106

SEC and Financial Reporting Institute 36th Annual SEC and Financial Reporting Institute Conference June 8, 2017 Millennium Biltmore Hotel Los Angeles, California

| Date post: | 03-Jun-2018 |

| Category: |

Documents |

| Upload: | truongdung |

| View: | 224 times |

| Download: | 2 times |

SEC and Financial Reporting Institute

36th Annual

SEC and Financial Reporting Institute Conference June 8, 2017 Millennium Biltmore Hotel Los Angeles, California

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

DOCUMENT INDEX

20170605

SEC and Financial Reporting Institute

Program and Speakers

1. Program

2. Speakers and Speaker Biographies

Presentation Slides

3. Session 1 - FASB Update

4. Session 2 & 3 - Current Accounting and Auditing Practice Issues

5. Session 5 - Being a CPA in the data age

6. Session 7 - Implementing “New GAAP”: Revenue Recognition, Leases, and Financial Instruments

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

PROGRAM

20170604

SEC and Financial Reporting Institute

Morning Sessions | Crystal Ballroom and Tiffany Room . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7:30 - 8:30 Registration and Continental Breakfast

8:30 - 8:40 SEC and Financial Reporting Institute Welcome

Lori L. Smith Assistant Professor USC Leventhal School of Accounting

William W. Holder Dean, Leventhal School of Accounting Alan Casden Dean’s Chair in Accounting USC Leventhal School of Accounting

8:40 - 9:50 Opening Addresses by the SEC and the FASB

Wesley R. Bricker Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

Matthew Esposito Assistant Director Financial Accounting Standards Board

9:50 - 10:35 Current Accounting & Auditing Practice Issues - Part I

Moderator Panelists John W. White Partner Cravath, Swaine & Moore LLP

Mark Kronforst Chief Accountant Division of Corporation Finance U.S. Securities and Exchange Commission

Marc Panucci Deputy Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

John May Partner, SEC Services Leader PricewaterhouseCoopers LLP

Sharon Varig VP, Controller and Chief Accounting Officer Aetna

10:35 - 10:50 Refreshment Break

10:50 - 12:40 Current Accounting & Auditing Practice Issues - Part II

Moderators Panelists John W. White Partner Cravath, Swaine & Moore LLP

Mark Kronforst Chief Accountant Division of Corporation Finance U.S. Securities and Exchange Commission

Marc Panucci Deputy Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

Lori L. Smith Assistant Professor USC Leventhal School of Accounting

John May Partner, SEC Services Leader PricewaterhouseCoopers LLP

Sharon Varig VP, Controller and Chief Accounting Officer Aetna

Helen A. Munter Director Registration and Inspections Public Company Accounting Oversight Board

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

PROGRAM

20170604

SEC and Financial Reporting Institute

Luncheon and Keynote Presentation | Biltmore Bowl . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

12:50 - 2:20 Luncheon and Keynote Presentation A Conversation with Jeannette Franzel, PCAOB Board Member

Introductions Luncheon Presentation Roger Molvar Board Member PacWest Bancorp

Dennis R. Beresford Executive in Residence J.M. Tull School of Accounting University of Georgia

Jeanette M. Franzel Board Member Public Company Accounting Oversight Board

Afternoon Sessions | Crystal Ballroom and Tiffany Room . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2:30 - 3:15 Being a CPA in the Digital Age

Moderator Panelist Lori L. Smith Assistant Professor USC Leventhal of School of Acctg

Max Carrier National Partner-in-Charge, eAudIT, KPMG Global

Delivery Center and Audit Data & Analytics KPMG LLP

3:15 - 4:05 OCA Consultation Trends

Moderator Panelist Scott A. Taub Managing Director Financial Reporting Advisors, LLC

Sagar Teotia Deputy Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

4:05 - 4:15 Refreshment Break

4:15 - 5:30 Implementing “New GAAP”: Revenue Recognition, Leases, Financial Instruments

Moderator Panelists Scott A. Taub Managing Director Financial Reporting Advisors, LLC

Kristin Bauer Partner Deloitte & Touche LLP

Joshua D. Paul Director, Technical Accounting Google

Rahul Gupta Partner, National Professional Standards Grant Thornton LLP

Shari Mager Managing Director KPMG LLP

Rick Lawlor Senior Finance Director, Corporate Accounting Microsoft

Reception | Tiffany Room . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5:30 - 6:30 Reception

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKERS

SEC and Financial Reporting Institute

Dennis R. Beresford Executive in Residence J.M. Tull School of Accounting

University of Georgia

Kristin Bauer Partner Deloitte & Touche LLP

Wesley R. Bricker Chief Accountant Office of the Chief Accountant

U.S. Securities and Exchange Commission

Max Carrier National Partner-in-Charge, eAudIT

KPMG LLP

Matthew Esposito Assistant Director Financial Accounting Standards Board

Jeanette M. Franzel Board Member Public Company Accounting Oversight Board

Rahul Gupta Partner, National Professional Standards Group

Grant Thornton LLP

William W. Holder Dean, Leventhal School of Accounting

Alan Casden Dean’s Chair in Accounting

USC Leventhal School of Accounting

Mark Kronforst Chief Accountant Division of Corporation Finance

U.S. Securities and Exchange Commission

Rick Lawlor Senior Finance Director, Corporate Accounting

Microsoft

Shari Mager Managing Director KPMG LLP

John May Partner, SEC Services PricewaterhouseCoopers LLP

Roger H. Molvar Board Member PacWest Bancorp

Helen A. Munter Director Division of Registration and Inspections

Public Company Accounting Oversight Board

Marc Panucci Deputy Chief Accountant Office of the Chief Accountant

U.S. Securities and Exchange Commission

Joshua D. Paul Director, Technical Accounting

Scott A. Taub Managing Director Financial Reporting Advisors, LLC

Sagar Teotia Deputy Chief Accountant Office of the Chief Accountant

U.S. Securities and Exchange Commission

Sharon Varig VP, Controller and Chief Accounting Officer

Aetna

John W. White Partner Cravath, Swaine & Moore LLP

20170604

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 1

SEC and Financial Reporting Institute

Dennis (Denny) R. Beresford is Executive in Residence at the J. M. Tull School of Accounting, Terry College of Business, University of Georgia. From July 1997 through June 2013 he was Ernst & Young Executive Professor of Accounting. From January 1987 through June 1997 he was chairman of the Financial Accounting Standards Board. Previously, he was national director of accounting standards for Ernst & Young. He is a graduate of the University of Southern California. Denny previously served on the boards of National Service Industries, Inc., WorldCom (MCI), Inc., Kimberly-Clark Corporation, Fannie Mae, and Legg Mason, Inc. He is also a member of the board of directors of the National Association of Corporate Directors and the Financial Reporting Committee of the Institute of Management Accountants. In 1995, Denny was awarded an honorary Doctor of Humane Letters degree from DePaul University. In 2004 he was elected to the Accounting Hall of Fame and received the AICPA Gold Medal for distinguished service. In 2006 he was selected as one of the inaugural inductees of Financial Executives International’s Hall of Fame. In 2012 the Journal of Accountancy named him as one of the “125 people of impact in accounting,” as among those who have had the most impact on the accounting profession since the AICPA was founded in 1887. In 2013 he received the Institute of Management Accountants’ first Distinguished Member Award.

Dennis R. Beresford Executive in Residence J.M. Tull School of Accounting University of Georgia

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 2

SEC and Financial Reporting Institute

Kristin Bauer Partner - National Office Deloitte & Touche LLP

Kristin Bauer specializes in technical accounting at Deloitte’s National Office serving as a consultation resource to engagement teams serving a broad range of industries. She specializes in revenue recognition and leases and has extensive experience in current implementation efforts. In her current role, Ms. Bauer’s responsibilities include formulating firm policies and interpretative guidance on accounting standards for Deloitte professionals, clients, and other parties interested in financial reporting and in communicating with accounting standard setters and regulators. Prior to rejoining Deloitte in 2014, Kristin was a Practice Fellow at the Financial Accounting Standards Board (FASB) from 2010 to 2014. During her time at the FASB, she led the FASB’s revenue recognition project team that developed the final revenue standard (ASU 2014-09 and IFRS 15). She was also a key contributor to the project team responsible for improving the financial reporting of leases, ultimately resulting in ASC 842 and IFRS 16. Before her fellowship, Kristin served in various roles in Deloitte’s National Office. As a consultation resource, she assisted engagement teams with addressing issues related to restatements, assessments of materiality, management integrity, possible fraud and illegal acts and client continuance. Kristin started her career in Deloitte’s Chicago office and served clients in that market for 10 years. Immediately prior to joining National Office, she was the lead senior manager on the IPO and subsequent-year audit of a newly created carve-out entity. She concentrated on large, public multinational clients and addressed technical accounting matters including adoption of new accounting pronouncements, carve-outs, acquisitions, and divestitures. Certified Public Accountant – Illinois and Connecticut Bachelor of Science in Accountancy, with Honors – University of Illinois — Urbana Champaign

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 3

SEC and Financial Reporting Institute

Wesley R. Bricker Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

Wes is the Chief Accountant for the U.S. Securities and Exchange Commission. In the role, he serves as the principal advisor to the SEC on accounting and auditing matters. He consults with registrants, auditors and other industry representatives, and is responsible for the oversight of the Financial Accounting Standards Board (FASB) and the Public Company Accounting Oversight Board (PCAOB), among the other duties of the Chief Accountant. He joined the SEC from PricewaterhouseCoopers LLP, where he was a partner responsible for clients in the banking, capital markets, financial technology, and investment management sectors. Earlier, he served as a professional accounting fellow in Office of the Chief Accountant and prior to that held various audit and professional practice positions at PwC, including in the firm’s national office during the global financial crisis advising on complex financial accounting matters. Mr. Bricker is trained as an accountant and lawyer with degrees from Elizabethtown College and the American University Washington College of Law. He is licensed to practice as a certified public accountant in Virginia, Maryland, the District of Columbia, Pennsylvania, and New Jersey and as an attorney in New York.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 4

SEC and Financial Reporting Institute

Max Carrier National Partner-in-Charge, eAudIT, KPMG Global Delivery Center and Audit Data & Analytics KPMG LLP

Max has been with KPMG for 37 years, successfully serving in a number of leadership positions. Max is currently the National Partner-in-Charge of eAudIT, KPMG Global Delivery Center and Audit Data & Analytics. Max’s leadership responsibilities have included financial and operations management, technology and data & analytics development, deployment and support, change management, centralization and standardization of services, budgeting and forecasting, strategic planning, assuring the global delivery of KPMG’s commitment to client care and audit quality, retaining and developing key resources, risk management, audits of Fortune 500 companies, and representing the Firm in the marketplace and business community. He is currently instrumental in the development and implementation of KPMG’s Data & Analytics Masters Program with Universities across the country. Publications and speaking engagements

• Presenter for Houston TSCPA Foundation and the Business and Industry Committee Expo focusing on the topic of data and analytics

• Panelist for American Accounting Association’s Accounting Programs Leadership Group and the Federation of Schools of Accountancy Annual Seminar on the topic of Big Data Resources

• Moderator and panelist for KPMG’s Audit Committee Institute Roundtable Series, focusing on the responsibilities and challenges of today’s audit committee members.

