NEW ISSUE - BOOK-ENTRY ONLY RATING: S&P:"AA-t" (See"RATING" herein) In the opinion ofThe Weist Law Firm Scotts Valley, California, Bond Counsel, subject, ho.vever to certain qualifications described in this Official Statem,nt, under existing law, interest on the Bonds is excluded from gross incorre for federal incorre tax purpose5i and such interest is ootan item of tax preference for purrx,ses of the federal alternative ninirrumtaxirrposed on individual sand corporations, although for the purpose of corrputing the alternative ninirrumtax irrposed on certain cor(Xlfations, such interest is taken into account in detemining certain incorre and earnings. In the further opinion of Bond Counsel, such interest is exerrpt from California personal income taxes See" TAX MATTERS" herein. Dated: Date of Delivery $7,685,00) PISMO BEACH PUBLIC Fl NANCI NG AGENCY (San Luis Obispo County, Califcrnia) SERIES 2017LEASE REVENUE BONDS (Pismo Beach Municipal Pier Prqject) Due: December 1, as shown on the Inside CCNer The abCNe-captioned Series 201 llease Revenue Bonds (the" Bonds") are being issued t,,, the Pismo Beach Public Financing Agency (the" Agency") pursuant to an Indenture, dated as of June I, 2017 (the" Indenture"), t,,, and between the Agency and Wilnington Trust, N.A., as trustee (the "Trustee"). The Bonds will bear interest at the rates shwn belw, payable seniannually on June I and December I of each year (each an" Interest Paym,ntDate"), comm,ncing December I, 2017. The Bonds are being issued as fully registered bonds, registered in the nam, of Cede & Co. as nominee of The Depository Trust Corrμuiy, New York, New York(" DTC"), and will be available to ultimate purchasers in the denonination of $5,000 or any integral multiple thereof, under the book-entry system maintained t,,, D TC. Purchasers ofB ands wi II not receive physical certificates representing their interest in the Bands. The Trustee will make paym,nts of the principal of, premium if any, and interest on the Bonds directly to DTC, or its noninee, Cede & Co., so long as DTC or Cede & Co. is the registered wner of the Bonds. Disbursements of such paym,nts to the Beneficial Owners of the Bonds is the responsibility of DTC' s Participants and Indirect Participants, as more fully described herein. See "THE BONDS- BOOK-ENTRY SYSTEM" herein. The Bonds are subject to optional, mandatory sinking account and extraordinary redemption prior to their stated maturities, as described herein. See "THE BONDS- Redemption Provisions" herein. The Bonds are being issued t,,, the Agency, to (i) finance the acquisition and construction of certain public capital imprcwem,nt~ and (ii) pay the costs of issuance associated with the issuance and sale of the Bonds See" PLAN OF FINANCE" herein. Pursuant to a Lease Agreem,nt, dated as of June I, 2017 (the" Lease"), t,,, and between the Agency and the City, the Agency has leased to the City certain real property and the improvem,nts thereon comprising the Pismo Beach City Hall and the Pismo Beach Police Station (the" Leased Facilities"). Under the Lease, the City will pay to the Agency certain base rental paym,nts (the" Base Rental Paym,nts") in armunts equal to the scheduled debt service on the Bands. Pursuant to the Indenture, the Agency will assign its right to receive the Base Rental Payments to the Trustee for the benefit of the Owners of the Bonds See "SECURITY FOR THE BONDS" herein. This cover page contains certain information for quick reference only and is not a summary of the security or terms of this issue. Potential investors are advised to read the entire Official Statement, including the section entitled" BOND OWNERS' RI SK S," to obtain information essential to the making of an informed investment decision with respect to the purchase of the Bonds. MATURITY SCHEDULE (See Inside Cover Page) The City is required under the Lease to make Base Rental Paym,nts in each year in consideration for the use of the Leased Facilities from any source of legally available fund~ and in an armunt sufficient to pay the annual principal of and interest on the Bonds. The City's obligation to make Base Rental Paym,nts is subject to abatement in the event of substantial interference with the use and possession of all or a part of the Leased Facilities. See "BOND OWNERS' RISKS - Abatem,nt' herein. The City has covenanted under the Lease to take such action as may be necessary to include and maintain all Base Rental Paym,nts in its annual budget and to make the necessary appropriations therefor, subject to such abatement NEITHER THE BONDS NOR THE OBLIGATION TO PAY PRINCIPAL OF OR INTEREST THEREON CONSTITUTES A DEBT, LIABILITY OR OBLIGATION OF THE AGENCY, THE CITY, THE STATE OF CALIFORNIA OR ANY OF ITS POLITICAL SUBDIVISIONS WITHIN THE MEANING OF ANY CONSTITUTIONAL LIMITATION ON INDEBTEDNESS, OR A PLEDGE OF THE FULL FAITH AND CREDIT OF THE CITY, BUT ARE SECURED SOLELY BY THE PLEDGE OF REVENUES, CONSISTING PRIMARILY OF BASE RENTAL PAYMENTS PAID BY THE CITY PURSUANT TO THE LEASE AND CERTAIN FUNDS HELD UNDER THE INDENTURE. THE BONDS ARE NOT SECURED BY A PLEDGE OF THE TAXING POWER OF THE CITY. The Bonds are offered when, as and if issued and accepted by the Underwriter, subject to the approving opinion of The Weist Law Firm Scotts Valley, California, Bond Counsel to the Agency. Certain legal matters will be passed on for theAgencyt,,,TheWeist Law Firm Scotts Valley, California, Disclosure Counsel, for the City and the Agency t,,, Hanley& Fleishman, LLP, Atascadero, California, as City Attorney and Agency Counsel, for the Underwriter byNi,on Peabody LLP, Los Angeles, California, and for the Trustee by its counsel. It is anticipated that the Bonds will be available for delivery through the book-entry facilities ofDTC on or aboutJ une 7, 2017. Dated: May 24, 2017

