2020 NORTH AMERICAN INDUSTRIAL OUTLOOK WEBCAST Rebecca Rockey Global Head of Forecasting David Bitner Americas Head of Capital Markets Research Carolyn Salzer Americas Head of Logistics & Industrial Research Tray Anderson Logistics & Industrial Services Lead, Americas

Transcript

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 1

2020 NORTH AMERICAN INDUSTRIAL OUTLOOK

WEBCAST

Rebecca RockeyGlobal Head of Forecasting

David BitnerAmericas Head of Capital Markets Research

Carolyn SalzerAmericas Head of Logistics & Industrial Research

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 9

NET ABSORPTION/ASKING RENT

4Q TRAILING AVERAGE

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

(200,000,000)

(100,000,000)

-

100,000,000

200,000,000

300,000,000

400,000,000

Net Absorption, MSF Weighted Asking Rent, $ PSF

Forecast

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 10

459.9 573.4ABSORPTION (MSF) DELIVERIES (MSF)

5.2% $6.95VACANCY (%) RENTS (PSF)

North American Industrial 2020-2021 Outlook

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 11

EconomicOutlook

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 12

THEME #1: GROWTH DECELERATING

Note: *In local currency units.Source: U.S. Bureau of Economic Analysis, Statistics Canada, Instituto Nacional de Estadística Geografía e Informática, Moody’s Analytics, Oxford Economics, International Monetary Fund, Cushman & Wakefield Research

2.9%

3.0%

3.1%

3.2%

3.3%

3.4%

3.5%

3.6%

3.7%

3.8%

3.9%

2010-2018Average

2018 2019 2020

Global Real GDP Growth

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2009Q3-2019Q3 2018 2019 2020F

Real GDP Growth*Canada Mexico U.S.

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 13

THEME #2: PRODUCTION ECONOMY SOFT

Note: *Canada does not have an ISM-equivalent although alternative PMI indices are available for the country (using different methodologies).Source: Oxford Econoomics, Statistics Canada, Board of Governors of the Federal Reserve, Instituto Nacional de Estadística Geografía e Informática,Cushman & Wakefield Research

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

F

Manufacturing JobsCanada Mexico U.S.

-10

-5

0

5

10

15

20

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Output is FallingCanadian Industrial Production Mexican Industrial ProductionU.S. Industrial Production Cass Shipments Index (3-mma)

-34k jobs-333k jobs-22k jobs

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 14

THEME #3: TRADE UNCERTAINTY TO PERSIST

Source: U.S. Department of Treasury, U.S. Congressional Budget Office, Moody’s Analytics, U.S. Bureau of Economic Analysis, Statistics Canada, Instituto Nacional de Estadística Geografía e Informática, PolicyUncertainty.com, Cushman & Wakefield Research

$0

$20

$40

$60

$80

$100

$120

$140

Corporate Tax CutSavings (TCJA)

Individual IncomeTax Savings (TJCA)

Cost of Tariffs

Billio

ns

Tariffs Offsetting Other Tailwinds

2018 2019-40

-30

-20

-10

0

10

20

30

40

50

60

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2018

2019

Business Confidence is DownGlobal Business Confidence North American Business Confidence

