72

3-1 ©2011 Pearson Education, Inc. Publishing as Prentice Hall

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | oswald-willis |

| View: | 216 times |

| Download: | 1 times |

3-1©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-2

THE CORPORATEINCOME TAX (1 of 2)

Corporate electionsComputing corporation’s

taxable incomeComputing a corporation’s

income tax liability

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-3

THE CORPORATEINCOME TAX (2 of 2)

Controlled groups of corporations

Tax planning considerationsCompliance and procedural

considerationsFinancial statement implications

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-4

Corporate ElectionsTax Year (1 of 2)

New corp elects tax year by filing return

First return may be for short-period

Some corporations restrictedS-corporation uses calendar yearAffiliated group member must be

same as parentPSCs usually calendar year©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-5

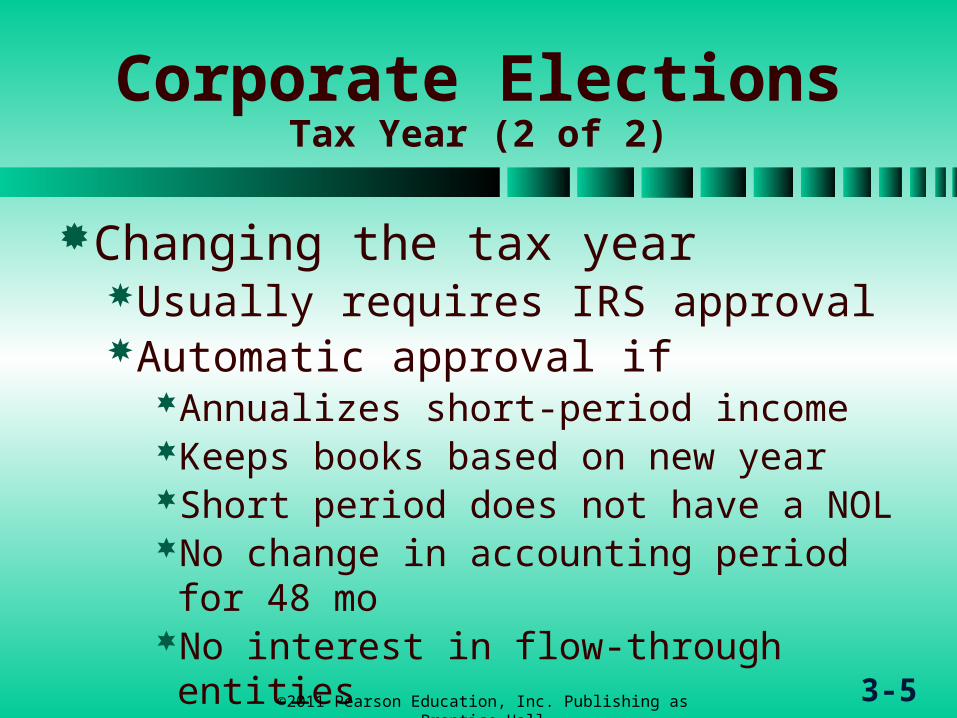

Corporate ElectionsTax Year (2 of 2)

Changing the tax yearUsually requires IRS approvalAutomatic approval if

Annualizes short-period incomeKeeps books based on new yearShort period does not have a NOLNo change in accounting period for 48

moNo interest in flow-through entitiesNot a specialized corporation©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-6

