanda

Tanzania

Uganda

Delivering the best digital experience everywhereReaching new markets and expanding acceptance with Masterpass QR

Strong progress to date

400K+merchant locations

20+issuers signed

8live markets

22enabled markets

©20

17 M

aste

rcar

d.

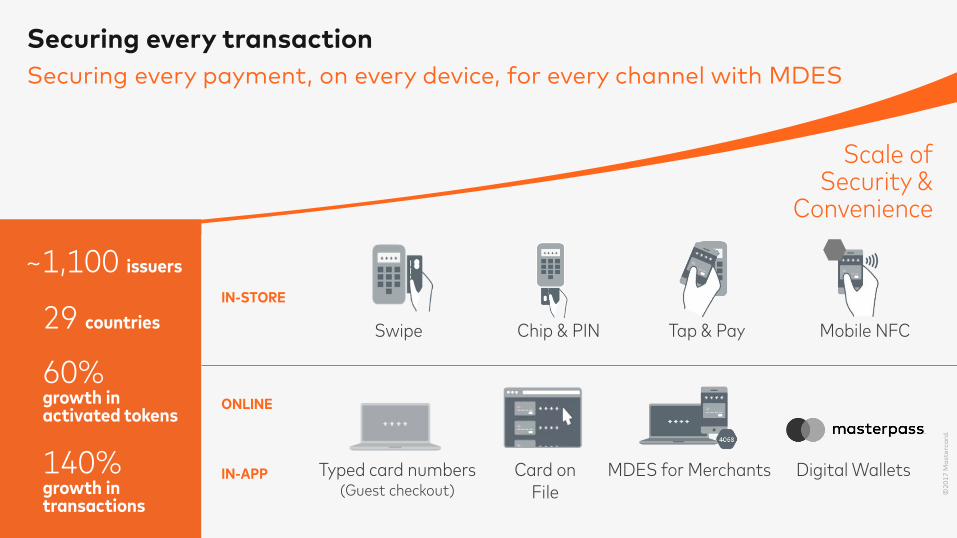

Securing every transactionSecuring every payment, on every device, for every channel with MDES

Typed card numbers(Guest checkout)

MDES for Merchants

Chip & PIN Mobile NFC

IN-STORE

ONLINE

IN-APP Digital WalletsCard onFile

Swipe Tap & Pay

©20

17 M

aste

rcar

d.

29 countries

60%growth inactivated tokens

140%growth in transactions

Scale of Security &

Convenience

~1,100 issuers

©20

17 M

aste

rcar

d.

Securing every transactionKeeping the consumer in control

©20

17 M

aste

rcar

d.

Capturing more payment flows

Product Solutions

PCE B2B P2P / B2CPoint of

InteractionAccounts Payable

Consumer Cards (Credit, Debit, Prepaid)

Commercial Cards (SME, T&E, P-Card, Fleet)

Virtual Cards / Mastercard B2B Hub

Mastercard Send / HomeSend

Fast ACH

Market Size* $45T $120T $60T

Opportunity$225T

Card Rails ACH / Fast ACH Rails

* Source: 2016 – Oxford Economics, Euromonitor, McKinsey Payment Data, Kaiser, MA Estimates

©20

17 M

aste

rcar

d.

Digitizing all forms of personal and business payments

Businesses

Governments

LicensedEntity

Sin

gle

Con

nect

ion MA Cards Purpose-Specified

PrepaidNon-MA

Cards

CashPick-up

Mobile Wallets

Person-to-Person

Bank Accounts

Mastercard Send™, a global integrated push payments platform, enabling domestic and cross-border funds transfers

Domestic

100Countries

HomeSend

Mastercard Send

©20

17 M

aste

rcar

d.

Disbursements

Domestic Person-to-Person Payments

Person-to-Merchant Payments

Cross-Border B2B Payments

Digitizing all forms of personal and business paymentsSignificant opportunity with good progress tapping into new flows

Cross-Border Remittances

HomeSend

Mastercard Send

©20

17 M

aste

rcar

d.

