f à c n s m l l l n à t k P à i d k à 0 à u l l k l k w X u à y j m j A à b k m j q à W n 6 à h 6 à a Y B i à B r r 6 à w g 8 n V m k o 8 e v à j à à @ r r à h q à D r t h r q à S v x à H h h t r r 6 à a 8 à r 8 à a e j l k 6 à t k à r m d l k 6 à W m m k l à B @ @ @ 8 26 April 2000 Extreme value theory - an empirical analysis of equity risk Abstract This paper is a case study in the use of extreme value theory (EVT) to estimate tail risks in financial markets. Its main argument is that EVT is a practical tool that allows riskmanagers to estimate tail risk. To illustrate this point, an EVT model is applied to a large sample of equity indices. Throughout, the emphasis is on the application of an EVT model, rather than its theoretical properties, and graphical tools are used to visualise results. Introduction Investment banks are exposed to risk from movements in prices of many instruments and across many markets. In this multivariate world, risk managers often focus attention on portfolio tail risk. Different measures of tail risk are essential to ‘slice and dice’ exposures from different viewpoints. Current best practice for assessing tail risk includes techniques such as value-at-riskand scenario analysis. This case study offers one example highlighting why extreme value theory (EVT) might become part of the risk manager’s toolkit in the future. The application of EVT discussed in this paper concerns equity risk, but it could apply equally to other markets. Equity risk is often partitioned into market and stock specific risk, where market risk is measured using an appropriate index. Large movements in indices may expose a portfolio to risk so our objective is to estimate the magnitude of such moves in a robust but consistent manner. The layout of the rest of this paper is as follows: first we investigate and comment on the data, next the data is summarised non-parametrically before fitting a EVT model, the results are then summarised in various ways, before finishing with some final comments. Exploratory data analysis The first task in any empirical analysis is to explore the data. EVT is very data hungry because the most informative events are historic crises and these are rare events by their very nature. It is critically important that the data used to estimate extreme events contain some information about extreme events. EVT will do no more than extract such information in an efficient and consistent manner. For example, Figure 1 shows a history of 10-day returns for four equity indices. Five years ofrecent history would highlight one big move in the Hang-Seng (IXH). Going back a further ten years highlights two other moves that exceeded 30% over 10-days. Does the switch from ‘one big move in five years’ to ‘three big moves in fifteen years’ give us extra information about the likelihood and magnitude of future big moves on the Hang-Seng? The situation is more extreme for the S&P500 (SPX) and the FTSE100 (FTSE), where the Oct 87 crash is out of all proportion to the big moves seen since then. The decision on how much historic data to use is likely to depend on how the results are to be used and there may be variation between different markets, levels in the organisation and motivation e.g. foreign exchange verses equity, chief risk officer verses trading desk, internal verses external. In practice, sensitivity to the length of the time period should be considered by

s m � l � l � l � n � à t � k � P à i � � d k à 0 à u l � l � k l � � k

w X u à y � j � m j �

A à b � k � m j q à W n � 6 à h � 6 à a Y B i à B r r 6 à w g

� � 8 � � n � V m � k o 8 � e

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

26 April 2000

Extreme value theory - an empirical analysis of equity risk

Abstract

This paper is a case study in the use of extreme value theory (EVT) to estimate tail risks

in financial markets. Its main argument is that EVT is a practical tool that allows risk

managers to estimate tail risk. To illustrate this point, an EVT model is applied to a

large sample of equity indices. Throughout, the emphasis is on the application of an

EVT model, rather than its theoretical properties, and graphical tools are used to

visualise results.

Introduction

Investment banks are exposed to risk from movements in prices of many instruments and across

many markets. In this multivariate world, risk managers often focus attention on portfolio tail

risk. Different measures of tail risk are essential to ‘slice and dice’ exposures from different

viewpoints. Current best practice for assessing tail risk includes techniques such as value-at-risk

and scenario analysis. This case study offers one example highlighting why extreme value theory

(EVT) might become part of the risk manager’s toolkit in the future.

