2017 Standard Scenarios Report: A U.S. Electricity Sector Outlook Wesley Cole, Trieu Mai, James Richards, and Paritosh Das, NREL Paul Donohoo-Vallett, U.S. DOE October 17, 2017 W. Cole et al., “2017 Standard Scenarios Report: A U.S. Electricity Sector Outlook,” NREL/TP-6A20-68548, 62 pp. (October 2017). NREL/PR-6A20-70328

Transcript

2017 Standard Scenarios Report: A U.S. Electricity Sector Outlook

Wesley Cole, Trieu Mai, James Richards, andParitosh Das, NREL

Paul Donohoo-Vallett, U.S. DOE

October 17, 2017

W. Cole et al., “2017 Standard Scenarios Report: A U.S. Electricity SectorOutlook,” NREL/TP-6A20-68548, 62 pp. (October 2017).NREL/PR-6A20-70328

NATIONAL RENEWABLE ENERGY LABORATORY 2

• Suite of 26 forward-looking scenarios (projections) of the U.S. power sector

• NREL report that identifies themes from the scenarios

o Uses the 26 scenarios to provide an outlook of the power sector

• Companion product of the Annual Technology Baseline

What is the “Standard Scenarios?”

NATIONAL RENEWABLE ENERGY LABORATORY 3

• Internal Value

o Consistency across analyses

o Improved efficiency

• External Value

o Share our input assumptions and model results

o Provide an additional perspective on power sector evolution

o Inform stakeholder decision-making

Why do we do the Standard Scenarios?

NATIONAL RENEWABLE ENERGY LABORATORY 4

• More scenarios

o Additional nuclear retirement sensitivities

o Low/high battery storage cost

o Low PV and Low Wind cost

• Clean Power Plan included only as a sensitivity

• Default nuclear retirements updated (mix of 60 and 80 years)

• State policy updates

• Various model improvements

Changes from last year

NATIONAL RENEWABLE ENERGY LABORATORY 5

• Summary of the Standard Scenarios

• Insights and perspectives from the 2017 Standard Scenarios (i.e., what is in the report)

• How to access the scenario data

Webinar Outline

The Standard Scenarios

NATIONAL RENEWABLE ENERGY LABORATORY 7

• Fuel prices: EIA Annual Energy Outlook (AEO) 2017

• Demand growth: AEO 2017

• Technology cost and performance: 2017 Annual Technology Baseline (ATB)

• Current policies (no Clean Power Plan)

• Current fleet characteristics: ABB Velocity Suite

The Mid-case Scenario

0

1

2

3

4

5

6

7

2010 2020 2030 2040 2050

Fu

el

Pri

ce

(2015$/M

MB

tu) Natural Gas

Coal

Uranium

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2010 2020 2030 2040 2050

Dem

an

d G

row

th

NATIONAL RENEWABLE ENERGY LABORATORY 8

Summary of the Standard Scenarios

Non-Policy Scenarios

Other

•Low Cost Financing

•Climate Change Impacts

•Reduced RE Resource

•Transmission Expansion Barriers

•Restricted Cooling Water

Fuel Cost

•High Oil & Gas Resource (AEO 2017)

•Low Oil & Gas Resource (AEO 2017)

Technology Cost

•Low RE Cost

•High RE Cost

•Low Wind Cost

•Low PV Cost

•Nuclear Breakthrough

•Low Battery Cost

•High Battery Cost

Retirements

•80 Year Nuclear

•60 Year Nuclear

•Accelerated Nuclear Retirement

•Accelerated Coal Retirement

Demand

•Low Demand

•High Demand

•Vehicle Electrification

Policy

•Clean Power Plan (as finalized in 2015)

•National 80% RPS by 2050

•83% CO2 Reduction by 2050

•ITC & PTC Extension to 2030

NATIONAL RENEWABLE ENERGY LABORATORY 9

Modeling Tools

• ReEDS: Central-planning optimization model of U.S. Electricity Sectoro 134 Balancing Areas

o Explicit consideration of RE integration issues

o Represents transmission

• dGen: Consumer adoption model of distributed PVo Solar PV

o County-level resolution

o Incorporates state and local incentives and rate structures

o Residential and C&I included

Electricity Sector Trends and Outlook

The Mid-case Scenario

NATIONAL RENEWABLE ENERGY LABORATORY 12

Most new energy growth is met by wind and solar.

