38

Management Accounting: Marginal Costing & Cost Volume Profit Analysis

| Date post: | 07-Apr-2018 |

| Category: |

Documents |

| Upload: | jyoti-meghani |

| View: | 220 times |

| Download: | 0 times |

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 1/38

Management Accounting:

Marginal Costing & Cost Volume

Profit Analysis

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 2/38

Meaning of Management

Accounting According to Anglo-American Council of

Productivity -:

³ It is the presentation of accountinginformation in such a way as to assistmanagement in the creation of policy and

the day to day operation of theundertaking.´

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 3/38

Management Accounting and

Financial AccountingFinancial Accounting

� Objective

To maintain account to

determine financial

position of business

� NatureIt deals with historical

data.

Management Accounting

� Objective

To help management to

formulate policies and

plan

� NatureIt deals with projection of

data for the future.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 4/38

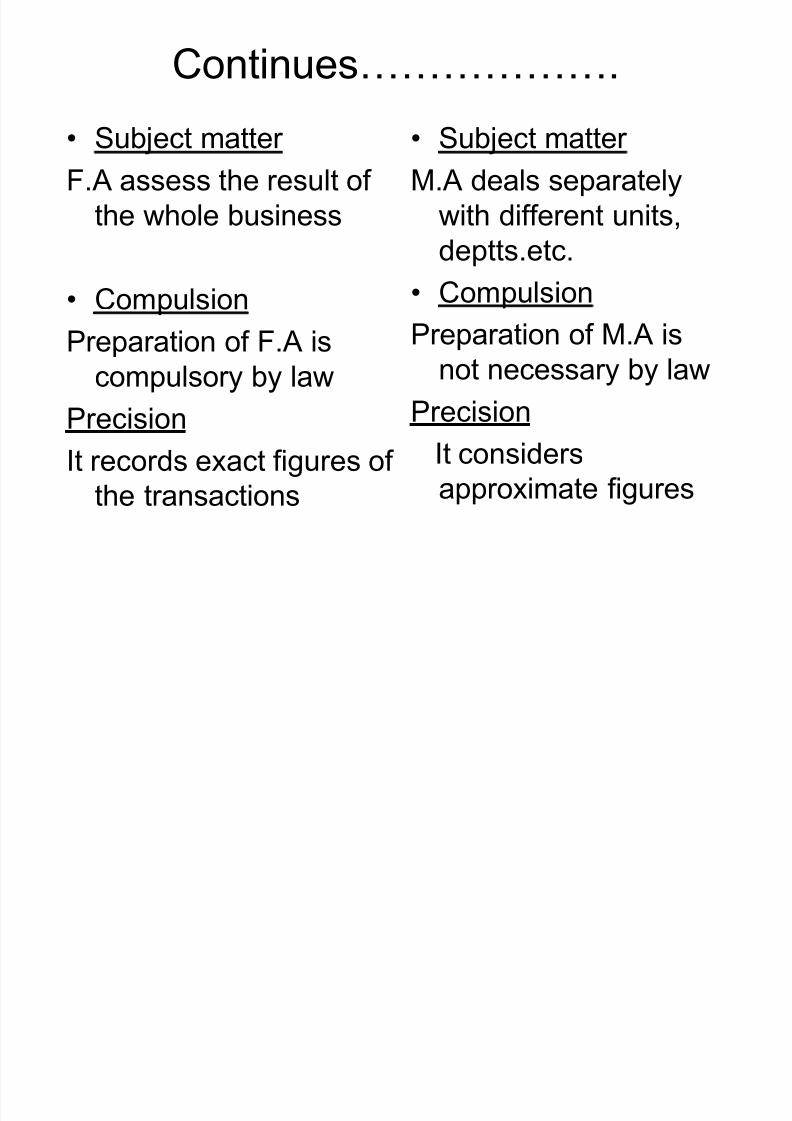

Continues««««««.

� Subject matter F.A assess the result of

the whole business

� Compulsion

Preparation of F.A is

compulsory by law

Precision

It records exact figures of

the transactions

� Subject matter M.A deals separately

with different units,

deptts.etc.