Transcript

NEW ISSUE - BOOK-ENTRY ONLY RATING: S&P:"AA-t" (See"RATING" herein)

In the opinion ofThe Weist Law Firm Scotts Valley, California, Bond Counsel, subject, ho.vever to certain qualifications described in this Official Statem,nt, under existing law, interest on the Bonds is excluded from gross incorre for federal incorre tax purpose5i and such interest is ootan item of tax preference for purrx,ses of the federal alternative ninirrumtaxirrposed on individual sand corporations, although for the purpose of corrputing the alternative ninirrumtax irrposed on certain cor(Xlfations, such interest is taken into account in detemining certain incorre and earnings. In the further opinion of Bond Counsel, such interest is exerrpt from California personal income taxes See" TAX MATTERS" herein.

Dated: Date of Delivery

$7,685,00) PISMO BEACH PUBLIC Fl NANCI NG AGENCY

(San Luis Obispo County, Califcrnia) SERIES 2017LEASE REVENUE BONDS

(Pismo Beach Municipal Pier Prqject)

Due: December 1, as shown on the Inside CCNer

The abCNe-captioned Series 201 llease Revenue Bonds (the" Bonds") are being issued t,,, the Pismo Beach Public Financing Agency (the" Agency") pursuant to an Indenture, dated as of June I, 2017 (the" Indenture"), t,,, and between the Agency and Wilnington Trust, N.A., as trustee (the "Trustee"). The Bonds will bear interest at the rates shwn belw, payable seniannually on June I and December I of each year (each an" Interest Paym,ntDate"), comm,ncing December I, 2017.

The Bonds are being issued as fully registered bonds, registered in the nam, of Cede & Co. as nominee of The Depository Trust Corrµuiy, New York, New York(" DTC"), and will be available to ultimate purchasers in the denonination of $5,000 or any integral multiple thereof, under the book-entry system maintained t,,, D TC. Purchasers ofB ands wi II not receive physical certificates representing their interest in the Bands. The Trustee will make paym,nts of the principal of, premium if any, and interest on the Bonds directly to DTC, or its noninee, Cede & Co., so long as DTC or Cede & Co. is the registered wner of the Bonds. Disbursements of such paym,nts to the Beneficial Owners of the Bonds is the responsibility of DTC' s Participants and Indirect Participants, as more fully described herein. See "THE BONDS- BOOK-ENTRY SYSTEM" herein.

The Bonds are subject to optional, mandatory sinking account and extraordinary redemption prior to their stated maturities, as described herein. See "THE BONDS- Redemption Provisions" herein.

The Bonds are being issued t,,, the Agency, to (i) finance the acquisition and construction of certain public capital imprcwem,nt~ and (ii) pay the costs of issuance associated with the issuance and sale of the Bonds See" PLAN OF FINANCE" herein.

Pursuant to a Lease Agreem,nt, dated as of June I, 2017 (the" Lease"), t,,, and between the Agency and the City, the Agency has leased to the City certain real property and the improvem,nts thereon comprising the Pismo Beach City Hall and the Pismo Beach Police Station (the" Leased Facilities"). Under the Lease, the City will pay to the Agency certain base rental paym,nts (the" Base Rental Paym,nts") in armunts equal to the scheduled debt service on the Bands. Pursuant to the Indenture, the Agency will assign its right to receive the Base Rental Payments to the Trustee for the benefit of the Owners of the Bonds See "SECURITY FOR THE BONDS" herein.

This cover page contains certain information for quick reference only and is not a summary of the security or terms of this issue. Potential investors are advised to read the entire Official Statement, including the section entitled" BOND OWNERS' RI SK S," to obtain information essential to the making of an informed investment decision with respect to the purchase of the Bonds.

MATURITY SCHEDULE (See Inside Cover Page)

The City is required under the Lease to make Base Rental Paym,nts in each year in consideration for the use of the Leased Facilities from any source of legally available fund~ and in an armunt sufficient to pay the annual principal of and interest on the Bonds. The City's obligation to make Base Rental Paym,nts is subject to abatement in the event of substantial interference with the use and possession of all or a part of the Leased Facilities. See "BOND OWNERS' RISKS -Abatem,nt' herein. The City has covenanted under the Lease to take such action as may be necessary to include and maintain all Base Rental Paym,nts in its annual budget and to make the necessary appropriations therefor, subject to such abatement

NEITHER THE BONDS NOR THE OBLIGATION TO PAY PRINCIPAL OF OR INTEREST THEREON CONSTITUTES A DEBT, LIABILITY OR OBLIGATION OF THE AGENCY, THE CITY, THE STATE OF CALIFORNIA OR ANY OF ITS POLITICAL SUBDIVISIONS WITHIN THE MEANING OF ANY CONSTITUTIONAL LIMITATION ON INDEBTEDNESS, OR A PLEDGE OF THE FULL FAITH AND CREDIT OF THE CITY, BUT ARE SECURED SOLELY BY THE PLEDGE OF REVENUES, CONSISTING PRIMARILY OF BASE RENTAL PAYMENTS PAID BY THE CITY PURSUANT TO THE LEASE AND CERTAIN FUNDS HELD UNDER THE INDENTURE. THE BONDS ARE NOT SECURED BY A PLEDGE OF THE TAXING POWER OF THE CITY.