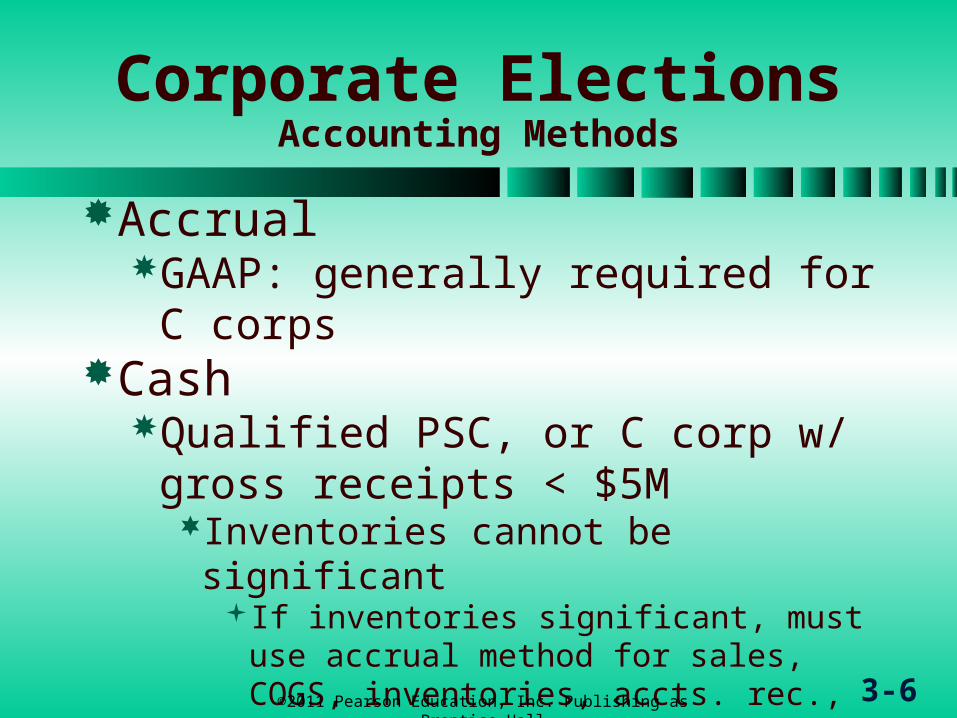

Corporate ElectionsAccounting Methods

AccrualGAAP: generally required for C

corpsCash

Qualified PSC, or C corp w/ gross receipts < $5MInventories cannot be significant

If inventories significant, must use accrual method for sales, COGS, inventories, accts. rec., & accts. pay. (the hybrid method)

Family farm w/ gross receipts < $25M

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-7

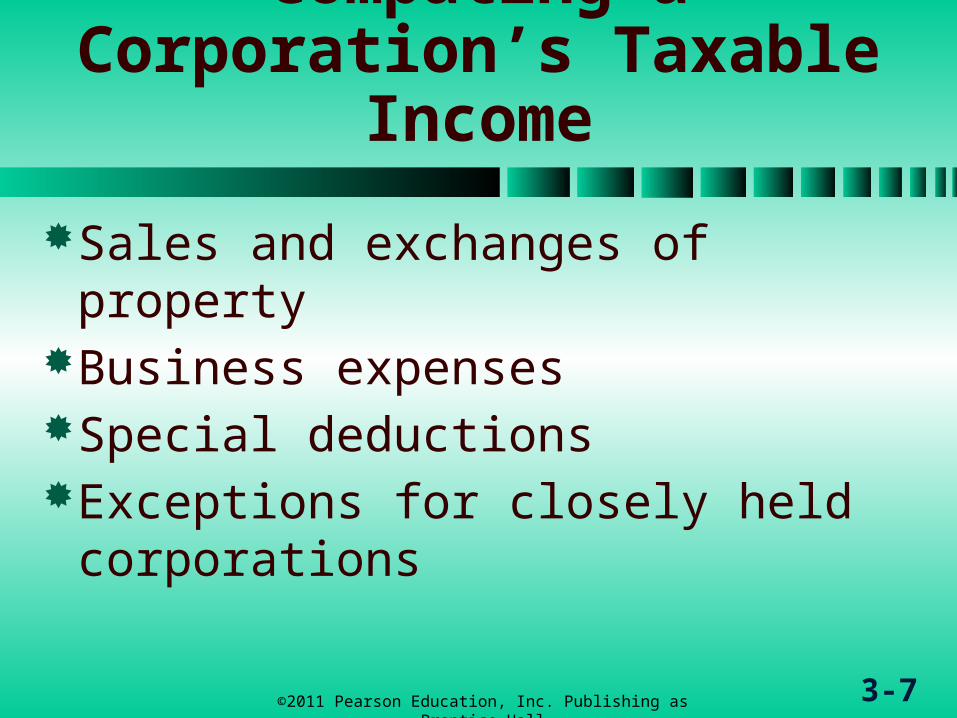

Computing a Corporation’s Taxable

Income

Sales and exchanges of propertyBusiness expensesSpecial deductionsExceptions for closely held