� Compulsion

Preparation of M.A is

not necessary by law

PrecisionIt considers

approximate figures

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 5/38

Cost Accounting and Management

Accounting� Cost Accounting

1. It records the

quantitative aspect of

a transaction2. Records the cost of

producing a product

and providing service

3. It only deals with cost

ascertainment

� Management Accounting

1. it records both qualitative

and quantitative aspect of

a transaction2. Provides information to

management for planning

and co-ordination

3. It is wider in scope as it

includes F.A, budgeting,

Tax, Planning.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 6/38

Continue««««««..

� Cost Accounting4. It uses both past and

present figures

5. It¶s development is

related to industrial

revolution

6. It follows certainprinciples and

procedures for

recording costs of

different products

� Management Accounting4. It is concerned with the

projection of figures for

future.

5. It develops inaccordance to the

modern business world

6. It does not follow any

specific rules and

regulations.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 7/38

MARGINAL COSTING

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 8/38

Marginal Cost

� According CIMA, London, Marginal Cost represents ³theamount of any volume of given output by which aggregatecost are changed if the volume of output is increased byone units.

� In practice, it is measured by the total variable costsattributable to one unit.

� For example, the cost of production of 1,000 units of

radios is Rs. 200000 and that of 1001 units is Rs. 200150the marginal cost is Rs. 150, i.e., 200150 ± 200000.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 9/38

Marginal Costing

� The Institute of Cost and Management,

London, has defined Marginal costing as

³the ascertainment of marginal costs and

of the effects on profit of changes in

volume or type of output by differentiating

between fixed costs and variable costs´.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 10/38

Marginal Costing

� ³In this technique of costing only variable

costs are charged to operational process

or products, leaving all indirect cost to be

written off against profit in the period in

which they arise´.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 11/38

Marginal Costing

� Is not a system of costing such as

process costing, job costing, operating

costing, etc.� A technique which is concerned with the

changes in costs and profits resulting

from changes in the volume of output.� It is also known as variable costing.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 12/38

