1©2009 Frost & Sullivan, All rights reserved www.frost.com

360 Degree Outlook and Growth

Strategies in the APAC

In- Vitro Diagnostics Industry

October 8, 2009

Presented By:

Nitin Naik

Vice President-Medical Technologies

Asia Pacific

2©2009 Frost & Sullivan, All rights reserved www.frost.com

Contents

Diagnostics

Industry

Briefing

2.

3.

1. 360 Degree Global Perspective

APAC Market Outlook

Industry Best Practices

3©2009 Frost & Sullivan, All rights reserved www.frost.com

The CEO’s Perspective of the Complex Business Universe

4©2009 Frost & Sullivan, All rights reserved www.frost.com

CEO Global Perspective

1. Reference Labs and CROs Expand

Services to Developing Countries.

2. Increased R&D Outsourcing by Pharma

& Biotech Companies

3. Earlier Launch of Diagnostic Tests in the

Asian/European Markets

4. Changing Global Trends Drive Adoption

of New Technologies.

5. Funding opportunities, primary

customer base and research strengths

are differentiated in the APAC region

GLOBAL

Political

&

Regulatory

Emerging

OpportunitiesCultural

CEO

5©2009 Frost & Sullivan, All rights reserved www.frost.com

REFERENCE LAB TESTING EXPANDING TO DEVELOPING WORLD

Advanced Markets

Reference labs based in the

U.S.,such as Quest Diagnostics

Inc., are looking for high growth

Asian markets

India

India has growing middle class

with increasing buying power

and demand for better

healthcare services.

China

China has a growing aging

population and increasing

healthcare spending.

India, China and S. Korea have some of the highest growth rates for healthcare spending in APAC and along with

the growing aging population and middle class, represent attractive markets for clinical testing. Additionally, the

increased prevalence of lifestyle diseases such as diabetes, cardiovascular diseases, and certain cancers

contributes to the increasing need of testing. U.S. based national reference laboratories have already taken the lead

to expand into these growing markets. Global expansion of clinical lab testing is likely to be influenced by

innovation, cost and readiness of the countries.