• Moderator and panelist at National Association of Corporate Director’s educational seminars discussing board and audit committee responsibilities and challenges, corporate governance and technology concerns.

• Guest lecturer to the undergraduate program at the University of Texas at Dallas, the Corporate Governance MBA program at Southern Methodist University, and the Masters in Accounting Program at The Ohio State University.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 5

SEC and Financial Reporting Institute

Matthew Esposito Assistant Director Financial Accounting Standards Board

Matthew Esposito is an assistant director of technical activities at the Financial Accounting Standards Board (FASB). Mr. Esposito oversees various technical areas, including those related to the accounting for financial instruments, credit losses, consolidation, and leases. He joined the FASB’s research and technical activities staff in September 2013. Before joining the FASB, Mr. Esposito was a director in Citigroup’s Accounting Policy Group in New York. Prior to joining Citigroup in December 2010, Mr. Esposito was a director in the Financial Instruments and Credit Group of PricewaterhouseCoopers and alum of their National Professional Services Group. Mr. Esposito has over 17 years of experience in the financial services industry, advising on technical accounting issues related to financial instruments under U.S. GAAP. He focused on technical accounting related to financial asset transfers, derivatives and hedging activities, credit losses, consolidation, and debt and equity classification matters. Mr. Esposito has extensive experience working with mortgage and asset-backed securities, loan products, derivatives, and customized structured transactions. Mr. Esposito has a B.S. in accounting from Binghamton University. He is a CPA in New York.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 6

SEC and Financial Reporting Institute

Jeanette M. Franzel Board Member Public Company Accounting Oversight Board

Jeanette M. Franzel is a Board Member of the Public Company Accounting Oversight Board (PCAOB). PCAOB’s mission is to oversee the audits of public companies and brokers and dealers to protect investors and further the public interest. Board Member Franzel brings extensive audit experience to the PCAOB after a distinguished career at the U.S. Government Accountability Office (GAO). She ended her tenure as Managing Director, overseeing all aspects of GAO’s financial audits of the U.S. federal government. From 2008 through 2011, Ms. Franzel’s team provided oversight of the U.S. government’s efforts to stabilize the financial markets and promote economic recovery. Earlier in her career, Ms. Franzel audited the federal government’s actions to resolve over one thousand failed banks and savings and loan institutions. Ms. Franzel has testified before congressional committees more than a dozen times. Ms. Franzel holds the following professional certifications: CPA, CIA, CMA and CGFM.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 7

SEC and Financial Reporting Institute

Rahul Gupta Partner, National Professional Standards Group Grant Thornton LLP

Rahul is a Partner in the National Professional Standards Group (NPSG) of Grant Thornton LLP. Rahul assists engagement teams and clients with technical accounting issues and monitors current accounting developments, under both U.S. GAAP and IFRS. Rahul is also involved in developing firm’s thought leadership on accounting issues, including liaising with Financial Accounting Standards Board (FASB), International Accounting Standards Board (IASB), AICPA and Securities and Exchange Commission. Rahul has more than sixteen years of public accounting experience in the United States and India. Rahul was a staff member at FASB from August 2011 through January 2016, where he provided technical depth and practical insight to assist the FASB in improving U.S. GAAP. Prior to joining the FASB, he was a senior manager in the firm’s NPSG, where he assisted engagement teams and firm’s clients with technical accounting issues. Prior to joining the NPSG, Rahul worked in the firm’s Dallas audit practice. In India, Rahul started his career working in the audit practice of Grant Thornton International’s Indian member firm in New Delhi focusing on clients that reported under U.S. GAAP. Rahul is a Certified Public Accountant in Texas and Illinois, and a Chartered Accountant (Associate Member) in India. Rahul holds a Bachelor of Commerce degree from Agra University, India, and a Post Graduate Diploma in Information System Audit from the Institute of Chartered Accountants of India.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 8

SEC and Financial Reporting Institute

William W. Holder Dean, Leventhal School of Accounting and Alan Casden Dean’s Chair in Accounting USC Leventhal School of Accounting

William Holder serves as Dean of the USC Leventhal School of Accounting, and holds the Alan Casden Dean’s Chair of Accountancy. Prior to his current post, Dean Holder was the Ernst & Young Professor of Accounting and Director of the SEC and Financial Reporting Institute in the Marshall School of Business at the University of Southern California. Dean Holder is an expert on financial reporting and auditing. He has published extensively on these subjects and received numerous awards during his career, including being twice named as one of the “Top 100 People” in the accounting profession and receiving the AICPA Gold Medal for Distinguished Service, the highest honor awarded by that organization. He has served on a number of governance and standard setting authorities including the Accounting Standards Executive Committee of the AICPA and the Governmental Accounting Standards Board. During Congressional hearings leading to passage of the Sarbanes/Oxley Act, he provided invited testimony about financial reporting, auditing and corporate governance.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 9

SEC and Financial Reporting Institute

Mark Kronforst Chief Accountant Division of Corporation Finance U.S. Securities and Exchange Commission

Mark Kronforst is the Chief Accountant in the Division of Corporation Finance at the U.S. Securities and Exchange Commission. Mark’s previous roles in the Division include Associate Director – Disclosure Operations and Deputy Chief Accountant. Before joining the Division in 2004, Mark worked for a large SEC registrant as the Director of Financial Reporting and as an audit senior manager in KPMG’s Silicon Valley and Minneapolis offices.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 10

SEC and Financial Reporting Institute

Rick Lawlor Senior Finance Director, Corporate Accounting Microsoft

As Microsoft’s Senior Finance Director in Corporate Accounting, Rick Lawlor is responsible for leading the global implementation of the New Leases Accounting Standard. Corporate Accounting is responsible for ensuring sound financial reporting and internal controls at the Microsoft. For the past 2 years, Rick has led the Central Finance team for Microsoft’s Cloud Infrastructure Finance team, transforming and managing Financial Planning & Analysis, Reporting & Systems, Standard Cost Allocations and Controls & Compliance across Microsoft’s commercial and consumer cloud businesses. Previously, Mr. Lawlor led the finance team for Microsoft’s Global Foundation Services division that delivers the cloud infrastructure and foundational technologies to power Microsoft’s online businesses worldwide. He was responsible for a significant team who managed the financial planning & analysis, capex management, operations, and accounting for cloud infrastructure and foundation technologies that powers Microsoft’s cloud services worldwide. Lawlor joined Microsoft in 2005 and previously led Strategy Sourcing and Procurement in the Windows & Online Services Divisions. Prior to Microsoft, he served as the CFO for Travelport a subsidiary of Cendant, where he was responsible for the financial management and was deeply involved in the company’s successful acquisition of Orbitz. Prior to Travelport/Cendant, he led a variety of business development and finance roles at two technology start-ups. Also he was a management consultant for PricewaterhouseCoopers and auditor for Deloitte & Touche. Mr. Lawlor graduated from The American University with a bachelor’s degree in Accounting and a Masters of Business Administration.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 11

SEC and Financial Reporting Institute

Shari Mager Managing Director Deal Advisory KPMG LLP

Shari Mager is a leader within KPMG’s M&A deal advisory practice, with a focus on accounting advisory, company mergers/acquisitions/divestitures, as well as debt and capital raises. In 20 years of consulting, Shari has managed domestic and international projects and relationships. Shari often serves as the senior adviser to executive teams of companies tackling their most challenging issues, including accounting change, M&A, and organizational transformation. Shari focuses on transactions, accounting advisory, equity, and debt capital raising for clients in a wide variety of industries, including technology, real estate, hospitality, healthcare, and life sciences. In her leadership role, Shari regularly exchanges ideas and discusses emerging issues with clients, in order to share insights and best practices. Shari has extensive experience in advising both financial sponsors and management teams of publicly-traded and privately-owned companies, as well as their board members, on financial accounting and reporting matters, and operational aspects of transactions. Shari is a frequent presenter at various Accounting & Reporting, M&A and IPO conferences and summits. Shari began her professional career in KPMG’s audit practice, and is a licensed CPA in Canada and in the US (California and North Carolina).

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 11

SEC and Financial Reporting Institute

John May Partner, SEC Services PricewaterhouseCoopers LLP

John has been a partner in PwC’s National Office for 16 years and is the leader of PwC's National SEC Services Group. From 1989 until 1996, John worked in PwC's Chicago office where he served public and private growth-oriented companies with a concentration in the manufacturing sector. From 1996 until 2000, he worked in PwC's Kansas City office where he focused on multinational SEC registrants in the transportation and services sectors. John is a member of the Center for Audit Quality SEC Regulations Committee and recently completed a two year term as the Committee’s chair. Additionally, John is a member of the CAQ's SEC Audit Practices Task Force. John is also a principal editor and author of a number of PwC publications including PwC's SEC Volume--a comprehensive manual for SEC registration and reporting.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 12

SEC and Financial Reporting Institute

Roger Molvar Board Member PacWest Bancorp

Roger H. Molvar serves as a director and member of the audit and the compensation, nominating, and governance committees of PacWest Bancorp, the largest independent bank headquartered in Los Angeles. In 2014, CapitalSource Bank merged with PacWest Bank in what was described as one of the top value creating banking transactions of the year. At CapitalSource Bank, Roger was a founding director and chair of both the audit and the risk management committees. Prior board service includes Farmers & Merchants Bank, La Opinión Media, and numerous civic and non-profit entities. From 2000 to 2004, Roger was chief executive officer of IndyMac Consumer Bank and previously, was an executive officer and management committee member of The Times Mirror Company, which was acquired by media giant Tribune Co. in 2000. Roger is chairman of the SEC and Financial Reporting Institute at the University of Southern California. He is an active participant in the West Audit Committee Network, which facilitates discussions on enhancing corporate governance, and serves on the Editorial Advisory Board of the AICPA’s Journal of Accountancy. He received his undergraduate degree in business administration from the University of Washington and is a graduate of the Graduate School of Financial Management at Dartmouth and the Stanford University Advanced Management College.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 13

