7/30/2018 SafeMoney.com https://safemoney.com/blog/retirement-income-planning/6-biggest-retirement-income-planning-… 2/14 6 Biggest Retirement Income Planning Mistakes to Avoid Sure, life happens and we make mistakes. We learn and try not to repeat them. But in retirement income planning, the margin for error is smaller. Just one or a few mistakes could derail your goals or even put your retirement on the rocks. If you are someone who plans to retire within the next 10 years or sooner, now is the perfect time to start putting your nancial house in order. However, as you devote attention to daily tasks in the workplace and your household, it can be hard to make your post- work future a priority. But retirement can come sooner than you think, and it’s prudent to start preparations before your time has passed. So, meet with your nancial professional (/advice/nd-an-advisor) to discuss your goals, review the status of your retirement assets, and evaluate your nancial picture. And as you near your retirement, it’s important to refrain from critical income planning mistakes. From

6 Biggest Retirement Income PlanningMistakes to Avoid

Sure, life happens and we make mistakes. We learn and try not torepeat them. But in retirement income planning, the margin for erroris smaller. Just one or a few mistakes could derail your goals or evenput your retirement on the rocks.

If you are someone who plans to retire within the next 10 years orsooner, now is the perfect time to start putting your �nancial housein order. However, as you devote attention to daily tasks in theworkplace and your household, it can be hard to make your post-work future a priority. But retirement can come sooner than youthink, and it’s prudent to start preparations before your time haspassed.

So, meet with your �nancial professional (/advice/�nd-an-advisor) todiscuss your goals, review the status of your retirement assets, andevaluate your �nancial picture. And as you near your retirement, it’simportant to refrain from critical income planning mistakes. From

bad saving and spending habits to easy-to-overlook risks andplanning pitfalls, here are six critical retirement income planningmistakes you should avoid.

Common Retirement IncomePlanning Mistakes

1. Not having a written plan. It’s simple, but the �rst step inachieving a comfortable, income-secure retirement is having a plan.Yet many investors don’t have a retirement plan. According to theEmployee Bene�t Research Institute, 59% of Americans haven’tcalculated how much retirement money they should have saved(https://www.ebri.org/pdf/surveys/rcs/2017/IB.431.Mar17.RCS17..21Mar1

Just as importantly, few people put a plan in writing. Again, theEmployee Bene�t Research Institute reports, just 11% of workingAmericans have created a written �nancial plan. Retired Americansdon’t fare much better— only 2 out of 10 (19%) have a writtenblueprint for their golden years.

Point is, having a written plan can be a real game-changer. Accordingto the Wells Fargo/Gallup Investor and Retirement Optimism Indexfrom earlier this year, investors with written retirement plans werealmost 200% more likely than those with none to believe they wouldhave enough money for retirement.

Likewise, in an April 2017 study by Koski Research for CharlesSchwab, those with a written plan were 60% more likely to make401(k) contributions and 200% more likely to stick with monthlysaving goals.

2. Potentially retiring too early. While it may be an exercise inpatience, working for even a few years longer can do wonders foryour income security. You bring home more money to work with, andif you’re behind in savings, you can put away those balances for yourretirement future. A delayed workplace departure also means moretime for your savings to grow tax-deferred.

Each year you work is another year you don’t have to take moneyfrom your retirement accounts, and subsequently your retirementincome rises. Even more importantly, if you are in your sixties,working longer boosts your Social Security bene�ts. By working anddelaying your bene�ts claiming until full retirement age, you willaccrue more credits and sidestep costly bene�t deductions that kickin with early �ling.

