4-1 The Fields of Insurance 1. Private insurance voluntary programs designed to protect individual against financial loss 2. Social Insurance compulsory insurance programs generally operated by government 3. Public Benefit Guarantee Programs quasi-social coverages usually associated with regulation

Transcript

4-1

The Fields of Insurance

1. Private insurancevoluntary programs designed to protect individual against financial loss

2. Social Insurancecompulsory insurance programs generally operated by government

3. Public Benefit Guarantee Programsquasi-social coverages usually associated with regulation

4-2

Private (Voluntary) Insurance

1. Usually (but not always) voluntary.

2. Usually (but not always) offered by private insurers.

4-3

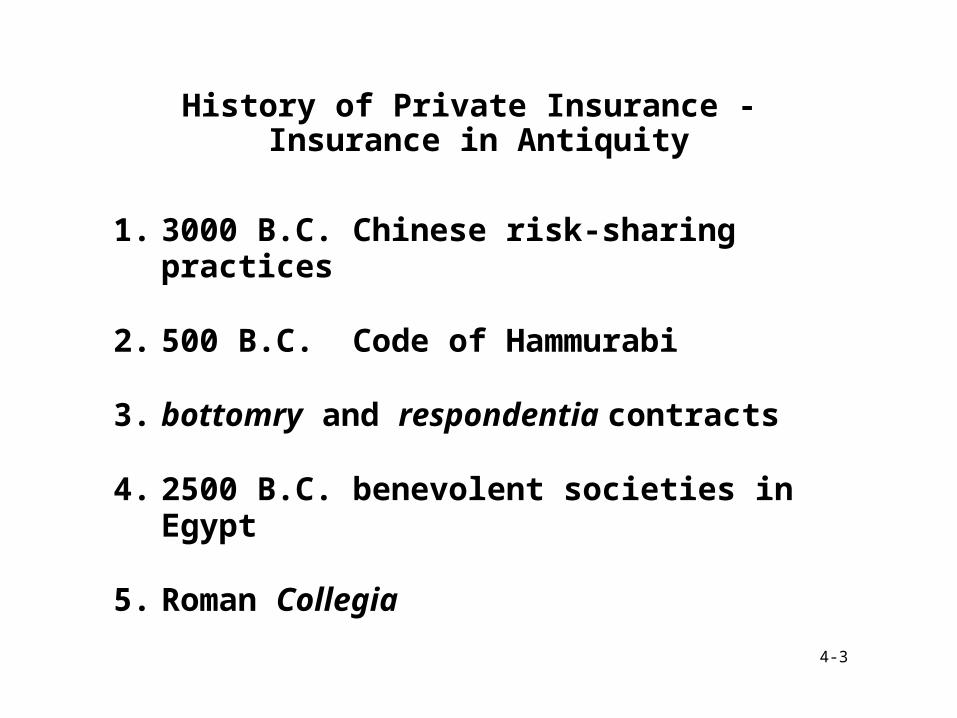

History of Private Insurance - Insurance in Antiquity

1. 3000 B.C. Chinese risk-sharing practices

2. 500 B.C. Code of Hammurabi

3. bottomry and respondentia contracts

4. 2500 B.C. benevolent societies in Egypt

5. Roman Collegia

4-4

History of Private Insurance -Marine and Fire Insurance

13th Century marine insurance originates in Italy

15th Century marine insurance to England by Lombard merchants

Year 1666 Fire of London (Dr. Nicholas Barbon)