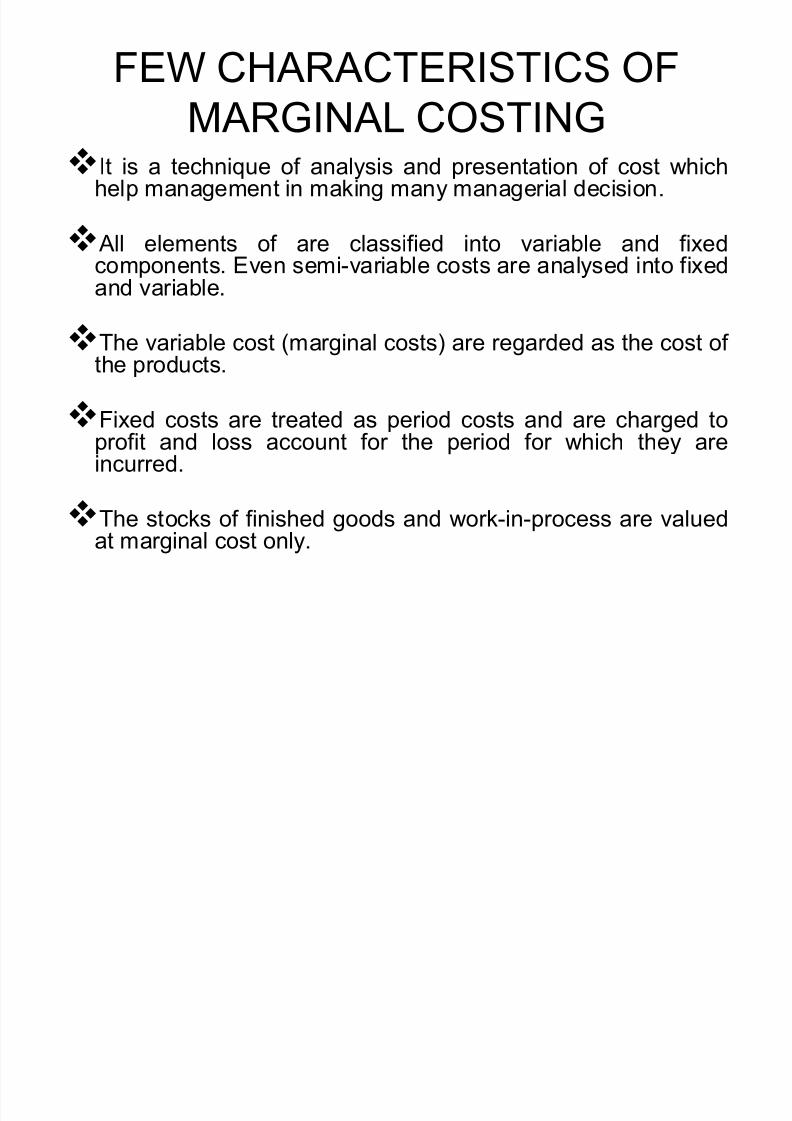

FEW CHARACTERISTICS OF

MARGINAL COSTINGIt is a technique of analysis and presentation of cost whichhelp management in making many managerial decision.

All elements of are classified into variable and fixed

components. Even semi-variable costs are analysed into fixedand variable.

The variable cost (marginal costs) are regarded as the cost of the products.

Fixed costs are treated as period costs and are charged toprofit and loss account for the period for which they areincurred.

The stocks of finished goods and work-in-process are valuedat marginal cost only.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 13/38

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 14/38

MARGINAL COST EQUATION

FOR THE SAKE OF CONVINIENCE, A MARGAL COST EQUATION CAN BEDERIVED AS FOLLOWS:-

Sales ± Variable cost = contribution.

Or, Sales = Variable cost + contribution.

Or, Sales = Variable cost + Fixed cost ± Profit / Loss.Or, Sales - Variable cost = Fixed cost ± Profit / Loss.

Or, S ± V = F ± P

Where µS¶ stands for Sales.

µV¶ stands for Variable cost.µF¶ stands for Fixed cost.

µP¶ stands for Profit / Loss.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 15/38

Profit / Volume Ratio (P/V Ratio or C /S Ratio)

P/V Ratio =Sales

Contribution

C S-V

= ---- = ------S S

Profit volume ratio is the ratio of contribution denoting the difference

between sales and variable cost. Since in the short term fixed cost does

not change, Profit/volume ratio also measures the rate of change of

profit due to change in the volume of sales.

If the sales price increases without corresponding increase in marginal

cost the contribution increases and the Profit volume ratio improves.

Similarly if the marginal cost is reduced with sale price remaining same

Profit/Volume ratio improves.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 16/38

Is a technique for studying the relationship between cost, volumeand profit.

Profits of an undertaking depends upon a large number of factors.

But the most important of these factors are the cost of manufacture,volume of sales and the selling price of the products.

In words of Herman C. Heiser,³the most significant single factor inprofit planning of the average business is the relationship betweenvolume of business, cost and profits .́

The CVP relationship is an important tool used for profit planning of a business.

