146

Annual Report >> 2 05 DenizBank Financial Services Group

Annual Report >>

2 05

DenizBank Financial Services Group

Contents

02 PART I. Introduction02 Consolidated Financial Highlights04 DenizBank Financial Services Group in Brief06 Zorlu Holding

08 PART II. Messages08 Message from the General Manager

12 PART III. Review of Operations in 200512 From the Captain’s Logbook 14 Banking Services15 DenizBank17 Retail Banking Group23 Business Banking Group28 Corporate Banking Group 29 Commercial Banking Group30 Private Banking 31 DenizBank AG32 DenizBank Moscow33 EuroDeniz Off-Shore Bank Limited34 Investment Banking and Brokerage Services35 DenizYat›r›m Securities37 EkspresInvest38 DenizTürev Securities38 Deniz Investment Trust39 Deniz Portfolio Management40 Leasing and Factoring Services41 DenizLeasing42 DenizFactoring44 Information Technology Services45 Intertech46 Cultural Services46 DenizKültür47 Human Resources and Training

48 PART IV. Management and Corporate Governance48 Board of Directors50 Executive Management55 Auditors56 Management Report on Corporate Governance 75 Investor Relations

76 PART V. Risk Management76 Risk Management Center78 Board of Internal Auditors

81 PART VI. Independent Audit Reports, Financial Statements and Notes

133 Directory135 Organizational Chart

01>

DenizBankFinancial Services GroupBanking Services> DenizBank> DenizBank AG (Vienna)> DenizBank Moscow (Moscow)> EuroDeniz Off-Shore Bank (Nicosia)Investment Banking and Brokerage Services> DenizYatırım Securities> EkspresInvest > DenizTürev Securities> Deniz Investment Trust> Deniz Portfolio ManagementLeasing and Factoring Services> DenizLeasing> DenizFactoringInformation Technology Services> IntertechCultural Services> DenizKültür

Consolidated Financial Highlights*

PART I. INTRODUCTION

2005 2004YTL millions YTL millions

Government Securities (TR)** 1,347 1,489Government Securities (US & European)** 79 333Loans, net 6,173 3,214Equity Participations 130 132Fixed Assets, net 145 102Total Assets 11,976 8,072Customer Deposits 6,980 5,109

Time 5,422 4,045Demand 1,558 1,064

Funds Borrowed from Banks 2,591 1,028Shareholders’ Equity 1,091 873Paid-in Capital 316 316L/Cs & L/Gs 3,211 2,496Interest Income 1,028 859Interest Expense (501) (458)Net Interest Income after Provisions 459 316Non-Interest Income 354 290Non-Interest Expense (587) (469)Net Profit 226 137

Number of DenizBank Branches 236 199Number of DFS Group Staff 5,724 4,912Capital Adequacy Ratio 14.7% 17.8%Return on Investment 23.1% 18.6%

* All financial figures included in this annual report (pages 2-79), have been extracted from audited consolidated financial statements issued inaccordance with the Accounting Regulations No. 15 and 17 published by the Banking Regulation and Supervision Agency (BRSA). Independentauditor’s report, consolidated financial statements and notes to consolidated financial statements presented on pages 83-132 of this reporthave been prepared in accordance with International Financial Reporting standards.

** Securities portfolios are evaluated at market prices.

03>

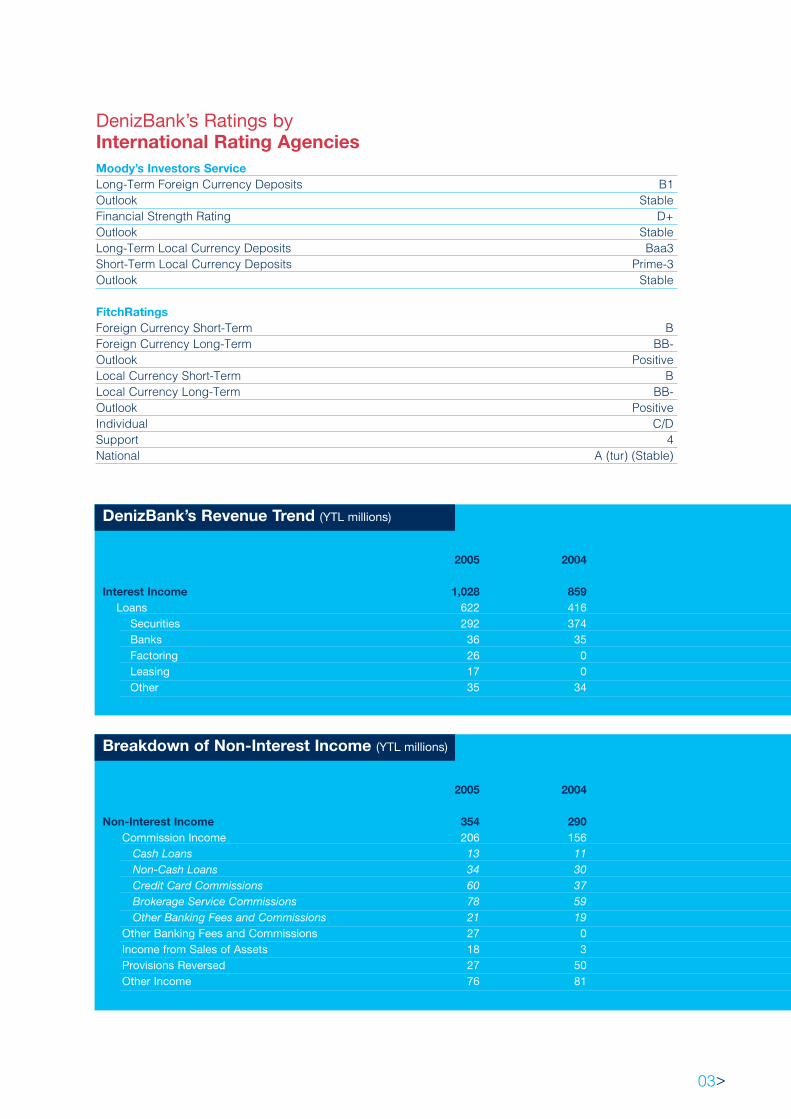

Moody’s Investors ServiceLong-Term Foreign Currency Deposits B1Outlook StableFinancial Strength Rating D+Outlook StableLong-Term Local Currency Deposits Baa3Short-Term Local Currency Deposits Prime-3Outlook Stable

FitchRatingsForeign Currency Short-Term BForeign Currency Long-Term BB-Outlook PositiveLocal Currency Short-Term BLocal Currency Long-Term BB-Outlook PositiveIndividual C/DSupport 4National A (tur) (Stable)

DenizBank’s Ratings by International Rating Agencies

DenizBank’s Revenue Trend (YTL millions)

2005 2004

Interest Income 1,028 859Loans 622 416

Securities 292 374Banks 36 35Factoring 26 0Leasing 17 0Other 35 34

Breakdown of Non-Interest Income (YTL millions)

2005 2004

Non-Interest Income 354 290Commission Income 206 156

Cash Loans 13 11Non-Cash Loans 34 30Credit Card Commissions 60 37Brokerage Service Commissions 78 59Other Banking Fees and Commissions 21 19

Other Banking Fees and Commissions 27 0Income from Sales of Assets 18 3Provisions Reversed 27 50Other Income 76 81

DenizBank Financial Services Group in Brief

The roots of the DenizBank Financial Services Group(DFS Group) date back to 1997 when DenizBank wasprivatized. Originally, DenizBank was established as astate-owned bank in 1938, primarily to help financethe newly emerging Turkish maritime industry.DenizBank soon became one of the foremost namesin the Turkish banking industry thanks to its highstandards and the diversity of the services it provided.In 1992, following a decision by the government toconsolidate a number of state-owned banks,DenizBank merged with Emlakbank. In 1997,DenizBank left this union and was privatized as aseparate entity. Operations commenced again inSeptember after Zorlu Holding acquired DenizBankfrom the Privatization Administration under a bankinglicense early in 1997.

>> FROM A BANK TO A FINANCIAL SERVICESGROUPAfter DenizBank was acquired by Zorlu Holding, arevitalization program was initiated that encompassedthe hiring of new personnel and opening branchesunder the new corporate identity. This was achievedunder the guidelines of a five-year strategic planwhere all targets were successfully met. Expansionwas supported by the acquisition of a number ofbranch offices from SDIF-controlled banks, as well asseveral financial companies including Tariflbank,which joined the Group at the end of 2002.Additionally, DenizBank established and/or acquiredfinancial companies that included banks in Austriaand Russia in addition to factoring, leasing,investment and asset management companies tocomplement its existing banking products andservices.

Encouraged by its strong capitalization and goodfinancial standing, DenizBank was able to takeadvantage of rapid developments in the financialservices industry and moved quickly to the forefront.In 2003, DenizBank Financial Services Group was setup along the lines of a financial supermarket able tooffer a wide range of financial services.

