Page 1

2nd Quarter 2016Fixed Income

Presentation

Investor Relations

Jonathan Rangel • IRO • [email protected]

+52 (55) 5228 9753

Israel Becerril • IR • [email protected]

+52 (55) 5340 5200

IR Agency

Alejandro Ramírez • [email protected]

www.creal.mx • [email protected]

Page 2

Unique attributes

HIGH YIELD

PRODUCTS

Mid to low income

segments not

attended by banks

CENTRALIZED

CREDIT ANALYSIS

AND FUNDING

PAYROLL

SMALL BUSINESS

USED CARS

DURABLE GOODS

GROUP LOANS

PARTNERING &

DECENTRALIZED

DISTRIBUTION

On site presence to

approach customers

Sales forces: 10,000 reps.

Shared income & risk

We develop a credit

analysis customized

to our clients

That generate

higher margins

TARGET

UNSERVED

CUSTOMER2

Crédito Real is a financial company operating where traditional banks are not effective

Page 3

Customers walking

into branches

Customer approach on site

Train & develop sales forces

Compete with existing

players with a loan portfolio

and a fully integrated

presence

Ally with strategic partnersExclusivity agreements

Standard credit analysis

focused on mid and high

income segments

Credit analysis standards

according to customers profile,

attending mid and low income

segments

Source: (1) Crédito Real, CNBV, Companies filings. Size of the circle reflects size of consumer loan portfolio.

Reaching underserved customers enhances growth and profitability

Credito RealTraditional banks

Bank Branches

Crédito Real Customers

65% of Crédito

Real Customers

0 to 300,000 adults More than 300,000

54.3% of population 45.7%

63% of Bank

Branches

RURAL TRANSITION SEMI-URBAN URBAN MID-CITIES BIG CITIES

Rural & semi-urban focus

3

High quality loan portfolio growth (1)

Creal

Gentera

Banorte Santander

Interacciones

Banregio

Inbursa

Unifin

Banco Azteca

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0% 10% 20% 30% 40% 50%

Ave

rage

NP

L R

atio

20

11

-20

15

% Consumer Portfolio CAGR 2011–2015

ROE (%)

23%

26%

5%

14% 14%

19%

18%

10%

22%

9%

Findep

Page 4

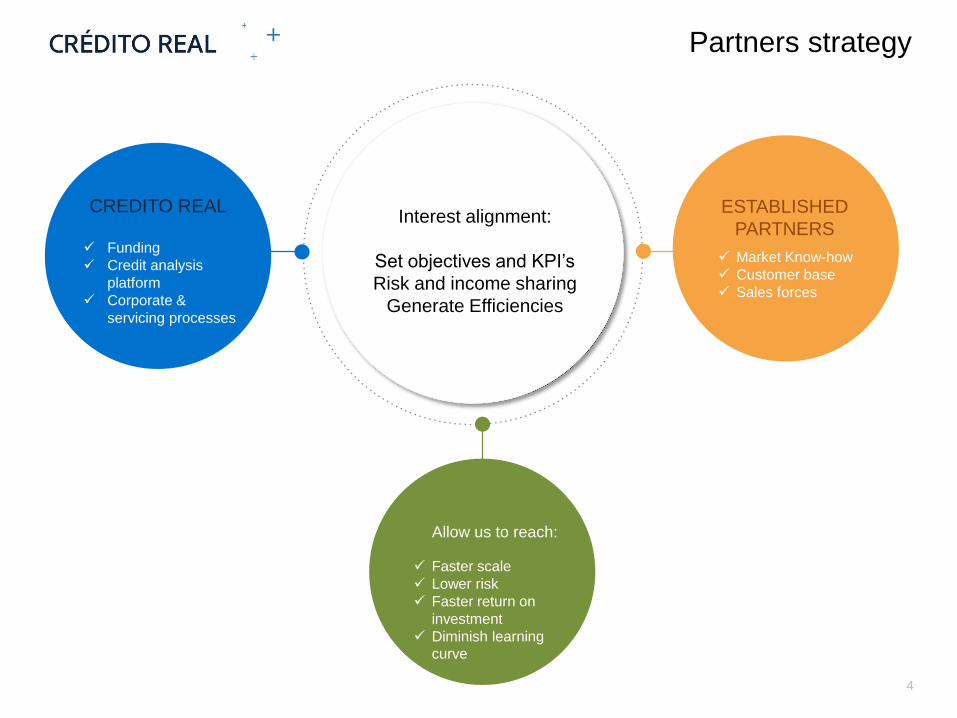

Partners strategy

Funding

Credit analysis

platform

Corporate &

servicing processes

Provides:

Market Know-how

Customer base

Sales forces

ESTABLISHED

PARTNERS

4

CREDITO REALInterest alignment:

Set objectives and KPI’s

Risk and income sharing

Generate Efficiencies

Allow us to reach:

Faster scale

Lower risk

Faster return on

investment

Diminish learning

curve

Page 5

22 Years of track record1993

Starts operations with durable good loans

2007

Partnership with Nexxus Capital Private Equity, Introduction of Group Loans

2010

Issuance of its US$210mm, 10.25%

Sr. Notes due 2015

2012

IPO in the BMV, Introduction of SME and

Used car loans

2011

Acquires 49% of payroll distributors

2004

Introduction of Payroll loans

1995

First public debt issuance

2014

Part of MSCI México Small-Cap Index, FTSE Small-Cap and IMC30 , Acquires remaining 51% of distributor Kondinero, Issuance of its US$425mm, 7.5% Sr. Notes due 2019

Experienced management team

2015

Partnership with car loan distributors in the USA, and

with a credit repair company

ANGEL ROMANOS / CEO

Founder, MBA from Wharton

CARLOS OCHOA / CFO

COO for 12 years, Master In Economics from Bristol University

PATRICIA FERRO / NEW BUSINESSES OFFICER

Extensive banking system background

LUIS RAMÓN RODRÍGUEZ / COO

Comprehensive experience analysis and collection in HSBC

LatAm

LUIS MAGALLANES/ CMO

Former Marketing VP at Coca Cola for Mexico, Brazil and LatAm

LUIS CARLOS AGUILAR / PAYROLL COMMERCIAL OFFICER

CFO for 13 years, MBA from IPADE

IKER OTEGUI / USED CARS OFFICER (USA)

Solid financial career in MABE and used cars Mexico

LUIS BERRONDO / HEAD OF M&A AND NEW PRODUCT

DEVELOPMENT

Previously served as the High-End Business General Manager at

Mabe

JONATHAN RANGEL / IRO

Former COMERCI´s IRO, MBA from IPADE

5

2016

Acquires 70% of Instacredit

Issuance of its US$625mm, 7.25% Sr Notes due 2023

Page 6

• Long-term commitment of main shareholders

• Financial & entrepreneurial legacy of main shareholders (BITAL, MABE)

Corporate structure

100%

49%

49%

38%

23%

51%

64%

65%

55%

24%

70%

99%

Corporate structure

• More than 80 strategic partners

• Partners network with + 10,000 sales reps.

• Centralized credit analysis & collection

• Management with over 15 years of experience.