The Bonds are offered when, as and if issued and accepted by the Underwriter, subject to the approving opinion of The Weist Law Firm Scotts Valley, California, Bond Counsel to the Agency. Certain legal matters will be passed on for theAgencyt,,,TheWeist Law Firm Scotts Valley, California, Disclosure Counsel, for the City and the Agency t,,, Hanley& Fleishman, LLP, Atascadero, California, as City Attorney and Agency Counsel, for the Underwriter byNi,on Peabody LLP, Los Angeles, California, and for the Trustee by its counsel. It is anticipated that the Bonds will be available for delivery through the book-entry facilities ofDTC on or aboutJ une 7, 2017.

Dated: May 24, 2017

DATES, PRINCIPAL AMOUNTS, INTEREST RATES AND YIELDS

$7,685,000 PISMO BEACH PUBLIC FINANCING AGENCY

(San Luis Obispo County, California) SERIES 2017 LEASE REVENUE BONDS

(Pismo Beach Municipal Pier Project)

MATURITY SCHEDULE (Base CUSIPt No. 72433P)

Maturity Date Principal Interest (December 12 Amount Rate Yield Price cusIPt

PISMO BEACH PUBLIC FINANCING AGENCY Pismo Beach, Califontla

AGENCY BOARD/ CITY COUNCIL

Ed Waage, Chair/Mayor Erik Howell, Vice-Chair/Mayor Pro Tempore Sheila Blake, Agency M ember!Counci /member

Marcia Guthrie, Agency Member!Councilmember Mary Ann Reiss, Agency Member!Councilmember

CITY I AGENCY STAFF

James R. Lewis, City Manager/Executive Director Nadia K. Feeser, Administrative Services Director/Treasurer

Susan West-Jones, Finance Manager Benjamin A. Fine, Public Works Director/City Engineer

Eric Eldridge, Senior Engineer Erica Inderlied, City Clerk/Secretary

Hanley & Fleishman, LLP, City Attorney/Agency Counsel

PROFESSIONAL SERVICES

Bond Counsel and Disclosure Counsel

The Weist Law Firm Scotts Valley, California

Municipal Advisor

Urban Futures, Incorporated Tustin, California

Trustee

Wilmington Trust, N.A. Costa Mesa, California

In making an investment decision investors must rely on their own examination of the terms of the offering, including the merits and risks involved. These securities have not been recommended by any federal or state securities commission or regulatory authority. Furthermore, neither the foregoing authorities nor Bond Counsel or Disclosure Counsel have confirmed the accuracy or determined the adequacy of this document. Any representation to the contrary is a criminal offense.

No dealer, broker, salesperson or other person has been authorized by the Agency or City to provide any information or to make any representations in connection with the offering or sale of the Bonds other than as contained herein and, if given or made, such other information or representation must not be relied upon as having been authorized by the Agency or City. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. All references to and summaries of the Indenture or other documents contained in this Official Statement are subject to the provisions of those documents and do not pmport to be complete statements of those documents.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matter of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as a representation of facts. Words or phrases "will likely result," "are expected to," "will continue," "is anticipated," "estimate," "project," "forecast," "expect," "intend" and similar expressions identify "forward looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other pmpose, unless authorized in writing by the Agency or City.

The Underwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as a part of its responsibilities to investors under the federal securities laws applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information set forth herein has been obtained from sources which are believed to be reliable, but it is not guaranteed as to accuracy or completeness. The information and expression of opinion herein are subj eel to change without notice and neither delivery of this Official Statement nor any sale made under the Indenture shall, under any circumstances, create any implication that there has been no change in the affairs of the Agency or City since the date hereof.

TI-IE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEi\!IPTION CONTAINED IN SUCH ACT. TI-IE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER TI-IE SECURITIES LAWS OF ANY STATE.

IN CONNECTION WITH TI-IE OFFERING OF TI-IE BONDS, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREY AIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. TI-IE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERS AND DEALER BANKS AND BANKS ACTING AS AGENT AND OTHERS AT PRICES LOWER THAN TI-IE PUBLIC OFFERING PRICES STATED ON THE COVER PAGE HEREOF AND SAID PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TO TIME BY TI-IE UNDERWRITER.

