108

Providing in-depth insight, data, and analysis of everything digital. BI Intelligence 7 PREDICTIONS ABOUT THE FUTURE OF MEDIA

| Date post: | 14-Feb-2017 |

| Category: |

Business |

| Upload: | ezhilarasan-natarajan |

| View: | 648 times |

| Download: | 1 times |

Providing in-depth insight, data, and analysis of everything digital. BI Intelligence

7 PREDICTIONS ABOUT THE FUTURE OF MEDIA

1. DIGITAL WILL INHERIT THE EARTH

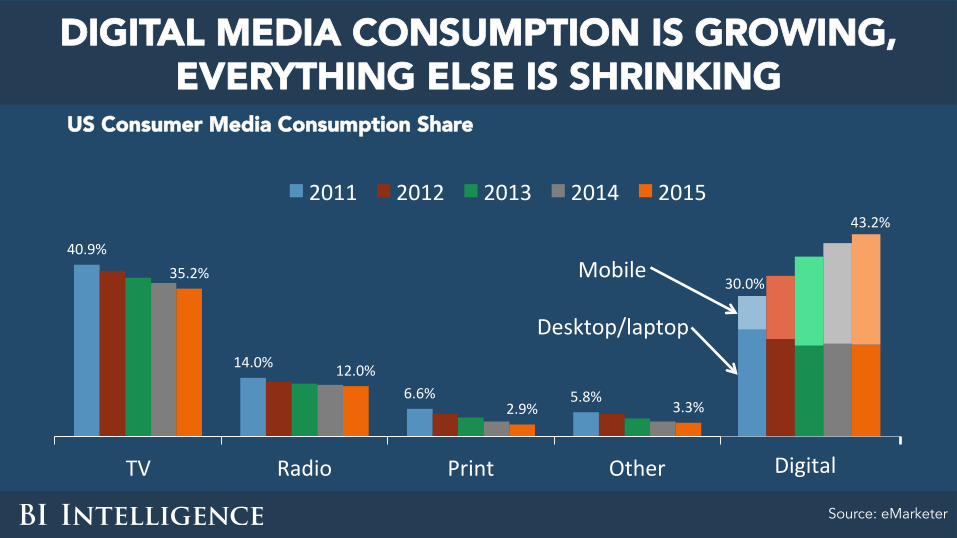

DIGITAL MEDIA CONSUMPTION IS GROWING, EVERYTHING ELSE IS SHRINKING

US Consumer Media Consumption Share

Source: eMarketer

43.2%

40.9%

14.0%

6.6% 5.8%

35.2%

12.0%

2.9% 3.3%

TV Radio Print Other

2011 2012 2013 2014 2015

Desktop/laptop

Digital

30.0%Mobile

And averages do not tell the whole story…

THE SHIFT IS GENERATIONAL Top 5 Media Mentions Among All Adults, 2013

Source: Ofcom

0 20 40 60 80 100

TotalAged16-24Aged25-34Aged35-44Aged45-54Aged55-64Aged65-74Aged75+ WatchTV

Readnewspapers/magazines

Listentotheradio

Goonlineonacomputer/laptop/netbook/tablet

Useasmartphone

GENERATIONS HAVE A PREDICTABLE LIFE CYCLE…

Source: Goldman Sachs

• First digital native generation(s)

• Already 45% of population and largest share of earners

• Profoundly different media habits

MILLENNIALS AND GEN Z

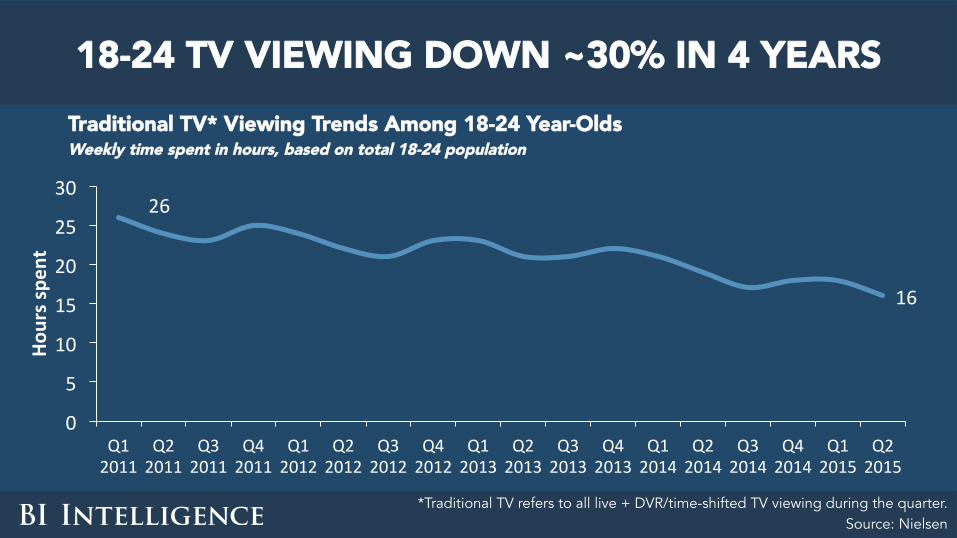

26

16

0

5

10

15

20

25

30

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Hourss

pent

18-24 TV VIEWING DOWN ~30% IN 4 YEARS Traditional TV* Viewing Trends Among 18-24 Year-Olds Weekly time spent in hours, based on total 18-24 population

*Traditional TV refers to all live + DVR/time-shifted TV viewing during the quarter. Source: Nielsen

Meanwhile…

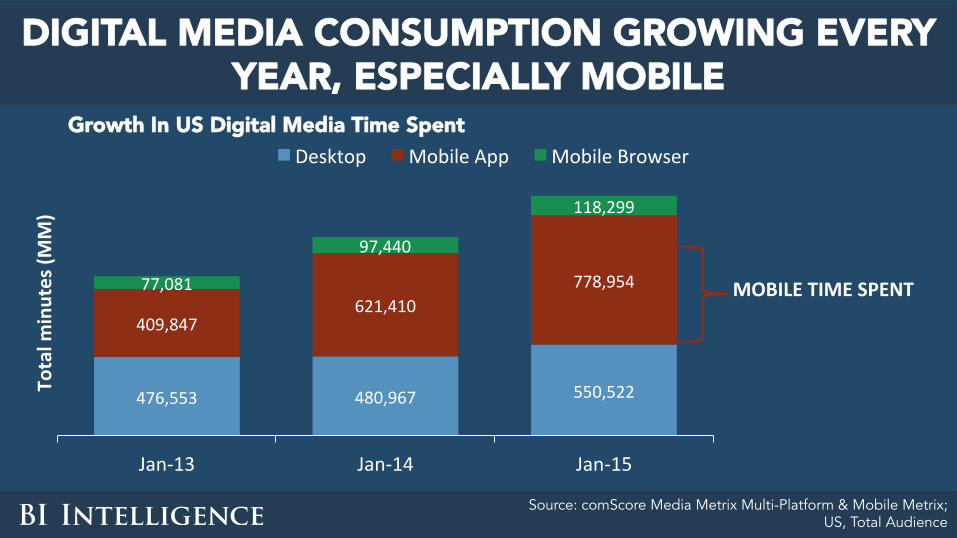

DIGITAL MEDIA CONSUMPTION GROWING EVERY YEAR, ESPECIALLY MOBILE

Source: comScore Media Metrix Multi-Platform & Mobile Metrix; US, Total Audience

476,553 480,967 550,522

409,847621,410

778,95477,081

97,440

118,299

Jan-13 Jan-14 Jan-15

Totalm

inutes(M

M)

Desktop MobileApp MobileBrowser

MOBILETIMESPENT

Growth In US Digital Media Time Spent

MILLENNIALS CHECK THEIR PHONES EVERY 10 MINUTES

Source: Kana Software

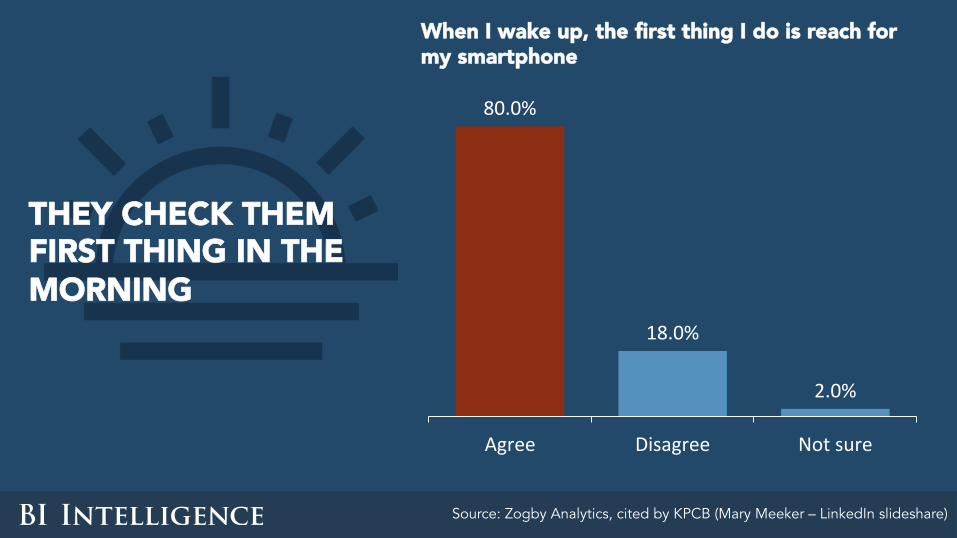

Source: Zogby Analytics, cited by KPCB (Mary Meeker – LinkedIn slideshare)