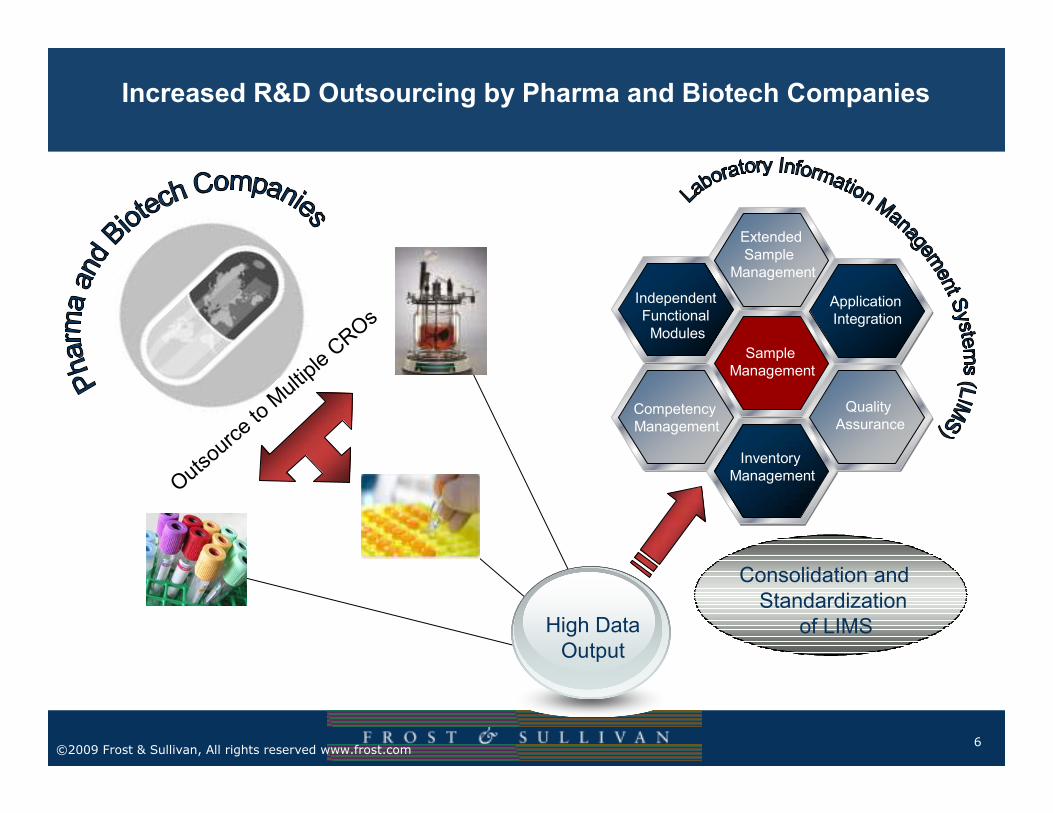

Reference Labs Expand Services to Developing Countries

6©2009 Frost & Sullivan, All rights reserved www.frost.com

High Data

Output

Consolidation and

Standardization

of LIMS

Outsource to Multiple CROs

Extended

Sample

Management

Independent

Functional

Modules

Sample

Management

Application

Integration

Quality

AssuranceCompetency

Management

Inventory

Management

Increased R&D Outsourcing by Pharma and Biotech Companies

7©2009 Frost & Sullivan, All rights reserved www.frost.com

CEO Integrated Industry Perspective

FluctuatingRaw MaterialLevels

Material Costs

Maintain Capital

SupplierRelationships

CEO

INTEGRATED

INDUSTRY

Secure Capital

1. Key Areas Spurs Integration of Pharmaceutical and Diagnostic Companies

2. Incorporation of Information Technology is the New Business Model.

3. The vertical alignment trend in the healthcare sector is affecting the clinical

diagnostic sector as well, and will strongly impact the healthcare industry

as a whole.

8©2009 Frost & Sullivan, All rights reserved www.frost.com

Incorporation of Information Technology is the New Business

Model

2010

Next Generation

Integrated Systems

20152015

Broader Data

Management

Tools

Patient

Support

Tools

Shareable

Personal

Health

Records

Web Portals

to EHR

Systems

Electronic

Management

of Sample

Transport

Reduced

Cost of

Logistics

Essential Part of

Clinical Diagnostics

Business

9©2009 Frost & Sullivan, All rights reserved www.frost.com

The Vertical Alignment in the Healthcare Sector Impacts Clinical

Diagnostics

Diagnostic Labs

Hospital and

Clinics

Healthcare

Insurance

Company

Vertical Alignment

Diagnostic Labs

Hospital and

Clinics

Healthcare

Insurance

Company

Interoperability

Healthcare Insurance Company

Hospital and Clinics Diagnostic Labs

Increasing Opportunities for Suppliers and IT

Infrastructure Providers

For Example: Alliance Technolgies is an Informational Technology and Healthcare services company that works

with payers, providers and patients to improve outcome and better manage costs by enabling secure flow of