Simplifying integration of our services

An API for Everything strategy

Enables others to easily integrate our services

Digitizes core product propositions and enables access to underlying network services

Provides tools to simplify the process further – SDKs, automation and test frameworks, sandboxes, etc.

More than 60 APIs available for banks, processors, merchants, startups across payments, data and security

©20

17 M

aste

rcar

d.

©20

17 M

aste

rcar

d.

Identifying and experimenting withfuture technologies, start-ups and trends

Augmenting our customers’ product

development and innovation capabilities

Embracingnew ways of innovating

Incubation of new products and solutions

Looking at the future from a

fresh perspective

Showcasing innovation

and co-creating with partners

Anticipating and building beyond the payment with Mastercard Labs

©20

17 M

aste

rcar

d.

Our approach is very straightforward

Partner-centric in everything we do

Delivering a great experience across every device and every channel

Enabling more payment flows in real-time

Experimenting andco-innovating with customers and partners

Leading set of APIs

Relentlessly securing every transaction

2017 Investment Community Meeting

Securing & Advancing Commerce

Ajay BhallaPresident, Enterprise Security Solutions

©20

17 M

aste

rcar

d.

Rapidly changing world creating huge opportunities

Internet of Things

I amMy Data

Trust in the Sharing Economy

First ‘Digital Native’ Generation

Attacks more global,contagion more rapid

©20

17 M

aste

rcar

d.

A strategy anchored on the principle of ‘security by design’

Issuers Merchants Consumers Governments

Secure assets againstcyber attacks

Prevent

Detect fraudulent behavior & attacksDetect

Redesign customer security experienceExperience

Identify Secure the account holder

©20

17 M

aste

rcar

d.

Successful strategy driving future vision to secure payments

Securing devices,data & networks

Leveraging Artificial Intelligence for smart solutions

Enhancing trust with‘Digital Identity’

Building frictionlesspayment experiences

Success so far Future focus

1.7 billion chip cards globally…

…chip security embedded in devices

Safety Net & Decision Intelligence®saving $ millions for issuers

4.5 billion digital identities verified over past year…

Account Continuity, IQ Series & Alerts optimize the consumer experience

…launched biometrics for mobile & cards

&

©20

17 M

aste

rcar

d.

Securing the Internet of Things

Every connected device to be a secure payment device

Every connected device is a potential entry point for hackers

Our portfolio of solutions secures devices,data and networks

NuData enhances our IoT capabilities, including:botnet automation, user behavior and device reputation

©20

17 M

aste

rcar

d.

Leveraging artificial intelligence for smart solutions

Artificial Intelligence needed to mine mountains of data, and create the best experiences for stakeholders

Artificial Intelligence deeply embedded in Mastercard network

Brighterion enhances our capabilities –Collaborative Artificial Intelligence uncovers deeply hidden data relationships

Innovation is enhancing detection of increasingly sophisticated attacks and improving the consumer experience

Detect fraudulent behavior & attacksDetect

©20

17 M

aste

rcar

d.

Our strategy is…

Ensuring EcosystemSecurity

Working with stakeholders to deploy amulti-layered strategy to secure andadvance commerce

Building competitive advantage withmarket-leading solutions and services

Creating Sources of Differentiation

Enabling new growth opportunitiesand businesses

DeliveringNew Sourcesof Growth

2017 Investment Community Meeting

North American MarketsCraig VosburgPresident, North America

©20

17 M

aste

rcar

d.

North America

51

61

8

15

24

3

16

4

23

PCE B2B P2P/B2C TOTAL

Carded ACH Cash & Check

$141 $25 $18 $571

Market size by payment flowVolume in $ Trillions

2 of top 5 Mastercard markets• % of global revenues• % of total volume

Cash/Check Opportunity(all flows)

PCE Growth (2017)• US• Canada

ACH Opportunity(all flows)

$23T

4.1%4.5%

$24T

41%35%

Note: Figures may not sum due to rounding. 1 Includes approximately $4 trillion in non-purchase personal consumption.Sources: 2016 – Oxford Economics, Euromonitor International, Kaiser Associates, McKinsey Payment Data, US Bureau of Economic Analysis, 2017; Statistics Canada, 2017; Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Clear strategy – focused on execution

Drivecore product

usage

Deliveradded value

to customers

Commercialize B2B, P2P, B2C

Grow share inall segments

Expandnew verticalsand segments

Partner First ApproachHelp our customers reach their consumers

anywhere, anytime, on any device, anyway they want to pay.

