12

Jérôme Contamine, Executive Vice President, Chief Financial Officer London – September 15, 2017 BofA-ML Global Healthcare Conference

| Date post: | 21-Jan-2018 |

| Category: |

Health & Medicine |

| Upload: | sanofi |

| View: | 239 times |

| Download: | 1 times |

Jérôme Contamine, Executive Vice President, Chief Financial Officer

London – September 15, 2017

BofA-ML Global Healthcare Conference

2

Forward Looking Statements

This presentation contains forward-looking statements as defined in the Private Securities Litigation Reform Act of

1995, as amended. Forward-looking statements are statements that are not historical facts. These statements include

projections and estimates and their underlying assumptions, statements regarding plans, objectives, intentions and

expectations with respect to future financial results, events, operations, services, product development and potential,

and statements regarding future performance. Forward-looking statements are generally identified by the words

“expects”, “anticipates”, “believes”, “intends”, “estimates”, “plans” and similar expressions. Although Sanofi’s

management believes that the expectations reflected in such forward-looking statements are reasonable, investors are

cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which

are difficult to predict and generally beyond the control of Sanofi, that could cause actual results and developments to

differ materially from those expressed in, or implied or projected by, the forward-looking information and statements.

These risks and uncertainties include among other things, the uncertainties inherent in research and development,

future clinical data and analysis, including post marketing, decisions by regulatory authorities, such as the FDA or the

EMA, regarding whether and when to approve any drug, device or biological application that may be filed for any such

product candidates as well as their decisions regarding labelling and other matters that could affect the availability or

commercial potential of such product candidates, the absence of guarantee that the product candidates if approved will

be commercially successful, the future approval and commercial success of therapeutic alternatives, Sanofi’s ability to

benefit from external growth opportunities and/or obtain regulatory clearances, risks associated with intellectual

property and any related pending or future litigation and the ultimate outcome of such litigation, trends in exchange

rates and prevailing interest rates, volatile economic conditions, the impact of cost containment initiatives and

subsequent changes thereto, the average number of shares outstanding as well as those discussed or identified in the

public filings with the SEC and the AMF made by Sanofi, including those listed under “Risk Factors” and “Cautionary

Statement Regarding Forward-Looking Statements” in Sanofi’s annual report on Form 20-F for the year ended

December 31, 2016. Other than as required by applicable law, Sanofi does not undertake any obligation to update or

revise any forward-looking information or statements.