• Committees: Audit, Corporate practices, Executive & Treasury

• 4 of 12 board members are independent

Service Companies

Main shareholders 40 %

Subsidiaries & Associates

PAYROLL GROUP LOANS USED CARS OTHERS

6

Free float 60%

Percentage of ownership

Page 7

74% 50% - 55%

6%

5% - 10%

8%

15% - 20%

2%

4%- 8%

10%

10% - 15%

2015 2019Used car loans

Group loans

Small business loans

Durable goods loans

Payroll loans

Diversified & Growing Loan portfolio

CAGR 10’-15´ 36%

ROE 2015 22%

NPL 2015 2.4%

CAGR 15’-19’ 15% - 20%

ROE 20% - 25%

NPL 2% - 3%

19%

7%

7%

5%

Organic Loan Portfolio Growth

50% - 80%

30% - 50%

25% - 35%

10% - 20%

5% - 10%

17

.6 b

illion

Expected CAGR

7

30

.8 -

36

.5 b

illion

Inorganic Growth

• Find established partners who are already profitable• Partners who keep running the business and remain as shareholders

Page 8

PAYROLL• Enter new markets (e.g. pensioners)

• Further consolidation

SMALL BUSINESS• Increase sales reps

• Increase origination through brokers

USED CARS

• Drive & Cash expansion

• Enlarge dealers network in Mexico and USA

• Focus on USA-Latino market with Don Carro and AFS

GROUP LOANS• Partner with other micro-lending companies

• Generate efficiencies & increase profitability

DURABLE GOODS • In house credit card, telemarketing and e-commerce

OTHERS• Inorganic growth: Instacredit, Resuelve & Credilikeme

Growth strategy

8

Page 9

2Q´16 Payroll Portfolio per Region

Payroll unique attributes

CREAL CONSUBANCO CREDIAMIGO

MARKET SHARE 35% 20% 10%

PRODUCT

DESCRIPTION

Personal loan linked

to payroll (low risk)Yes Yes

DISTRIBUTION

Network in rural areas +

4,000

sales reps + 250 branches

Integrated

operations

Integrated

operations

CAGR 53% 20% 18%

AVERAGE DURATION 40 months Yes Yes

ONSITE PRESENCE Yes Yes Yes

DIFFERENTIATORSExclusivity with 3 main

Distributors / 12 alliancesX X

• No exclusivity agreements with government entities

• Government entities carefully selected

• Non direct relation with government entities or unions

• Disclosed fees for every contract

14%Served market

Competitive landscape

86%Unserved market

• On site distribution in rural and semi-urban communities

• Manage of sales forces

• Over 250 customized agreements with government entities

• Equity stake and exclusivity with 3 main distributors

• Funding constraints for small players

Business practices

Entry barriers

2Q´16 Payroll Portfolio per Sector

Market of approximately 7 million employees

9

41.5%

20.3%

12.0%

8.2%

5.9%

5.8%

2.8%1.0% 2.4%

Federal Education

IMSS

Government

Health

State Education

Education Ministry

12.8%

9.1%

8.0%

6.6%

6.3%

6.1%

2.4%2.2%

2.0%1.8%

1.8%1.5%

1.4%1.3%

1.1%

35.6%

OAXACA

MEXICO CITY

ESTADO DE MEXICO

VERACRUZ

GUERRERO

CHIAPAS

GUANAJUATO

TABASCO

SAN LUIS POTOSI

JALISCO

MICHOACAN

HIDALGO

CAMPECHE

SINALOA

TAMAULIPAS

OTHERS

Page 10

3,350

3,400

3,450

3,500

3,550

3,600

3,650

Micro Little Medium Big

Credito Real Traditional banks

Average loan amount

Average loan term

Interest rate

Use of proceeds

~3 million

4-6 months

18%

Working capital

7.7 million

14-41 months

8-14% + commissions

Capex & working capital

Origination & Service

• Key account executives strengthen the Customer relation

model

• Application process takes up to 72 hours

• Site-visits at least once a year

• Risk assessment based in quantitative and qualitative

information

• Distribution through on-site presence

• Massive attention model based on branches

• Application process takes several weeks

• Limited customer site-visits

• Risk assessment based only in qualitative information

• Distribution through branches

SME differentiators

NPL

Source(1) INEGI (2009) and CNBV 2012

SMEs represents 52% of Mexican GDP and 80% of labor force(1)

# of Businesses in thousands

Rate of Businesses with loans

6.5%

29.2%

39.6%

52.6%

Creal Target Market

Diversified sector base Market share(1)Portfolio expansion & NPL

10

-15%

-6%

3%

12%

1.0x

1.5x

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

Loan

Gro

wth

Credito RealSectorNPL Crédito RealNPL Sector

34%

29%

14%

10%

10%

2%

Commerce Services

Textile Others

Construction Agriculture

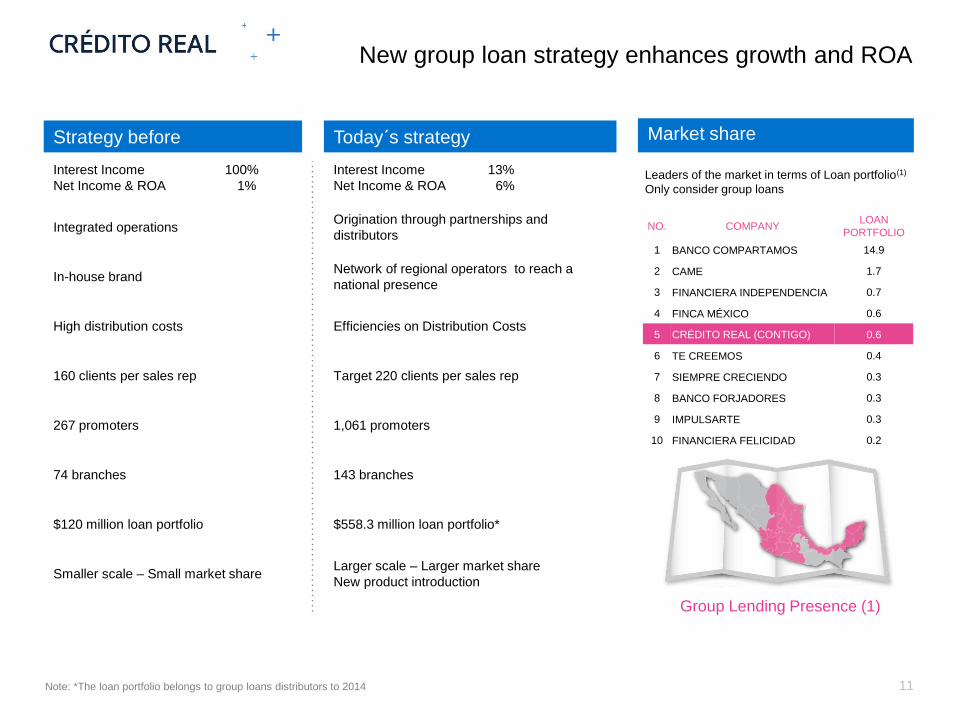

Page 11

Strategy before Today´s strategy

Interest Income 100%

Net Income & ROA 1%

Interest Income 13%

Net Income & ROA 6%

Integrated operationsOrigination through partnerships and

distributors

In-house brandNetwork of regional operators to reach a

national presence

High distribution costs Efficiencies on Distribution Costs

160 clients per sales rep Target 220 clients per sales rep

267 promoters 1,061 promoters

74 branches 143 branches

$120 million loan portfolio $558.3 million loan portfolio*

Smaller scale – Small market shareLarger scale – Larger market share

New product introduction

New group loan strategy enhances growth and ROA

Note: *The loan portfolio belongs to group loans distributors to 2014

Leaders of the market in terms of Loan portfolio(1)

Only consider group loans

Group Lending Presence (1)