No dramatic changes until post-2040.

Mid-case Power Sector Evolution

13

The U.S. power system evolves to a system primarily powered by natural gas and renewable energy

Upper figure: 2016Renewable Energy Generation: 15%

Natural Gas Generation: 34%

Lower figure: 2050Renewable Energy Generation: 45%

Natural Gas Generation: 30%

Theme #1: A promising future for natural gas and renewable energy

NATIONAL RENEWABLE ENERGY LABORATORY 15

Historical net additions are defined as the differences in installed net summer capacity at the end of the year shown from the end of the prior year. Planned net additions are defined as planned capacity minus planned retirements. Planned additions differ from forecasted additions and can understate the amount of renewable capacity under consideration, as renewable technologies can have short siting and construction periods.Data sources: EIA Electric Power Annual and Electric Power Monthly

Recent historical and planned capacity additions are predominantly natural gas and renewable energy technologies

-30

-20

-10

0

10

20

30

40

50

Net

An

nu

al

Ch

an

ge in

C

ap

acit

y (

GW

)

RE

NG

Coal

Nuclear

Other

Historical net additions Planned net additions

NATIONAL RENEWABLE ENERGY LABORATORY 16

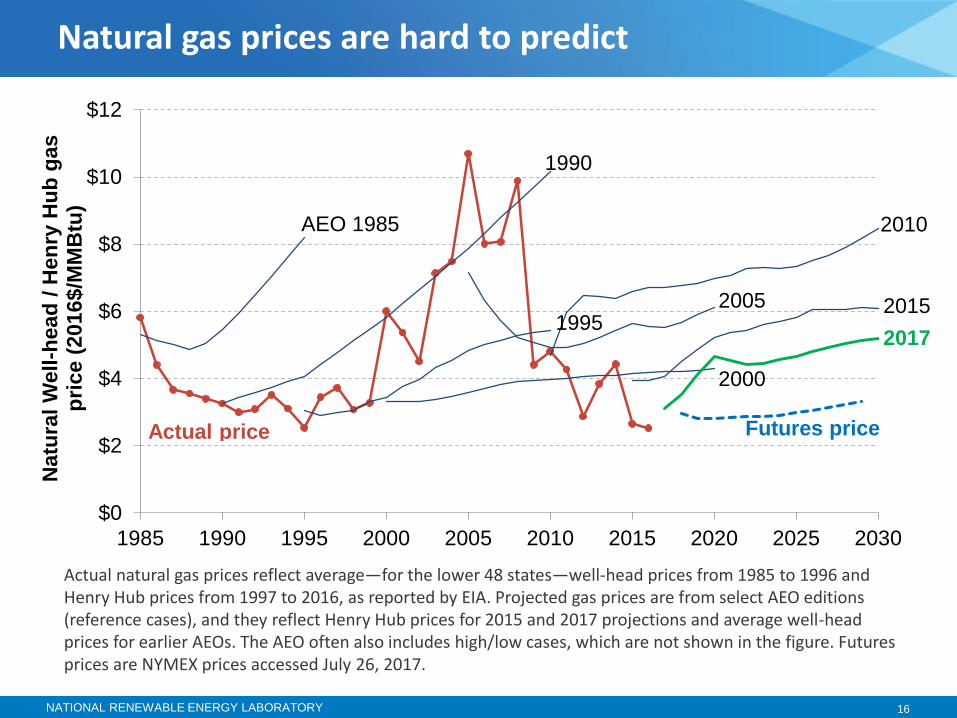

Actual natural gas prices reflect average—for the lower 48 states—well-head prices from 1985 to 1996 and Henry Hub prices from 1997 to 2016, as reported by EIA. Projected gas prices are from select AEO editions (reference cases), and they reflect Henry Hub prices for 2015 and 2017 projections and average well-head prices for earlier AEOs. The AEO often also includes high/low cases, which are not shown in the figure. Futures prices are NYMEX prices accessed July 26, 2017.

Natural gas prices are hard to predict

$0

$2

$4

$6

$8

$10

$12

1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Natu

ral

Well

-head

/ H

en

ry H

ub

gas

pri

ce (

2016$/M

MB

tu)

AEO 1985

1990

1995

2000

Actual price

2005

2010

2015

2017

Futures price

NATIONAL RENEWABLE ENERGY LABORATORY 17

The figure is a modified version of one from Margolis, Feldman, and Boff (2017).