SEC and Financial Reporting Institute

Helen A. Munter Director Division of Registration and Inspections Public Company Accounting Oversight Board

Helen Munter is the director of the Division of Registration and Inspections, which is the PCAOB’s largest operating division. Ms. Munter oversees all division operations including firm registration, the Global Network Firm Inspection Program, the Non-Affiliate Firm Inspection Program, and the Broker-Dealer Interim Inspection Program. Prior to being named director in 2011, Helen was a deputy director and team leader for several of the PCAOB’s largest and most complex inspections. During her tenure as deputy director, Helen led the team of accountants that established many of the inspections processes that are in place today. In addition, she was responsible for opening the PCAOB’s San Mateo office where she served as regional leader until she assumed the role of division director. Before joining the PCAOB in 2004, Helen was an audit partner and deputy director of professional practice in the San Francisco office of Deloitte & Touche LLP. She spent 16 years at Deloitte in the San Francisco and Barcelona, Spain offices. Helen received a B.A. from the University of California at Berkeley. She is a certified public accountant and is fluent in Spanish.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 14

SEC and Financial Reporting Institute

Marc Panucci Deputy Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

Marc is a Deputy Chief Accountant in the Office of the Chief Accountant at the U.S. Securities and Exchange Commission (SEC). His responsibilities include leading the activities of the Office of the Chief Accountant’s Professional Practice Group (PPG). These activities include understanding investor and audit committee perspectives and consulting with registrants and auditors on the application of internal control over financial reporting obligations, independence requirements and auditing standards. He also assists the SEC in its oversight responsibility for the activities of the Public Company Accounting Oversight Board (PCAOB) and monitors the development of auditing standards, both in the U.S. and internationally. Before joining the Commission, Marc was a Partner at PwC from 2010 to 2016. His responsibilities included providing consultation and support regarding implementation, application, and development of auditing policies and standards, including leading the firm’s efforts related to internal control over financial reporting consultations. Marc was also responsible for the development of the firm’s positions related to international and domestic audit standard-setting matters. Marc was also a board member of the AICPA’s Auditing Standard Board (ASB). The ASB is responsible for development of auditing standards and guidance related to non-issuers. Marc also previously worked at the SEC from 2007 to 2010, including as a Senior Associate Chief Accountant in the Office of the Chief Accountant. During this time, he specialized in the SEC's guidance related to the evaluation of internal control over financial reporting, auditing matters relating to public companies, and the SEC's activities with respect to its oversight role over the PCAOB. Marc received a Bachelor of Science degree in Accounting from Robert Morris College. He is a Certified Public Accountant in Pennsylvania and New Jersey.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 15

SEC and Financial Reporting Institute

Joshua D. Paul Director, Technical Accounting Google

Josh is the Director of Technical Accounting at Google, leading Google’s technical accounting & policy, SEC reporting and treasury accounting. Josh was previously a partner at PricewaterhouseCoopers. He has diverse experience serving a variety of companies including Fortune 500 public companies. He has experience ranging from large, complex multinationals to small and mid-cap companies. Josh also was in PwC’s National Office and handled hundreds of client consultations. He focused on revenue recognition, stock-based compensation, and business combinations. While in PwC’s National Office, Josh spoke regularly at Firm, client and industry events around the country. Josh was also Professional Accounting Fellow in the Office of the Chief Accountant of the U.S. Securities and Exchange Commission. In this role, he worked with registrants on complex accounting and reporting matters, monitored the activities of various professional accounting standard setting bodies within the United States and internationally, and worked on various regulatory matters facing U.S. capital markets.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 16

SEC and Financial Reporting Institute

Lori L. Smith Director SEC and Financial Reporting Institute Assistant Professor of Clinical Accounting USC Leventhal School of Accounting

Lori Smith is an expert in auditing and financial accounting and reporting with extensive experience from two perspectives - as an audit and assurance partner with a global professional services firm and as a company executive for a fortune 500 public company. Lori is Assistant Professor of Clinical Accounting at the USC Leventhal School of Accounting, focusing on public company financial reporting and ethics. She also serves as Assistant Dean for Academic Administration for USC Leventhal and as Director for the SEC and Financial Reporting Institute. Prior to joining USC, Lori was an audit and assurance partner with Deloitte and Touche LLP and Director of Accounting for Bergen Brunswig Corporation. Lori received a Bachelor of Science degree in Accounting from University of Southern California and is a certified public accountant licensed in California.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 17

SEC and Financial Reporting Institute

Scott A. Taub Managing Director Financial Reporting Advisors, LLC

Scott A. Taub joined Financial Reporting Advisors, LLC (FRA) as a Managing Director in 2007. Based in Chicago, Illinois, FRA provides consulting services related to accounting and SEC reporting and litigation support services. From September 2002 through January 2007, Mr. Taub was a Deputy Chief Accountant at the Securities and Exchange Commission (SEC). He twice served as Acting Chief Accountant for a total of 14 months. He played a key role in the SEC’s implementation of the accounting reforms under the landmark Sarbanes-Oxley Act, and was responsible for the day-to-day operations of the Office of the Chief Accountant, including resolution of accounting and auditing practice issues, rulemaking, oversight of private sector standard-setting efforts, and regulation of auditors. Mr. Taub represented the SEC in many venues, including the FASB and IASB’s advisory committees, and in front of the House Financial Services Subcommittee on Capital Markets, Insurance and Government Sponsored Enterprises. He also served as the SEC Observer to the FASB’s Emerging Issues Task Force (EITF) and as Chair of the Accounting and Disclosure committee of the International Organization of Securities Commissions (IOSCO). He twice served as Acting Chief Accountant for a total of 14 months. Mr. Taub also was a member of the SEC staff between 1999 and 2001 as a Professional Accounting Fellow in the Office of the Chief Accountant. Prior to September 2002, Mr. Taub was a partner in Arthur Andersen's national office. The role of that group within Andersen was to consult on complex financial reporting matters; establish and disseminate Andersen’s policies regarding financial reporting matters; and represent the firm before various standards setters including the FASB, SEC, AICPA, and IASB. Mr. Taub consulted and authored interpretive guidance for Andersen on a wide variety of accounting and reporting issues, including revenue recognition, business combinations, compensation arrangements, intangible assets, and investment accounting. Prior to joining Andersen’s national office, he was member of the audit practice in the firm’s Detroit office serving publicly held and privately owned companies in a variety of industries.

(continues)

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 18

SEC and Financial Reporting Institute

Scott A. Taub (continued) Mr. Taub is currently a member of the FASB/IASB Joint Transition Group for Revenue Recognition. He previously served on the IASB's IFRS Interpretations Committee and the FASB’s Valuation Resource Group. He is a frequent speaker, having addressed numerous audiences sponsored by a variety of organizations. He was the primary author of several SEC reports and publications, including the Report and Recommendations Pursuant to Section 401(c) of the Sarbanes-Oxley Act of 2002 On Arrangements with Off-Balance Sheet Implications, Special Purpose Entities, and Transparency of Filings by Issuers and the Study Pursuant to Section 108(d) of the Sarbanes-Oxley Act of 2002 on the Adoption by the United States Financial Reporting System of a Principles-Based Accounting System. Mr. Taub is the author of the Revenue Recognition Guide, a 500-page comprehensive guide to accounting for revenue recognition published by CCH and a co-author of CCH's Financial Instruments Guide. Mr. Taub attended the University of Michigan in Ann Arbor, where he received an undergraduate degree in economics in 1990, and won the William A. Paton Award for his performance on the CPA exam. In 2005 Mr. Taub won the SEC’s award for Supervisory Excellence. He is a licensed CPA in Michigan and is a member of the American Institute of Certified Public Accountants.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 19

SEC and Financial Reporting Institute

Sagar Teotia Deputy Chief Accountant Office of the Chief Accountant U.S. Securities and Exchange Commission

Sagar Teotia is currently the Deputy Chief Accountant in the Office of the Chief Accountant (OCA) at the U.S. Securities and Exchange Commission (SEC). In this role, Mr. Teotia leads the activities of the office’s accounting group which includes consulting with public companies and divisions and offices within the SEC on the application of accounting standards and financial disclosure requirements. Mr. Teotia also serves as an advisor to the Commission on accounting matters while also working closely with private sector bodies such as the Financial Accounting Standards Board (FASB). Prior to Mr. Teotia joining as Deputy Chief Accountant of the SEC, Mr. Teotia was a Partner at Deloitte in the National Office Accounting Consultation group (Accounting Consultation) in Chicago. In his role in Accounting Consultation, he frequently consulted on accounting and reporting issues related to financial instruments, business combinations, and compensation (stock based and pension). Prior to joining Deloitte’s National Office in Chicago, Mr. Teotia was a professional accounting fellow (PAF) in OCA at the SEC. Mr. Teotia’s responsibilities as a PAF included providing accounting conclusions on complicated technical accounting issues to SEC Registrants, actively monitoring and providing oversight comments to the FASB on current standard setting projects, and working on several special projects within OCA. Mr. Teotia received an accounting degree from the University of Illinois at Urbana-Champaign. He is licensed to practice as a certified public accountant in Illinois.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 20

SEC and Financial Reporting Institute

Sharon Virag VP, Controller and Chief Accounting Officer Aetna

Sharon Virag is the VP, Controller and Chief Accounting officer of AETNA, a Fortune 50 diversified healthcare benefits company with over $60 billion in revenue, where she is responsible for controllership, tax, treasury, Finance Transformation and Finance Shared Services for the company. Sharon is also a member of the Financial Accounting Standards Advisory Council (FASAC), a group that advises the Financial Accounting Standards Board (FASB) on matters related to board projects and agenda prioritization, as well as a member of the Corporate Reporting Committee of the Financial Executives Institute (FEI). Prior to joining Aetna, Sharon was the Vice President, Chief Accounting Officer of AES Corp., a global power company operating in 23 countries, generating $17 billion in annual revenues on $42 billion in assets under management. She also held Global Controller positions at several General Electric businesses between 2010 and 2013, as well as multiple posts, both domestic and international, at General Motors Company (“GM”) from 2008 to 2010, including Assistant Corporate Controller; Controller, GM AsiaPacific; and Director of Internal Control and Sox Compliance. In addition to her private sector experience, Sharon was with the Public Company Accounting Oversight Board (“PCAOB”) from 2005 to 2008, where she served as the project leader for Auditing Standard No. 5, the Board’s requirements/regulations for Sarbanes-Oxley Section 404, and acted as staff liaison to the Securities & Exchange Commission Advisory Committee on Improvements to Financial Reporting (CiFER), among other roles. Sharon started her financial career in auditing, including working for Deloitte & Touche, LLP from 1998 to 2004 as an Audit Senior Manager and Audit Manager. She has a BS in Accounting from California State University and is a Certified Public Accountant in the State of Arizona.

