55

How to Value Bonds and Stocks

| Date post: | 01-Jun-2018 |

| Category: |

Documents |

| Upload: | kamrul-hasan-khan-shatil |

| View: | 213 times |

| Download: | 0 times |

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 1/55

How to Value

Bonds and

Stocks

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 2/55

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 3/55

Bond Definitions

• "ond• #ar $alue (face $alue)

• %oupon rate

• %oupon pament• &aturit date

• Time to &aturit

• 'ield or 'ield to maturit

• %urrent 'ield

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 4/55

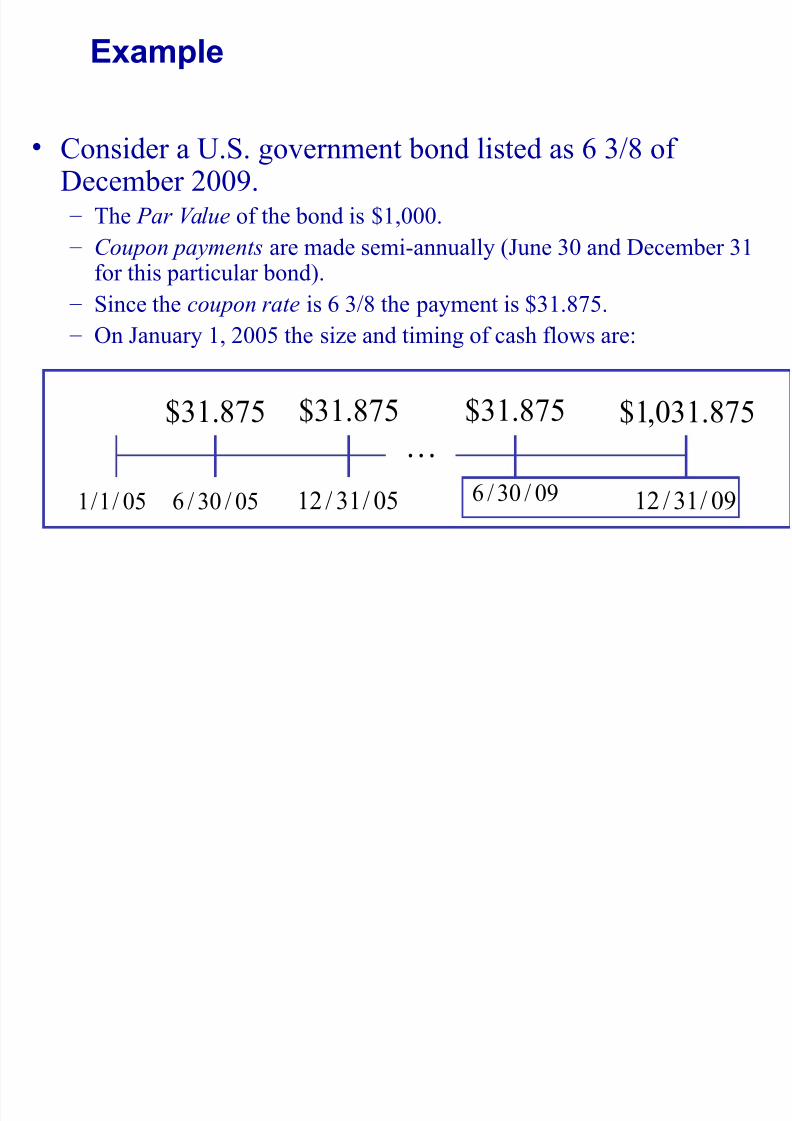

Example

• %onsider a !S! go$ernment bond listed as *+, ofDecember -../! – The Par Value of the bond is 012...!

– Coupon payments are made semi3annuall (4une *. and December *1

for this particular bond)! – Since the coupon rate is *+, the pament is 0*1!,56!

– 7n 4anuar 12 -..6 the size and timing of cash flows are:

.6+1+1

,56!*10

.6+*.+

,56!*10

.6+*1+1-

,56!*10

./+*.+

,56!.*1210

./+*1+1-

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 5/55

Level-Coupon Bonds: Example

8ind the present $alue (as of 4anuar 12 -..9)2 of a 3*+, coupon T3 bond with semi3annual paments2 and a maturit date of

December -../ if the 'T& is 63percent!

– 7n 4anuar 12 -..9 the size and timing of cash flows are:

.9+1+1

,56!*10

.9+*.+

,56!*10

.9+*1+1-

,56!*10

./+*.+

,56!.*1210

./+*1+1-

6-!.5.210).-6!1(

...210

).-6!1(

11

-.6!

