? Provide deeper insight, latest developments? No econometrics, just general idea

? Wall Street Journal or Financial Times? Access to Internet, some Excel experience, basic

knowledge of econometrics? It is assumed that basic courses are still

remembered by you.? Groups of 4 or 5 (pls let secretary know by Friday)

11/01/2002Introduction6

Cases Cases (40% of the grade+20% for exam).(40% of the grade+20% for exam).? What case report is NOT:

– Not copy of textbook or article.– Not exercise in history of economics or finance. I do not care (at least, in

that class) who got Nobel Prize for what...

? Ideal case report is similar to consulting report:– Analysis of data that is in the case (preferrably statistical analysis)– Covering all relevant issues (pros and cons)

– Take the position and defend it!– Case report is not War and Peace. Be brief!– Please understand what you are writing about.– Cases are due before the discussion session.

? Do not spend more than 2 days on ANY case!? Class discussion is part of the case work.

9511 Investments - 1 4

11/01/2002Introduction7

Investment Project Investment Project (30% of the grade).(30% of the grade).? Main Goal: to give you hands-on experience in basic

investment management.? Developing the trading game plan by March.

– Main goal: lock- in the group into chosen strategy– Main document: short ”prospectus” (see web site for

details).? Trade (March-May)? Write final report (May)

– Assess your performance. What worked and what did not? Were your constraints binding?

– What did you learn?

11/01/2002Introduction8

My assumptions about you:My assumptions about you:?You know and understand basic regression

analysis (what is R2, statistical significance, etc.)

?You remember conditions of optimality from Microecon. Course

?You remember basics from Finance I and Investments

?You are willing to learn...

9511 Investments - 1 5

11/01/2002Introduction9

AssetsAssets? Real vs. Financial assets? Role of financial assets

– Consumption Timing– Allocation of Risk– Separation of Ownership

? Various financial assets– Money market– Fixed- income– Equities– Derivatives

? Trading the assets– types of market organizations– types of orders you can place

11/01/2002Introduction10

EquityEquity? Common stock? Preferred stock? Distinguish

? dividend yield (Yt=dt-1/Pt) from ? holding-period rate of return

? Excess rate of return: Rt,t+1 – rt

(as when buying on margin)

t

ttttt P

dPPR 11

1,??

???

?

9511 Investments - 1 6

11/01/2002Introduction11

Where to get data?Where to get data?? Easiest: web search engine, financial sites (Yahoo,

– Look at departamental web site: http://www.hhs.se/secfi/Databases/Databases.htm

? Dividends? Volume? Splits

11/01/2002Introduction12

IndexesIndexes

? Uses– Track average returns– Comparing performance of managers– Base of derivatives

? Factors in constructing or using an Index– Representative?– Broad or narrow?– How is it constructed?– Subjectivity Factor (Bethleham Steel)