Market share

NO. COMPANYLOAN

PORTFOLIO

1 BANCO COMPARTAMOS 14.9

2 CAME 1.7

3 FINANCIERA INDEPENDENCIA 0.7

4 FINCA MÉXICO 0.6

5 CRÉDITO REAL (CONTIGO) 0.6

6 TE CREEMOS 0.4

7 SIEMPRE CRECIENDO 0.3

8 BANCO FORJADORES 0.3

9 IMPULSARTE 0.3

10 FINANCIERA FELICIDAD 0.2

11

Page 12

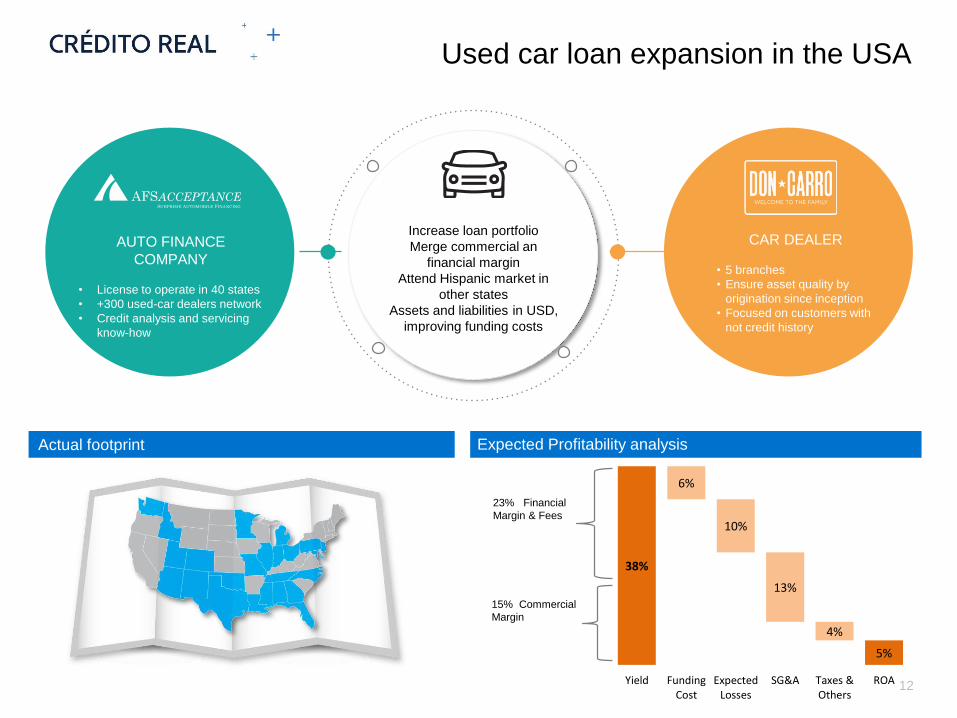

38%

6%

10%

13%

4%

5%

Yield FundingCost

ExpectedLosses

SG&A Taxes &Others

ROA

Used car loan expansion in the USA

AUTO FINANCE

COMPANY

• License to operate in 40 states

• +300 used-car dealers network

• Credit analysis and servicing

know-how

CAR DEALER

• 5 branches

• Ensure asset quality by

origination since inception

• Focused on customers with

not credit history

Increase loan portfolio

Merge commercial an

financial margin

Attend Hispanic market in

other states

Assets and liabilities in USD,

improving funding costs

23% Financial

Margin & Fees

15% Commercial

Margin

Actual footprint

12

Expected Profitability analysis

Page 13

Loan diversification by region Loan diversification by product

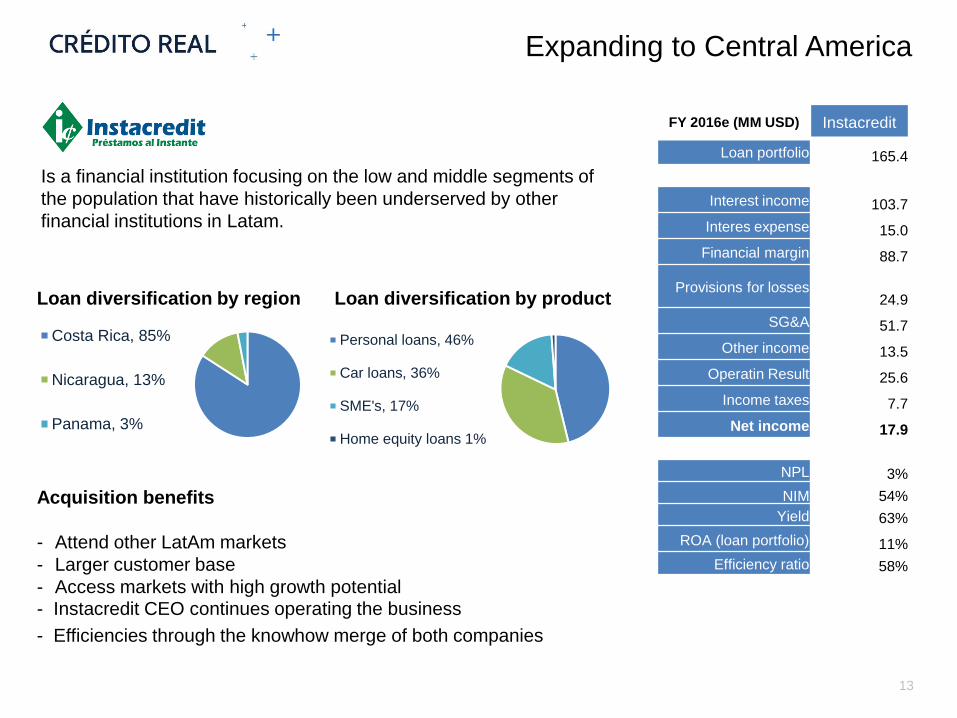

- Instacredit CEO continues operating the business

- Efficiencies through the knowhow merge of both companies

FY 2016e (MM USD) Instacredit

Loan portfolio 165.4

Interest income 103.7

Interes expense 15.0

Financial margin 88.7

Provisions for losses24.9

SG&A 51.7

Other income 13.5

Operatin Result 25.6

Income taxes 7.7

Net income 17.9

NPL 3%

NIM 54%

Yield 63%

ROA (loan portfolio) 11%

Efficiency ratio 58%

Expanding to Central America

13

Acquisition benefits

- Attend other LatAm markets

- Larger customer base

- Access markets with high growth potential

Is a financial institution focusing on the low and middle segments of

the population that have historically been underserved by other

financial institutions in Latam.

Costa Rica, 85%

Nicaragua, 13%

Panama, 3%

Personal loans, 46%

Car loans, 36%

SME's, 17%

Home equity loans 1%

Page 14

Outstanding asset quality

Stable levels of NPLs with sufficient reserves (1)

Product Credito Real** Banking Sector*

Payroll 2.3% 2.9%

Durable goods 2.7% 4.4%

SME 2.5% 2.8%

Group loans 0.9% 3.6%

Used Cars 1.9% 1.6%

Total 2.3% 3.1%

Instacredit 3.4%(2) 1.2%(3)

• Selective with distributors and government entities

• Specialized collection management

• Income and risk shared with distributors

• Loan structure to reduce default risk

• Regional footprint

*Average LTM ended on May 2016, except group loans for banking sector that is until December 2014. Source CNBV

** Average LTM ended on June 2016. For Group loans NPL belongs to distributors

(1) Reserves calculated as end of period allowance for loan losses divided by total loan portfolio

(2) Instacredit NPL Average of last six months

(3) Metric: Banking sector Total loan portfolio. Average LTM ended on June, 2016. Source BCCR

Average NPLs comparison*

14

1.8% 1.6% 1.7% 1.5% 1.5% 1.5%1.9% 1.9% 2.2% 2.1% 2.0% 2.4% 2.7% 2.3%

1.9% 1.9% 1.9% 1.9% 2.0%

3.2% 3.1% 3.0% 3.2%

2.6% 2.8% 2.8%

3.9% 3.7%

1Q 13 2Q 13 3Q 13 4Q 13 1Q 14 2Q 14 3Q 14 4Q 14 1Q 15 2Q 15 3Q 15 4Q 15 1Q 16 2Q 16

NPL Reserves / Total Loan Portfolio

Page 15

Yield and return drivers

Yield

2015

Yield

2019Drivers

PAYROLL 29% 35% • Effect of acquiring 51% of Credifiel and Credito Maestro

DURABLE GOODS 17% 21% • Development of new products

SMALL BUSINESS 14% 18%• Diversification of Fondo H portfolio focused on business with higher

rates

GROUP LOANS 13% 12%• Change of business strategy through consolidation of regional players

• ROA enhanced by earnings participation

USED CARS 42% 30% • Increased competition in Mexico & USA

AVERAGE YIELD

ROA

27%

6%

28%

7%

• Expected ROA 5% - 7%

• Expected ROE 20% - 25%

*Reported as of December 2015 YTD 15

Page 16

1,004

1,225

1,371

333 375

2013 2014 2015 2Q 15 2Q 16

2,724

3,327

4,264

976

1,655

2013 2014 2015 2Q 15 2Q 16

10,423

13,805

17,610

14,790

22,193

2013 2014 2015 2Q 15 2Q 16

Key financial indicators

CAGR ’13–’15: 30.0% YoY Growth : 50.0% CAGR ’13–’15: 25.1% YoY Growth: 69.5%

NIM % (1) Net income

CAGR ‘13–'15 : 16.9% YoY Growth : 12.6%

Loan portfolio Interest incomeMX$mm MX$mm

MX$mm

16

22.8%

19.3%21.0%

20.3%

23.0%

2013 2014 2015 2Q 15 2Q 16

Page 17

7.7%

6.9%

6.0%6.3%

4.7%

2013 2014 2015 2Q 15 2Q 16

41.8%38.8% 38.1%

40.5%

36.9%

2013 2014 2015 2Q 15 2Q 16

25.1% 26.8%

35.9%32.3%

59.1%

2013 2014 2015 2Q 15 2Q 16

24.5% 24.7%

22.2% 22.9%

19.1%

2013 2014 2015 2Q 15 2Q 16

Performance metrics

ROAE Efficiency ratio (1)

