7. Regression with a binary dependent variable Up to now: • Dependent variable Y has a metric scale (it can take on any value on the real line) In this section: • Y takes on either the value 1 or 0 (binary variable) • We aim at finding out and modeling which determinants (X - regressors) cause Y to take on the values 1 or 0 189

Transcript

7. Regression with a binary dependent variable

Up to now:

• Dependent variable Y has a metric scale(it can take on any value on the real line)

In this section:

• Y takes on either the value 1 or 0(binary variable)

• We aim at finding out and modeling which determinants (X-regressors) cause Y to take on the values 1 or 0

189

Examples:

• What is the effect of a tuition subsidy on an individual’sdecision to go to college (Y = 1)?

• Which factors determine whether a teenager takes up smok-ing (Y = 1)?

• What determines if a country receives foreign aid (Y = 1)?

• What determines if a job applicant is successful (Y = 1)?

190

Data set examined in this section:

• Boston Home Mortgage Disclosure Act (HMDA) data set

• Which factors determine whether a mortgage application isdenied (Y ≡ DENY = 1) or approved (Y ≡ DENY = 0)

• Potential factors (regressors):

The required loan payment (P ) relative to the applicantsincome (I):

X1 ≡ P/I RATIO

The applicant’s race

X2 ≡ BLACK =

{

1 if the applicant is black0 if the applicant is white

191

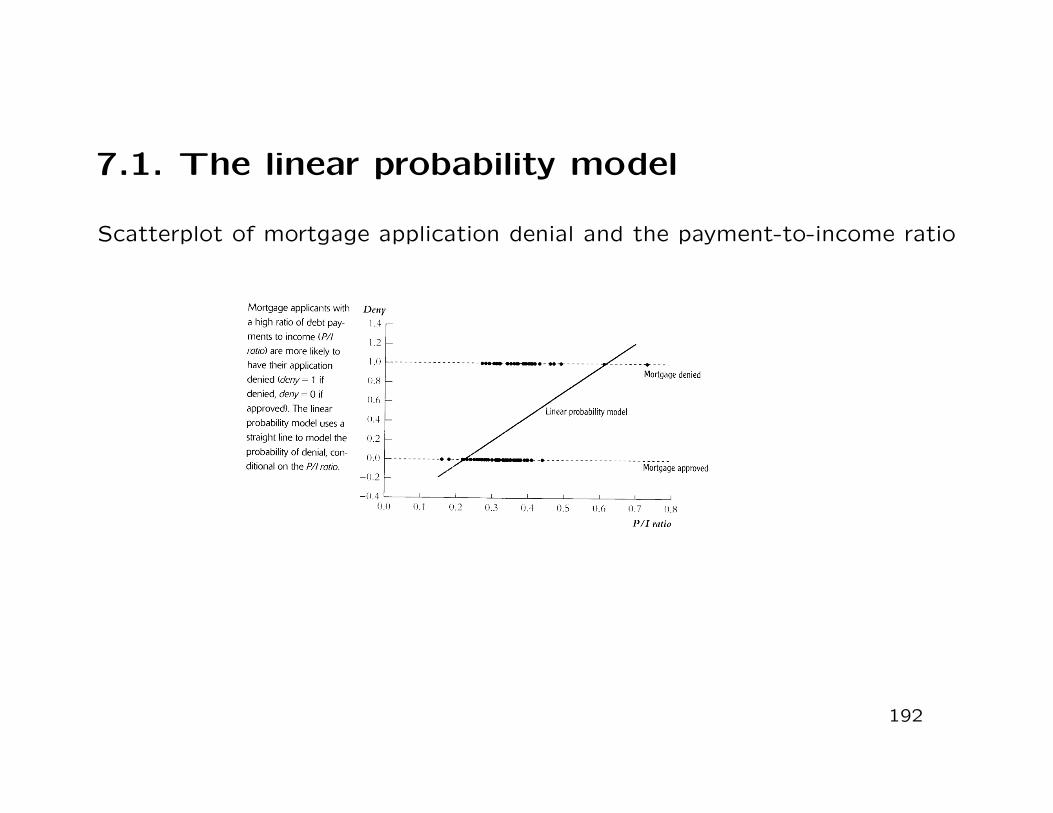

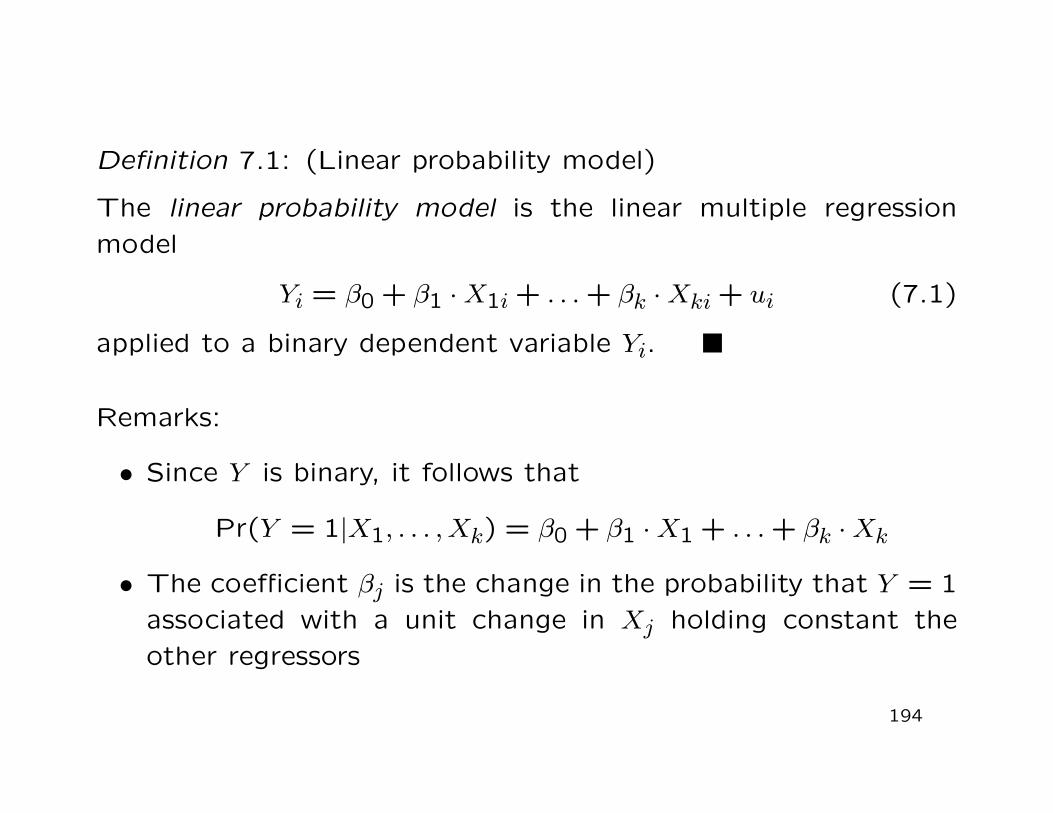

7.1. The linear probability model

Scatterplot of mortgage application denial and the payment-to-income ratio

192

Meaning of the OLS regression line:

• Plot of the predicted value of Y = DENY as a function of theregressor X1 = P/I RATIO

• For example, when P/I RATIO = 0.3 the predicted value ofDENY is 0.2

• The coefficient βj is the change in the probability that Y = 1associated with a unit change in Xj holding constant theother regressors

194

Remarks: [continued]

• The regression coefficients can be estimated by OLS

• The errors of the linear probability model are always het-eroskedastic

−→ Use heteroskedasticity-robust standard errors for confi-dence intervals and hypothesis tests

• The R2 is not a useful measure-of-fit(alternative measures-of-fit are discussed later)

