49

3Q FY 2017

3Q FY 2017

The following document contains Lutronic’s proprietary information and is not intended to be used in any other manner other than expressly written. All business and financial data contained herein are in compliance with Korean IFRS. Any forecast within is not individually confirmed. These are forward-looking statements that relate to the Company’s estimated business and financial performance, with expressions using ‘ forecast’, ‘assessment’, ‘plan’, or ‘expectation’(‘E’). Forward-looking information and/or any interpretation may be affected by business environments and thus includes inherent differences that may vary from the final results. In addition, all forward-looking information is based on current market condition and the Company’s direction at present, and is subject to changes without further notice, according to changes in business environment or realignment of strategy. The Company, its affiliates, advisors or representatives shall not be held responsible for any damages from use of information herein, including gross negligence or otherwise. This material cannot be used as evidence for responsibilities relating to the result of investment performance of the investor.

2

DISCLAIMER

COMPANY OVERVIEW

3

LUTRONIC HQ

Lutronic Vision, INC

Biovision Technologies, LLC

Rudong Lutronic Medical Techology co,

LTD

Lutronic Aesthetics, INC Lutronic Japan co, LTD Lutronic Shanghai, LTD Lutronic Germany

CEO : HAELYUNG HWANG

내용

Lutronic Corp.

구분

Name

CEO

Date of Incorporation

Date Listed On KOSDAQ

Capital

Main Business

Headquarters

Website

Employees

Academic Background

Award Winning Career

• Dec. 2013 Korea Venture Show ‘Industry Award ‘

• Dec. 2010 Minister of Knowledge Economy Award

(Global IT-CEO award)

• Nov. 2007 Presidential Merit Award venture Industry

Promotion

Haelyung Hwang

July 8, 1997

July 4, 2006

KRW 6,400 millions (Dec. 31, 2016)

Laser and Energy-based Device Developer & Manufacture

219, Sowon-ro, Deogyang-gu,

Goyang-si, Gyeonggi-do, Korea

www.lutronic.com

306 (in Head Office only), total 380

Yale University (Economics, Electronic Engineering as minor)

내용 구분

Work Experience

• The Korean Society of Medical & Biological Engineering Vice Chair

• Ministry of Health and Welfare Health Technology Policy

Deliberative Committee

• Commissioner of high-tech medical complex, an affiliated

organization of prime minister's office

• Advanced Technology Center Association Director

• KOSDAQ Association – Vice Chair

• Ministry of Trade, Industry and Energy Internal assessment

committee

• Laser Systems, Inc . Vice Chair for Asia Marketing

COMPANY OVERVIEW

4

Corporate Governance (Board Members)

5

Haelyung Hwang KH Dominic Lee Charles Cholsoo Lho Jung Woo Lee

CEO Director Outside Director Auditor on Board

Refer to the previous page. Partner Corporate Finance , Altacap CFO MCM, American Tape Marketing and Product Management, Samsung Elec.

Chairman & CEO, Amicus Group Director , Center for Global Cooperation, Samsung Economic Research Institute Economic Research Asst, World Trade Organization

Advisor My Assets Asset Management Vice President Korea Securities Dealers Association President and CEO, the Herald Korea CEO Dongseo Securities / Coryo Securities

Global Medical Laser Devices

Financial Overview Competitive Assets

Top aesthetic laser company in Asia

3-4% of global market share

KOSDAQ listed in 2006

Involved in Aesthetics, Spinal Surgery,

and Ophthalmology

Market capitalization of KRW 325B

(USD 304M) as of January 2018

FY2016 revenue of about KRW 81B

(USD 71M) with 70% of revenue from

Global Sales

292patents / Global Regulatory

Approvals

International network of KOLs and

partners in 60 countries

World’s first laser for treating the

retina without damaging

photoreceptors

LUTRONIC CORP.

6

EVOLVING BUSINESS

Ophthalmology Smart Surgery Aesthetic

Global market : $3 B (2017), CAGR 14%

3~4% Global MS

Continual Expansion of New Products

Dermatology, Plastic surgery

Korean market : $300 M (2013)

Approved by MFDS2014)

Recurring Business

Neurosurgery + other (disc pain)

Global market : $10 B + α (2015)

DME, CSC : MFDS, CE approval

CSME: FDA clearance

World’s first laser for treating retina with no damage to photoreceptors.