Purpose of Official Statement .................................................................................................................. 1 Authority for Issuance of the Bonds ......................................................................................................... 1 Purpose of the Bonds ................................................................................................................................ 1 Security for the Bonds .............................................................................................................................. 2 No Debt Service Reserve ......................................................................................................................... 3 The City .................................................................................................................................................... 3 The Agency .............................................................................................................................................. 3 Description of the Bonds .......................................................................................................................... 4 Additional Bonds ...................................................................................................................................... 4 Continuing Disclosure .............................................................................................................................. 4 Tax Matters .............................................................................................................................................. 5 Forward-Looking Statements ................................................................................................................... 5 Risk Factors .............................................................................................................................................. 5 Further Information .................................................................................................................................. 5

PLAN OF FINANCE ....................................................................................................................................... 6

~~~ 6 Estimated Sources and Uses of Bond Proceeds ....................................................................................... 7 Debt Service Requirements ...................................................................................................................... 8

THE LEASED FACILITIES ........................................................................................................................... 9

Description ............................................................................................................................................... 9 Estimated Values of the Leased Facilities ................................................................................................ 9 Modifications of Leased Facilities ......................................................................................................... 10 Subleasing of Leased Facilities .............................................................................................................. 10 Substitution or Release of Leased Facilities ........................................................................................... 10

THE BONDS .................................................................................................................................................. 11

Authority for Issuance ............................................................................................................................ 11 General Provisions ................................................................................................................................. 11 Redemption Provisions .......................................................................................................................... 13 Book-Entry System ................................................................................................................................ 15

SECURITY FOR THE BONDS .................................................................................................................... 15

General ................................................................................................................................................... 15 Revenues ................................................................................................................................................ 15 Base Rental Payments ............................................................................................................................ 16 Lease Payments; Covenant to Appropriate ............................................................................................ 16 Budget and Appropriation of Base Rental Payments ............................................................................. 16 Abatement .............................................................................................................................................. 17 Insurance ................................................................................................................................................ 17 No Debt Service Reserve ....................................................................................................................... 18 Additional Bonds .................................................................................................................................... 19 Maintenance, Utilities, Taxes and Assessments ..................................................................................... 21

TABLE OF CONTENTS (Cont.)

THE AGENCY .............................................................................................................................................. 22

THE CITY ...................................................................................................................................................... 22

General ................................................................................................................................................... 22

CITY FINANCIAL INFORMATION ........................................................................................................... 24