With that said, Social Security claiming depends on a number offactors. You may have a family history or medical history in which youexpect to have a shorter retirement duration. In that case, earlyclaiming may make sense. Or maybe you worry about getting what's

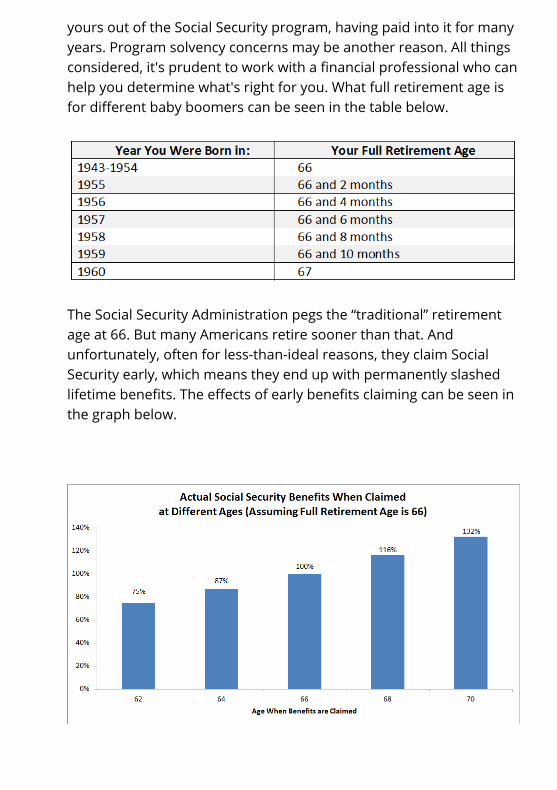

yours out of the Social Security program, having paid into it for manyyears. Program solvency concerns may be another reason. All thingsconsidered, it's prudent to work with a �nancial professional who canhelp you determine what's right for you. What full retirement age isfor di�erent baby boomers can be seen in the table below.

The Social Security Administration pegs the “traditional” retirementage at 66. But many Americans retire sooner than that. Andunfortunately, often for less-than-ideal reasons, they claim SocialSecurity early, which means they end up with permanently slashedlifetime bene�ts. The e�ects of early bene�ts claiming can be seen inthe graph below.

According to the Center for Retirement Research at Boston College,more Americans start collecting bene�ts at age 62 than any otherage. And in 2015, among Americans who actually chose their claimingage – as opposed to transitioning into Social Security bene�ts fromdisability bene�ts at full retirement age – 64% of men and 72% ofwomen took their bene�ts earlier(https://www.fool.com/retirement/2017/05/07/when-do-most-americans-claim-social-security.aspx) than their full retirement age.

If you do plan to keep working and claim your bene�ts early, beaware of the downsides. The Social Security Administration limitsbene�t payments when you are taking home work income before fullretirement age. In 2018, when you claim your bene�ts early, the SSAdeducts $1.00 of bene�ts for every $2.00 of earnings over $17,040.This applies when claiming bene�ts early before the year in whichsomeone attains full retirement age.

If you claim bene�ts in the year of your full retirement age -- but notthe precise month when your full retirement age actually kicks in --$1.00 of bene�ts is taken from every $3.00 of earnings above$45,360. Note this second deduction applies in the months of theyear of your full retirement age.

3. Not having a “retirement-ready” diversi�cation strategy. Sure,deciding on an investment strategy and putting away money intoretirement accounts takes work. Years of discipline and hard work!But while accumulating assets and building up savings requiresdiligence, it’s often taking money out of those retirement accounts –and minimizing taxes – that is trickier.

Retirement is di�erent than the working years, because you will nolonger have a job salary or wage earnings. Now, it’s a matter ofdrawing on accumulated assets for income. And while withdrawalguidelines such as “the 4% rule” may be helpful, the economicassumptions undergirding them are likely to change. So, it’simportant to consider the following points:

Do you have safeguards in place so you have steady, reliableincome streams, even in poor market conditions?Does your portfolio have suitable asset protections so yourmoney lasts for potentially 30 years or longer – especially as lifeexpectancies increase?How exposed is your portfolio to market volatility?Generally speaking, is the amount of risk your portfolio carriesappropriate for your age, circumstances, and �nancial picture?

It’s prudent to work with a knowledgeable �nancial professional(/advice/�nd-an-advisor) – someone who understands theimportance of income, protection, and risk management inretirement – to help you answer these important questions.

4. Planning only for joint income needs. If you are married or havea partner, chances are your retirement income plan is based on twopeople. Your plan may account for your needs together, and mayinclude joint lifetime Social Security payments, pooled investmentfunds, cumulative portfolio assets, and your total savings. But whatabout the question of survivorship? What would happen when one ofyou is gone?

