Understanding of financial derivatives 1 CHAPTER 1 Introduction Definition of Derivatives One of the most significant events in the securities markets has been the development and expansion of financial derivatives. The term ³derivatives´ is used to refer to financial instruments which derive their value from some underlying assets. The underlying assets could be equities (shares), debt (bonds, T-bills, and notes), currencies, and even indices ofthese various assets, such as the Nifty 50 Index. Derivatives derive their names from theirrespective underlying asset. Thus if a derivative¶s underlying asset is equity, it is called equity derivative and so on. Derivat ives can be traded either on a r egulated exchange , such a s the NSE or off the exchanges, i.e., directly between the different parties, which is called ³over-the-counter´ (OTC) trading. (In India only exchange traded equity derivatives are permitted under the law.) The basic purpose of derivatives is to transfer the price risk(inherent in fluctuations of the asset prices) from one party to another; they facilitate the allocation of risk to those who are willing to take it. In so doing, derivatives help mitigate the risk arising from the future uncertainty of prices. For example, on November 1, 2010 a rice farmer may wish to sell his harvest at a future date (say January 1, 20 11) for a pre-determined fixed price to eliminate the risk of change in prices by that date. Such a transaction is an example of a derivatives contract. The price of this derivative is driven by the spot price ofrice which is the "underlying". Origin of derivatives While trading in derivatives products has grown tremendously in recent times, the earliest evidence of these types of instruments can be traced back to ancient Greece. Even though derivatives have been in existence in some form or the other since ancient ti mes, the advent of modern day derivatives contracts is attributed to farmers¶ need to protect themselves against a decline in crop prices due to various economic and environmental factors. Thus, derivatives contracts initially developed in commodities. The first ³futures´ contracts can be traced to the Yodoya rice market in Osaka, Japan around 1650. The farmers were afraid of rice prices falling in the future at the time of harvesting. To lock in a price (that is, to sell the rice at a predetermined fixed price in the future), the farmers entered into contracts with the buyers. These were evidently standardized contracts, much

Transcript

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 1/43

Understanding of financial derivatives

1

CHAPTER 1

Introduction

Definition of Derivatives

One of the most significant events in the securities markets has been the development and

expansion of financial derivatives. The term ³derivatives´ is used to refer to financial

instruments which derive their value from some underlying assets. The underlying assets

could be equities (shares), debt (bonds, T-bills, and notes), currencies, and even indices of

these various assets, such as the Nifty 50 Index. Derivatives derive their names from their

respective underlying asset. Thus if a derivative¶s underlying asset is equity, it is called

equity derivative and so on. Derivatives can be traded either on a regulated exchange, such as

the NSE or off the exchanges, i.e., directly between the different parties, which is called

³over-the-counter´ (OTC) trading. (In India only exchange traded equity derivatives are

permitted under the law.) The basic purpose of derivatives is to transfer the price risk

(inherent in fluctuations of the asset prices) from one party to another; they facilitate the

allocation of risk to those who are willing to take it. In so doing, derivatives help mitigate the

risk arising from the future uncertainty of prices. For example, on November 1, 2010 a rice

farmer may wish to sell his harvest at a future date (say January 1, 2011) for a pre-determined

fixed price to eliminate the risk of change in prices by that date. Such a transaction is an

example of a derivatives contract. The price of this derivative is driven by the spot price of

rice which is the "underlying".

Origin of derivatives

While trading in derivatives products has grown tremendously in recent times,

earliest evidence of these types of instruments can be traced back to ancient Greec

Even though derivatives have been in existence in some form or the other since ancient times,

the advent of modern day derivatives contracts is attributed to farmers¶ need to protect

themselves against a decline in crop prices due to various economic and environmental

factors. Thus, derivatives contracts initially developed in commodities. The first ³futures´

contracts can be traced to the Yodoya rice market in Osaka, Japan around 1650. The

farmers were afraid of rice prices falling in the future at the time of harvesting. To lock in a

price (that is, to sell the rice at a predetermined fixed price in the future), the farmers

entered into contracts with the buyers. These were evidently standardized contracts, much

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 2/43

Understanding of financial derivatives

2

like today¶s futures contracts.

In 1848, the Chicago Board of Trade (CBOT) was established to facilitate trading of

forward contracts on various commodities. From then on, futures contracts on commodities

have remained more or less in the same form, as we know them today.

While the basics of derivatives are the same for all assets such as equities, bonds,

currencies, and commodities, we will focus on derivatives in the equity markets and all

examples that we discuss will use stocks and index (basket of stocks).

Derivatives in India

In India, derivatives markets have been functioning since the nineteenth cen

with organized trading in cotton through the establishment of the Cotton Trade Association in

1875. Derivatives, as exchange traded financial instruments were introduced in India in

June 2000. The National Stock Exchange (NSE) is the largest exchange in India in

derivatives, trading in various derivatives contracts. The first contract to be launched on

NSE was the Nifty 50 index futures contract. In a span of one and a half years after the

introduction of index futures, index options, stock options and stock futures were also

introduced in the derivatives segment for trading. NSE¶s equity derivatives segment is called

the Futures & Options Segment or F&O Segment. NSE also trades in Currency and Interest

Rate Futures contracts under a separate segment.

A series of reforms in the financial markets paved way for the development of exchange-

traded equity derivatives markets in India. In 1993, the NSE was established as an electronic,

national exchange and it started operations in 1994. It improved the efficiency and

transparency of the stock markets by offering a fully automated screen-based trading

system with real-time price dissemination. A report on exchange traded derivatives, by the

L.C. Gupta Committee, set up by the Securities and Exchange Board of India (SEBI),

recommended a phased introduction of derivatives instruments with bi-level regulation

(i.e., self-regulation by exchanges, with SEBI providing the overall regulatory and

supervisory role). Another report, by the J.R. Varma Committee in 1998, worked out the

various operational details such as margining and risk management systems for these

instruments. In 1999, the Securities Contracts (Regulation) Act of 1956, or SC(R)A, was

amended so that derivatives could be declared as ³securities .́ This allowed the regulatory

framework for trading securities, to be extended to derivatives. The Act considers

derivatives on equities to be legal and valid, but only if they are traded on exchanges.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 3/43

Understanding of financial derivatives

3

The Securities Contracts (Regulation) Act, 1956 defines "derivatives" to include:

i. A security derived from a debt instrument, share, loan whether secured or unsecured,

risk instrument, or contract for differences or any other form of security.

ii. A contract which derives its value from the prices, or index of pr

underlying securities.

At present, the equity derivatives market is the most active derivatives market in India.

Trading volumes in equity derivatives are, on an average, more than three and a half times the

trading volumes in the cash equity markets.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 4/43

Understanding of financial derivatives

4

CHAPTER 2

NEED AND USE OF DERIVATIVES

A. NEED FOR DERIVATIVES

Diverse situations in the market make the need for derivatives in the investment ring. Before

investing one has to analyze the situation and look for the reason for choosing derivatives as

an investment option. This is an important step to be taken and hence requires attention.

i. FUND MANAGEMENT

The question of effective utilization of funds is foremost in the mind of various investors.

This is because there is a certain cost attached to the funds that are worth something for

people. This cost has to be borne by the person who is using the funds and hence the main

mantra in the financial markets is to free up the funds as fast as possible and use them to earn

a higher rate of return. This will ensure that the funds have a better use which in turn makes

the entire assets available with the investor effective.