THEY KEEP THEM IN REACH 24 HOURS A DAY

My smartphone never leaves my side, night or day

87.0%

12.0%2.0%

Agree Disagree Notsure

Source: Zogby Analytics, cited by KPCB (Mary Meeker – LinkedIn slideshare)

THEY CHECK THEM FIRST THING IN THE MORNING

When I wake up, the first thing I do is reach for my smartphone

80.0%

18.0%

2.0%

Agree Disagree Notsure

So here’s a glimpse at the past, present, and future of media…

THE PAST (~2000): 3% DIGITAL

Source: Ofcom

0%10%20%30%40%50%60%70%80%90%

100%

Smartphone

Computer/laptop/tablet

Radio

TV

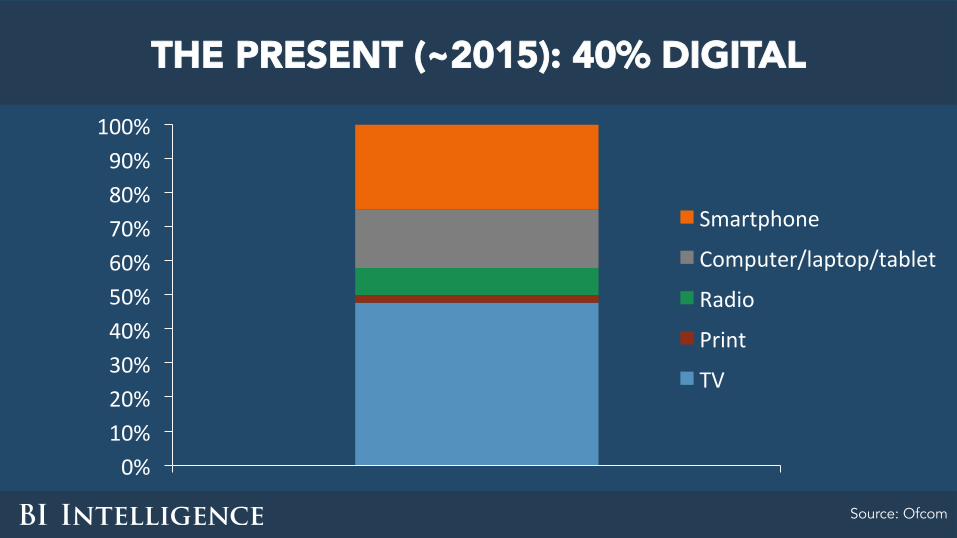

THE PRESENT (~2015): 40% DIGITAL

Source: Ofcom

0%10%20%30%40%50%60%70%80%90%100%

Smartphone

Computer/laptop/tablet

Radio

TV

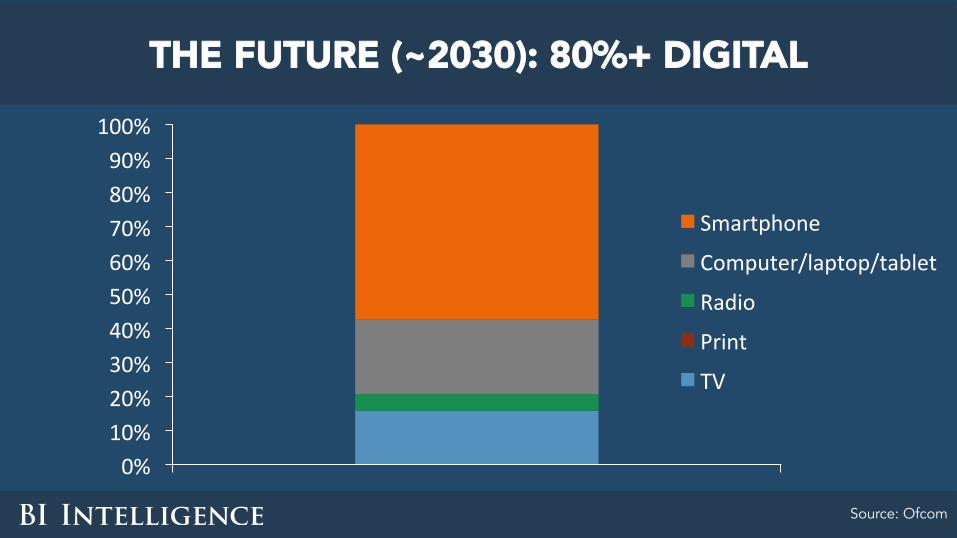

THE FUTURE (~2030): 80%+ DIGITAL

Source: Ofcom

0%10%20%30%40%50%60%70%80%90%

100%

Smartphone

Computer/laptop/tablet

Radio

TV

2. SUBSCRIPTIONS FOR THE WIN!

Remember when pundits said digital content had to be free

because no one would ever pay?

Oops.

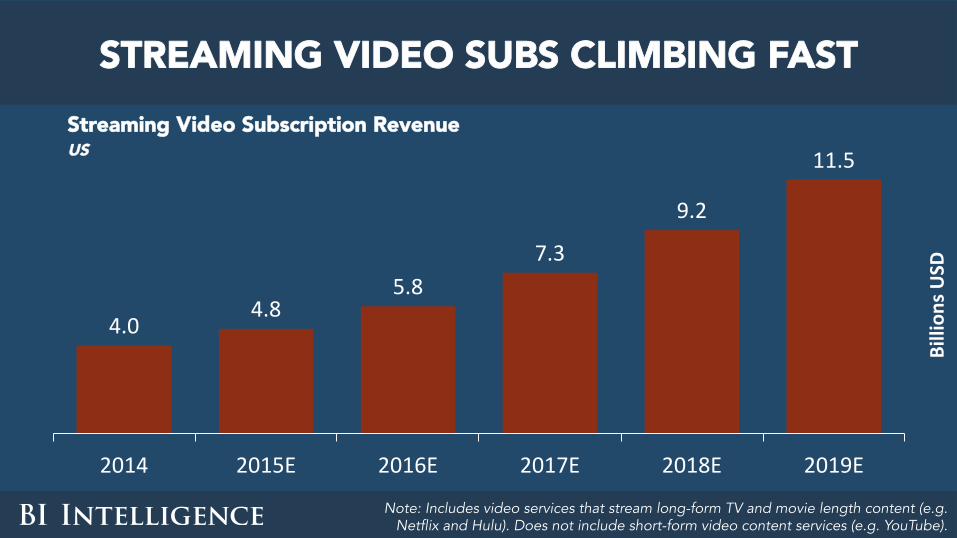

4.04.8

5.87.3

9.2

11.5

2014 2015E 2016E 2017E 2018E 2019E

Billion

sUSD

STREAMING VIDEO SUBS CLIMBING FAST Streaming Video Subscription Revenue US

Note: Includes video services that stream long-form TV and movie length content (e.g. Netflix and Hulu). Does not include short-form video content services (e.g. YouTube).

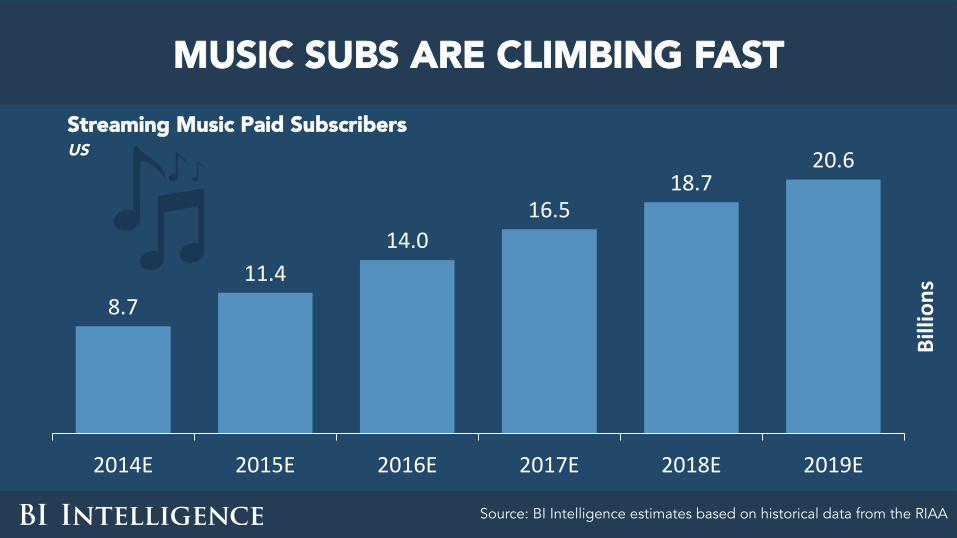

8.711.4

14.016.5

18.720.6

2014E 2015E 2016E 2017E 2018E 2019E

Billion

s

MUSIC SUBS ARE CLIMBING FAST Streaming Music Paid Subscribers US

Source: BI Intelligence estimates based on historical data from the RIAA

AdverZsing

SubscripZons

$-

$20

$40

$60

$80

$100

$120

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414

Millions

EVEN “PRINT” SUBS ARE CLIMBING FAST New York Times Digital Revenue Global

Source: The New York Times

The new pundit story is that there’s one right model — subs or ads

The truth is that both work, as do a la carte sales.