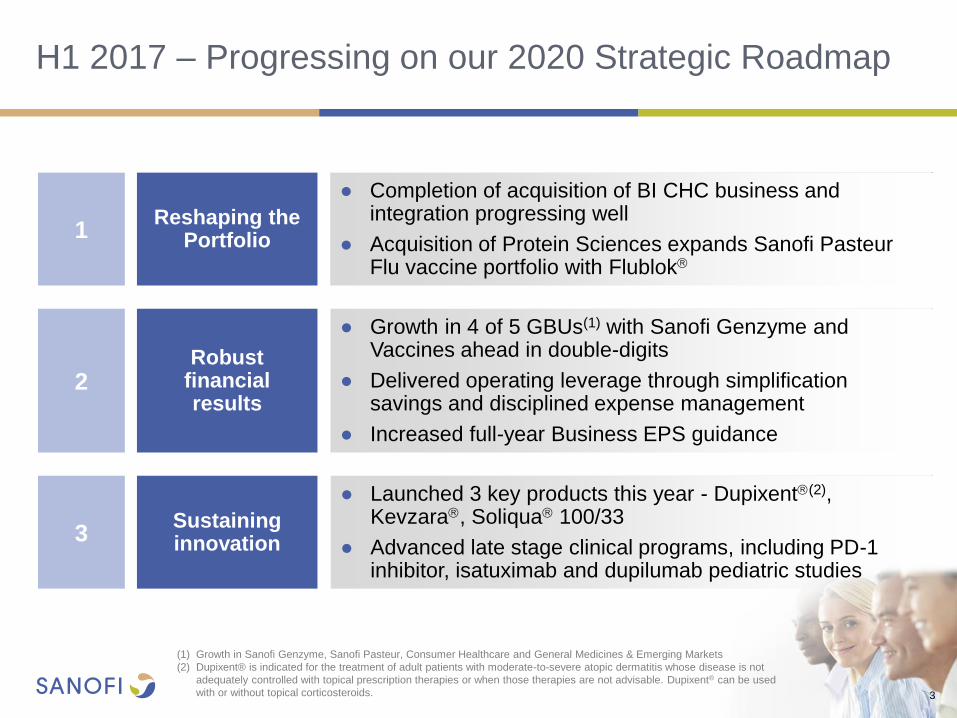

H1 2017 – Progressing on our 2020 Strategic Roadmap

3

1

● Completion of acquisition of BI CHC business and integration progressing well

● Acquisition of Protein Sciences expands Sanofi Pasteur Flu vaccine portfolio with Flublok

Reshaping the Portfolio

● Growth in 4 of 5 GBUs(1) with Sanofi Genzyme and Vaccines ahead in double-digits

● Delivered operating leverage through simplification savings and disciplined expense management

● Increased full-year Business EPS guidance

2 Robust

financial results

3

● Launched 3 key products this year - Dupixent(2), Kevzara, Soliqua 100/33

● Advanced late stage clinical programs, including PD-1 inhibitor, isatuximab and dupilumab pediatric studies

Sustaining innovation

(1) Growth in Sanofi Genzyme, Sanofi Pasteur, Consumer Healthcare and General Medicines & Emerging Markets

(2) Dupixent® is indicated for the treatment of adult patients with moderate-to-severe atopic dermatitis whose disease is not

adequately controlled with topical prescription therapies or when those therapies are not advisable. Dupixent® can be used

with or without topical corticosteroids.

H1 2017 Sales Benefited from Change in Structure and

Simplified Organization Supported Business EPS

4 CER : Constant Exchange Rates

Business EPS

H1 2017

€2.77

H1 2016

€2.64

+2.7% at CER

Company Sales

€15,926m €17,311m

H1 2016 H1 2017

+7.0% at CER

5

Growth

at CER/CS(1)

Diversified Business Model Drives Growth and More than

Offset Diabetes Performance in H1 2017

(1) Growth at CER and Constant Structure on the basis of H1 2016

sales including CHC sales from Boehringer Ingelheim, SPMSD

sales and others

(2) Does not include Emerging Markets sales

(3) On a CER basis, growth was +24.5%

(4) Consumer Healthcare includes sales in Emerging Markets

(5) On a CER basis, growth was +42.6%

(6) Includes Emerging Markets sales for Diabetes &

Cardiovascular and Specialty Care

(7) Emerging Markets: World excluding U.S., Canada, Western &

Eastern Europe (except Eurasia), Japan, South Korea,

Australia, New Zealand and Puerto Rico

(8) Excluding global Consumer Healthcare sales and Vaccines Pictures by Freepik

H1 2017 Sales by Global Business Unit

Company Sales €17,311m

+2.0%

€2,805m

Diabetes & Cardiovascular -11.4%

€2,818m

Sanofi Genzyme (Specialty Care) +14.9%

€1,800m

Sanofi Pasteur (Vaccines) +16.5%

€7,384m

General Medicines & Emerging Markets +0.3% (6,7,8)

(2)

(2)

(4) €2,504m

Consumer Healthcare +2.4% (5)

(3)