Year 1688 Lloyd’s coffeehouse in operation

Year 1752 Ben Franklin’s Philadelphia Contributionship

Year 1792 First U.S. capital stock company, Insurance Company of North America

4-5

History of Private InsuranceCasualty Insurance

1848 Accident insurance for railroad travelers

1859 Travelers Insurance Company in U.S. sells accident insurance for travelers

1866 Steam boiler Insurance

1876 Fidelity bonds

1886 Employers liability insurance

1889 Elevators and public liability

1898 Automobile liability insurance

4-6

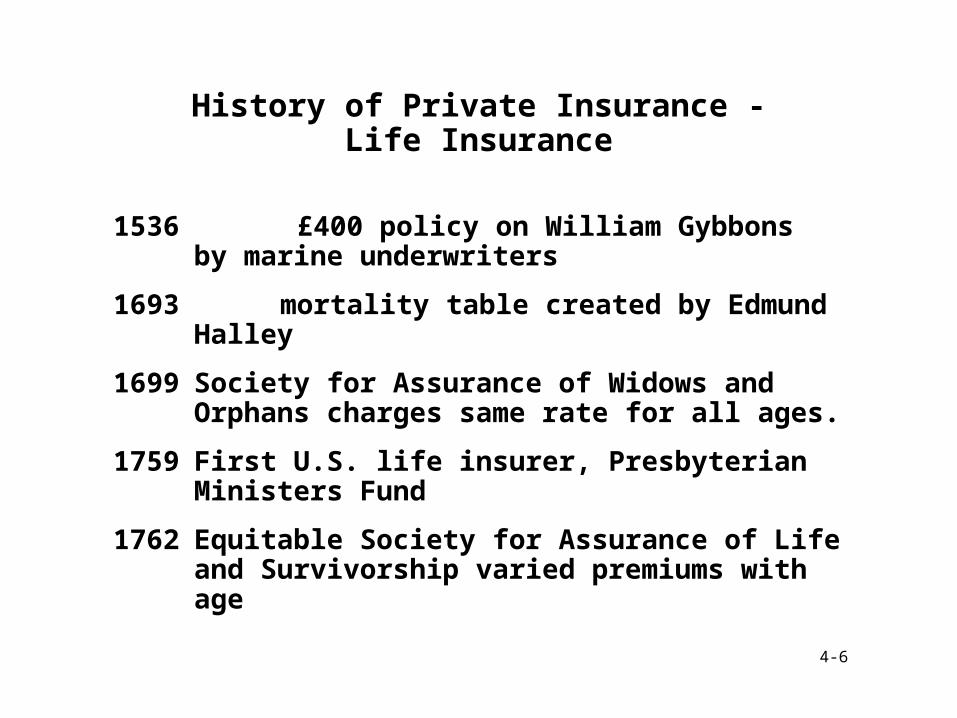

History of Private Insurance -Life Insurance

1536 £400 policy on William Gybbons by marine underwriters

1693 mortality table created by Edmund Halley

1699 Society for Assurance of Widows and Orphans charges same rate for all ages.

1759 First U.S. life insurer, Presbyterian Ministers Fund

1762 Equitable Society for Assurance of Life and Survivorship varied premiums with age

4-7

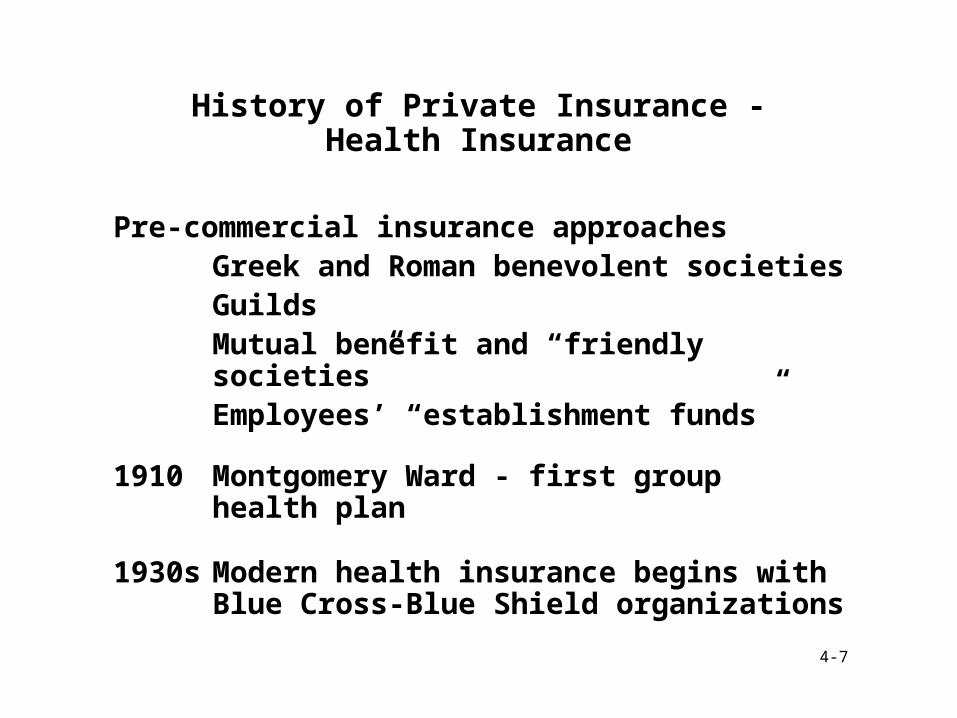

History of Private Insurance -Health Insurance

Pre-commercial insurance approachesGreek and Roman benevolent societiesGuildsMutual benefit and “friendly societies”Employees’ “establishment funds”