Budget Process ....................................................................................................................................... 24 Financial Reporting ................................................................................................................................ 27 General Fund Revenues and Expenditure .............................................................................................. 27 Transient Occupancy Tax ....................................................................................................................... 29 Property Taxes ........................................................................................................................................ 29 Sales Taxes ............................................................................................................................................. 32 Financial Statements .............................................................................................................................. 34 General Fund Historical Financial Data ................................................................................................. 34 Relevant Fiscal Policies ......................................................................................................................... 37 Risk Management. .................................................................................................................................. 39 Employee Retirement System; CalPERS ............................................................................................... 41 Other Post-Employment Benefits ("OPEB") ......................................................................................... 49

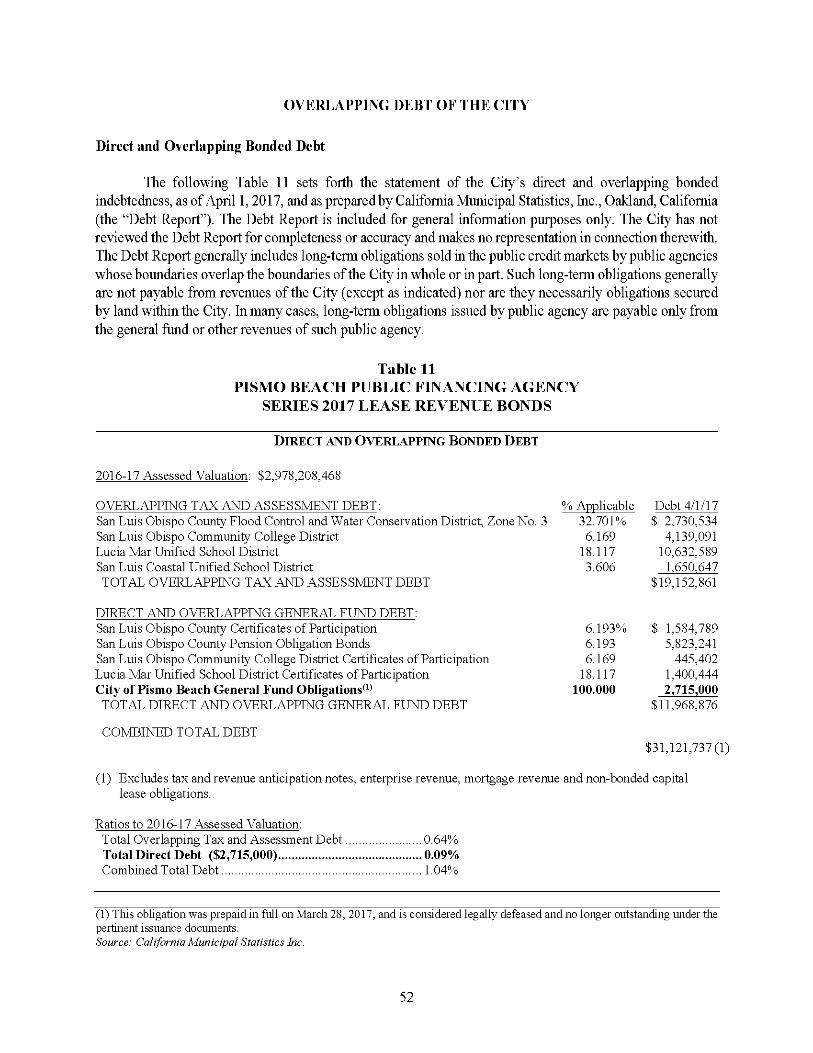

OVERLAPPING DEBT OF THE CITY ....................................................................................................... 52

Direct and Overlapping Bonded Debt .................................................................................................... 52

BOND OWNERS' RISKS ............................................................................................................................. 53

Future Financial Condition ..................................................................................................................... 53 Additional Obligations of the City ......................................................................................................... 53 Substitution or Release of Leased Facilities; Additional Bonds ............................................................ 53 Base Rental Payments Are Not Debt ..................................................................................................... 54 Abatement .............................................................................................................................................. 5 5 Risk of Uninsured Loss .......................................................................................................................... 55 Accuracy of Assumptions ...................................................................................................................... 5 5 Eminent Domain .................................................................................................................................... 56 Hazardous Substances ............................................................................................................................ 56 Nuclear Power Plant ............................................................................................................................... 56 Closure of DCPP .................................................................................................................................... 57 Bankruptcy ............................................................................................................................................. 5 8 No Liability of Agency to the Owners ................................................................................................... 59 State Budget Information ....................................................................................................................... 59 Risks Related to Taxation in California ................................................................................................. 60 Future Initiatives .................................................................................................................................... 64 Limitations on Remedies ........................................................................................................................ 64 Limited Recourse on Default; No Acceleration of Base Rental Payments ............................................ 64 Early Redemption Risk .......................................................................................................................... 65 Natural Disasters .................................................................................................................................... 65 Possible Insufficiency of Insurance Proceeds ........................................................................................ 65 Loss of Tax Exemption .......................................................................................................................... 66 IRS Audit of Tax-Exempt Bonds ........................................................................................................... 66

APPENDIXC FORM OF CONTINUING DISCLOSURE CERTIFICATE . C-1

APPENDIXD GENERAL INFORMATION REGARDING THE CITY OF PISMO BEACH AND SURROUNDING AREA D-1

APPENDIXE FORM OF OPINION OF BOND COUNSEL .E-1

APPENDIXF DTC AND THE BOOK-ENTRY ONLY SYSTEM . F-1

111

OFFICIAL STATEMENT

$7,685,000 PISMO BEACH PUBLIC FINANCING AGENCY

(San Luis Obispo County, California) SERIES 2017 LEASE REVENUE BONDS

(Pismo Beach Municipal Pier Project)

INTRODUCTION

This introduction contains only a brief summary of certain of the terms of the Bonds, and a brief overview of the contents of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement, including the cover page and appendices hereto, and the documents summarized or described herein. A full review should be made of the entire Official Statement including the Appendices hereto.

The offering of the Bonds to potential investors is made only by means of the entire Official Statement. Capitalized terms used and not otherwise defined in the body of the Official Statement shall have the meanings given to them in ''APPENDIX A - SUMMARY OF PRINCIPAL LEGAL DOCUMENTS" hereto.

Purpose of Official Statement

This Official Statement, which includes the cover page and the appendices hereto, is provided to furnish information in connection with the sale by the Pismo Beach Public Financing Agency (the "Agency") of its Series 2017 Lease Revenue Bonds (Pismo Beach Municipal Pier Project) (the "Bonds") in the aggregate principal amount of $7,685,000. Certain capitalized terms used herein are defined in "APPENDIX A -SUMMARY OF PRINCIPAL LEGAL DOCUMENTS- Definitions."

Authority for Issuance of the Bonds

The Bonds are issued pursuant to the provisions of the Marks-Roos Local Bond Pooling Act of 1985, constituting Article 4 of the Act (commencing with Section 6584) (the "Bond Law"), a Resolution adopted by the Board of Directors of the Agency on May 16, 2017 (the "Agency Resolution"), a Resolution adopted by the City Council of the City of Pismo Beach (the "City") on May 16, 2017 (the "City Resolution," and together with the Agency Resolution, the "Resolutions"), and an Indenture (the "Indenture"), dated as June 1, 2017, by and between the Agency and Wilmington Trust, N.A., as trustee (the "Trustee").