9511 Investments - 1 7

11/01/2002Introduction13

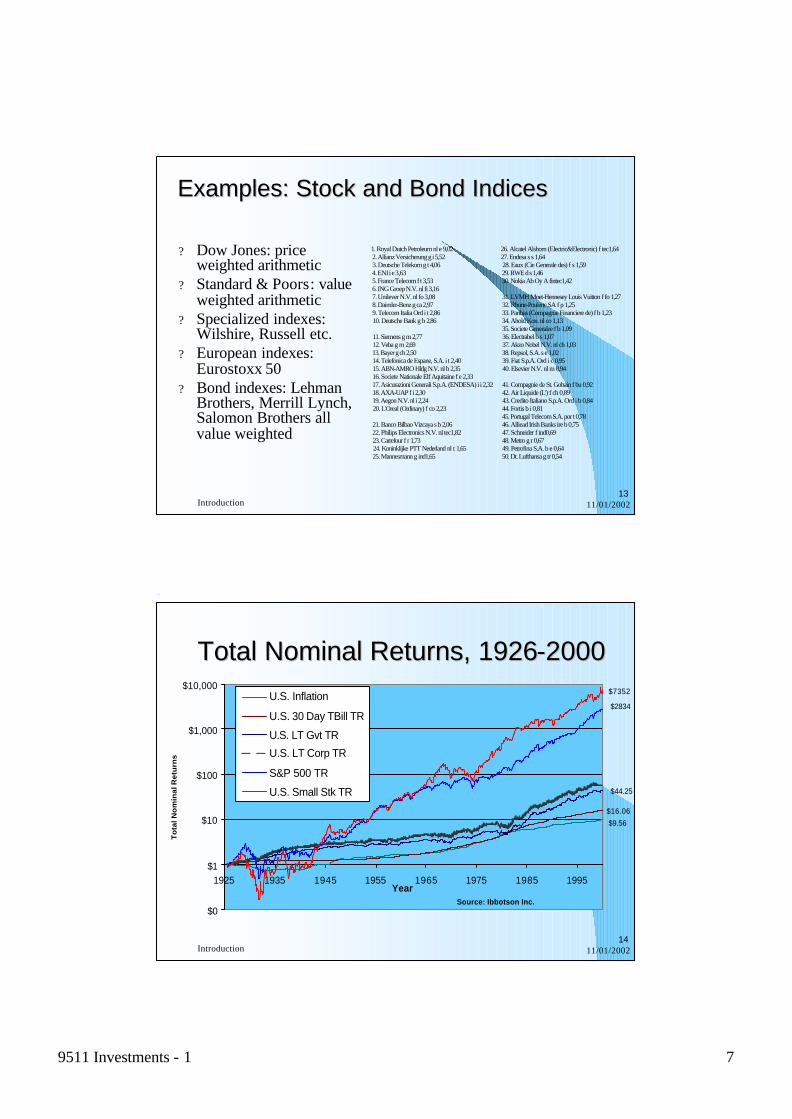

Examples: Stock and Bond IndicesExamples: Stock and Bond Indices

1. Royal Dutch Petroleum nl e 9,02 2. Allianz Versicherung g i 5,52 3. Deutsche Telekom g t 4,06 4. ENI i e 3,63 5. France Telecom f t 3,53 6. ING Groep N.V. nl fi 3,16 7. Unilever N.V. nl fo 3,08 8. Daimler-Benz g ca 2,97 9. Telecom Italia Ord i t 2,86 10. Deutsche Bank g b 2,86

11. Siemens g m 2,77 12. Veba g m 2,69 13. Bayer g ch 2,50 14. Telefonica de Espane, S.A. i t 2,40 15. ABN-AMRO Hldg N.V. nl b 2,35 16. Societe Nationale Elf Aquitaine f e 2,33 17. Asicurazioni Generali S.p.A. (ENDESA) i i 2,32 18. AXA-UAP f i 2,30 19. Aegon N.V. nl i 2,24 20. L'Oreal (Ordinary) f co 2,23

21. Banco Bilbao Vizcaya s b 2,06 22. Philips Electronics N.V. nl tec1,82 23. Carrefour f r 1,73 24. Koninklijke PTT Nederland nl t 1,65 25. Mannesmann g ind1,65

26. Alcatel Alshom (Electric&Electronic) f tec1,6427. Endesa s s 1,64 28. Eaux (Cie Generale des) f s 1,59 29. RWE d s 1,46 30. Nokia Ab Oy A fintec1,42

31. LVMH Moet-Hennesey Louis Vuitton f fo 1,27 32. Rhone-Poulenc SA f p 1,25 33. Paribas (Compagnie Financiere de) f b 1,23 34. Ahold Kon. nl co 1,13 35. Societe Generalee f b 1,09 36. Electrabel b s 1,07 37. Akzo Nobel N.V. nl ch 1,03 38. Repsol, S.A. s e 1,02 39. Fiat S.p.A. Ord i c 0,95 40. Elsevier N.V. nl m 0,94

41. Compagnie de St. Gobain f bu 0,92 42. Air Liquide (L') f ch 0,89 43. Credito Italiano S.p.A. Ord i b 0,84 44. Fortis b i 0,81 45. Portugal Telecom S.A. por t 0,78 46. Alliead Irish Banks ire b 0,75 47. Schneider f ind0,69 48. Metro g r 0,67 49. Petrofina S.A. b e 0,64 50. Dt. Lufthansa g tr 0,54

? Dow Jones: price weighted arithmetic

? Standard & Poors: value weighted arithmetic

? Specialized indexes: Wilshire, Russell etc.