So are renewable energy costs

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

PV

Mo

du

le P

rice (

2016$/W

)

Estimates Made in 2008200920102011201220132014201520162017Actual

NATIONAL RENEWABLE ENERGY LABORATORY 18

0

500

1,000

1,500

2,000

2,500

3,000

TW

h

0

500

1,000

1,500

2,000

2,500

3,000

TW

h

Uncertainties in future technology and market conditions drive uncertainties in projected generation across many technologies

0

500

1,000

1,500

2,000

2,500

3,000

TW

h

Sensitivity Range

Mid-case0

500

1,000

1,500

2,000

2,500

3,000

TW

h

Renewable Energy Natural Gas

Coal Nuclear

NATIONAL RENEWABLE ENERGY LABORATORY 19

Interaction of Natural Gas and Renewable Energy

0

500

1,000

1,500

2,000

2,500

3,000

0 1,000 2,000 3,000 4,000

NG

Ge

nera

tio

n (

TW

h)

RE Generation (TWh)

2020 2030 2040 2050

Low RE Cost

High NG Price

Low NG Price

High RE Cost

0

200

400

600

800

1,000

0 1,000 2,000 3,000 4,000N

G C

ap

acit

y (

GW

)RE Generation (TWh)

2020 2030 2040 2050

Although future competition for RE and NG exists, there is also complementary generation and capacity growth

20

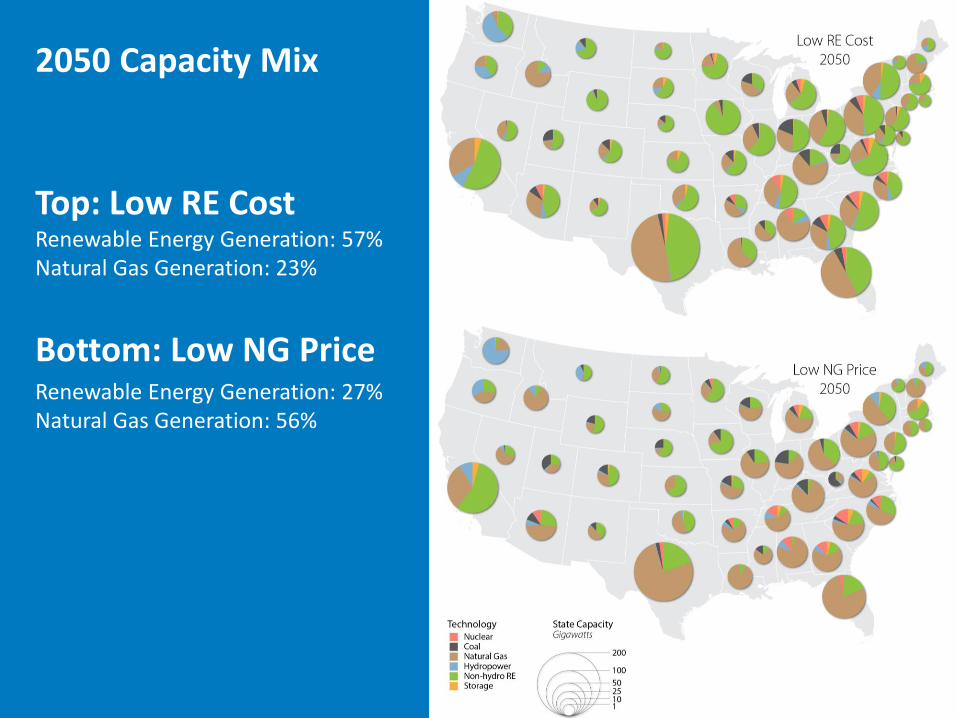

2050 Capacity Mix

Top: Low RE CostRenewable Energy Generation: 57%Natural Gas Generation: 23%

Bottom: Low NG PriceRenewable Energy Generation: 27%Natural Gas Generation: 56%

NATIONAL RENEWABLE ENERGY LABORATORY 21

Power sector emissions and water use are mostly flat in all non-policy scenarios

Emissions and Water

0

0.5

1

1.5

2

2.5

2020 2030 2040 2050

CO

2E

mis

sio

ns

(billio

n m

etr

ic t

on

s)

Sensitivity Range

Mid-case

0

200

400

600

800

1,000

1,200

1,400

1,600

2020 2030 2040 2050

Wa

ter

Co

nsu

mp

tio

n

(billio

n g

allo

ns)

Theme #2: Wind and Solar Competition

NATIONAL RENEWABLE ENERGY LABORATORY 23

Recent growth in RE generation is primarily from wind and from PV

0

100

200

300

400

500

600

7002000

2001

2002

2003

2004

20

05

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

RE

Gen

era

tio

n (

TW

h)

Geothermal, CSP, Bio

Wind

DPV

UPV

Hydropower(three-year rolling average)

6.8%

8.5%

NATIONAL RENEWABLE ENERGY LABORATORY 24

Note that PPAs are market values that reflect the impact of tax credits and other incentives.