7

212.9 302.4 345.2

426 502.4

588.6 206.8 158.9

176.8

224.8 218.5

256

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2011 2012 2013 2014 2015 2016

Domestic Global

0.4

10.6

27.9

52.7

66.7

2012 2013 2014 2015 2016

0.1%

2.0%

4.3%

7.3% 7.9%

Revenue Operating Income

(Unit : KRW 100 millions) (Unit : KRW 100 millions)

Quarter Performance (5year)

((Unit : KRW 100 millions)

REVENUE TREND (CONSOLIDATED)

8

-50

0

50

100

150

200

250

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Revenue Operating Income

2017 3Q(CONSOLIDATED)

3Q ‘17 2Q ‘17 3Q ‘16 YoY QoQ

Revenue 20,745 22,515 18,801 10.34% -7.86%

COGS 10,479 11,401 7,662 36.77% -8.09%

Gross Profit 10,266 11,114 11,139 -7.84% -7.63%

SG&A 11,318 12,562 10,074 12.35% -9.90%

Operating Income -1,052 -1,448 1,065 Turned

Negative 27.35%

EBIT -1,324 -920 55 Turned

Negative -43.91%

Income Tax 455 578 -312 245.83% -21.28%

Net Income -1,779 -1,498 367 Turned

Negative -18.76%

22,515 20,745

-1,448 -1052

-6.43

-5.07

-7.00

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

-5,000

0

5,000

10,000

15,000

20,000

25,000

2017 Q2 2017 Q3

Revenue O. Income O.I. % (KRW millions)

18,801 20,745

1,065

-1052

5.66

-5.07

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

-5,000

0

5,000

10,000

15,000

20,000

25,000

2016 Q3 2017 Q3

Revenue O. Income O.I. %

(KRW millions, %)

(KRW millions)

2017 3Q(NON-CONSOLIDATED)

10

21,212 19,924

1,623 1,526

7.65

7.66

7.65

7.65

7.65

7.65

7.65

7.66

7.66

7.66

0

5,000

10,000

15,000

20,000

25,000

2017 Q2 2017 Q3

Revenue O. Income O.I. % 3Q ‘17 2Q ‘17 3Q ‘16 YoY QoQ

Revenue 19,924 21,212 19,161 3.98% -6.07%

COGS 10,715 11,414 8,592 24.71% -6.12%

Gross Profit 9,209 9,798 10,569 -12.87% -6.01%

SG&A 7,683 8,175 6,715 14.42% -6.02%

Operating Income 1,526 1,623 3,854 -60.4% -5.98%

EBIT 1,373 1,854 2,908 -52.79% -25.94%

Income Tax 344 366 0 - -6.01%

Net Income 1,029 1,488 2,908 -64.61% -30.85%

19,161 19,924

3,854

1,526

20.11

7.66

0.00

5.00

10.00

15.00

20.00

25.00

0

5,000

10,000

15,000

20,000

25,000

2016 Q3 2017 Q3

Revenue O. Income O.I. %

(KRW millions)

(KRW millions)

(KRW millions, %)

Global Aesthetic Market Revenue of Global Players in 2016

2,075

2,387

2,580 2,791

3,003

3,242

(Unit : USD millions)

$433.5

$354

$298

$118

$71

2015 2016 2017 2018 2019 2020

source: Medical Insight, 2016 Energy-Based Device, Body Shaping & Skin Tightening Device

Source : Companies *Listed companies

AESTHETIC - MARKET

11

(Unit : USD millions)

998 1,162 1,236 1,323 1,411 1,516

479

540 593

648 705

768

426

486 533

582 629

678

172

199 218

238

258

280

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016 2017 2018 2019 2020

North America Europe Asia Latin America

Source: Medical Insight, 2016 Energy-Based Device, Body Shaping & Skin Tightening Device

GLOBAL AESTHETIC DEVICE MARKET

12

(Unit : USD millions)

Multiple Energy Sources Ensure Optimal Treatment

13

Multiple Energy Sources Ensure Optimal Treatment

14

PRODUCT

15

GLOBAL CLINICAL RESEARCH

GLOBAL NETWORK OF KEY OPINION LEADERS (KOL)

230 + ACADEMIC PUBLICATIONS / 400+ CLINICAL STUDIES PUBLISHED IN PEER-REVIEWED JOURNALS

Aesthetic Clinical Research and Global kol

16

0

2000

4000

6000

8000

10000

12000

2013 2015 2017

Disk Pain Surgery Market (non-insurance) Macro Trends Driving Growing Demand

(Unit : KRW 100 millions)

Source : LUTRONIC

Smart surgery – market (KOR)