6

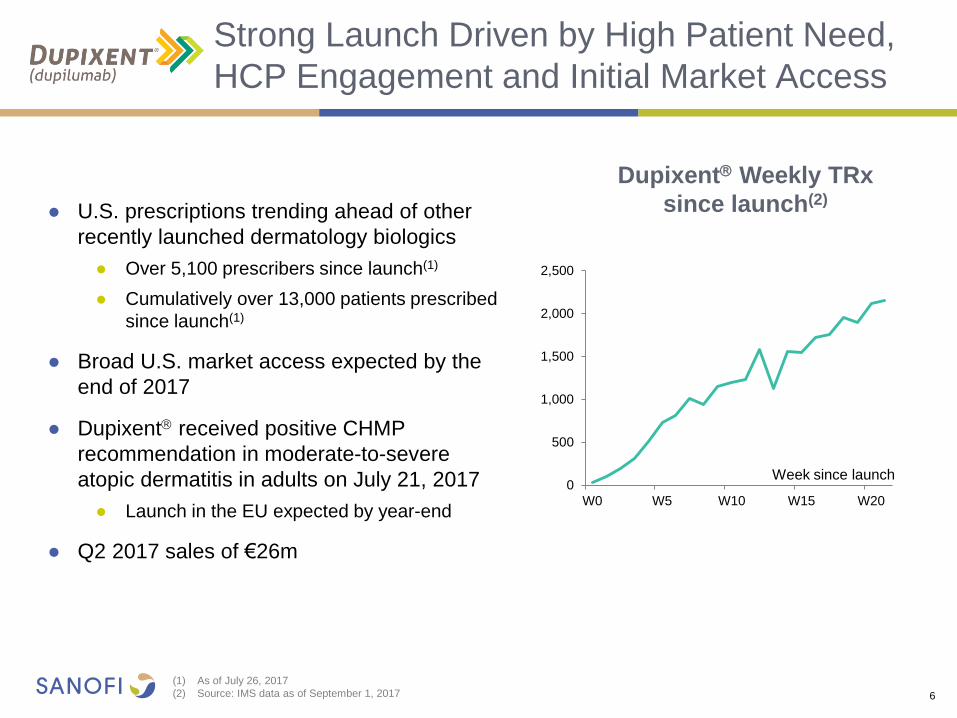

● U.S. prescriptions trending ahead of other

recently launched dermatology biologics

● Over 5,100 prescribers since launch(1)

● Cumulatively over 13,000 patients prescribed

since launch(1)

● Broad U.S. market access expected by the

end of 2017

● Dupixent received positive CHMP

recommendation in moderate-to-severe

atopic dermatitis in adults on July 21, 2017

● Launch in the EU expected by year-end

● Q2 2017 sales of €26m

(1) As of July 26, 2017

(2) Source: IMS data as of September 1, 2017

Strong Launch Driven by High Patient Need,

HCP Engagement and Initial Market Access

Dupixent Weekly TRx

since launch(2)