>> ALL CONTEMPORARY FINANCIALSERVICES UNDER A SINGLE UMBRELLAIn addition to DenizBank, the DFS Group has sevendomestic and two international financial subsidiaries,a branch in Bahrain, as well as EuroDeniz Off-ShoreBank Ltd, an off-shore banking subsidiary in theTurkish Republic of Northern Cyprus. Thesesubsidiaries are DenizYat›r›m Securities,EkspresInvest, Deniz Investment Trust, Deniz PortfolioManagement, DenizTürev Securities, DenizLeasing,DenizFactoring, Intertech and DenizKültür on thedomestic side and DenizBank AG and DenizBankMoscow on the international side.

With major operations, financial control andaccounting functions centralized, the DFS Group hassuccessfully transformed DenizBank’s branch officesinto marketing centers thereby optimizing the numberof employees and improving operational efficiency.

PART I. INTRODUCTION

Supported by its strong shareholder base andsuccessful financial performance, the DenizBankFinancial Services Group aims to become one of theleading financial services groups in Turkey.

>> A SERVICE NETWORK REACHING ALLSEGMENTS OF THE SOCIETYThe DFS Group possesses a service network thatreaches all segments of society throughout Turkey. Italso has a solid standing in the Internet environmentproviding the facility to conduct financial transactionsfrom anywhere in the world to both individual andcorporate customers.

With adherence to the highest ethical businesspractices and corporate governance principles, theDFS Group has created sustainable, multi-facetedrelationships with corporate and retail clients focusingon small and medium-size establishments, exporters,project financing and individuals. The DFS Group alsoserves certain niche markets such as ship financing,tourism, agricultural loans, foreign constructionprojects, medical care and education.

The Group continually strives for excellence in its corebusiness areas utilizing a carefully developed branchnetwork equipped with the latest technology andaccompanied by alternative distribution channels.Drawing on the experience and vision of itsmanagement team, the DFS Group provides itscustomers with services that are of the highest quality.

>> EXPANDING BEYOND ITS BORDERSTurkey, now on the verge of becoming an EUmember, is rapidly transforming its institutions tocomply with EU standards and practices. Since thefirst day of its establishment, DenizBank and itsfinancial institutions adopted the best internationalbusiness practices. The DFS Group operates in EUcountries as well through DenizBank AG, itssubsidiary based in Vienna, Austria.

The Group also has a subsidiary in Russia, anotherimportant trading partner for Turkey. It rendersservices to customers engaged in commerce in theregion and is able to meet a variety of their financialrequirements.

Supported by its strong shareholder base andsuccessful financial performance, the DFS Groupaims to become one of the leading financial servicesgroups in Turkey. It plans to expand beyond Turkey’sborders into the EU and Russia through itssubsidiaries.

05>

ZorluHolding

Zorlu Holding, established as a small-scale producerof textiles in the early 1950s, is now one of the largestand most extensive industrial conglomerates inTurkey. With a total of 65 companies, Zorlu Holdinghas 15 large-scale industrial facilities operating in theinternational arena and three power plants providingemployment for 30,000 people. In 2005, Zorlu Holdingcompanies achieved a total turnover of US$ 4.3 billionand a foreign sales of US$ 2.5 billion.

Currently, In addition to financial services ZorluHolding currently concentrates on three majorbusiness areas:

>> HOME TEXTILES AND POLYESTER YARNOperations in the home textiles sector havedeveloped rapidly prompting Zorlu Holding to enterinternational markets. Currently, the Holding has atotal of ten textile plants, located in Turkey, France,South Africa, Iran and Turkmenistan.

>> ELECTRONICS, CONSUMER DURABLESAND INFORMATION TECHNOLOGYVestel Electronics, a publicly listed company, is ZorluHolding’s flagship in the Electronics, ConsumerDurables and IT Group. This group is comprised of19 companies: nine domestic and ten overseas.

>> ENERGY PRODUCTIONZorlu Energy currently serves 300 industrial facilitiesthroughout Turkey via the operation of four powerplants, with an installed capacity of 387 MW. TheCompany has also formed partnerships with domesticfirms to establish power plants with 1,140 MW powercapacity in Russia and Israel; the preliminary work forthis project has already been initiated. Zorlu O&M,another energy sector-related company within ZorluHolding was established in 2000 to provideoperational and maintenance services to both ZorluEnergy and non-Zorlu Holding companies. Other ZorluHolding companies operating in the energy sector areZorlu Industrial and Power Plants, Zorlu Petrogas,Amity Oil, Zorlu Electric, Zorlu Natural Gas, TurkishThrace Natural Gas Distribution Company andGaziantep Natural Gas Distribution Company.

PART I. INTRODUCTION

With a total of 65 companies, Zorlu Holding has15 large-scale industrial facilities operating in theinternational arena and three power plants providingemployment for 30,000 people.

07>

Zorlu Holding’s Key Financial and Operational Figures (US$ millions)

2005 2004 2003

Home Textiles GroupTotal assets 1,900 1,850 1,850Net sales 850 850 830Exports* 300 350 255Imports 270 280 135Total foreign trade volume 570 630 390

Electronics, Consumer Durables and IT GroupTotal assets 2,500 2,400 1,250Net sales 3,300 3,200 1,700Exports* 2,500 2,200 1,400Imports 1,550 1,500 1,000Total foreign trade volume 4,050 3,700 2,400

Energy GroupTotal assets 460 380 295Net sales 170 150 110Imports 65 15 16Installed capacity (MW) 387 211 211Power generated (kWh millions) 1,765 1,570 1,404Steam generated (tons thousands) 556 476 462

Zorlu Holding’s Foreign Trade Volume (US$ millions)

2005 2004 2003

Total exports* 2,800 2,550 1,655Total imports 1,885 1,795 1,151Total foreign trade volume 4,685 4,345 2,806

* Includes net sales of the subsidiaries with production facilities outside Turkey.

Message from the General Manager

DenizBank continues to sail successfully with its pre-set route.

Our bank, ranked "eighth among the fastest growingbanks in the world in terms of its equity capital (Tier 1 Capital)" by the internationally respected financemagazine The Banker in its July 2005 issue, hasfurther increased its successful balance sheet andprofitability growth, both of which are over sectoraverages. As a matter of fact, by mid-2005, we hadalready achieved the year end profit of 2004.According to our year-end consolidated financialstatements, total assets increased by 48% and

reached YTL 11,976 million (US$ 8,925 million). Netprofit for the same period increased by 66% andreached YTL 226 million (US$ 169 million).

Our total credits increased by 92% compared to theprevious year. The rate of increase of our businessloans, which we consider a strategic area forDenizBank, is 215%. Corporate and commercialsegment loans grew by 75% and the increase inconsumer credits except for credit cards was 206%.The greatest increase in consumer credits was inhome loans, which grew nine times since thebeginning of the year. There was an increase of 188%in consumer loans since January, thanks to the specialcampaigns that targeted various occupational groups.

DenizBank’s customer deposits increased to YTL6,980 million in 2005, paralleling its expandingnetwork of branches and a growing customer base.There was a total increase of 53% in commercialdeposits as a result of our strategic focus onbusinesses of all sizes.

DenizBank continued with this successfulperformance in the international markets with five-andseven-year securitization loans totaling US$ 300million received in June secured by internationalremittances. Furthermore, through the syndicated loanagreement signed in October, a total credit ofUS$ 650 million was obtained from internationalbanks; US$ 300 million with a term of one year andUS$ 350 million with a term of two years.

PART II. MESSAGES

DenizBank has further increased its successful balancesheet and profitability growth, both of which are overindustrial averages.

As a result of the segmentation work carried out lastyear, we set different goals for each of our customersegments. In order to guarantee successful results foreach segment, we created an identity for eachsegment and attracted the attention of the targetcustomers. We developed new products and servicesfor each segment within the scope of their particularidentity and increased market penetration. Especiallyin the corporate and commercial segment, wefocused on niche markets and added new customersto our portfolio. We provided loans totaling to US$ 150million to over one hundred projects in tourism andUS$ 550 million to 75 projects in the ship buildingsector. We allocated US$ 100 million on a per projectbasis to the health sector and US$ 30 million tocommercial banking customers. We target a rise inthe current cross-sales ratio of 5.7 to 6.5 by focusingon cash flow management products in these nichemarkets.

In the SME banking segment, we based our entirecredit allocation and structuring decisions on creditscorecards, achieving another first in Turkey. Thisallowed us to harmonize with Basel II credit riskmanagement processes and to make credit decisionsin as little as 72 hours. We carried out productstandardization and developed cash managementtools to provide mass marketing opportunities forSMEs. We moved into new and profitable areas in thissegment, currently undiscovered, through activemarketing campaigns and achieved significant costsaving by using alternative distribution channels,

thereby increasing our profitability. In 2005, the NakitKart (Cash Card) utilizing our POS terminals wasinitiated; this has found wide usage especially amongsuppliers and distributors as an alternative to post-dated checks and promissory notes. In the retailsegment, we developed specialized ProductPackages addressing specific financial needs ofcertain occupational groups such as teachers,financial advisors and Turkish Armed Forcesmembers and retirees.