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 21

SEC and Financial Reporting Institute

John W. White Partner Cravath, Swaine & Moore LLP

John W. White is a partner in Cravath’s Corporate Department and serves as Chair of its Corporate Governance and Board Advisory practice. From 2006 through 2008, he served as Director of the Division of Corporation Finance at the U.S. Securities and Exchange Commission, which oversees disclosure and reporting by public companies in the United States. While on the SEC staff, Mr. White led the Division through one of the most significant and prolific rulemaking periods in its history, including the Commission’s adoption of final rules addressing executive compensation disclosure, Sarbanes‑Oxley Section 404’s internal control requirements, internet access to proxy materials, oil and gas disclosure, use of interactive data in financial reporting, shareholder proposals relating to the election of directors, private offerings, and capital raising and reporting by smaller public companies, as well as the Commission’s issuance of guidance regarding the use of corporate websites. International initiatives included acceptance of International Financial Reporting Standards (IFRS) by foreign private issuers, the proposed roadmap for use of IFRS by U.S. issuers and modernizing the Commission’s rules on cross‑border tender offers and deregistration and exemption from registration of foreign issuers, as well as revisions to the public reporting regime for foreign private issuers. He played an integral role in the SEC’s response to market turmoil throughout 2008, ensuring that the Division acted swiftly and appropriately to facilitate strategic transactions and access to capital for public companies. During his over 25 years as a partner at Cravath, Mr. White has focused his practice on representing public companies on a wide variety of matters including corporate governance matters, public reporting obligations, public financings and restatements and other financial crises. Mr. White is a member of the Standing Advisory Group (SAG), which advises the Public Company Accounting Oversight Board (PCAOB). He has also served on the Financial Accounting Standards Advisory Council (FASAC), which advises the Financial Accounting Standard Board (FASB).

(continues)

SEC and Financial Reporting Institute Conference

June 8, 2017 | Millennium Biltmore Hotel Los Angeles

SPEAKER BIOGRAPHIES

20170604 22

SEC and Financial Reporting Institute

John W. White (continued) He is a member of the Board of Trustees and the Audit Committees of both the Practising Law Institute and the SEC Historical Society. Mr. White is a frequent speaker on corporate governance and the securities laws. He served three years on the New York Stock Exchange’s Legal Advisory Committee, four years as Chairman of the Securities Regulation Institute and five years as Co‑chair of PLI’s Annual Institute on Securities Regulation. He is currently a member of the Annual Institute’s Advisory Committee as well as the Advisory Committee for PLI’s Annual Institute in Europe. Additionally, he serves as an inaugural member of The American College of Governance Counsel. Mr. White was twice selected by National Association of Corporate Directors (NACD) as one of the 100 most influential people in the boardroom and corporate governance community. He is also recognized by Chambers USA: America’s Leading Lawyers for Business in both securities regulation and capital markets and is named in The Legal 500, The Best Lawyers in America and Ethisphere Institute’s “Attorneys Who Matter.” Lawdragon has named Mr. White a nationwide “Legend” and inducted him as a “Power Broker” into its “Hall of Fame.” Mr. White received a B.S. with honors in accounting from the University of Virginia in 1970, and in May 1970 he received the Elijah Watts Sells award for the highest score in the nation on the Uniform CPA Examination. He received a J.D. magna cum laude from New York University School of Law in 1973, where he was Managing Editor of the Law Review. After a judicial clerkship with Hon. John J. Gibbons of the U.S. Court of Appeals for the Third Circuit, Mr. White joined Cravath in 1975 and became a partner in 1980. At Cravath, he has served as Recruiting Partner, Corporate Managing Partner, Finance Partner and twice as Head of the Corporate Department.

1

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The views expressed in this presentation are those of the presenter.Official positions of the FASB are reached only after extensive due process and deliberations

FASB Update

Matt Esposito

Assistant Director, Financial Accounting Standards Board

36th Annual SEC and Financial Reporting Institute Conference

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Agenda

2

Revenue Recognition

Leases

Credit Losses

Public Business Entities

Hedging

Q&A

2

Revenue Recognition

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Converged standards

issued

May 2014

Jan 2016

Key clarification amendments

issued

Mar–May 2016

Jan 2017

Mandatory effective date for public

entities

Jan 2018

Implementation Timeline

4

Joint IASB/FASB TRGIASB/FASB available for implementation questions

SAB 74 disclosures on possible impact of application

FASB-only TRG(IASB observer)

3

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Joint Transition Resource Group (TRG)

5

To solicit, analyze, & discuss stakeholder issues arising from implementation of the new guidanceTo solicit, analyze, & discuss stakeholder issues arising from implementation of the new guidance

To inform the FASB and the IASB about those implementation issues, which will help the Boards determine what, if any, action will be needed to address those issues

To inform the FASB and the IASB about those implementation issues, which will help the Boards determine what, if any, action will be needed to address those issues

To provide a forum for stakeholders to learn about the new guidance from others involved with implementationTo provide a forum for stakeholders to learn about the new guidance from others involved with implementation

Objectives:

The TRG will not issue authoritative guidance

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Revenue Recognition TRG Activities

6

A majority of the TRG issues were educational

Input from TRG led to amendments to clarify the Boards’ intent for a

handful of issues

72Discussed at

TRG Meetings**

36Discussed directly with

stakeholders

0Open

108Submissions

to Date*

*Data as of May 2017

4

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

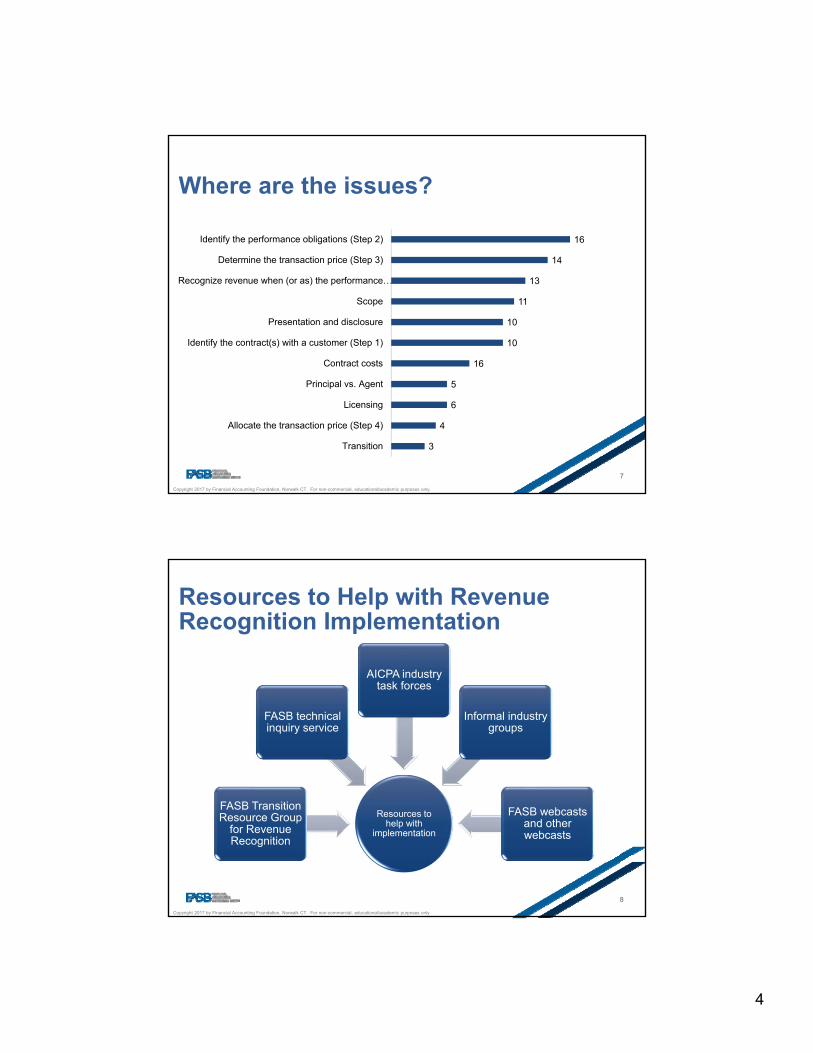

3

4

6

5

16

10

10

11

13

14

16

Transition

Allocate the transaction price (Step 4)

Licensing

Principal vs. Agent

Contract costs

Identify the contract(s) with a customer (Step 1)

Presentation and disclosure

Scope

Recognize revenue when (or as) the performance…

Determine the transaction price (Step 3)

Identify the performance obligations (Step 2)

Where are the issues?