195

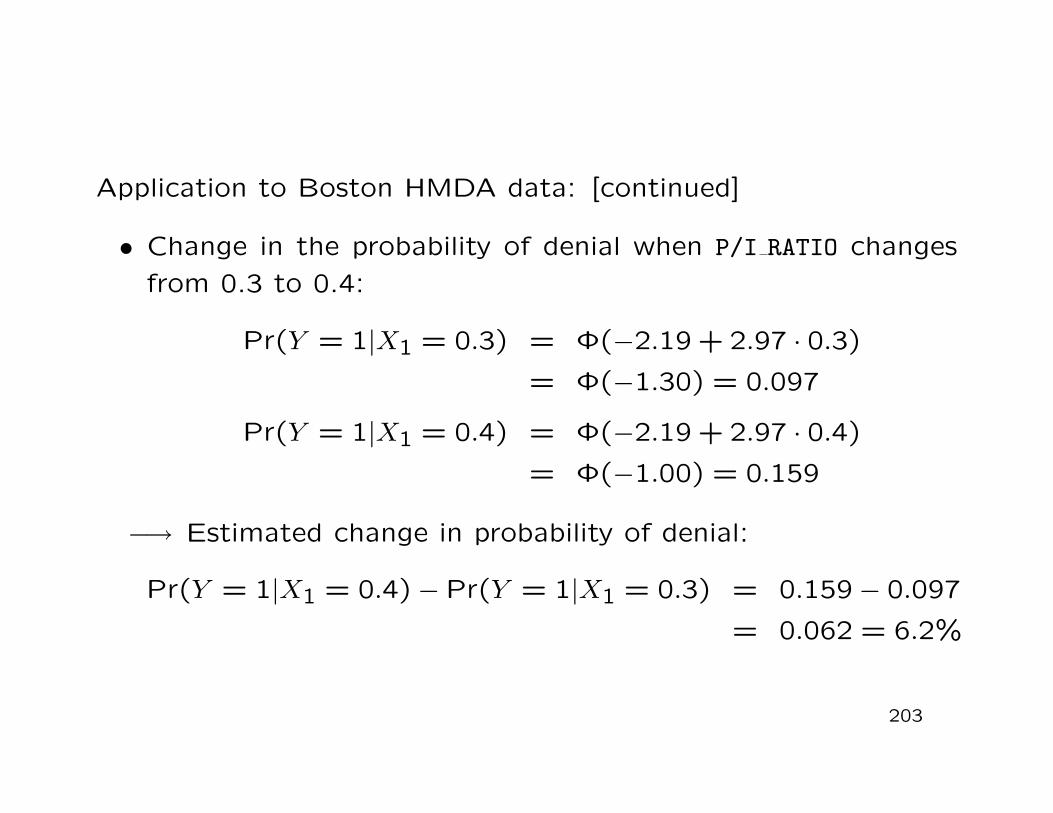

Application to Boston HMDA data:

• OLS regression of DENY on P/I RATIO yields

DENY = −0.080 + 0.604 · P/I RATIO

(0.032) (0.098)

• Coefficient on DENY is positive and significant at the 1% level

• If P/I RATIO increases by 0.1, the probability of denial in-creases by 0.604× 0.1 ≈ 0.060 = 6%(predicted change in the probability of denial given a changein the regressor)