corporations

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-8

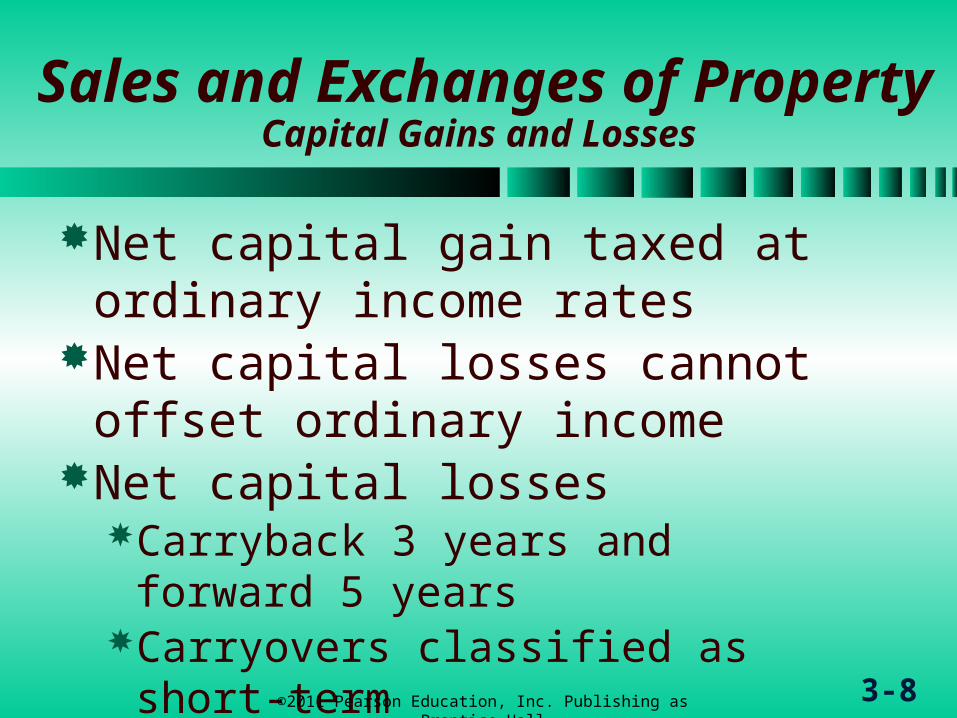

Sales and Exchanges of Property Capital Gains and Losses

Net capital gain taxed at ordinary income rates

Net capital losses cannot offset ordinary income

Net capital lossesCarryback 3 years and forward 5

yearsCarryovers classified as short-

termExpired losses are lost forever

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-9

Sales and Exchanges of Property

§291 Tax Benefit Recapture Rule

§1250 property sold at a gain Amount of depreciation in excess

of straight line is characterized as ordinary income plus

An additional 20% of all depreciation characterized as ordinary income under §291

No §1250 recapture under MACRS ©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-10

Business Expenses

General ruleOrganizational expendituresStart-up expendituresLimitations on deductions for

accrued compensationCharitable contributions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-11

General Rule

All ordinary and necessary expenses reasonable in amount

No deductions for Interest on loans to buy tax exemptsIllegal bribes or kickbacksFines or penaltiesInsurance premiums if corp is

beneficiary©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-12

Organizational Expenditures(1 of 2)

Expenses incident to creating corpE.g., legal, accounting, temporary

director fees, state incorporation fees

§248 election deemed to be madeNo need to filed election w/ 1st

returnMay expense first $5K of org costs

$5K reduced $ for $ when org costs > $50K

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-13

Organizational Expenditures(2 of 2)

Amortize remainder over 180 months

Expenditures must be incurred before end of first year of business

May elect to capitalize and not amortizeElection irrevocable

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-14

Start-up Expenditures(1 of 3)

Non-organizational Ordinary and necessary

expensesPaid or incurred BEFORE the

actual start of business operations

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-15

Start-up Expenditures(2 of 3)

Examples of include expenses to:Investigate creation or acquisition

of an active trade or businessCreate an active trade or businessConduct an activity engaged in for

profit or production of income before business operations begin

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-16

Start-up Expenditures(3 of 3)

Election to expense first $5K of org costs$5K reduced $ for $ when org costs >

$50KRemainder amortized over 180 months

Election must be made by due date for filing tax return for first year of operation or ownership

Election deemed to be made w/ 1st returnMay elect to capitalize with no

amortization

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-17

Limitation on Deductions for Accrued Compensation

Accrued bonuses/compensation must be paid within 2-1/2 months after close of tax yearIf paid after 2-1/2 months,

payment deemed deferred compensation and is deductible in year paid

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-18

Charitable Contributions(1 of 4)

Timing of deductionDeducted in the year paid Accrual basis corps may elect to

include payment made w/in 2-1/2 months following the end of tax yearBoard of directors must have

authorized contribution during year it was accrued

Must meet substantiation requirements to deduct contribution

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-19

Charitable Contributions(2 of 4)

Donated moneyDeduction equals amount donated

Non-cash propertyAmount USUALLY equal to FMV of

property donatedOrdinary income property

Deduction limited to FMV less Ord Inc or STCG that would have been recognized if property were sold (includes recapture)©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-20

Charitable Contributions(3 of 4)

Non-cash property (continued)Certain inventory related to

exempt functionDeduction = adjusted basis + 1/2 gainSimilar rule for computer technology

donated for educational purposesSpecial rules pertaining to

contributions of computer equipment, book inventory, and wholesale food inventory©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-21

Charitable Contributions(4 of 4)