A similar situation in a spot market can be costly, where payment has to be made for

everything bought and sold for those looking at a quick turnover and movement. Derivatives

on the other hand provide an option where one is able to take the required position using the

same amount of funds. This can meet a larger objective but at the same time the risk involved

in the investment will also increase. The investment is also highly liquid and the position can

be changed quickly as the need arises.

ii. LEVERAGING

One of the biggest benefits of using derivatives is that one can leverage on the existing

resources available with a person. If earlier a person could buy just a certain amount of

investments with the given funds, now the amount can be multiplied by a few times by use of

derivatives.

This enables a person to ensure that he is able to take a larger position in the markets even

with the same amount of funds. This can be a factor that can help scale up the operation of

the person or entity and result in a much larger activity. If these were not present then the

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 5/43

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 6/43

Understanding of financial derivatives

6

derivative instruments that provide the additional choices for the players in order to achieve

their financial objectives.

These objectives can be very wide and they can be spread across a large number of areas but

while this is being achieved it is important to look at the route that is being used in the

process. This is the reason why the role of derivatives assumes importance, as they are able to

ensure that a lot of the targets that people have set before their investments are achieved in a

manner that they feel comfortable with. Derivatives provide the necessary additional choices

for people and hence a route that is needed under these circumstances.

vi. DYNAMIC NATURE

The entire area of derivatives is dynamic in nature and this is probably one of the main points

that separate the route from all others that are present in the market. With various other

investment routes there are only a certain objectives that can be achieved in terms of the

investment and the manner of the investment being conducted.

This is not the case of derivative where the canvas is very wide. Due to this feature there are a

lot more options that can be achieved using the route of derivatives. The most important thing

is that when derivatives are used there is also the choice for a person to create a structure that

will be completely different from what is on offer in the menu. By using various strategies

there can be a lot of dynamic positions that will come into play depending upon the situation.

This increases the need for such an instrument because it is the route that will help in

achieving the dynamism that is expected.

vii. CREATIVITY

Derivatives are a route to increase the creativity in a team or among members because this

leaves a wide arena for people in order to ensure that they are able to make the best out of the

situation. With the instruments in front of them people are encouraged to create structures as

well as positions that will result in an overall improvement of the financial situation. People

in the area consider this best as it enables a lot of them to be creative in their efforts and make

the best use of the situation.

This kind of creativity is also very good from the point of view of keeping employees happy

and using them effectively. This also provides a lot of financial benefits in terms of either

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 7/43

Understanding of financial derivatives

7

savings or additional earnings for the entity and also enables people to realize the potential

that they have.

B. USE OF DERIVATIVES

There are various uses of derivatives depending upon the conditions under which they

operate. Hence, there has to be a clear objective about the way in which these instruments are

used. While there is a need for derivatives in several conditions the use of the derivatives will

look at a more practical aspect of how these instruments are actually put to use by the people

in their daily work.

i. NORMAL INVESTING

Many people think that the derivatives are just another route for investment and hence are

often used as a normal way of investing. Many of them consider derivatives as a means in

which they can achieve their investment objective.

The impact of such a move can have varied results depending upon the use of the instrument.

But people have different needs and hence they will be comfortable with a certain way of

working. There are people who consider derivatives to be a normal way of taking the required

risk and hence it becomes a simple way in which the investment can take place. This

becomes a comfortable way to invest and complete the investment requirements.

ii. USE AR BITRAGE OPPORTUNITIES

Often there are opportunities in the form of arbitrage or some other gain that looks very

evident. The best way to benefit from such a situation is to take a certain position that will

result in a larger gain occurring to the person if the situation develops as per the expectation.

Derivatives are the route that will help in making use of such opportunities and making a nice

handsome gain out of the situation. This is crucial because the window of opportunity in

several cases will not remain outstanding for a long point of time and hence it has to be

exploited quickly. This will be done using the route of derivatives, which will also push upthe risk in the transaction because the loss can be as severe.

iii. DEPLOY EXTRA FUNDS

There are several people who have a large portfolio but do not know what to do with the

funds. There is a large amount available with them and hence they are always on the lookout

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 8/43

Understanding of financial derivatives

8

for several opportunities or areas where they can deploy the necessary funds and make

investments just to keep the funds moving around.

For this category of people the route of derivatives is a very good option because it meets

several of the requirements that they have. There is some action that always takes place in the

derivatives market and hence money is always rolling with returns coming at regular

intervals. While many would disagree with this kind of expectation, this method of investing

is very useful for those who love making some extra money and hence a loss in the area will

also have not much impact. Though the loss might be inevitable, extra funds will find a good

alternative use, which is considered as an asset by several people.

iv. ADDITIONAL POSITIONS

Often the route of derivatives is used for the purpose of taking additional position in the

market. There are always some investments that are lying around and if these are used in

conjunction with derivative investments then it can result in an additional position that is

possible using the available sum of money. If this is done in the right manner then the impact

of this can be contained.

Such additional positions might not always be a good option but their use can be very

effective under certain conditions. Keeping the risk factor in mind at all times is very

important when derivatives are used in different arenas.

v. SPECULATION

This is probably the biggest use of derivatives present in various markets across the world.

For a normal investor this is not the way to use derivatives because it can result in a large

impact if things do not work out as expected. Those who can afford to lose money can use

derivatives in this manner and satisfy their requirements.

Speculation is done in order to garner large gains from a certain expectation but this pushes

up the risk element quite high. Due to this factor it might not be effective for everyone in themanner that was expected. However, a very large percentage of those using derivatives have

speculation at the top of their list as the purpose for using this route.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 9/43

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 10/43

Understanding of financial derivatives

10

Any investor can trade into the derivatives based on equities and hence they are quite popular

across the world. A lot of trading takes place on various exchanges across the world in equity

derivatives and this allows for higher risk but also often higher returns for investors.

ii. DEBT

There are various types of debt instruments that are present in the world of finance. More and

more variants are entering the market depending upon the requirement of various customers.

For various companies the need for funds from the debt route is one of the ways in which

they can meet their requirement of finance.

The more complicated version of the entire capital structure is created using debt derivatives

and hence there are various ways in which new instruments are created using the derivatives

route. The presence of derivatives on the debt side means that here the instruments are

created where the needs of funds are met for the required time duration and then the resulting

money is raised. However, the repayment and other details often related to the conversion of

the instruments in other forms takes place through the working of the derivatives.

Funds are required at specific point of time and these can then be utilized for the purpose of

business and is possible by using debt derivatives. There are various additional conditions

that have to be met including maintenance of the strength of the capital structure of the

enterprise and so on. All this can be done with the help of derivatives.

iii. FOREIGN EXCHANGE

The foreign exchange area has a well-developed market and there is a lot of trading that takes

place in the foreign exchange markets across the world. The most developed part of the

foreign exchange market relates to derivatives because of the fact that a lot of demand for the

exchange takes place in the future.

There is the spot market where the transaction takes place at this point of time and the entiretransaction is completed at this stage itself. However, a lot of demand for foreign exchange

arises at a stage in the future because a lot of demand takes place at some time that is there in

the future.