1910 Montgomery Ward - first group health plan

1930s Modern health insurance begins with Blue Cross-Blue Shield organizations

4-8

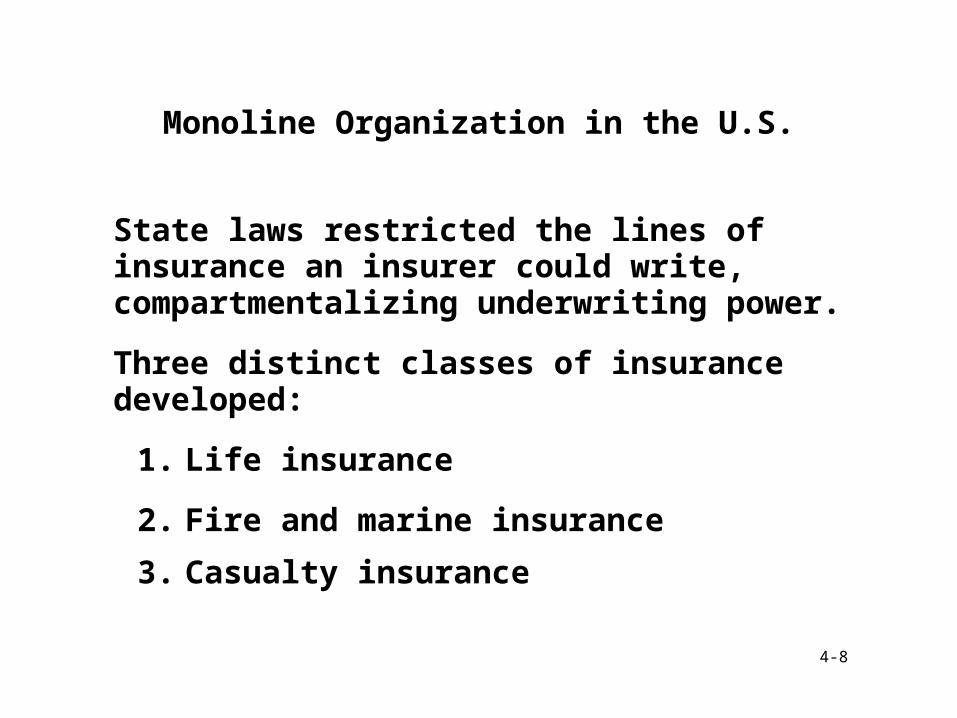

Monoline Organization in the U.S.

State laws restricted the lines of insurance an insurer could write, compartmentalizing underwriting power.

Three distinct classes of insurance developed:

1. Life insurance

2. Fire and marine insurance

3. Casualty insurance

4-9

Reasons for Monoline Organization

1. It was supposed that specialization would promote proficiency.

2. Segregation of insurance by class would simplify financial regulation.

3. Fear of danger in combining fire insurance (which seemed subject to catastrophes) with life insurance.

4. New York’s Appleton Rule required insurers to follow New York law in other states.

4-10

Multiple-Line Transition

1. States began to change laws in the 1940’s to permit multiple-line underwriting (writing of property and casualty by a single company).

2. New York permitted multiple-line underwriting in 1949.

3. Greatest benefit of multiple-line underwriting has been the “package policy.”

4. Compartmentalization still exists between life insurers and property and casualty insurers.

4-11

Modern Classification of Insurance Coverages

1. Life insurance

2. Accident and health insurance

3. Property and Liability insurance

4-12

Private (Voluntary) Insurance

1. Life insurance

2. Accident and health insurance

3. Property and liability

• fire

• marine

• casualty

• fidelity and surety bonds

4-13

Casualty Insurance

accident and health insuranceautomobileliabilityworkers compensationboiler and machineryplate glassburglary, robbery, theftcredit insurancetitle insurance

4-14

Social Insurance

Based on the notion that there are some people in society who face fundamental risks that they cannot deal with themselves.

Social insurance programs rest on the premise that if an individual cannot provide for a reasonable standard of living through personal efforts, society should assist.