? European indexes: Eurostoxx 50

? Bond indexes: Lehman Brothers, Merrill Lynch, Salomon Brothers all value weighted

11/01/2002Introduction14

Total Nominal Returns, 1926Total Nominal Returns, 1926--20002000

$0

$1

$10

$100

$1,000

$10,000

1925 1935 1945 1955 1965 1975 1985 1995Year

To

tal N

om

inal

Ret

urn

s

U.S. Inflation

U.S. 30 Day TBill TR

U.S. LT Gvt TR

U.S. LT Corp TR

S&P 500 TR

U.S. Small Stk TR

Source: Ibbotson Inc.

$9.56

$16.06

$2834

$7352

$44.25

9511 Investments - 1 8

11/01/2002Introduction15

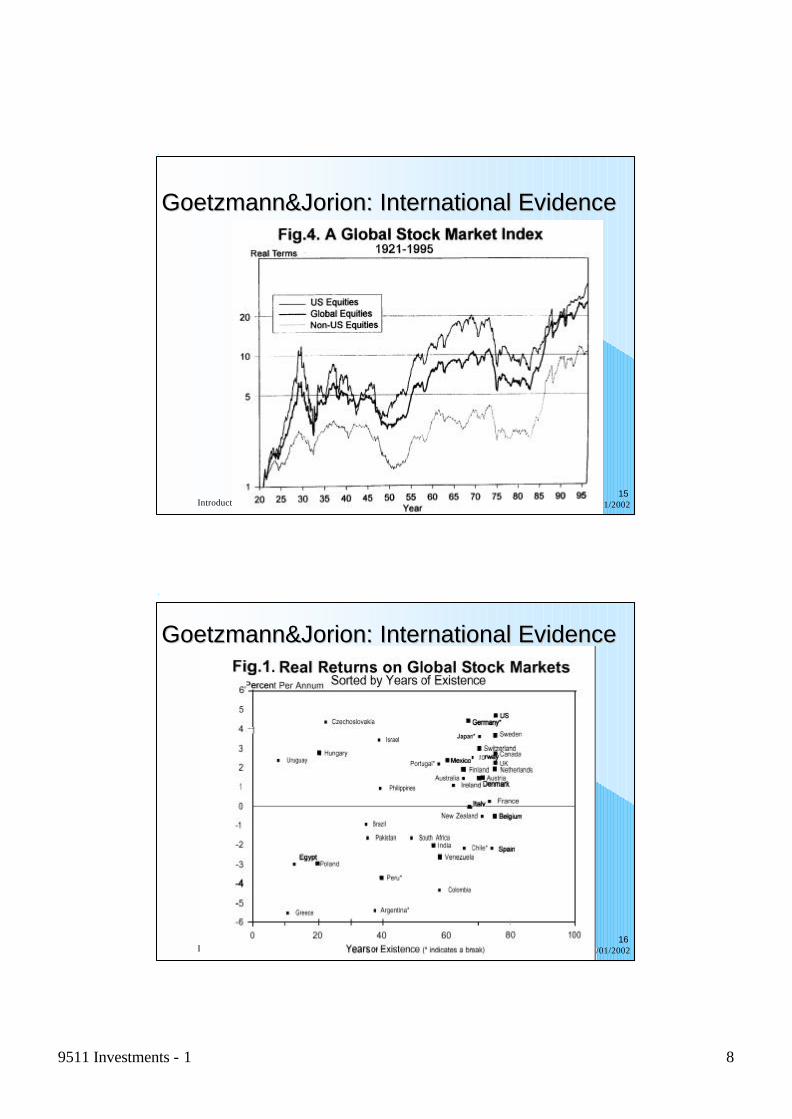

Goetzmann&Jorion: International EvidenceGoetzmann&Jorion: International Evidence

11/01/2002Introduction16

Goetzmann&Jorion: International EvidenceGoetzmann&Jorion: International Evidence

? Commodities futures? Stock index futures; program trading? Financial futures

? bond price futures? interest-rate futures? currency futures

11/01/2002Introduction18

The job of investment management: The job of investment management: objectives and constraintsobjectives and constraints

? Individual investor (or private banker, managed accounts): total return to individual’s horizon

? Hedge fund: total rate of return? Mutual fund: return in excess of benchmark ? Pension fund:

? defined contributions: longer-run return or return relative to benchmark

? defined benefits: LR total return relative to liabilities

? Insurance company: return relative to liabilities

9511 Investments - 1 10

11/01/2002Introduction19

Investors´ particularsInvestors´ particulars

? Attitude to risk? Time horizon (do

not confuse with holding period)

? Non-traded risks (liabilities, labor income, human capital)

? Constraints0%

20%

40%

60%

80%

100%

Cons

./Inco

me

Cons

./Grow

th

Modera

te Ri

sk

Aggr.