The application of EVT discussed in this paper concerns equity risk, but it could apply equally to

other markets. Equity risk is often partitioned into market and stock specific risk, where market

risk is measured using an appropriate index. Large movements in indices may expose a portfolio

to risk so our objective is to estimate the magnitude of such moves in a robust but consistent

manner.

The layout of the rest of this paper is as follows: first we investigate and comment on the data,

next the data is summarised non-parametrically before fitting a EVT model, the results are then

summarised in various ways, before finishing with some final comments.

Exploratory data analysis

The first task in any empirical analysis is to explore the data. EVT is very data hungry because

the most informative events are historic crises and these are rare events by their very nature. It is

critically important that the data used to estimate extreme events contain some information about

extreme events. EVT will do no more than extract such information in an efficient and consistent

manner.For example, Figure 1 shows a history of 10-day returns for four equity indices. Five years of

recent history would highlight one big move in the Hang-Seng (IXH). Going back a further ten

years highlights two other moves that exceeded 30% over 10-days. Does the switch from ‘one

big move in five years’ to ‘three big moves in fifteen years’ give us extra information about the

likelihood and magnitude of future big moves on the Hang-Seng? The situation is more extreme

for the S&P500 (SPX) and the FTSE100 (FTSE), where the Oct 87 crash is out of all proportion

to the big moves seen since then.

The decision on how much historic data to use is likely to depend on how the results are to be

used and there may be variation between different markets, levels in the organisation and

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã B Ã � Ã I

comparing the analysis for different time windows, such as 5 years verses 10 years of data, and

by comparing results with and without a period when a crash occurred such as October 1987 for

equities.

Common arguments for using as much historic data as possible include: ‘rare events require a

long history in order to see several such events’, ‘the longer the historical period the more

extreme the worst observed movements’ and ‘we don’t want to throw away information’.

Counter arguments to going far back in history include: ‘markets are different now compared to

the distant past’, ‘we should use the same historic period as used within the VaR model for

consistency’ and ‘we should use the same historic period for all the time series in our analysis(the range of the shortest time series)’. A more detailed discussion of this point is beyond the

scope of this paper. As our objective is to illustrate EVT, we use up to fifteen years of data

where available (November 1984 to August 1999).

To decide if a data source is reliable, it is worthwhile spot checking the biggest moves with

alternative sources. Discrepancies often occur and should be resolved. Sometimes it is due to

unavoidable anomalies, such as the data being recorded in different time zones but such

differences are magnified when markets crash. For example, if a market closed early because of

the crash then its closing price may not match the closing price in other markets, which remained

open, or perhaps which closed earlier in the day before the crash occurred. Results may be

sensitive to these issues so care is required.

-40

-20

0

20SGD.IXP

1985 1990 1995 2000

HKD.IXH

GBP.FTSE

-40

-20

0

20USD.SPX

1985 1990 1995 2000

Time (years)

R e t u r n o v e r t h e h o l d i n g p e r i o d ( % )

28 Oct 97 -42%27 Oct 87 -47%

6 Jun 89 -36%

27 Oct 87 -30%27 Oct 87 -31%

27 Oct 87 -52%

Figure 1 Time series plots of non-overlapping 10-day equity index returns. Two industrialised indices,FTSE100 (FTSE) and S&P500 (SPX), and two emerging market indices, Singapore (IXP) and Hang Seng

IXH) are shown. The worst observed moves were in October 1987.