17

Source : LUTRONIC

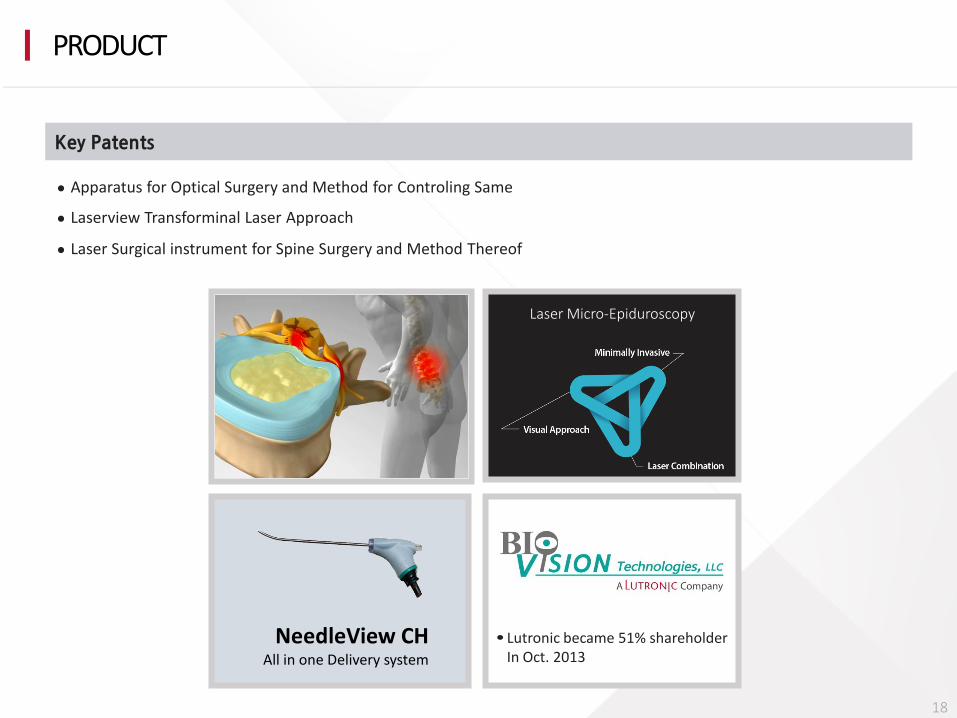

Trans-foraminal Epiduroscopic Laser Annuloplasty (TELA) TELA is a minimally invasive procedure technique for the management of pain caused by various spinal disorders, wherein physicians utilize a specialized epidural scope called the NeedleView CH, which is the only one of its kind worldwide.

Key Patents

Apparatus for Optical Surgery and Method for Controling Same

Laserview Transforminal Laser Approach

Laser Surgical instrument for Spine Surgery and Method Thereof

NeedleView CH All in one Delivery system

Laser Micro-Epiduroscopy

Lutronic became 51% shareholder In Oct. 2013

PRODUCT

18

CSC (Central Serous Chorioretinopathy)

Approval in CE, MFDS (KFDA) / Clearance FDA (for CSME) No-Alternative Therapy

AMD (Age-related Macular Degeneration)

Ultimate Goal Preventive Medicine

DME (Diabetic Macular Edema)

Approval in CE, MFDS (KFDA) / Clearance FDA (for CSME) Targeting : Anti-VEGF Non-responder + Anti-VEGF Combination

PLATFORM TECHNOLOGY FOR THE RETINA TREATMENT

19

Iris

Pupil

Cornea

Lens

Retina

Optic Nerve

Blind Spot

Ciliary

LASER

NON-LASER

RPE layer < 5µm >

Retina Layer <300µm>

Retinal Pigment Epithelium Regeneration

Sourse : Asian Retina Clinical Cases, Hakyoung KIM, Hyeong Gon Yu, The Korean Retina Society. & Lutronic R&D Center

MECHANISM OF THERAPY

20

OBJECT

EYE

BRAIN (VISUAL CENTER)