Cost-Volume-Profit Analysis

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 17/38

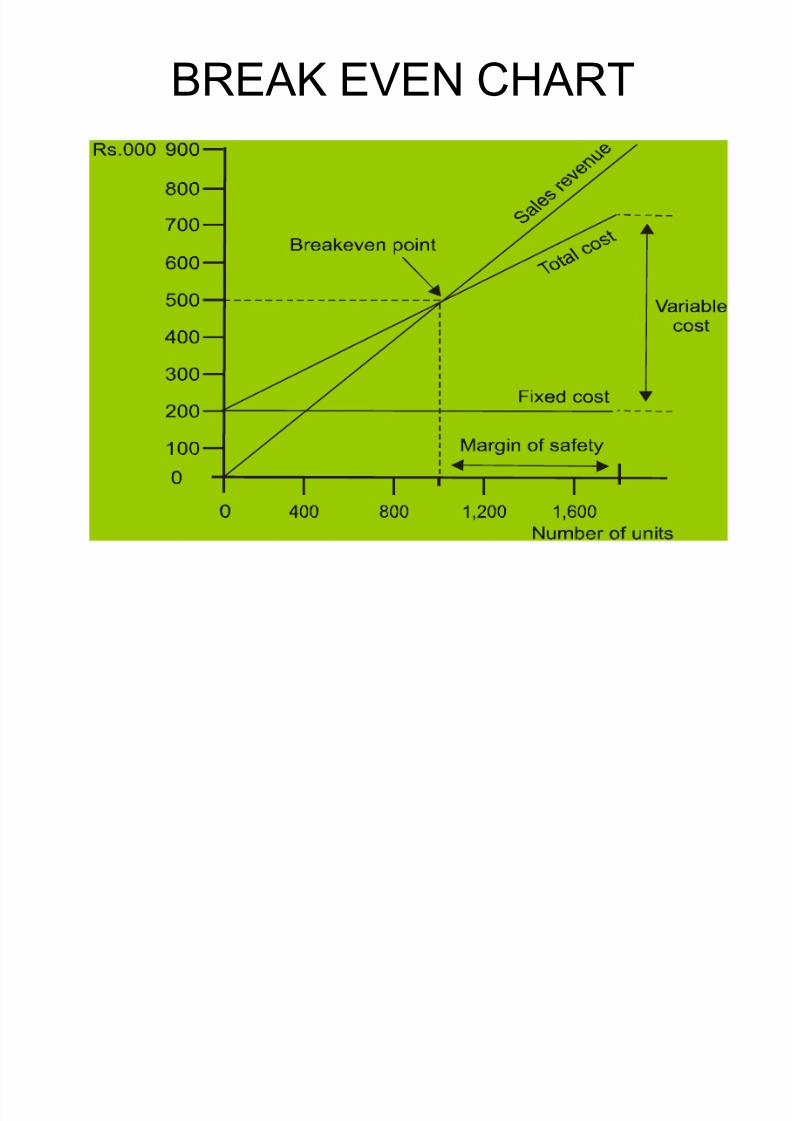

BREAK EVEN CHART

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 18/38

Break Even Point

� Break even point represents that volume of productionwhere total cost equal total revenue resulting into a no-profitno-loss situation. If output falls below that point, there is lossand if output exceeds the point there is profit. Therefore at

break even pointRevenue = Total Cost

Sales(S) = Cost (C) = Fixed Cost + Variable Cost

Sales - variable Cost = Contribution = Fixed Cost

� At break even point the contribution earned just covers thefixed cost and at levels below the point contribution earned isnot adequate to match the fixed cost and at levels above thepoint contribution earned more than recovers the fixed cost.

BEP = Fixed Cost/ PV Ratio

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 19/38

Margin of Safety

� Margin of safety is the difference between the sales or production ata particular level of activity and the break even sales a production.

M/S Ratio = ASR-BESR

ASR

M/S Ratio = margin of safety ratio, ASR = Actual Sales Revenue, BESR =

Break Even Sales Revenue

� A large margin of safety indicates the soundness of the businessand correspondingly a small margin of business indicates a not too-sound position. Margin of safety can be improved by lowering thefixed cost and variable costs, increasing the volumes of sales andproduction, increasing the selling prices or changing the product mixresulting into a better overall Profit/Volume ratio.

Profit

Margin of safety = -----------------------

Profit/Volume ratio

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 20/38

You are given the following data for the year 2007 of B Co. Ltd:

Variable cost 60000 60%

Fixed cost 30000 30%Net profit 10000 10%

Sales 100000 100%

Find out

(a)Break-even point

(b)P/V ratio(c)Margin of safety

(a)

(b)

(c) Margin of safety = Actual Sales ± BE point = 1,00,000 ± 75,000= Rs. 25,000

40% 1,00,000

60,0001,00,000

S

VS ratioP/V !

!

!