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã C Ã � Ã I

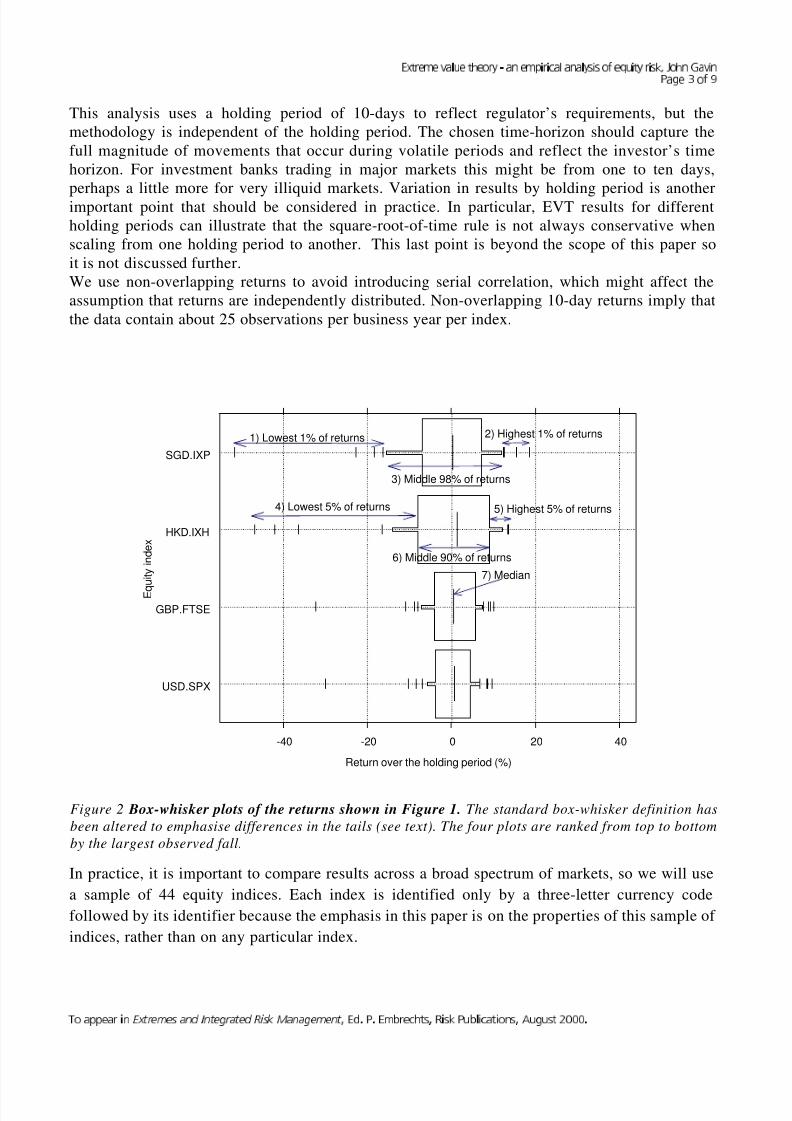

This analysis uses a holding period of 10-days to reflect regulator’s requirements, but the

methodology is independent of the holding period. The chosen time-horizon should capture the

full magnitude of movements that occur during volatile periods and reflect the investor’s time

horizon. For investment banks trading in major markets this might be from one to ten days,

perhaps a little more for very illiquid markets. Variation in results by holding period is anotherimportant point that should be considered in practice. In particular, EVT results for different

holding periods can illustrate that the square-root-of-time rule is not always conservative when

scaling from one holding period to another. This last point is beyond the scope of this paper so

it is not discussed further.

We use non-overlapping returns to avoid introducing serial correlation, which might affect the

assumption that returns are independently distributed. Non-overlapping 10-day returns imply that

the data contain about 25 observations per business year per index.

In practice, it is important to compare results across a broad spectrum of markets, so we will use

a sample of 44 equity indices. Each index is identified only by a three-letter currency code

followed by its identifier because the emphasis in this paper is on the properties of this sample of

indices, rather than on any particular index.