Capitalization ROAA

Notes:

(1) Efficiency index consists of administrative and promotion expenses for the period divided by the sum of (a) financial margin and (b) the difference

between (i) commissions and fees collected and (ii) commissions and fees paid for the period 17

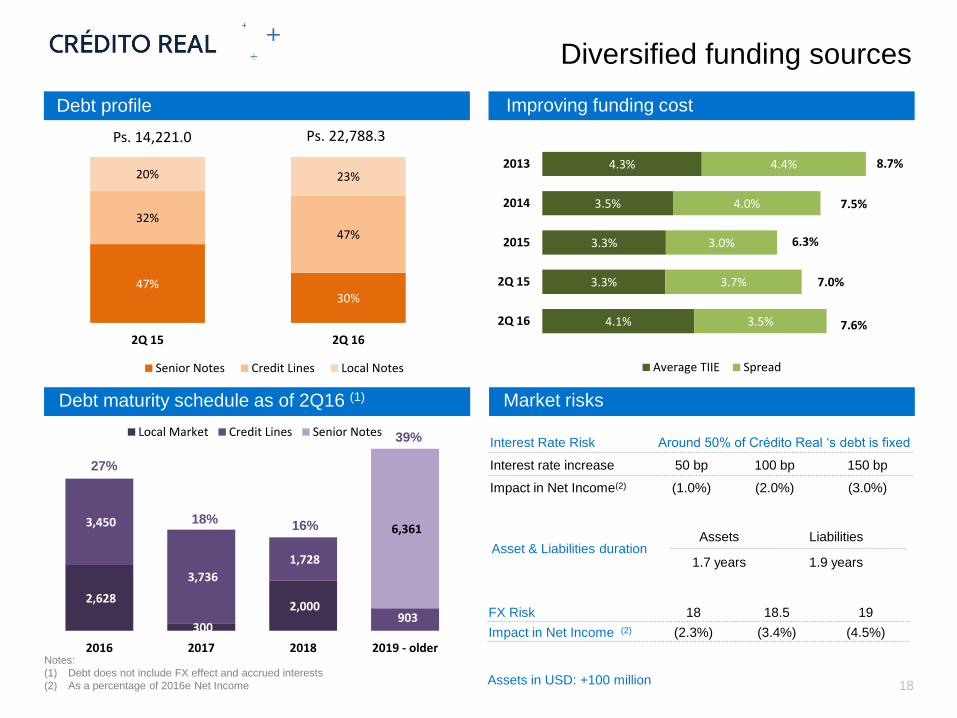

Page 18

2,628

300

2,000

3,450

3,736

1,728

903

6,361

2016 2017 2018 2019 - older

Local Market Credit Lines Senior Notes

4.1%

3.3%

3.3%

3.5%

4.3%

3.5%

3.7%

3.0%

4.0%

4.4%

2Q 16

2Q 15

2015

2014

2013

Average TIIE Spread

Diversified funding sources

Improving funding costDebt profile

Debt maturity schedule as of 2Q16 (1)

Notes:

(1) Debt does not include FX effect and accrued interests

(2) As a percentage of 2016e Net Income

Market risks

Interest Rate Risk Around 50% of Crédito Real ‘s debt is fixed

Interest rate increase 50 bp 100 bp 150 bp

Impact in Net Income(2) (1.0%) (2.0%) (3.0%)

FX Risk 18 18.5 19

Impact in Net Income (2) (2.3%) (3.4%) (4.5%)

27%

18%16%

39%

Asset & Liabilities duration Assets Liabilities

1.7 years 1.9 years

18

8.7%

7.5%

6.3%

7.0%

7.6%

Assets in USD: +100 million

47%30%

32%

47%

20% 23%

2Q 15 2Q 16

Ps. 14,221.0

Senior Notes Credit Lines Local Notes

Ps. 22,788.3

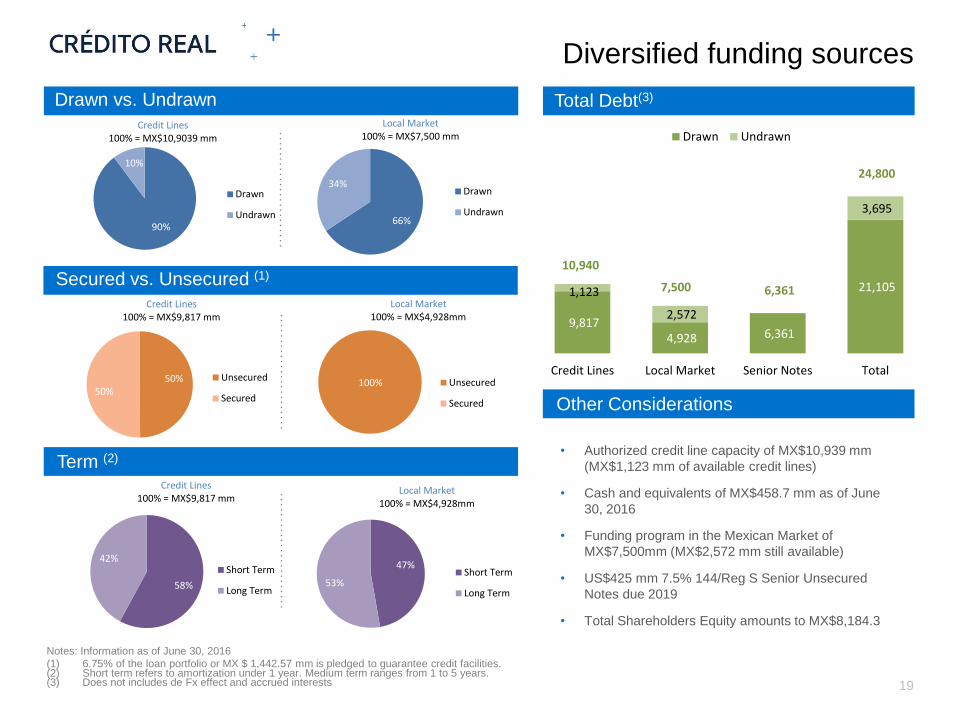

Page 19

9,817 4,928 6,361

21,105 1,123

2,572

3,695

Credit Lines Local Market Senior Notes Total

Drawn Undrawn

Diversified funding sources

Notes: Information as of June 30, 2016

(1) 6.75% of the loan portfolio or MX $ 1,442.57 mm is pledged to guarantee credit facilities.(2) Short term refers to amortization under 1 year. Medium term ranges from 1 to 5 years.(3) Does not includes de Fx effect and accrued interests

• Authorized credit line capacity of MX$10,939 mm

(MX$1,123 mm of available credit lines)

• Cash and equivalents of MX$458.7 mm as of June

30, 2016

• Funding program in the Mexican Market of

MX$7,500mm (MX$2,572 mm still available)

• US$425 mm 7.5% 144/Reg S Senior Unsecured

Notes due 2019

• Total Shareholders Equity amounts to MX$8,184.3

Total Debt(3)Drawn vs. Undrawn

Term (2)

Other Considerations

Secured vs. Unsecured (1)

19

10,940

7,500 6,361

24,800

90%

10%

Credit Lines100% = MX$10,9039 mm

Drawn

Undrawn66%

34%

Local Market100% = MX$7,500 mm

Drawn

Undrawn

50%50%

Credit Lines100% = MX$9,817 mm

Unsecured

Secured

58%

42%

Credit Lines100% = MX$9,817 mm

Short Term

Long Term

100%

Local Market100% = MX$4,928mm

Unsecured

Secured

47%

53%

Local Market100% = MX$4,928mm

Short Term

Long Term

Page 20

883

1,745

300

1,000 1,000

928

2,522

1,076

1,159

1,052

448

1,134

236

201

157 903

6,361

sep-16 dic-16 mar-17 jun-17 sep-17 dic-17 mar-18 jun-18 sep-18 dic-18 2019 +

Local Market Credit Lines Senior Notes

Debt Maturity Profile

Notes: Information as of June 30, 2016Does not includes de FX effect and accrued interests