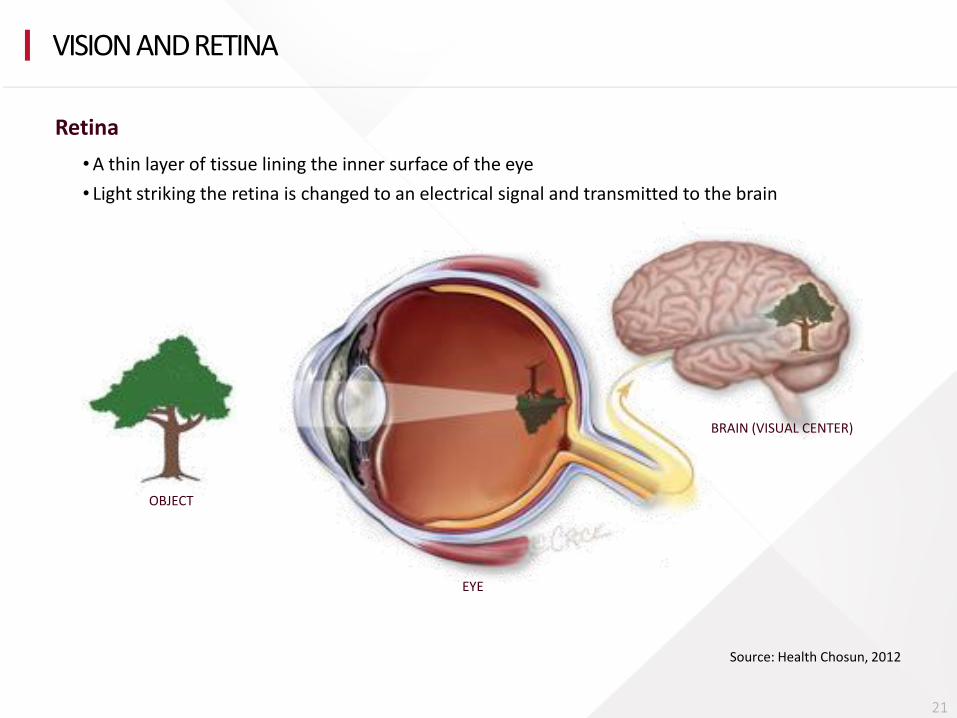

Source: Health Chosun, 2012

Retina

VISION AND RETINA

21

•A thin layer of tissue lining the inner surface of the eye

• Light striking the retina is changed to an electrical signal and transmitted to the brain

MACULA

22

Source: NIH

Photoreceptors

Retinal Pigment Epithelial Cells

Bruch’s Membrane

Choroid

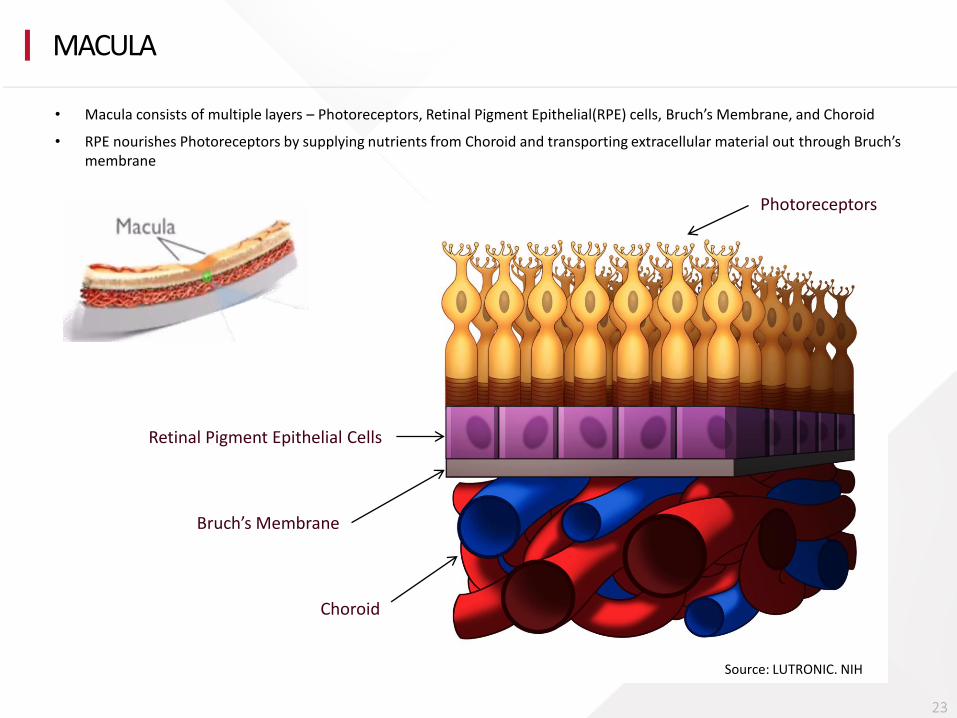

MACULA

23

Source: LUTRONIC. NIH

• Macula consists of multiple layers – Photoreceptors, Retinal Pigment Epithelial(RPE) cells, Bruch’s Membrane, and Choroid

• RPE nourishes Photoreceptors by supplying nutrients from Choroid and transporting extracellular material out through Bruch’s membrane

Leakage of fluid accumulates under the central macula, resulting in blurred or

distorted vision which may progressively decline with each recurrence

CENTRAL SEROUS CHORIORETINOPATHY (CSC)

24

The cause is not known and believed to be exacerbated by stress

The overall incidence is approximately 6 per 100,000 population, mostly among professional male in age of 41 to 46

No conventional standard of care exists without causing damage, due to the occurrence in the central macula area

83%

10%

2% 5%

MAJOR ASIA USA KOREA MAJOR EU

70%

30%

Acute Chronic

GLOBAl PATIENT 6 PER 100,000 Incidence of CSC 180,000 prevalence Chronic 48,000

Source : Incidence of CSC, Journal Ophthalmology 2008 World Bank, CIA FactBook

INCIDENCE OF CSC

25

Location : Korea

No. of Patients : 12

Period : 6 months

Result : Reduction in subretinal fluid / Stable or improved vision / Enhancements of retinal sensitivity / no scotoma

CASE 7.