75,000Rs.40%

30,000

ratio P/V

F point BE !!!

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 21/38

(a) You are given the following data for the coming year for a factory.

Budgeted output 800000 units

Fixed expenses Rs. 4000000

Variable expenses/ unit Rs. 10Selling price/ unit Rs. 20

Find the break-even point.

(b) If price is reduced to Rs. 18, what will be the new break-evenpoint?

(a) Contribution = S ± V = Rs. 20 ± Rs. 10 = Rs. 10 per unit.

(b) When selling price is reduced

New selling price = Rs. 18New Contribution = Rs. 18 ± Rs. 10 = Rs. 8 per unit.

New

units 40000010Rs.

4000000

unit per on Contributi

cost Fixed ointB.E. !!!

units. 5000008s.

4000000s. Point. . !!

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 22/38

X Ltd. which is a multi product Company furnishes thefollowing data for the current year

Particulars First Half Year Second Half Year

Sales Rs 450000 Rs 500000

Total Cost Rs 400000 Rs 430000

Assuming that there is no change in prices and variable costand that the fixed expenses are incurred equally in the twohalf-year periods, calculate for the year

(i) Profit volume ratio

(ii) Fixed expenses

(iii) Break even sales

(iv) Margin of Safety Ratio

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 23/38

Sales Revenue ± Total Cost = Net Profit

Rs. 450000 - Rs 400000 = Rs 50000(1st Half)

Rs. 500000 - Rs 430000 = Rs 70000(2nd Half)