,56!*101-1-

=+

−= PV

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 6/55

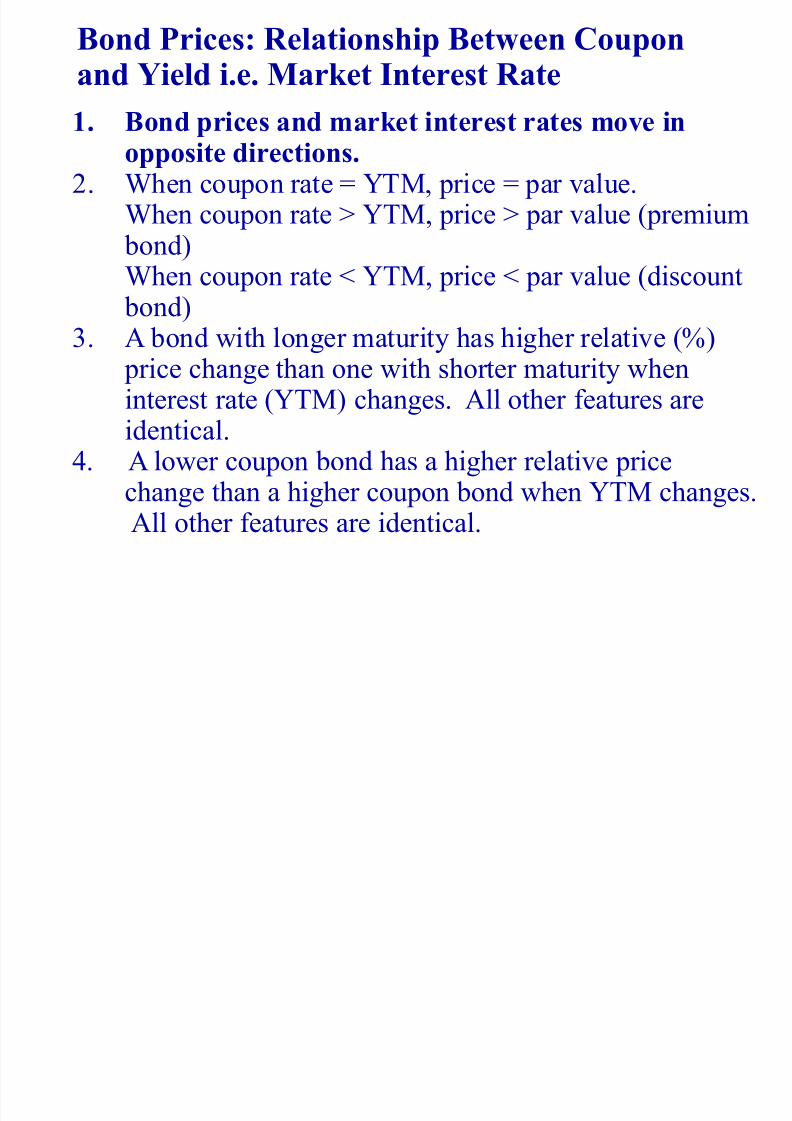

Bond Prices: Relationship Between Couponand Yield i.e. Market Interest Rate

. Bond prices and !arket interest rates !ove inopposite directions.

-! hen coupon rate ; 'T&2 price ; par $alue!hen coupon rate < 'T&2 price < par $alue (premium

bond)

hen coupon rate = 'T&2 price = par $alue (discount bond)

*! > bond with longer maturit has higher relati$e (?) price change than one with shorter maturit when

interest rate ('T&) changes! >ll other features areidentical!9! > lower coupon bond has a higher relati$e price

change than a higher coupon bond when 'T& changes!>ll other features are identical!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 7/55