46-year-old female (Right eye)

Source: Seungbum Kang, Young Gun Park, Jae Ryun Kim,Eric Seifert, Dirk Theisen-Kunde, Ralf Brinkmann,and Young Jung Roh, Selective Retina Therapy in Patients with Chronic Central Serous Chorioretinopathy: A pilot study, MEDICINE

CSC SIGNAL STUDY (KOR.)

26

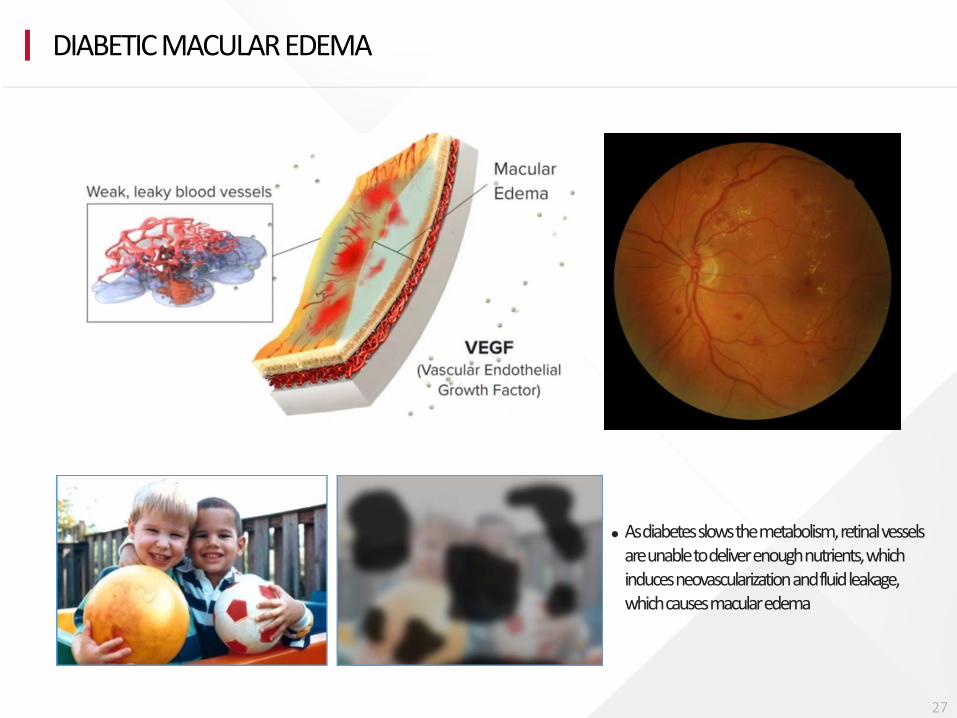

As diabetes slows the metabolism, retinal vessels are unable to deliver enough nutrients, which induces neovascularization and fluid leakage, which causes macular edema

DIABETIC MACULAR EDEMA

27

Rest of World 29%

Chinal 20%

Latin America 12%

Western Europe

11%

United States 10%

India 9%

Other Wealthy Nations

6%

Japan 3%

Rest of World

Chinal

Latin America

Western Europe

United States

India

Other Wealthy Nations Japan

Estimated global DME population is 105 million

First target is 24million patients at a later stage of DME

Early DR DME

Diabetic eye disease classification

85.4%

24.0% 19.3%

PDR

Source: Market scope 2015

PREVALENCE OF DME

28

Location : Germany

No. of Patients : 39

Source : Roider J, Klatt C, Brinkmann R et al. Selective retina therapy (SRT) for clinical significant diabetic macular edema. Graefes Arch Clin Exp Ophthalmol. 2010;248:1263-1272

DME (Diabetic Macular Edema)

Jul. 2013 MFDS Approval

Nov. 2013 EU CE Approval

Oct. 2016 US FDA Clearance(CSME)

CLINICAL TRIAL – DME

29

0

10

20

30

40

Best Better Stable

Period : 6months

Result : Stable or improved ision Change in thickness of fovea

11.8(2)

17.6(3)

41.2(7)

29.4(5)

0

10

20

30

40

50

≥1-line deterioration

Stable (<1-line change)