Purpose of the Bonds

The Bonds are being issued to provide funds to (i) finance the acquisition and construction of certain public capital improvements, and (ii) pay the costs of issuance associated with the issuance and sale of the Bonds. See "PLAN OF FINANCE" herein.

I

Security for the Bonds

Pursuant to a Site Lease, dated as of June 1, 2017 (the "Site Lease"), by and between the City and the Agency, the Agency has agreed to lease from the City certain real property and the improvements thereon, more commonly known as the (i) City of Pismo Beach City Hall located at 760 Mattie Road, Pismo Beach, California, and (ii) City of Pismo Beach Police Department located at 1000 Bello Street, Pismo Beach, California (collectively, the "Leased Facilities"), in exchange for a portion of the proceeds from the sale of the Bonds. Pursuant to a Lease Agreement, dated as of June 1, 2017 (the "Lease"), by and between the Agency, as Lessor, and the City, as Lessee, the Agency has leased the Leased Facilities back to the City. Under the Lease, the City will pay to the Agency certain base rental payments (the "Base Rental Payments") in amounts equal to the scheduled debt service on the Bonds. See "LEASED FACILITIES" herein.

The Bonds are special obligations of the Agency secured by and payable solely from Revenues, defined in the Indenture as all amounts received by the Agency as lessor under the Lease, including, without limiting the generality of the foregoing, scheduled Base Rental Payments, prepayments, and insurance and condemnation proceeds, and all interest, profits or other income derived from the investment of amounts in any fund or account established under the Indenture. Under the Lease, the City has covenanted and agreed, subject to abatement, to budget and appropriate from its General Fund amounts sufficient to make Base Rental Payments. The obligation of the City to make Base Rental Payments under the Lease is an unsecured obligation of the City, payable from legally available funds. See "SECURITY FOR THE BONDS" herein.

Pursuant to an Assignment Agreement, dated as of June 1, 2017 (the "Assignment Agreement"), by and between the Agency and the Trustee relating to the Bonds the Agency will assign, as further security for its obligations to make timely payment of principal of and interest on the Bonds to the Trustee for the benefit of the Owners certain of the Agency's rights under the Lease, including the right to receive Base Rental Payments and the right to exercise any remedies provided in the Lease in the event of a default by the City thereunder.

Under the Lease, in addition to Base Rental Payments, the City has agreed to pay Additional Rental payments in such amounts in each year as shall be required for the payment of all costs and expenses (not otherwise paid for or provided for out of the proceeds of sale of the Bonds) incurred by the Agency or the Trustee in connection with the execution, performance or enforcement of the Lease or the assignment thereof, the Indenture, or the Agency's or the Trustee's interest in the Leased Facilities.

Pursuant to the Indenture, the Agency transfers in trust, grants a security interest in and assigns to the Trustee, for the benefit of the Bondowners, all of the Revenues and other assets pledged under the Indenture, except only amounts required for the compensation or indemnification of the Trustee as provided in the Indenture, and all of the Agency's rights under the Lease, including its right to receive Base Rental Payments, but excluding the right to receive Additional Rental ( defined herein).

Under the Lease, the City has the right to substitute alternate real property or improvements for the Leased Facilities, release existing property or add additional real property or equipment to the Leased Facilities.

2

The obligation of the City to make Base Rental Payments under the Lease is an unsecured obligation of the City, payable from legally available funds. Under the Lease, the City has covenanted to budget and appropriate sufficient funds to make all rental payments required to be made under the Lease, subject only to abatement as provided therein. See "BOND OWNERS' RISKS - Base Rental Payments Are Not Debt" and "- Abatement" herein.

Neither the Bonds nor the obligation to pay principal of or interest thereon constitutes a debt, obligation or liability of the City, the County San Luis Obispo (the "County"), the State of California or any of its political subdivisions within the meaning of any Constitutional limitation on indebtedness, or a pledge of the full faith and credit of the City, but are secured solely by the pledge of Revenues by the Agency and certain funds held under the Indenture. The Bonds are not secured by a pledge of the taxing power of the City.

No Debt Service Reserve

Neither the City nor the Authority have undertaken to fund any debt service reserve to secure the payment of debt service on the Bonds.

The City

The City of Pismo Beach is located in the central coast area of California in the southern portion of San Luis Obispo County. It sits astride Highway 101 approximately eight miles south of the City of San Luis Obispo. Pismo Beach is approximately 196 miles north of Los Angeles and approximately 249 miles south of San Francisco. The City is a popular resort community situated directly on the Pacific Ocean and extends to the east into the foothills of the coast range mountains. Temperatures are mild year-round, with average highs between 60 and 80 degrees, and average lows between 45 and 55 degrees. Average annual rainfall, mostly occurring between December and March, is approximately 15 inches per year. See THE CITY" and "APPENDIX D - GENERAL INFORMATION REGARDING THE CITY OF PISMO BEACH AND SURROUNDING AREA" herein.

The Agency

The Pismo Beach Public Financing Agency is a joint powers authority formed by its members, the City and Industrial Development Authority of the City of Pismo Beach (the "Authority"). The Agency was established pursuant to that certain Joint Exercise of Powers Agreement dated May 2, 2017, by and between the City and the Authority (the "JPA Agreement"). Such JP A Agreement was entered into pursuant to the provisions of Articles 1, 2 and 4 of Chapter 5 of Division 7 of Title 1 of the California Government Code. The Agency is governed by a five-member Board of Directors (the "Board"), which consists of the members of the City Council of the City.

The Agency was created for the purpose of assisting the financing or refinancing of certain public capital facilities within the City. Under the Bond Law, the Agency has the power to purchase bonds issued by any local agency at public or negotiated sale and may sell such bonds to public or private purchasers at public or negotiated sale. See "THE AGENCY" herein.

3

Description of the Bonds