Most media companies have dual revenue streams.

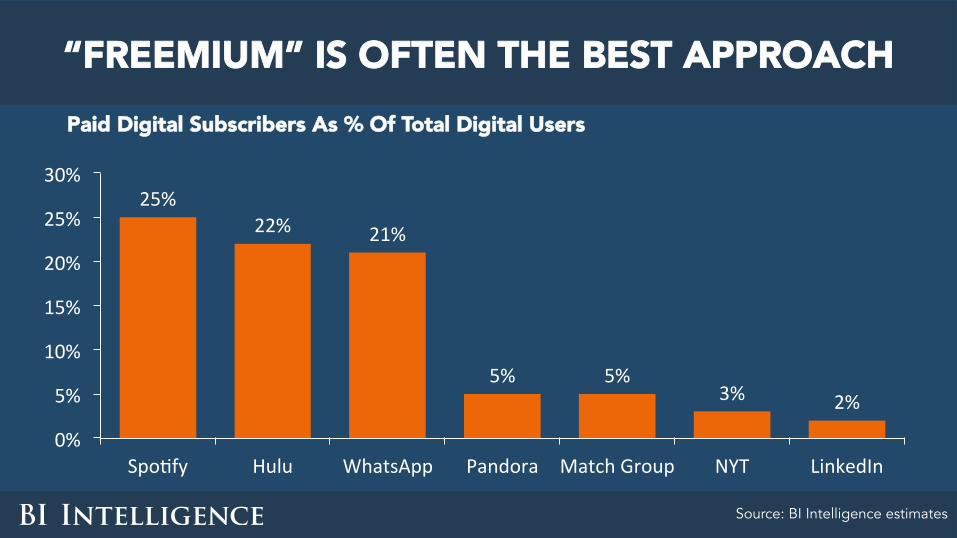

“FREEMIUM” IS OFTEN THE BEST APPROACH Paid Digital Subscribers As % Of Total Digital Users

Source: BI Intelligence estimates

25%22% 21%

5% 5%3% 2%

0%

5%

10%

15%

20%

25%

30%

SpoZfy Hulu WhatsApp Pandora MatchGroup NYT LinkedIn

3. (NATIVE) DIGITAL ADVERTISING WILL CONTINUE TO THRIVE

The best definition of “native ads”…

Ads that fit the way content and stories in the medium are consumed.

“NATIVE ADS”

In digital, “search” and “scroll” are the dominant ways content is consumed.

BEHOLD THE POWER OF NATIVE DIGITAL ADS

Note: Based on GAAP revenue. Source: Company Filings, BI Intelligence estimates

FacebookYahoo

AOLTwiber

$0

$5

$10

$15

$20

$25

Billion

s

Digital Advertising Revenues Global

“Read, watch, and listen” are also digital formats.

But the experience is different than in legacy media.

Native digital brand ads will increasingly take advantage of the digital difference.

4. THE EXISTENTIAL CRISIS OF AD BLOCKING WILL RESOLVE ITSELF —

BUT CAREFUL WHAT YOU WISH FOR

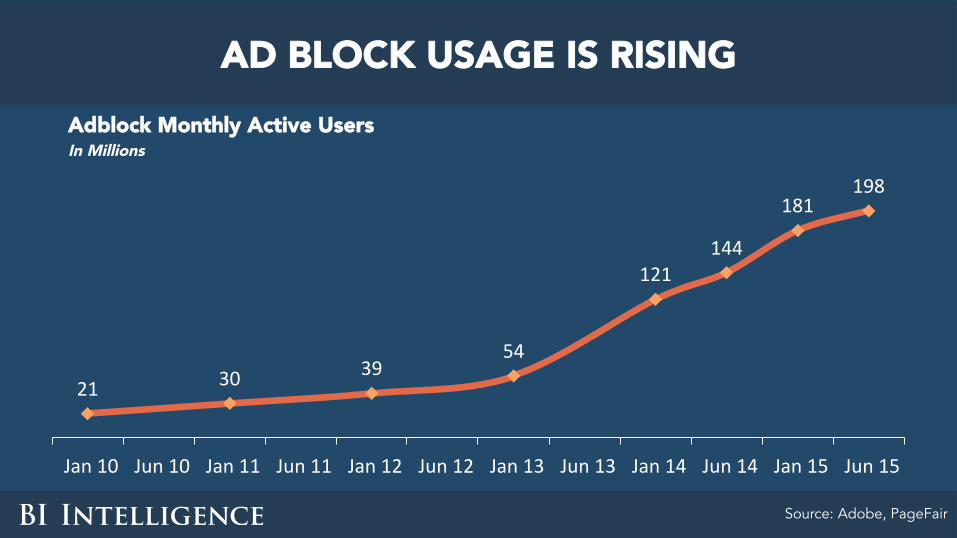

AD BLOCK USAGE IS RISING

Source: Adobe, PageFair

21 30 3954

121144

181198

Jan10 Jun10 Jan11 Jun11 Jan12 Jun12 Jan13 Jun13 Jan14 Jun14 Jan15 Jun15

Adblock Monthly Active Users In Millions

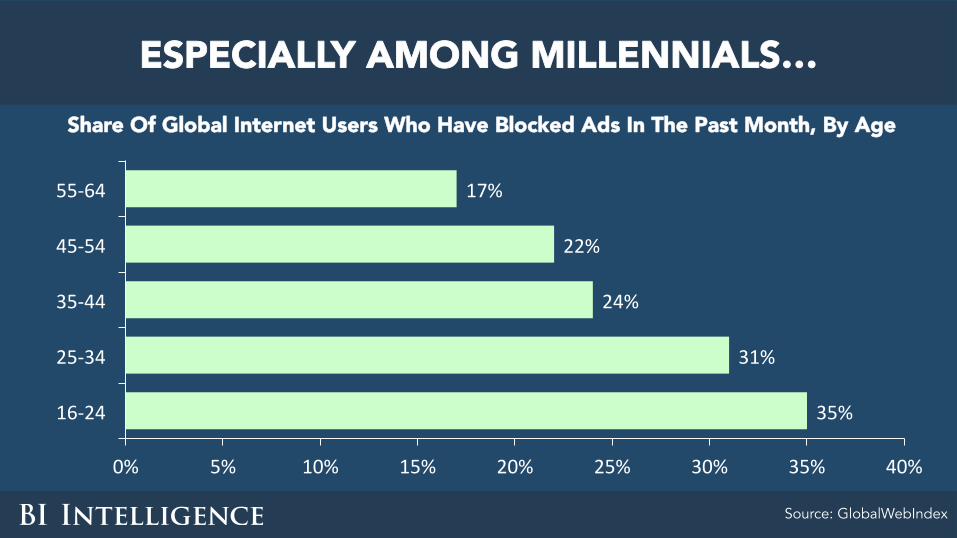

ESPECIALLY AMONG MILLENNIALS… Share Of Global Internet Users Who Have Blocked Ads In The Past Month, By Age

Source: GlobalWebIndex

35%

31%

24%

22%

17%

0% 5% 10% 15% 20% 25% 30% 35% 40%

16-24

25-34

35-44

45-54

55-64

Source:GlobalWebIndex

AND TECHIES

Note: Estimated to nearest 5% increment Source: PageFair

30%25%25%

20%20%20%

15%15%

10%10%10%

5%

GamesTechnology

ComicsAdult

EntertainmentSportsNews

BusinessLifestyle

LocalFinanceTravel

Ad-Block Usage Rates, By Vertical Global

There is a lot of self-interested finger-pointing, moralizing,

and rationalizing going on — from all parties.

If all ads are blocked, most free content will cease to exist.

ONE THING IS CLEAR…

So what will happen?

Quality will improve!

Publishers, platforms, and advertisers will focus more on user experience and choice.

People will choose to view ads from, and/or subscribe to,

publishers and platforms they like.