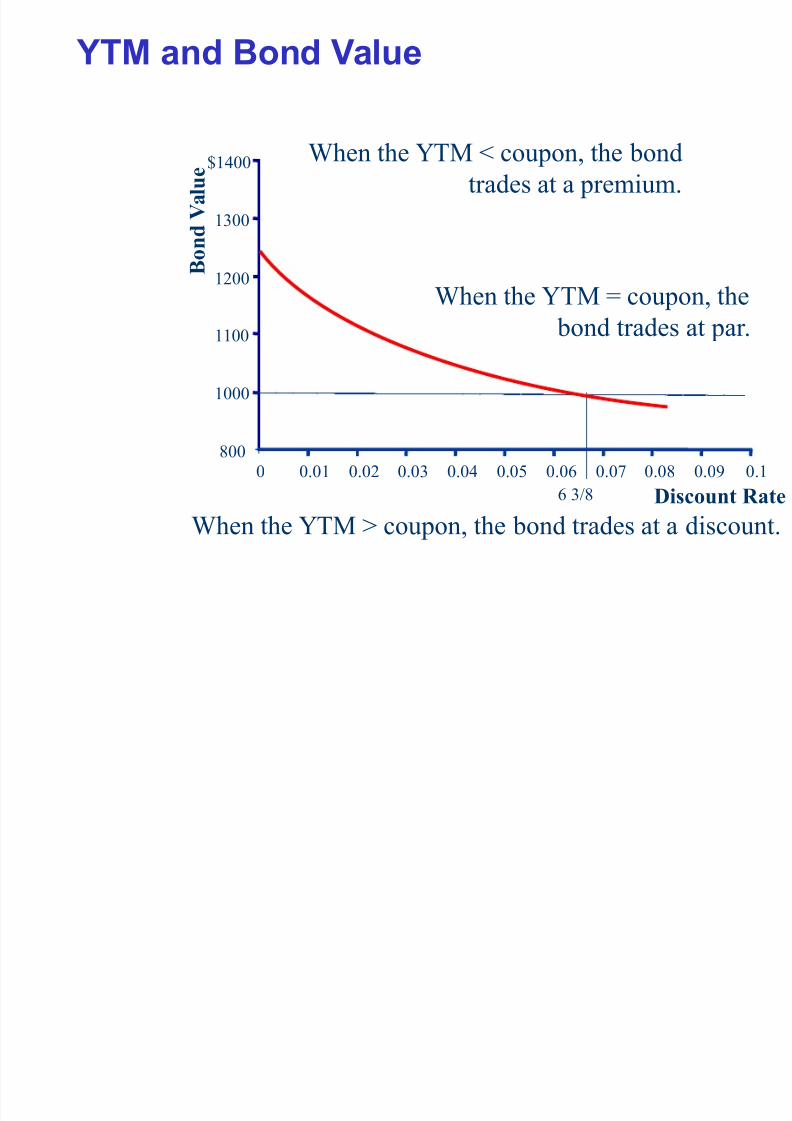

YTM and Bond Value

hen the 'T& = coupon2 the bond

trades at a premium!

hen the 'T& ; coupon2 the

bond trades at par!

hen the 'T& < coupon2 the bond trades at a discount!

,..

1...

11..

1-..

1*..

019..

. .!.1 .!.- .!.* .!.9 .!.6 .!. .!.5 .!., .!./ .!1

Discount Rate

B o n d " a l u e

*+,

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 8/55

Maturity and Bond rice Volatility

%onsider two otherwise identical

bonds!

The long3maturit bond will ha$e

much more $olatilit with respect tochanges in the discount rate

C Discount Rate

B o n d " a l u e

Par

Short &aturit "ond

@ong &aturit "ond

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 9/55

Coupon !ate and Bond rice Volatility

%onsider two otherwise identical bonds!

The low3coupon bond will ha$e much more

$olatilit with respect to changes in thediscount rate

Discount Rate

B

o n d " a l u e

Aigh %oupon "ond

@ow %oupon "ond

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 10/55

The Bond Indenture

• Bond Indenture is the contract between issuerand in$estor which includes detailed terms andconditions regarding the bond issue! Bt containsthe different rights of the bondholders and

restrictions applicable to the bond issuer! Btgenerall includes the following:

– The basic terms of the bonds

– The total amount of bonds issued – > description of propert used as securit2 if applicable

– Sinking fund pro$isions

– %all pro$isions

– Details of protecti$e co$enants

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 11/55

The Bond Indenture

Trustee (a bank or other financial institution)

works as the middle man between issuer and

in$estor! The trust compan or the trustee makes

sure that the terms of the indenture are obeed2

manages the sinking fund2 and represents the bondholders if the issuer defaults on its paments!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 12/55

• #ecurit$ – %ollateral – secured b financial securities

– &ortgage – secured b real propert2 normall

land or buildings

– Debentures – unsecured

– Cotes – unsecured debt with original maturit less

than 1. ears

• #eniorit$

this indicates preference of recei$ing debt

obligations and termed as senior or unior!

The Bond Indenture

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 13/55

Call provision allows the issuer to call back orrepurchase part or all of the bond issue at stated prices o$er a specified period! %orporate bondsare usuall callable!