MX$mm

20

1,811

4,267

1,076

1,459

1,052

448

2,134

236

1,201

157

7,264

Page 21

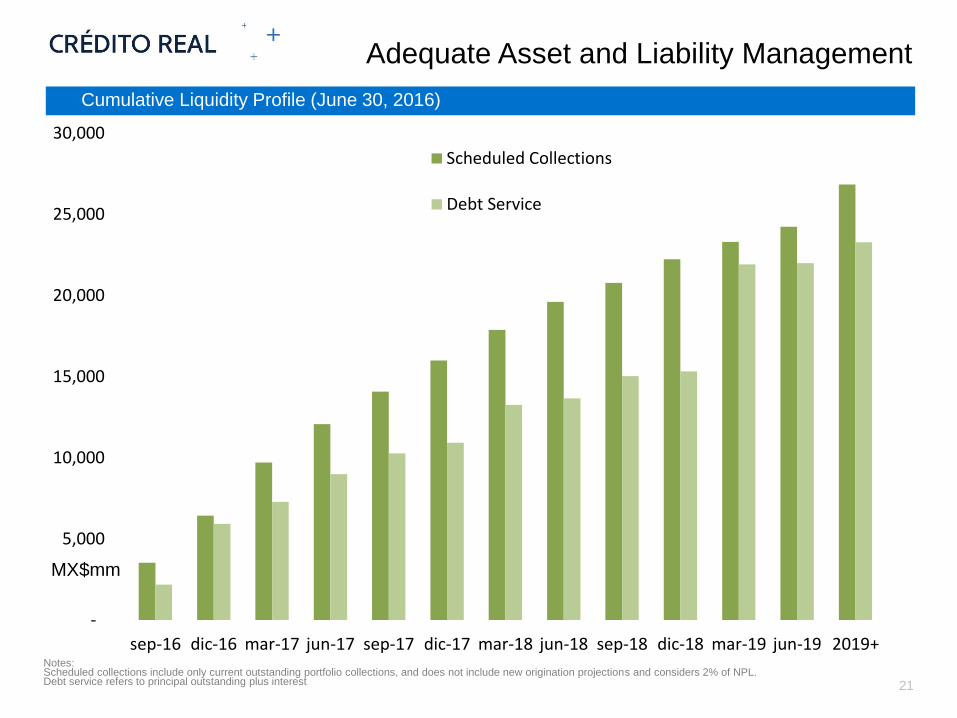

Adequate Asset and Liability Management

Notes: Scheduled collections include only current outstanding portfolio collections, and does not include new origination projections and considers 2% of NPL.Debt service refers to principal outstanding plus interest

Cumulative Liquidity Profile (June 30, 2016)

21

MX$mm

-

5,000

10,000

15,000

20,000

25,000

30,000

sep-16 dic-16 mar-17 jun-17 sep-17 dic-17 mar-18 jun-18 sep-18 dic-18 mar-19 jun-19 2019+

Scheduled Collections

Debt Service

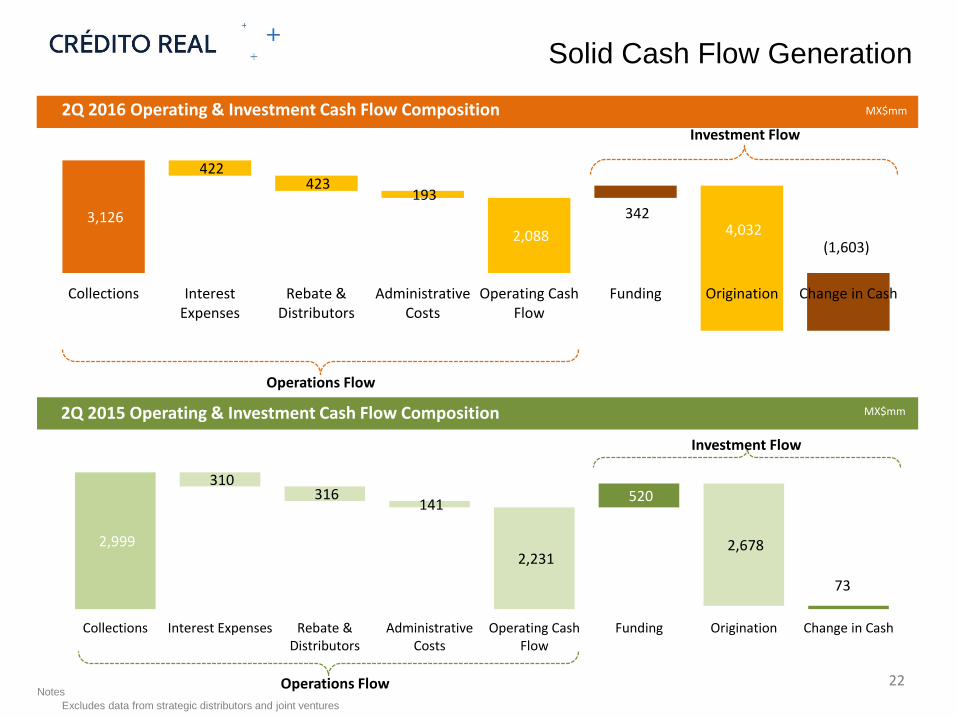

Page 22

2,999

310 316

141

2,231

520

2,678

73

Collections Interest Expenses Rebate &Distributors

AdministrativeCosts

Operating CashFlow

Funding Origination Change in Cash

3,126

422 423

193

2,088

342 4,032

(1,603)

Collections InterestExpenses

Rebate &Distributors

AdministrativeCosts

Operating CashFlow

Funding Origination Change in Cash

Cash Flow Generation

22Notes

MX$mm

2Q 2016 Operating & Investment Cash Flow Composition MX$mm

Investment Flow

Excludes data from strategic distributors and joint ventures

2Q 2015 Operating & Investment Cash Flow Composition

Operations Flow

Investment Flow

Operations Flow

Solid Cash Flow Generation

Page 23

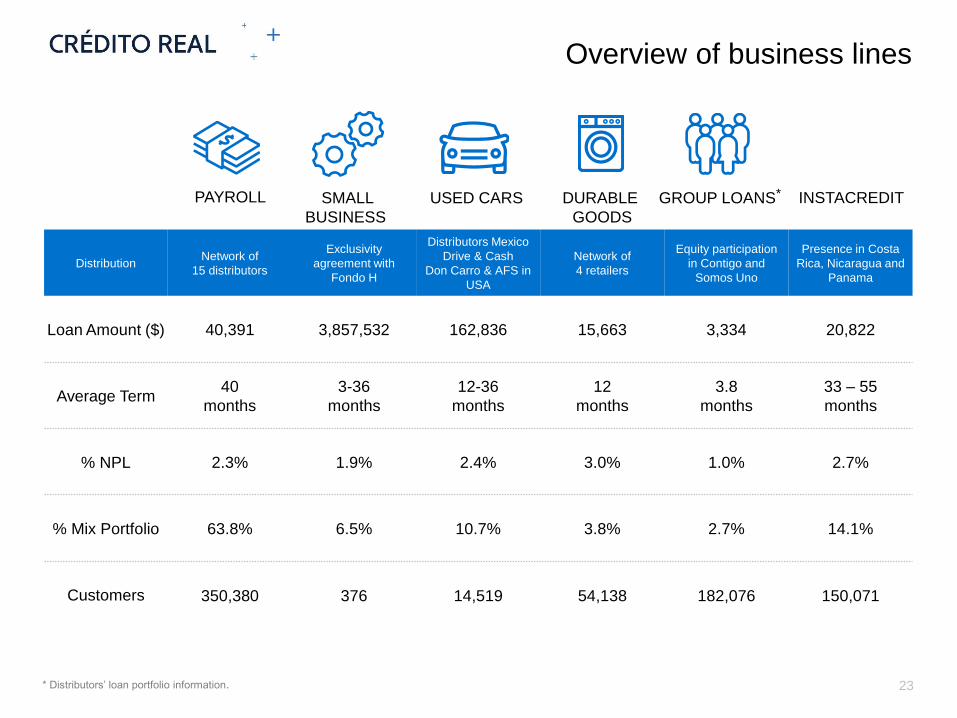

Overview of business lines

DistributionNetwork of

15 distributors

Exclusivity

agreement with

Fondo H

Distributors Mexico

Drive & Cash

Don Carro & AFS in

USA

Network of

4 retailers

Equity participation

in Contigo and

Somos Uno

Presence in Costa

Rica, Nicaragua and

Panama

Loan Amount ($) 40,391 3,857,532 162,836 15,663 3,334 20,822

Average Term40

months

3-36

months

12-36

months

12

months

3.8

months

33 – 55

months

% NPL 2.3% 1.9% 2.4% 3.0% 1.0% 2.7%

% Mix Portfolio 63.8% 6.5% 10.7% 3.8% 2.7% 14.1%

Customers 350,380 376 14,519 54,138 182,076 150,071

* Distributors’ loan portfolio information.