USD.SPX

GBP.FTSE

HKD.IXH

SGD.IXP

-40 -20 0 20 40

Return over the holding period (%)

E q

u i t y

i n d e x

4) Lowest 5% of returns

1) Lowest 1% of returns

3) Middle 98% of returns

2) Highest 1% of returns

5) Highest 5% of returns

6) Middle 90% of returns

7) Median

Figure 2 Box-whisker plots of the returns shown in Figure 1. The standard box-whisker definition has

been altered to emphasise differences in the tails (see text). The four plots are ranked from top to bottom

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã D Ã � Ã I

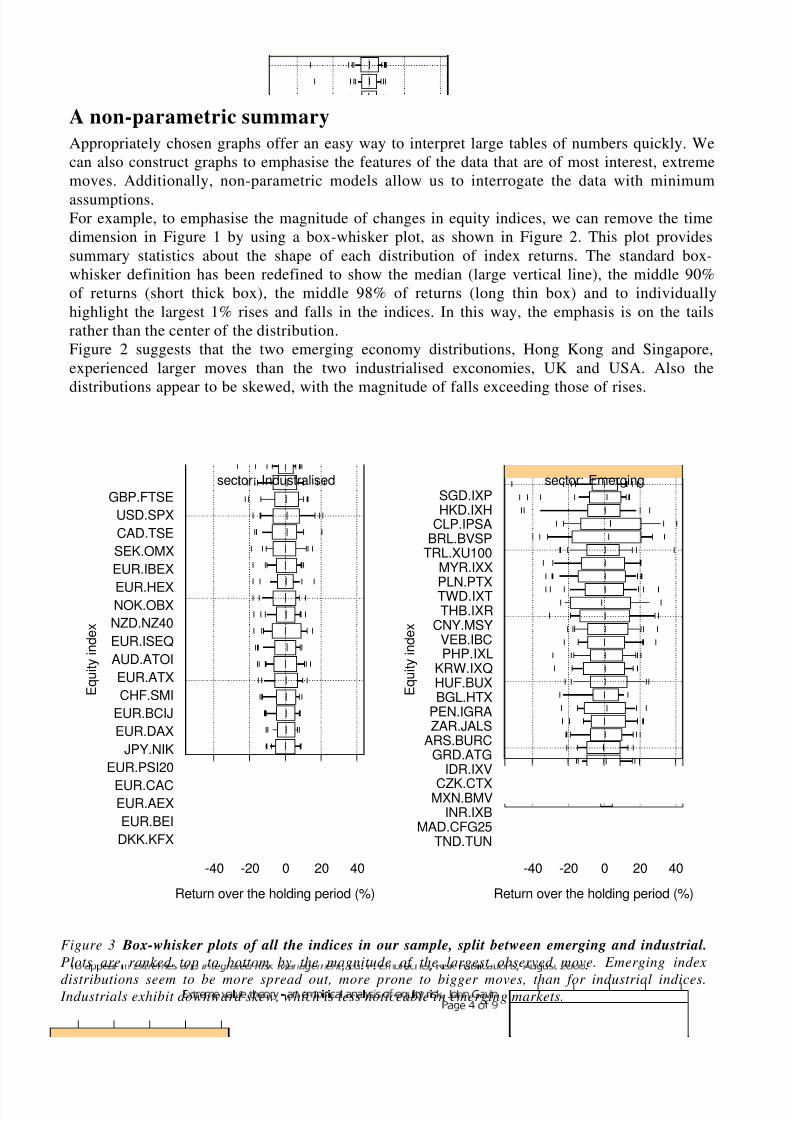

A non-parametric summary

Appropriately chosen graphs offer an easy way to interpret large tables of numbers quickly. We

can also construct graphs to emphasise the features of the data that are of most interest, extreme

moves. Additionally, non-parametric models allow us to interrogate the data with minimum

assumptions.For example, to emphasise the magnitude of changes in equity indices, we can remove the time

dimension in Figure 1 by using a box-whisker plot, as shown in Figure 2. This plot provides

summary statistics about the shape of each distribution of index returns. The standard box-

whisker definition has been redefined to show the median (large vertical line), the middle 90%

of returns (short thick box), the middle 98% of returns (long thin box) and to individually

highlight the largest 1% rises and falls in the indices. In this way, the emphasis is on the tails

rather than the center of the distribution.