On a differential basis,

Sales Revenue-Total Cost=Net Profit

50000 ± 30000 = 20000

Only VC changes with change in S, Total Cost = VC

PV Ratio = (S-V)/S = (50000-30000)/50000 = 40%

VV Ratio = V/S = 30000/50000=60%

SR=FC + VC + NP

950000= FC + 0.60(950000) + 120000FC = 950000 ± 570000 ± 120000 = Rs 260000

BEP = FC/PV Ratio = 260000/0.40 = Rs 650000

M /S Ratio = (950000-650000)/950000 = 31.58%

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 24/38

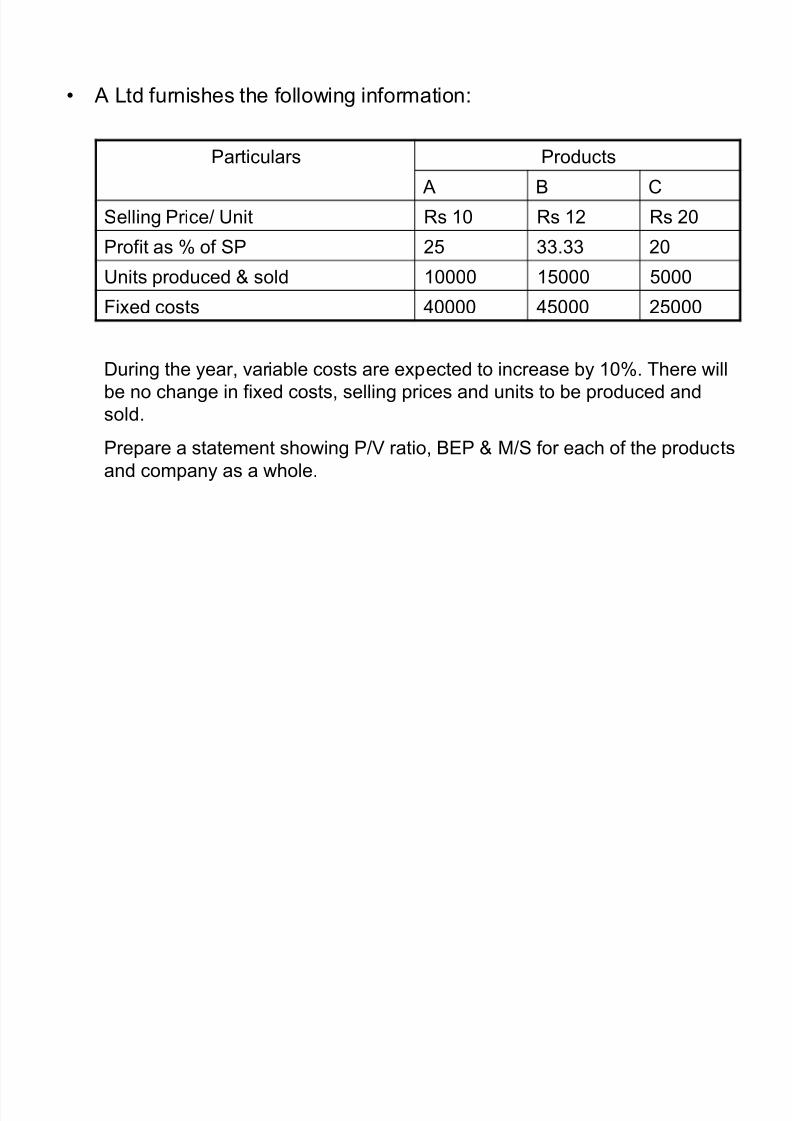

� A Ltd furnishes the following information:

Particulars Products

A B C

Selling Price/ Unit Rs 10 Rs 12 Rs 20

Profit as % of SP 25 33.33 20

Units produced & sold 10000 15000 5000Fixed costs 40000 45000 25000

During the year, variable costs are expected to increase by 10%. There will

be no change in fixed costs, selling prices and units to be produced and

sold.

Prepare a statement showing P/V ratio, BEP & M/S for each of the products

and company as a whole.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 25/38

Particulars

Year 1 Year 2

A B C COMBINED A B C COMBINED

Units produced & sold 10000 15000 5000 30000 10000 15000 5000 30000

Selling Price/Unit 10 12 20 12.667 10 12 20 12.667

Sales Revenue 100000 180000 100000 380000 100000 180000 100000 380000

Less: Variable Cost 35000 75000 55000 165000 38500 82500 60500 181500

Contribution 65000 105000 45000 215000 61500 97500 39500 198500

Less: Fixed Cost 40000 45000 25000 110000 40000 45000 25000 110000

Operating Profit 25000 60000 20000 105000 21500 52500 14500 88500

P/V Ratio (%) 65 58.33 45 56.58 61.5 54.17 39.5 52.24

BEP 194419 210579

Margin of Safety 185581 169421

Variable Cost = Sale Revenue - Fixed Cost - Net Profit

For Product A 100000-40000-(0.25*100000) = 35000 (Y1) Y2=35000*1.10 = 38500

For Product B 180000-45000-(0.3333*180000) = 75000 (Y1) Y2=75000*1.10 = 82500

For Product C 100000-25000-(0.20*100000) = 55000 (Y1) Y2=55000*1.10 = 60500

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 26/38

MANAGERIAL APPLICATION OF MARGINAL

COSTING

� PRICING DECISION

� PROFIT PLANNING

� MAKE OR BUY DECISIONS

� KEY FACTORS OR LIMITING FACTORS

� SELECTION OF A SUITABLE SALES MIX

� EFFECT OF CHANGES IN SALES PRICE

� DETERMINATION OF OPTIMUM LEVEL OF ACTIVITY

� EVALUATION OF PERFORMANCE

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 27/38

PRICING DECISION

� PRICING UNDER NORMAL CONDITION (Prices are basedon total cost of sales or marginal cost plus high margin on marginal cost)

� SELLING PRICE BELOW THE MARGINAL COST(Different circumstances such as introduction of new product, making aproduct popular, helping a joint product, goods are of perishable nature, theconcern had already purchased huge quantities of raw materials and theprices of these materials is falling considerably in the market, to obviateshut-down costs, to capture future market, to capture foreign market)

� PRICING DURING STIFF COMPETITION AND TRADEDEPRESSION (Some part of fixed cost to be covered, competitors

are to be eliminated from the market )

� ACEPTING SPECIAL ORDERS,BULK ORDERS, ADDITIONAL ORDERS, EXPORT ORDERS AND EXPLORING NEW MARKETS (below normal market price toutilise idle capacity)

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 28/38

PROFIT PLANNING

� DESIRED SALES WITH DESIRED LEVEL OF PROFIT

� DESIRED PROFIT WITH DESIRED LEVEL OF SALES

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 29/38

ILLUSTRATION

From the following particular s, calculate:i. Break-even point in terms of sales value.

ii. Number of units that must be sold to earn a profit of Rs. 90,000.