196

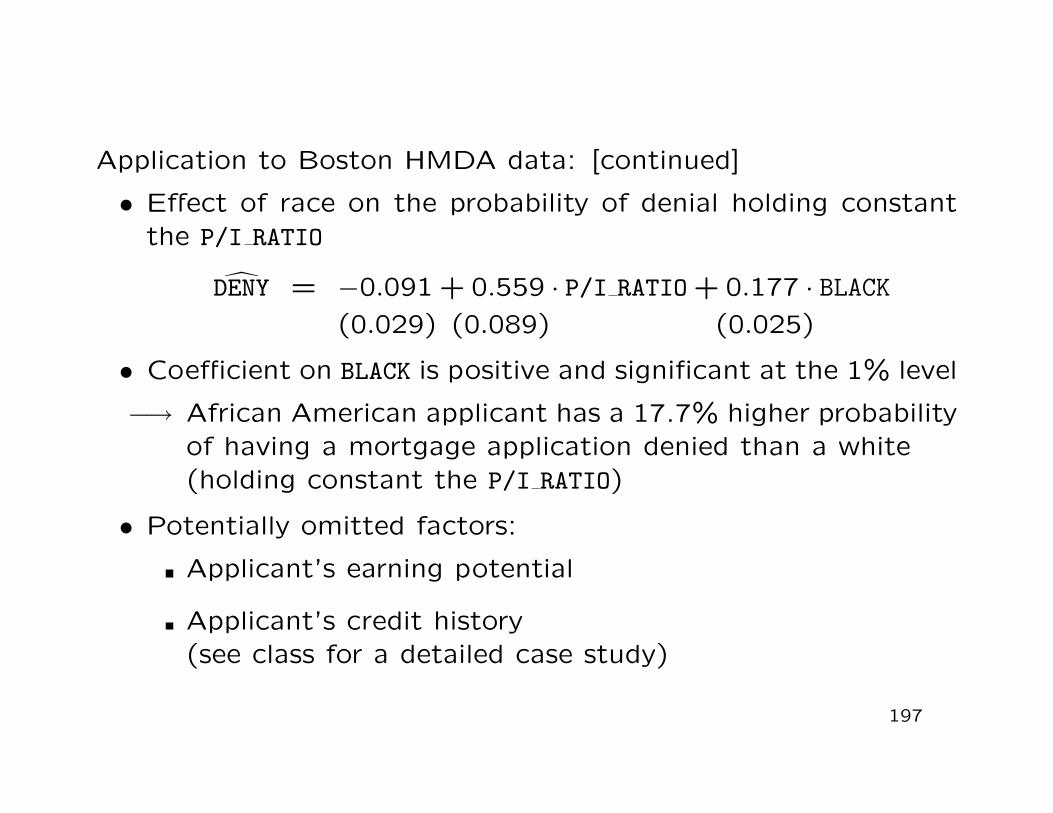

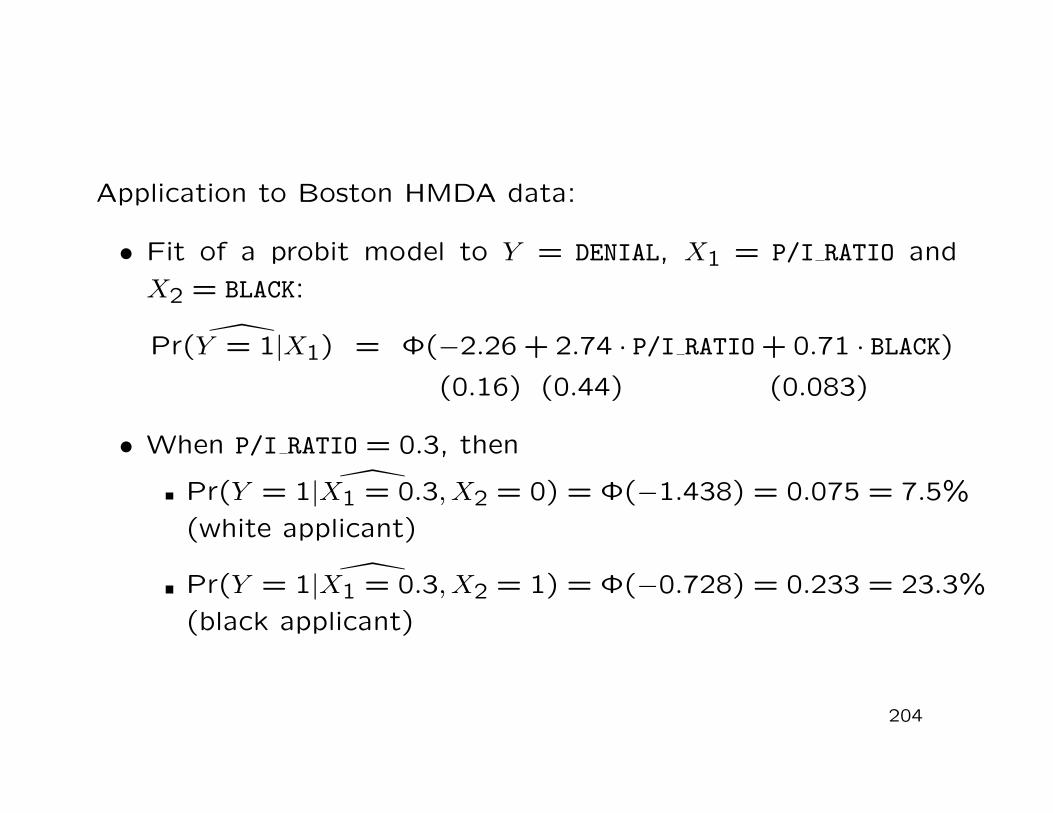

Application to Boston HMDA data: [continued]

• Effect of race on the probability of