Call pre!iu! is the difference between call price and the stated or par $alue of the bond!

Deferred call provision prohibits the issuer to

call back the bonds prior to a certain date! Call protected bond can not be repurchased

during a certain time period b the issuer

Protective covenants

The Bond Indenture

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 14/55

Bond Characteristics and Re%uired Returns

• The coupon rate depends on the riskcharacteristics of the bond when issued

• hich bonds will ha$e the higher coupon2 all

else eualF – Secured debt $ersus a debenture

– Subordinated debenture $ersus senior debt

– > bond with a sinking fund $ersus one without

– > callable bond $ersus a non3callable bond

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 15/55

&ccrued Interest ' (uoted Bond Price

The bond prices that are uoted in the financial

pages are not the prices that in$estors pa for the bond! "ecause the %uoted or clean price does not

include accrued interest between coupon pament

dates! Aowe$er2 in$estors pa the in$oice price ordirty price i!e! stated price plus accrued interest!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 16/55

Default Risk or Credit Risk refers to the possibilit that the bond issuing

firm ma default in paing the promised cashflows either coupons during the life of the bondsor the face amount at maturit!

There are $arious credit ratin) a)encies thatregularl publish their rating on corporate bonds based on the default or credit risk of the bondissuing firm! "ased on the rating2 bonds areclassified as investment grade bonds and non-investment grade bonds or junk bonds. 4unk bonds ha$e high credit risk and also pro$idehigh ield to the in$estors!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 17/55

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 18/55

,ero-Coupon Bonds

•&ake no periodic interest paments (coupon rate; .?)

• The entire ield3to3maturit comes from the

difference between the purchase price and the par

$alue

• %annot sell for more than par $alue

• Sometimes called zeroes2 or deep discount bonds

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 19/55

Pure Discount Bonds

Bnformation needed for $aluing pure discount bonds: – Time to maturit (T ) ; &aturit date 3 todaGs date

– 8ace $alue ( F )

– Discount rate (r )

T r

F PV

)1( +=

#resent $alue of a pure discount bond at time .:

.

.0

1

.0

-

.0

1−T

F 0

T

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 20/55

Pure Discount Bonds: *+a!ple

8ind the $alue of a *.3ear zero3coupon bond with

a 012... par $alue and a 'T& of ?!

11!1590).!1(

...210

)1( *. ==

+=

T r

F PV

.

.0

1

.0

-

.0

-/

...210

*.

.

.0

1

.0

-

.0

-/

...210

*.

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 21/55

loatin) Rate Bonds

•%oupon rate floats depending on some indeH$alue

• EHamples – adustable rate mortgages and

inflation3linked Treasuries

• There is less price risk with floating rate bonds

– The coupon floats2 so it is less likel to differ

substantiall from the ield3to3maturit

• %oupons ma ha$e a IcollarJ – the rate cannot go

abo$e a specified IceilingJ or below a specified

IfloorJ

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 22/55

Inflation and Interest Rates

•Keal rate of interest

• Cominal rate of interest

• The 8isher Effect defines the relationship

between real rates2 nominal rates and inflation

• (1 L K) ; (1 L r)(1 L h)2 where

– K ; nominal rate

– r ; real rate

– h ; eHpected inflation rate

• >pproHimation

– K ; r L h

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 23/55

*+a!ple

• Bf we reuire a 1.? real return and we eHpectinflation to be ,?2 what is the nominal rateF

• K ; (1!1)(1!.,) – 1 ; !1,, ; 1,!,?

• >pproHimation: K ; 1.? L ,? ; 1,?• "ecause the real return and eHpected inflation

are relati$el high2 there is significant

difference between the actual 8isher Effectand the approHimation!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 24/55

Differences Between Debt and *%uit$

• Debt

– Cot an ownership interest – %reditors do not ha$e

$oting rights – Bnterest is considered a

cost of doing business

and is taH deductible – %reditors ha$e legal

recourse if interest or principal paments aremissed

– EHcess debt can lead tofinancial distress and bankruptc

• Euit

– 7wnership interest – %ommon stockholders $ote

for the board of directors andother issues

– Di$idends are not considered

a cost of doing business andare not taH deductible

– Di$idends are not a liabilitof the firm and stockholdersha$e no legal recourse ifdi$idends are not paid

– >n all euit firm can not go bankrupt

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 25/55

Term Structure of "nterest !ates

The short3term interest rates and long3term interestrates generall differ from each other! Sometimes2short3term rates are higher2 sometimes lower!

The relationship between short and long3term interestrates is known as the ter! structure of interest rates.