≥1-line to <2-line improvement

≥2-line improvement

11.8(2)

29.4(5)

23.5(4)

35.3(6)

0

10

20

30

40

MMT increased ≥5%

compared to baseline

MMT stationary (<5% change compared to

baseline)

MMT decreased ≥5% to <10% compared to

baseline improvement

MMT decreased ≥10% compared

to baseline

Retubak Thickness Improvement Vision Improvement

Location : Korea

No. of Patients : 21 (23 eyes)

Period : 6 months

Source: Young Gun Park, Jae Ryun Kim, Seungbum Kang, Eric Seifert, Dirk Theisen-Kunde, Ralf Brinkmann,Young-Jung Roh / Safety and Efficacy of Selective Retina Therapy (SRT) for the Treatment of Diabetic Macular Edema in Korean Patients. / Graefes Arch Clin Exp Ophthalmol DOI 10.1007/s00417-015-3262-1

DME CLINICAL TRIAL (KOR.)

30

Result : Stable or improved vision / Change in thickness of fovea / Improved retinal sensitivity / Demonstrated Clinically significant effect and safety on Korean patients

DRY-AMD) WET-AMD)

Drusen

AGE-RELATED MACULAR DEGENERATION (AMD)

31

10% 90%

As aging progresses, the ability of the RPE cells to nourish the photoreceptors diminishes

• Dry AMD: Degraded RPE cells fail to transport extracellular material which then begins to build up (Drusen) in between Bruch’s membrane and the RPE Drusen interfere with the supply of nutrients to the photoreceptors which could lead to vision loss Approximately 90% of AMD patients suffer from Dry AMD

• Wet AMD: As Dry AMD advances, new blood vessels grow (neovascularization) and penetrate Bruch’s membrane and RPE cells in order to supply nutrients to the photoreceptors

The new and immature blood vessels are weak and prone to bleeding and leakage, resulting in blood and protein leakages, thus damaging the photoreceptors and fueling rapid vision loss Approximately 10% of AMD patients suffer from Wet AMD

Res of World 31%

stern Europe 15% China

13%

India 13%

Latin America 11%

United States 9%

Other Wealthy Nations

5%

Japan 3%

Res of World

stern Europe

China

India

Latin America

United States

Other Wealthy Nations Japan

Estimated global Dry AMD population is

90% of 138 million

Disease Classification

84.2%

6.4% 7.8%

1.6%

Early AMD GA only Neovascular only

Neovascular& GA

NO Current Treatment

Source: Market scope 2015

PREVALENCE OF AMD

32

PLATFORM TECHNOLOGY FOR THE RETINA TREATMENT

CSC DME AMD

Target : 6 per 100,000 (30%)

Existing treatments : None

Target : 90% of 138 M patients

Existing treatments

Wet-AMD : anti-VEGF*PC, etc

Dry-AMD : None

Target : 24 M patients

Existing treatments

anti-VEGF*

PC(Photo-coagulation Laser)

*Anti-VEGF Global Market (2015) : Approximately 10B (USD) Indication : DME + wet-AMD Lucentis (Norvatis) + Eylea (Bayer) + Avastin (Roche)

Pan-Retinal Photocoagulation Sample Only for DME, wet-AMD

POST-PC TREATMENT

SCARS

Ranibizumab 2,140 USD

Aflibercept 2,040 USD

Bevacizumab 240 USD

(OFF-LABEL) PC treatment causes secondary thermal damage to the surrounding tissues and leaves permanent scars.

Source: Market scope 2015

Photocoagulation Laser ANTI-VEGF Injection Steroid Injection Surgery (i.2. Vitrectomy)

CURRENT TREATMENTS FOR ETINAL DISEASE

34

If the macula is treated with a PC laser, permanent loss of visual acuity will occur.

RPE RPE

Conventional Photocoagulation R:GEN

출처1 (X500) 출처2 (X200)

Selectively damages RPE cells to repair or regenerate

Vision loss (scotoma, scar)

Fovea treatment is impossible

White burn

Irradiation selectively damages only the RPE

Fovea irradiation possible

Automatic dosimetry for added safety

Source1 : Roider, Brinkmann. Selective retinal pigment epithelium laser treatment theoretinal and clinical aspects. Laser in Ophthalmology – Basic, Diagnostic and Surgical Aspects, pp. 119-129