7

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Resources to Help with Revenue Recognition Implementation

8

Resources to help with

implementation

FASB Transition Resource Group

for Revenue Recognition

FASB technical inquiry service

AICPA industry task forces

Informal industry groups

FASB webcasts and other webcasts

5

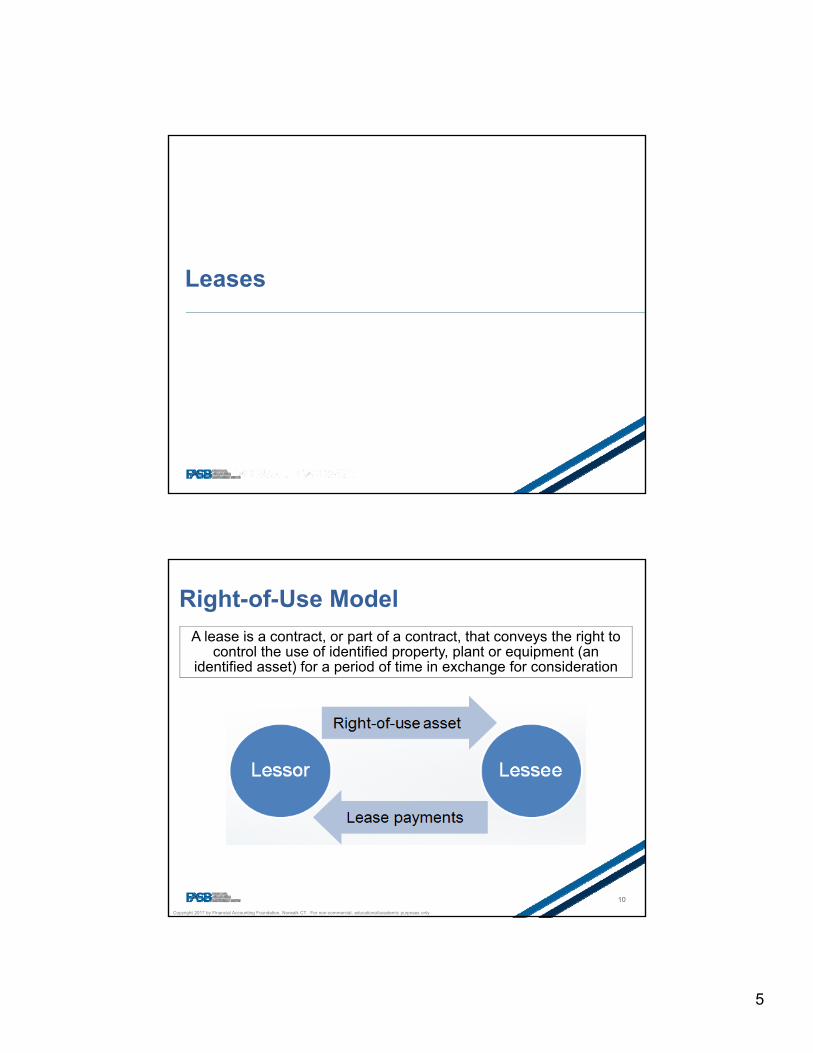

Leases

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

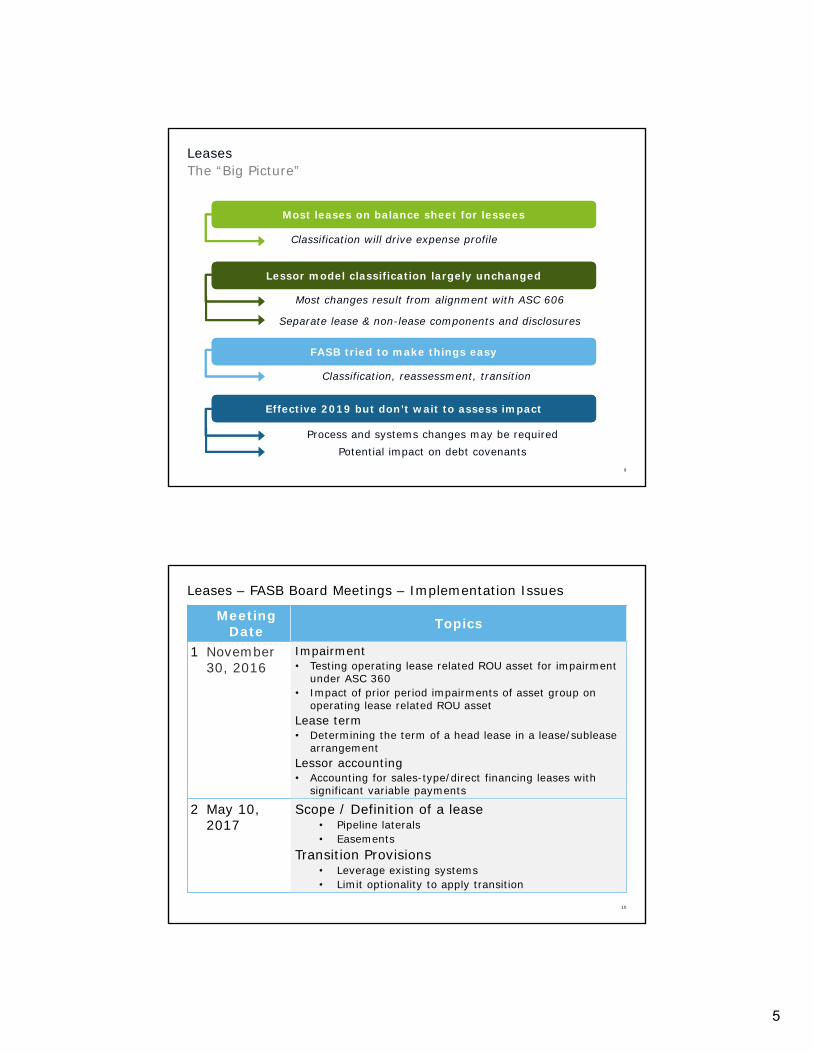

Right-of-Use Model

10

A lease is a contract, or part of a contract, that conveys the right to control the use of identified property, plant or equipment (an

identified asset) for a period of time in exchange for consideration

6

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Identifying a Lease

11

Lease contracts in the scope of Topic 842

involve

An identified asset

That is explicitly or implicitly specified

Supplier has no practical ability to substitute and would not economically benefit from substituting

the asset

The right to control the use during the lease

term

Decision-making authority over the use of

the asset

The ability to obtain substantially all

economic benefits from the use of the asset

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Lessee Accounting Overview

12

Finance

Operating

Right-of-use (ROU) asset

Lease liability

Amortization expense

Interest expense

Cash paid for principal and

interest payments

Right-of-use (ROU) asset

Lease liability

Single lease expense on a straight-line basis

Cash paid for lease payments

Income Statement Cash Flow StatementBalance Sheet

Classification is similar to the classification in Topic 840

Recognition and measurement exemption for short-term leases

Don’t forget to check the video Leases: A Quick Example of the Display Approach available on the FASB Leases Project webpage

7

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Lessor Accounting Overview

13

Sales-Type & Direct

Financing

Operating

Net investment in the lease

Interest income and any selling profit on the

lease1

Cash received for leases

Continue to recognize

underlying asset

Lease income, typically on a straight-line basis

Cash received for leases

Income Statement Cash Flow StatementBalance Sheet

Classification is similar to the classification in Topic 840, but with some important changes

1 Selling profit is recognized at lease commencement for sales-type leases and over the lease term for direct financing leases (note: selling profit is rare for direct financing leases)

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Leases: Scope and Scope Exceptions

14

The Leases standard does not apply to:

Leases of intangible

assets(Topic 350)

Leases of assets under construction (Topic 360)

Leases of biological assets

(Topic 905)

Leases to explore for or

use nonregenerative

resources (Topics 930 and

932)

Leases of inventory

(Topic 330)

Scope: All leases, including subleases

8

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Leases: Overview of Inquiries

15

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The Leases completed project page contains the following resources for more information on the new standard:

- The final Accounting Standards Update (ASU)

- The press release introducing the ASU

- FASB In Focus—a summary of the ASU

- FASB: Understanding Costs and Benefits

- Video #1: Why a New Leases Standard?

- Video #2: Putting It on the Balance Sheet

- Video #3: The Display Approach: A Quick Example

Leases Standard: Resources

16

9

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

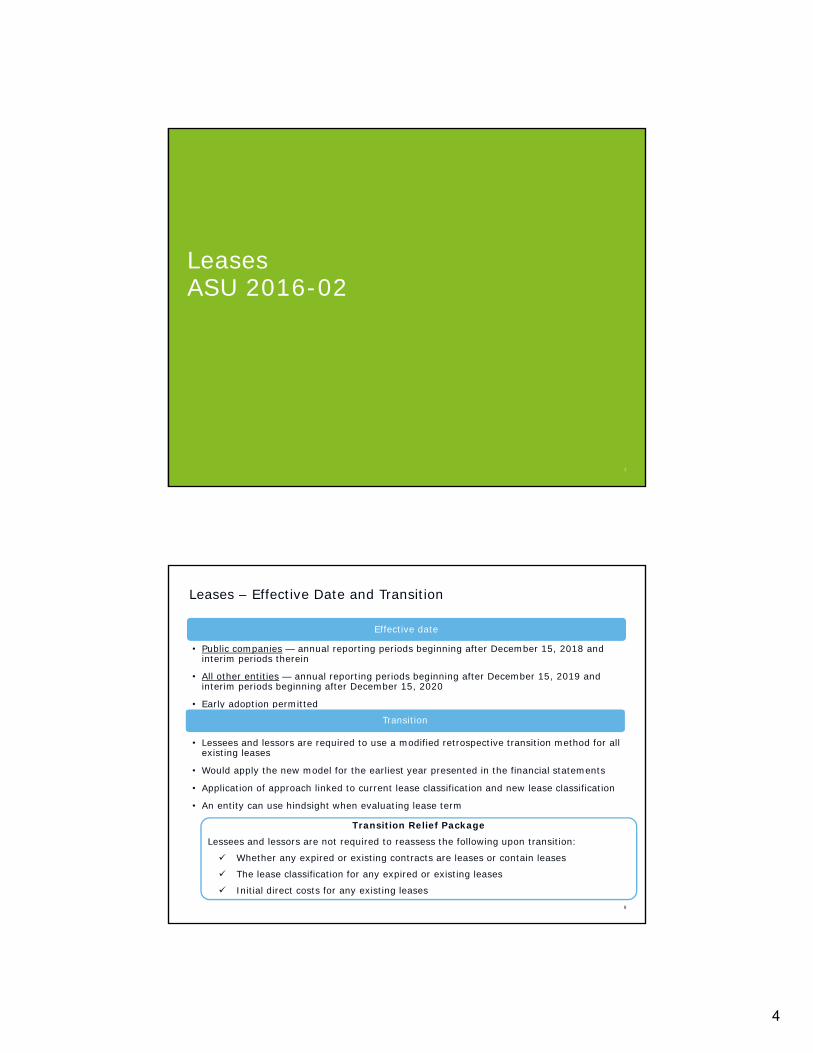

Leases: Effective Dates

• Fiscal years beginning after December 15, 2018, including interim periods within those fiscal years

Public Companies*

• Fiscal years beginning after December 15, 2019 and interim periods beginning after December 15, 2020

All Other Organizations

• Permitted for all organizations

Early Application

* “Public Companies” refers to the following: (1) public business entities, (2) a not-for-profit entity that has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an-over-the-counter market, and (3) an employee benefit plan that files or furnishes statements with or to the SEC

17

Credit Losses

10

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Credit Losses . . . What’s Changing?

19

Loans Debt SecuritiesHeld for

InvestmentCECL

Held to Maturity

CECL

Held for Sale

Lower of amortized cost basis or market

**

Available for Sale

AFS credit-loss model *

Trading FV-NI **

Under new credit-loss model for AFS, credit losses will be recorded through an allowance. Allowance will be limited to difference between debt security’s amortized cost basis and its fair value.