When one member of a couple passes away, a number of thingschange. Social Security income diminishes, other income sourcesmay dwindle, and there may be tax implications with the deceasedparty’s assets, if they weren’t speci�ed as jointly-owned property.

If you do have retirement accounts earmarked for the survivor, youwill want to prepare now. Make sure the bene�ciaries on thoseaccounts are updated, so there's an e�cient wealth transfer. It'simportant to assure that you and/or your partner will have access tothat money when one of you is gone.

So, you will want to be sure that no matter what, the survivingpartner is well-prepared. They may also be left to deal with healthproblems or other costly issues tied to aging. Your retirement incomeplan should account for those situations, as well – especially if one of

you is no longer around to help your signi�cant other. From a�nancial protection standpoint, joint life insurance of the "�rst-to-die"variety may be worth consideration. This type of life policy givesinstant liquidity to the surving partner once someone deceases, ithelps them bypass costly probate, and it gives the surviving partnerwith a tax-advantaged income source.

5. Neglecting costly health and care needs. Many people thinkthey won’t have any long-term care needs. But the numbers maysurprise you. According to the U.S. Department of Health and HumanServices, someone turning 65 today has a 70% chance of needinglong-term care in the future. And for that matter, other health costs,not to mention all-around costs of care services, can add up quickly.

Along with dumping pensions, employers are steadily taking healthcoverage in retirement o� the table. Medicare may not pay for asmany of the health costs that you think it does. For example, someexpenditures not covered by Medicare(https://www.medicare.gov/what-medicare-covers/not-covered/item-and-services-not-covered-by-part-a-and-b.html) include:

Long-term careMajority of dental careDenturesHearing aids and examinations for �tting themEye examinations related to eyewear prescriptions

Now, to give an idea of retirement health costs in real-world �gures.The �nancial research �rm HealthView Services projects(http://www.hvs�nancial.com/2017-retirement-health-care-costs-data-report/) for total health costs:

Total healthcare premiums, or Medicare Parts B and D,supplemental insurance, and dental insurance, for a healthy 65-year-old couple retiring in 2017 are projected to be $321,994.When accounting for the value of future dollars, the �gureshoots up to $485,246!

Factoring in deductibles, co-payments, and out-of-pocket costs,total retirement healthcare costs are projected to be $404,253for a 2017-retiring, 65-year-old couple. When accounting forfuture dollars, the �gure goes up to $607,662.

As for costs of long-term care: If someone requires care in a nursinghome, the average cost is around $4,000-$6,000 per month. Or$48,000-$72,000 annually! Or say someone needs care from a homehealth aide or nurse – that can cost $100 per day, or as much as$3,000 per month.

There may be solutions to these needs, besides having to liquidate allof your assets to cover the costs of care services. Consult with aknowledgeable �nancial professional (/advice/�nd-an-advisor) whocan help you anticipate and prepare for these risks.

6. Not planning for a potentially long retirement. Lifeexpectancies are on the rise. Thanks to medical and technologyinnovations, people are living longer. And in turn, this increasinglongevity acts as a “risk multiplier,” enhancing the e�ects thatin�ation, taxes, market corrections, and other risks may have overthe years.

If people are married, they live longer. A married couple’s lifeexpectancy is age 93. Research projections estimate a 25% chance forone partner to live to age 97. As we continue to see more innovationson the medical and technology fronts, people may live even longer!

So, your retirement income plan should account for a potentially longretirement lifespan. That can be as many as 30 years or possibly evenlonger. You should have annual projections of your expected monthlycosts-of-living, miscellaneous spending, and how you’ll pay for them.Overall, the goal is to make sure your money lasts as you need it – soyou can enjoy a comfortable and �nancially con�dent retirementlifestyle.

Ready for Personal Guidance withYour Income Plan?If you are ready for guidance on creating a plan that emphasizes income certainty, protection, and risk management – or you need a second opinion of your existing strategy – a financial professional can help you.

SafeMoney.com financial professionals have been featured by Fox Business, CNBC, PBS, MarketWatch, ProtectWealth.com, and many other outlets. Many people have been giving great feedback on the three booklets offered on the homepage of SafeMoney.com.

Please feel free to visit and download whatever booklet may be of interest to you. There is never any cost to you. you.