Figure 2 suggests that the two emerging economy distributions, Hong Kong and Singapore,

experienced larger moves than the two industrialised exconomies, UK and USA. Also the

distributions appear to be skewed, with the magnitude of falls exceeding those of rises.

Figure 3 Box-whisker plots of all the indices in our sample, split between emerging and industrial.

Plots are ranked top to bottom by the magnitude of the largest observed move. Emerging index

distributions seem to be more spread out, more prone to bigger moves, than for industrial indices. Industrials exhibit downward skew, which is less noticeable in emerging markets.

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã E Ã � Ã I

Figure 3 extends this approach to all of the indices in our sample but categorises the

distributions into industrial and emerging, of which there are about twenty each. Of the

industrials, the S&P and FTSE have produced the biggest moves, due to the October 1987 crash.

Singapore has produced the biggest fall among the emerging indices, followed by Hong Kong.

Belgium (BEI) and Denmark (KFX) produced the least extreme falls among the industrials. Thehistory of the time series for Madagaskar (CFG25) and Tunesian (TUN) was short relative to

other indices. Across both categories the top-ten biggest falls were in emerging indices, the

exception being the FTSE, and seventeen of the bottom twenty were industrial (not shown). So

these results, and further exploratory data anlaysis,are hinting that there might be a difference

between the fat-tailedness of the distributions between industrial and emerging indices. It also

suggests a downward skew (to the left) so we might want to distinguish between extreme

positive and negative distributions.

An EVT model

Following Embrechts, Resnick and Samorodnitsky1, we use a generalised Pareto distribution

(GPD), )(,

xG β ξ

, to approximate the distribution of large log-returns from an equity index,

++++++++++++

++++++++++

+

+

-------------

-

-

10^-3

10^-2

10^-1

USD.SPX

0 10 20 30 40 50

++++++++++++++++++

+

+

---------------

-

-

SGD.IXP

0 10 20 30 40 50

Return over holding period (%)

C u m u l a t i v e p r o b a b i l i t y

+ -Positive move - data & fit Negative move - data & fit

Figure 4 POT model fitted separately to the positive and negative returns on the S&P500 (SPX)

and Singapore (IXP) indices. The plus (+) and minus (-) signs are the largest 10% of the positive

and negative 10-day returns, respectively. Negative moves are generally fatter tailed than positive

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã F Ã � Ã I

)( xF u

, for moves in excess of some threshold, u. The GPD is a two-parameter distribution

function

=−−

≠+−−

0), / exp(1

0,) / 1(1)(

/ 1

, ξ β

ξ β ξ ξ

β ξ x

x xG where β and ξ are called the scale and shape

parameters, respectively. This model ignores data in the centre of the distribution on theassumption that small (frequent) moves in an index do not contain any information about the

magnitude nor likelihood of large (infrequent) moves. It is sometimes called the peaks over

threshold (POT) model. The two panels in Figure 4 show the empirical and fitted cumulative

probabilities, from the POT model, for two indices in our sample. Positive and (the absolute

value of) negative moves are analysed separately with the threshold set at the 90% confidence

level (90% quantile). The x-axis measures the size of the move over 10-days and the y-axis

shows the (log-10 scale) cumulative probability, starting at the threshold. This value is equal to

one minus the confidence level, so2

10−

= y corresponds to the 99% confidence level. Observed

positive and negative moves are shown as plus (+) and minus (-), respectively. For example, the

second worst falls for the S&P and Singapore were about –10% and –22% respectively, and both

events have empirical probabilities of about2

10−

= y (99% confidence level). On to each set of

observed data a GPD distribution has been superimposed using maximum likelihood to estimate

the parameters. The threshold choice is subjective but values around this level were found to

produce satisfactory results. More generally, it is necessary to test our sensitivity to this

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã G Ã � Ã I

From the graph, we can see that our estimates of (the absolute value of) negative and positive

moves are 11% and 8% for the S&P, and 23% and 15% for Singapore, at the 99% confidence

level. These are the x-values at which the horizontal line2

10−

= y crosses the fitted distributions.