0

500

1,000

1,500

2,000

2,500

W0 W5 W10 W15 W20

Week since launch

7

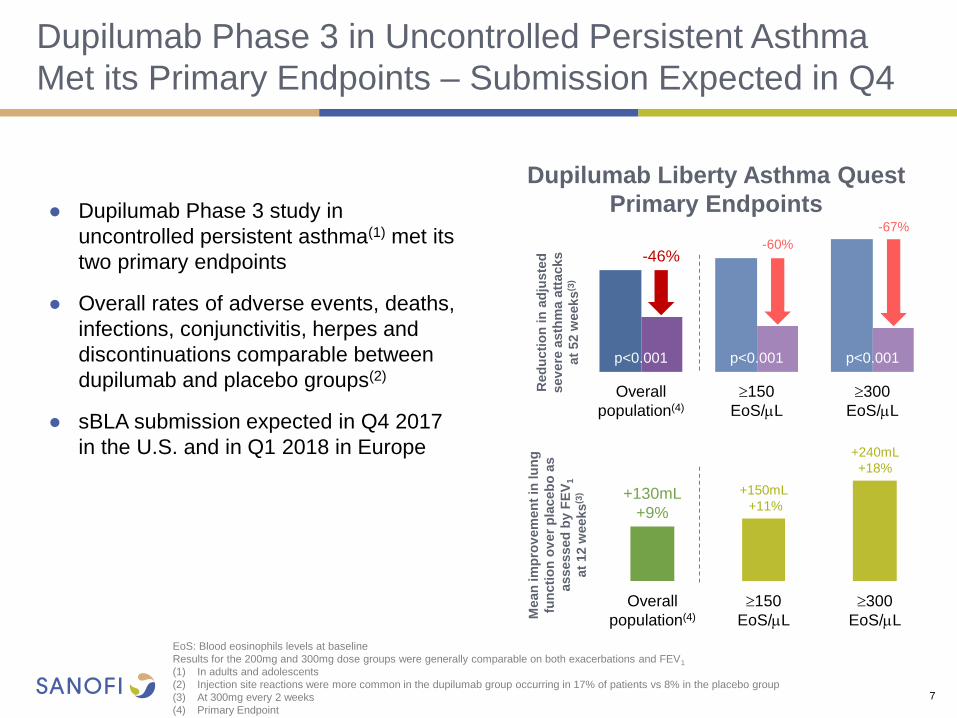

● Dupilumab Phase 3 study in

uncontrolled persistent asthma(1) met its

two primary endpoints

● Overall rates of adverse events, deaths,

infections, conjunctivitis, herpes and

discontinuations comparable between

dupilumab and placebo groups(2)

● sBLA submission expected in Q4 2017

in the U.S. and in Q1 2018 in Europe

EoS: Blood eosinophils levels at baseline

Results for the 200mg and 300mg dose groups were generally comparable on both exacerbations and FEV1

(1) In adults and adolescents

(2) Injection site reactions were more common in the dupilumab group occurring in 17% of patients vs 8% in the placebo group

(3) At 300mg every 2 weeks

(4) Primary Endpoint

Dupilumab Liberty Asthma Quest

Primary Endpoints

Dupilumab Phase 3 in Uncontrolled Persistent Asthma

Met its Primary Endpoints – Submission Expected in Q4

p<0.001

p<0.001 p<0.001

Red

ucti

on

in

ad

jus

ted

sev

ere

asth

ma a

ttacks

at

52 w

eeks

(3)

Overall

population(4)

150

EoS/L

300

EoS/L Mean

im

pro

vem

en

t in

lu

ng

fun

cti

on

ov

er

pla

ceb

o a

s

assessed

by F

EV

1

at

12 w

eeks

(3)

150

EoS/L

Overall

population(4)