DenizBank was the first privately owned bank to beengaged in agricultural lending in the Turkish bankingsector. Within the scope of the agricultural bankingservices offered through our 74 branches in Turkey,we provide agricultural credits with favorableconditions to farmers within the framework ofagreements signed with almost all of tractor andagricultural equipment producers. With Üretici Kart(Producer Card), we serve farmers in their purchasesand payment transactions with member firms. As ofthe end of 2005, Üretici Kart was being used by 2,560firms.

Our another strategic area of interest isbancassurance. As a result of cooperation with AxaOyak, Güven Sigorta and Garanti Pension FundCompany, insurance services encompassing variousareas that include workplace, agricultural, accident,fire, property and life coverage are offered atDenizBank branches.

09>

Message from the General Manager

The number of our credit cards totaled 1,380,869 atyear-end, including Miles & More, DenizBank andBonus Card. Purchases made with Miles & More Visaoffer free miles that can be used at Lufthansa, partnerairlines and hotels; customers using this credit cardtotaled 12,983 by the end of the year.

DenizBank serves 1,800 large national andmultinational companies in the corporate segment.Long-standing collaboration based on loyalty havebeen built with these companies engaged inbusinesses in various sectors including energy,construction, telecommunications, mining, finance andfood-offering them high-quality banking products andservices. We plan to further increase our market sharein the corporate segment. Customs duty paymentsthrough @ç›kDeniz Internet Branch are a result of ourendeavors to accomplish this objective.

There was a significant increase in DenizBank’sproject finance credits during 2005. Projects in theareas of health, energy and mass housing wereprioritized and a total of US$ 286 million was providedto those selected from among 50 projects totaling toUS$ 2 billion. Financing of oil products amounting to

US$ 300 million and various merchandise amountingto US$ 300 million were also realized within 2005.

With a total of YTL 43.5 billion in equity tradingvolume, DenizYat›r›m Securities, together withExpresInvest, maintained their leading position for thelast three years from among 107 brokerage houses.

In the second Corporate Governance AssessmentReport issued this year by EFG ‹stanbul Securities, aleading investment advisory firm, DenizBank wasrated at the top of the list, scoring the highest pointsfor corporate governance. Publicly traded companiesin Turkey were examined within the framework of theircompliance to corporate governance principles andevaluated according to 48 criteria under six headings.With the points it scored, DenizBank was placed inthe first category under five different headings. In thisreport, companies placed in the highest categoriesare listed along with their peers in terms ofimportance placed on investor relations, adherence tocorporate ethical codes, separation of the ExecutiveManagement and the Board of Directors, principles oftransparency and growth of capital efficiency. Wewere extremely proud that DenizBank was rated firstamong Turkey’s largest, long-standing companies in

PART II. MESSAGES

In the Corporate Governance Assessment Report issuedthis year by EFG İstanbul Securities, a leadinginvestment advisory firm, DenizBank was rated at thetop of the list, scoring the highest points for corporategovernance.

terms of corporate governance. DenizBank’s Board ofDirectors, consisting of seven members, three ofwhom are independent, does not include anyone fromthe Zorlu family, the majority shareholder. The minorityshareholders are represented by an independentmember on the Board. At DenizBank, all auditing andinspection activities are carried out at the Board ofDirectors level and risk management activities areconsidered to be a process integrated into the entireorganization.

Other important developments that took place in 2005were rating upgrades from Moody’s and FitchRatingsand an increase of the paid-in capitals of oursubsidiaries CJSC DenizBank Moscow,DenizFactoring and DenizLeasing.

DenizBank continues to sail on its course under theleadership of experienced captains, overcoming allobstacles. With each passing day, new shareholders,customers, business partners and employees arebrought aboard this safe and sound ship. I would like

to extend my thanks to all family members that makeup the DenizBank Financial Services Group. It is withtheir support and high ideals that we and ourshareholders sail in safe seas; our business partnerswho make every effort to ensure that our journey iscomfortable and secure and also our customers whosail with us on our ship.

We will continue to sail together on open seas in thedays to come.

Hakan Ateş

11>

February 2005The international credit rating agency Moody’shas rated DenizBank’s long-term local currencydeposits ‘Baa3’ and raised its foreign currencydeposits outlook from "Stable" to "Positive."

DenizBank was used as a case study at theMicrosoft Executive Summit held in Prague, onFebruary 2-3, marking an internationalaccomplishment for its IT infrastructure.

Microsoft and Intertech, a DenizBanksubsidiary, combined forces and made thedecision to initiate a project to develop newbanking software for DenizBank.

March 2005DenizBank Consumer Banking Group prepareda special loan package for teachers that enablethem to receive credits in the fastest and mostadvantageous manner - within the framework ofthe special lending practice that targets variousoccupational groups.

May 2005FitchRatings raised DenizBank’s long-termforeign currency and local currency ratingsfrom B (+) to BB (-) and its individual ratingfrom D to C/D. DenizBank’s short-term foreigncurrency and local currency support andnational ratings were confirmed as B, 4 andA (-), respectively. The outlook of the Bank’s alllong-term ratings was listed as "Stable."

DenizBank signed a cooperation agreementwith the leading international airline companyLufthansa’s Frequent Flyer Program Miles &More International; subsequently launching theMiles & More Visa Card.

DenizBank Consumer Banking Group created aspecial credit package for officers, NCOs andretirees of the Turkish Armed Forces.

PART III. REVIEW OF OPERATIONS IN 2005

From the

Captain’s

Logbook...

F INANCIAL SERV ICES GROUP

June 2005DenizBank received five-year and seven-yearsecuritization loans worth US$ 220 million andUS$ 80 million, respectively, from internationalmarkets, secured by customer remittances fromabroad.

July 2005DenizBank was declared the eighth fastestgrowing bank in the world, climbing 222 steps,in the ratings from The Banker based onchanges in Tier-1 capital growth.

August 2005DenizBank was placed in the lead position byscoring the highest points in the "CorporateGovernance" ratings of EFG ‹stanbul Securities,in which it took part for the first time.

September 2005DenizBank added two new loans to itsadvantageous home loans program calledDown Payment for Housing and 100% HomeLoan thus expanding the scope of its productsand services in this area.

DenizBank announced that it would sponsor all‹stanbul State Symphony Orchestra concerts tobe held in the 2005-2006 season, throughcoordination with DenizKültür.

October 2005DenizBank received a syndicated loan facility ofUS$ 650 million, participated by 78 internationalbanks from 28 countries.

DenizBank’s subsidiary, Tarifl Securities, wasrenamed DenizTürev Securities; the Company’scapital of YTL 7.0 million was increased to YTL8.0 million.

November 2005DenizBank’s subsidiary, CJSC DenizBankMoscow, increased its capital from Ruble246,498,000 to Ruble 516,472,000.

December 2005The international credit rating agency Moody’sraised DenizBank’s foreign currency depositsrating from B2 to B1.

FitchRatings raised DenizBank’s outlook from"Stable" to "Positive" and confirmed its BB-rating. DenizBank’s National rating was raisedfrom A (-) to A.

DenizBank’s SME Banking Group appointed400 portfolio managers as members ofTuruncular (The Orange Team), to sustain itssupport of SMEs.

Once again - full speed ahead!

Hakan Ateş

13>

DenizBank Financial Services GroupBanking Services

PART III. REVIEW OF OPERATIONS IN 2005

DenizBank occupies the sixth place among Turkey’sprivate sector banks in terms of total consolidatedassets.

>> DENİZBANK AT A GLANCEFollowing another year of favorable results, total assetsof DenizBank reached US$ 8,925 million by the end of2005, an increase of 48% over US$ 6,041 million in2004. By the end of the year, the Bank’s shareholders’equity stood at US$ 813 million, recording an increaseof 25% above the US$ 653 million posted in 2004. Thecapital adequacy ratio of DenizBank was as high as14.7%, with its free capital ratio, one of the best in theTurkish banking system, at 6.4%. By the end of 2005,DenizBank had 236 branches and a Call Center.

DenizBank occupies the sixth place among Turkey’sprivate sector banks in terms of total consolidatedassets. In a report published in the July 2005 issue ofthe world-famous magazine The Banker, DenizBankwas rated eighth among the top 1,000 banks in theworld in terms of Tier-1 capital growth. In the August2005 CG Universe Report by EFG ‹stanbul Securities,DenizBank took the first place in terms of compliance tocorporate governance principles.

15>

DenizBank Balance Sheet Structure (%)

2005 2004

AssetsLoans 51.6 39.8Banks 19.0 20.4Turkish Treasury Securities 11.2 18.4Cash and Reserves 6.4 8.6G7 Securities 0.7 4.1Other 11.1 8.7

LiabilitiesCustomer Deposits 58.3 63.3Shareholders’ Equity * 9.1 10.8Borrowings 28.2 20.5Other 4.4 5.4

Balance Sheet Total (US$ millions) 8,925 6,041

* DenizBank’s capital was raised from YTL 290 million to YTL 316.1 million on January 17, 2005 according to the Board of Directors’ resolution on December 31, 2004.