clinical data between healthcare organizations

10©2009 Frost & Sullivan, All rights reserved www.frost.com

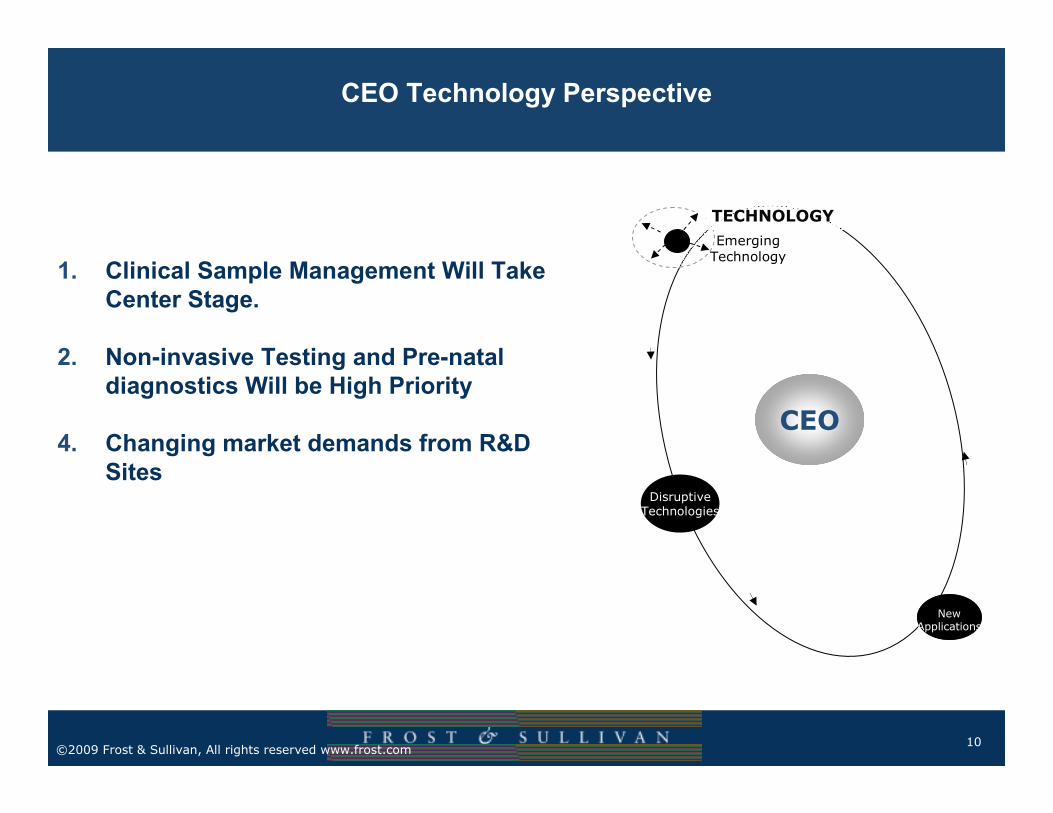

CEO Technology Perspective

NewApplications

DisruptiveTechnologies

TECHNOLOGY

EmergingTechnology

CEO

1. Clinical Sample Management Will Take

Center Stage.

