Page 1

2018 Malaysian Budget

Highlights & GST Updates

Moderator: Dr Veerinderjeet Singh

Panel Speakers:

• Datuk Noor Azian Abdul Hamid

• Dato’ Sri Subromaniam Tholasy

• Mr. MA Sivanesan

• Mr Saravana Kumar

Page 2

Backdrop to the 2018 Budget

International

geopolitical uncertainty

Dependence on

unskilled foreign labour

Low innovation and

skills development

Stabilising global

crude oil prices

Slow pace of technology

adoption & automation

Fiscal discipline

Sovereign downgrade

and drop in rankingsCulture that resists change

and performance development

Page 3

StrategiesPrimarily involving:

Invigorating investment

Developing the future generation

Prioritising the wellbeing of the People

Driving inclusive development

Fortifying the 4IR and digital economy

Enhancing efficiency and delivery of GLCs and public service

Basically consistent with previous Budgets

Budget Theme:

Inclusive economy

Wellbeing of the People

Towards National Transformation 2050

Page 4

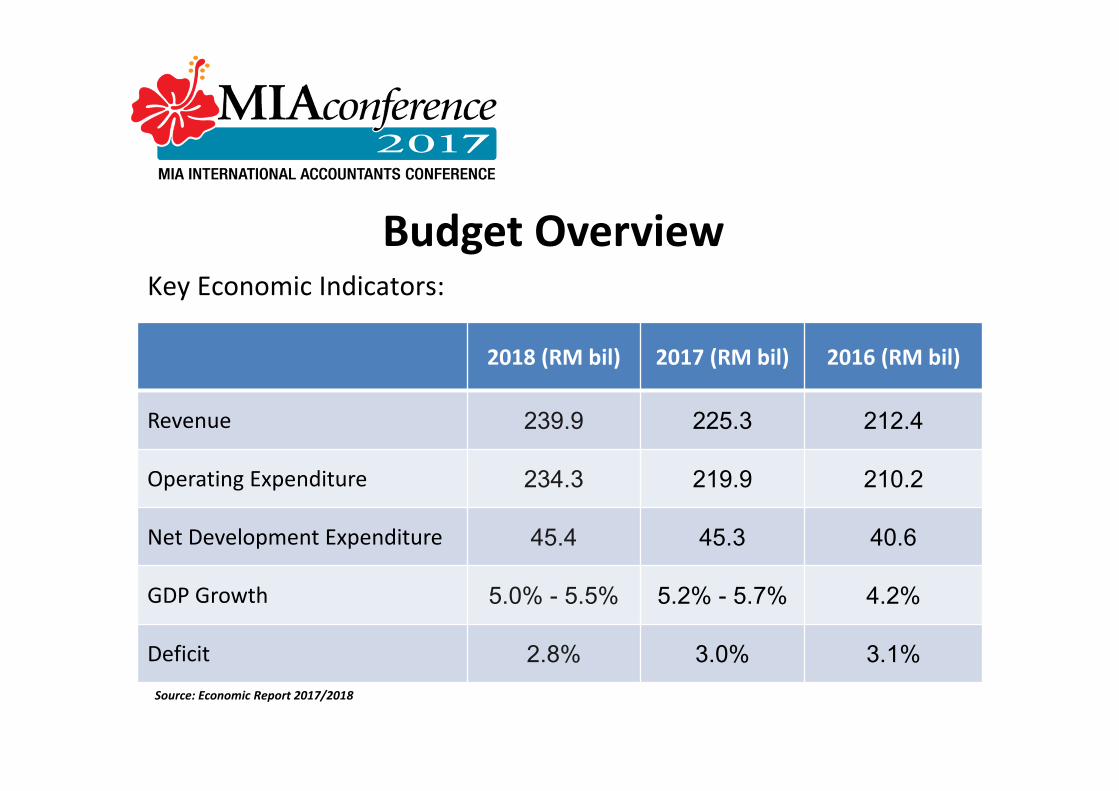

Budget OverviewKey Economic Indicators:

2018 (RM bil) 2017 (RM bil) 2016 (RM bil)