Banking ServicesDenizBank

>> DENIZBANK’S SHAREHOLDING STRUCTUREDenizBank’s shareholding structure is shown in thetable above. DenizBank’s shareholding structure doesnot contain any cross-shareholdings.

>> CUSTOMER SEGMENTATIONIn 2004, following a restructuring, the Bank’scommercial and corporate business activities weredivided into three segments to allow for specializationand diversification of products and services cateringto varying customer needs. These segments includeCorporate Banking serving companies with an annualturnover of over US$ 25 million, Commercial Bankingserving companies with an annual turnover ofbetween US$ 5.0 million and US$ 25 million, and SME

Banking serving companies with an annual turnover ofless than US$ 5.0 million.

The restructuring process also entailed a separationof responsibilities among branch offices designatedas retail & SME, corporate and full service branches.Changes were made in the organizational set-up andworkflow to provide the basis for better customerinteraction, as well as increased efficiency inmarketing channels and sales. This segmentationassisted the enhancement of DenizBank’s businessvolume especially in the small business segmentwhere many new companies were added to thecustomer portfolio.

PART III. REVIEW OF OPERATIONS IN 2005

Denizbank’s Shareholding Structure

Shareholders Number of shares Total Nominal Value-YTL Share Ratio Zorlu Holding A.Ş. 237,063,940,440 237,063,940 74.997%Other 11,059,560 11,060 0.003%Publicly Held 79,025,000,000 79,025,000 25.000%Total 316,100,000,000 316,100,000 100%

Share of Credit Allocations by Segments (%)

2005 2004Corporate Credits 37.6 33.4Commercial Credits 30.2 42Consumer Credits 13.6 8.5SME Banking Credits 12.5 7.1Credit Card Credits 6.0 9.0

Total Credits (US$ millions) 4,601 2,405

The restructuring process entailed a separation ofresponsibilities among branch offices designated asretail, corporate and full service branches.

>> RETAIL BANKING GROUP

Retail MarketingIn 2005, sales campaigns were conducted by theCRM Department using the Automatic Sales andSales Opportunities Screens, for the purpose offocusing the branch marketing staff on potentialcustomers. These customers can be displayed usingthe Sales Opportunities Screen and diverse productsand services can be offered to current customersthrough the Automatic Sales Screen.

With five campaigns conducted in 2005, sales weremade to 35,819 of a total of 47,905 customersthrough the Automatic Sales Screens and to 6,546 ofa total of 73,062 customers through the SalesOpportunities Screens.

Retail Banking Products and Their PerformanceCredit Cards

Performance of DenizBank Credit CardsCredit Cards Market Share (%)

2004 860,108 3.222005 1,380,869 4.61

Volume of Shopping with DenizBank Credit CardsUS$ millions Market Share (%)

2004 954 1.972005 1,458 2.29

Credit Volume of DenizBank Credit CardsUS$ millions Market Share (%)

2004 216 2.072005 277 2.14

Bonus CardBonus Card was the first multi-branded chip-basedVisa / MasterCard credit card in Turkey offering bothinstallments and rebate awards. There are 100,000partner businesses as members in the Bonusprogram which offers installments and cash rebates toBonus cardholders.

Bonus Card offers shopping opportunities to theBonus cardholders at millions of business venuescarrying the Visa / MasterCard emblem throughout theworld. Bonus cardholders can shop from membermerchants by spending the bonuses they earned fromprevious purchases.

Number of DenizBank Bonus Cards2004 484,6882005 718,509

Miles & More Visa CardMiles & More Visa Card is a credit card that evolvedfrom the cooperation of Miles & More International andDenizBank, offering free miles for each transaction. Miles& More Visa Card holders can use their award miles byconverting them into airline tickets at Lufthansa Airlinesand 33 other major airline companies, by renting cars atpartner car rental companies or by lodging at thepartner chain hotels.

The credit card practices and campaigns conducted in2005 are as follows:

• A series of cross-sales campaigns were organizedfor DenizBank’s current customers. DenizBank BonusCard was marketed to those DenizBank customerswith regular loan payments, those who participated inthe public offering of the Bank and to DenizYat›r›m

17>

Banking ServicesDenizBank

Securities customers; Miles & More Visa Card wasmarketed to customers with frequent internationalcredit card usage.

• fiansDenizi Award Program was launched.fiansDenizi is a credit card award program thatmotivates DenizBank and Bonus Card credit cardholders to use their cards to win bonuses in eachtransaction; this program increases the utilization rateand continuously updates the customer by sendingSMS messages to their mobile phones.

• A series of campaigns were conducted withDenizBank credit cards to increase the turnover ofcredit cards and the number of cardholders and todecrease costs.

Campaigns aimed at increasing the turnover ofDenizBank credit cards:

• Lucky Bonus Days• fiansDenizi• Cindrella Bonus• Deferred Payments, Extra Bonuses and Extra Installment Campaigns• Prize Drawing Campaigns

Campaigns aimed at increasing the number of creditcard holders:

• Referral Campaign• Cross-sales

Campaigns aimed at cost reduction:• E-mail Only

Consumer LoansThe volume of DenizBank consumer loans, which wasYTL 275 million in 2004, reached YTL 840 million in2005. DenizBank’s market share increased to 2.9% in2005, up from 2.2% in 2004.

The volume of DenizBank consumer loans registereda significant increase in 2005 mainly due to a deeperpenetration provided by a segment-focusedmarketing approach. The campaigns that targetedoccupational groups such as teachers, Turkish ArmedForces members and retirees, free-lance accountantsand financial advisors, doctors and dentists played amajor role in this increase. A new mortgage loan withan increased limit called Personal Financing Loan waslaunched; this is a brand new consumer loan practice.

The home loans provided in 2005 increasedsubstantially as a result of the revitalized residentialconstruction projects throughout Turkey. In addition toproviding home loans to individual customers,package deals were provided to constructioncompanies through joint projects.

The joint projects conducted with constructioncompanies and their volume are as follows:

• K‹PTAfi 5th Phase Housing Project: Total volume ofYTL 74 million for 760 houses• K‹PTAfi Pendik Aydos: Total volume of YTL 32million for 351 houses• Avrupa Konutlar› (European Residences): Totalvolume of YTL 10.7 million for 105 houses

In 2005, consumers were presented with differentalternatives in the area of home loans, some of whichwere “a first in Turkey”. They include:

• 100% Home Loan with a limit equaling the appraisalvalue of the house• Down Payment for Housing which aims atcomplementing a home loan received from anotherbank• Housing Development and Renewal Loan.

PART III. REVIEW OF OPERATIONS IN 2005

The volume of DenizBank consumer loans registered asignificant increase in 2005 mainly due to a deeperpenetration provided by a segment-focused marketingapproach.

Overdraft FacilityDenizBank raised the number of customers havingoverdraft limits to 125,000 from 72,500 in the previousyear. As a consequence, the overdraft total of YTL38.3 million at the end of 2004 was increased to YTL60.8 million at the end of 2005. The expansion of theBank’s overdraft facility volume was further enhancedby salary and private school tuition paymentagreements.

Salary Payment ServiceDenizbank provided salary payments services to90,339 individuals by the end of 2004, and thisnumber increased to 100,000 by the end of 2005.Total amount of salaries paid increased from YTL 38.1million to YTL 64.5 million in 2005.

In 2005, DenizBank delivered salary payments for 392private companies and 565 public institutions.

Composition of DenizBank’s Deposits 2005 2004

Time YTL 73% 75%Demand YTL 27% 25%

Total YTL Deposits US$ 2,016 US$ 1,216 million million

2005 2004Time FX 81% 81%Demand FX 19% 19%

Total FX Deposit US$ 3,390 US$ 2,636million million

Loans/Deposit Ratio 63% 88%

Retail Loan Allocation and Risk Monitoring Retail Loan Allocation DepartmentAll credit card applications are evaluated on the ROTASystem (application evaluation system). With thissystem, the Consumer Credit Bureau and the CentralBank of Turkey databases are automatically queried;applications that do not conform to the prescribedconditions are automatically rejected.

A system for personal loans that would function over theROTA system is currently in the development stage. Anagreement has been signed with Experian Scorex forthe development of a personal loan scorecard. Allpersonal loan applications, assessments and allocationtransactions will be carried out over the ROTA Systemfollowing the launching of the new system in the firstquarter of 2006.

Thanks to the ROTA System, the current period of 24hours for responding to credit applications delivered tothe Retail Loan Allocation Department in a completemanner, will be further decreased.

Risk Monitoring DepartmentIn the Risk Monitoring Department where credit riskconcerning personal loans and credit cards ismonitored, monitoring transactions are conductedcentrally and any delays are initially notified throughSMS messages. Customers that do not makepayments within seven days are notified of their delaysby phone. Search results are coded and stored on thesystem and the codes that require action aremonitored.

Notices are prepared and dispatched centrally for creditcard customers who fail to pay their debts for twoconsecutive periods, while monthly correspondence isheld with branches for the initiation of administrativefollow-up for personal loan customers.

19>

Banking ServicesDenizBank

Files of customers who fail to make correct and timelypayments are transferred to the Legal Department forthe initiation of legal proceedings.