Max deduction is 10% of “adjusted taxable income” (ATI)ATI is taxable income before NOL

carryback, capital loss carryback, dividend received deduction or charitable contribution deduction

Excess carried forward for 5 yrsCreates a deferred tax asset

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-22

Special Deductions

U.S. Production activities deductionOther names for the deduction

Domestic production activities deductionManufacturing deduction

Dividends-received deductionNet operating lossesSequencing of the deduction

calculations©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-23

U.S. Production Activities Deduction

(1 of 3)

Deduction is lesser of a % timesQualified production activities

income ORTaxable income before the U.S.

production activities deductionPhased-in percentages

6% for 2007-20099% for 2010 and thereafter

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-24

U.S. Production Activities Deduction

(2 of 3)

Qualified production activities incomeDomestic production gross receipts

from lease, rental, sale, or exchange, of tangible property manufactured in the U.S. LESS

Expenses related to qualified income including CoGS, & indirect allocable expenses

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-25

U.S. Production Activities Deduction

(3 of 3)

Deduction limited to 50% of W-2 wages

Not an expense for financial accountingCreates a permanent difference

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-26

Dividends Received Deduction(1 of 3)

Corps owning < 20% of a domestic corporation deduct lesser of70% of Dividends Received or70% of taxable income before

NOL, capital loss carryback or DRD

Exception to taxable income limitationIf 70% of dividend received creates

an NOL, then the full DRD is deductible

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-27

Dividends Received Deduction(2 of 3)

Corps owning 20% and < 80% of a domestic corp 80% deduction instead of 70%

Corps owning 80% of domestic corpMember of affiliated group 100% deduction

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-28

Dividends Received Deduction(3 of 3)

No deduction is allowed if :Paying corp is a foreign corpStock purchased w/borrowed

moneyStock of paying corp held for < 46

daysResults in a permanent

differenceAffects effective tax rate, but not

deferred taxes

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-29

Net Operating Losses(NOL)

Deductions exceed gross income for the year before NOL carrybacks

NOL may be carried back 2 yrs & then forward 20 yrsCorp may elect to forgo

carryback & only carry NOL forward 20 yrs

Creates a deferred tax asset©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-30

Sequencing of the Deduction Calculations

Charitable contributions, DRD, NOL, and all other deductions must be taken in the following order1. All other deductions2. Charitable contributions3. DRD4. NOL5. U.S. production activities

deduction

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-31

Exceptions for Closely-Held Corporations (1 of 3)

Special rules apply to shareholders who own >50% of corp§1239 sale of depreciable

property to corp causes gain to be ordinary income to the controlling shareholder

§267 disallows loss on sale of property by corp to controlling shareholder Loss may be recovered by

shareholder if later sells prop at a gain

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-32

Exceptions for Closely-Held Corporations (2 of 3)

Special rules apply to shareholder who own >50% of corp (continued)Corporation and shareholder

using different accounting methodsDefers deduction for accrued

expenses owed by accrual-method corp to cash-method controlling shareholder until income recognized by cash-method shareholder

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-33

Exceptions for Closely-Held Corporations (3 of 3)

Loss limitation rulesIf 5 or fewer s/hs own > 50% of the

stock, the corp’s losses are limited to amount corp has “at risk”Losses not currently deductible are

carried over to be used in a later yearMay also be subject to passive activity

rulesPSCs and closely held corps subject

to passive activity limitation rules©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-34

Computing a Corporation’s Income Tax

Liability

General rulesRegular income tax formulaPersonal service companies

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-35

General Rules

The tax rates are graduatedRate surcharges eliminate

benefit of lower graduated tax rates from lower income brackets

Corps with income >$18.33M pay a flat 35% on all income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-36