Figure from Wiser, Bolinger, and Seel (2017).

Wind and PV PPA prices show noticeable decline and convergence over the past decade

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

PPA Execution Date

Utility-Scale PV

Utility-Scale Wind

Leve

lize

d P

PA

Pri

ce (

20

16

$/M

Wh

)

250 MW

30 MW

99 MW

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

NATIONAL RENEWABLE ENERGY LABORATORY 25

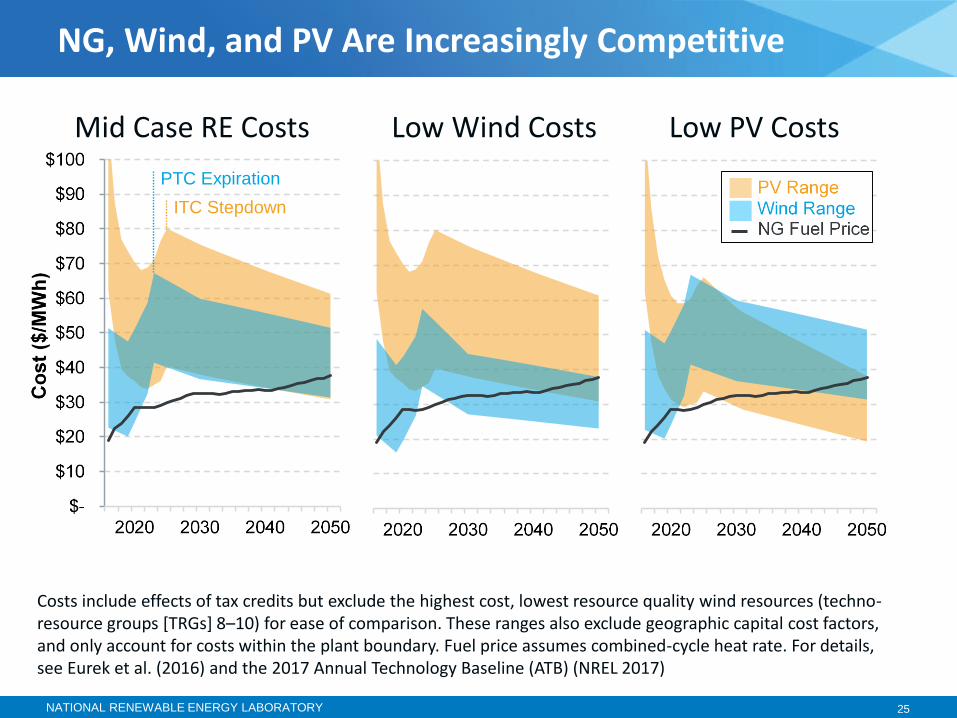

NG, Wind, and PV Are Increasingly Competitive

ITC Stepdown

PTC Expiration

Mid Case RE Costs Low Wind Costs Low PV Costs

Costs include effects of tax credits but exclude the highest cost, lowest resource quality wind resources (techno-resource groups [TRGs] 8–10) for ease of comparison. These ranges also exclude geographic capital cost factors, and only account for costs within the plant boundary. Fuel price assumes combined-cycle heat rate. For details, see Eurek et al. (2016) and the 2017 Annual Technology Baseline (ATB) (NREL 2017)