Alternative Distribution ChannelsThrough DenizBank’s alternative distribution channels,customers may access all services, except for cashtransactions, without the need to visit a branch office. Inaddition to routine banking applications, these servicesalso include investment products that DenizBankcustomers can buy through the Internet Branch, ATMs,Kiosks and the Call Center. Through these channels,they can buy and sell mutual funds, government bondsand Treasury bills. Customers can also change foreigncurrency and buy prepaid GSM cards throughalternative distribution channels. Additionally, debit card

applications can also be made through all four of thesechannels.

In addition to applications through branches and thewebsite, customers can now apply and register onlinefor Internet banking services by simply calling the CallCenter.

In 2005, DenizBank’s newly designed, more functionaland user-friendly website was launched, enablingcustomers to reach the information they seek moreeasily and rapidly. The design of the @ç›kDeniz InternetBranch was renewed to create a better visual match andin more direct relation to and standardization with themain site. Together with the new design, performanceimprovement efforts were also carried out to increasetransaction speed.

PART III. REVIEW OF OPERATIONS IN 2005

DenizBank’s Alternative Distribution Channels’ Performance

2005 2004

Internet Branch Number of Customers 157,845 102,235Total Number of Transactions 4,992,686 2,772,380

Call CenterNumber of Customers 785,046 440,046Total Number of Transactions 4,950,000 3,105,828

Number of Kiosks 98 97

Number of ATMs 301 217

Number of Transactions on ADCs/Total Number of Transactions 24% 19%

Cost Savings Due to ADCs US$ 5,180,000 US$ 3,175,000

Through DenizBank’s alternative distribution channels,customers may access all services, except for cashtransactions, without the need to visit a branch office.

To promote the use of alternative distribution channels,customers are awarded DenizY›ld›z› (Sea Star) points at@ç›kDeniz, the Call Center and the Kiosks, in proportionto their usage of the channel. DenizY›ld›z› entitles thecustomer to certain privileges or benefits in theirtransactions with the Bank.

The constantly changing face of banking has demandedthat Alternative Distribution Channel management to beconducted through technology-based, user-friendlyapplications that make access to banking serviceseasier and more reachable globally. New technology isable to deliver account and market data on a real-timeonline basis. As an additional feature, informationcaptured in alternative distribution channels facilitatesCRM applications and cross-selling activities.

@ç›kDeniz Internet BranchIn operation since 1999, DenizBank’s Internet branch,@ç›kDeniz, has capabilities for modular transactionsand information search facilities. Through thisinnovative medium, the Bank’s customers canconduct all of their banking and investmenttransactions online. These transactions includeaccount information, credit card, investment andforeign currency transactions, money transfers, billpayments and communication with the Call Centerpersonnel.

Consumer credit applications can now be filed onlinethrough the @ç›kDeniz Internet branch. This furtherfacilitates elimination of paperwork while speeding upthe pace of credit approvals. Additionally, customsduty payments have been added to the list ofpayments DenizBank customers may make via

@ç›kDeniz. This option has facilitated the use of theInternet branch by companies that carry out dailytransactions with customs offices.

Sales of shares are also handled by DenizBank’sInternet branch within the framework of IPOs.Brokerage transactions conducted by investorsremotely in the comfort of their homes make@ç›kDeniz an ideal platform for trading securities.

In 2005, DenizBank customers conducted 4,870,000transactions through the Internet branch, an increaseof 176% over the 2004 figure.

SMS BankingDenizBank initiated SMS banking to increaseaccessibility and build confidence in the ease ofremotely conducted banking transactions. Themessage receiving capability of mobile phonesprovides a convenient platform for confirming certaintransactions and informing the customers of bond andTreasury bill maturity endings and new products. Forthose customers looking for absolute security in theirInternet banking transactions, personal codes aredirectly delivered to their mobile phones.

GPRS BankingIn line with its principle to offer the best solutions thatmatch the needs and expectations of its customers,DenizBank initiated GPRS banking. Together withSMS Banking, this new service aims to make remotebanking transactions faster and less expensive.

Through GPRS Banking, DenizBank offers itscustomers the opportunity to monitor their accounts,

21>

Banking ServicesDenizBank

carry out money transfers, receive credit cardinformation, make credit card payments and receivestock portfolio information using the @ç›kDenizwebsite via their mobile phones from any location.

fiifreTek and fiifreTek MobileIn 2005, DenizBank launched fiifreTek, an applicationthat generates a new password for transactions thatwill be used only once, enabling @ç›kDeniz Internetbranch customers to carry out their bankingtransactions more securely. Thanks to fiifreTek, a two-step security option is offered to users for their moneytransfer transactions or @ç›kDeniz accesses (username, e-password, @ç›kDeniz password and fiifreTekpassword).

fiifreTek Mobile is an application downloaded to java-supported mobile phones that generates a newpassword for every access. This is a one-timepassword that can be used anywhere over mobilephones to help users feel more secure.

Contact CenterIn addition to the rapid and simple serviceopportunities the Contact Center has provided toDenizBank customers via technology, as of 2005, ithas assumed a new role and has initiated sales andmarketing activities. The Center serves as the solechannel for credit applications through telephone(AloKredi), a first-in-Turkey. As a low-cost servicechannel offering efficient, rapid data processingservices, the Contact Center has created significant

added value with regard to sales and marketingactivities through making outgoing calls coordinatedwith the Marketing Department and/or the branchesand Cross-Sales and Sales Opportunities campaigns.

Accordingly, successful overdraft account and creditcard marketing activities were achieved in 2005;personal accident insurance policies were sold toover 1,000 customers through sales effortsundertaken during the last two months of the year.

In 2005, the number of incoming calls to the ContactCenter rose to 4,200,000; the number of outgoingcalls reached 850,000.

ATMs and KiosksATMs assist customers with their petty cash needsand for the most part are instrumental in the provisionof salary disbursements. In addition to the DenizBankInternet Branch, in-branch and off-site banking kiosksalso allow debit or credit cardholders to sign in withtheir personal passwords.

Cash withdrawal, credit card transactions, balanceinquiry and account statement, cash deposit, billpayments, information update, transfers andpassword changes can be transacted throughDenizBank ATMs.

In 2005, the kiosks started issuing debit and creditcard passwords. This has enabled users to obtaintheir passwords more easily, quickly and securely.

PART III. REVIEW OF OPERATIONS IN 2005

Adopting a customer-focused strategy, DenizBankSME Banking increased the number of products on theshelves of its financial supermarket with speciallydeveloped credit packages tailored to the needs of smallcompanies representing numerous different businesslines.

>> BUSINESS BANKING GROUP

Customer Relations Management (CRM) andBranch Planning

In 2005, DenizBank expanded its distribution networkto 236 branches in 52 cities, primarily in micro-markets where consumers and small businesscustomers are concentrated. The network of brancheswere restructured to meet the needs of diversecustomer segments and to concentrate on these so-called micro-markets. With the aim of increasingmarket efficiency and concentration, the Bankestablished its fourth Regional Directorate in ‹stanbul,the city assuming the leading role in Turkey’seconomic growth.

As part of CRM activities, product penetration israpidly increasing through the Automatic SalesPlatform, an application that decreases transactiontimes by automating sales processes and offeringcentralized product sales opportunities. Customersegmentation is implemented effectively at alldistribution channels of the Bank, enabling increasedefficiency by defining customers and determiningservice levels. Product purchasing trends computedthrough usage ratios and data mining models can bedisplayed by individual customers and shared byportfolio managers through the newly developedCustomer Relations Management platform.

SME Banking

DenizBank SME Banking, developed to serve smallcompanies with an annual sales turnover of belowUS$ 5.0 million, continued its rapid growth in 2005. Asof the end of 2005, the number of customers reached121,523, credit limit US$ 1.2 billion and outstandingloans US$ 614 million. SME Banking customers’deposits and investment accounts reached a total ofUS$ 800 million.

Adopting a customer-focused strategy, DenizBankSME Banking increased the number of products onthe shelves of its financial supermarket with speciallydeveloped credit packages tailored to the needs ofsmall companies representing numerous differentbusiness lines. By analyzing the cash cycles ofsectors such as tourism, food products, white goods,furniture and stationery, credit products providing themost advantageous payment terms for these sectorswere developed. In addition, credit products forworkplace renovations and refurbishments andequipment and technology purchases with diverseterms were launched.

Thanks to the scorecard driven credit evaluationmodel responding swiftly to credit applications ofSMEs, a credit decision can be reached within 72

23>

Banking ServicesDenizBank

hours at the latest, following completion of allpaperwork. The most important feature of the creditevaluation model is the fact that it takes intoconsideration criteria such as the experience,reputation and background of the business owner,which demonstrate his/her commercial reputation, inaddition to available financial data. Each week 1,000credit applications are evaluated through this model.