For Singapore, the fit suggests that there is a difference between the magnitude of large positiveversus negative moves, for a fixed confidence level. For the S&P, there is little to distinguish the

magnitude of positive moves from negative moves, for absolute moves in the interval 4.5% to

+6%. Beyond that, negative moves are larger for any chosen confidence level and the difference

increases for points further out in the tail. In other examples (not shown), it is possible for the

positive and negative fits to have a crossover point, making it worthwhile to consider all points

along the tail rather than just a single point.

Notice that the distribution for positive moves on the S&P seems to have an upper bound, so our

99% estimate of an 8% rise in the index is not that different from our 99.9% estimate of a 10%

rise, approximately. This suggests that there is an upper limit to how much this index can rise

over 10-days, even in a strong bull market.

A natural question to consider is whether we could consider the positive and negative estimate

for the S&P to be about the same. It is possible to place pointwise confidence intervals around

each estimated point (Embrechts, Resnick and Samorodnitsky1, McNeil

2) but a more pertinent

question is whether this difference is materially significant from a business perspective. For this

reason we choose to look at a sample from the population of equity indices and focus on the

variation across the sample rather than the variation for a single index.

By repeating this analysis for each index, we can produce an EVT estimate for each index.

Figure 5 summarises the results for the 99% confidence level. These estimates of 10-day moves

vary from around from 5% to 35%. Industrial indices tend to produce smaller moves than

emerging market indices and a second order effect appears to be that negative moves tend to

exceed positive moves, as our earlier non-parametric analysis suggested.

Estimating risk along the tail

This penultimate section addresses two questions: For a fixed confidence level, is there a concise

way to summarise the results for our sample of equity indices? Secondly, how might the results

change if we repeat the analysis for different confidence levels?

We use a decision tree to draw general conclusions about the magnitude of large moves in equity

indices. Our goal with this model is to produce an economic description of our EVT estimates

for a fixed confidence level, by adding background information. This information is an attempt

to encapsulate expert knowledge about factors that might influence the behaviour of equity

indices under stress conditions, such as distinguishing between positive and negative moves, thematurity of the underlying economy (industrialised or emerging) or the credit rating of the

associated country. We extend this approach by building a decision tree at different confidence

levels, then we consider differences between these trees.

A decision tree is a transparent tool for summarising data using a simple set of rules. The tree is

a sequence of binary rules, each associated with some decision. First, a variable is selected, then

the population is divided into two at a selected breakpoint of that variable. Each split is then

independently subdivided further on the same principle, recursively forming a binary tree

structure. Tree models are easy to interpret and they emphasise the more important variables.

However, solutions are not unique and the technique is still being developed. Breiman,