denial holding constantthe P/I RATIO

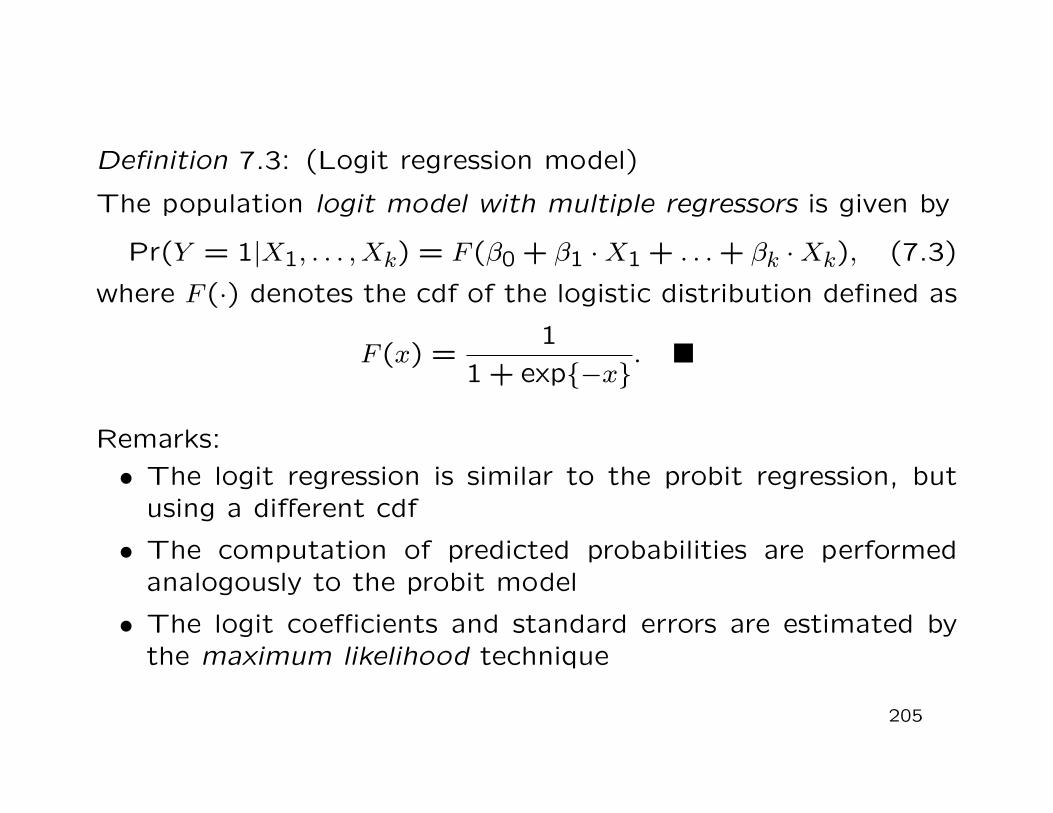

where F (·) denotes the cdf of the logistic distribution defined as

F (x) =1

1 + exp{−x}.