No substantive change to current practice.

Allowance for purchased financial assets with credit deterioration determined in similar manner; however, initial allowance added to purchase price, rather than as provision expense.

**

PCD

PCD

PCD

PCD

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Allowance for Credit Losses . . .

A valuation account

Deducted from amortized cost basis of financial assets

Used to present “net amount expected to be collected”

Changes flow through net income

Credit Losses Standard: Measurement

20 20

Amortized cost . . . unpaid principal balance (UPB) lent to a customer

adjusted for loan fees and origination expenses,

repayments, writeoffs, nonaccrual practices, and

certain hedging transactions

Amount expected to be collected. . .

remaining amounts expected to be

collected from loans

Book the differenceas Allowance

11

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Credit Losses: Effective Dates

21

Public Business Entities that are SEC Filers

(Annual and Interim)

Reporting Periods beginning after Dec. 15,

2019

Public Business Entities that are not SEC Filers (Annual and

Interim)

Non-Public Business Entities* (Annual Periods only)

Reporting Periods beginning after Dec. 15, 2020

Non-Public Business Entities* (Annual and

Interim)

Reporting Periods beginning after Dec. 15,

2021

*Includes not-for-profit entities and employee benefit plans

The entire standard is available for early application for periods beginning after Dec. 15, 2018

A separation was made in effective date decisions for Public Business Entities to allow smaller community banks that do not file with the SEC additional time to implement the standard

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Transition Resource Group (TRG)

22

Solicit, analyze, & discuss stakeholder issues arising from implementation of the new guidanceSolicit, analyze, & discuss stakeholder issues arising from implementation of the new guidance

Inform FASB about those implementation issues to help Board determine if/what action needed to address themInform FASB about those implementation issues to help Board determine if/what action needed to address them

Provide forum for stakeholders to learn about new guidance from others involved with implementationProvide forum for stakeholders to learn about new guidance from others involved with implementation

Objectives:

The TRG will not issue authoritative guidance

12

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Preparers• Large & small banks• Credit unions• Insurance companies

Auditors

• Various client bases

Users

Credit Losses TRG Structure

23

The TRG comprises experts across a wide spectrum of stakeholders

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

First public meeting: April 2016

TRG members reviewed drafts of the standard and illustrations to help ensure the standard was clear and could be applied.

Feedback received at meeting indicated that overall the standard is clear and operational.

Credit Losses TRG – April 2016 Meeting

24

13

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The Credit Losses web portal contains educational materials as well as TRG information

The education section contains:

- The final Accounting Standards Update

- The press release introducing the ASU

- FASB In Focus—a summary of the ASU

- FASB: Understanding Costs and Benefits

- Video: Why a New Credit Losses Standard?

The TRG section contains:

- Meeting webcast archive

- Meeting agendas and memos

Credit Losses: Resources

25

Public Business Entity Definition

14

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Common Q&As . . . What’s a “PBE”?

27

Note: PBEs must be a business entity, so a not-for-profit entity and an employee benefit plan are excluded.

Note: PBEs must be a business entity, so a not-for-profit entity and an employee benefit plan are excluded.

“Public Business

Entity” meets any

of these criteria . . .

Master GlossaryMaster

Glossary

A. Required to (or voluntarily does) file or furnish its financial statements with Securities and Exchange Commission (SEC)

B. Required to file or furnish its financial statements with a regulatory agency other than the SEC in accordance with:

the Securities Exchange Act of 1934 (Act), as amended

or rules and regulations promulgated under the Act

C. Required to file or furnish its financial statements with a foreign or domestic regulatory agency

with issuance of securities not subject to contractual restrictions on transfer

D. Has issued, or is a conduit bond obligor for, securities that are traded, listed or quoted on an exchange or an OTC market

E. Has securities not subject to contractual restrictions on transfer, and required by law, contract, or regulation to both . . .

prepare U.S. GAAP financial statements (including notes)

make them publically available on a periodic basis

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Criterion D: Has issued, or is a conduit bond obligor for, securities that are traded, listed or quoted on an exchange or an OTC marketCriterion D: Has issued, or is a conduit bond obligor for, securities that are traded, listed or quoted on an exchange or an OTC market

Common Q&As . . . What’s a “PBE”?

28

Criterion D intended to be narrow . . .

Did not substantially change from prior definitions of . . .

o “public entity” and “nonpublic entity”

“An OTC market” is a public market . . .

o Where information on trading, listing or quoting activity is

made publicly available

o Examples: “OTC Pink Sheets” and “OTC Bulletin Board”

Transaction activity in nonpublic markets . . .

o Would not make an entity a PBE

o Example: “PORTAL,” a private securities trading platform . . .

o Available only to Qualified Institutional Buyers (QIBs)

15

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Criterion E: Has securities not subject to contractual restrictions on transfer, and required by law, contract, or regulation to both . . .

prepare U.S. GAAP financial statements (including notes)

make them publically available on a periodic basis

Criterion E: Has securities not subject to contractual restrictions on transfer, and required by law, contract, or regulation to both . . .

prepare U.S. GAAP financial statements (including notes)

make them publically available on a periodic basis

Common Q&As . . . What’s a “PBE”?

29

Investors

Bank Holding Company

Bank Subsidiary

Has a financial statement requirement under FDICIA, but . . . no unrestricted securities issued

No financial statement requirement, even if financials are filed on behalf of subsidiary

No “look through” required

Neither entity a PBE because . . . Unrestricted common equity in nonpublic market

Restricted common equity 100% owned

by BHC

Entire PBE definition, including Criterion E, should be applied “entity by entity”

o Example: analysis under Criterion E (assume Criteria A - D are not met):

Hedging

16

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Hedge Accounting – Revised Model

31

Hedge of Nonfinancial Item

Hedge of Financial Instrument

Fair ValueHedge

CashFlow

Hedge

Hedge of inventory

Hedge of forecasted

purchase or sale of inventory

Swap fixed rate debt to

floating

Swap floating rate debt to fixed

“Effective” portion of changes in FV of hedging derivative deferred in OCI

NEW: “Ineffective” portion deferred in OCI

Amounts previously recorded in AOCI are reclassified into earnings in the reporting period when the hedged item affects earnings.

NEW: Presentation of gain or loss on derivative in same income statement line item as hedged item.

Derivative marked to fair value through earnings

NEW: Presentation of derivative gain or loss in the same income statement line item as hedged item

Basis of hedged item adjusted for changes in FV attributable to hedged risk--also through earnings

Basis adjustment offsets derivative mark to earnings

For Qualifying Hedging Relationships*

*The highly effective qualifying threshold (80%-125%) of current GAAP will be retained

The concept of separately recording “ineffectiveness” will be eliminated from hedge accounting

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Component Hedging – Revised Model

32

Hedge of Financial Instrument

Hedge of Nonfinancial Item

What is an entity allowed to designate as the hedged item?

NEW: Contractually

Specified Component

No changes to designated risks for financial instruments. Component hedging will now be allowed for both types of hedged items

Interest Rate Risk

Credit Risk

Foreign Exchange

Risk

Variability in total cash flows (CF Hedges)

or Overall

changes in fair value

(FV Hedges)

Variability in total cash flows (CF Hedges)

or Overall

changes in fair value

(FV Hedges)

17

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

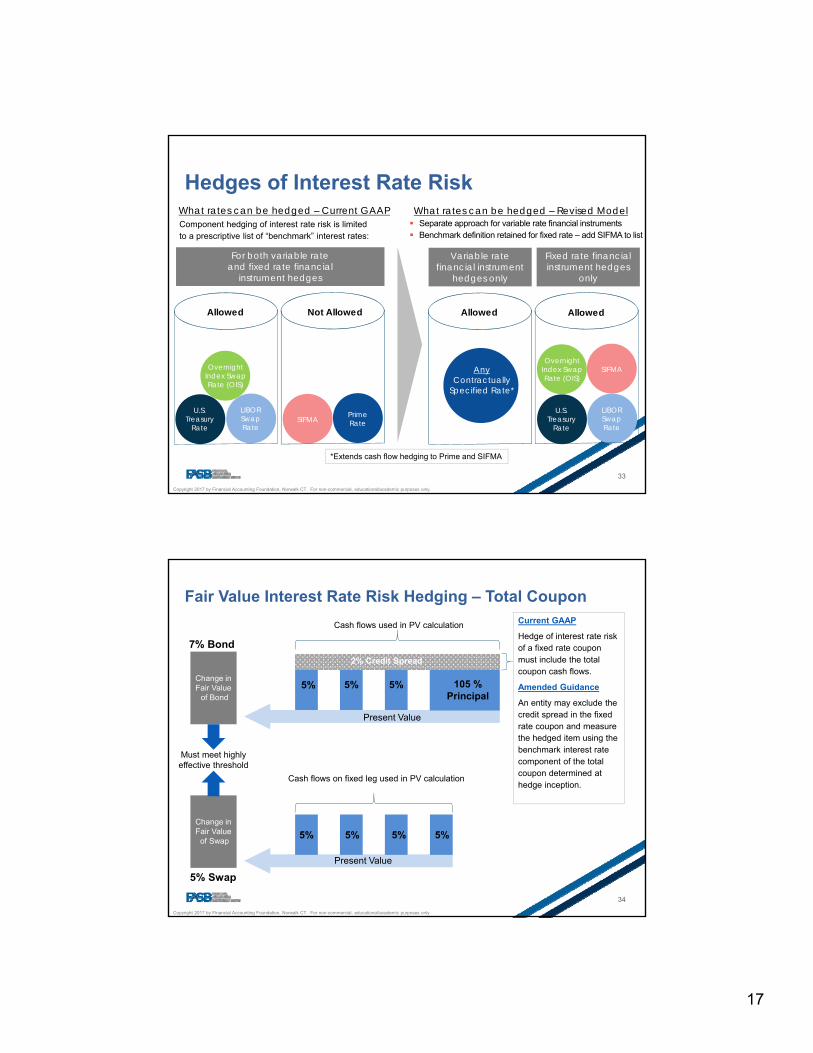

Hedges of Interest Rate Risk

33

Component hedging of interest rate risk is limited to a prescriptive list of “benchmark” interest rates:

U.S. Treasury

Rate

LIBORSwapRate

OvernightIndex SwapRate (OIS)

SIFMAPrime Rate

Allowed Not Allowed

For both variable rate and fixed rate financial

instrument hedges

U.S. Treasury

Rate

LIBORSwapRate

OvernightIndex SwapRate (OIS)

SIFMA

Allowed

Variable rate financial instrument

hedges only

Fixed rate financial instrument hedges

only

Allowed

AnyContractually

Specified Rate*

Separate approach for variable rate financial instruments Benchmark definition retained for fixed rate – add SIFMA to list

*Extends cash flow hedging to Prime and SIFMA

What rates can be hedged – Current GAAP What rates can be hedged – Revised Model

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Fair Value Interest Rate Risk Hedging – Total Coupon

34

Change inFair Value

of Swap

Change inFair Value

of Bond

Present Value

Present Value

Must meet highly effective threshold

7% Bond

5% Swap

5% 5% 5% 105 %Principal

5% 5% 5% 5%

Cash flows on fixed leg used in PV calculation

Cash flows used in PV calculation

2% Credit Spread

Current GAAP

Hedge of interest rate risk of a fixed rate coupon must include the total coupon cash flows.