The term structure of interest rates indicates theno!inal interest rates on default free pure discount

bonds of all maturities! Bn other words2 the term

structure tells us the pure time $alue of mone fordifferent lengths of time!

hen long3term rates are higher than short3term rates – it is said that the term structure is upward sloping!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 26/55

Term Structure of "nterest !ates

hen short3term rates are higher than the long3termrates2 it is said that the term structure is downwardsloping! The term structure can also be humped when

both the rates increase initiall and after that start todecline as longer and longer term rates are considered!

The most common shape of the term structure isupward sloping with $ariable steepness!

The shape of the term structure is determined b threefactors such as the real rate of interest2 the inflationrate and the interest rate risk! The real interest rate isthe basic component underling e$er interest rate2regardless of time to maturit! >s such2 real rate doesnot actuall determine the shape of the term structurerather it influences o$erall interest rates!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 27/55

Term Structure of "nterest !ates

7n the other hand2 the prospect of future inflationstrongl influences the shape of the term structure! >sfuture inflation erodes the $alue of mone that will berecei$ed in future from current in$estment2 thein$estors demand compensation for this loss in the

form of higher nominal rates! This eHtra compensationis called inflation pre!iu!! Bf in$estors belie$e theinflation rate will be higher in the future2 then longterm rates will tend to be higher than the short3term

rates! Therefore2 an upward sloping term structure maindicate an increase in inflation in future and $ice$ersa!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 28/55

Term Structure of "nterest !ates

The third component of the term structure is the

compensation for interest rate risk that increases with

the term to maturit! @onger3term bonds ha$e more

interest rate risk than the shorter3term bonds and

in$estors demand eHtra compensation in the form ofhigher rates for bearing this risk – this is known as

interest rate risk pre!iu!! 8or longer term to

maturit2 the greater is the interest rate risk2 therefore

interest rate risk premium increases with maturit!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 29/55

#p$ard-Slopin% Yield Curve

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 30/55

&o$n$ard-Slopin% Yield Curve

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 31/55

Bond Yields and t'e Yield Curve

> graph of the Treasur ields relati$e to maturit is

called the Treasur$ $ield curve or simpl the $ield

curve! The shape of the ield cur$e reflects the term

structure of interest rates! Bn fact2 ield cur$e and the

term structure of interest rates are almost the samething eHcept that the term structure is based on pure

discount bonds whereas ield cur$e is based on coupon

bond ields! >s such2 the Treasur ields are based on

the same three factors that determine term structure!"esides2 the Treasur notes and bonds are default free2

subect taH2 and highl liuid!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 32/55

Treasury Yield Curve May (() *++(

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 33/55

Bond Yields and t'e Yield Curve

The scenario is different in case of corporate bonds!

These bonds ha$e the possibilit of default! >s such2

in$estors reuire higher ield as compensation for this

risk2 this eHtra compensation is called default risk

pre!iu!! Bn$estors reuire additional return for bondsthat are subect to taH – this is known as ta+abilit$

pre!iu!! "onds ha$e different degrees of liuidit!

The more liuid bonds ha$e lower ields and $ice

$ersa! This is called li%uidit$ pre!iu!!8inall2 anthing else that affects the risk of the cash

flows to the bondholders2 will affect the bond ield!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 34/55

Valuation of Common Stocks

• Di$idends $ersus %apital Mains

• Naluation of Different Tpes of Stocks

– Oero Mrowth – %onstant Mrowth

– Differential Mrowth

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 35/55

Case (: ,ero ro$t'

• >ssume that di$idends will remain at the same le$el fore$er

r P

r r r P

Di$

)1(

Di$

)1(

Di$

)1(

Di$

.

*

*

-

-

1

1

.

=

++++++=

===*-1 Di$Di$Di$

Since future cash flows are constant2 the $alue of a zerogrowth stock is the present $alue of a perpetuit:

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 36/55

Case *: Constant ro$t'

)1(Di$Di$ .1 g +=

Since future cash flows grow at a constant ratefore$er2 the $alue of a constant growth stock isthe present $alue of a growing perpetuit:

g r P

−= 1

.

Di$

>ssume that di$idends will grow at a constant rate2 g 2

fore$er! i.e.

-

.1- )1(Di$)1(Di$Di$ g g +=+=

.

.

*

.-* )1(Di$)1(Di$Di$ g g +=+=.

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 37/55

Case .: &ifferential ro$t'

• >ssume that di$idends will grow at different ratesin the foreseeable future and then will grow at aconstant rate thereafter!