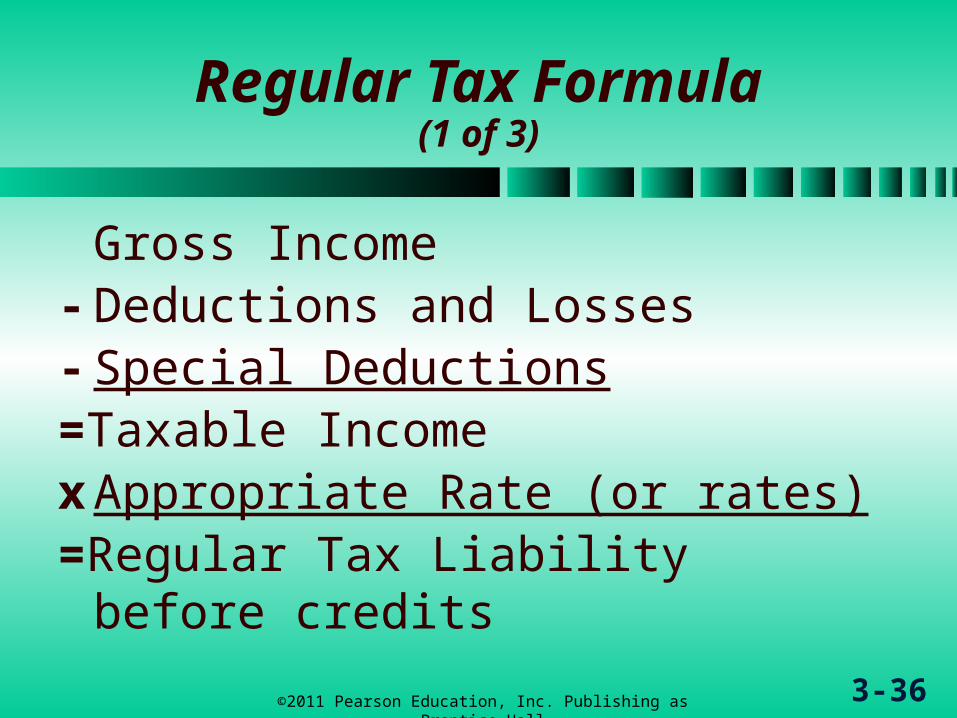

Regular Tax Formula(1 of 3)

Gross Income- Deductions and Losses- Special Deductions=Taxable IncomexAppropriate Rate (or rates)=Regular Tax Liability before

credits

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-37

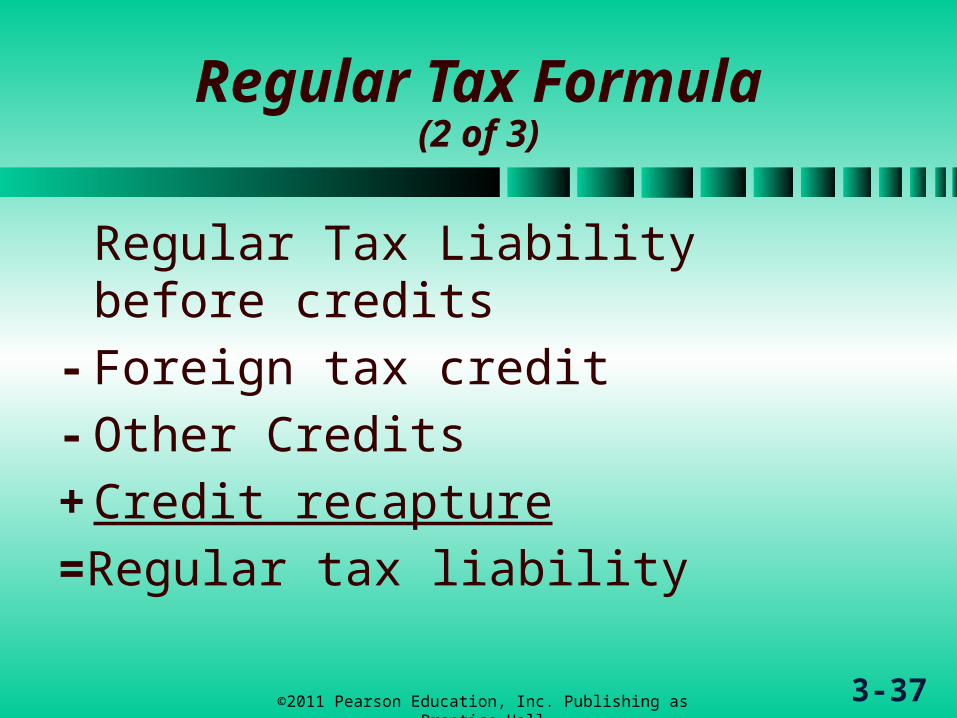

Regular Tax Formula(2 of 3)