This gives the rise for derivatives in order to protect the position of the entity that is

undertaking the transaction. In the world of international business where large deals

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 11/43

Understanding of financial derivatives

11

regarding trade as well as purchase and sale of goods and products take place there will be

large settlement in the future. When the transactions are across countries the factor of foreign

exchange comes into the picture and this can be a very disruptive force. If the exchange rate

moves against the expectations then there can be a financial situation that is completely

opposite to what has been expected and this can result in financial difficulties.

Here is where derivatives help protect the position of a party with regard to the entire

transaction and hence they are extremely popular. By undertaking a certain exercise one can

know the extent of the risk that is being taken and what will be the cost for the entire

transaction. This has to be considered because the entire world of foreign exchange moves

through the use of derivatives.

The foreign exchange market is such that a very small change can have a very large impact

because the transaction value is extremely high. The use of derivatives in the nature of

options, forwards, futures and swaps, which are the most preferred routes ensure that the

objective of the entire exercise is met. This makes the use of derivatives one of the most

common routes to be adopted in this field.

iv. COMMODITIES

There is the route of various commodities that are traded on the commodity exchanges across

the world. The commodities are varied in nature and can range from something like oil to

sugar and from wheat to even oilseeds. This kind of variation means that there are a lot of

factors that are at play in the entire thing.

The first is that there are different players in each of the segment and hence a lot of factors

come into play. On one hand are the various farmers who produce the various commodities

who would want a good price for the product. If the derivatives market was not available then

they would be subject to the market position and this can mean serious trouble because in

case of an oversupply, the price fall can prove to be disastrous. In addition, there are several

areas where there are middlemen who pocket a large part of the entire earnings from thecommodity which can leave the original farmers bankrupt.

On the other side are the various dealers who also supply same things to the market and often

to the end consumer. They are interested in ensuring that there is a continuous supply of the

product especially when they are required. Due to this there is the situation where they have

to ensure that there is some reliability in the system that they have created and this will be

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 12/43

Understanding of financial derivatives

12

possible only through the route of derivatives.

The position of supply and demand is met through the route of derivatives and they are the

best way available for the purpose of ensuring that the needs across the world are met. There

are several commodities that are used in the production of various other items and hence if

there has to be some activity then there is a need to lock into the supply of these items at the

specified prices. In such a situation it is the derivatives that come in the picture.

The derivatives are also a route that gives an indication about the position in a particular

commodity and hence they would look at the position on this front and then take the

necessary decision about the way they should approach the issue accordingly.

v. MUTUAL FUNDS

One of the best areas where derivatives are used is in case of mutual funds that can be based

on a large number of things. Mutual funds are a derivative product because the value of the

fund depends upon the value of a particular asset. While there are mutual funds in areas

related to equity, debt and various commodities there is also an additional area to be

considered.

This is the area of real estate and there are a lot of funds whose value depends upon the

position of the real estate and the various movements of the price. Due to this reason this also

becomes an area that will be covered by derivatives. Often it is impossible for an investor toinvest small amounts in the real estate sector, however, there are a lot of people who would

like to ensure that they are able to get the best returns out of the area.

This is possible when there are mutual funds that are related to the area of real estate. The

funds will be invested in real estate and then the change in the value will be reflected in the

returns of the fund. This is a good opportunity for investors to ensure that they are able to get

the maximum benefit from the entire route.

If there were no derivatives that were present in this area then it would not be possible for aninvestor to ensure that they are able to benefit from the gain that would occur for investments

in this area. There are specific features of such funds and hence they have to be treated in a

separate manner. This is the reason why different types of funds have to be considered in a

different manner. There has to be a mode of operation of these funds and hence they have to

be treated differently.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 13/43

Understanding of financial derivatives

13

In addition, mutual funds themselves use derivative instruments for a whole host of purposes

and across various schemes. Now there are specific schemes present in the market that will

invest in derivative instruments to achieve the desired objectives.

vi. STOCK AND INDEX DERIVATIVES

Derivatives in the equity markets have really taken off and there are a lot of investors who are

looking at trading through these instruments. The derivatives that are present in the equity

markets of the country are mainly of two types and hence they signify the importance that is

given to the different types of derivatives. The investors and those who trade are also now

familiar with these derivatives and it makes it easy for them to actually understand how this

operates and what they actually mean for them as an investor. The derivatives in the market

are based upon these two areas.

a) Stock derivatives

Here the derivatives are based upon individual stocks and due to this factor they are linked to

the prices of the stock. There can thus be futures related to individual stocks like Reliance or

Infosys. Similarly, there can also be options on the same stocks and hence their movement

will be linked to the movement of the stock in the cash market. Stock derivatives enables a

person to undertake activity based on individual stocks and hence the view of the person on

the particular stock can then be played out using the various options and due to this reason

they are also quite popular. The main advantage of these instruments are that they enable a

person to gain from their view regarding a particular share in a higher manner than what they

would have experience in normal terms.

b) Index derivatives

These are opposite to what stock derivatives stand for because here a specified index can be

at the center of the entire range of activities of the derivatives trading. Instead of a particular

stock here the person takes a view on the index as a whole and in many cases this refers to the

market as a whole. Here the items covered are much wider and hence there is a need to

exercise due diligence and care in the entire matter.

Index derivatives are very popular with all those people who would like to take a broader

view of the market and thus are able to predict overall trends in a better manner. Due to this

reason there is also an element of a general overview that is taken by those who deal in index

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 14/43

Understanding of financial derivatives

14

derivatives. Again index derivatives can be related to the futures or options on the various

indices present in the market. The two main indices, which are at the center of attention in the

Indian market, are the Sensex and the Nifty.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 15/43

Understanding of financial derivatives

15

CHAPTER 4

TERMS USED IN THE DERIVATIVES TRADING

Introduction

There are various terms that are used in the derivatives segment and one must be aware of

what they mean and how they can be used for the purpose of various types of analysis as well

as dealings. Each of them has their own separate meaning along with the use. This is a vast

field that is also developing quite fast and so one also has to be alert to the new developments

occurring in the field.

1. DERIVATIVES

Most people get confused with the main term derivatives as they are not aware about the clear

meaning of this and get confused about the operation of various instruments. Derivative in

simple words is a product whose value is derived from some other product. The basic

variable, which is the underlying can include a wide variety of areas like equity, foreign

exchange or some commodity too. There are various types of derivatives and there will be

different factors that are driving their prices. However, the way in which the underlying asset

is being impacted will also play a role in the price of the derivative

2. FORWARD CONTRACT

A forward contract is a type of derivative that is present in various markets across the world.

One of the most important features of a forward contract is that it is a customized contract

between two entities. This means that there will be a difference in the way in which different

parties will be creating the forward contract because this will be done according to the

convenience of both of them and the way in which they would like to deal. The other feature

of the contract is that the settlement will take place some day in the future and hence it isknown as a forward contract. The price for this purpose will be determined at this point of

time and the specified and pre agreed price would be applicable. Thus it provides the benefit

of undertaking transactions in the future with the details being decided at this point of time.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 16/43

Understanding of financial derivatives

16

3. FUTURES

There are different terminologies used in the derivatives market and often can create a lot of

confusion between the features of various items. Forwards and futures are two such terms

that lead to a lot of confusion. A futures contract is different from a forward contract. This is

also a contract that falls into the category of derivatives. A future is an agreement between

two parties to buy or sell a specific asset at a specific price at a specific time in the future. In

such a contract, the details of the transaction are determined at the present time and here there

will be a decision to buy or sell the asset at the price that is determined but at a time that will

come sometime in the future. For several people this might seem to be just like a forward

contract but here there will be the additional feature of the contracts being standardized and

that they are also exchange traded in nature. These are traded on the exchange and the various

details regarding the composition and the construction of the contract are fixed.