Risk

Merrill Lynch Risk CategoriesStocks Bonds Cash

11/01/2002Introduction20

Investment PhilosophyInvestment Philosophy

? Global or specialized into asset classes: ? domestic or world? stocks, bonds, currencies? small-cap or large-cap? value vs. growth? technology vs old boring

stocks? Currency hedging,

portfolio insurance.

? Passive (index funds):? Full replication? Optimization sampling? Synthetic replication

? Active:? Security selection (bottom

up)? Asset allocation (top-

down): optimize across pre-specified categories

? strategic (or LT) allocation

? Market timing? Tactical allocation

9511 Investments - 1 11

11/01/2002Introduction21

Top down vs. BottomTop down vs. Bottom--UpUp“One way is to tell yourself, ‘I want to have 8% in autos,’ because you have a hunch that autos are going to do well. You can close your eyes and throw darts at a list of auto stocks, and buy a few. Another way is to analyze each company on a case-by-case basis…In the first instance, the 8% weighting in autos is deliberate and the choice of companies is incidental; in the second, the choice of companies is deliberate and the weighting is incidental.”

Peter Lynch

11/01/2002Introduction22

How to live with risk?How to live with risk?? Know and classify risks into

asset classes. On what basis?? Price risk (Country (incl.

Political risk), Industry,statistical categories)

? Credit risk, counterparty risk? Tail risk or risk of ruin

? Most important classification concept: statistical correlation? pitfalls of correlations? quasi-arbitrage opportunities

(“convergence trades”): LTCM and limits of arbitrage (Shleifer &Visny)

Large vs. Small Cap: Total Return (01.1954=$1)