2. Non-invasive Testing and Pre-natal

diagnostics Will be High Priority

4. Changing market demands from R&D

Sites

11©2009 Frost & Sullivan, All rights reserved www.frost.com

Clinical Sample Management Will Take Center Stage

Efficient storage

systems

to aid test

outsourcing

Use of non-invasive

Collection methods

With degree of

sophistication in clinical

sample handling, clinical

diagnostics will witness

growth in developing

countries

Use of chemical

techniques

to store samples

Use of nanofluidics

to improve

workflow

Use of non-invasive

collection methods

Clinical

SampleVolume

optimization

Transportation

Storage

Collection

12©2009 Frost & Sullivan, All rights reserved www.frost.com

Current Market Scenario Future Market Scenario

Automation

Multiplex

Lab-On-Chip

Integration

Fragment Based

Manual Handling

Immunoassays

Large Footprints

High Throughput

Screening

Stand-alone

Changing Market Demands from R&D Sites

Faster, Easier, Automated

13©2009 Frost & Sullivan, All rights reserved www.frost.com

ECONOMIC

Country Risk

Economic Trends &Issues

EconomicThreats

Economic Trends

CEO

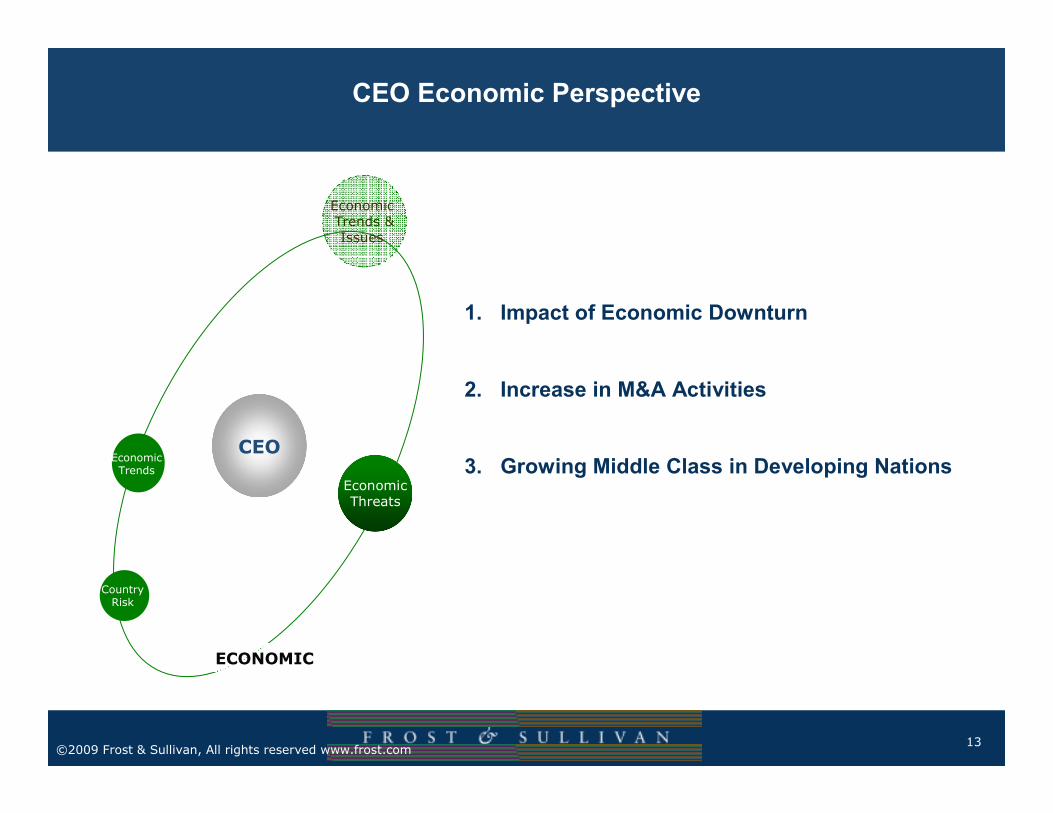

CEO Economic Perspective

1. Impact of Economic Downturn

2. Increase in M&A Activities

3. Growing Middle Class in Developing Nations

14©2009 Frost & Sullivan, All rights reserved www.frost.com

Global

Economic

Downturn

Unemployment Exchange Rate

Fluctuations

Savvy InvestmentsOperational

Efficiency

Negative

Positive

Global Economic Downturn Impacts the Industry

15©2009 Frost & Sullivan, All rights reserved www.frost.com

Test Kit

Providers

(Diagnostic

Companies)

Sample

Processing

Platform

Manufacturers

Test Service

Providers

(Laboratories)