*PAYROLL SMALL

BUSINESS

USED CARS DURABLE

GOODS

GROUP LOANS

23

INSTACREDIT

Page 24

Payroll & Durable goods

Payroll loan description

50% interest income

50% risk sharing

Public Sector Employees

+ 300 agreements

+ 4,000 sales

representatives

Distributors

Government AgencyCollection Trust

Credit Analysis & Funding

Loan disbursement

Durable goods loan description

Retailers

4 retailers

115 stores

Over 50,000

customers

Collection

Customer servicing

Loan disbursement

5% to 7% of interest income

ProductDescription

Personal loans for unionized government employees

repaid through direct payroll

TargetMarkets

• Unionized public employees C+, C and D+• Average annual income USD from $6,000 to $10,000

ProductStatistics

• Avg. loan amount – MX$40,391• Avg. term – 40 months• Avg. annual interest rate – 40% - 55% 50% shared

with payroll distributors• Payment frequency – Bi-weekly• Customers – 350,380 (46.6 % of total Credito Real

customers)

Distribution

NetworkNetwork in rural & semiurban areas

ProductDescription

Loans to finance purchases of durable goods from

selected retailers

TargetMarkets

B, C+, C and D

ProductStatistics

• Avg. loan amount – MX$15,663• Avg. term – 12 months• Avg. annual interest rate – 40% - 50%• Payment frequency – Monthly• Customers – 54,138

(7.2 % of total Credito Real customers)

Distribution

Network

Well known retailers that uses own sales forces to

promote our credit products

Origination and collection process Origination and collection process

Credit Analysis & Funding

24

Page 25

Group loans & Small business

Group loans description

Origination and collection process

Funding

Loan disbursement

Collection

Promoters

Groups of 12-25 borrowers,

all members warranty the

loans, disbursement of 10%

Customers

Distributor

Small business loan description

Origination and collection process

Funding

30% sharing of operating income

SMEsFondo H

distributor

Loan disbursement

Collection

ProductDescription

Loans to finance micro-business working capital

requirements

TargetMarkets

Women in suburban areas C-, D and E

ProductStatistics

• Avg. loan amount – MX$3,334• Avg. term – 3.8 months / 14.1 weeks• Avg. annual interest rate – 90% - 110%• Payment frequency – Weekly• Customers – 182,076 (24.2 % of total customers)

Distribution

NetworkStrategic alliances with distributors

ProductDescription

Loans for working capital to small businesses

TargetMarkets

Medium and little size business

ProductStatistics

• Avg. loan amount –MX $3,857,532• Term 3 - 36 months• Avg. annual interest rate – 18% • Payment frequency – Monthly• Customers – 376

Distribution

NetworkStrategic alliance: 30% sharing of operating income

Credit Analysis & FundingCredit Analysis & Funding

25

Page 26

Origination and collection process

Used Cars

Loan description

Credit

Analysis

Car Dealer

Approved

× Not Approved

Customer

Funding, income

& risk sharing

Drive & Cash Used cars Used cars USA

Buys Cars from

customer

(50% of Market Value)

Customer lease car

Acquire car through auction

Upgrade Car

Sale & financing of used car

(direct & indirect lending)

CollectionC

olle

ctio

n

Funding

Product Description Sale & leaseback Loans for used cars Loans for used cars

Target MarketsB, C+ and C. Independent professionals with working capitals needs

C+, C and C-C+, C and C- (Hispanic market with no credit history)

Product Features

• Loan amount ~ 100,000 • Term - 1-12 months• Avg. annual interest rate - 35% to 60%• Payment frequency - monthly • Insurance fee• GPS systems to secure cars• Car invoice as loan guarantee

• Loan amount – MX $50,000 -$200,000

• Term 1 - 48 months• Avg. annual interest rate 25% - 35%• Payment frequency – Monthly• Income from insurance• GPS systems to secure cars

• Loan amount – 18,900 usd• Term – 48 months• Avg. annual interest rate – 20% - 25%

+ commecrial margin (30% - 35%)• Payment frequency – Biweekly • Income from insurance

Distribution Network 45 branches in 20 states of Mexico

Strategic alliances with car dealers that

use own sales forces to promote our

credit products

• 5 dealerships in Dallas-FortWorth, Texas

• License to operate in 40 states• Agreements with 466 car dealers

DRIVE & CASH USED CARS USED CARS USA

Credit

Analysis

Approved

× Not Approved

26

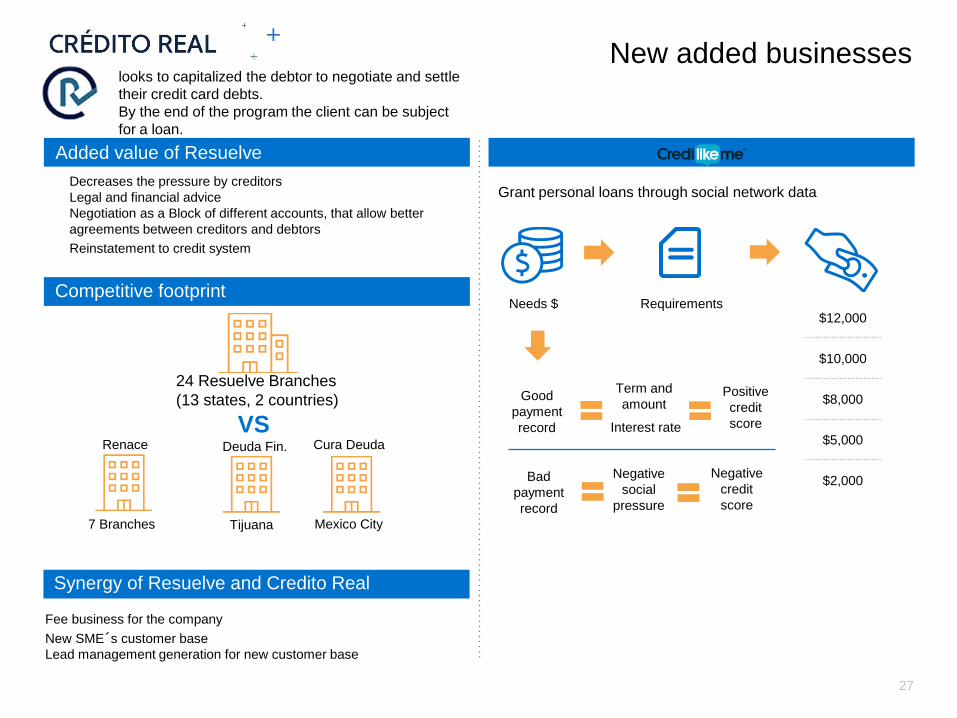

Page 27

Decreases the pressure by creditors

Legal and financial advice

Negotiation as a Block of different accounts, that allow better

agreements between creditors and debtors

Reinstatement to credit system

New added businesseslooks to capitalized the debtor to negotiate and settle

their credit card debts.

By the end of the program the client can be subject

for a loan.

Fee business for the company

New SME´s customer base

Lead management generation for new customer base

24 Resuelve Branches

(13 states, 2 countries)

7 Branches Tijuana Mexico City

Renace Deuda Fin. Cura Deuda

Added value of Resuelve

Competitive footprint

Grant personal loans through social network data

VS

Needs $ Requirements

Good

payment

record Interest rate

Term and

amountPositive

credit

score

$12,000

$10,000

$8,000

$5,000

$2,000Bad

payment

record

Negative

social

pressure

Negative

credit

score

27

Synergy of Resuelve and Credito Real

Page 28

Distribution model

DISTRIBUTION INTEREST ALIGNMENT ALLOW US TO REACH

PAYROLL

• 15 distributors, owning 100% of

Kondinero and 49% of the other two

largest.