$1

$3

$5

$7

$9

$11

$13

$15

$17

1954 1959 1964 1969

Large CapSmall CapLarge CapSmall Cap

HIGH CORRELATION? =0.99

LOW CORRELATION

? =0.5

9511 Investments - 1 12

11/01/2002Introduction23

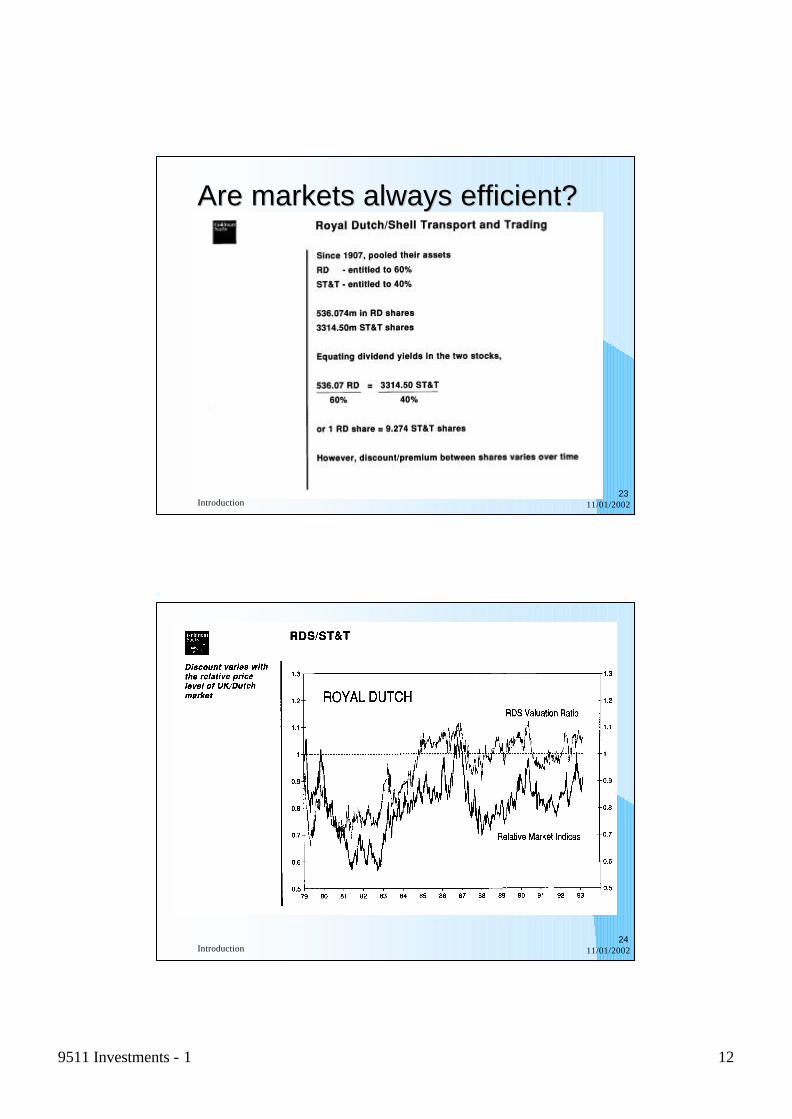

Are markets always efficient?Are markets always efficient?

11/01/2002Introduction24

9511 Investments - 1 13

11/01/2002Introduction25

Primary vs. Secondary Security Primary vs. Secondary Security SalesSales?Primary

– New issue– Key factor: issuer receives the proceeds from the

sale– Problem: Not enough prior history ? lemons

?Secondary– Existing owner sells to another party– Issuing firm doesn’t receive proceeds and is not

directly involved

11/01/2002Introduction26

Investment Banking Investment Banking ArrangementsArrangements? Underwritten vs. “Best Efforts”