4. OPTIONS

An option is another type of derivative contract that is very popular in the investment world.

An option gives the right but not the obligation to do a certain thing as laid out in the contract

and this is a great benefit because the person can complete the transaction only when they

feel that this is beneficial to them. If they feel that the situation is not in their favour then

there is no need for them to put through the transaction. There are two types of options- call

option and put option. The former gives the right but not an obligation to buy a certain assetand the latter gives a right but not the obligation to sell a certain asset.

5. WARRANTS

In the markets there are several types of instruments that are present and floating all around.

A warrant is one such offering, which is in the nature of an option. A warrant in simple words

is an instrument that gives the right to a person to buy some assets at a certain price within a

specified time limit. A lot of investors will have witnessed warrants that come along with

some share offerings and they offer additional shares at a certain price within a specified time

period. These are often very useful in providing the required benefit for the targeted group

where the benefit comes at a date in the future. Again based upon the actual situation the

person holding the warrant will decide upon exercising the warrant.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 17/43

Understanding of financial derivatives

17

6. SWAPS

Swaps are a common derivative instrument used in the debt market. These are agreements

between two parties and is mostly a private agreement. The agreement is to exchange cash

flows at some time in the future according to a decided calculation or a formula. There are

various types of swaps that are used in the market. Under an interest rate swap the cash flow

from two interest flows are swapped while in currency swap both the principal as well as the

interest are swapped. Thus here there is a different currency that can also come into the

picture.

7. EXCHANGE TRADED DERIVATIVES

As the name suggests these are derivative products that are traded on an exchange. There are

various exchanges related to different assets and on these exchanges when there are

derivatives traded they are known as exchange traded derivatives. One of the most important

features that will distinguish a derivative as an exchange traded one is the fact that these will

be of a specific size and will be conducted in a specific manner. Thus everything related to

the construction and the trading of the derivative is known and fixed and this makes them

standard in several respects. Within this category there can be several types of derivatives

that are created and traded.

8. OTC DERIVATIVES

OTC derivatives are known as over the counter derivatives. The most important feature of

this derivative is that they are not traded on any exchange but are traded over the counter.

This means that one does not have to go through the exchange mechanism to deal with the

derivatives but two parties can by themselves sit down and decide to deal in the transaction

without any additional presence or the completion of any more details. The most important

factor here is that there is a large amount of flexibility in creating and dealing in the

instruments and hence this is a big advantage as far as the various parties who are involved

are concerned.

9. INDEX

There are various indices that are present in the market for various areas. An index is a

number that will measure and reflect the change in a set of values over a period of time. This

is a very easy way of looking at the various areas and then knowing the kind of change that

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 18/43

Understanding of financial derivatives

18

has occurred in the area. When there is an index one can also compare the change in the

values witnessed over a period of time.

10. INDEX BASED DERIVATIVES

Each derivative requires an underlying asset to be covered and based on which the existing

prices will be determined. When a particular derivate is based on an index then it is known as

an index based derivative. The movement of the index that is taking place will determine the

price of such a derivative and hence it is linked to the performance of the index. Since an

index is often the best way in which a person can track what is happening in a particular area

this becomes a good way to ensure that the investor can also get the best out of the situation.

11. EXCHANGE TRADED FUNDS

When an index is mentioned exchange traded funds cannot be far behind. These are

instruments that are mutual funds but the only point of difference is that they are also traded

during the day on the exchanges. These funds are usually based on a particular index and

hence they will track the movement of the index and perform accordingly. The advantage

here is that the investor is able to track the investment better and it also gives them a good

way of exiting the investment when required. The features of both a mutual fund as well as a

stock makes it an interesting concept for a lot of investors.

12. COST OF CARRY

The spot price and the futures price shows a difference at different points of time and this can

be explained by the cost of carry. The cost of carry is nothing but the storage cost plus the

interest cost that is required to be paid for the purpose of financing the asset. The figure will

also have to account for the income earned on the asset and this will be reduced from the cost

so arrived at. This will give an indication of the extent of the expense that is incurred in

holding the futures position on account of these two aspects.

13. IMPLIED VOLATILITY

This is a measure of how volatile the particular stock or asset is and it is useful in the process

of finding out the cost of derivative instruments. The logic is that the higher the volatility, the

larger is the chance that the various targets would be achieved and hence there has to be a

careful watch on this figure for the kind of indications and signals that it sends out because

proper interpretation is very important.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 19/43

Understanding of financial derivatives

19

CHAPTER 5

FORWARDS, FUTURES AND OPTIONS

There are various types of derivatives traded on exchanges across the world. They range

from the very simple to the most complex products. The following are the three basic forms of

derivatives, which are the building blocks for many complex derivatives instruments:

1. Forwards

2. Futures

3. Options

1. FORWARDS

A forward contract or simply a forward is a contract between two parties to buy or sell an

asset at a certain future date for a certain price that is pre-decided on the date of the contract.

The future date is referred to as expiry date and the pre-decided price is referred to as

Forward Price. It may be noted that Forwards are private contracts and their terms are

determined by the parties involved.

A forward is thus an agreement between two parties in which one party, the buyer, enters

into an agreement with the other party, the seller that he would buy from the seller an

underlying asset on the expiry date at the forward price. Therefore, it is a commitment by

both the parties to engage in a transaction at a later date with the price set in advance. This

is different from a spot market contract, which involves immediate payment and

immediate transfer of asset.

The party that agrees to buy the asset on a future date is referred to as a long investor and

is said to have a long position. Similarly the party that agrees to sell the asset in a future

date is referred to as a short investor and is said to have a short position. The price agreed

upon is called the delivery price or the Forward Price.

Forward contracts are traded only in Over the Counter (OTC) market and not

exchanges. OTC market is a private market where individuals/institutions can trade

through negotiations on a one to one basis.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 20/43

Understanding of financial derivatives

20

There are several features that are present in the construction of a forward contract and each

of these will vary with each of the forward contracts being constructed. Here is a look at

several of the factors that will vary with respect to a forward contract.

CONTRACT SIZE

The contract size refers to the amount or the extent of the asset that make up each contract for

a particular asset. This is a prerequisite for every derivative contract because only when the

contract size is known will the agreement be completed. For example, if one is looking to

trade in a contract size in shares then it might be 500 shares or 1000 shares or so on. When a

particular contract is built on a customized basis then it will include the underlying asset in

the quantity that is required for the purpose of the transaction and no more. This also gives

the required amount of flexibility in putting together the transaction. Thus, for example, if there is a requirement for 12 kg of gold for a particular entity and a forward contract is to be

entered into then it will be undertaken for this specific contract size and hence will form the

base of the entire transaction.

EXPIRY DATE

The forward contract has to expire on a particular date because this is the time when the

settlement between the two parties will take place. However the good part is that the expiry

date can be fixed as the one where both the parties are comfortable with the confirmation and

the completion of the contract. There is no compulsion by some outside party in the fixing of

a particular date as the expiry date. The expiry date can be fixed as a particular day even

when it might not be possible in some other ways because there are no restrictions that will

be applicable. The key part of the entire transaction is that both the parties to the contract

have to agree upon the fix the necessary expiry date. As a matter of convenience this can also

be taken to be a round figure like 3 months or 6 months or so on.