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã H Ã � Ã I

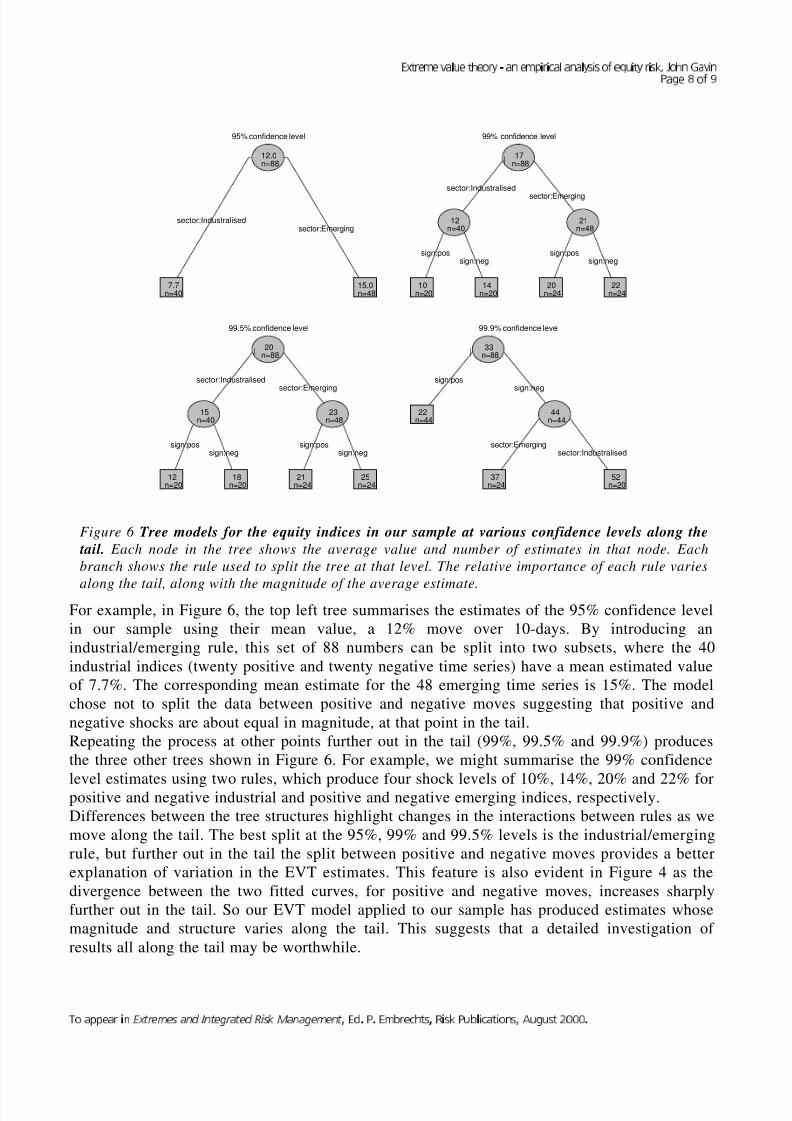

For example, in Figure 6, the top left tree summarises the estimates of the 95% confidence level

in our sample using their mean value, a 12% move over 10-days. By introducing an

industrial/emerging rule, this set of 88 numbers can be split into two subsets, where the 40

industrial indices (twenty positive and twenty negative time series) have a mean estimated value

of 7.7%. The corresponding mean estimate for the 48 emerging time series is 15%. The model

chose not to split the data between positive and negative moves suggesting that positive and

negative shocks are about equal in magnitude, at that point in the tail.

Repeating the process at other points further out in the tail (99%, 99.5% and 99.9%) produces

the three other trees shown in Figure 6. For example, we might summarise the 99% confidence

level estimates using two rules, which produce four shock levels of 10%, 14%, 20% and 22% forpositive and negative industrial and positive and negative emerging indices, respectively.

Differences between the tree structures highlight changes in the interactions between rules as we

move along the tail. The best split at the 95%, 99% and 99.5% levels is the industrial/emerging

rule, but further out in the tail the split between positive and negative moves provides a better

explanation of variation in the EVT estimates. This feature is also evident in Figure 4 as the

divergence between the two fitted curves, for positive and negative moves, increases sharply

further out in the tail. So our EVT model applied to our sample has produced estimates whose

magnitude and structure varies along the tail. This suggests that a detailed investigation of

results all along the tail may be worthwhile.