Amended Guidance

An entity may exclude the credit spread in the fixed rate coupon and measure the hedged item using the benchmark interest rate component of the total coupon determined at hedge inception.

18

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

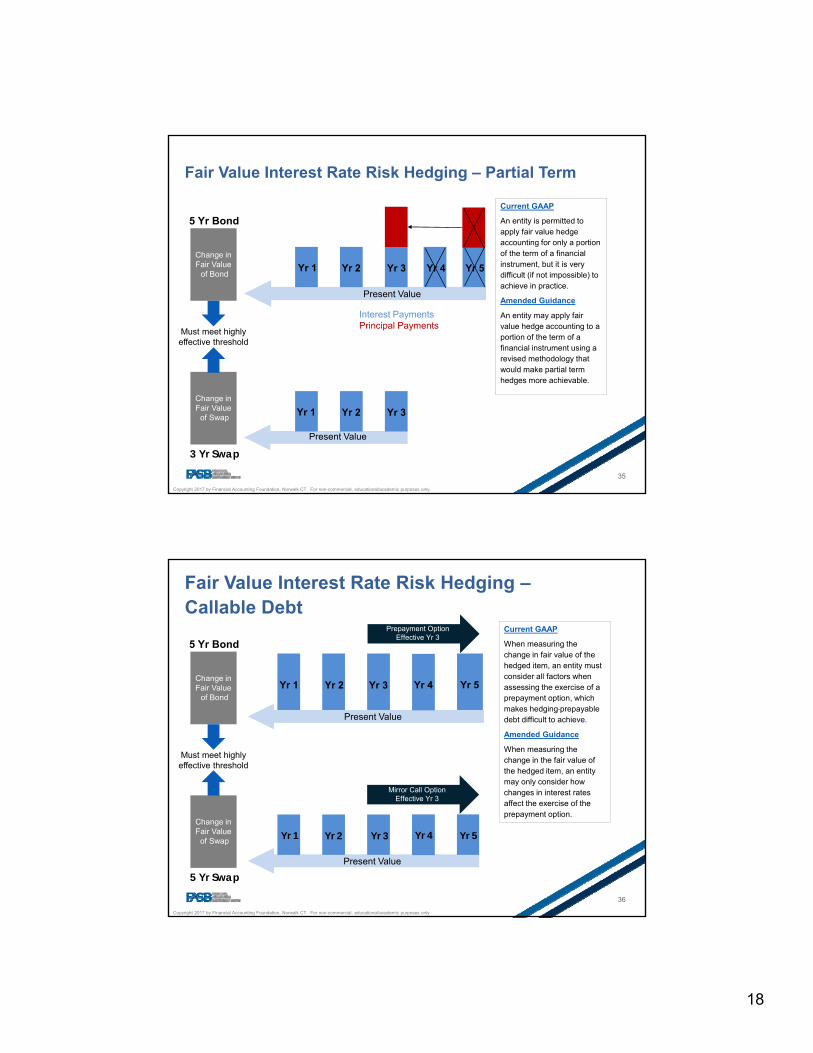

Fair Value Interest Rate Risk Hedging – Partial Term

35

Change inFair Value

of Swap

Change inFair Value

of Bond

Present Value

Present Value

Must meet highly effective threshold

5 Yr Bond

3 Yr Swap

Yr 1 Yr 2 Yr 3

Current GAAP

An entity is permitted to apply fair value hedge accounting for only a portion of the term of a financial instrument, but it is very difficult (if not impossible) to achieve in practice.

Amended Guidance

An entity may apply fair value hedge accounting to a portion of the term of a financial instrument using a revised methodology that would make partial term hedges more achievable.

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Interest Payments Principal Payments

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Fair Value Interest Rate Risk Hedging –Callable Debt

36

Change inFair Value

of Swap

Change inFair Value

of Bond

Present Value

Present Value

Must meet highly effective threshold

5 Yr Bond

5 Yr Swap

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Mirror Call OptionEffective Yr 3

Prepayment Option Effective Yr 3

Current GAAP

When measuring the change in fair value of the hedged item, an entity must consider all factors when assessing the exercise of a prepayment option, which makes hedging prepayable debt difficult to achieve.

Amended Guidance

When measuring the change in the fair value of the hedged item, an entity may only consider how changes in interest rates affect the exercise of the prepayment option.

19

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Hedging - Other Simplifications

37

A concern of many stakeholders relates to the complex and burdensome nature of complying with certain existing requirements. In response to these concerns, Board decisions included the following changes to Topic 815:

Qualitative Testing: For all hedging relationships that do not meet the requirements for the shortcut or the critical terms match methods, an initial quantitative assessment of hedge effectiveness will be required (same as current GAAP). However, in all subsequent periods an entity may qualitatively assess hedge effectiveness unless facts and circumstances change.

Hedge Documentation / Effectiveness Testing:

- An entity may perform the quantitative testing portion of hedge documentation before or at the three-month effectiveness testing period. The quantitative testing does not have to be at hedge inception. The timing of the preparation of all other hedge documentation elements would not change.

- A private company that is not a financial institution would have up to the time when the next interim (if applicable) or annual financial statements are available to be issued to perform all initial and subsequent effectiveness testing and designate the method of assessing effectiveness.

Shortcut Method: An entity may apply a long-haul method if use of the shortcut method was or is no longer appropriate, as long as the hedge is highly effective from inception of the hedging relationship through the assessment date.

FASB Agenda Prioritization

20

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

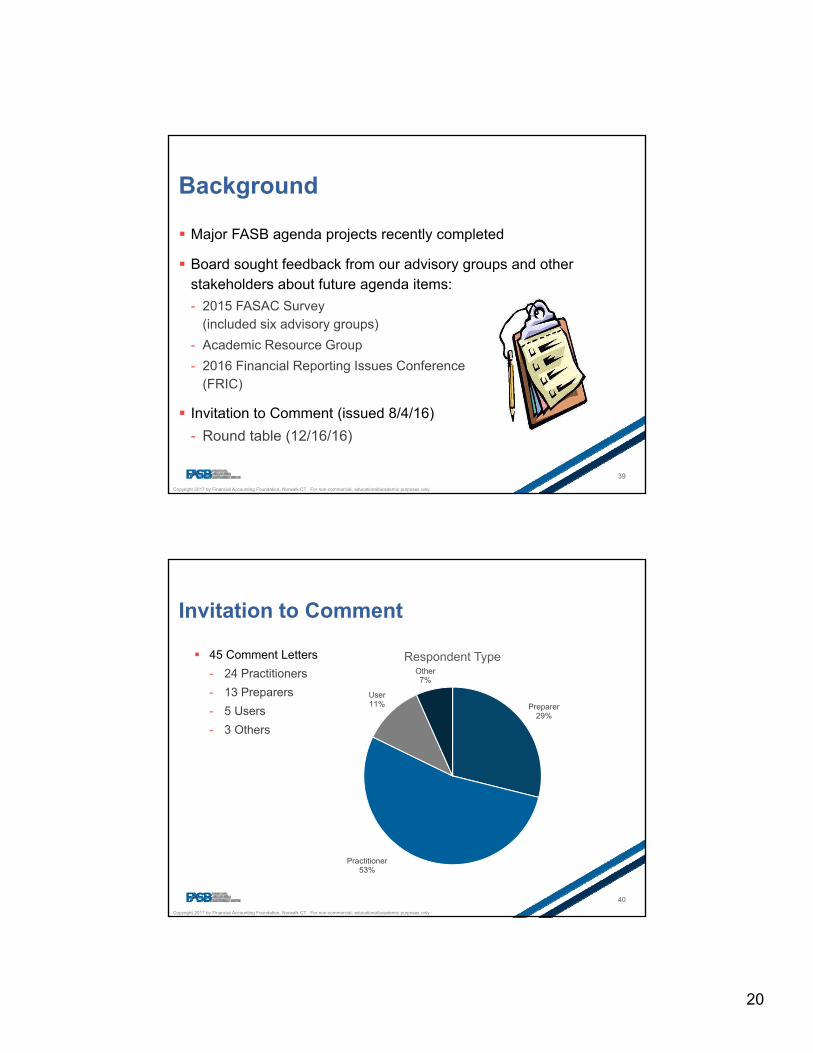

Major FASB agenda projects recently completed

Board sought feedback from our advisory groups and other stakeholders about future agenda items:

- 2015 FASAC Survey(included six advisory groups)

- Academic Resource Group

- 2016 Financial Reporting Issues Conference(FRIC)

Invitation to Comment (issued 8/4/16)

- Round table (12/16/16)