300

EoS/L

p<0.001 p<0.001 p<0.001

-46% -60%

-67%

+130mL

+9%

+150mL

+11%

+240mL

+18%

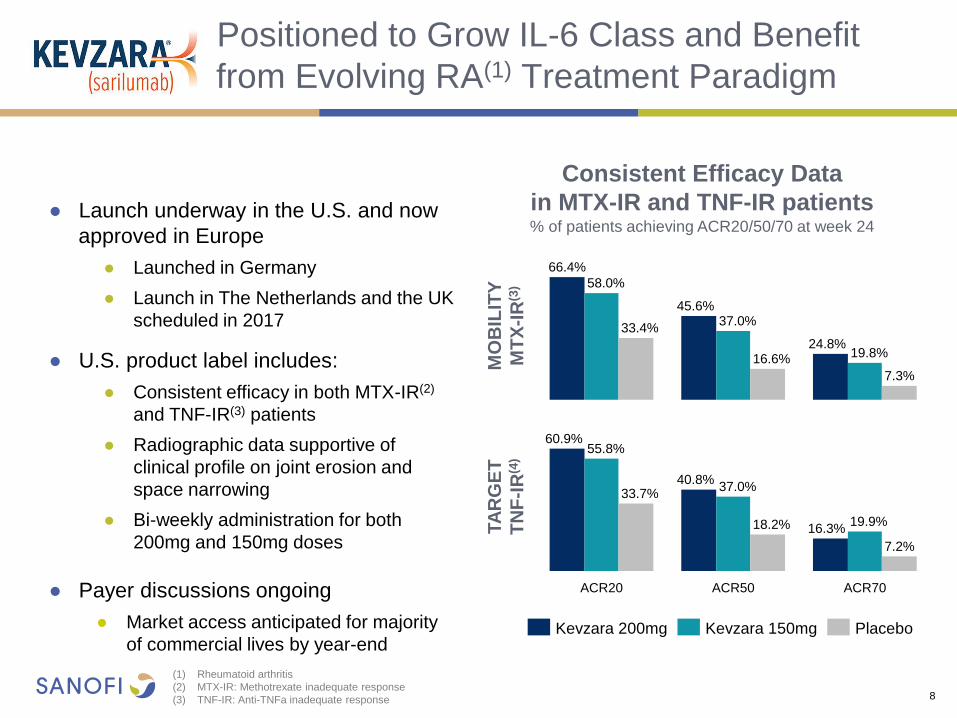

Positioned to Grow IL-6 Class and Benefit

from Evolving RA(1) Treatment Paradigm

8

● Launch underway in the U.S. and now

approved in Europe

● Launched in Germany

● Launch in The Netherlands and the UK

scheduled in 2017

● U.S. product label includes:

● Consistent efficacy in both MTX-IR(2)

and TNF-IR(3) patients

● Radiographic data supportive of

clinical profile on joint erosion and

space narrowing

● Bi-weekly administration for both

200mg and 150mg doses

● Payer discussions ongoing

● Market access anticipated for majority

of commercial lives by year-end

(1) Rheumatoid arthritis

(2) MTX-IR: Methotrexate inadequate response

(3) TNF-IR: Anti-TNFa inadequate response

Consistent Efficacy Data

in MTX-IR and TNF-IR patients % of patients achieving ACR20/50/70 at week 24

19.8% 24.8%

37.0% 45.6%

58.0%

66.4%

33.4%

16.6%

7.3%

Kevzara 150mg Kevzara 200mg Placebo

18.2%

ACR70

19.9% 16.3%

ACR50

37.0% 40.8%

ACR20

55.8% 60.9%

33.7%

7.2%

MO

BIL

ITY

MT

X-I

R(3

)

TA

RG

ET

TN

F-I

R(4

)

9

CHC Sales Grew in H1 2017 and BI Integration On Track

(1) Growth at CER and Constant Structure on the basis of H1 2016 sales including CHC sales from Boehringer Ingelheim and Others

(2) 42 countries have exited transitional distribution service agreement by early July 2017. Remaining 13 countries expected to exit transitional

distribution service agreement by April 2018.

● CHC sales up +2.4% at CER/CS(1)

● Europe was up +1.6% due to strong and

early cough and cold season

● U.S. sales increased +2.5%

● Emerging Markets up +3.0% with all core

categories growing

● BI integration progressing according to plan

● Over 95% of BI CHC sales will be recognized

by end of 2017(2)

9

H1 2017 Global CHC Sales at CER/CS

€669m +6.7%

€621m +4.1%

€468m -3.2%

€334m -1.2%

€412m +2.8%

Allergy, Cough & Cold

Pain

Other

Nutritional

Digestive

Accelerated Decline in Diabetes Sales

Partially Mitigated by Toujeo

10

● Diabetes sales declined -9.2% at CER in H1

2017 driven by anticipated U.S. challenges

● U.S. diabetes sales decline (-19% in H1 2017)

expected to accelerate in H2 2017

● Toujeo sales reached €402m (+60% at CER)

● Achieved 13% basal market share in Europe(1)

● Continued share gain in the U.S. Basal market(2)

● Reached 15.5% market share in Japan

● Soliqua 100/33 U.S. payer coverage

improving

● Access secured for 65% of commercial lives

● Comprehensive 2018 U.S. payer coverage

update to be provided with Q3 2017 results

(1) Based on latest available data in each country

(2) 7.9% based on IMS data as of July 14, 2017

(3) In other countries where Toujeo is launched, based on latest available monthly data