4-15

Social Insurance Definition

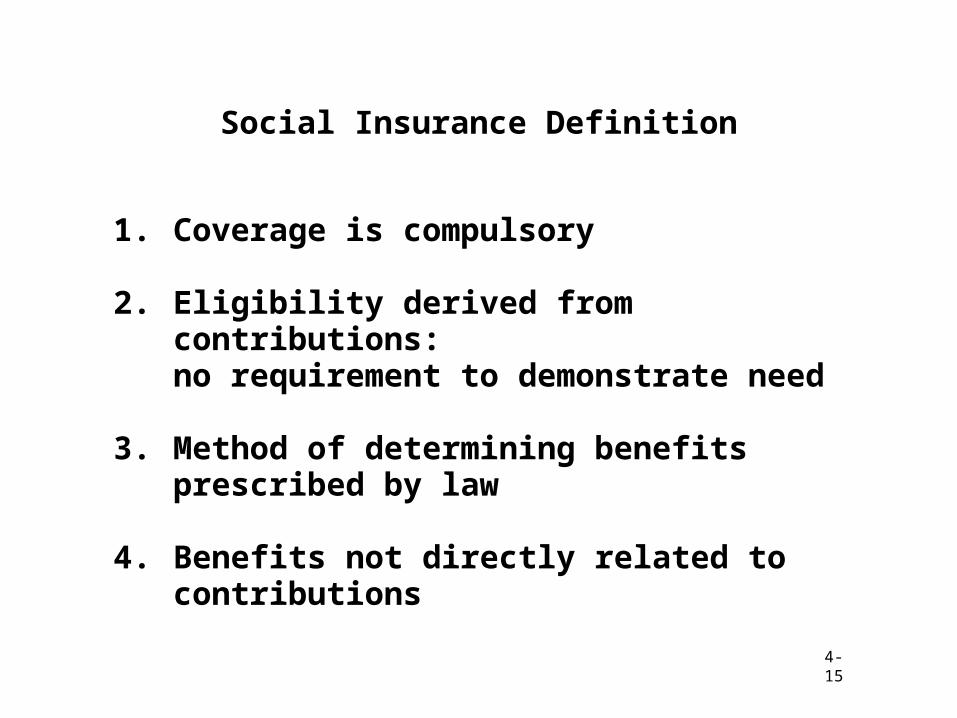

1. Coverage is compulsory

2. Eligibility derived from contributions: no requirement to demonstrate need

3. Method of determining benefits prescribed by law

4. Benefits not directly related to contributions

4-16

Social Insurance Definition

5. Definite long-range plan for financing

6. Cost borne primarily by contributions

7. Plan administered or supervised by government

8. Plan not established solely for government employees

4-17

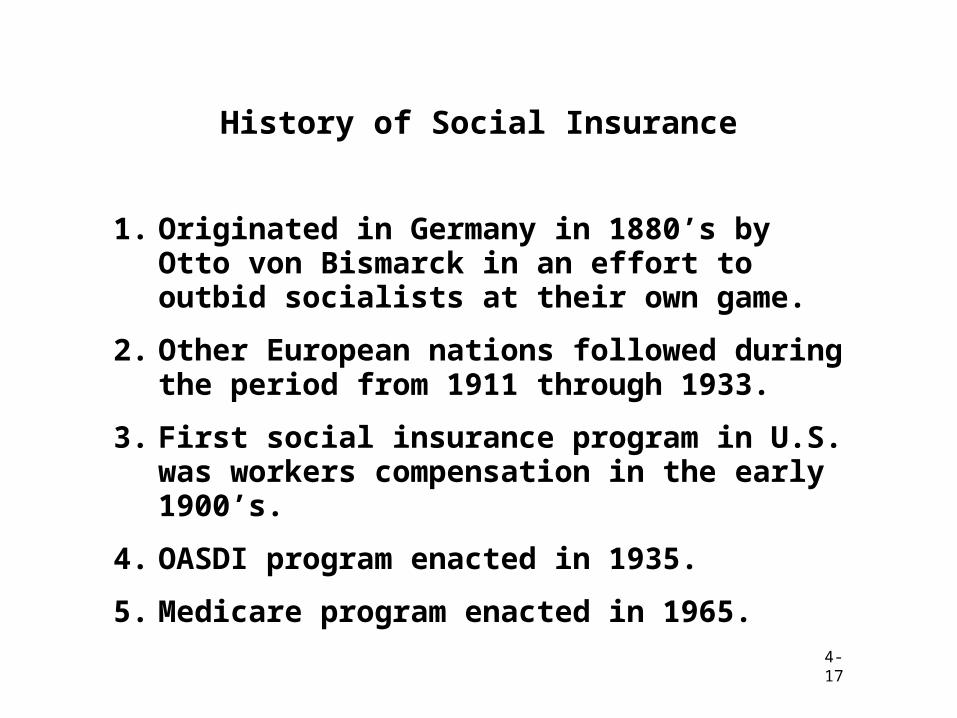

History of Social Insurance

1. Originated in Germany in 1880’s by Otto von Bismarck in an effort to outbid socialists at their own game.

2. Other European nations followed during the period from 1911 through 1933.