Win inDigital

ScaleServices

Build New Payments Businesses

ExpandProduct Distribution

GrowAcceptance

GROW

BUILD

DIVERSIFY

©20

17 M

aste

rcar

d.

Expand product distributionStrong and growing relationships

United States Canada• Positioned to grow consumer credit

share with 6 of top 8 issuers

• 25 co-brand wins since 2015

• Present on over 60% of US debit cards

• Share growth with 3 of 4 top commercial issuers

• Exclusive brand for many of the largest prepaid programs

• Growing credit share

• Strong co-brand position

• Growing Debit Mastercard

• Double digit commercial volumegrowth (twice the market)

• Significant new prepaid programs

Sources: The Nilson Report, 2017; Euromonitor International, 2017; Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Grow acceptanceAccelerate growth through new verticals and partnerships

North America Acceptance Points

11% CAGRin North America acceptance points since 2012

Significant ongoing growth potentialNew verticals, digital, connected devices

2010 2011 2012 2013 2014 2015 2016 2017

Websites and new verticalssuch as rent, healthcare, utilities, etc.

Payments facilitators(e.g., Square)

Digital gateways(e.g., Stripe)

10MM

Sources: Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Win in digitalSecuring the future

80% of eligible MA accounts enabled for tokenization

DigitalEnablement

DigitalPartnerships

DigitalFuture

600+ participantsin Mastercard Digital Enablement Express

40+ millionaccounts enabledfor digital by default

Sources: Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Scale servicesDriving core product differentiation and incremental revenues

Advisors

65+ million accounts managed on our loyalty platform

Enabling digital payment and IoT strategies for merchants

Loyalty

Processing

Data & Analytics

Almost half of transactions benefit from our optional fraud scoring solutions (a 50% increase over last year)Fraud Solutions

Labs as a Service

Over 50% of customers use our project-based consulting services

30+ customer Launchpad events since January 2016

Over 60% of customers use our data & analytics solutions

©20

17 M

aste

rcar

d.

Packaging solutions to deliver customer value

Core Products

Instant Payouts

Digital Assets

Acceptance

Masterpass

All U.S. Co-Brands

Core ProductsDigital Assets

Data and Analytics

Fraud SolutionsMarketing Assets

Loyalty Solutions

Mastercard Labs

Consumer CreditConsumer Debit

Commercial

APT

Mastercard Advisors

Marketing Assets

Loyalty Solutions

AAdvantage™Co-Brand Programs

Fraud SolutionsMastercard Labs

©20

17 M

aste

rcar

d.

Build new payments businessesEnabling choice through single Mastercard partnership`

Products and SolutionsPotential Applications

B2B P2P B2CT&E Cards

Procurement Cards

Virtual Cards

Mastercard Send / HomeSend

Mastercard B2B Hub

Fast ACH

Established

New

©20

17 M

aste

rcar

d.

Positioning Mastercard for long-term success

Significant ongoing growth opportunity

Strongcustomer partnerships

Momentumacross the business

Focused ondelivering results

2017 Investment Community Meeting

International Markets OverviewAnn CairnsPresident, International

©20

17 M

aste

rcar

d.

International Markets

15

1

164

56

35

94

13

41

8

63

PCE B2B P2P/B2C TOTAL

Carded ACH Cash & Check

$311 $98 $43 $1731

Market size by payment flowVolume in $ Trillions

GDV Growth (2016)

Market share growing across all regions

14%

Note: Figures may not sum due to rounding.1 Includes non-PCE card spend.Sources: Oxford Economics, 2016 – Euromonitor International, Kaiser Associates, McKinsey Payment Data; Mastercard internal analysis.