Payment. Principal of the Bonds will be payable in each of the years and in the amounts set forth on the front cover hereof at the principal corporate office of the Trustee in Costa Mesa, California. Interest on the Bonds will be paid by check of the Trustee mailed on the interest payment date by first class mail to the person entitled thereto. Initially, interest on and principal and premium, if any, of the Bonds will be payable when due by wire of the Trustee to DTC which will in tum remit such interest, principal and premium, if any, to DTC Participants (as defined herein), which will in tum remit such interest, principal and premium, if any, to Beneficial Owners (as defined herein) of the Bonds. See "THE BONDS - Book-Entry System" herein.

Redemption. The Bonds are subject to optional, extraordinary and mandatory sinking account redemption prior to their stated maturity dates, as provided herein. See "THE BONDS - Redemption Provisions" herein.

Form of Bonds. The Bonds will be issued in fully registered form, without coupons, in the minimum denominations of $5,000 or any integral multiple thereof. Any Bond may, in accordance with its terms, be transferred or exchanged, pursuant to the provisions of the Indenture. See "THE BONDS - General" herein. When delivered, the Bonds will be registered in the name of The Depository Trust Company, New York, New York ("DTC"), or its nominee. DTC will act as securities depository for the Bonds. Purchasers of the Bonds will not receive certificates representing the Bonds purchased. See "THE BONDS - Book-Entry System" herein.

Additional Bonds

Pursuant to the Indenture and the Lease, the Agency may issue additional bonds, notes or other indebtedness (the "Additional Bonds") payable from Revenues on a parity with the Bonds so long as no default has occurred and is continuing under the Indenture, the Site Lease or the Lease and provided that certain conditions set forth in the Indenture have been satisfied. In addition, the City may issue or incur other obligations payable from the City's General Fund. See "SECURITY FOR THE BONDS-Additional Bonds" herein.

Continuing Disclosure

The City will covenant for the benefit of owners of the Bonds to provide certain financial information and operating data relating to the City by the date that is nine months after the end of the City's Fiscal Year (currently March 31 based on the City's Fiscal Year end of June 30), commencing with the report for the fiscal year ended June 30, 2017 (the "Annual Report"), and to provide notices of the occurrence of certain enumerated events. Such reports are required to be filed with the Municipal Securities Rulemaking Board through its Electronic Municipal Market Access system ("EMMA").

The specific nature of the information to be contained in the Annual Report or the notices of enumerated events is described in "APPENDIX C - FORM OF CONTINUING DISCLOSURE CERTIFICATE" attached to this Official Statement. These covenants have been made in order to assist the Underwriter in complying with Securities Exchange Commission Rule 15c2 12(b)(5) (the "Rule"). See "CONTINUING DISCLOSURE" herein.

4

Tax Matters

Assuming compliance with certain covenants and provisions of the Internal Revenue Code of 1986, as amended (the "Tax Code"), in the opinion of Bond Counsel, interest with respect to the Bonds will not be includable in gross income for federal income tax purposes although it may be includable in the calculation for certain taxes. Also in the opinion of Bond Counsel, interest on the Bonds will be exempt from State of California (the "State") personal income taxes. See "TAX MATTERS" herein.

Forward-Looking Statements

Certain statements included or incorporated by reference in this Official Statement constitute "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27 A of the United States Securities Act of 1933, as amended. Such statements are generally identifiable by the terminology used such as "plan," "intend," "expect," "propose," "estimate," "project," "budget," "anticipate," or other similar words. The achievement of certain results or other expectations contained in such forwardlooking statements involves known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements described to be materially different from any future results, performance, or achievements expressed or implied by such forward-looking statements. The presentation of information herein, including tables of receipt of revenues, is intended to show recent historical information and, except for a budget discussion for Fiscal Year 2016-17, is not intended to indicate future or continuing trends in the financial position or other affairs of the City. No representation is made that past experience, as it might be shown by such financial and other information, will necessarily continue or be repeated in the future. See "BOND OWNERS' RISKS -Accuracy of Assumptions" herein.

NO UPDATES OR REVISIONS TO THESE FORWARD-LOOKING STATEMENTS ARE EXPECTED TO BE ISSUED IF OR WHEN THE EXPECTATIONS, EVENTS, CONDITIONS, OR CIRCUMSTANCES ON WHICH SUCH STATEMENTS ARE BASED CHANGE. THE FORWARDLOOKING STATEMENTS IN THIS OFFICIAL STATEMENT ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE EXPRESSED IN OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. READERS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON SUCH FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE HEREOF.

Risk Factors

The purchase of the Bonds involves certain risks. For a general discussion of certain special factors and considerations relevant to an investment in the Bonds, in addition to the other matters set forth herein, see "BONDOWNERS' RISKS" herein. The Bonds are not appropriate investments for investors who are not able to bear the associated risks. Investors should read the entire Official Statement to obtain information essential to the making of an informed investment decision.

Further Information

Brief descriptions of the Bonds, the Indenture, the Lease, the Site Lease, the Assignment Agreement and other documents agreements and statutes referred to in this Official Statement as well as the description

5

of the Bonds, do not purport to be comprehensive or definitive. Such summaries, references and descriptions are qualified in their entireties by reference to each such document or statute. For definitions of certain capitalized terms used herein and not otherwise defined, and a description of certain terms relating to the Bonds, see "APPENDIX A- SUMMARY OF PRINCIPAL LEGAL DOCUMENTS" herein.

PLAN OF FINANCE

The Project

The Agency will fund the Project Fund, in the amount set forth in Table 1 below, from the proceeds of the Bonds to partially fund the rehabilitation and renovation of the Pismo Beach Municipal Pier, which work includes upgrading the existing timber piles with steel piles; replacing the timber braces, decking, and handrails; and cleaning and recoating the existing steel piles and steel pile caps, a new electrical system, waterline for fire protection, upgraded lighting, benches, tables and other public amenities (the "Project"). The maintenance and repairs will not expand the Pier beyond the existing configuration and footprint with one exception at the entrance where a new PG&E electrical box will be located.