Regular Tax Liability before credits

- Foreign tax credit- Other Credits+ Credit recapture=Regular tax liability

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-38

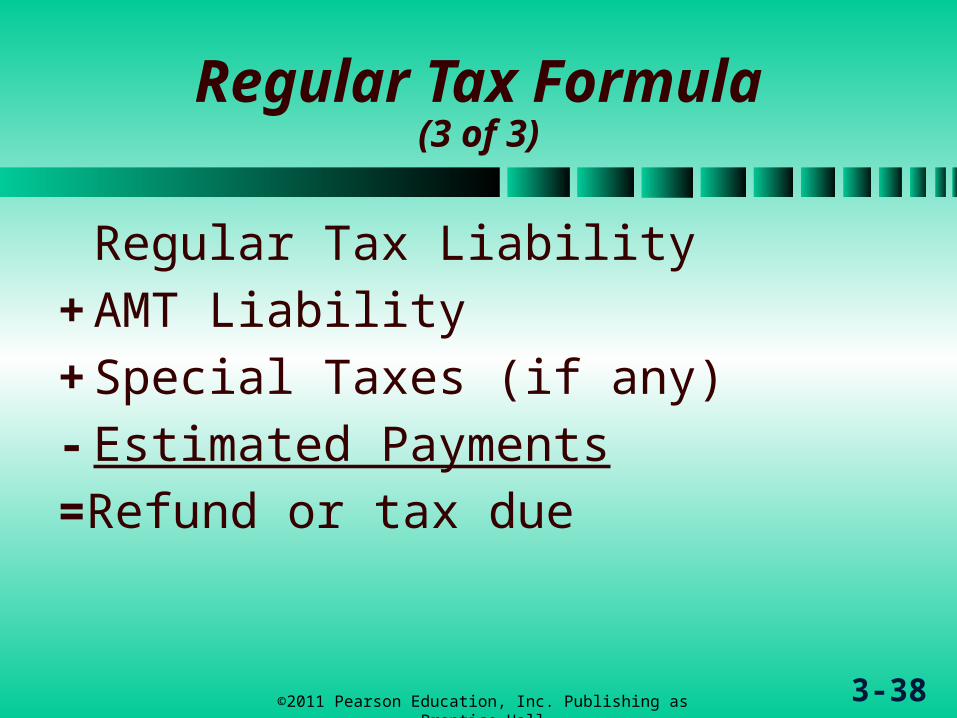

Regular Tax Formula(3 of 3)

Regular Tax Liability+ AMT Liability+ Special Taxes (if any)- Estimated Payments=Refund or tax due

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-39

Personal Service Corporations

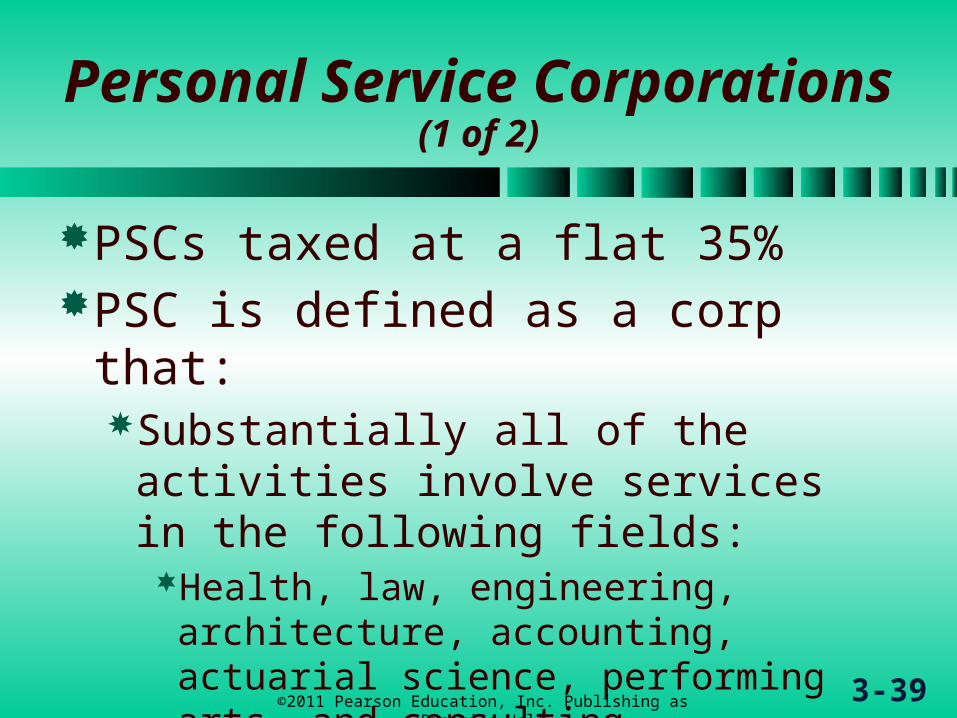

(1 of 2)

PSCs taxed at a flat 35%PSC is defined as a corp that:

Substantially all of the activities involve services in the following fields:Health, law, engineering,

architecture, accounting, actuarial science, performing arts, and consulting

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-40

Personal Service Corporations

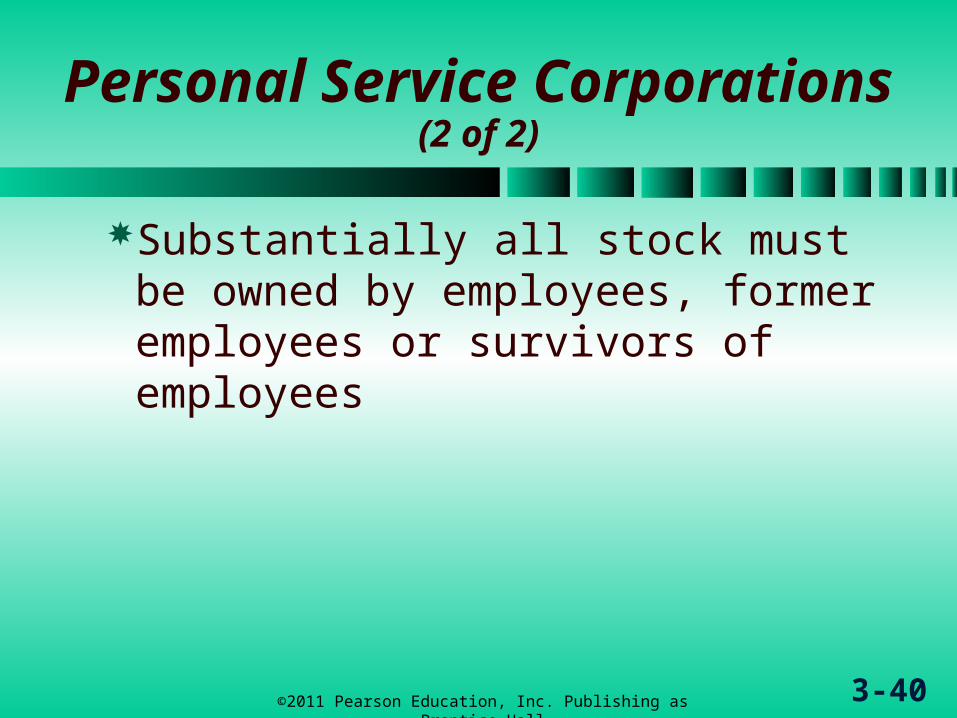

(2 of 2)

Substantially all stock must be owned by employees, former employees or survivors of employees

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-41

Controlled Groups

Why special rules are neededWhat is a controlled group?Special rules applying to

controlled groupsConsolidated tax returns

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-42

Why Special Rules are Needed

Prevent shareholders from using multiple corporations to avoid having income taxed at 35%Each corporation would be able to

take advantage of lower graduated rates

Lower graduated rates must be spread among all corporations in a controlled group©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-43

What Is a Controlled Group?

Two or more corps owned directly or indirectly by same shareholder or group of shareholders

Types of controlled groupsParent-subsidiaryBrother-sisterCombined

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-44

Parent-Subsidiary Controlled Group

One corp directly owns at least:80% of voting power of all classes

of voting stock OR80% of total value of all classes of

stock of subsidiary corporation

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-45

Brother-Sister Controlled Group

50%-80% definitionFive or fewer individuals, trusts or

estates own:At least 80% of voting power or at

least 80% of value of stock of two or more corporations AND

> 50% of the voting power or value is held by identical owners (common ownership)

50%-only definition is 2nd test above

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-46

Combined Controlled Groups

Three or more corps which meet the following criteria:Each corporation is a member of a

parent-subsidiary or brother-sister group

At least one is both a parent and a member of a brother-sister group

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-47

Special Rules Applying to Controlled Groups (1 of 2)

Benefits allocated among members5% and 3% surcharge

50%-only test for brother-sister groups

$40,000 AMT exemption amount50%-only test for brother-sister

groupsThe $250,000 minimum

accumulated earnings credit50%-only test for brother-sister

groups

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-48

Special Rules Applying to Controlled Groups (2 of 2)

Benefits allocated (continued)§179 expense amount

50%-80% test for brother-sister groups50% used for parent-sub test instead of

80%The $25,000 general business credit

limit50%-80% test for brother-sister groups

No loss on sale of assets between members

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-49

Consolidated Tax Returns

Affiliated groupsAdvantages of filing a

consolidated returnDisadvantages of filing a

consolidated return

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-50

Affiliated Groups(1 of 2)

One or more chains of includible corps connected through stock ownership to a common parent

Common parent directly owns 80% of voting power AND value of at least one includible corporation

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-51

Affiliated Groups(2 of 2)

Each corp owned at least 80/80 by another member of the group

An affiliated group MAY file a consolidated returnCapital losses offset capital gains

from other group membersOperating losses reduce operating

income from other group members

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-52

Consolidated Return Advantages

Losses of one member offset gains of another member

Capital losses of one member offset capital gains of another member

Profits and gains from intercompany transactions deferred until sale outside the group