Cash/Check Opportunity(all flows)

PCE Growth (2017)

ACH Opportunity(all flows)

$63T

7%

$94T

©20

17 M

aste

rcar

d.

Clear priorities, focused execution

Win in Digital

Grow Diversify

BuildSmartCities

EnterNew Markets

New flowsACH/B2B/P2P Differentiate

throughServices

Create newPartnerships

Attract newConsumers

Strengthen theCore Business

ExpandAcceptance

2017 Investment Community Meeting

Europe PanelAnn Cairns, Javier Perez, Mark Barnett, Carlo Enrico

©20

17 M

aste

rcar

d.

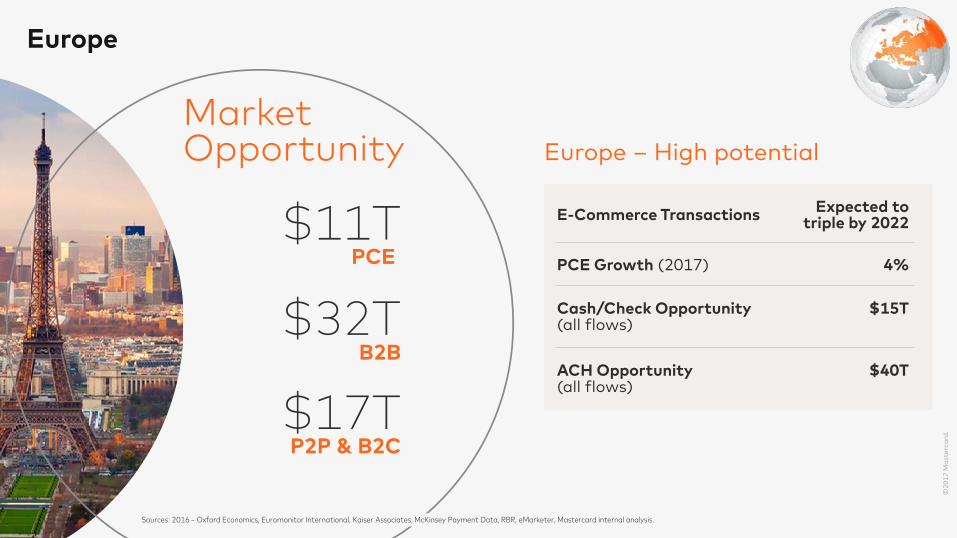

Europe

$11TPCE

$32TB2B

$17TP2P & B2C

MarketOpportunity Europe – High potential

E-Commerce Transactions

Cash/Check Opportunity(all flows)

PCE Growth (2017)

ACH Opportunity(all flows)

$15T

4%

$40T

Expected to triple by 2022

Sources: 2016 – Oxford Economics, Euromonitor International, Kaiser Associates, McKinsey Payment Data, RBR, eMarketer, Mastercard internal analysis.

2017 Investment Community Meeting

Asia Pacific OverviewLing Hai, Ari SarkerCo-Presidents, Asia-Pacific

©20

17 M

aste

rcar

d.

Asia Pacific

Asia – Dynamic and diverse

HNWI (2015)Wealth

Middle Class Consumption

#1 Wealthiest in the World$14T

PCE

$54TB2B

$20TP2P & B2C

MarketOpportunity

Cash/Check Opportunity(all flows)

PCE Growth (2017)

ACH Opportunity(all flows)

$39T

7%

$44T

Expected to more than double by 2025

Sources: 2016 – Oxford Economics, Euromonitor International, Kaiser Associates, McKinsey Payment Data, RBR, eMarketer, Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Grow Diversify Build

Asia Pacific – China

Differentiatethrough Services

Strengthen theCore businesswith 4xsingle-brandedcard issuance

ExpandAcceptanceto 10 million in 5 years

Scale digitalPartnerships

GrowCommercial

• Loyalty• Insights• Safety & Security

M D E S

Win in Digital

Capitalizing on China… medium to long term opportunity

©20

17 M

aste

rcar

d.