NATIONAL RENEWABLE ENERGY LABORATORY 26

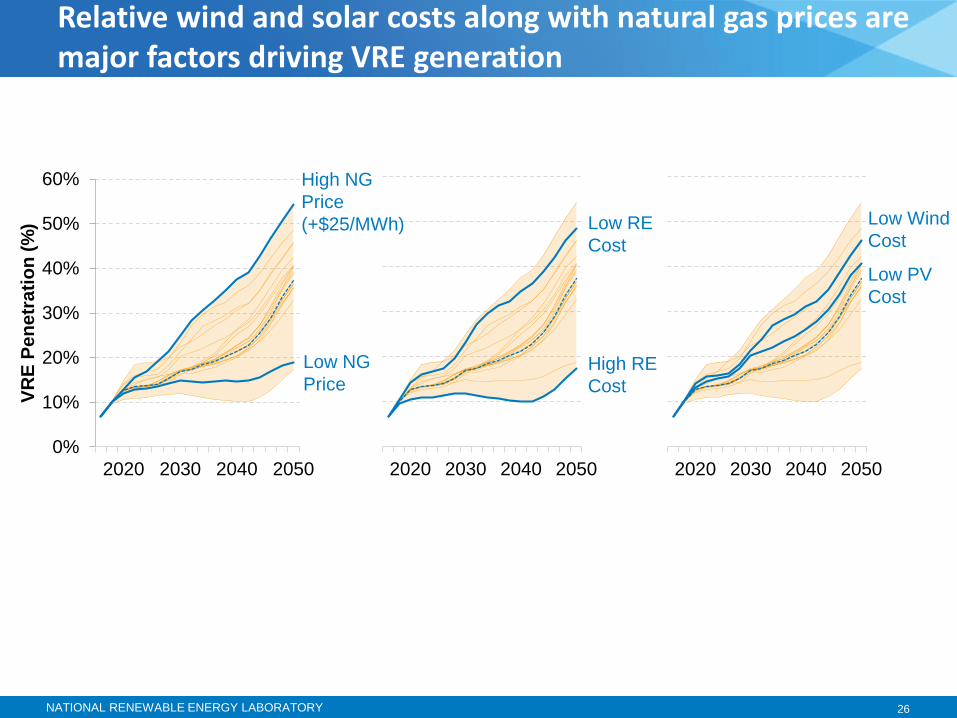

Relative wind and solar costs along with natural gas prices are major factors driving VRE generation

0%

10%

20%

30%

40%

50%

60%

2020 2030 2040 2050

VR

E P

en

etr

ati

on

(%

)

2020 2030 2040 20502020 2030 2040 2050

High NG

Price

(+$25/MWh)

Low NG

Price

Low RE

Cost

High RE

Cost

Low Wind

Cost

Low PV

Cost

NATIONAL RENEWABLE ENERGY LABORATORY 27

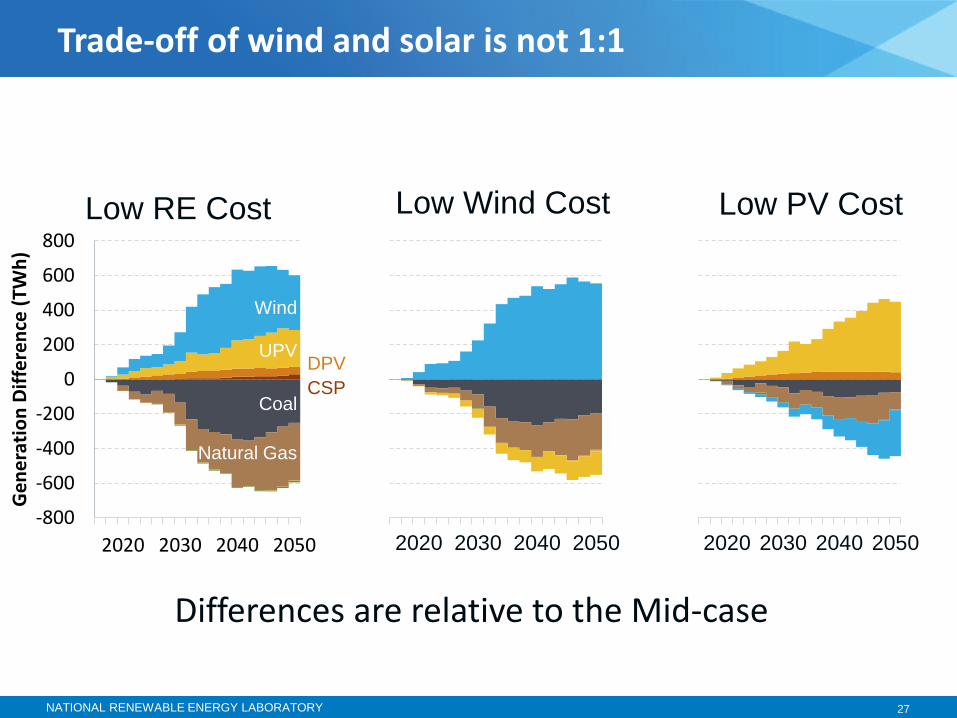

2020 2030 2040 2050

Trade-off of wind and solar is not 1:1

Low RE Cost Low Wind Cost Low PV Cost

-800

-600

-400

-200

0

200

400

600

800

2020 2030 2040 2050

Ge

ne

rati

on

Dif

fere

nce

(TW

h)