ASSET TYPE

If there is a derivative contract that is taking place through the route of an exchange then one

of the major things that will seem like a restriction is the type of assets. A forward contract

does not take place through the exchange and this creates another benefit in terms of the asset

that can be selected for the purpose. In case of a forward contract as this restriction of only

specific types of assets is not present the two parties may decide to trade in an asset where

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 21/43

Understanding of financial derivatives

21

they want to make a deal. This increases the scope of the various transactions that can take

place through this medium. The good part of this type of benefit is that a person will be able

to select the asset that they want to trade in or enter into a forward contract and then be able

to execute it in an effective manner.

ASSET QUALITY

One of the major factors that often create a situation of low liquidity is that the quality of the

asset being traded does not match with the specifications laid down in the exchange or at

some other place. In case of a forward even if the asset quality is of a slightly different type

then this can be traded because the contract will be created in such a manner that the asset

quality is taken care of by the other details in the contract. This is a very good way of

ensuring that the right method is adopted in conducting the transaction. It also ensure that the

right value is available for the contract and the person who are transacting in the contract

know precisely what they are doing and the manner in which they will be able to deal with

the situation.

SETTLEMENT OF FORWARD CONTRACTS

When a forward contract expires, there are two alternate arrangements possible to settle

the obligation of the parties: physical settlement and cash settlement. Both types of

settlements happen on the expiry date and are given below.

Physical Settlement

A forward contract can be settled by the physical delivery of the underlying asset by a

short investor (i.e. the seller) to the long investor (i.e. the buyer) and the payment of the

agreed forward price by the buyer to the seller on the agreed settlement date. The

following example will help us understand the physical settlement process.

Illustration

Consider two parties (A and B) enter into a forward contract on 1 August, 2009 where, Aagrees to deliver 1000 stocks of Unitech to B, at a price of Rs. 100 per share, on 29

thAugust,

2009 (the expiry date). In this contract, A, who has committed to sell 1000 stocks of

Unitech at Rs. 100 per share on 29th

August, 2009 has a short position and B, who has

committed to buy 1000 stocks at Rs. 100 per share is said to have a long position.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 22/43

Understanding of financial derivatives

22

In case of physical settlement, on 29th August, 2009 (expiry date), A has to actually deliver

1000 Unitech shares to B and B has to pay the price (1000 * Rs. 100 = Rs. 10,000) to A.

In case A does not have 1000 shares to deliver on 29th August, 2009, he has to purchase it

from the spot market and then deliver the stocks to B.

On the expiry date the profit/loss for each party depends on the settlement price, that is, the

closing price in the spot market on 29th

August, 2009. The closing price on any given day is

the weighted average price of the underlying during the last half an hour of trading in

that day. Depending on the closing price, three different scenarios of profit/loss

possible for each party. They are as follows:

Scenario I. Closing spot price on 29 August, 2009 (S T) is greater than the Forward price (FT)

Assume that the closing price of Unitech on the settlement date 29 August, 2009 is Rs.

105. Since the short investor has sold Unitech at Rs. 100 in the Forward market on 1

August, 2009, he can buy 1000 Unitech shares at Rs.105 from the market and deliver

them to the long investor. Therefore the person who has a short position makes a loss of

(100 - 105) X 1000 = Rs. 5000. If the long investor sells the shares in the spot market

immediately after receiving them, he would make an equivalent profit of (105 - 100) X

1000 = Rs. 5000.

Scenario II. Closing Spot price on 29 August (S T), 2009 is the same as the Forward price

(FT)

The short seller will buy the stock from the market at Rs.100 and give it to the long

investor. As the settlement price is same as the Forward price, neither party will gain or

lose anything.

Scenario III. Closing Spot price (ST) on 29 August is less than the futures price (FT)

Assume that the closing price of Unitech on 29 August, 2009 is Rs. 95. The short investor,

who has sold Unitech at Rs. 100 in the Forward market on 1 August, 2009, will buy thestock from the market at Rs. 95 and deliver it to the long investor. Therefore the person

who has a short position would make a profit of (100 - 95) X 1000 = Rs. 5000 and the

person who has long position in the contract will lose an equivalent amount (Rs. 5000), if

he sells the shares in the spot market immediately after receiving them.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 23/43

Understanding of financial derivatives

23

The main disadvantage of physical settlement is that it results in huge transactio

in terms of actual purchase of securities by the party holding a short position (in this case

A) and transfer of the security to the party in the long position (in this case B). Further, if

the party in the long position is actually not interested in holding the security, then she

will have to incur further transaction cost in disposing off the security. An alternative way

of settlement, which helps in minimizing this cost, is through cash settlement.

Cash Settlement

Cash settlement does not involve actual delivery or receipt of the security. Each party

either pays (receives) cash equal to the net loss (profit) arising out of their respective position

in the contract. So, in case of Scenario I mentioned above, where the spot price at the

expiry date (ST) was greater than the forward price (FT), the party with the short position

will have to pay an amount equivalent to the net loss to the part y at the long position. In

our example, A will simply pay Rs. 5000 to B on the expiry date. The opposite is the case in

Scenario (III), when ST < FT. The long party will be at a loss and have to pay an amount

equivalent to the net loss to the short party. In our example, B will have to pay Rs. 5000 to A

on the expiry date. In case of Scenario (II) where ST = FT, there is no need for any party to

pay anything to the other party.

Please note that the profit and loss position in case of physical settlement and cash

settlement is the same except for the transaction costs which is involved in the physicalsettlement.

DEFAULT RISK IN FORWARD CONTRACTS

A drawback of forward contracts is that they are subject to default risk. Regardless of

whether the contract is for physical or cash settlement, there exists a potential for one party

to default, i.e. not honor the contract. It could be either the buyer or the seller. This results

in the other party suffering a loss. This risk of making losses due to any of the two parties

defaulting is known as counter party risk. The main reason behind such risk is the absence

of any mediator between the parties, who could have undertaken the task of ensu

that both the parties fulfill their obligations arising out of the contract. Default risk is

also referred to as counter party risk or credit risk.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 24/43