Asia Pacific – IndiaThe rise of India…

Economy on the move...GDP expected to double by 20251.GrowthOutlook

Government Policy

Digital India push – Demonetization & Goods & Service Tax (GST); Regulatory environment fostering open competitive market.

DigitalEnablement

Technology Stack...1.2B2 biometric ID system; Proxy based FAST payment.Unprecedented investment in 4G/LTE & fiber broadband infrastructure.

Infrastructure Power Airports RoadRail

Accelerating Fintechs

Fintech operating at a large scale backed by local and international accelerators, angel investors, PE & VC firms.

1. Oxford Economics 2.UIDAI, GOI

©20

17 M

aste

rcar

d.

Grow Diversify Build

Asia Pacific – India

SmartCitiesby winning in Transit

ExpandAcceptancethrough aggregators

ScalePartnershipswithin the digital ecosystem

Strengthen theCore business by increasing Debit share & winning in Affluent

GrowCommercial

Win in Digital

2017 Investment Community Meeting

Latin America OverviewGilberto CaldartPresident, Latin America & Caribbean

©20

17 M

aste

rcar

d.

Latin America and Caribbean

$3TPCE

$6TB2B

$4TP2P & B2C

MarketOpportunity

Population 15+ (2016)% underbanked

478 M49%

Latin America – Young and vibrant

PurchaseVolume

2016 MA LAC PerformanceLast 5yr CAGR

$196 B(17%)

Cash/Check Opportunity(all flows)

PCE Growth (2017)

ACH Opportunity(all flows)

$5T

8%

$7T

Sources: 2016 – Oxford Economics, Euromonitor International, Kaiser Associates, McKinsey Payment Data, Frontier Strategy Group, eMarketer, Mastercard internal analysis.

©20

17 M

aste

rcar

d.

Grow Diversify Build

Latin America and Caribbean – Brazil

Strengthen theCore business

Expand Acceptance

Differentiate throughServices

Scale & build strong Partnerships

Capture more flowsACH/B2B/P2P

SmartCities

Win in Digital

©20

17 M

aste

rcar

d.

Emerging Markets takeaways

Some of the world’s biggest economies

High cash usage Digitally savvy and connected population

Strong relationships within a diversified customer base

A one-stop shop, various payments rails, different channels

Digital, key driver in migration of cash to electronic payments

2017 Investment Community Meeting

Financial PerspectiveMartina Hund-MejeanChief Financial Officer

©20

17 M

aste

rcar

d.

Raised2017FinancialOutlook

Net Revenue*

Operating Expense*

Tax Rate

FX Impact

High end of low double-digits growth range

High single-digit growth

Full-year rate of about28%

Positive Operating Leverage

Slight benefit

* All figures are on a currency-neutral basis. Amounts exclude acquisitions and special items; see Appendix B for reconciliation of non-GAAP measures.

©20

17 M

aste

rcar

d.

Investment priorities

GROWCore Business

• Digital / Masterpass

• Acceptance

• Mastercard B2B Hub

• Network

DIVERSIFYCustomers & Geographies

• Emerging Markets

– China

– India

• Artificial Intelligence

• Fast ACH

• Data Analytics

BUILDNew Businesses

©20

17 M

aste

rcar

d.

Fast ACH business model

Role EconomicsTiming / Dependencies

Infrastructure

Operator Fixed pricing based oncapacity Country

level decision by regulators/schemeTechnology provider License +

implementation fees

Scheme / AppB2B, Bill Pay, Disbursement, P2P & P2M solutions

Value-based pricing Pay by Bank app in trial in UK

Services Comprehensive value-added services

Similar to traditional services model

Initial solutions being offered

©20

17 M

aste

rcar

d.

Capital planning priorities

Balance Sheet Long-Term Business Growth

Shareholder Return Capital Structure

Preservestrong balance sheet, liquidity and credit ratings

Investmentsin organic opportunitiesand M&A

Continue toreturn excess cashwith bias towards share repurchases

Gradual and disciplinedmigration to more normalized mixof debt and equity over time

©20

17 M

aste

rcar

d.