Background

39

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Invitation to Comment

40

45 Comment Letters

- 24 Practitioners

- 13 Preparers

- 5 Users

- 3 Others

Preparer29%

Practitioner53%

User11%

Other7%

Respondent Type

21

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

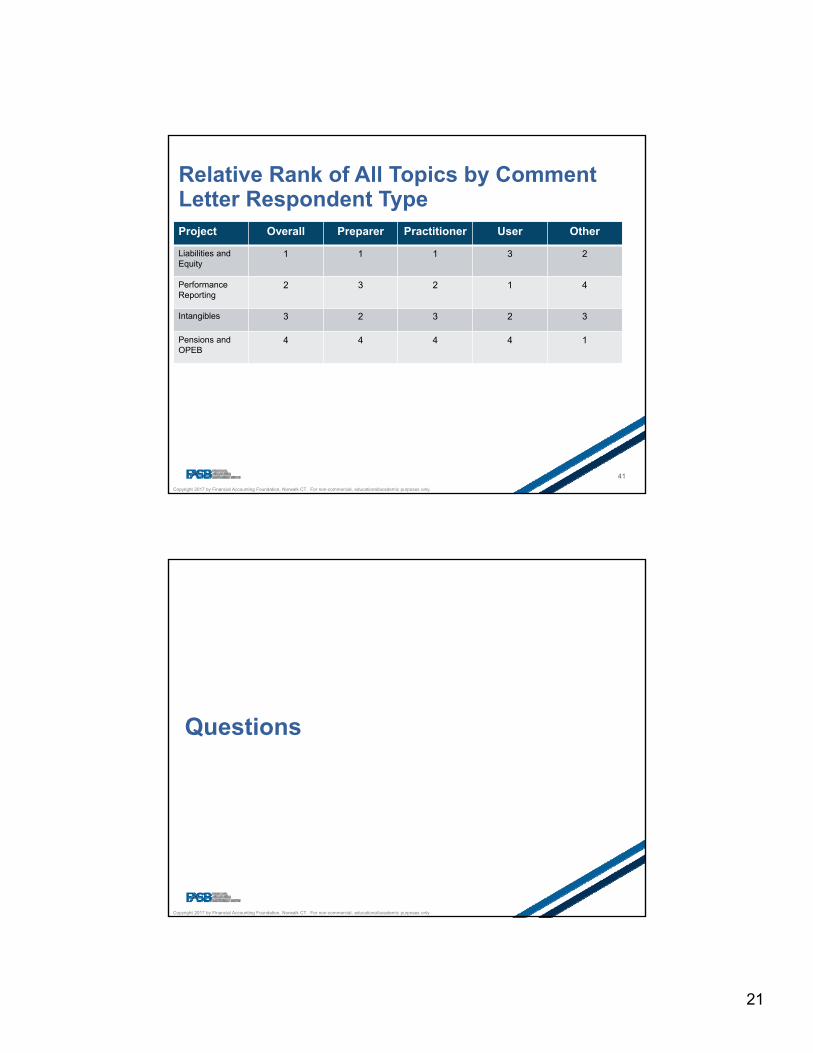

Project Overall Preparer Practitioner User Other

Liabilities and Equity

1 1 1 3 2

Performance Reporting

2 3 2 1 4

Intangibles 3 2 3 2 3

Pensions and OPEB

4 4 4 4 1

Relative Rank of All Topics by Comment Letter Respondent Type

41

Copyright 2017 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Questions

1

Current Accounting and Auditing Practice Issues – Part I

John White (moderator)

Mark Kronforst

John May

Marc Panucci

Sharon Virag

Disclaimers

• Each presenter is speaking in his or her own personal capacity and the views expressed are theirs alone and do not necessarily reflect the views of their employer, their colleagues or other people with whom they are associated or of any organizations with which they are or have been affiliated.

• The material discussed in this program is for training and illustrative purposes only and does not purport to reflect appropriate or inappropriate disclosure or procedures that should be followed or inquiries that should be made, if any, in any particular situation.

2

Topics for Panel

1. Non-GAAP Measures: One Year Later

2. Drill Down on Contingencies

3. Regulation S-X: Rule 3-13 Waivers

4. Expanded Auditor’s Report

5. Revisiting ICFR

6. Inspections: What’s New!

7. Independence Matters

8. Form AP Roll-Out

9. The SEC Comment Process

1. Non-GAAP Measures:One Year Later

3

Non-GAAP Basics

• Reg G and Reg S-K Item 10(e) contain the disclosure requirements

• Location of the disclosure determines applicable requirements– Reg G: Any public disclosure

– Form 8-K Item 2.02 (furnished): Earnings press releases

– Reg S-K Item 10(e): Filings with the SEC

• Special circumstances or exceptions– Compensation measures in proxy statements

– Segments

– M&A

5

Non-GAAP Basics (cont’d)

• Overriding principle: Not materially misleading

• Disclosure requirements:– Reg G: Most directly comparable GAAP financial measure and reconciliation

– Form 8-K Item 2.02: Reg G requirements plus equal or greater prominence, investor usefulness, and management purposes

– Reg S-K Item 10(e): Reg G and Form 8-K Item 2.02 requirements plusexpress prohibitions relating to liquidity measures, face of pro formas, financial statements (including notes), non-recurring items, and titles

• Increased SEC Staff focus in recent years– “Supplement . . . and not supplant” GAAP measures

– Prime source of Corp Fin comments in 2016

6

4

7

May 2016: Updated Guidance

• Materially misleading: (Reg G, Rule 100(b)) – Exclusion of normal, recurring, cash operating expenses

– Cherry picking

– Individually tailored accounting principles

• Equal or greater prominence

• Per share liquidity measures

• Non-GAAP forward-looking EPS guidance

• Calculation/presentation of income tax effects

8

Non-GAAP: Controls and Oversight

• Importance of controls– Deciding on non-GAAP measures and adjustments

– Disclosure controls and procedures

• Audit Committee role– CAQ: Questions on Non-GAAP Measures: A Tool for Audit

Committees (June 2016)

– CAQ: Non-GAAP Financial Measures: Continuing the Conversation (December 2016)

• Auditor’s role

• Compensation Committee role

• Enforcement “sweep”

5

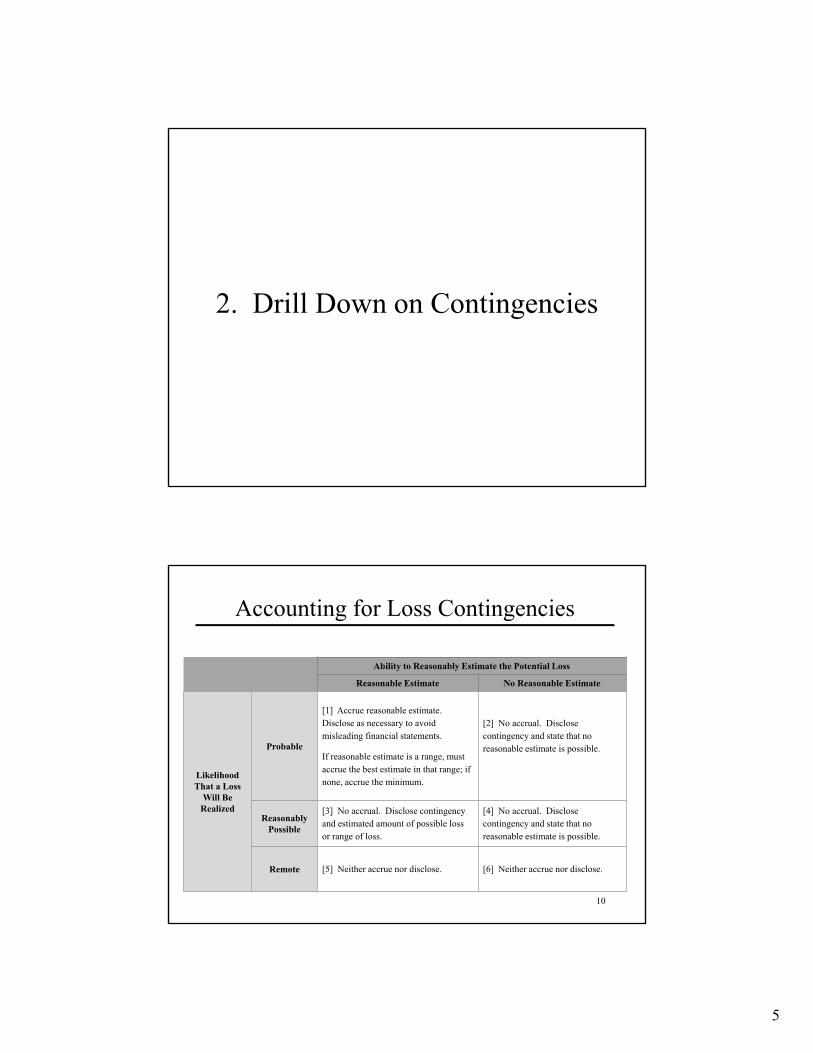

2. Drill Down on Contingencies

Accounting for Loss Contingencies

10

Ability to Reasonably Estimate the Potential Loss

Reasonable Estimate No Reasonable Estimate

Likelihood That a Loss

Will Be Realized

Probable

[1] Accrue reasonable estimate. Disclose as necessary to avoid misleading financial statements.

If reasonable estimate is a range, must accrue the best estimate in that range; if none, accrue the minimum.

[2] No accrual. Disclose contingency and state that no reasonable estimate is possible.

Reasonably Possible

[3] No accrual. Disclose contingency and estimated amount of possible loss or range of loss.

[4] No accrual. Disclose contingency and state that no reasonable estimate is possible.

Remote [5] Neither accrue nor disclose. [6] Neither accrue nor disclose.

6

Contingencies

• Disclosure basics:– Use terms consistent with ASC 450-20

– Explaining an inability to estimate

– Give estimates of reasonably possible losses (aggregation permitted in some circumstances)

• When to accrue and how much– Impact of settlement offers

• Settlements without prior accruals– Expect questions

– Foreshadowing disclosure (prior to recording loss)

• What do your auditors expect of you?

• Dealing with the lawyers

11

SEC Comment Letters

Stericycle Inc. (June – August 2016)– SEC Staff comment asked why Stericycle was unable

to estimate the amount or range of reasonably possible loss for a lawsuit when the settlement agreement was entered into shortly after the filing of the Q1 2015 10-Q.

– Stericycle acknowledged it could have recorded $45 million in accrued liabilities arising out of the settlement in Q1 2015 (as opposed to Q2 2015) and restated its previously issued financial statements.

12

7

Enforcement Actions

RPM International (September 2016)– SEC charged company with...

• Failure to disclose a loss contingency for a DOJ investigation

• Failure to accrue a probable and estimable liability

• Failure to disclose material weakness in ICFR and DCP

– GC also charged for failure to inform CEO, CFO, audit committee and independent auditors

13

Enforcement Actions

General Motors (January 2017)– SEC charged company with...

• Deficient internal accounting controls, resulting in failure to assess potential impact of defective ignition switch on financial statements

• Failure to notify internal accountants of the company’s internal investigation for 18 months

• Therefore, accountants were unable to evaluate if a loss was reasonably possibly and if disclosure was required

– $1 million settlement

14

8

Questions

Break

9

Current Accounting and Auditing Practice Issues – Part II

John White (moderator)

Lori Smith (moderator)

Mark Kronforst