Wind

Coal

Natural Gas

UPV

2020 2030 2040 2050

Differences are relative to the Mid-case

DPV

CSP

Theme #3: There is a lot of potential for low-cost battery storage

NATIONAL RENEWABLE ENERGY LABORATORY 29

Battery costs are from Cole, Marcy, et al. (2016) and NG-CT costs are from the 2017 Annual Technology Baseline (NREL 2017).

W) High Battery CostMid-case Battery CostLow Battery CostNG-CT

NATIONAL RENEWABLE ENERGY LABORATORY 30

Cumulative storage capacity over time

0

50

100

150

2002

016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

2044

2046

20

48

2050

Sto

rag

e C

ap

acit

y (

GW

)

Sensitivity Range

Mid-case

Low Battery Cost

Carbon Cap

80% National RPS

High NG Price

NATIONAL RENEWABLE ENERGY LABORATORY 31

Storage vs. VRE penetration

0

50

100

150

200

250

0 0.2 0.4 0.6 0.8

2050 S

tora

ge

Cap

acit

y (

GW

)

2050 VRE Penetration Fraction

Low Battery Cost

Scenario

NATIONAL RENEWABLE ENERGY LABORATORY 32

Low-cost storage enables higher RE penetration

-150

-100

-50

0

50

100

150

200

2020 2030 2040 2050

Gen

era

tio

n (

TW

h)

-150

-100

-50

0

50

100

150

200

2020 2030 2040 2050

Cap

aci

ty (

GW

)

Storage

Solar

Wind

Hydro

Geo/Bio

NG-CT/OGS

NG-CC

Coal

Nuclear

Differences relative to the Mid-case

Theme #4: Uncertainty in nuclear retirements lead to uncertainty in

future capacity and generation needs

NATIONAL RENEWABLE ENERGY LABORATORY 34

Recent and announced nuclear retirements

NATIONAL RENEWABLE ENERGY LABORATORY 35

Nuclear capacity over time across the four retirement scenarios

0

20

40

60

80

100

120

2015 2020 2025 2030 2035 2040 2045 2050

Nu

cle

ar C

apac

ity

(GW

)

80-year

Mid-case

60-year

Early Retire

NATIONAL RENEWABLE ENERGY LABORATORY 36

NG-CC is natural gas combined cycle, NG-CT is natural gas combustion turbine, OGS is oil-gas-steam, and Geo/Bio is geothermal and biopower.

Generation and capacity differences by technology relative to the Mid-case scenario for 2030 and 2050

-400

-300

-200

-100

0

100

200

300

400

2030

2050

2030

2050

2030

2050

Early

Retire

60-year 80-

year

Dif

fere

nce

in

Gen

erati

on

fro

m

Mid

-case

(T

Wh

)

-125

-75

-25

25

75

125

2030

2050

2030

2050

2030

2050

Early

Retire

60-year 80-

year

Dif

fere

nce

in

Cap

aci

ty f

rom

Mid

-case

(G

W)

Storage

Solar

Wind

Hydro

Geo/Bio

NG-

CT/OGSNG-CC

Coal

Nuclear

NATIONAL RENEWABLE ENERGY LABORATORY 37

Impact of nuclear retirements on CO2 emissions

How to Access Scenario Data

NATIONAL RENEWABLE ENERGY LABORATORY 39

Scenario data available online

NATIONAL RENEWABLE ENERGY LABORATORY 40

• Standard Scenarios provides a framework to

o Improve analysis and modeling work

o Provide a perspective on the U.S. electricity sector evolution

o Get access to state-level projections

• Themes from 2017:

o Growth in natural gas and renewables

o Competition between wind and PV

o The large potential for battery storage

o Nuclear lifetimes

Summary

www.nrel.gov

NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable Energy, operated by the Alliance for Sustainable Energy, LLC.