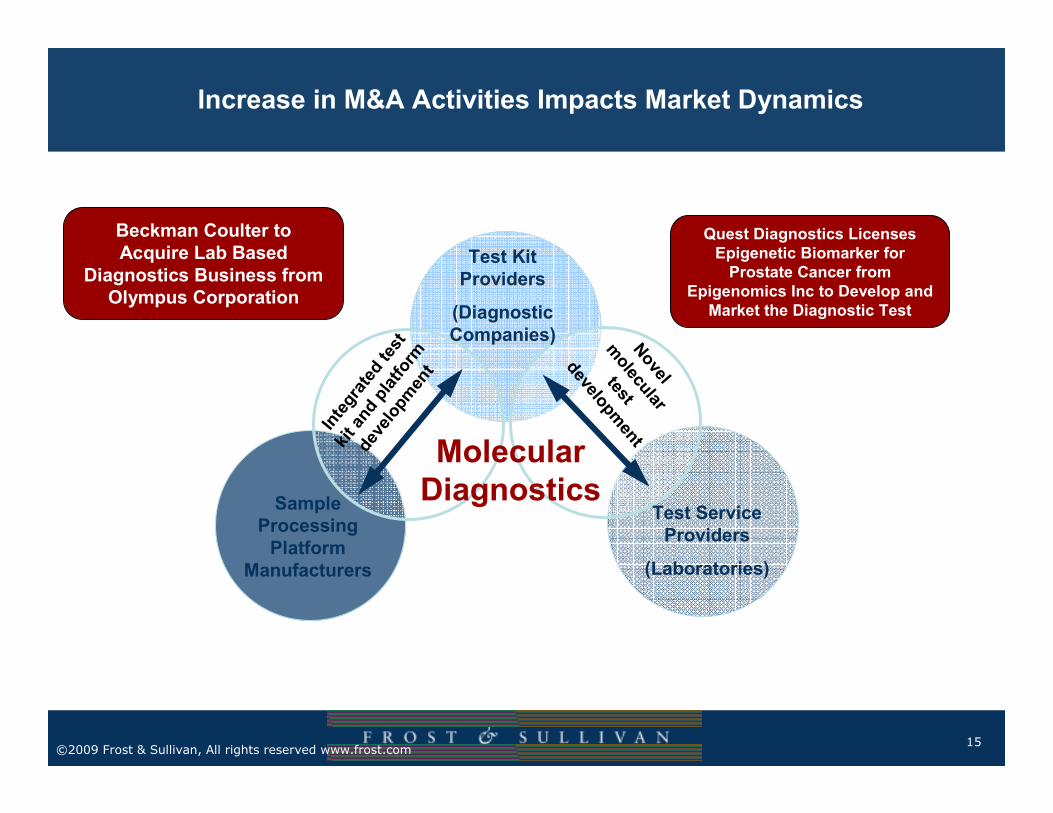

Molecular

Diagnostics

Integrated test

kit and platform

development

Novel

molecular

test

development

Quest Diagnostics Licenses

Epigenetic Biomarker for

Prostate Cancer from

Epigenomics Inc to Develop and

Market the Diagnostic Test

Beckman Coulter to

Acquire Lab Based

Diagnostics Business from

Olympus Corporation

Increase in M&A Activities Impacts Market Dynamics

16©2009 Frost & Sullivan, All rights reserved www.frost.com

CEO Competitive Perspective

In-Direc

t

Competi

tion

Competi

tive

Strategy

Competi

tive

Benchm

arking

Emergin

g

Competi

tion

COMPETITIVE

CEO

1. Diagnostic Potential of New Diseases Increases Competition.

2. Vendors Offer Competitive Workflows

17©2009 Frost & Sullivan, All rights reserved www.frost.com

Diagnostic Potential of New Diseases Increases Competition

2012

BENCH BED SIDE

Multiplex Detection

Panels for Cancer

Differentiated Product

Development

2005

2011

Increasing Competition

2020

Target miRNAs important

in cell differentiation

Multiplex Detection

Panels for Cardiac and Diabetes

Increasing Diagnostic

Tests

Differentiate between

Chronic & Life Style Diseases

18©2009 Frost & Sullivan, All rights reserved www.frost.com

Large up-front costs, Quality

disparitiesMergers & Acquisitions Maintain ‘best-in-class’ rep

Vendors Offer Complete Workflows to Remain Competitive

Validation

• RNAi

• Antisense

oligonucleotides

• Mimics and inhibitors

• shRNA

Sample Preparation Functional Analysis

• Sample collection

• Nucleic acid

purification

• Protein purification

• Automated liquid

handling

• Microarray

• Multiplex assay

• Sequencing

• High content screening

• Cell based assays

Detection and

Quantification Analysis

• qRT-PCR

• ELISA

• Mass spectrometry

• Western blotting

Workflow

Technologies

Validation

Strategies to Fill Workflow ChallengesBenefits

Revenues sharingAlliances Align with top provider

Large R&D costs In-house Development Easy integration

19©2009 Frost & Sullivan, All rights reserved www.frost.com

CEO Customer Perspective

CEOCUSTOMER

NonCustomer

Demo-graphics

Behavior

Competitor’sCustomers

1. Bargaining Power of Hospital and Physician Owned Labs

2. R&D Sites Prefer Walk Away Solutions

20©2009 Frost & Sullivan, All rights reserved www.frost.com

Endocrinologists, Family

practitioners & Internists are

leading adopters of these

testing methods in POLs

OB/GYN, Pediatricians,

and Cardiologists are

leading in adoption for

pregnancy, infectious

disease, and coagulation

tests, respectively

FOBT and urinalysis are

commonly used in many

specialties

0%

20%

40%

60%

80%

100%

Glucose handheld

meters HbA1c

Cholesterol/Lipid

Chemistry

analyzers

Immunoassay

analyzers

Drugs of Abuse

rapid test kits

Infectious Disease

rapid test kits

Pregnancy/Fertility

rapid test kits

Hematology

analyzers

Hemostasis

Coagulation

systems

Cardiac

Biomarkers

Fecal Occult

Blood Tests

Urinalysis systems

The current utilization pattern of tests in physician office laboratories illustrates high utilization for

glucose handheld meters, fertility test kits, fecal occult blood tests, and urinalysis systems.

Hospital and Physician-owned Laboratories Lead Routine Testing

Percentage of Physicians UtilizingTest

Internal Medicine Pediatrics OB/GYN Family Practice/GP Cardiology Endocrinology

Test Types

Utilized Testing by

Physician Specialty

21©2009 Frost & Sullivan, All rights reserved www.frost.com

Top Reasons for Satisfaction

(% of respondents, N=298)

Genomic Technology

Usefulness/

relevance to

research

Easy to

use

High

accuracy

Well integrated

with existing

technologies

High

specificity/

selectivity

PCR/Thermal cycling 21 43 5 7 12

Gel Based (Northern/ Southern) 16 28 16 4 11

Multiplex assay 16 6 15 4 3

qPCR/RT-PCR 24 15 20 3 28

CE sequencing 14 14 23 6 8

Next Generation sequencing 20 13 13 13 --

Microarray 28 14 6 10 7

Automated liquid handling 10 6 6 12 4

SMD platforms 20 15 20 10 20

DNA/RNA isolation & purification 19 29 5 6 2

RNA interference 47 15 6 6 16

Transfection 33 38 2 9 3

Ease-of-use features and technology integration are critical for customer satisfaction in the

fast-paced and demanding end-user community for drug discovery technologies.