• More than 4,000 sales representative

• More than 100 telephone operators

Sharing 50% of interest income and

sharing 50% of risk. Equity participation.

• 350,380 customers

• More than 300 agreements

• 30 states

• 80 cities

• About 40% of historical renewal rate

SMALL BUSINESS• Fondo H, presence in Mexico City and

metropolitan area

• 8 sales reps & brokers

• Operating Margin sharing 30%

(interest income – interest expense –

provisions)

• Exclusivity & Non-compete.

• Financing more than 250 business

including: manufacturing, distribution

and services sector

• 2 states

• High customer retention

USED CARS

• 18 distributors

• One Partnership with 45 branches in

20 states of Mexico

• 2 Partnerships in the USA

• More than 400 locations in the USA

• 51% equity share in Drive & Cash

• 65% equity share in AFS Acceptance

• 64% equity share in Don Carro

• 50% interest income & risk sharing

• 14,519 clients

• 20 states in Mexico

• USA States with Hispanics

concentration

GROUP LOANS• 2 Partnerships & 1 Alliance

• 161 branches

• More than 1,251 promoters

• 38% & 23% equity share respectively

in each Partnership

• 182,076 customers

• 67 cities

• 20 states

• Groups of 12 to 25 borrowers

• About 60% of renewal rate

DURABLE GOODS

• 4 different retailers

• 115 stores

• Continuous sales force trainee

• More than 800 sales reps.

•Rebate from 5% to 7% of future

interest

•Paid up front with no credit risk

• 54,138 customers

• Approval rate around 30%

INSTACREDIT

• Personal, Cars, SME’s and

Mortgages loans

• 67 branches

• More than 440 promoters

• 70% equity share

• 150,071 customers

• Presence in Costa Rica, Nicaragua

and Panama

OTHERS

Resuelve

• 24 Branches

Credilikeme

• Finthech

Resuelve

• 56% equity share

Credilikeme

• 24% equity share

Resuelve:

• 13 states

• 2 countries

• 20,876 customers

Credilikeme

• ~6,000 customers

• National presence

28

Page 29

197.1%

124.9%

79.6%67.1%

52.7%

31.0%21.4%

35.9%

5.9% 7.4%

27.2%

5.8%

USA Canada Germany Brazil Colombia Mexico

Market opportunity

Source: World Bank and Euromonitor. Data of Consumer Loan Penetration to 2014, except

Mexico that is for 2014. Data of Credit Penetration to Private Sector to 2012, except Canada

that is to 2008

Note 1: Population utilizing banking services.

Income level by bracket (approximate annual amount in USD):

“A/B” +108,400; “C+” 76,500; “Cm/C” 29,700; “D” 8,900; “E” 3,400.

Source: CNBV 2012, Agustin Carstens (Central Bank Minister)

Low penetration of credit Limited access to banking services

Strong Government Support

Consumer Loan Penetration as % GDP

Credit Penetration to Private Sector as %

GDP8.0

16.6

39.9

52.5

21%

79%

96%

83%

57%

25%

Target Market

2013

Population Segment Population (mm) Bancarization (1)

Financial reform should

double the current credit

penetration as % of GDP

within the next 5 years• SME credit guarantee

program allows to limit loss

severities to 50% of the

principal amount.

• Crédito Real is in process to

guarantee part of its SME

loan portfolio

28%

56%

Actual 2019

Evolution of Population

81%79%

2000 2013

Cm to C, D & E A, B & C+

19%

21%

Population (mm) Population (mm)

18

79

25

92

Target Market

Source: AMAI

A&B

C+

Cm to C

D&E

29

Page 30

Crédito Real Mexico (1) Brazil (5) Colombia (6) USA (2) Canada(3) Germany (4)

Benchmark 4.25% 14.25% 5.75% 0.50% - 0.50% 0.05%

Credit Card 21.5% - 65.0% 76% - 323% 20.2% - 31.9% 10.3% - 28.0% 14.6%

Mortgage 10.9% - 17.3% 11.90% 7% - 13% 3.50% 1.6% - 3.5%

Payroll 40% - 55% 24.4% - 123.4% 20.0% 30.0% 9.0% (c) 9.0% (c)

Durable Goods 40% - 50% 69.3% 38.6% 10.5% 3.3% 3.0%

SME's 18% - 35% 14.5% (a) 11.7% 8.2% 7.5% 2.9%

Microcredit 90% - 110% 90% - 205.5% 22.0% 30.9% 11% - 17% 8.5%

Used Car Loans 25% - 35% 10.4% - 16.4% (a) (b) 22.8% (b) 20.0% (b) 4% - 7.5% (b) 5.5% - 7.2% (b)

1 Source: Banxico, Condusef, Profeco, IMCO, CAME (2) Source: FED, Credit Cards Survey, CBS, Bank rate (3) Source: BOC, Car Loans Canada.

4 Source: European Central Bank, European commission (5) Source: BACEN, Bloomberg, Economic Commission for LATAM and the Caribbean.

6 Source: BANREP, Superintendencia.

Notes: (a) Commissions not included (b) Interest rates for new car loans (c) Interest rate for personal loans

Interest rate comparison

30

Page 31

Financial information / Profit & loss statement

31

Profit & Loss

Ps. Millions 2Q'16 2Q'15 Var % Var YTD’16 YTD’15 Var %Var 2015 2014

Interest Income 1,654.7

976.2 678.5 69.5% 2,994.0

1,919.2

1,074.8 56.0% 4,264.2 3,327.1

Interest Expense (422.9) (240.3) 182.6 76.0% (745.7) (464.9)

280.8 60.4% (952.3) (882.3)

Financial Margin 1,231.8

735.9

496.0 67.4% 2,248.3

1,454.3

794.0 54.6% 3,311.9 2,444.8

Provision for Loan Losses (208.0) (58.8) 149.3 254.0% (255.4) (136.3)

119.0 87.3% (345.6) (264.5) Financial Margin adjusted for Credit Risks 1,023.8

677.1

346.7 51.2% 1,993.0

1,318.0

675.0 51.2% 2,966.3 2,180.3

Commissions and fees charged 106.8

-

106.8 - 254.7

- 254.7 - - -

Commissions and fees paid (76.0) (50.6) 25.4 50.3% (134.5) (73.6) 61.0 82.9% (142.2) (99.0)

Other income from operations 229.6

3.5

226.1 6,440.3% 290.8

15.9 274.9 1,723.7% 36.2 23.7

Administrative and promotion expenses (746.6) (221.6) 525.0 236.8% (1,310.4) (458.8) 851.6 185.6% (1,138.1) (629.6)

Operating result 537.6

408.4

129.2 31.6% 1,093.6

801.5 292.1 36.4% 1,722.3 1,475.4

Income taxes (148.9) (91.9) 57.0 62.0% (281.6) (176.8) 104.8 59.3% (421.6) (334.8)

Income before participation in the results of subsidiaries 388.7

316.5 72.2 22.8% 812.1

624.8 187.3 30.0% 1,300.7 1,140.7

Participation in the results of subsidiaries and associates and non-controlling participation (13.8) 16.6 (30.4) (183.1%) (30.9) 35.0 (65.9) (188.3%) 70.6 84.1

Net Income 374.9 333.1 41.8 12.6% 781.1 659.8 121.4 18.4% 1,371.4 1,224.8

Page 32

Financial information / Balance sheet

32

Balance Sheet

Ps. Millions 2Q'16 2Q'15 Var % Var 2015 2014 Var % Var

Cash and cash equivalents 172.3 23.1 149.2 647.1% 120.8 53.8 67.1 124.7%

Investments in securities 286.4 791.0 (504.6) (63.8%) 543.3 1,251.2 (707.9) (56.6%) Securities and derivatives transactions 2,725.1 1,488.7 1,236.4 83.1% 2,112.8 950.3 1,162.6 122.3%

Performing loan portfolio

Commercial loans 21,676.5 14,482.6 7,193.9 49.7% 17,193.6 13,544.3 3,649.3 26.9%

Total performing loan portfolio 21,676.5 14,482.6 7,193.9 49.7% 17,193.6 13,544.3 3,649.3 26.9%

Non-performing loan portfolio

Commercial loans 516.2 307.7 208.5 67.8% 416.1 260.6 155.5 59.6% Total non-performing loan portfolio 516.2 307.7 208.5 67.8% 416.1 260.6 155.5 59.6%