These decisions will not all be voluntary.

5. THE NEXT BIG PLATFORM IS…

As smartphones get boring, everyone is hunting

for the next big platform.

Many candidates have been suggested — glasses, watches, cars, virtual reality…

None of these will be the next big platform.

Smart glasses flopped.

Smartwatches haven’t entirely flopped, but no one will be reading, watching,

or listening to media on them anytime soon.

Cars won’t become media and communications platforms —

other platforms will be used inside them.

VR is promising, but it’s still too early.

VR INSTALLED BASE STILL SMALL Estimated Global Virtual Reality Headset Shipments

Source: BI Intelligence estimates, 2015

-

5

10

15

20

25

30

2015E 2016E 2017E 2018E 2019E 2020E

Shipmen

ts(M

illions)

• Complicated to use

• Screen resolution low

• Display often nausea-inducing

• Prices steep

AND EXPERIENCE STILL LEAVES MUCH TO BE DESIRED

Messaging apps!

SO THE NEXT BIG PLATFORM WILL BE…

Source: Salesforce

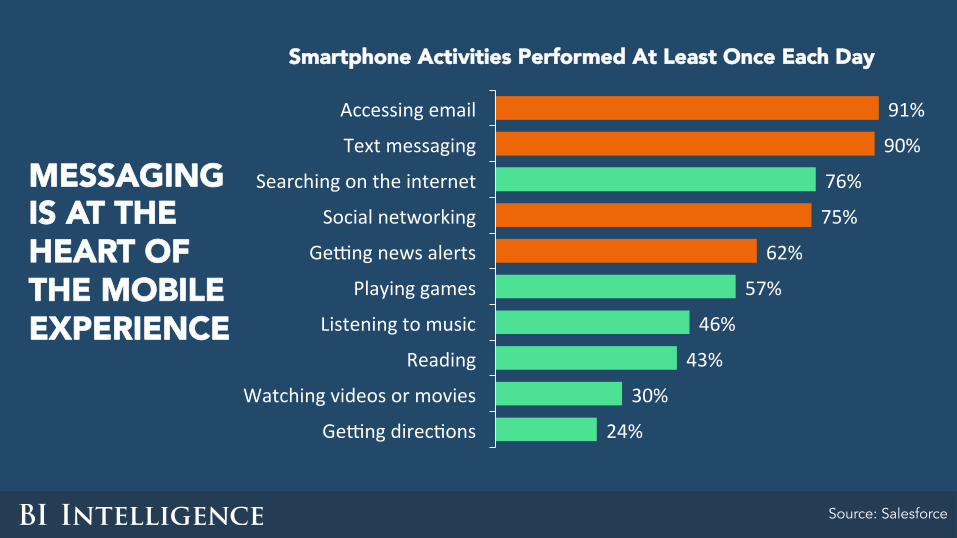

MESSAGING IS AT THE HEART OF THE MOBILE EXPERIENCE

Smartphone Activities Performed At Least Once Each Day

24%

30%

43%

46%

57%

62%

75%

76%

90%

91%

GecngdirecZons

Watchingvideosormovies

Reading

Listeningtomusic

Playinggames

Gecngnewsalerts

Socialnetworking

Searchingontheinternet

Textmessaging

Accessingemail

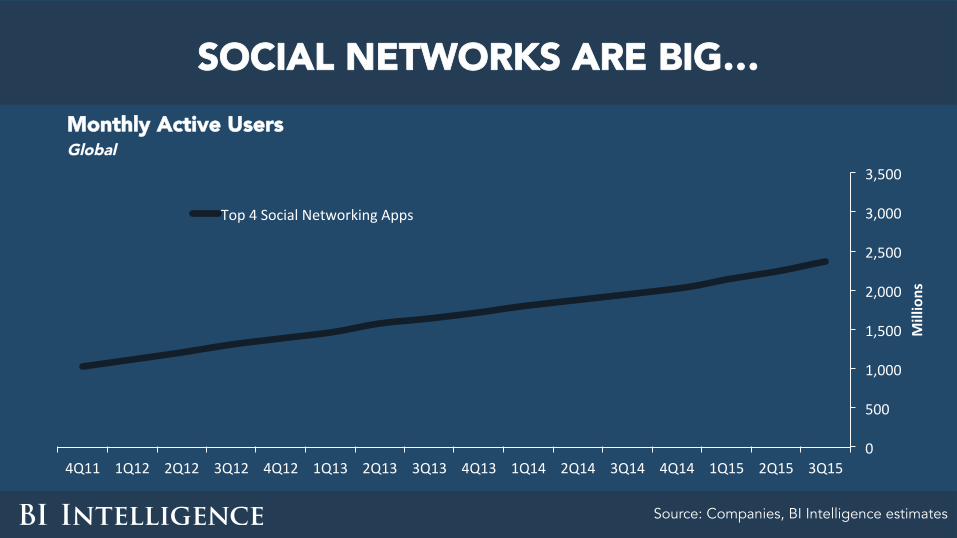

SOCIAL NETWORKS ARE BIG…

Source: Companies, BI Intelligence estimates

Monthly Active Users Global

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

Millions

Top4SocialNetworkingApps

BUT MESSAGING APPS ARE ALREADY BIGGER

Source: Companies, BI Intelligence estimates

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

Millions

Top4SocialNetworkingApps

Top4MessagingApps

Monthly Active Users Global

0

100

200

300

400

500

600

700

800

900

1000

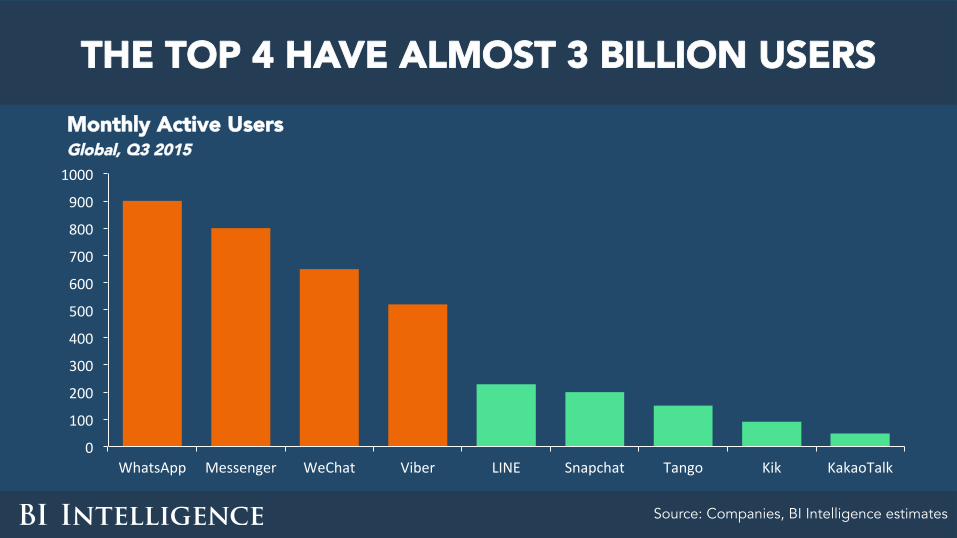

WhatsApp Messenger WeChat Viber LINE Snapchat Tango Kik KakaoTalk

Monthly Active Users Global, Q3 2015

THE TOP 4 HAVE ALMOST 3 BILLION USERS

Source: Companies, BI Intelligence estimates

FACEBOOK OWNS TWO — PLUS INSTAGRAM Facebook Messenger Monthly Active Users Global