|

sector:Industralisedsector:Emerging

12.0n=88

7.7n=40

15.0n=48

95% confidence level

|

sector:Industralised

sign:pos sign:pos

sector:Emerging

sign:neg sign:neg

17n=88

12n=40

10n=20

14n=20

21n=48

20n=24

22n=24

99% confidence level

|

sector:Industralised

sign:pos sign:pos

sector:Emerging

sign:neg sign:neg

20n=88

15n=40

12n=20

18n=20

23n=48

21n=24

25n=24

99.5% confidence level

|

sign:pos

sector:Emerging

sign:neg

sector:Industralised

33n=88

22n=44

44n=44

37n=24

52n=20

99.9% confidence level

Figure 6 Tree models for the equity indices in our sample at various confidence levels along the

tail. Each node in the tree shows the average value and number of estimates in that node. Each

branch shows the rule used to split the tree at that level. The relative importance of each rule varies

along the tail, along with the magnitude of the average estimate.

v à � � � j à � à @ � � � r � r � à h � q à D � � r t � h � r q à S v � x à H h � h t r � r � � 6 à a � 8 à r 8 à a e � j � � � l k 6 à t � k � à r m � d � � � l � k 6 à W m � m k l à B @ @ @ 8

a p l j � e � à n � d m � à l � � j q à 7 à � à � e � j � � � d à � � d q k � k à � à � m � l q à j � k � 6 à f � à c � n �

r � � � Ã I Ã � Ã I

Final remarks

This case study discussed some of the practical issues that arise from using EVT to measure tail

risk in finance. Our overall conclusion is that EVT is a complementary tool to existing

techniques, such as VaR and stress testing. It should become a standard part of the risk

manager’s toolkit to demonstrate to traders and to regulators a consistent, robust methodologyfor stressing individual risk factors. In particular, it implies our understanding of risk is not

measured solely in terms of volatility.

Some EVT issues were only briefly mentioned and require more detailed consideration in

practice including: the choice of threshold u, the best fitting procedure to estimate the shape and

scale parameters, the extra benefit of producing pointwise confidence intervals for our estimates

and variation between samples from different data sources. We did not discuss other potentially

useful EVT estimates such as excess of loss, the expected loss given that the loss exceed some

point in the tail.

How different estimates relate to the real world is an important practical topic. For example, an

estimate at the 99.9% confidence level is likely to produce a number that few traders can relateto in they day-to-day experience of managing a market sensitive portfolio. So points that far out

in the tail may not have much practical value from a trader’s perspective.

The regression tree offers one way of adding expert knowledge to the solution by introducing

rules for partitioning the data into homogenous groups. This model might also be used to make

predictions for indices not in our sample. However, it is worth reiterating that each point is an

estimate derived from our EVT model, so each point is itself subject to measurement error.

We finish by acknowledging that this short case study ignores many important equity risks for

simplicity, especially specific, volatility and spread risk. It should be viewed as only a starting

point for equity portfolio risk analysis.

AcknowledgementsThis paper was written mainly because of the encouragement of Paul Embrecths and Alexander

McNeil. It has benefited from many conversations with colleagues, especially Helmut Glemser,

but all errors are mine alone. Analysis was carried out in SPlus4

using mainly McNeil’s EVIS5

library for the EVT results, but also Thearneau’s recursive partitioning (rpart 6 ) for the tree

model and Harrell’s hmisc6

libraries for some of the graphs. The data are taken from a

proprietary UBS database.

References

1. P. Embrechts, S. Resnick and G. Samorodnitsky, Living on the edge, Risk, January 1998, 96-

100.2. A. McNeil, History repeating, Risk, January 1998, 99.

3. L. Breiman, J. H. Friedman, R. A. Olshen, and C. J. Stone, 1984, Classification and

regression trees, Belmont, MA: Wadsworth.

4. SPlus, www.mathsoft.com /splus

5. Extreme Values in SPlus (EVIS), A. McNeil, www.math.ethz.ch/~mcneil/software.html

6. Hmisc library of SPlus routines, F. Harrell, hesweb1.med.virginia.edu/biostat/s/Hmisc.html

7. J. Atkinson and T. Therneau, An introduction to recursive partitioning using the rpart

routine, Technical report 61, Mayo Clinic, Section of Statistics, 1997 (ported to Windows by