Understanding of financial derivatives

24

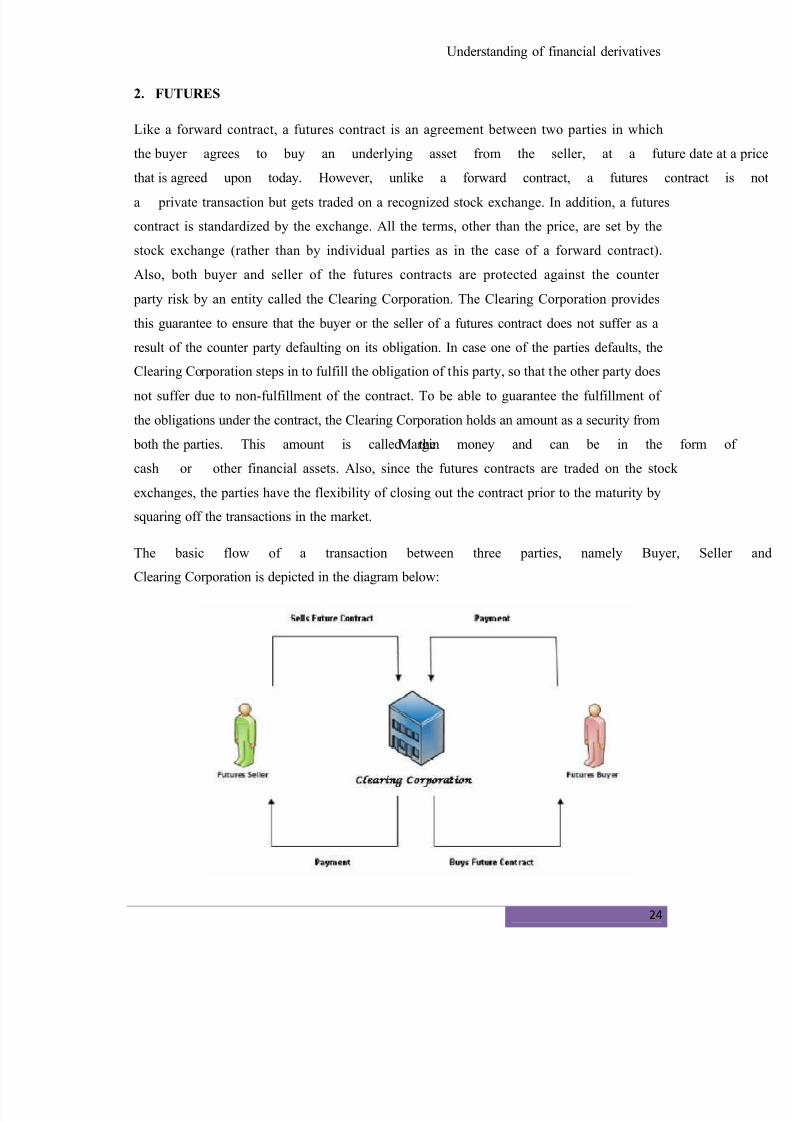

2. FUTURES

Like a forward contract, a futures contract is an agreement between two parties in which

the buyer agrees to buy an underlying asset from the seller, at a future date at

that is agreed upon today. However, unlike a forward contract, a futures contract i

a private transaction but gets traded on a recognized stock exchange. In addition, a futures

contract is standardized by the exchange. All the terms, other than the price, are set by the

stock exchange (rather than by individual parties as in the case of a forward contract).

Also, both buyer and seller of the futures contracts are protected against the counter

party risk by an entity called the Clearing Corporation. The Clearing Corporation provides

this guarantee to ensure that the buyer or the seller of a futures contract does not suffer as a

result of the counter party defaulting on its obligation. In case one of the parties defaults, the

Clearing Corporation steps in to fulfill the obligation of this party, so that the other party does

not suffer due to non-fulfillment of the contract. To be able to guarantee the fulfillment of

the obligations under the contract, the Clearing Corporation holds an amount as a security from

both the parties. This amount is called theMargin money and can be in the form o

cash or other financial assets. Also, since the futures contracts are traded on the stock

exchanges, the parties have the flexibility of closing out the contract prior to the maturity by

squaring off the transactions in the market.

The basic flow of a transaction between three parties, namely Buyer, Seller

Clearing Corporation is depicted in the diagram below:

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 25/43

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 26/43

Understanding of financial derivatives

26

DATE OF EXPIRY

The futures contract which looks at buying or selling an asset at a certain time in the future

also ensures that the date of expiry is specified and this is fixed on the exchange. Thus this

eliminates any disputes or confusion that often arises when a direct deal is made between two

parties as in this case the date of expiry is clearly outlined and hence is the date, which has to

be followed. In case of derivatives in stocks on the Indian exchange, the date of expiry is the

last Thursday of the month.

MONTH OF DELIVERY

There are also specified months in which the entire transaction will take place hence the date

of expiry will also be accompanied by the details of the month of making the delivery. This is

a significant factor because with this detail the entire working of the contract is very clear and

eliminates any chance of making a wrong estimate or creating any confusion.

PRICE QUOTATION

The price quotation is also specified so that the various price changes that occur in the futures

contract will take place as per the expectations. The details will be laid out regarding the

quantum of the price change that will be permitted along with the units of the price. This will

ensure that anyone dealing with the futures contract will know very clearly the kind of price

change that is possible.

SETTLEMENT

The settlement of the entire transaction is very important because the method and the manner

of settlement hold an important place in derivatives trading. There are two ways of settlement

that are possible. The first is a cash settlement and the second one is a settlement by delivery.

Under the cash settlement the entire transaction is closed on the specific day considering the

decided price and the position is settled by cash. On the other hand when it comes to delivery

there will be actual delivery of the asset at the time of settlement and hence this will requirethe presence of several other aspects of infrastructure that will have to be present.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 27/43

Understanding of financial derivatives

27

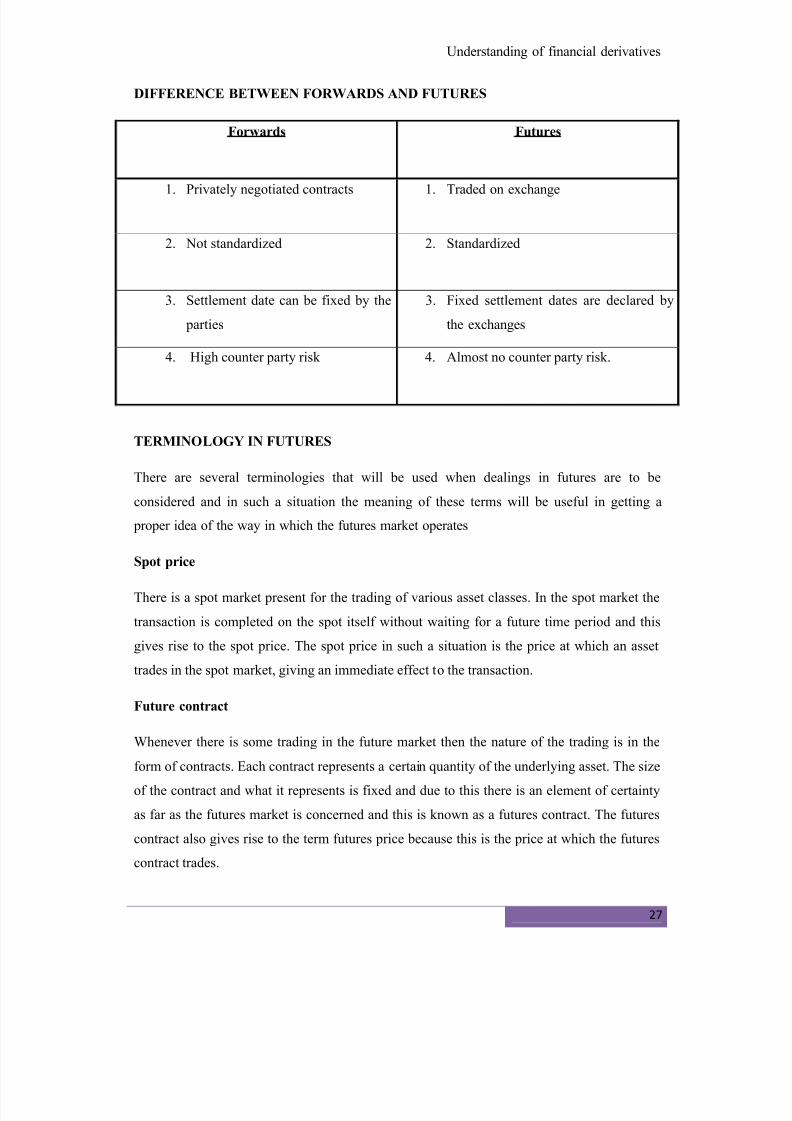

DIFFERENCE BETWEEN FORWARDS AND FUTURES

Forwards Futures

1. Privately negotiated contracts 1. Traded on exchange

2. Not standardized 2. Standardized

3. Settlement date can be fixed by the

parties

3. Fixed settlement dates are declared by

the exchanges

4. High counter party risk 4. Almost no counter party risk.

TERMINOLOGY IN FUTURES

There are several terminologies that will be used when dealings in futures are to be