Loan portfolio 22,192.7 14,790.3 7,402.4 50.0% 17,609.6 13,804.9 3,804.7 27.6%

Less: Allowance for loan losses 825.6 391.7 433.9 110.8% 485.5 420.1 65.4 15.6%

Loan portfolio (net) 21,367.1 14,398.6 6,968.5 48.4% 17,124.1 13,384.8 3,739.4 27.9%

Other accounts receivable (net) 3,368.5 1,946.0 1,422.4 73.1% 2,258.9 1,156.2 1,102.7 95.4% Property, furniture and fixtures (net) 251.0 119.0 132.0 111.0% 149.1 85.5 63.6 74.4% Long-term investments in shares 891.2 792.6 98.6 12.4% 835.6 859.0 (23.4) (2.7%)

Other assets Debt insurance costs, intangibles and others 4,019.3 2,120.3 1,899.0 89.6% 2,850.8 2,174.8 676.0 31.1%

Total assets 33,080.8 21,679.3 11,401.5 52.6% 25,995.5 19,915.5 6,080.0 30.5% Notes payable (certificados bursatiles) 4,935.0 2,911.9 2,023.1 69.5% 3,610.4 2,571.9 1,038.5 40.4%

Senior notes payable 7,913.4 6,738.2 1,175.2 17.4% 7,334.6 6,561.0 773.6 11.8% Bank loans and borrowings from other entities

Short-term 4,897.6 813.5 4,084.1 502.0% 3,490.5 1,120.3 2,370.2 211.6%

Long-term 5,042.3 3,757.5 1,284.8 34.2% 3,008.4 3,140.8 (132.3) (4.2%)

9,939.8 4,571.0 5,368.8 117.5% 6,498.9 4,261.0 2,237.9 52.5%

Total Debt 22,788.3 14,221.0 8,567.2 60.2% 17,443.9 13,393.9 4,049.9 30.2%

Income taxes payable 80.8 28.9 51.9 179.3% 88.3 51.9 36.4 70.0%

Other accounts payable 2,027.4 1,443.0 584.4 40.5% 1,750.8 1,112.4 638.4 57.4%

Total liabilities 24,896.5 15,693.0 9,203.5 58.6% 19,283.0 14,558.3 4,724.7 32.5%

Stockholders' equity

Capital stock 2,114.5 2,110.4 4.0 0.2% 2,108.1 2,135.0 (26.8) (1.3%)

Earned capital: Accumulated results from prior years 4,435.7 3,203.8 1,231.8 38.4% 3,035.2 1,977.4 1,057.8 53.5% Result from valuation of cash flow hedges, net 208.1 4.3 203.8 4,729.5% 89.3 5.6 83.7 1,495.2% Cumulative translation adjustment 50.7 - 50.7 - 2.8 - 2.8 - Controlling position in subsidiaries 594.3 9.9 584.5 5,925.2% 105.8 14.5 91.4 630.9%

Net income 781.1 657.8 123.3 18.7% 1,371.4 1,224.8 146.6 12.0%

Total stockholders' equity 8,184.3 5,986.3 2,198.0 36.7% 6,712.5 5,357.2 1,355.3 25.3% Total Liabilities and Stockholders' equity 33,080.8 21,679.3 11,401.5 52.6% 25,995.5 19,915.5 6,080.0 30.5%

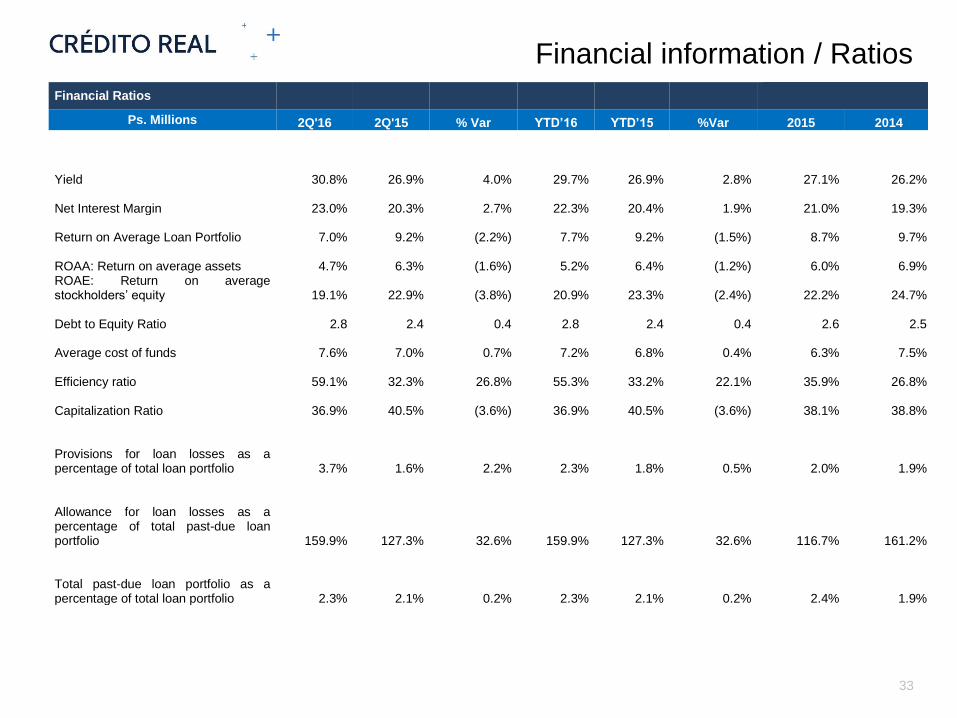

Page 33

Financial information / Ratios

33

Financial Ratios

Ps. Millions 2Q'16 2Q'15 % Var YTD’16 YTD’15 %Var 2015 2014

Yield 30.8% 26.9% 4.0% 29.7% 26.9% 2.8% 27.1% 26.2% Net Interest Margin 23.0% 20.3% 2.7% 22.3% 20.4% 1.9% 21.0% 19.3% Return on Average Loan Portfolio 7.0% 9.2% (2.2%) 7.7% 9.2% (1.5%) 8.7% 9.7% ROAA: Return on average assets 4.7% 6.3% (1.6%) 5.2% 6.4% (1.2%) 6.0% 6.9% ROAE: Return on average stockholders’ equity 19.1% 22.9% (3.8%) 20.9% 23.3% (2.4%) 22.2% 24.7% Debt to Equity Ratio 2.8 2.4 0.4 2.8 2.4 0.4 2.6 2.5 Average cost of funds 7.6% 7.0% 0.7% 7.2% 6.8% 0.4% 6.3% 7.5% Efficiency ratio 59.1% 32.3% 26.8% 55.3% 33.2% 22.1% 35.9% 26.8% Capitalization Ratio 36.9% 40.5% (3.6%) 36.9% 40.5% (3.6%) 38.1% 38.8% Provisions for loan losses as a percentage of total loan portfolio 3.7% 1.6% 2.2% 2.3% 1.8% 0.5% 2.0% 1.9% Allowance for loan losses as a percentage of total past-due loan portfolio 159.9% 127.3% 32.6% 159.9% 127.3% 32.6% 116.7% 161.2% Total past-due loan portfolio as a percentage of total loan portfolio 2.3% 2.1% 0.2% 2.3% 2.1% 0.2% 2.4% 1.9%

Page 34

Disclaimer

This presentation does not constitute or form part of any offer or invitation for sale or subscription of or

solicitation or invitation of any offer to buy or subscribe for any securities, nor shall it or any part of it form the

basis of or be relied on in connection with any contract or commitment whatsoever.

This presentation contains statements that constitute forward-looking statements which involve risks and

uncertainties. These statements include descriptions regarding the intent, belief or current expectations of the

Company or its officers with respect to the consolidated results of operations and financial condition, and future

events and plans of the Company. These statements can be recognized by the use of words such as “expects,”

“plans,” “will,” “estimates,” “projects,” or words of similar meaning. Such forward-looking statements are not

guarantees of future performance and actual results may differ from those in the forward-looking statements as a

result of various factors and assumptions. You are cautioned not to place undue reliance on these forward

looking statements, which are based on the current view of the management of the Company on future events.

The Company does not undertake to revise forward-looking statements to reflect future events or circumstances.

34