Return of capital$23+ billion returned to shareholders since IPO

$1.1$1.7

$2.4

$3.4 $3.5 $3.5

$2.5

$0.1$0.1

$0.3

$0.5$0.7 $0.8

$0.7

$1.2

$1.9

$2.7

$3.9$4.2 $4.3

$3.2

2011 2012 2013 2014 2015 2016 Aug 2017 YTD$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$ in

bill

ion

s

Share Repurchase

Dividends

Note: Figures may not sum due to rounding

©20

17 M

aste

rcar

d.

Long-term revenue growth potential

Revenue Growth

Potential

B2BP2P/B2C

New Flows

~$180T

PCE

~$45TServices

Mix

Pricing

Share

Low - MidTeens

~5% Annual Growth4-5% Secular Growth**Adj. for available market

MarketVolume/

TransactionsOpportunity

©20

17 M

aste

rcar

d.

Driving growth beyond the core

Core~75%

Services~25%

% of 2016 Revenue

Margin Level

Processing

Loyalty

Advisors

Safety & Security

Margin Expansion with ScaleRevenue CAGR* (2014 – 2016)Core ~9% Services ~29%

23 ppt ex-acquisitions6 ppt acquisitions

* On a currency-neutral basis; see Appendix C for reconciliation of non-GAAP measures

©20

17 M

aste

rcar

d.

Minimal impact expected from new revenue recognition rules

Primary ImpactCertain customer incentives will be recognized over the life of the contract, rather than when earned by the customer

Rules have now been clarifiedRebates and Incentives to continue to be treated as contra revenue

Implementation will occur prospectively starting in

Jan 2018Impact on 2017

expected to be minimal

©20

17 M

aste

rcar

d.

Raised longer-term performance objectives

2016–2018Performance Objectives

Prior

Net RevenueCAGR %*

High end of low double-digit

~20%

Lowdouble-digit

Mid-teens

Annual Operating Margin %

EPS CAGR %*

Minimum50%

Minimum50%

Updated

* On a currency-neutral basis, excluding certain items. See Appendix D for reconciliation of non-GAAP measures.

©20

17 M

aste

rcar

d.

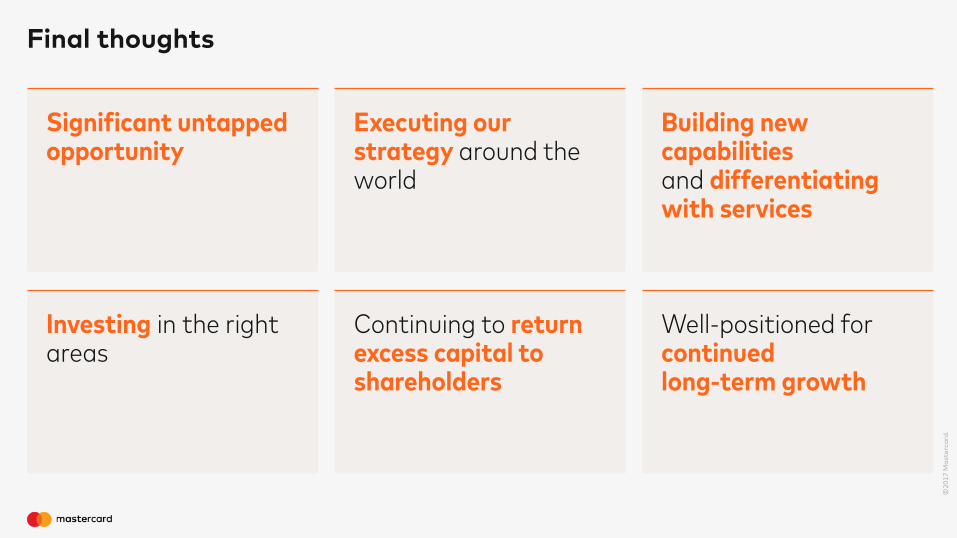

Final thoughts

Significant untapped opportunity

Executing our strategy around the world

Building new capabilitiesand differentiatingwith services

Investing in the right areas

Continuing to return excess capital to shareholders

Well-positioned for continuedlong-term growth

2017 Investment Community Meeting

Appendices

©20

17 M

aste

rcar

d.