• To $alue a Differential Mrowth Stock2 we need to: – Estimate future di$idends in the foreseeable future!

– Estimate the future stock price when the stock becomes a %onstant Mrowth Stock (case -)!

– %ompute the total present $alue of the estimatedfuture di$idends and future stock price at theappropriate discount rate!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 38/55

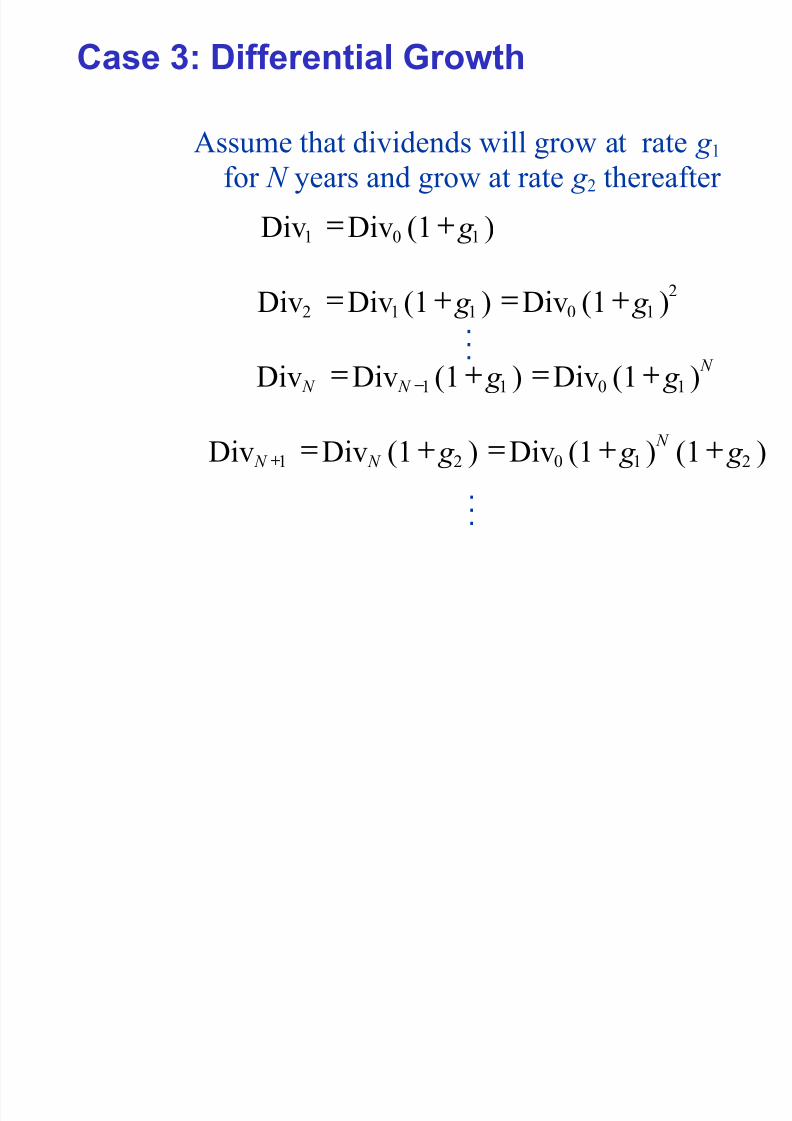

Case .: &ifferential ro$t'

)(1Di$Di$ 1.1 g +=

>ssume that di$idends will grow at rate g 1 for N ears and grow at rate g - thereafter

-

1.11- )(1Di$)(1Di$Di$ g g +=+=

N

N N g g )(1Di$)(1Di$Di$ 1.11 +=+= −

)(1)(1Di$)(1Di$Di$ -1.-1 g g g N

N N ++=+=+

.

.

.

.

.

.

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 39/55

Case .: &ifferential ro$t'

Di$idends will grow at rate g 1 for N earsand grow at rate g - thereafter

)(1Di$ 1. g + -

1. )(1Di$ g +

…0 1 2

N

g )(1Di$ 1. + )(1)(1Di$

)(1Di$

-1.