Undertaking new endeavors in 2005, DenizBank SMEBanking launched its training and consultationservices under the Business Notes name. Thisinitiative was planned to provide support and meet theinformation requirements of small businesses oncertain issues during stages of development andgrowth, enabling them to continue moving aheadmore easily and securely. The main topics taken up atthe seminars organized are tax and financialmanagement, labor law, foreign trade, EUharmonization processes and Basel II criteria.Following the seminars, consultation services areprovided to customers by business experts on thesetopics, free of charge. Within the scope of thisinitiative, nearly 2,000 business owners participated inthree seminars conducted during 2005. Theseseminars will continue in 2006 throughout the country.

With the aim of supporting more SMEs, DenizBankSME Banking Group launched its Turuncular (TheOrange Team) campaign with a press conference onDecember 12, 2005, mobilizing the services of nearly400 portfolio managers specialized in SME Bankingtransactions. These efforts, aiming at furtherpublicizing DenizBank’s SME Banking brand name,were supported by intensive advertisementcampaigns on television, radio, newspapers andmagazines.

SME Banking Customer BaseNumber of Number ofSmall-size Medium-size

Companies Companies Total2004 45,056 13,458 58,514 2005 91,143 30,380 121,523

SME Banking Cash Credit Allocations2005 2004

Number of customers that received a credit line 35,122 12,154

Total cash credits utilized by SMEs (US$ millions) 446 132

Cash Management

In business life, narrowing profit margins increase theimportance of operational costs and cash flowplanning in financial management. DenizBank CashManagement aims to help its customers create costadvantages, decrease operational costs and reducecollection risk, by offering them state-of-the-arttechnological facilities for payment and collectiontransactions.

Electronic Collection ServicesThe E-ve-t Tahsil Et (Electronic Data Transfer-Collect)system, enabling supplier companies to automaticallycollect payments from their distributors-dealers, wasdeveloped for the purpose of forming a collectionsystem between the supplier company and its regularcustomers. Within the scope of this system, contractsare signed with companies from various sectors, firstand foremost iron and steel, petroleum products,construction materials, automotive, agriculture, foodand telecommunications. The E-ve-t Havuz Hesap(Electronic Data Transfer-Pool Account) provides a

PART III. REVIEW OF OPERATIONS IN 2005

With the aim of supporting more businesses, DenizBankSME Banking Group launched its Turuncular (TheOrange Team) campaign, mobilizing the services ofnearly 400 portfolio managers specialized in SMEBanking transactions.

smooth and automatic cash flow between theheadquarters of the current customers and theiragencies, regional offices and liaison offices.

Since 2004, collection and payment services havebeen delivered through the Nakit Kart (Cash Card),which can be described as a kind of electronic checkbook that functions in the form of a closed circuitbetween the wholesaler and the retailer.

In 2005, approximately 100,000 collectiontransactions amounting to YTL 288 million werecarried out with E-ve-t Tahsil Et, Nakit Kart and E-ve-tHavuz Hesap. A credit limit of YTL 54 million wasallocated to the members of this system within thescope of these applications, scoring a 343% increasein collection amounts and 350% in credit limits,compared to 2004.

With regard to the Kiptafl Baflakflehir Housescollection project initiated in 2004, YTL 83 million wasrealized within 2005, with the addition of new Kiptaflhousing projects. People who purchase houses maketheir down payments and installment paymentsthrough DenizBank, the only bank involved in theproject.

In 2005, a contract was signed with BaflkentUniversity for the collection of tuition fee paymentsand other payments by students enrolled at theUniversity. The amount collected in the fall termtotaled YTL 46 million.

Electronic Payment ServicesWithin the E-ve-t-Öde (Electronic Data Transfer-Pay)electronic collection system that allows more than oneEFT-transfer transaction during a single access,217,000 electronic transactions amounting to nearlyYTL 1.5 billion were realized in 2005.

Efforts to expand the use of the E-ve-t-Gümrük(Electronic Data Transfer-Customs) application,allowing more than one customs payment through theInternet Branch, are underway.

Institutional CollectionsDenizBank is one of the banks leading the way inadopting online collection systems for the SocialInsurance Institution, the Turkish ElectricityDistribution Company and taxes. In 2005, the Bankachieved a volume of YTL 3.4 billion in institutionalcollections. DenizBank won the ‹stanbul GasDistribution Company tender for a third year in a row;this project had a collection volume of YTL 255 millionin 2005.

Western UnionIn 2005, money transfers through the Western Unionsystem achieved over 90,000 transactions for avolume of US$ 64 million. DenizBank earned acommission income of more than US$ 775,000.

25>

Banking ServicesDenizBank

member vendor companies on a 24/7 basis. They arealso offered installment and/or discount facilities forpurchases made with these cards. In 2005, the numberof vendors accepting the Producer Card increased to2,560.

DenizBank has signed special agreements withcompanies that purchase produce from farmers andcarries out other projects in cooperation with them. TheBank created a special version of the Producer Card, aSmart Card application, a first in Turkey and the world,with Kütahya Sugar Factory.

2. Medium-term Agricultural LoansSpecial products have been designed toaccommodate farmers’ frequent needs. The mostimportant aspect of these products is the offer ofequal installments or flexible repayment schedules,tailored to the farmers’ production cycles and cashflow patterns. The products offered within this scopeare as follows:

• Tractor and Equipment Loans• Dairy Husbandry Loans• Greenhouse Construction Loans• Field Purchasing Loans• Fruit Facility Loans

Agreements have been made with ten tractormanufacturers and/or importers to facilitate thegranting of tractor credits to DenizBank customers,granted with buy-back guarantees.

Number of Agricultural Banking Customers with aCredit Line2004 9,8002005 19,500

Agricultural Credit Allocations (US$ millions)2004 382005 129

PART III. REVIEW OF OPERATIONS IN 2005

Agricultural Banking

After the acquisition of Tariflbank in 2002, DenizBankstarted providing support to the agricultural sector,Tariflbank’s traditional area of involvement. AnAgricultural Banking Department was establishedwithin DenizBank, a unique move in the Turkishbanking system. The geographical range and scopeof agricultural credits were expanded in 2005 toencompass 74 branches and 19,500 producers withYTL 173 million issued credits.

Agricultural Banking provides finance and otherbanking services to the agricultural sector, which hasan exclusive structure encompassing individuals whoearn their livelihood through agriculture plus corporatebodies engaged in this sector. Thus, the productsdeveloped address farmers and correspond to therealities of the agricultural sector. The best example ofthis is the loan model with a single repayment peryear, which suits the farmers’ cash flow patterns. Thespecial logo and brand created for the AgriculturalBanking Department demonstrate the importanceDenizBank gives to this area.

While a series of credits are provided for the diverseneeds of farmers, there are two main types ofagricultural loans granted by DenizBank:

1. Short-term Agricultural Loans (Producer Card)Short-term credits are granted to the agriculturalsegment through the use of a Producer Card, whichcarries a maximum term of 12 months. It providesfarmers with agricultural working capital loans tailoredto their particular requirements and cash flow patterns.Farmers can use their Producer Cards by makingpurchases from member vendor companies or drawingcash from ATMs. In other words, with the ProducerCard, farmers are provided the opportunity to use cashcredits through ATMs to purchase fertilizers, agriculturalchemicals, fuel-oil, spare parts and other needs from

Agricultural Banking provides finance and other bankingservices to the agricultural sector, which has anexclusive structure encompassing individuals who earntheir livelihood through agriculture plus corporate bodiesengaged in this sector.

Bancassurance Services

In 2005, DenizBank was one of the most successfulbanks delivering insurance services, thanks to its richproduct range serving different customer needs andefficient employment of its marketing and sales-focused policies.

Evidence of the dynamic development of DenizBank’sinsurance services during 2005 were thestrengthening of its insurance IT infrastructure as aresult of the cooperation with Axa Oyak, motivation ofthe branch personnel in insurance sales throughtraining activities and the joint offering of banking andinsurance products.

The Bank offers bancassurance services includingworkplace, agricultural, accident, fire, home and lifeinsurance. Furthermore, existing insurance policies ofthe customers are followed-up and extended onrenewal dates.

As a result of the increase in the activities focusing oninsurance services targeting the maritime andagricultural sectors, 22 vessels were insured andlong-term insurance transactions were started for farmtractors with the newly developed Long-Term TractorComprehensive Insurance Policy product offeringfavorable price advantages. In the area of agriculturalinsurance, product and greenhouse insurancepolicies were provided to farmers within the scope ofan agency agreement with Güven Sigorta.

Non-life insurance premiums that totaled YTL 6.4million in 2004 increased by 183% to reach YTL 18.1million in 2005; life insurance premiums of YTL 1.8million increased by 233% to reach YTL 6 million. In

2005, total insurance premiums amounted to YTL 24.1million while insurance commission income was YTL 4million. DenizBank branches issued a total of 137,000policies during 2005; 90,000 of which were for life and47,000 for non-life insurance policies.

Through the cooperation carried out with GarantiPension Fund in the last quarter of 2005, DenizBankbranches began providing private pension plans.Over 400 members of the branch staff were trained tobecome Private Pension Representatives. DenizPortfolio Management now manages the GovernmentDebt Instruments Pension Investment Fund includedin the pension plans.