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-53

Consolidated Return Disadvantages

Election binding on all subsequent tax yearsUnless IRS grants permission

otherwiseLosses from intercompany

transactions deferred until sale outside the group

Additional administrative costs©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-54

Tax Planning Considerations

Compensation planning for shareholder-employees

Special election to allocate reduced tax rate benefits

Using NOL carryovers and carrybacks

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-55

Compensation Planning

Salary paymentsReduce double taxation if paid to

shareholder-employees Fringe benefits

Deducted by corporation and certain benefits are not be taxable to shareholder-employee

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-56

Allocating Reduced Tax Rate Benefits

A controlled group may apportion lower tax rates in any manner to member corporationsReduce benefits to members with

little or no incomeIncrease benefits to members

with the highest income

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-57

Using NOL Carryovers and Carrybacks

Two optionsCarryback to 2nd previous year,

then 1st previous year, then forward

Forgo the carrybacks and carry forward

Examine marginal tax rates in prior years and expected marginal tax rates in future years to maximize tax benefit

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-58

Compliance and Procedural

Considerations Estimated Taxes

Estimated taxes required if corp owes >$500 for current year.

Pay in four installmentsEach installment 25% of annual

liability Underpayment of estimated tax

penaltySmall corps exempt from penalty if

Pay in lesser of 100% of prior or current year’s tax liability

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-59

Compliance and Procedural

Considerations Filing Requirements

Return is required each year regardless of income

Use form 1120 Use form 1120A if gross receipts,

total income & total assets each < $500K

Large corps (assets>$10M) must fill out more detailed schedule M-3

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-60

Financial Statement Implications

ASC 740 - Income Taxes (SFAS 109)

Temporary differencesDeferred tax assets and the

valuation allowanceASC 740 - Uncertain Tax Positions

(FIN 48)Balance sheet classificationTax provision process©2011 Pearson Education, Inc. Publishing as Prentice

Hall

3-61

ASC 740 - Income TaxesScope

Establishes principles of accounting for current and deferred taxesArising from temporary

differences

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-62

ASC 740 - Income TaxesPrinciples

Addresses financial statement consequences of Rev, exp, gains/losses recognized in

different years for tax and financial statement purposes

Events affecting book/tax differences in bases of assets and liabilities

Loss & credit carrybacks or carryforwards

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-63

ASC 740 - Income TaxesObjectives

Recognize current yr taxes payable or refundable

Recognize deferred tax liabilities and assets for future tax consequences of events on fin stmts or tax return

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-64

Temporary Differences(1 of 2)

Deferred tax liabilities occur whenRev/gains recognized earlier for

book than taxExp/losses deducted earlier for tax

than bookTax basis of asset < book basisTax basis of liability > book basis

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-65

Temporary Differences(2 of 2)

Deferred tax assets occur whenRev/gains recognized earlier for tax

than bookExp/losses deducted earlier for book

than taxTax basis of asset > book basisTax basis of liability < book basisLoss/credit carryforwards exist

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-66

Deferred Tax Assets and the Valuation Allowance

Deferred tax assetFirm will realize tax benefit of

event in the futureValuation allowance used for

portion of benefit not likely to be realizedUse “more likely than not” standard

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-67

ASC 740 - Uncertain Tax Positions

Formerly FIN 48

Two-step to account for uncertain tax positionsDetermine if position exceeds

“more likely than not” (>50%) probability of being sustained on its merits by IRSIf not, corp cannot recognize tax

benefitRecords liability for unrecognized tax

benefitsIf yes, measure amount of benefit

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-68

Balance Sheet Classification

Classify as current or noncurrentIf related to another asset or

liability use classification of related asset/liab

Net current assets and liabilitiesNet noncurrent assets and

liabilities

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-69

Tax Provision Process(1 of 3)

1. Identify temporary differences and tax carryforwards

2. Prepare “roll forward” schedules3. Apply appropriate tax rates in

roll forward schedules to determine deferred tax asset/liability balances

4. Adjust deferred tax assets by valuation allowance if necessary

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-70

Tax Provision Process(2 of 3)

5. Adjust income tax expense for uncertain tax positions under FIN 48

6. Determine current federal income taxes payable (current tax expense)

7. Determine total federal income tax expense (benefit)

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3-71

Tax Provision Process(3 of 3)

8. Prepare and record tax journal entries

9. Prepare tax provision reconciliation

10. Prepare tax rate reconciliation11. Prepare financial statements

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Comments or questions about PowerPoint Slides?Contact Dr. Richard Newmark at University of Northern Colorado’s

Kenneth W. Monfort College of [email protected]

3-72©2011 Pearson Education, Inc. Publishing as Prentice Hall