considered and in such a situation the meaning of these terms will be useful in getting a

proper idea of the way in which the futures market operates

Spot price

There is a spot market present for the trading of various asset classes. In the spot market the

transaction is completed on the spot itself without waiting for a future time period and this

gives rise to the spot price. The spot price in such a situation is the price at which an asset

trades in the spot market, giving an immediate effect to the transaction.

Future contract

Whenever there is some trading in the future market then the nature of the trading is in the

form of contracts. Each contract represents a certain quantity of the underlying asset. The size

of the contract and what it represents is fixed and due to this there is an element of certainty

as far as the futures market is concerned and this is known as a futures contract. The futures

contract also gives rise to the term futures price because this is the price at which the futures

contract trades.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 28/43

Understanding of financial derivatives

28

Expiry date

This is the date on which the futures contract expires. It is specified in the futures contract

and it denotes the last date till which the particular contract will be traded. After the expiry

date there will be no further trading in the contract and this contract itself will cease to exist.

Due to this reason the expiry date is important as it seeks to highlight the extent of the life of

the contract

Futures contract cycle

The period for which the futures contract is in existence is called the contract cycle. There

can be different time periods for which a contract cycle may be on. This can be a month or it

can be three months or also as per the situation. However the contract cycle in existence from

a particular day will also be considered important because of the fact that it will give an idea

as to when the contract cycle expires.

Basis

When it comes to the area of financial futures the term basis refers to the futures price less the

spot price. The basis will be different for various situations and it will also keep changing

however, the general trend of the basis has to be noted because this is an important factor. In

most cases the futures price exceeds the spot price and hence the basis will be positive

however the situation can be different too and hence this would also have to be tackled whenthe situation arises

Cost of carry

There is a reason why there is a difference between the futures price and the spot price and

this can be understood using the concept of cost of carry. The cost here measures the storage

cost plus the interest that will be incurred in order to finance the asset. In this calculation the

amount earned would be reduced from this figure to arrive at the actual cost of carry. One has

to understand that due to the fact that there is some storage cost plus interest the futures pricehas to be higher than the spot one

Initial margin

There are different types of margin that are present in the process of investing in futures.

These margins are useful for the purpose of ensuring that the risk in the entire transaction is

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 29/43

Understanding of financial derivatives

29

covered. Due to this reason the amounts are collected under various heads known as margins.

One of them is called the initial margin. This is the figure that has to be deposited in the

futures account on entering the transaction and is hence known as the initial margin.

Mark to market margin

This is the margin requirement that most people would be familiar with. In the futures

process every day the outstanding position of the investor is marked to the market price and

depending upon the movement the investor either has to pay more margin or their margin

requirement is reduced. Due to this factor there is the mark to market margin, which will take

care of the fact that the changes in the price in the asset will be reflected regularly on a daily

basis.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 30/43

Understanding of financial derivatives

30

3. OPTIONS

Like forwards and futures, options are derivative instruments that provide the opportunity

to buy or sell an underlying asset on a future date. An option is a derivative contract

between a buyer and a seller, where one party (say First Party) gives to the other (say

Second Party) the right, but not the obligation, to buy from (or sell to) the First Party the

underlying asset on or before a specific day at an agreed -upon price. In return for granting

the option, the party granting the option collects a payment from the other party. This

payment collected is called the ³premium´ or price of the option.

The right to buy or sell is held by the ³option buyer´ (also called the option holder); the

party granting the right is t he ³option seller´ or ³option writer´. Unlike forwards and futures

contracts, options require a cash payment (called the premium) upfront from the option buyer

to the option seller. This payment is called option premium or option price. Options can be

traded either on the stock exchange or in over the counter (OTC) markets. Options

traded on the exchanges are backed by the Clearing Corporation thereby minimizing the

risk arising due to default by the counter parties involved. Options traded in the OTC

market however are not backed by the Clearing Corporation.

TYPES OF OPTIONS

There are various types of options that are present in the market and the investor has a choice

to select from what is put in front of them. Depending upon the circumstances and the

manner of their operation, the right type of option can be chosen for the desired transaction.

a. Call option

A call option is the right but not the obligation to buy a particular asset at a specified price on

a specified date. When such an option is purchased then it will be very clearly mentioned that

the person can buy a specified quantity of the asset at the given price on the particular day.

The idea behind buying a call option is that the person expects the price of the asset to rise in

the future. In order to profit from this price rise the person is locking himself into the cost of

the asset from this time period itself and hence the person knows that from this stage itself

that their cost will be the specific amount fixed.

If the price actually rises as expectated, the investor will gain because they have already

locked into the cost from this time period itself. In such a situation on the specified day the

person will exercise the option and enjoy the gains. However if the expected situation does

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 31/43

Understanding of financial derivatives

31

not develop then the person who has bought the option cannot exercise the option and thus

restrict the losses that would have occurred.

A good example of this is when a person buys a call option for Indian Hotels that entitles him

to 1000 shares of the company at Rs 140 at share at the end of January 2007. In this case the

investor will wait till the end of the specified period and then depending upon the share price

in the market will decide about exercising or not exercising the option. If the price is above

his cost then there is a gain available to the investor and hence they will exercise the option

however there is no obligation to actually exercise the option and hence if the price is say Rs

125 then nothing will be done and the required shares will not be bought.

b. Put option

A put option is opposite to a call option. Here the option gives the right but not the obligation

to sell a particular asset at a specified price at a specified date in the future. The put option is

a very useful tool because this can protect the gains of the investor and hence assure them a

specific price for the assets that they hold. Here on the specified date the person who has sold

the asset can complete the transaction at the specified price if they feel that this is beneficial

to them. On the other hand if they feel that they will make a loss in the process then they are

under no obligation to complete the transaction.

A put option is extremely useful in order to get a particular price for the assets that a person

has. It protects against the downside of the market because if one has bought a put option and

the market price falls after that then the buyer of the option has little cause to worry because

they are assured of the price that has been fixed under the put option. At the same time if the

situation does not work out as expected and the price actually rises then they can walk away

after letting go of the premium paid on the transaction. This is useful when one has an

expectation of a fall in the prices of an asset so that they will be able to gain from the

situation by ensuring that their sale is at a higher price.

A good example of this is the put option of Satyam Computers at Rs 550 one month down the

line. If the price of the company is Rs 650 on the particular day then the option will not be

exercised because it will result in a loss for the investor. On the other hand if the price has

dipped to say Rs 380 then the option will be exercised and hence the person will gain due to

the locking in of the sale price of the shares at that point of time.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 32/43

Understanding of financial derivatives

32

c. American option

This is another variation of the option as here the key feature is the timing of the exercise of

the option. An American option is one that can be exercised at anytime during the tenure of

the option. This feature is very important because it can help the investor make use of any

intermediate price changes that occur in the market and get the best out of the situation.