Source2 :LUTRONIC

PC VS. R:GEN

35

After 1 week After 3 months After 6 months

Source : LUTRONIC

SAFETY OF R:GEN

36

Anti-VEGF Market Global Photocoagulation Laser Market

2935 3772 3977 4205 4301 3639 2948

25 838

1881 2775 4089 5200

2010 2011 2012 2013 2014 2015 2016

Eylea

Lucentis

6213 5984 6146 6745 7015 6944 6876

2010 2011 2012 2013 2014 2015 2016

Avastin

OPHTHALMOLOGY (MACULAR TREATMENT) - MARKET

37

Source: Annual reports, IR data Source: Market Scope (Dec. 2013)

Microsecond Pulse Laser 527nm/ 1.7µs

PlATFORM TECHNOLOGY FOR THE RETINA TREATMENT

38

Auto - controltechnology Laser Ramp-up and RTF Technology

Pulses: 100hz / 1.7µs

Real-Time Feedback CHECK RPE CELLS WITH LIGHT AND SOUND IN 1 µS (1 X 10-6 SEC) DUAL DOSIMETRY SENSORS: OPTOACOUSTIC + REFLECTOMETRY

World’s first laser for treating the retina without damaging photoreceptors(70 Patents)

HOW IT WORKS

RPE Layer

RPE Layer

39

R:GEN CORE TECHNOLOGY – MICROSECOND PULSE LASER

Developed a selective laser treatment device for ONLY the RPE cells with a 527 nm/1.7 μs laser

Source : M. A. MAINSTER, Retinal-Temperature Increases Produced by Intense Light Sources JOURNAL OF THE OPTICAL SOCIETY OF AMERICA, VOL. 60, NO. 2

40

R:GEN CORE TECHNOLOGY – REAL-TIME FEEDBACK

Auto-control technology (safety) Check RPE Cells with LIGHT and SOUND in 1 µs (1 x 10-6 sec)

Source : LUTRONIC

41

R:GEN - AIMING “MAXIMUM PROFITABILITY”

Recurring Business Model (Disposable)

1. No/Less up-front investment 2. High added-value for doctors 3. Safe, Effective + Valuable

※ U.S MARKET

42

PC ANTI-VEGF R:GEN Therapy

Social Cost $700~900 $1,800 (Average) $2,000 +

Clinic Net $700~900

(- Depreciation Cost) $300 $1,000 +

Total Cost $1,400 (Twice a year) $14,000 (Seven a year) $6,000 (Three a year)

Comparison

• Side effects (Partial

Blindness)

• Only slows down symptoms

• Direct injection to the eye

• Develops tolerance

• Only slows down symptoms

(vision loss after a time period)

• Secured both safety and

efficacy

• Immediate daily life after

therapy

• Potential treatment of the

cause

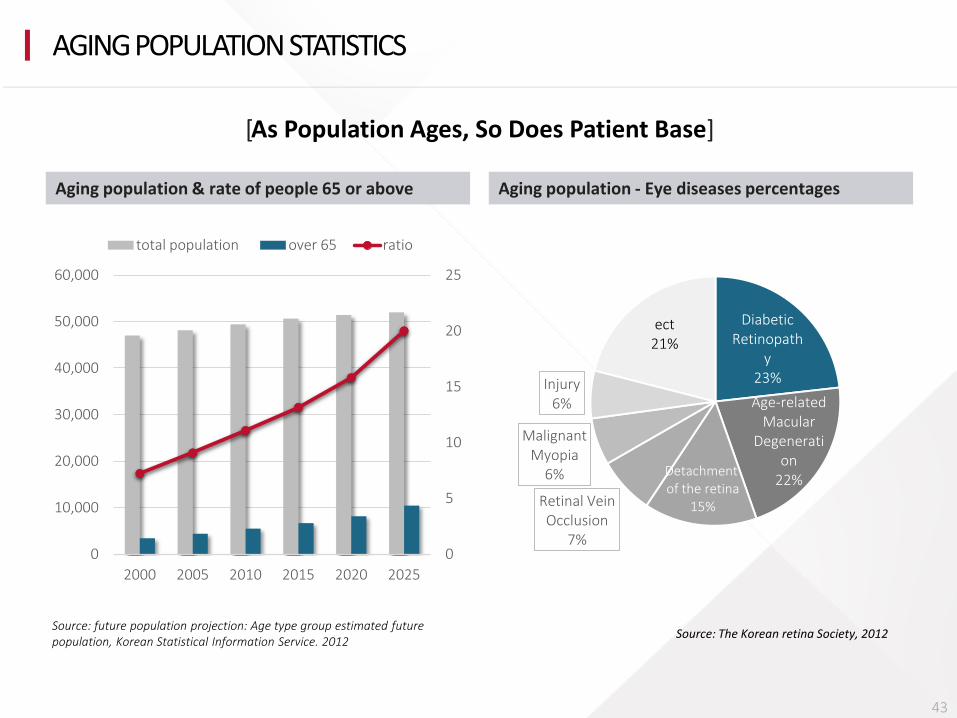

AGING POPULATION STATISTICS

Aging population - Eye diseases percentages Aging population & rate of people 65 or above