Remarks:• The logit regression is similar to the probit regression, but

using a different cdf

• The computation of predicted probabilities are performedanalogously to the probit model

• The logit coefficients and standard errors are estimated bythe maximum likelihood technique

205

Remarks: [continued]

• In practice, logit and probit regressions often produce similarresults

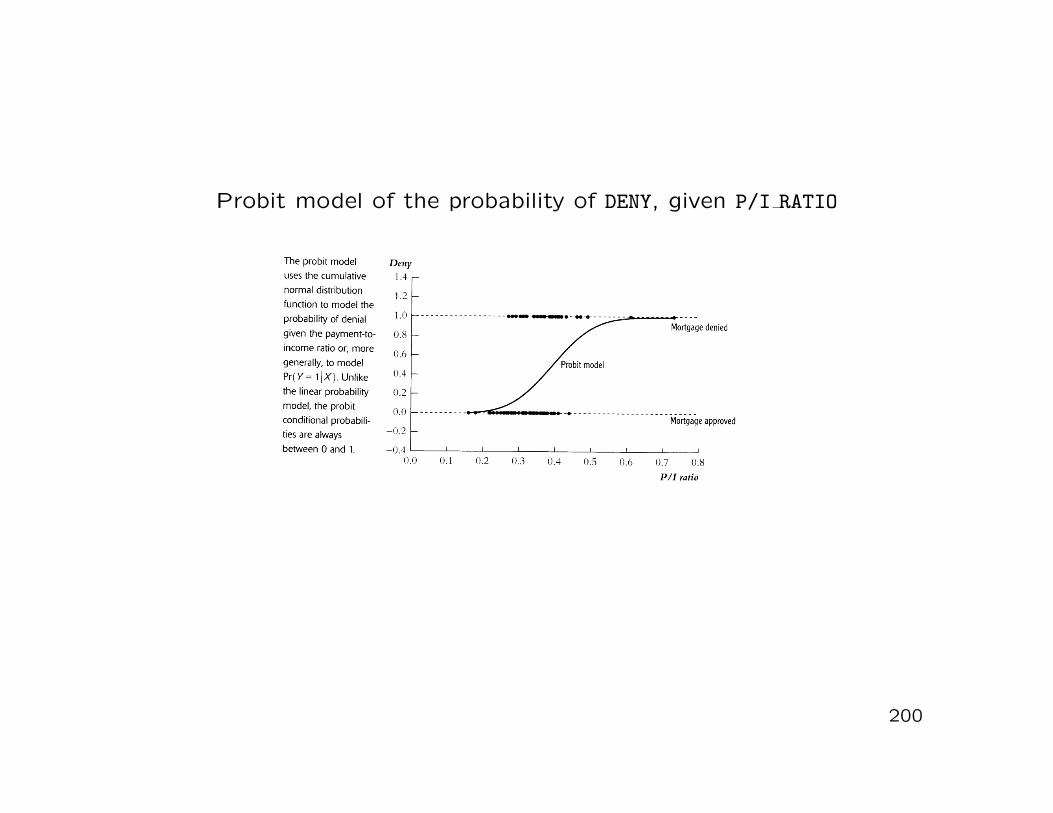

Probit and logit models of the probability of DENY, given P/I RATIO

206

7.3. Estimation and inference in the logit andprobit models

Alternative estimation techniques:

• Nonlinear least squares estimation by minimizing the sum ofsquared prediction mistakes:

n∑

i=1[Yi −Φ(b0 + b1X1i + . . . + bkXki)]

2 −→ minb0,...,bk

(7.4)

(see Eq. (2.2) on Slide 12)