Appendix ANon-GAAP reconciliation ($ in millions, except per share data)

Note: Table may not sum due to rounding1 Adjusted for both the translational and transactional foreign currency impact2 Impact of the U.S. Merchant Litigation Settlement (2011: $770 million pre-tax ($0.39 per diluted share); 2012: $20 million pre-tax ($0.01 per diluted share); 2013: $95 million pre-tax ($0.05 per diluted share); 2015: the termination of the U.S.

employee pension plan in $79 million pre-tax ($0.04 per diluted share) and U.K. Merchant Litigation Provision of $61 million pre-tax ($0.04 per diluted share); 2016: the U.K. Merchant Litigation Provision $117 million pre-tax ($0.08 per diluted share).

5-Year

2011 2012 2013 2014 2015 2016 CAGR

CAGRCurrency-neutral 1

Net revenue $ 6,714 $ 7,391 $ 8,312 $ 9,441 $ 9,667 $ 10,776 10% 13%

Operating income - as reported $ 2,713 $ 3,937 $ 4,503 $ 5,106 $ 5,078 $ 5,761 16% 20%Special items 2 770 20 95 - 140 117 Adjusted operating income $ 3,483 $ 3,957 $ 4,598 $ 5,106 $ 5,218 $ 5,878 11% 15%

Operating margin - as reported 40.4% 53.3% 54.2% 54.1% 52.5% 53.5%Special items 2 11.5% 0.3% 1.1% -% 1.4% 1.1%Adjusted operating margin 51.9% 53.5% 55.3% 54.1% 54.0% 54.5%

GAAP diluted EPS $ 1.48 $ 2.19 $ 2.56 $ 3.10 $ 3.35 $ 3.69 20% 24%Special items 2 0.39 0.01 0.05 - 0.08 0.08 Non-GAAP diluted EPS $ 1.87 $ 2.20 $ 2.61 $ 3.10 $ 3.43 $ 3.77 15% 19%

©20

17 M

aste

rcar

d.

Appendix BNon-GAAP reconciliation2017 full-year financial outlook

2017 vs. 2016Increase / (Decrease)

Net revenue Operating expenses

Forecasted growth - U.S. GAAP 1 Mid-teens High end of low-double digits

Special items 2 — 2%

Acquisitions (2)% (6)%

Foreign currency 3 (0-1)% (0-1)%

Forecasted growth - excluding special items andacquisitions, currency-neutral

High end of low-double digits High-single digit

1 2017 forecast versus 2016 actuals 2 Impact of Canadian merchant litigation (2017: $15M pre-tax) and U.K. merchant litigation provisions (2016: $117M pre-tax)3 Impact of foreign currency for both the translational and transactional impacts

©20

17 M

aste

rcar

d.

2014-20163-Year CAGR

Increase/(Decrease)

Core Revenue Services Revenue

GAAP 5% 25%

Foreign currency1 4% 4%

Non-GAAP – currency-neutral 9% 29%

Acquisitions2 — (6)%

Non-GAAP - excluding acquisitions, currency-neutral 9% 23%

Appendix CNon-GAAP reconciliation2014-2016 net revenue CAGR

1 Impact of foreign currency for both the translational and transactional impacts

2 Excludes the impact for acquisitions made during the 2014-2016 period.

©20

17 M

aste

rcar

d.

2016-20183-Year CAGR

Increase/(Decrease)

Prior Updated

Net Revenue EPS1 Net Revenue EPS1

GAAP Low-double digit Low-double digit Mid-teens High-teens

Special items2 — (1)% — (1)%

Acquisitions3 — — (1)% 1%

Foreign currency4 1% 1% (0-1)% (1)%

Significant tax items5 — 4% — 4%

Non-GAAP - excluding special items,acquisitions, currency-neutral, normalized taxes

Low-double digit Mid-teens High end of low double-digit ~20%

Appendix DNon-GAAP reconciliationLong-term performance objectives

1 Based on 2015 pro forma EPS utilized to measure 3‐year diluted EPS target performance (2016‐2018). See Appendix E 2 Impact of the 2015 termination of the U.S. employee pension plan ($0.04 per diluted share) and the U.K. merchant litigation provision ($0.04 per diluted share) 3 Impact of 2017 acquisitions 4 Impact of foreign currency for both the translational and transactional impacts5 Impact of discrete tax benefits and the tax impact of non-recurring repatriation benefits in 2015 ($0.31 per diluted share)

©20

17 M

aste

rcar

d.