R&D Sites Prefer Easy-to-use Walk-away Solutions

Secondary Reason for SatisfactionPrimary Reason for Satisfaction

22©2009 Frost & Sullivan, All rights reserved www.frost.com

Contents

Diagnostics

Industry

Briefing

2.

3.

1. 360 Degree Perspective

APAC Market Outlook

Industry Best Practices

23©2009 Frost & Sullivan, All rights reserved www.frost.com

10 Key Trends in the Asian Health Care Industry

1) Cost & Quality, & Demographics of Healthcare1) Cost & Quality, & Demographics of Healthcare

2) Changing Demographics – Aging Population2) Changing Demographics – Aging Population

3) Changing Business Models 3) Changing Business Models

4) Evolving and Unique Disease Profiles4) Evolving and Unique Disease Profiles

5) Medical Tourism & Wellness5) Medical Tourism & Wellness

6) Insurance : Increasing Accessibility6) Insurance : Increasing Accessibility

7) Technology as a Driver7) Technology as a Driver

8) Human Resources : The Reverse Brain Drain8) Human Resources : The Reverse Brain Drain

9) Private Public Partnerships9) Private Public Partnerships

10) Increasing M&A/ Private Equity Activity10) Increasing M&A/ Private Equity Activity

“Globalization has radically altered

the business model for service and

manufacturing industries.

Health, traditionally regarded

as a local industry, is becoming

global as well. It’s changing

the way the Chinese think about

financing hospitals, Americans

recruit physicians, Australians

reimburse providers for care,

Europeans embrace competition,

and Middle Eastern governments

build for future generations”.

24©2009 Frost & Sullivan, All rights reserved www.frost.com

Spending on Diagnostics Set to Increase

Asia Healthcare Spend by Area, 2009-2020

• Major opportunities within

diagnostics and

monitoring

• Products and services will

not be standalone but will

be “packaged” to target

specific diseases.

• Example : predict avian

flu, diagnose, treat,

monitor

25©2009 Frost & Sullivan, All rights reserved www.frost.com

Focus by Disease Areas

26©2009 Frost & Sullivan, All rights reserved www.frost.com

Contents

Diagnostics

Industry

Briefing

2.

3.

1. 360 Degree Perspective

APAC Market Outlook

Industry Best Practices

27©2009 Frost & Sullivan, All rights reserved www.frost.com

Value system

Educate

IntegrateInnovate

Invest

To provide

cost

effective

solution

To gain

competitive

edge

To frame

winning

strategies

To create

brand

loyalty

Invest in technology

to develop cost

effective scalable

solutions with high

robustness

Develop innovative

esoteric tests with

high clinical

relevance for

existing diseases

Integrate novel tests

with existing

platforms to provide

comprehensive test

menu

Provide educational

awareness to

promote novel

predictive tests

Best Practice (1)

Durable Competitive Advantage Drives Growth

New Technology meets a market need and value

J Reduction in death

' Reduction in disease burden

' Reduction in disease management cost

28©2009 Frost & Sullivan, All rights reserved www.frost.com

Patient FocusedPatient Focused

Productivity Improvement StrategiesProductivity Improvement StrategiesProductivity Improvement Strategies

Integrative Integrative

Systems BiologySystems Biology

ProteomicsProteomics

TranscriptomicsTranscriptomics

GenomicsGenomics

Integrative Integrative

Workflow Workflow

TechnologiesTechnologies

InfoTechInfoTech

Enhance Customer Enhance Customer

BaseBase

MetabolomicsMetabolomics

Bio StatisticsBio Statistics Clinical ResearchClinical Research

Molecular BiologyMolecular Biology

Best Practice (2)

Durable competitive advantage through integrated approach

29©2009 Frost & Sullivan, All rights reserved www.frost.com

Thank You!