DenizBank Bancassurance Performance(US$ millions)

2005 2004Premium Production 18.0 5.7Commission Income 3.0 1.1

DenizBank aims to maintain its success inbancassurance by increasing its Private PensionPlans activities, as well as insurance services in 2006.

27>

Banking ServicesDenizBank

>> CORPORATE AND COMMERCIAL BANKING GROUPS

DenizBank Corporate and Commercial Banking2005 2004

Number of Corporate Customers 1,854 1,290Number of Commercial Customers 10,000 7,750Corporate + Commercial

Banking Market Share 4.75% 3.95%

>> CORPORATE BANKING GROUPThe Corporate Banking segment started 2005 with 1,290customers; by year end the number had reached 1,854.Corporate customer services were delivered through sixcorporate banking centers. The large-scale andmultinational companies included in this segment havemore sophisticated banking requirements. The 50-member marketing team composed of trained andexperienced professionals can tailor complex productpackages according to customer requests.

In addition to offering dynamic solutions to the bankingneeds of multinational and large-scale customers in itsportfolio, the Corporate Banking Group acts as anintermediary for capital movements such asprivatizations, mergers and acquisitions. It assumes anactive role in the marketplace within niche sectors suchas health, tourism, maritime and education.

The Group creates synergy with other businesssegments of the Bank, contributing to its total businessvolume.

Total credit portfolio of the Corporate Banking Group,which was US$ 1.8 billion at the end of 2004, reachedUS$ 2.7 billion in 2005, for an increase of 50%.

The Corporate Banking Group aims at raising the Bank’smarket share by increasing activities with corporatecustomers, thereby reinforcing its image in this sector.

Project FinanceThe Project Finance Department initiated its activitiesunder the Corporate Banking Group in February 2005.It serves as an intermediary in the development of abusiness concept that creates the maximumeconomic value. Aiming to create value for new andexpansion investments to be realized in prioritizedsectors of energy, health, maritime, construction,tourism and education, the Department also offersfinancial restructuring and project managementservices.

DenizBank’s Project Finance Department is equippedwith the necessary means to respond swiftly toprojects of all sizes. As a result of its projectmanagers being specialized in prioritized sectors andIT support, the Department operates within a projectpartnership approach and a principle of “well-structured solutions”.

PART III. REVIEW OF OPERATIONS IN 2005

DenizBank’s Project Finance Department is equippedwith the necessary means to respond swiftly to projectsof all sizes. As a result of its project managers beingspecialized in prioritized sectors and IT support, theDepartment operates within a project partnershipapproach and a principle of “well-structured solutions”.

In 2005, the Department evaluated 50 projectstotaling US$ 2 billion; it allocated funds worth US$ 286million to the approved projects. It also providedproject consultation services to various energy, healthand education institutions and served as a consultantfor tender-related issues for its customers with regardto the cement factories being sold by the SavingsDeposit Insurance Fund.

Having focused primarily on determining its prioritizedsectors, specializing in these sectors and forming thetechnical infrastructure required for projectmanagement therein in 2005, the Department aims atenlarging its project finance customer portfolio during2006.

>> COMMERCIAL BANKING GROUPWith the focused efforts of 205 expert sales andmarketing personnel working in the area ofcommercial banking, DenizBank is one of the mostactive players in this market segment. The Bank offerscommercial banking services to companies with anannual turnover of between US$ 5 to 25 millionthrough its 62 branches. Six of these branches havebeen converted into Commercial Centers serving onlycommercial segment customers, thereby meetingcustomer requests as quickly as possible.

The number of commercial customers, which was7,750 at the beginning of the year, exceeded 10,000as a result of the intensive marketing activities carriedout in this area. In addition to gaining new customers,another area of focus was further specialization inbusiness lines the commercial segment customersoperate in.

Outstanding credit volume granted to commercialsegment customers reached US$ 2.4 billion in 2005,an increase of over 30%.

In 2005, significant progress was noted in nichesectors, which constitutes an important part of theBank’s marketing approach. To date, a credit limit ofUS$ 700 million was allocated to the maritime sectorfor 75 projects; DenizBank has become one of theleading banks in this sector. The credit limit allocatedto the tourism sector was US$ 360 million for over 100investments. With support provided by the ProjectFinance Department, the commercial bankingsegment concentrated on healthcare, education andenergy sectors, in addition to maritime and tourism.The activities in these sectors continue to increaseand all sectors are closely monitored to create newmarketing opportunities and avoid problem loans.

29>

Banking ServicesDenizBank

>> PRIVATE BANKING

The DenizBank Private Banking Center, which beganoperations in September 2004 in ‹stanbul under theTreasury Department, grew rapidly in 2005.Individuals with cash investments worth US$ 150,000and above, defined as the upper segment ofindividual customers, usually require moresophisticated services in addition to traditionalbanking transactions. DenizBank endeavors to reacha higher market share in private banking, bygenerating solutions tailored to a variety of requestsmade by high networth customers.

Customer portfolio managers tasked with meetingprivate banking needs are trained and experiencedprofessionals who can assess dynamic investmenttrends in line with customers’ risk perceptions andadvise them accordingly.

The Baflkent Private Banking Center in Ankara startedoperations in September 2005 along with preparationsfor establishing the Ege Private Banking Center inIzmir. The Ege Private Banking Center will start itsoperations within the first few months of 2006. Due toan enlarging organizational structure, in November2005, the Private Banking Group was establishedunder Treasury Management.

The Private Banking Centers offers customers thehighest level of return with minimum risk, making useof the synergy of DenizBank’s Financial ServicesGroup. With a brand new approach different from the

practices of other banks, Private Banking Centersremain in contact with the customers directed throughDenizBank branches located in their area, along withtheir own customers, thereby creating positivesynergy.

Through Private Banking Centers, DenizBank aims atproviding its customers the opportunity to reach allfinancial markets under a single roof. With this inmind, stock transactions initiated in the PrivateBanking Centers through a cooperation withDenizYat›r›m Securities in April 2005 proved to bevery profitable in a very short time. In addition totraditional products, transactions involving derivativeproducts which are fairly new in Turkey are alsointensively carried out. Thanks to comprehensiveproduct information available on the Bank’s platforms,all potential risks and changes in taxes, in addition toinformation on returns, are shared with customers.

The Private Banking Group aims to reach a widercustomer base through the corners set up within thecurrent branch premises. Private Banking Corners willalso be set up within the three corporate branches in‹stanbul. Depending on the results of this pilotpractice, corners will continue to be set up in othervenues.

Having closed 2005 as the leader within the Bank interms of Treasury bonds, foreign currency andEurobond transaction volumes, the Private BankingGroup will continue expanding in 2006, furtherincreasing its transaction volume and offering newproducts.

PART III. REVIEW OF OPERATIONS IN 2005

DenizBank is gradually increasing its share in tradevolume between Turkey-Austria-Russian Federationtriangle, pursuing close cooperation with the subsidiariesin Austria and the Russian Federation.

>> INTERNATIONAL SUBSIDIARIES

BackgroundEstablished in 1996 by the former Esbank of Turkey,Esbank AG Vienna was acquired by DenizBank inAugust 2002 for a sum of € 25 million; DenizBankFinancial Services Group attained an opportunity tooffer comprehensive foreign trade finance andpayment services to a large client base in Europe andTurkey through entrance into the Eurozone bankingmarket. Subsequent to the acquisition in 2003, thename was changed to DenizBank AG.

DenizBank AG is a member of the Austrian Deposit Insurance Fund, the International ForfaitingAssociation, the Austrian Bankers’ Association and the Austrian-Turkish Cooperation Council.

Widespread PresenceIn July 2003, DenizBank AG opened its first branchbeyond the borders of Austria in Frankfurt, thefinancial center of Germany. With the inauguration ofthe Linz Branch in August 2003, the Innsbruckbranch in June 2004 and the Dortmund and Grazbranches in August 2005, the number of DenizBankAG branches increased to nine. The premises of theFrankfurt branch were enlarged at the same time asthe premises of the Südbahnhof branch toaccommodate the increased volume of business andto serve also as a Call Center. The representativeoffice of DenizBank AG, established in ‹stanbul in

2004, in an effort to follow the Turkish marketdevelopments more closely, has increased itsnumber of personnel and improved technicalmakeup to establish a more active presence there.

Wide Range of Products and ServicesDenizBank is gradually increasing its share in tradevolume between Turkey-Austria-Russian Federationtriangle, pursuing close cooperation with thesubsidiaries in Austria and the Russian Federation.DenizBank AG plans to expand its activities in theEurozone via new branches in Germany. The Bankwill continue to act as an intermediary for the foreigntrade transactions of Turkish companies in Eurozonecountries, delivering forfaiting, non-cash credits andforeign currency transfer services. Other services ofthe Bank include consumer and small businessloans, alternative savings programs, credit cards,money transfers and various insurance products.Particularly through the Internet banking service(www.denizbank.at), initiated at the beginning of2005, there has been a significant increase in theBank’s customers and transaction volume.DenizBank AG launched private banking services in2004 and is expected to grow further in this segmentwith customer assets under management reaching€ 50 million.