Source: Company, BI Intelligence estimates

0100200300400500600700800900

4Q111Q122Q123Q124Q121Q132Q133Q134Q131Q142Q143Q144Q141Q152Q153Q15

Millions

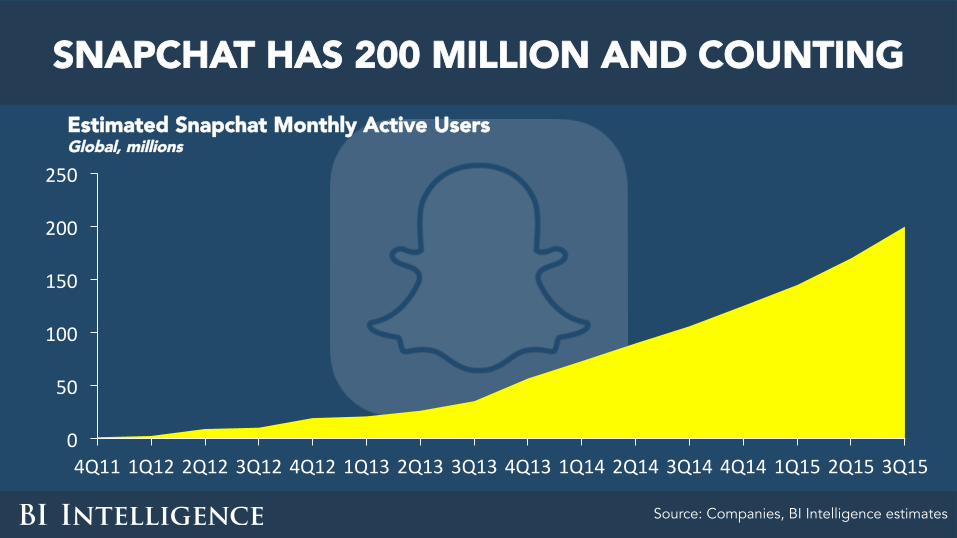

SNAPCHAT HAS 200 MILLION AND COUNTING

0

50

100

150

200

250

4Q111Q122Q123Q124Q121Q132Q133Q134Q131Q142Q143Q144Q141Q152Q153Q15

Estimated Snapchat Monthly Active Users Global, millions

Source: Companies, BI Intelligence estimates

YOU CAN DO EVERYTHING IN THESE APPS

Calls Chat GIFs

Games SZckers VoIP

Taxi E-commerce Music

Video Payments URLBar/Search

UZliZes QRCodes

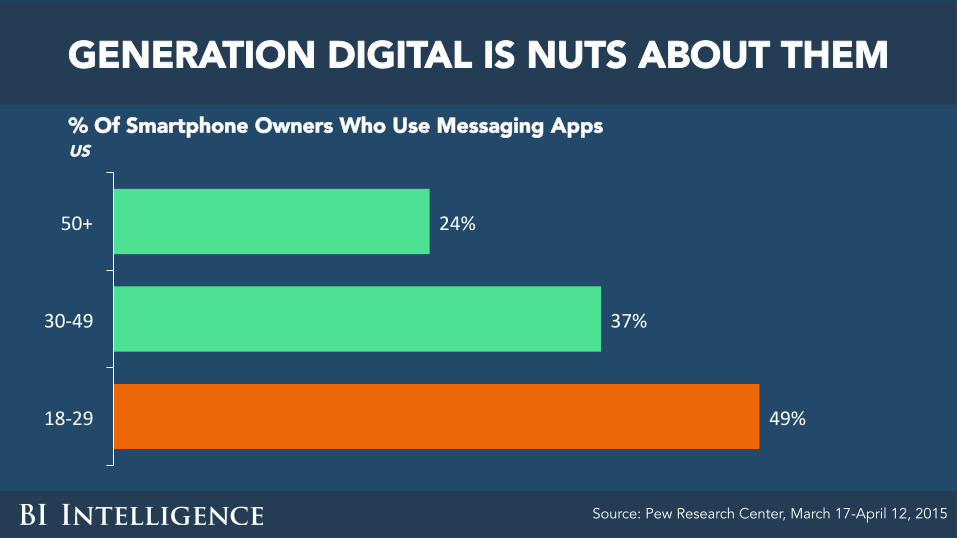

GENERATION DIGITAL IS NUTS ABOUT THEM % Of Smartphone Owners Who Use Messaging Apps US

Source: Pew Research Center, March 17-April 12, 2015

49%

37%

24%

18-29

30-49

50+

6. TV NETWORKS WILL SOON FEEL NEWSPAPERS’ PAIN

TRADITIONAL TV HAS PASSED ITS PEAK Households With Pay TV Vs. Subscription OTT, U.S., 2010-2015E, Millions

Leichman Research Group, US Census Bureau, Activate analysis

99 100.9 100.8 99.3 9897.1

23 28 33 38 4350.3

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015E

PayTVHouseholds DigitalSubscripZon(OTT)Households

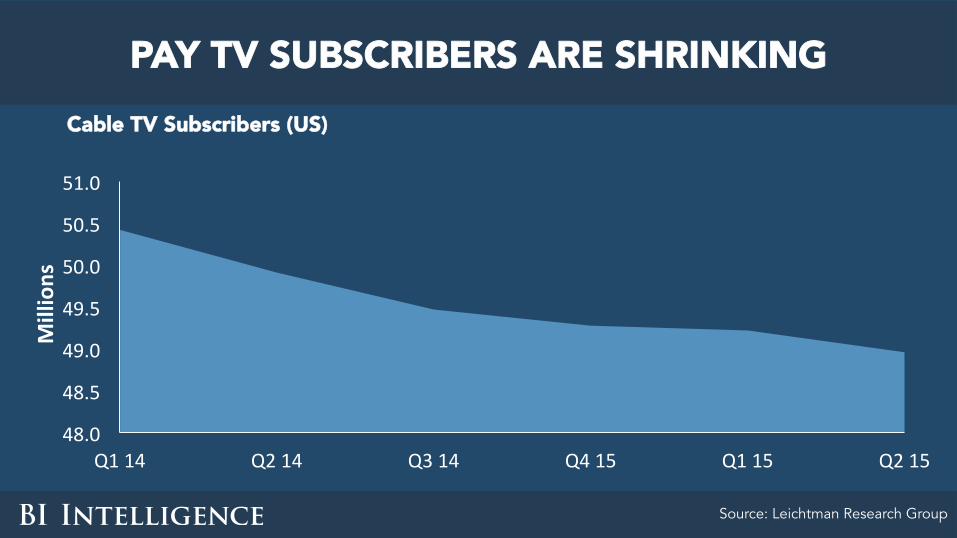

PAY TV SUBSCRIBERS ARE SHRINKING Cable TV Subscribers (US)

Source: Leichtman Research Group

48.0

48.5

49.0

49.5

50.0

50.5

51.0

Q114 Q214 Q314 Q415 Q115 Q215

Millions

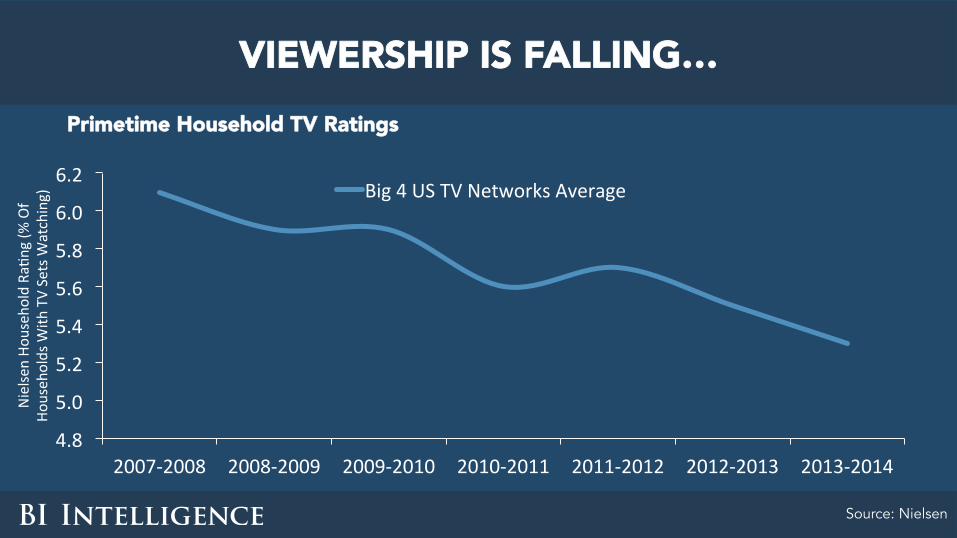

VIEWERSHIP IS FALLING… Primetime Household TV Ratings

Source: Nielsen

4.8

5.0

5.2

5.4

5.6

5.8

6.0

6.2

2007-2008 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

Nielse

nHo

useh

oldRa

Zng(%

Of

Househ

oldsW

ithTVSetsW

atching) Big4USTVNetworksAverage

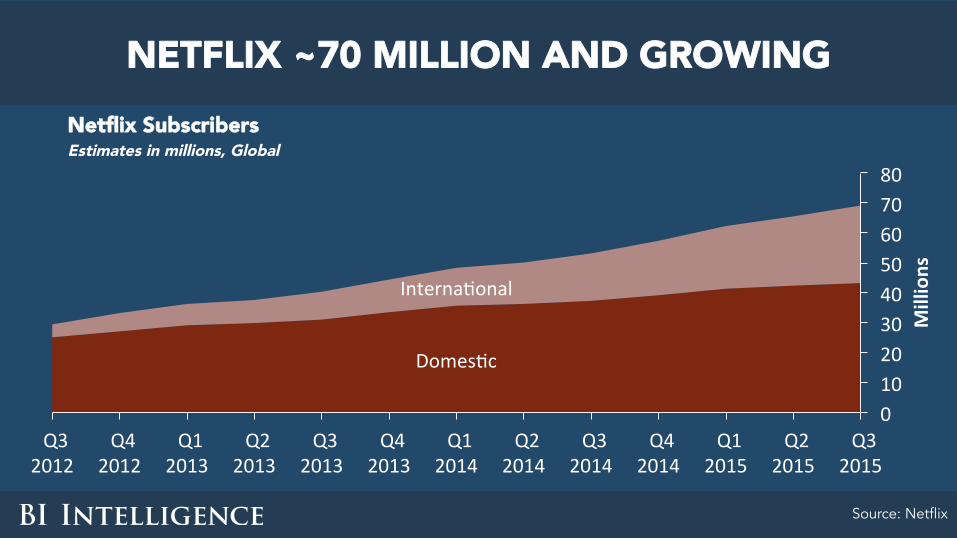

Meanwhile…

NETFLIX ~70 MILLION AND GROWING Netflix Subscribers Estimates in millions, Global