3. First social insurance program in U.S. was workers compensation in the early 1900’s.

4. OASDI program enacted in 1935.

5. Medicare program enacted in 1965.

4-18

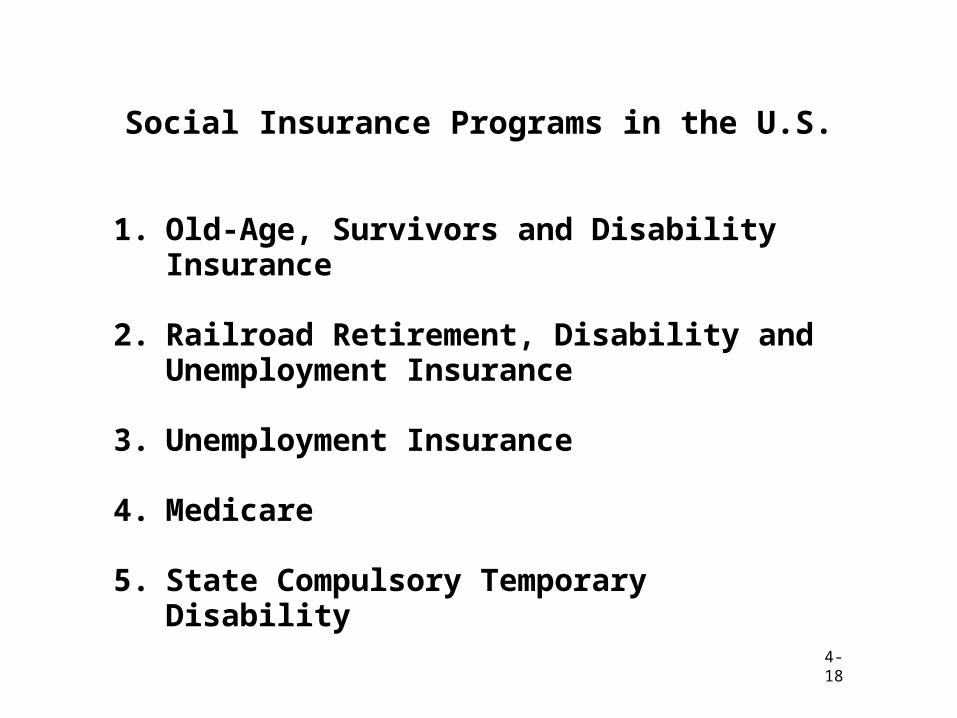

Social Insurance Programs in the U.S.

1. Old-Age, Survivors and Disability Insurance

2. Railroad Retirement, Disability and Unemployment Insurance

3. Unemployment Insurance

4. Medicare

5. State Compulsory Temporary Disability

4-19

Public Guarantee Insurance Programs

1. Quasi social insurance programs, mainly in connection with financial institutions

2. Public Guarantee Insurance Programs are usually allied with the function of regulation

3. Insurance principle is used to protect lenders, depositors, or investors against loss resulting from failure of a financial institution