Moreover, DenizBank AG is involved actively inproject finance facilities through the credit linesallocated to energy, education and tourisminvestments in Turkey.

31>

Banking ServicesDenizBank

Sound Financial ResultsAt the end of 2005, DenizBank AG had total assets of€ 868.3 million (€ 585.5 million in 2004), shareholders’equity of € 44.3 million (€ 38.8 million in 2004) andbefore-tax profit of € 7 million (€ 5.1 million in 2004).In 2005, the Bank obtained a syndicated loan facilityof US$ 80 million from 23 participating internationalbanks.

BackgroundDenizBank acquired ‹ktisat Bank Moscow at thebeginning of 2003. Subsequent to the acquisition, thename of the bank was changed to DenizBankMoscow and its capital was increased from US$ 1.7million to US$ 8 million; an additional increase in2005, of US$ 10 million, brought this total to US$ 24.3million. The shares of DenizBank Moscow aredistributed between DenizBank AG and DenizBankA.fi., which currently own 51% and 49% of the sharecapital of the Bank, respectively. DenizBank Moscowis a member of the State Deposit Insurance System,the Association of Russian Banks and the Associationof Russian-Turkish Businessmen (RTIB).

Business Goals and Core ActivitiesDenizBank Moscow was established with a vision tocreate a medium-size commercial bank that wouldserve as a full financial service provider primarily toTurkish and Russian businesses in the Turkey-European Union-Russian Federation / CIS triangle.

As a result of the intensifying commercial andinvestment relations between Turkey and Russia, thetrading volume between the two countries exceededUS$ 15 billion as of the end of 2005, and there areapproximately 30,000 Turkish citizens, mainlyentrepreneurs and workers, living in the RussianFederation. Investments by 1,000 Turkish companiesengaged in various sectors have reached US$ 2billion and the aggregate annual revenue is at US$ 5billion with tourism, manufacturing and imports in thelead, along with an ongoing construction projectvolume of US$ 5 billion. They provide a uniqueopportunity for DenizBank Moscow to become amedium-sized commercial bank providing credit, non-credit and trade finance products to entrepreneursdoing business in the Russian Federation.

The Bank serves as a ‘first stop’ for DenizBank clientsin Turkey currently conducting business in Russia orfor those who want to pursue possible businessopportunities there. The electronics division of ZorluHolding in Russia, Vestel CIS, the textile division, TaçTextiles and the energy division, Zorlu Energy, alsoprovide the Bank with valuable business potential andcontributes to synergy building.

In addition to its core business of commercialbanking, DenizBank Moscow has also become anactive player in the Russian foreign exchange andmoney markets, as well as in fixed-income securitiestrading and investments.

PART III. REVIEW OF OPERATIONS IN 2005

In addition to its core business of commercial banking,DenizBank Moscow has also become an active player inthe Russian foreign exchange and money markets, aswell as in fixed-income securities trading andinvestments.

Activities in 2005In 2004, DenizBank Moscow acquired a license fromthe Central Bank of the Russian Federation to startretail banking activities and collect depositsdenominated in both the Ruble and foreigncurrencies. The Bank has also obtained licenses fordealership, brokerage, depository and custodyoperations. Furthermore, DenizBank Moscow wasadmitted to the newly enacted State DepositInsurance System and MICEX - Moscow InterbankCurrency Exchange and initiated transactions in theexchange.

In 2005, the Bank increased its trade finance volumesignificantly and widened its international anddomestic correspondent network, thereby enlargingits funding base with these banks.

The IT infrastructure of the Bank was updated withnew hardware and a VPN connection was establishedwith DenizBank in ‹stanbul resulting in uninterruptedinformation sharing and communication. In addition tothe renewed and upgraded Internet website, the Bankcompleted its Business Continuity and EmergencyPlans in 2005. Infrastructure shortcomings wereeliminated in the area of risk assessment, andmanagement systems.

In 2005, the Bank reached major Turkish companiesoperating in the Russian Federation mainly in theconstruction and tourism sectors. Major constructionprojects around the entire Russian Federation weresupported with cash and non-cash credit lines; the

tourism sector was provided with cash managementservices through the opening of Remote Cash Units,in addition to cash credits.

In 2005, DenizBank Moscow’s total assets increased104% to US$ 116.4 million from US$ 57.1 million in2004. Its shareholders’ equity registered a 115%increase and reached US$ 20.6 million from US$ 9.6million in 2004. The Bank posted a before tax profit ofUS$ 2.1 million at the end of 2005.

DenizBank had acquired EuroDeniz Off-Shore BankLimited, located in the Turkish Republic of NorthernCyprus from the Savings Deposit Insurance Fund atthe beginning of 2002. The Bank is an off-shore bank,licensed to undertake all commercial bankingtransactions.

At the end of 2005, EuroDeniz Off-Shore Bank had abalance sheet total of US$ 726.5 million (US$ 386.2million in 2004) and shareholders’ equity of US$ 27.3million (US$ 69.2 million in 2004).

33>

DenizBank Financial Services GroupInvestment Banking and Brokerage Services

PART III. REVIEW OF OPERATIONS IN 2005

With the largest brokerage houses in Turkey, DenizYatırımSecurities ranks second among more than 100 in terms ofaverage market shares for the last three years.

A Strong Presence in Turkey’s Capital MarketsTargeting leadership to meet financial return andservice quality expectations of its clients as well asthe creation of a solid position in capital markets,DenizYat›r›m Securities was established in January1998 as a DenizBank subsidiary. The company haspioneered in several areas and obtained a leadingposition among capital market institutions by offeringall the activities within the capital markets investmentbanking product range in an efficient and transparentmanner. Meanwhile, the company has taken intoaccount the common denominator made up of clients,employees, shareholders and regulatory institutions,thanks to the synergy generated through its corporatestructure, professional management team and 236DenizBank branches.

DenizYat›r›m Securities has pioneered in several areaswithin the capital markets between 1998 and 2005.• Acquisition of Tektafl Securities - January 2000

• The first merger of brokerage houses realized inTurkish capital markets

• Public Offering of Zorlu Energy - May 2000 • Record number of investor applications: 474,274

• Public Offering of Fenerbahçe Sportif - February2004 • The first and only brokerage house offering fullunderwriting guarantee prior to the public offering • More than six-fold demand in small-size individualinvestor category

• Public Offering of DenizBank - September 2004 • Domestic demand exceeding US$ 200 millionreceived by DenizYat›r›m Securities alone

• Public Offering of Trabzonspor Sportif - April 2005 • 8.1-fold demand from small-size individual investorcategory

With the largest brokerage houses in Turkey,DenizYat›r›m Securities ranks second among morethan 100 in terms of average market shares for thelast three years. The success achieved by thecompany is a result of the efficient use of the tradingrooms, Internet sites and call centers located in 236DenizBank branches all over Turkey. DenizYat›r›mSecurities has 156 VIP and 78 regular trading roomsin 122 DenizBank branches.

35>

2005

2004

2003

2002

2001

2000

1999

27,429

24,205

13,668

8,862

4,239

3,060

488

Equity Trading Volume in Domestic Markets (YTL millions)

2005

2004

2003

2002

2001

2000

1999

5.10

5.85

4.68

4.20

2.28

1.38

0.66

DenizYatırım Market Share (%)

Investment Banking and Brokerage Services

Results for 2005 placed DenizYat›r›m Securitiesamong the top players in the market again. With 320employees working throughout Turkey, DenizYat›r›mSecurities has maintained its leading position inTurkey’s capital markets.

Domestic MarketsDenizYat›r›m Securities achieved an equity tradingvolume of YTL 27.4 billion (US$ 20.4 billion) and amarket share of 5.1%. As of the end of 2005, thecompany reached a customer asset size of US$ 1.2billion with 78,477 active account holders.

Corporate Finance Although a relatively new company, DenizYat›r›mSecurities has become one of the most important brandsin Turkey with regard to investment banking, makingmajor achievements with the projects it has realized.Several public offerings under DenizYat›r›m Securities’leadership are anticipated in 2006. Additionally, the

company provides financial consultation to thePrivatization Administration for Türk Telekom’s block saleand public offering. With the block sale tender of TürkTelekom held in July 2005, Turkish Treasury’s TürkTelekom shares of 55% were sold to Oger Telecom for asum of US$ 6.55 billion; the shares were transferred toOger Telecom when an agreement was signed inNovember 2005. This amount is the largest privatizationand strategic block sale value in the history of theTurkish Republic. DenizYat›r›m Securities will act asPrivatization Administration’s financial consultant anddomestic consortium leader for the Türk Telekom publicoffering planned to be held in 2006.

DenizYat›r›m Securities acted as the consortium leaderfor the Trabzonspor Sportif IPO held in April 2005 for atotal sales volume of US$ 24.3 million; purchase orderswere 8.1 times the shares on offer and were collected inthe small-size individual investor category while US$ 109million worth of orders were received in total for the IPO.

PART III. REVIEW OF OPERATIONS IN 2005

Public Offering Projects in 2005

Brokerage House Total Demand (US$) %