Source: Netflix

DomesZc

InternaZonal

01020304050607080

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Millions

012345678910

2011 2012 2013 2014 2015E

Millions

HULU ~10 MILLION AND GROWING Hulu Subscribers Estimates in millions, Global

Source: Hulu, BI Intelligence estimates

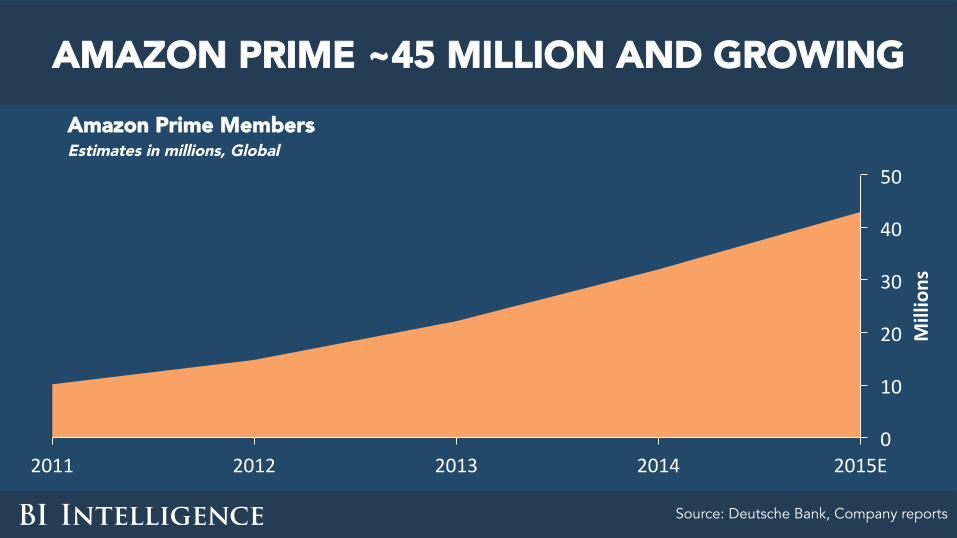

AMAZON PRIME ~45 MILLION AND GROWING Amazon Prime Members Estimates in millions, Global

Source: Deutsche Bank, Company reports

0

10

20

30

40

50

2011 2012 2013 2014 2015E

Millions

-510152025303540

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Millions

Global US

APPLE TV 35 MILLION+ AND GROWING Apple TV Installed Base

Source: BI Intelligence estimates

58%

73%83%

89%

63%68%

63%

42%

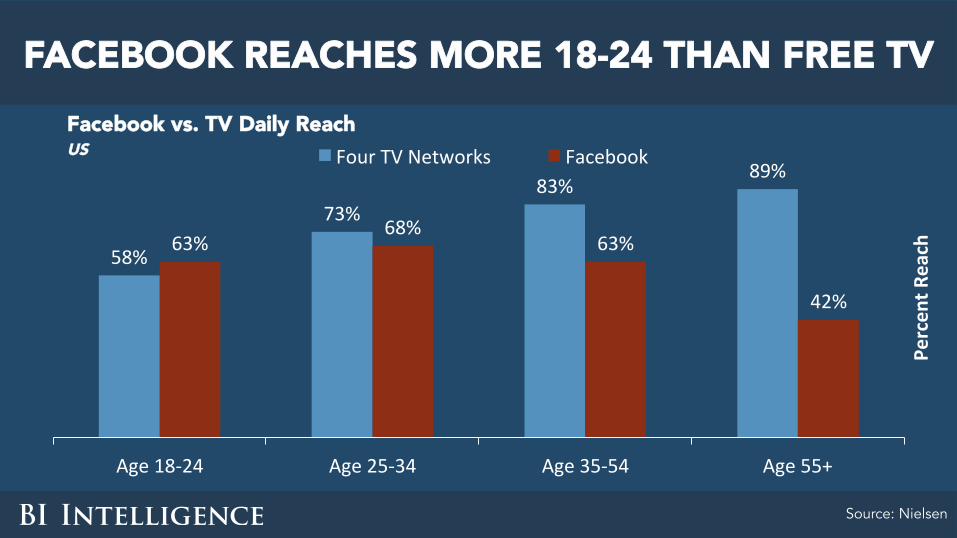

Age18-24 Age25-34 Age35-54 Age55+

Percen

tReach

FourTVNetworks Facebook

FACEBOOK REACHES MORE 18-24 THAN FREE TV

Source: Nielsen

Facebook vs. TV Daily Reach US

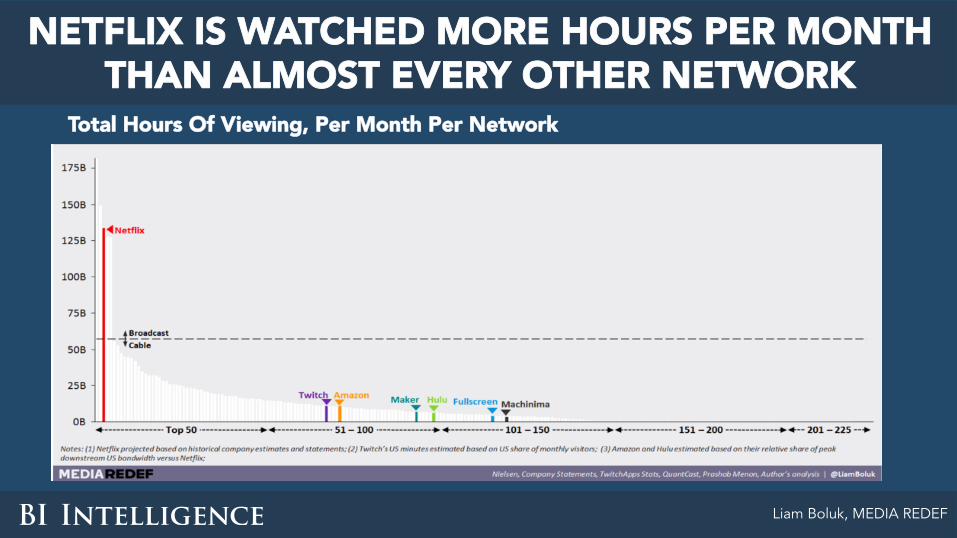

NETFLIX IS WATCHED MORE HOURS PER MONTH THAN ALMOST EVERY OTHER NETWORK

Total Hours Of Viewing, Per Month Per Network

Liam Boluk, MEDIA REDEF

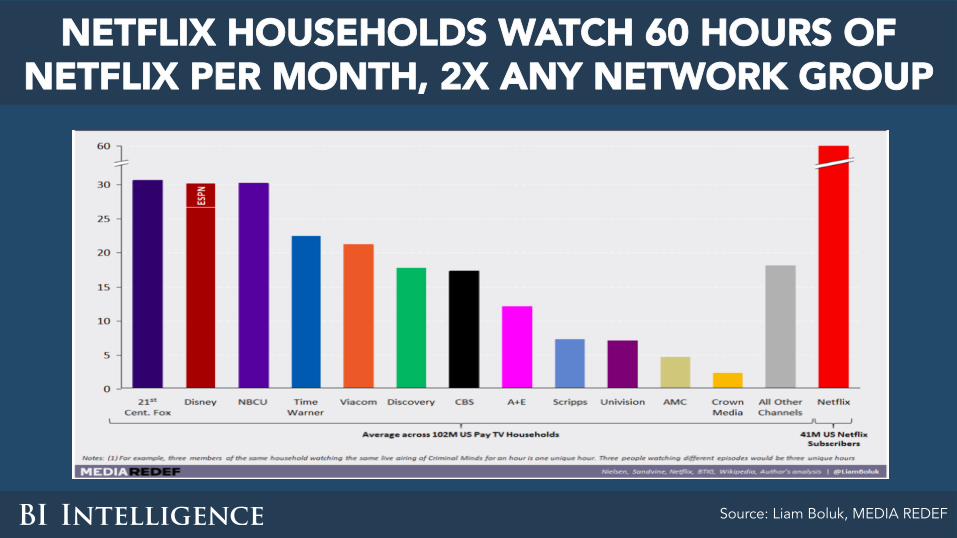

NETFLIX HOUSEHOLDS WATCH 60 HOURS OF NETFLIX PER MONTH, 2X ANY NETWORK GROUP

Source: Liam Boluk, MEDIA REDEF

YES, TV STILL DOMINATES VIEWING TIME US Consumer Time Spent On Video Per Month, 2015E, Hours