4-20

Federal Public Guarantee Programs

1. Federal Deposit Insurance Corporation

2. National Credit Union Administration

3. Securities Investor Protection Corporation

4. Pension Benefit Guarantee Corporation

4-21

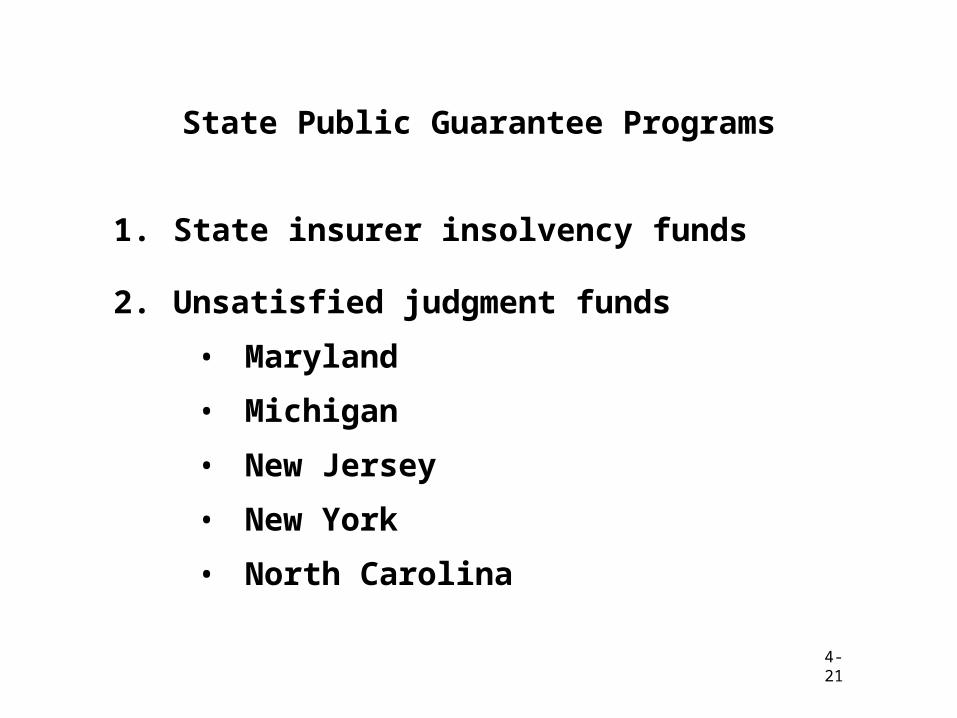

State Public Guarantee Programs

1. State insurer insolvency funds

2. Unsatisfied judgment funds

• Maryland

• Michigan

• New Jersey

• New York

• North Carolina

4-22

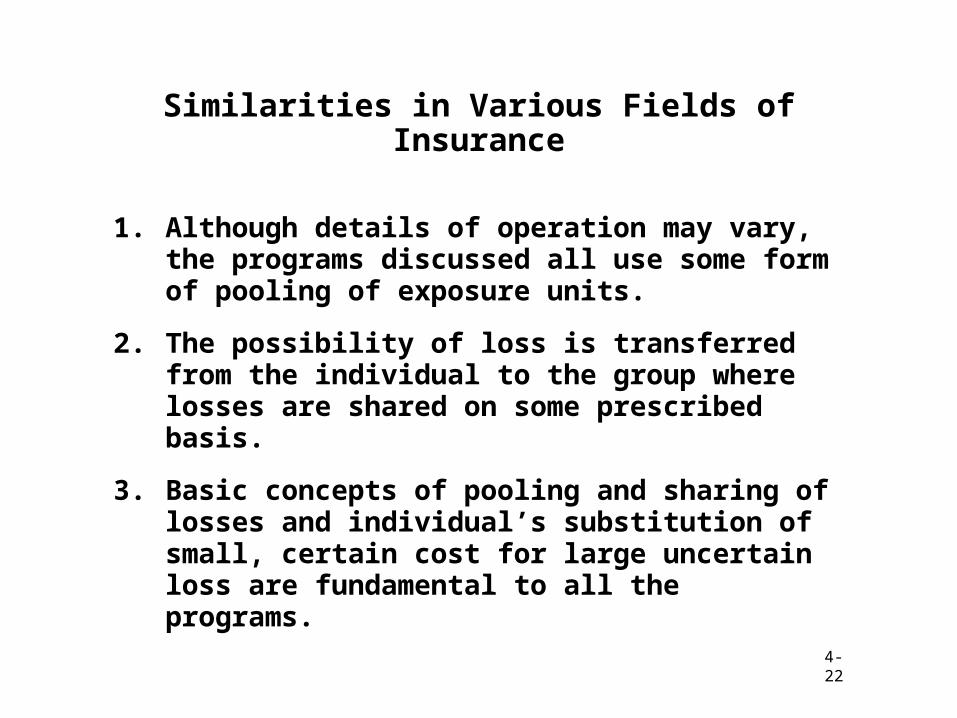

Similarities in Various Fields of Insurance

1. Although details of operation may vary, the programs discussed all use some form of pooling of exposure units.

2. The possibility of loss is transferred from the individual to the group where losses are shared on some prescribed basis.

3. Basic concepts of pooling and sharing of losses and individual’s substitution of small, certain cost for large uncertain loss are fundamental to all the programs.