0

5

10

15

20

25

0

10,000

20,000

30,000

40,000

50,000

60,000

2000 2005 2010 2015 2020 2025

total population over 65 ratio

Diabetic Retinopath

y 23%

Age-related Macular

Degeneration

22% Detachment of the retina

15% Retinal Vein Occlusion

7%

Malignant Myopia

6%

Injury 6%

ect 21%

Source: The Korean retina Society, 2012 Source: future population projection: Age type group estimated future population, Korean Statistical Information Service. 2012

[As Population Ages, So Does Patient Base]

43

APPENDIX

44

CURRENT CAPITALIZATION TABLE

CEO 24.41%

FOREIGN 5.49%

INSTITUTIONAL 10.4%

OTHERS 59.7%

Stockholder Number Rate

CEO 2,734,049 24.41%

Foreign 615,410 5.49%

Institutional 1,164,805 10.4%

Others 6,332,271 59.7%

Total 10,846,535 100.00%

※ The total is based on stocks with voting rights (1,701,067 shares of convertible preferred stock are not included.)

Dec. 31. 2016

45

FINANCIAL HIGHLIGHTS – STOCK PERFORMANCE

JANUARY 2018

Current(20 day Avg.) 13,088 KRW 52wk H/L 17,150 KRW / 10,000 KRW Market Cap $304M

PRICE EARNING RATIO (5Y)

0

200

400

600

800

1000

1200

1400

1600

Lutronic Healthcare KOSDAQ

46

FINANCIAL STATEMENTS (K-IFRS, IN KRW 0.1B, CONSOLIDATED)

SUBJECT 2014 2015 2016

Ⅰ. Current assets 324.7 561.0 1,150.0

Ⅱ. Noncurrent assets 480.0 733.9 767.1

Intangible assets 231.9 300.3 331.5

Total assets 804.7 1,294.9 1,917.1

Ⅰ. Current Liabilities 325.8 370.4 397.2

Ⅱ. Noncurrent Liabilities 153.6 176.0 165.5

total Liabilities 479.4 546.4 562.8

Ⅰ. Capital 52.0 54.1 64.5

Ⅱ. Additional Paid-in Capital

199.5 294.8 884.4

Ⅲ. Earned surplus 96.9 178.3 226.5

Ⅳ. Elements of other shareholder's equity

-9.9 240.8 196.8

V. Non-controlling interests -13.2 -19.4 -17.9

Total stockholders’ equity 325.3 748.5 1,354.3

Statement of Comprehensive Income Statement of Financial Position

SUBJECT 2014 2015 2016

Ⅰ. revenue 650.8 720.9 845.0

Domestic 224.8 218.5 256.3

Export 426.0 502.4 588.6

Ⅱ. 0perating Income 27.9 52.7 66.7

Ⅲ. Pre-tax Income 10.5 58.3 75.5

Ⅳ. Net Income 8.7 52.6 53.0

Statement of Cash Flow

SUBJECT 2014 2015 2016

Operating Cash flow 48.4 77.7 55.7

47

FINANCIAL STATEMENTS(K-IFRS, IN KRW 0.1B, NON-CONSOLIDATED)

SUBJECT 2014 2015 2016

Ⅰ. Current assets 310.1 556.0 1,132.4

Ⅱ. Noncurrent assets 595.3 840.4 952.1

Intangible assets other than goodwill

213.9 292.8 309.4

Total Assets 905.4 1,396.4 2,084.5

Ⅰ. Current Liabilities 266.1 296.5 310.2

Ⅱ. Noncurrent Liabilities 152.8 177.7 171.0

Total liabilities 418.9 474.2 481.2

Ⅰ. Capital 52.0 54.1 64.5

Ⅱ. Additional Paid-in Capital

199.5 294.8 884.4

Ⅲ. Earned surplus 248.7 331.6 455.5

Ⅳ. Elements of other shareholder's equity

-13.7 241.8 198.9

Total stockholders’ equity 486.5 922.3 1,603.3

Statement of Comprehensive Income Statement of Financial Position

SUBJECT 2014 2015 2016

Ⅰ. revenue 638.1 710.1 810.3

Ⅱ. 0perating Income 61.7 79.8 143.2

Ⅲ. Pre-tax Income 53.3 86.8 156.0

Ⅳ. Net Income 52.0 80.9 132.0

Statement of Cash Flow

SUBJECT 2014 2015 2016

Operating Cash flow 67.8 83.7 66.9

48