– Underwritten: firm commitment on proceeds to the issuing firm

– Best Efforts: no firm commitment? Negotiated vs. Competitive Bid

– Negotiated: issuing firm negotiates terms with investment banker

– Competitive bid: issuer structures the offering and secures bids

9511 Investments - 1 14

11/01/2002Introduction27

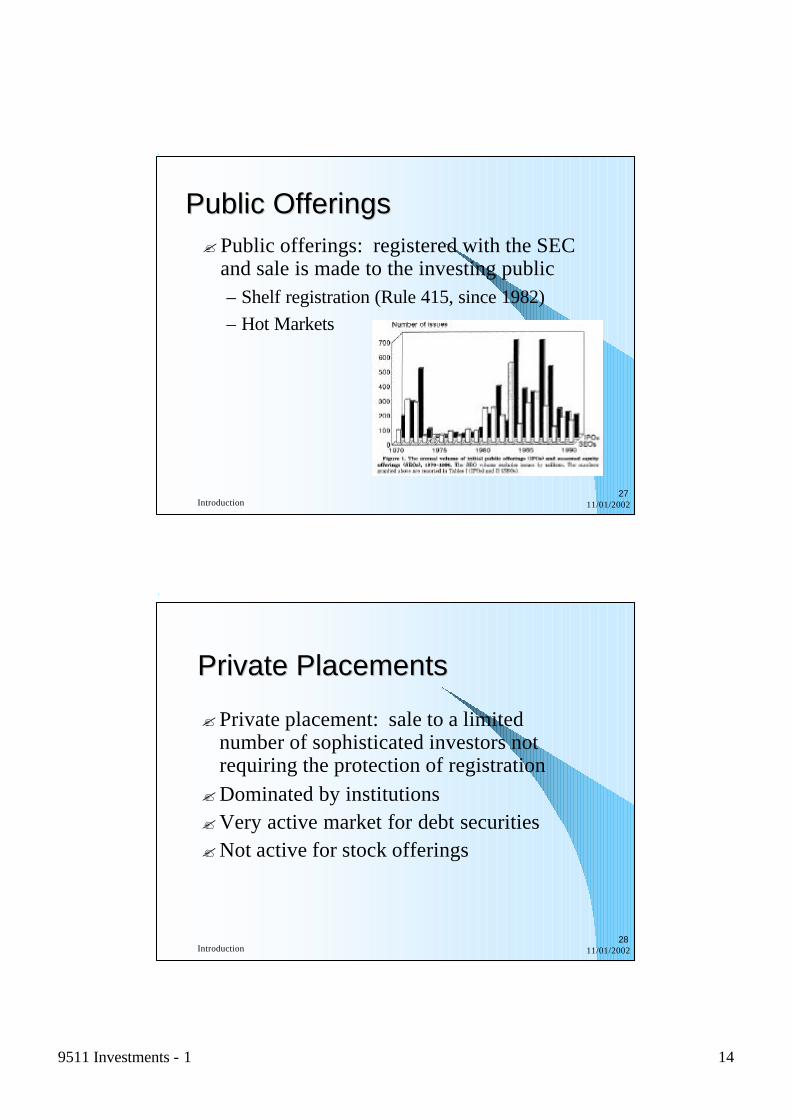

Public OfferingsPublic Offerings?Public offerings: registered with the SEC

and sale is made to the investing public– Shelf registration (Rule 415, since 1982)– Hot Markets

11/01/2002Introduction28

Private PlacementsPrivate Placements

?Private placement: sale to a limited number of sophisticated investors not requiring the protection of registration

?Dominated by institutions?Very active market for debt securities?Not active for stock offerings

9511 Investments - 1 15

11/01/2002Introduction29

Organization of Secondary Organization of Secondary MarketsMarkets?Organized exchanges?OTC market?Third market?Fourth market

11/01/2002Introduction30

Execution SystemExecution System

Dealers Market Oral Auction

Order-Matching System

Brokered Markets

Characterization Quote-Driven Order-Driven Order-Driven Brokered Who offers liquidity? Dealers

Dealers and Limit-Order Book Traders (via LOB) Traders

Who arranges trades? Dealers Traders, Dealers Brokers or Exchanges Brokers

Matching algorithm

Clients choose dealers

Negotiations (under trading rules) Trading rules

Brokers match traders

Examples NASDAQ NYSE SSE Upstairs market

9511 Investments - 1 16

11/01/2002Introduction31

Organized ExchangesOrganized Exchanges?Auction markets with centralized order

flow?Dealership function: can be competitive or

assigned by the exchange (Specialists)– Price continuity– Immediacy

? Securities: stock, futures contracts, options, and to a lesser extent, bonds

?Examples: NYSE, AMEX, Regionals, CBOE

11/01/2002Introduction32

OTC MarketOTC Market

?Dealer market without centralized order flow

?NASDAQ: largest organized stock market for OTC trading; information system for individuals, brokers and dealers

?Securities: stocks, bonds and some derivatives– Most secondary bonds transactions

9511 Investments - 1 17

11/01/2002Introduction33

Third Third and Fourth and Fourth MarketMarket

?Trading of listed securities away from the exchange

? Institutional market: to facilitate trades of larger blocks of securities

? Involves services of dealers and brokers(third market) or completely automated (INSTINET)

? Informational content of trades is very high!

11/01/2002Introduction34

ECN Unique Features Client Base

% ECN Mkt Share [Daily

Vol, $M] Partners (co-ownership) and Relationship

ArchipelagoIntegrated ECN order book-filing for exchange status

10.4% shares: Goldman Sachs, ETrade, CNBC, Instinet, American Century Ventures/J.P. Morgan, Merrill Lynch, Pacific Coast Exchange, GDP, and Virago Enterprises; Relationships: Pacific Stock Exchange,Tradepoint

Brut Third market, self-clearing with Sungard

Institutional investors, broker-dealers 8 [39]

Sungard Data Systems (20%), smaller stakes held by Bear Stearns, Bridge, Goldman Sachs, Knight-Trimark, Merrill Lynch, Morgan Stanley, Salomon Smith Barney

Instinet

Global market access, liquidity, discretionary pricing

Wholly owned subsidiary of Reuters; Relationships: Archipelago, ETrade, TheStreet.com

IslandLiquidity,transparency-filing for exchange status

Online brokerage and day-trading firms, proprietary desks/firms 19 [95]

Owned by Datek Online, Relationships: U-Click, TradingLab

RediBook

Relationship with Spear, Leeds & Kellogg, the largest clearing house

Hedge-fund managers, individual & inst. Investors, options MM 16 [79]

Spear, Leads & Kellogg*; Fidelity Investments; Charles Schwab; Donaldson, Lufkin & Jenrette; Lehman Brothers; Credit Suisse First Boston; Bank of America; and TD Waterhouse