-

g g

g

N

N

++=

+

…

N N+1

…

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 40/55

Case .: &ifferential ro$t'

e can $alue this as the sum of: an N 3ear annuit growing at rate g 1

+

+−

−

=T

T

A

r

g

g r

C P

)1(

)1(1 1

1

plus the discounted $alue of a perpetuitgrowing at rate g - that starts in ear N L1

N Br

g r P

)1(

Di$-

1 C

+

−

=

+

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 41/55

Case .: &ifferential ro$t'

To $alue a Differential Mrowth Stock2 we can use

N T

T

r

g r

r

g

g r

C P

)1(

Di$

)1(

)1(1

-

1 C

1

1 +

−+

++−

−=

+

7r we can cash flow it out!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 42/55

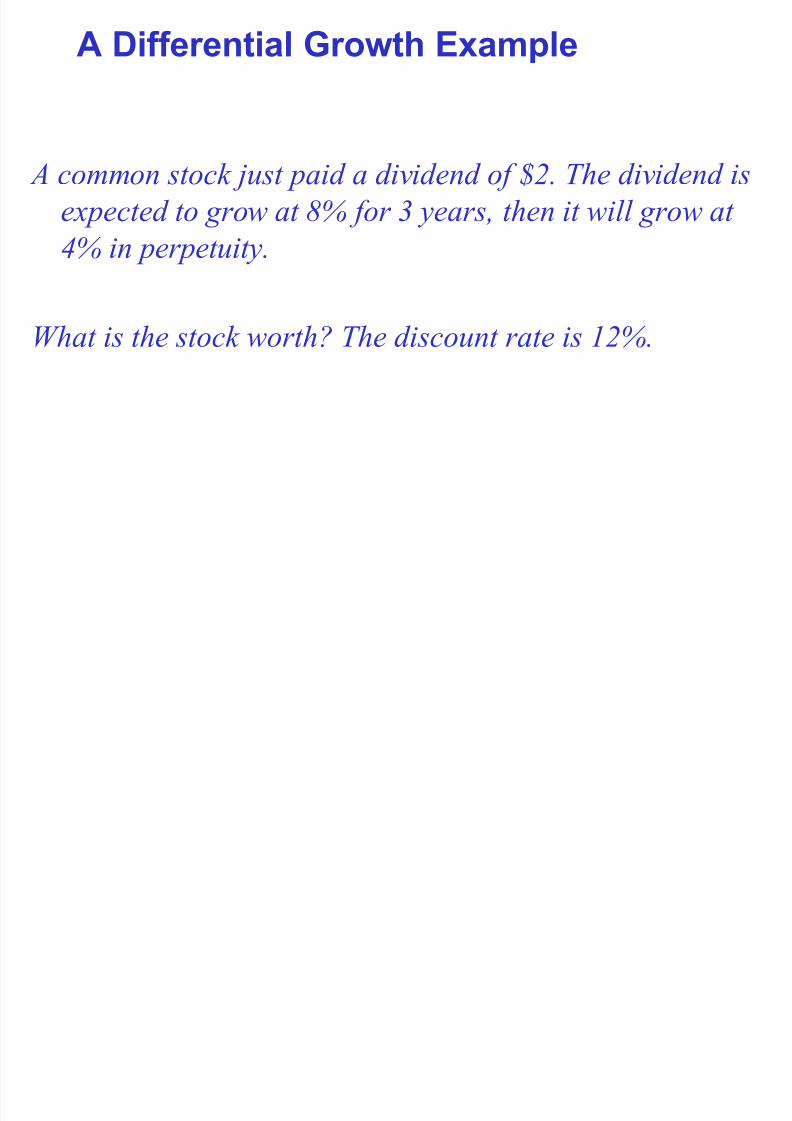

/ &ifferential ro$t' Example

A common stock just paid a dividend of $. T!e dividend is

e"pected to gro# at % for & years' t!en it #ill gro# at

(% in perpetuity.

)!at is t!e stock #ort!* T!e discount rate is +%.

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 43/55

0it' t'e 1ormula

N T

T

r

g r

r

g

g r

C P

)1(

Di$

)1(

)1(1

-

1 C

1

1 +

−

+

++

−−

=+

*

*

*

*

)1-!1(

.9!1-!).9!1().,!1(-0

)1-!1(

).,!1(1

.,!1-!

).,!1(-0

−+

−

−×= P

[ ] ( )*)1-!1(56!*-0,/!1690 +−×= P

*1!-*06,!60 += P ,/!-,0= P

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 44/55

232 Estimates of arameters in t'e

&ividend-&iscount Model

• The $alue of a firm depends upon its growth rate2

g 2 and its discount rate2 r !

– here does g come fromF

– here does r come fromF

0' d f 4

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 45/55

0'ere does g come from4

g ; Ketention ratio P Keturn on retained earnings

0'ere does r come from4

• The discount rate can be broken into two parts! – The di$idend ield

– The growth rate (in di$idends)

• Bn practice2 there is a great deal of estimationerror in$ol$ed in estimating r !