Revenue 239.9 225.3 212.4

Operating Expenditure 234.3 219.9 210.2

Net Development Expenditure 45.4 45.3 40.6

GDP Growth 5.0% - 5.5% 5.2% - 5.7% 4.2%

Deficit 2.8% 3.0% 3.1%

Source: Economic Report 2017/2018

Page 5

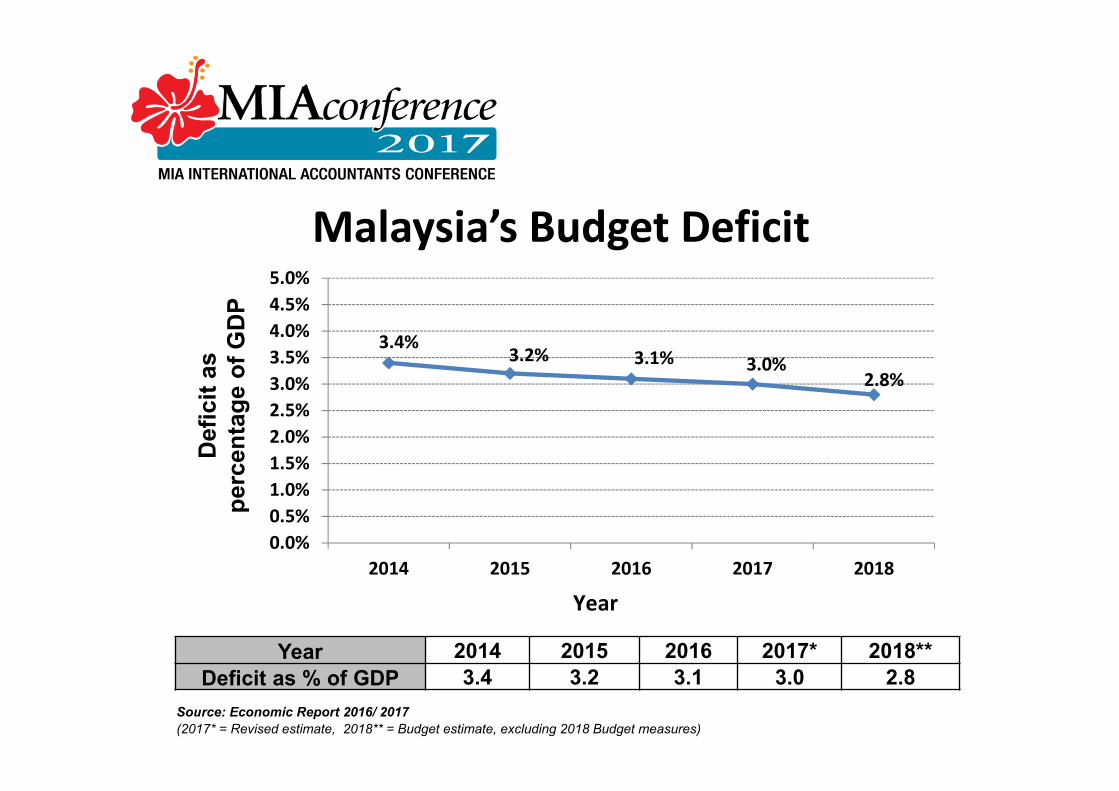

Malaysia’s Budget Deficit

Year 2014 2015 2016 2017* 2018**

Deficit as % of GDP 3.4 3.2 3.1 3.0 2.8

Source: Economic Report 2016/ 2017

(2017* = Revised estimate, 2018** = Budget estimate, excluding 2018 Budget measures)