• Maximum likelihood estimation

207

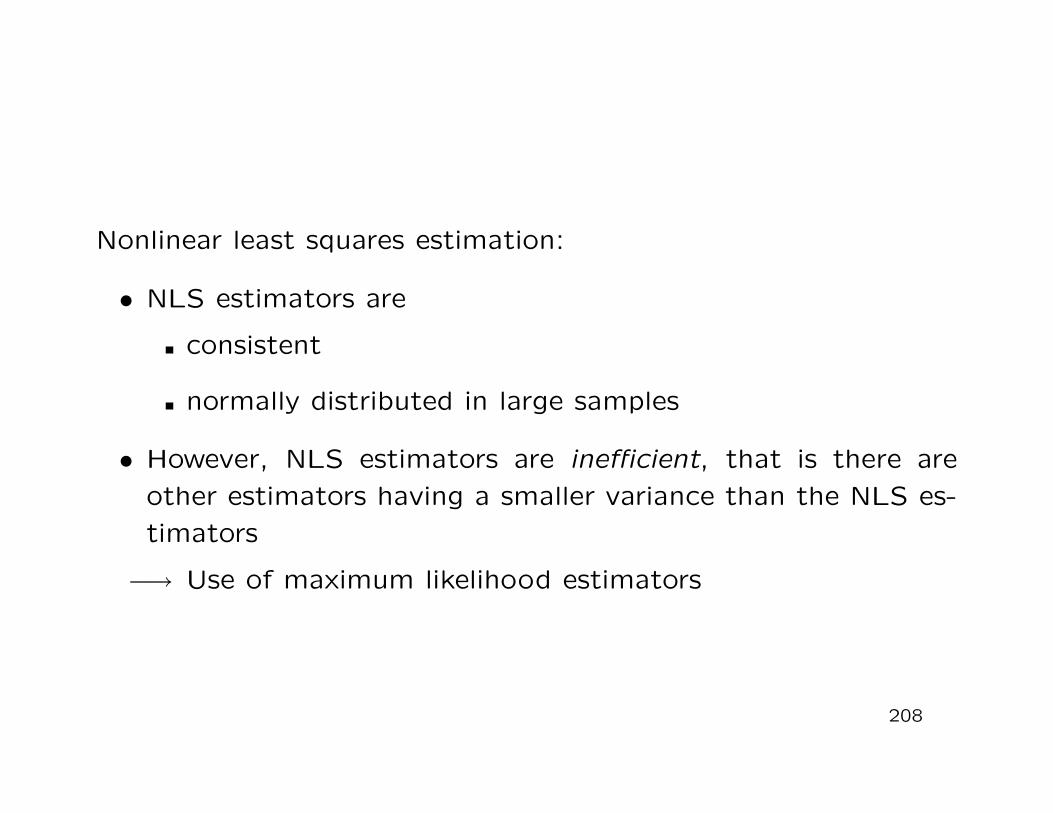

Nonlinear least squares estimation:

• NLS estimators are

consistent

normally distributed in large samples

• However, NLS estimators are inefficient, that is there areother estimators having a smaller variance than the NLS es-timators

−→ Use of maximum likelihood estimators

208

Maximum likelihood estimation:

• ML estimators are

consistent

normally distributed in large samples

• More efficient than NLS estimators

• ML estimation is discussed in the lecture Advanced Statistics

Statistical inference based on MLE:

• Since ML estimators are normally distributed in large sam-ples, statistical inference about probit and logit coefficientsbased on MLE proceeds in the same way as inference aboutthe linear regression functions coefficients based on the OLSestimator

209

In particular:

• Hypothesis tests are performed using the t- and F -statistics(see Sections 3.2.–3.4.)

• Confidence intervals are constructed according to Formula(3.3) on Slide 55

Measures-of-fit:

• The conventional R2 is inappropriate for probit and logit re-gression models

• Two frequently encountered measures-of-fit with binary de-pendent variables are the

Fraction correctly predicted

Pseudo-R2

210

Fraction correctly predicted:

• This measure-of-fit is based on a simple classification rule

• An observation Yi is said to be correctly predicted,

if Yi = 1 and Pr(Yi = 1|X1i, . . . , Xki) > 0.5 or

if Yi = 0 and Pr(Yi = 1|X1i, . . . , Xki) < 0.5

• Otherwise Yi is said to be incorrectly predicted

• The fraction correctly predicted is the fraction of the n ob-servations Y1, . . . , Yn that are correctly predicted

Pseudo-R2:

• The Pseudo-R2 compares values of the maximized likelihood-function with all regressors to the value of the likelihoodfunction with no regressor

211

Case study:

• Application to Boston HMDA data(see class)

Other limited dependent variable models:

• Censored and truncated regression models

• Sample selection models

• Count data

• Ordered responses

• Discrete choice data

• For details see Ruud (2000) and Wooldridge (2002)