The price changes on a daily basis while the specified date in the option is at some time in the

future. Now assume that a person has bought a call option on a share for Rs 50 that would be

exercised after a period of 1 month. However after 15 days the person finds that the price of

the company has already reached Rs 75 and there is no certainty that it would stay at that

level. In such a situation the person would like to exercise the option get the shares and sell

them off so that they are able to make the difference in the transaction. This will be possible

only when the option is an American option because that enables a person to exercise it at

any time during the tenure. Here there is more flexibility for the investor because it gets them

to act according to the changing situation that will be beneficial for them.

d. European option

This is another type of option that is present in the market where the option cannot be

exercised at any time before the specified date. This takes away the benefit of exercising it if

the situation turns favourable and hence the person will have to wait till the date specified in

the option for the purpose of completing the transaction. This often acts as a disadvantage

because the person is not able to take the benefit of any situation that arises in the

intermediate period.

This is suitable for areas where there is not much intermediate activity and changes that

impact the prices significantly. Due to this factor there is no need for constant monitoring or

intervention and hence the European option will be suitable for the situation that has

developed here.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 33/43

Understanding of financial derivatives

33

TERMS USED IN OPTIONS

There are various terms that are used for the purpose of dealing in options and one needs to

be familiar with them in order to be able to understand the complete nature of the activities

that are conducted in this area.

Option holder

The person who buys the option is known as the option holder. This is the person who has

bought either a call or a put option and is the one who has the right but not the obligation to

undertake the entire transaction. It is in the hands of the option holder as to what has to be

done with respect to the option and how this is to be tackled. Hence there is an important role

to be played by the option holder when it comes to dealing in options

Option writer

The option writer is at the other end of the option transaction. For every option that is bought

by a person and this can be a put option or a call option there has to be someone else who has

to write the option. Writing an option means meeting the conditions of the option. For

example writing a call option means having to buy a particular share at a particular price and

writing a put option means having to sell a share at a certain price.

The difference between an option holder and an option writer is quite huge because of the

very basic nature of the activity. There is no right for an option writer to move away from the

requirements of the option. Thus unlike a holder they cannot say that the option will not be

honoured and completed. If they have written a call option and this is exercised then they will

have to buy the asset at the specified price. In order to compensate for this feature that they

face the option writer earns money from writing option while the option holder has to pay

money for the purpose of getting the benefit of the options.

Exercise price

The option has a price that is fixed for the purpose of the particular option. The price at which

the option will be carried out is known as the exercise price. This is the price at which the

option holder can buy or sell the asset involved in the option. It is an integral part of an option

transaction because the price for the option is a very important component that has to be

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 34/43

Understanding of financial derivatives

34

present. The exercise price is mentioned clearly at the time of entering in to the option

contract.

Expiry date

An option has a date on which the option holder has a right to buy or sell a particular asset.

This date is the time when the decision has to be taken on the option and when the option will

expiry. This date is known as the expiry date and is a very important role to play because it

determines the time period for the option. After this expiry date the option will cease to be in

operation and hence it has to be exercised by or on the expiry date.

Option exercise

When the option process leads to buying or selling of the asset as per the terms of the option

then it is said that the option has been exercised. The exercise of the option will result in a

situation where the transaction is completed. In case the option is not exercised then the

option will lapse and there will be no transaction however this does not mean that there will

be no earnings for everyone. When an option expires the option writer will get to keep the

option premium that has been collected on the writing of the option

Option premium

A lot has been said about options and the kind of benefits that they provide. The entire

transaction of getting a right but not the obligation to undertake several activities would be

there in consideration for a cost. In this situation the cost is in the form of option premium

that has to be paid by the person buying the option to the option writer. This is the cost for the

entire transaction and even if the option is not exercised there will not be the return of the

option premium

For example if a person goes to buy a call option on Infosys at Rs 2300 then there will be an

option premium that has to be paid on this transaction. In this case the figure might be Rs 50.

This results in the actual cost for the option holder to be RS 2350. If the price is above thisfigure then only will the exercise of the option become favourable. In case the option is not

exercised and the option holder walks away from the situation then the Rs 50 paid for each

share in the option contract will be the loss for the person and this on the other side of the

transaction is the income for the option writer.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 35/43

Understanding of financial derivatives

35

At the money option

In case of options there has to be a constant lookout for the position of the market price as

compared to the exercise price. This is to check for the position in case the option has to be

exercised at any point of time. In such a situation when the market price is equal to the

exercise price then in this case the option is said to be at the money. At this stage of the

option there is no loss or no profit being made by the option holder. Thus this is actually a

neutral stage for both a call as well as a put option

In the money option

An option where the option holder is making money is said to be in the money option. The

important thing is that the situation when this will happen will differ according to the nature

of the option. Again the market price and the exercise price are to be considered in

determining the position. In case of a call option when the market price is greater than the

exercise price then the option is said to be in the money. In case of a put option the situation

is reversed because when the market price is lower than the exercise price the option becomes

in the money. This means a profitable situation for the investor holding the option.

Out of the money option

There are also times when things are not going the way of the investor and the situation is

opposite to what was expected. In such a case the option becomes an out of the money

option. In this case too the nature of the position will depend upon the type of the option. In

case of a call option if the market price is less than the exercise price then the option is said to

be out of the money while in case of a put option if the market price is higher than the

exercise price then the option is said to be out of the money. For the option holder if the

option remains out of the money then at the time of expiry this will not be exercised.

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 36/43

8/7/2019 28 febuary

http://slidepdf.com/reader/full/28-febuary 37/43

Understanding of financial derivatives

37

For example, an investor holding Reliance shares may be worried about adverse future price

movements and may want to hedge the price risk. He can do so by holding a short position

in the derivatives market. The investor can go short in Reliance futures at the NSE. This

protects him from price movements in Reliance stock. In case the price of Reliance

shares falls, the investor will lose money in the shares but will make up for this loss by the

gain made in Reliance Futures. Note that a short position holder in a futures contract

makes a profit if the price of the underlying asset falls in the future. In this way, futures

contract allows an investor to manage his price risk.

Similarly, a sugar manufacturing company could hedge against any probable loss in the

future due to a fall in the prices of sugar by holding a short position in the futures/ forwards

market. If the prices of sugar fall, the company may lose on the sugar sale but the loss will

be offset by profit made in the futures contract.

Long Hedge

A long hedge involves holding a long position in the futures market. A Long

holder agrees to buy the underlying asset at the expiry date by paying the agreed futures/

forward price. This strategy is used by those who will need to acquire the underlying asset

in the future.

For example, a chocolate manufacturer who needs to acquire sugar in the future will be

worried about any loss that may arise if the price of sugar increases in the future. To hedge

against this risk, the chocolate manufacturer can hold a long position in the sugar futures.

If the price of sugar rises, the chocolate manufacture may have to pay more to acquire

sugar in the normal market, but he will be compensated against this loss through

profit that will arise in the futures market. Note that a long position holder in a futures

contract makes a profit if the price of the underlying asset increases in the future.

Long hedge strategy can also be used by those investors who desire to purchase the

underlying asset at a future date (that is, when he acquires the cash to purchase the asset)