3.4%3.2% 3.1% 3.0%

2.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2014 2015 2016 2017 2018

Defi

cit

as

perc

en

tag

e o

f G

DP

Year

Page 6

The 2018 Federal Government Budget

Borrowings and

Use of

Government's

Assets

14.4%

Income Taxes

42.6%Non-Tax

Revenue

15.0%

Indirect Taxes

22.8%

Other Direct Taxes

3.0%Where it comes from

RM280.251

million

1 Includes revenue, borrowings and use of Government’s assets.

Source: Ministry of Finance, Malaysia

Page 7

The 2018 Federal Government Budget

Emoluments

28.2%

Debt Service

Charges

11.0%

General

Administration

1.1%

Subsidies and

social assistance

9.5%

Other

Expenditure

11.2%

Economic

Services

9.2%

Social Services

4.3%

Security

1.8%

Supplies and

Services

12.0%

Retirement

charges

8.8%

Grants and

Transfer to State

Governments

2.9%

Where it goes

Source: Ministry of Finance, Malaysia

RM280.251

million

1 Excludes contingency reserves.

Page 8

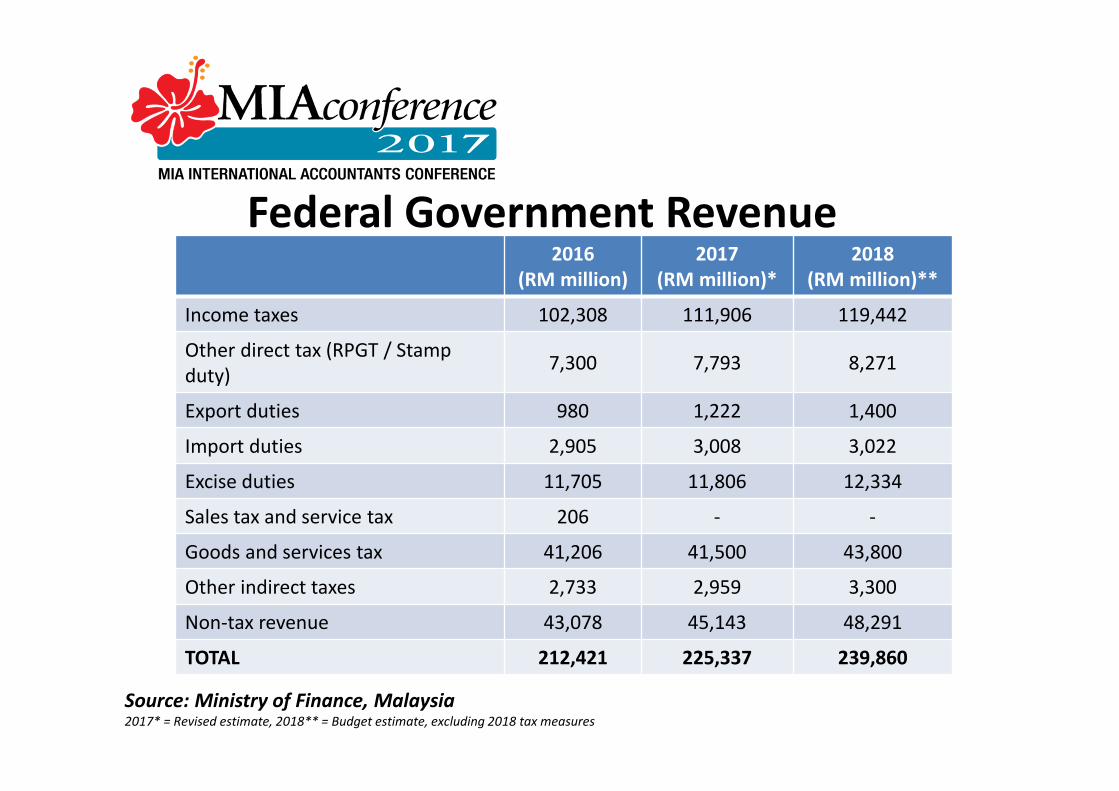

Federal Government Revenue2016

(RM million)

2017

(RM million)*

2018

(RM million)**

Income taxes 102,308 111,906 119,442

Other direct tax (RPGT / Stamp

duty)7,300 7,793 8,271

Export duties 980 1,222 1,400

Import duties 2,905 3,008 3,022

Excise duties 11,705 11,806 12,334

Sales tax and service tax 206 - -

Goods and services tax 41,206 41,500 43,800

Other indirect taxes 2,733 2,959 3,300

Non-tax revenue 43,078 45,143 48,291

TOTAL 212,421 225,337 239,860

Source: Ministry of Finance, Malaysia2017* = Revised estimate, 2018** = Budget estimate, excluding 2018 tax measures

Page 9

Comparison of Corporate Tax Rate

– ASEAN countries

1718.5

20 20 20

24 24 25 25

30

0

5

10

15

20

25

30

35

Co

rpo

rate

Ta

x R

ate

(G

en

era

l)

(%)

ASEAN countries

Page 10

Comparison of Top Corporate Tax Rates

1718.5

20 20 20

24 24 25 25

30

25

30

20

25 25

3028

35

0

5

10

15

20

25

30

35

40

To

p C

orp

ora

te T

ax R

ate

(%

)

Page 11

Comparison of Top Personal Income

Tax Rates

0

2022

24 2528 30

32 3335.5 35 35

39.6

45 45 4548

52

0

10

20

30

40

50

60

To

p P

ers

on

al

Inc

om

e T

ax

Ra

te

(%)

Page 12

2018 Budget Outlook

01Fiscal thrust

Reliance on direct tax revenueNo reduction in corporate taxesReduction in personal taxes

08Encourage growth in

manufacturing sector

Enhancing CA on automation equipment

02Increase disposable

incomeReduction of tax rate for middle income groupContinuation of BRIM handout

05Health

tourismTax exemption on export of health services

06Implementing of

Malaysia’s Digital Policy

CA on development of customisedsoftware (consultation fee, licensing fee, etc.)

04Empowering women who

return to workTax exemption on employment income

07Transfer

Pricing

Guidelines

updated in

stages in line

with BEPS

03Stimulate venture capital activities

Various tax benefits available

Page 13

2018 Budget OutlookFiscal discipline

Reliance on GST but total revenue to increase by 6.4% over

2017.

Targeted growth 5 – 5.5% for 2018 despite economic

uncertainty and subdued growth across the global economy

Domestic demand and private investment are the key drivers

for 2017/2018

People centric Budget—certainly an election budget!

Pro-business strategies – focus on SMEs, etc

No new tax incentives

Personal tax rate reduction of 2% aimed at the M40 group but

all benefit

Page 14

2018 Budget Outlook (cont’d)

Digital economy – only the DFTZ mentioned….

Compliance burden will be increased for all businesses with more

tax audits

Rumours on estate duty/inheritance tax,

Personal tax reliefs – no further consolidation or increases

Reiteration of Government’s commitment to OECD tax initiatives

such as the Base Erosion & Profit Shifting project

Usual allocation of funds for various initiatives – effectiveness in

managing the process?

Nothing substantive given the constraints

Page 15

Challenges / Concerns

High Income

Nation by

2020 is

unlikely

Global

Competition

for FDI

Efficiency in

Tax CollectionMore tax audits

Oil Price

VolatilityImpact revenue

Inadequate

Governance

of Funds

Global

Economic

OutlookStill face downgrade

risks

Balanced

Budget by 2020

is unlikelyChallenge in

reducing fiscal deficit

Earnings

Stripping

Rule

Inadequate

Governance

of Funds

Review of the

Incentives

Regime neededSimplicity, certainty

& transparency

Holistic Review

of the Tax

System is

neededHigh income

/developed nation

status