U.S.-China trade war begins

Great Recession

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 15

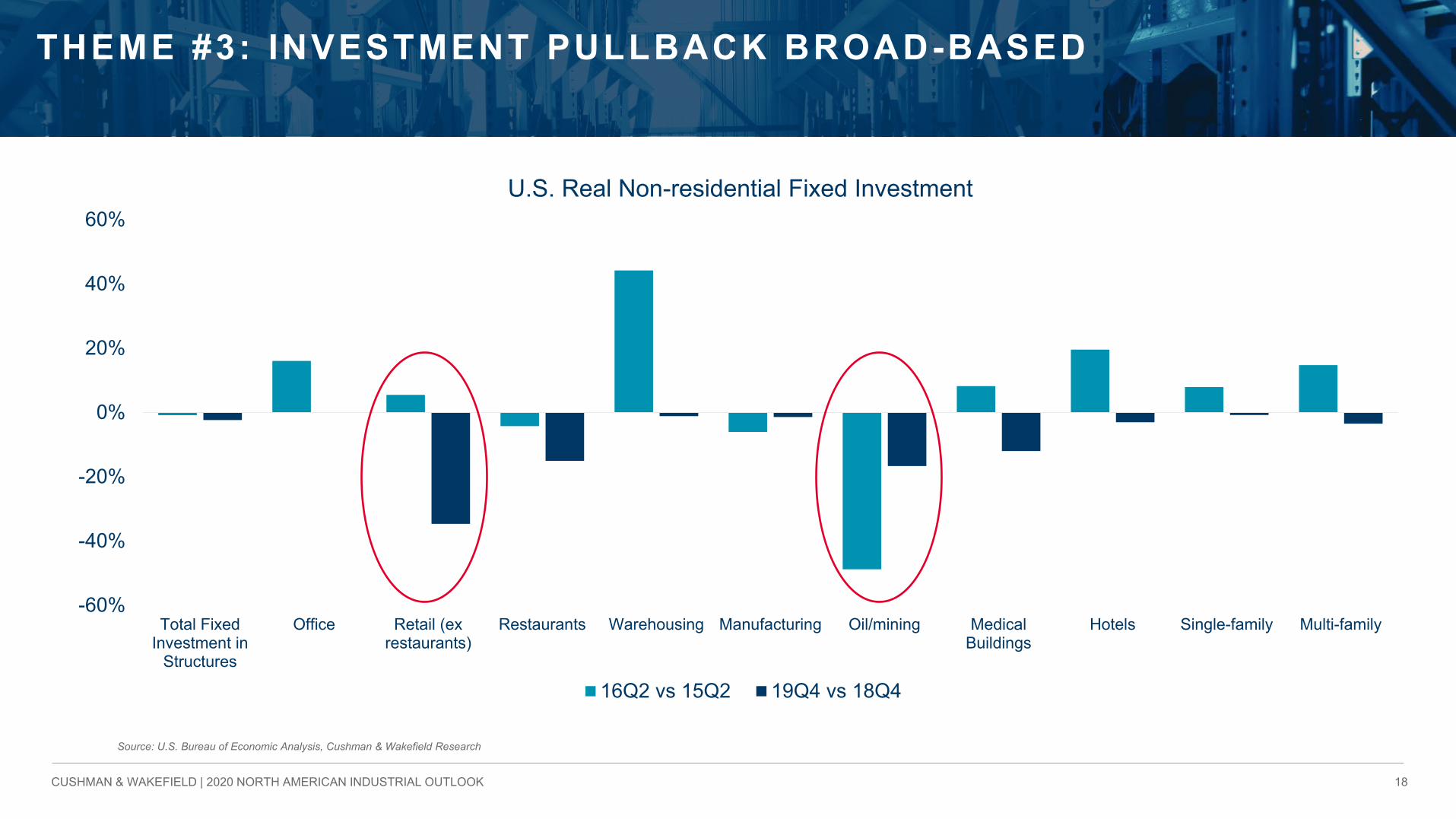

THEME #3: INVESTMENT PULLBACK BROAD-BASED

Source: CPB World Trade Monitor, International Monetary Fund, Cushman & Wakefield Research

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Canada Mexico U.S. NAFTA World

Bilateral Gross Trade Flows with China(Jan-Oct Total, Yr/Yr %Change)

2016 2017 2018 2019

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Investment Pulling BackCanada Mexico U.S.

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 16

THEME #3: INVESTMENT PULLBACK BROAD-BASED

Source: U.S. Bureau of Economic Analysis, Cushman & Wakefield Research

CUSHMAN & WAKEFIELD | 2020 NORTH AMERICAN INDUSTRIAL OUTLOOK 20

WITH EXCEPTIONS…

THEME #4: LOW INFLATION, LOW INTEREST RATES

Note: *Core PCE inflation, **Private Consumption Deflator, ***Consumer Price IndexSource: U.S. Bureau of Economic Analysis, Statistics Canada, Cabinet Office of Japan, Statistical Office of the European Communities, Oxford Economics, Federal Reserve Bank of Philadelphia Survey of Professional Forecasters, Cushman & Wakefield Research