Toujeo Market Share(1) Top EU Countries, Japan, the U.S. and Other

0%

5%

10%

15%

20%

W0 W20 W40 W60 W80 W100

Germany Italy Spain

UK USA Japan

France Other(3)

Week since launch

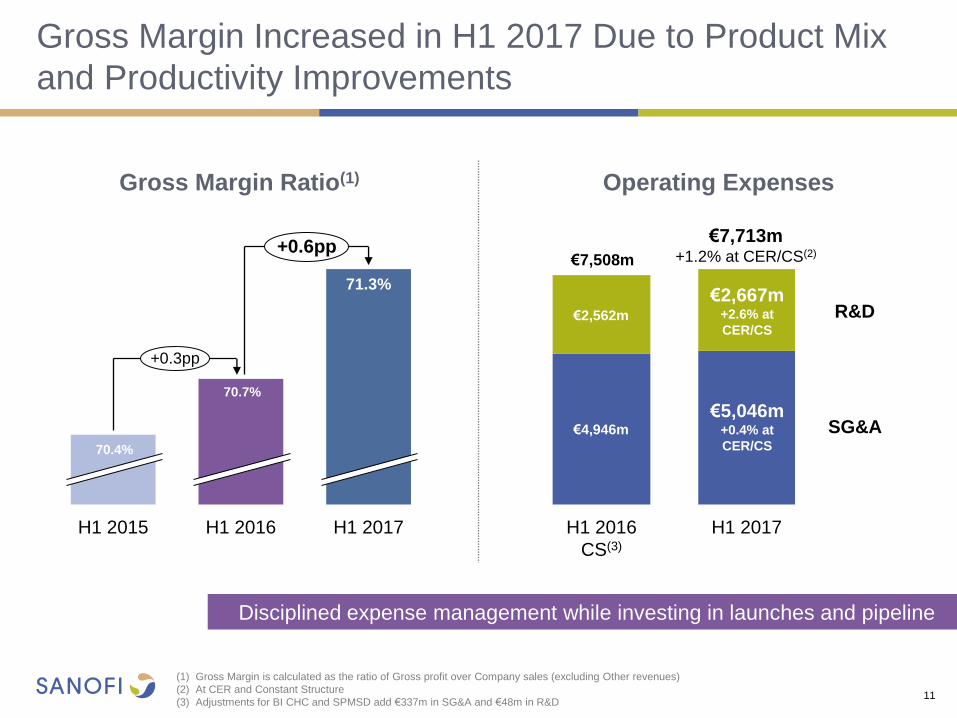

Gross Margin Increased in H1 2017 Due to Product Mix

and Productivity Improvements

11

(1) Gross Margin is calculated as the ratio of Gross profit over Company sales (excluding Other revenues)

(2) At CER and Constant Structure

(3) Adjustments for BI CHC and SPMSD add €337m in SG&A and €48m in R&D

Gross Margin Ratio(1)

SG&A

R&D

H1 2017 H1 2016

CS(3)

€2,667m +2.6% at

CER/CS

€5,046m +0.4% at

CER/CS

€7,713m +1.2% at CER/CS(2)

€7,508m

€2,562m

€4,946m

Disciplined expense management while investing in launches and pipeline

71.7%

+0.6pp

+0.3pp

H1 2017 H1 2016 H1 2015

Operating Expenses

71.3%

70.7%

70.4%

12

(1) Compared to FY2016 and barring major unforeseen adverse events

(2) FY 2016 Business EPS of €5.68

(3) Difference between variation on a reported basis and variation at CER

Raising Business EPS Guidance at CER

for H1 2017 Performance

Business EPS

+1%(3)

based on June 2017 average exchange rates

Broadly Stable at CER(1,2)

FY 2017

FX impact on Business EPS