Source: Digitalsmiths, eMarketer, GfK, Sandvine, Nielsen, TDG, Activate analysis

TradiZonalTV72%

SubscripZonTV14%

Ad-Supported9%

PaidDownloads5% Total:177hours

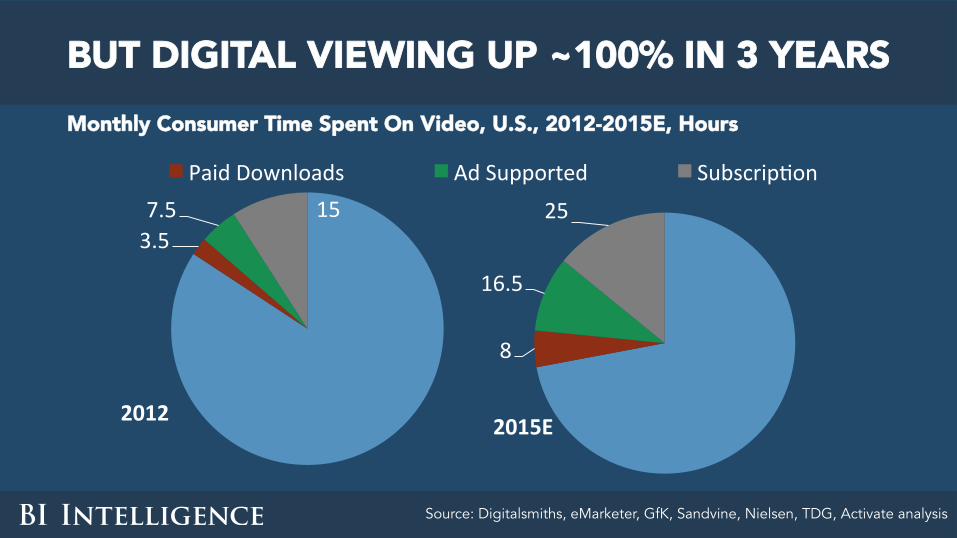

BUT DIGITAL VIEWING UP ~100% IN 3 YEARS

Source: Digitalsmiths, eMarketer, GfK, Sandvine, Nielsen, TDG, Activate analysis

3.57.5 15

PaidDownloads AdSupported SubscripZon

2012

8

16.5

25

2015E

Monthly Consumer Time Spent On Video, U.S., 2012-2015E, Hours

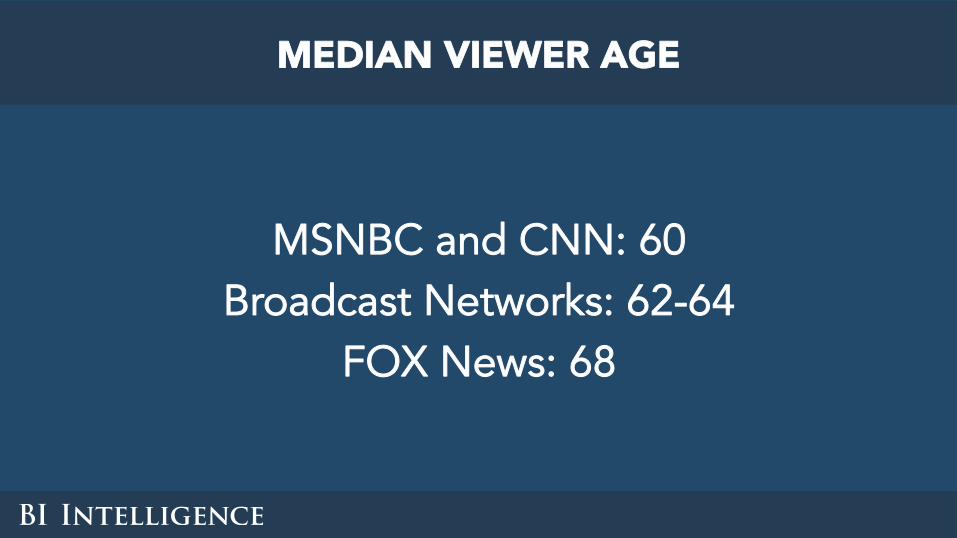

And the TV audience is increasingly a specific demographic…

MSNBC and CNN: 60 Broadcast Networks: 62-64

FOX News: 68

MEDIAN VIEWER AGE

Convenience.

WHY IS DIGITAL TV GROWING?

We can watch what we want to watch when we want to watch it

— on any screen.

WHY IS DIGITAL GROWING?

So what’s going to happen?

First, ignore people who say “TV will die.”

Old media don’t die. They just find their niche(s). See radio and print.

There are three key parts of “TV” — and two of them are thriving.

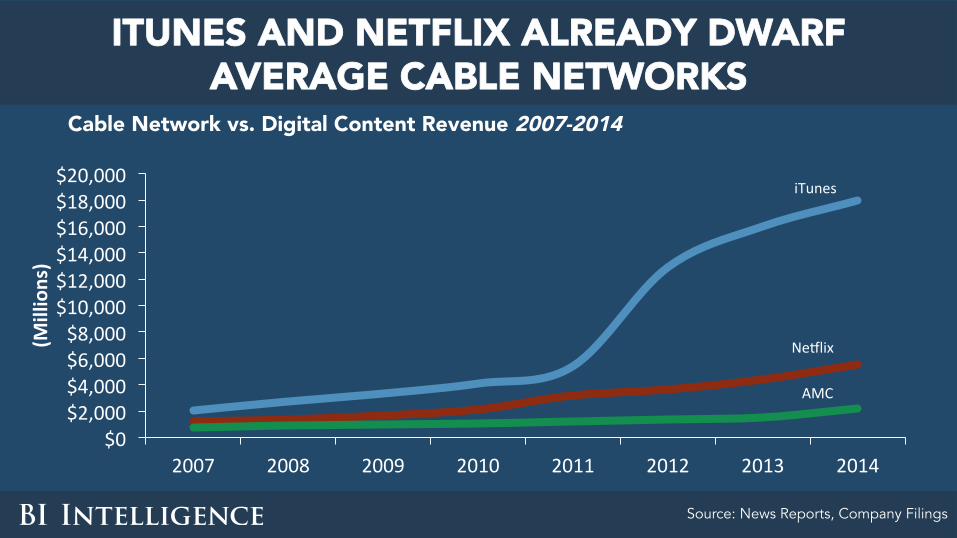

1. Digital TV networks will continue to thrive

iTunes

Neilix

AMC

$0$2,000$4,000$6,000$8,000$10,000$12,000$14,000$16,000$18,000$20,000

2007 2008 2009 2010 2011 2012 2013 2014

(Millions)

ITUNES AND NETFLIX ALREADY DWARF AVERAGE CABLE NETWORKS

Source: News Reports, Company Filings

Cable Network vs. Digital Content Revenue 2007-2014

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2007 2008 2009 2010 2011 2012 2013 2014

(Millions) CBSAd

YouTubeAdRevenue

AMCNetworksRevenue

CBSAdRevenue

YOUTUBE REVENUE CLOSING IN ON BROADCAST NETWORKS

YouTube Ad Revenue Vs. CBS Ad Revenue And AMC Networks Revenue

Source: News Reports, Company Filings, BI Intelligence estimates, BofA Merrill Lynch Global Research

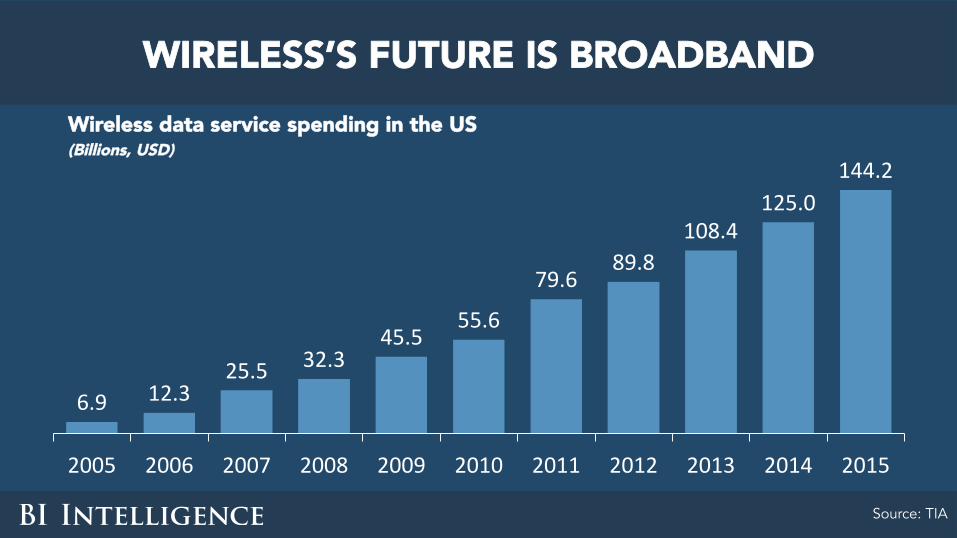

2. Access providers will continue to thrive — unless (until?)

real price competition

CABLE’S FUTURE IS BROADBAND Cable Subscribers Millions By Service (US)

Note: Select major cable providers Source: Leichtman Research Group

50 50 50 50 49 49 49 49 4949 49 50 51 51 52 53 53 54

Q313 Q413 Q114 Q214 Q314 Q414 Q115 Q215 Q315

TV Broadband

6.9 12.325.5 32.3

45.555.6

79.689.8

108.4125.0

144.2

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WIRELESS’S FUTURE IS BROADBAND Wireless data service spending in the US (Billions, USD)

Source: TIA

3. Traditional TV networks will go through ~decades of pain

Why?