TradeBook

Global market access through Bloomberg terminals, pegging, discretionary pricing

Institutional investors, broker-dealers 8 [40]

Owned by Bloomberg, Relationships: ITG-Posit, E-Crossnet

ECN’sECN’s

9511 Investments - 1 18

11/01/2002Introduction35

Stockholm Stock Exchange Stockholm Stock Exchange (SAX trading system)(SAX trading system)

? Similar to Paris (CAC) and Toronto (CATS)– Centralized, consolidated and transparent limit order

book– Automatic matching– Only authorized brokerages can trade directly– Brokerages can act as dual capacity dealers

? Front-running

– Separate small-order execution system– Anonymity: only dealer knows who is behind the order

he is placing? His own trade? Trade of ”sophisticated” customer.

11/01/2002Introduction36

Costs of TradingCosts of Trading?Commission: fee paid to broker for making

the transaction?Spread: cost of trading with dealer

– Bid: price dealer will buy from you– Ask: price dealer will sell to you– Spread: ask - bid

?Combination: on some trades both are paid?Discount brokers: payment for order flow

9511 Investments - 1 19

11/01/2002Introduction37

Types of OrdersTypes of Orders? Instructions to the brokers on how to

complete the order?Market?Limit

– Amihud & Mendelson(1991): Immediacy is supplied by limit orders and is consumed by market orders

– SSE: Direct subsidies for Limit Order?Stop loss

11/01/2002Introduction38

?Using only a portion of the proceeds for an investment

?Borrow remaining component?Margin arrangements differ for stocks and

futures

Margin TradingMargin Trading

9511 Investments - 1 20

11/01/2002Introduction39

?Maximum margin– Currently 50%– Set by the Fed

?Maintenance margin– Minimum level the equity margin can

be?Margin call

– Call for more equity funds

Stock Margin TradingStock Margin Trading

11/01/2002Introduction40

Regulation of Securities Regulation of Securities MarketsMarkets?Government Regulation?Self-Regulation ?Circuit Breakers? Insider Trading

9511 Investments - 1 21

11/01/2002Introduction41

”New economy” and investment industry: ”New economy” and investment industry: ValuationValuation

? Is Internet comparable with Industrial Revolutions?? No (Robert J. Gordon, NBER WP7833)

– Productivity does not grow in 88% of economy, moreover, after correcting for computing purchases it decelerates

– WWW does not boost the demand of computer outside of normal responce to price decline (i.e., demand curve is essentially the same)

– Use of PCs and Internet involves the substitution of existing activity from one medium to another. Thus, private and social returns are different

? Thus, no new valuation philosophy is justified.

11/01/2002Introduction42

Technology and Delivery of Technology and Delivery of Investment Service (1)Investment Service (1)

? Structure of Investment Industry is changing.– Brokers´pretax margin down from 15% in 98 to 10% in 02– Structure of revenues changes from comissions to fees

0

10

20

30

40

50

60

70

80

Bln

US

$

1998 1999 2000 2001 2002 2003

Retail Brokerage Industry- RevenuesAdvisory FeesMutual Funds FeesNet Investment IncomePmnt for order flow/MiscCommission

Source: MSDW research

9511 Investments - 1 22

11/01/2002Introduction43

Technology and Delivery of Technology and Delivery of Investment Service (2)Investment Service (2)? Information processing cost goes down (37% in 5 yrs)? Information delivery cost approaches 0.? No more ”proprietary” sales , higher specialization.? Middle man is gone.

– Standard Life insurance policy: 50% in Yr1, 5% thereafter, total benefit ?13% of premium.

? Market segmentation increases (might result in higher price dispersion, see Brown and Goolsbee, NBER w7996)

11/01/2002Introduction44

GlobalizationGlobalization

International and Global Markets Continue Developing

? Managing foreign exchange? Diversification to improve

performance? Instruments and vehicles continue to

develop? Information and analysis improves

9511 Investments - 1 23

11/01/2002Introduction45

Financial EngineeringFinancial EngineeringRepackaging Services f Financial

Intermediaries?Bundling and unbundling of cash flows?Slicing and dicing of cash flows? Integration of investments & corporate