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 46/55

235 ro$t' 6pportunities

• Mrowth opportunities are opportunities to

in$est in positi$e C#N proects!

• The $alue of a firm can be conceptualized as

the sum of the $alue of a firm that pas out

1..3percent of its earnings as di$idends and

the net present $alue of the growth

opportunities!

NPV,-r

P/ P +=

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 47/55

237 T'e &ividend ro$t' Model and t'e

8V6 Model 9/dvanced

• e ha$e two was to $alue a stock:

– The di$idend discount model!

– The price of a share of stock can be calculated as thesum of its price as a cash cow plus the per3share $alue

of its growth opportunities!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 48/55

T'e &ividend ro$t' Model and t'e

8V6 Model

%onsider a firm that has E#S of 06 at the end of the first

ear2 a di$idend3paout ratio of *.?2 a discount rate of

13percent2 and a return on retained earnings of -.3

percent!• The di$idend at ear one will be 06 P !*. ; 01!6. per share!

• The retention ratio is !5. ( ; 1 3!*.) impling a growth rate in

di$idends of 19? ; !5. P -.?

8rom the di$idend growth model2 the price of a share is:

56019!1!

6.!10Di$1.

=−

=−

= g r

P

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 49/55

T'e 8V6 Model

8irst2 we must calculate the $alue of the firm as acash cow!

-6!*101!

60Di$1.

===r

P

Second2 we must calculate the $alue of thegrowth opportunities!

56!9*019!1!

,560!1!

-.!6.!*6.!*

. =−=−

×+−

= g r P

8inall2 56056!9*-6!*1. =+= P

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 50/55

23; rice Earnin%s !atio

• &an analsts freuentl relate earnings per share to price!

• The price earnings ratio is the multiple

– %alculated as current stock price di$ided b annual E#S

– T!e )all /treet 0ournal uses last 9 uarterGs earnings

P/

share per#riceratio#+E =

8irms whose shares are Iin fashionJ sell at high multiples! Mrowth

stocks for eHample!

8irms whose shares are out of fa$or sell at low multiples! Nalue

stocks for eHample!

8irms whose shares are Iin fashionJ sell at high multiples! Mrowth

stocks for eHample!

8irms whose shares are out of fa$or sell at low multiples! Nalue

stocks for eHample!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 51/55

6t'er rice !atio /nalysis

• &an analsts freuentl relate earnings pershare to $ariables other than price2 e.g.:

– #rice+%ash 8low (7%8) Katio

• cash flow ; net income L depreciation ; cash flowfrom operations or operating cash flow

– #rice+Sales• current stock price di$ided b annual sales per share

– #rice+"ook ( &arket to "ook Katio)• price di$ided b book $alue of euit2 which is

measured as assets – liabilities

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 52/55

23(+ Summary and Conclusions

Bn this chapter2 we used the time $alue of mone

formulae from pre$ious chapters to $alue bonds

and stocks!

1! The $alue of a zero3coupon bond is

-! The $alue of a perpetuit is

T

r

F PV

)1( +

=

r

C PV =

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 53/55

23(+ Summary and Conclusions (continued)

*! The $alue of a coupon bond is the sum of the#N of the annuit of coupon paments plus the

#N of the par $alue at maturit!

T T r

F

r r

C PV

)1()1(

11

++

+−=

The ield to maturit ('T&) of a bond is that single rate thatdiscounts the paments on the bond to the purchase price!

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 54/55

23(+ Summary and Conclusions (continued)

6! > stock can be $alued b discounting itsdi$idends! There are three cases:

N T

T

r

g r

r

g

g r

C P

)1(

Di$

)1(

)1(1

-

1 C

1

1 +

−

+

++−

−=

+

r P

Di$. =Oero growth in di$idends

g r P

−= 1

.

Di$%onstant growth in

di$idends

Differential growth in di$idends

8/9/2019 508 Managerial Finance Bond Nd Stock Value

http://slidepdf.com/reader/full/508-managerial-finance-bond-nd-stock-value 55/55

! The growth rate can be estimated as: g ; Ketention ratio P Keturn on retained earnings

5! >n alternati$e method of $aluing a stock was

presented2 the C#NM7 $alues a stock as thesum of its Icash cowJ $alue plus the present

$alue of growth opportunities!

NPV,-r

P/ P +=

23(+ Summary and Conclusions (continued)