Fixed Factory Overhead cost = Rs. 60,000.

Fixed Selling Overhead cost = Rs. 12,000.

Variable Manufacturing Cost per Unit = Rs. 12.

Variable Selling Cost per unit = Rs. 3.

Selling Price per unit = Rs. 24.

BEP = Fixed Cost/P/V Ratio

Fixed Cost = Fixed Factory Overhead + Fixed Selling Overhead

= 60000 + 12000 = 72000P/V Ratio = (S ± V)/S = [24 ± (12+3)]/24 = 9/24 = 37.5%

BEP = 72000/0.375 = Rs 192000

Desired Sales volume for profit of Rs 90000 = (F + P)/(S - V) = (F + P)/C=72000+90000/9 = 18000 units

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 30/38

MAKE OR BUY DECISION

� Variable cost of manufacturing (internal) should be

compared with purchase price (outside)

� If variable cost of manufacturing is lower than purchase

price-MAKE

� If purchase price is lower than variable cost of manufacturing -BUY

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 31/38

� A manufacturing company finds that while the cost of making a component No. 0.51 in its own workshop is Rs.8.00 each, the same is available in market at Rs. 6.50

with an assurance of continuous supply. Give your suggestion whether to make or buy this component.

� Give also your views in case the supplier reduces theprice from Rs. 6.50 to Rs. 5.50. The cost of data follows:-

Materials 3. 00

Direct Labor 2. 00

Other Variable Expenses. 1. 00

Depreciation And Other

Fixed Expenses.

2. 00

Total . 8. 00

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 32/38

KEY FACTORS OR LIMITING FACTORS

� Contribution per unit of limiting factor should be

the criteria to assess the profitability of a product

� Product giving highest contribution should be

preferred .

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 33/38

SELECTION OF A SUITABLE SALES MIX

� Product with higher contribution should be

retained and their production to be increased

� Product with lower contribution should be

dropped or their production to be reduced

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 34/38

EFFECT OF CHANGES IN SALES PRICE

� Effect of changes in any of the component

particularly sales price can be easily analysed

under marginal costing

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 35/38

DETERMINATION OF OPTIMUM LEVEL

OF ACTIVITY

� Contribution at the different level of activity can

be found

� Level of activity which gives the highest

contribution will be the optimum level

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 36/38

EVALUATION OF PERFORMANCE

� Contribution of different products,

department or sales divisions can becompared.

� Addition/ Elimination of product lines/divisions/shifts/departments

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 37/38

Fun Garments Ltd. manufactures readymade garments anduses its cut pieces of cloth to manufacture toys. The followingstatement of cost has been prepared:

(Amount in Rs.)

Particular s Readymade Garments Toys Total

Direct Material 80000 6000 86000

Direct Labour 13000 1200 14200

Variable Overheads 17000 2800 19800Fixed Overheads 24000 3000 27000

Total Cost 134000 13000 147000

Sales 170000 12000 182000

Profit (loss) 36000 (1000) 35000

The cut pieces used in toys have a scrap value of Rs 1000 if sold in the market. On account of loss in manufacturing of toys, it is suggested to discontinue their manufacturing. Advisethe management.

8/6/2019 6.Mgmt Accounting

http://slidepdf.com/reader/full/6mgmt-accounting 38/38

Particulars Production

of Toys

Non-

Production

of ToysSales Revenue 12000 -

Scrap Value - 1000

Less: Avoidable costsDirect Material 6000

Direct Labour 1200

Variable Overheads 2800

Differential Revenue 2000 1000

Management is advised that differential revenue

favours continuation of production of Toys.