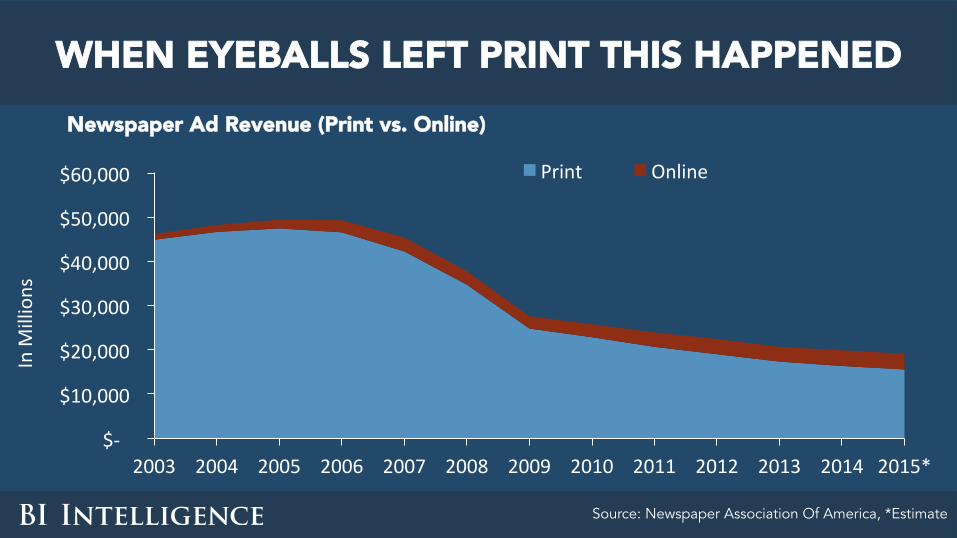

Money follows eyeballs.

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

InM

illions

Print Online

WHEN EYEBALLS LEFT PRINT THIS HAPPENED Newspaper Ad Revenue (Print vs. Online)

Source: Newspaper Association Of America, *Estimate

THERE ARE TOO MANY NETWORKS Channels Receivable And Watched Per TV Household US

Source: Nielsen

129.3 136.4151.4

168.5 179.1 189.1

17.3 17.7 17.8 17.5 17.8 17.5

2008 2009 2010 2011 2012 2013

AverageTVChannelsReceived AverageTVChannelsWatched

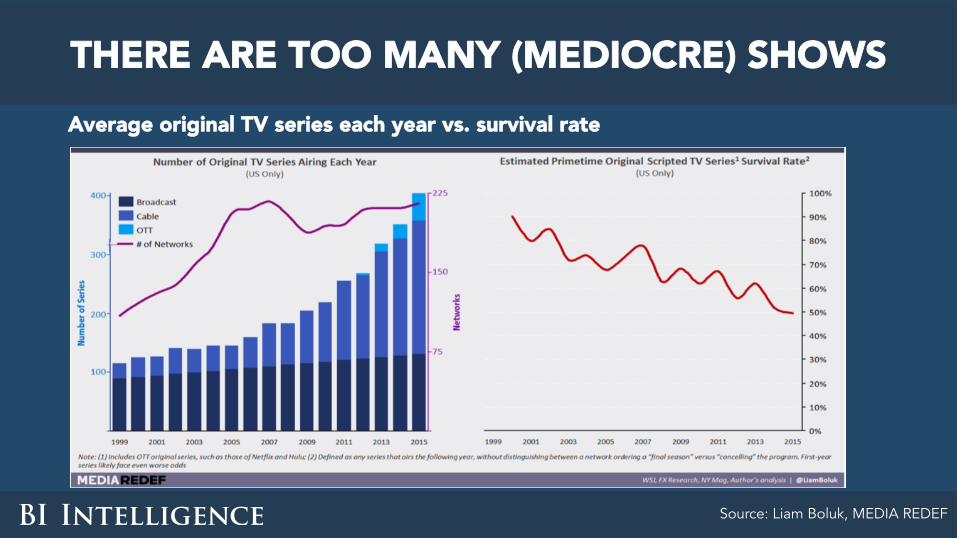

THERE ARE TOO MANY (MEDIOCRE) SHOWS Average original TV series each year vs. survival rate

Source: Liam Boluk, MEDIA REDEF

So get ready for years of consolidation and pain.

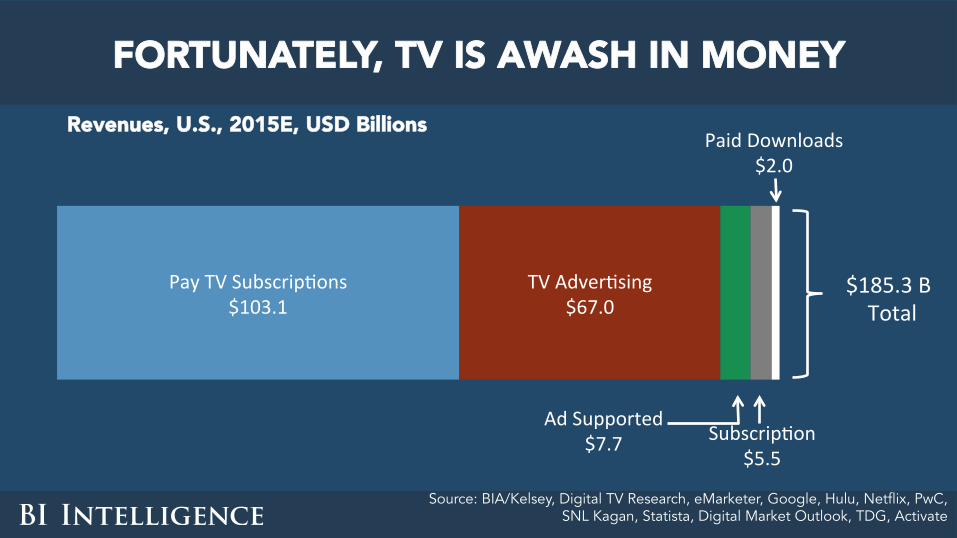

PayTVSubscripZons$103.1

TVAdverZsing$67.0

AdSupported$7.7 SubscripZon

$5.5

PaidDownloads$2.0

$185.3BTotal

FORTUNATELY, TV IS AWASH IN MONEY Revenues, U.S., 2015E, USD Billions

Source: BIA/Kelsey, Digital TV Research, eMarketer, Google, Hulu, Netflix, PwC, SNL Kagan, Statista, Digital Market Outlook, TDG, Activate

So they’ll suffer in style.

7. POWER AND WEALTH WILL BE MORE CONCENTRATED THAN EVER

$66.0

$48.8

$27.4

$13.8 $13.3 $12.5$5.5 $4.6 $3.2 $2.5 $1.6

Google Disney TimeWarner

CBS Viacom Facebook Neilix Yahoo Ganneb AOL NewYorkTimes

(Billions) -8.2%YoY

-9.7%YoY

-4.6%YoY

8.7%YoY

58.4%YoY

0.8%YoY

-3.7%YoY

10.3%YoY

8.4%YoY

25.8%YoY

-1.3%YoY

DIGITAL MEDIA IS THE NEW “BIG MEDIA” 2014 Revenue Select Media Companies

Source: Company Filings, BI Intelligence estimates

And “big media” companies are now distinctly medium-sized.

$233.7

$132.4 $127.1

$68.8 $66.0

Apple AT&T Verizon Comcast Google

Billion

s

27.9%YoY

2.9%YoY

5.4%YoY

6.4%YoY

10.3%YoY

THIS IS THE NEW “BIG” 2014 Revenue Select Media Companies

Source: Company Filings, BI Intelligence estimates

THANK YOU!

Sign up for BI Intelligence to get more content like this...

Subscribe to Business Insider’s research service to get rich analysis and key insights on today’s most relevant topics in the digital landscape:

http://read.bi/intelligence