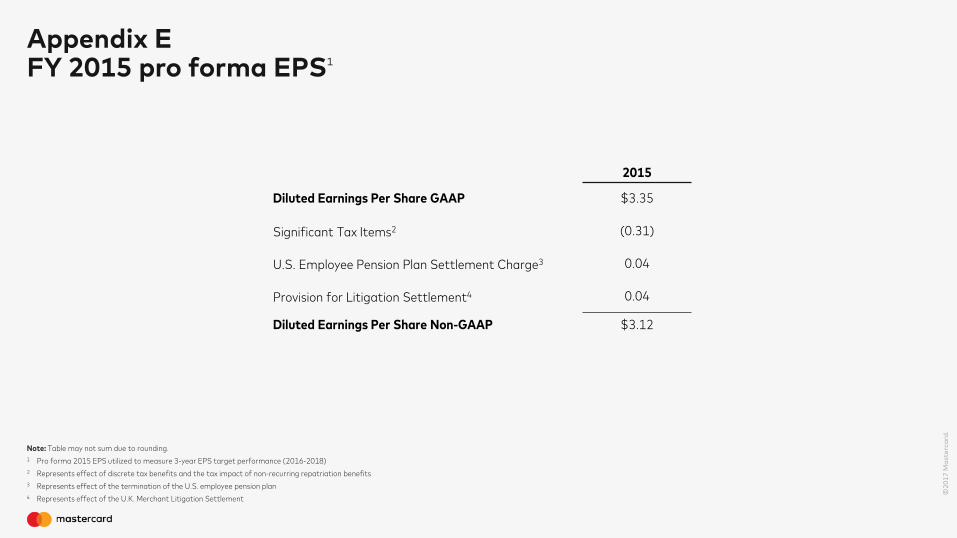

Appendix EFY 2015 pro forma EPS1

2015

Diluted Earnings Per Share GAAP $3.35

Significant Tax Items2 (0.31)

U.S. Employee Pension Plan Settlement Charge3 0.04

Provision for Litigation Settlement4 0.04

Diluted Earnings Per Share Non-GAAP $3.12

Note: Table may not sum due to rounding.1 Pro forma 2015 EPS utilized to measure 3-year EPS target performance (2016-2018)2 Represents effect of discrete tax benefits and the tax impact of non-recurring repatriation benefits3 Represents effect of the termination of the U.S. employee pension plan4 Represents effect of the U.K. Merchant Litigation Settlement

©20

17 M

aste

rcar

d.

Appendix FArticle 8 impacts on worldwide GDV

Growth (Local Currency)

1H2017GDV

Consumer Credit 6%Consumer Credit normalized for Article 8 7%

Consumer Debit 2%Consumer Debit normalized for Article 8 8%

Prepaid 14%Prepaid normalized for Article 8 15%

Commercial 13%Commercial normalized for Article 8 15%

Worldwide 5%Worldwide normalized for Article 8 8%

Note: Article 8 of the EU Interchange Fee Regulation which relates to card payments and which became effective June 9, 2016, states that a network can no longer charge fees on domestic EEA payment transactions that do not use its payment brand. Prior to that, Mastercard collected a de minimis assessment fee in a few countries, particularly France, on transactions with Mastercard co-badged cards if the brands of domestic networks (as opposed to Mastercard) were used. As a result, the non-Mastercard co-badged volume is no longer being included.

To aid in understanding the underlying trends in the business, the table above reflects adjusted growth rates for the impact of Article 8, by eliminating the related co-badged volumes in prior periods.