The estimated construction cost is approximately $8.8 million, and will be funded by the City through a combination of sources from transient occupancy taxes, sales tax, general fund revenues, and bond proceeds. Work will be performed in a series of phases and is anticipated to be completed by Fall of 2019.

The Pier, in its current location, was originally constructed in 1924. Since that time the Pier has suffered damage during several storms. A partial collapse of the Pier in 1983 prompted the State to reconstruct a portion of it in 1985. Sections of the Pier are more than 90 years old and, in a comprehensive structural inspection performed in 2015, it was recommended that several areas of the of the Pier be rehabilitated. This prompted the City to be proactive and address the Pier issues prior to any structural failures.

The Pier measures approximately 1,200 feet in overall length and varies in width from approximately 32 feet to more than 182 feet. The Pier is made up of both timber and steel piles. It is comprised of approximately 497 piles: 382 timber piles and 115 steel piles. The steel piles are located at the most seaward end of the Pier between the 51st and 72nd bents (rows of supports). The deck area is approximately 60,100 square feet and there is approximately 2,840 lineal feet of guard railing. The Pier includes cantilevered fishing decks, four widened diamond-shaped pop-outs, and one tapered section giving the Pismo Pier its unique and iconic shape. In addition to pedestrian and restricted vehicular traffic, the Pier supports electrical utility conduit, water and sewer piping, a bait shack, and an information kiosk.

The Pier is a popular venue for events and ceremonies for residents and visitors, hosting just under a million visitors a year, and is a symbol of Pismo Beach and its Classic California culture. This project is plarmed by the City to be part of a series of future projects that will transform the downtown, waterfront, and public parks in Pismo Beach.

6

Estimated Sources and Uses of Bond Proceeds

Table 1 sets forth the estimated sources and uses of funds relating to the issuance of the Bonds.

Table 1 PISMO BEACH PUBLIC FINANCING AGENCY

SERIES 2017 LEASE REVENUE BONDS

ESTIMATED SOURCES AND USES OF FUNDS

Sources of Funds: Par amount of Bonds Plus: Original Issue Premium Less: Underwriter's Discount

Total Sources

Uses of Funds: Project Fund Costs oflssuance Fund(!)

Total Uses

$7,685,000.00 190,762.65 (48,325.27)

$7 827 437.38

$7,694,000.00 133 437.38

$7 827 437.38

(1) Costs of Issuance include legal fees, municipal advisor fees, title insurance, printing costs, recording costs, rating agency fees, Trustee fees, and other miscellaneous expenses in connection with the issuance, sale and deliveiy of the Bonds

[Remainder of Page Intentionally Left Blank]

7

Debt Service Requirements

Table 2 sets forth annual principal aud interest on the Bonds (assuming no redemptions of the Bonds, other thau mandatory sinking account redemptions).

Bond Year

Table 2 PISMO BEACH PUBLIC FINANCING AGENCY

SERIES 2017 LEASE REVENUE BONDS

ANNUAL DEBT SERVICE SCHEDULE

Principal Portion of Interest Portion of Total (December 1) Debt Service Debt Service Debt Service

Under the Lease and the Site Lease, the Leased Facilities consist of the (i) City of Pismo Beach City Hall site and facilities located at 760 Mattie Road, Pismo Beach, California, (the "City Hall"), and (ii) City of Pismo Beach Police Department site and facilities located at 1000 Bello Street, Pismo Beach, California (the "Police Department"). The Agency will lease the Leased Facilities to the City pursuant to the Lease. Under the Lease, the City is required to maintain the Leased Facilities in good working order.

Description of City Hall. City Hall is comprised of a two story, 15, 7 47-square foot building that was constructed in 1990, and a single story 4, 718-square foot building that was constructed in 1990, both of which are built upon on land owned by the City. The City Hall building is made of Concrete mat foundation, wood load bearing and shear walls, truss floor and roof systems. The building contains a sprinkler system. The site is fully landscaped and includes parking and lighting.

The City Hall buildings and adjacent parking are located on an approximate sixty-six thousand square feet site. The City Hall houses the City Council Chambers and members' offices, the offices of City Manager, Administrative Services, Finance, Community Development and Public Works as well as other administration offices of the City.

Description of Police Department. The Police Department is comprised of a single story, 10,950-square foot Class A+ Police and Public Safety facility built to "special service standards" in 1997. The Police Department building is made of concrete spread and strip footings and light wood load bearing walls. The building contains a sprinkler system and complies with the Americans with Disabilities Act. The site is fully landscaped and includes parking and lighting.

The Police Department houses a jail facility, a communications center, administrative offices, training and conference rooms, locker rooms, interview rooms, a dispatch center and a secured lobby. The building was built to "Essential Services" standards, and meets California jail certification standards.

Estimated Values of the Leased Facilities

The City and the Agency, based on comparable properties, and other records they maintain, estimate the current fair rental value of the Leased Facilities to be not less than the amount of the annual Lease Payments; however, the City makes no assurances regarding the ability to rel et any component of the Leased Facilities or the amount of rental income to be received in the event that any component of the Leased Facilities is relet.

The City, based certain on comparable properties, insurance appraisals, third-party reports, and other records they maintain, estimate the collective value of the Leased Facilities to be more than $8.2 million. Bond Owners do not have a mortgage on any portion of the Leased Facilities. See the caption "BOND OWNERS' RISKS" herein.

9

Modifications of Leased Facilities

Under the Lease, the City will have the right during the term of the Lease to make additions, modifications and improvements to the Leased Facilities or any portion thereof. Such additions, modifications and improvements may not in any way damage the Leased Facilities, or cause the Leased Facilities to be used for purposes other than those authorized under the provisions of state and federal law; and the Leased Facilities, upon completion of any additions, modifications and improvements, must be of a value which is not substantially less than the value thereof immediately prior to the making of such additions, modifications and improvements.

Subleasing of Leased Facilities

Under the Lease, the City may sublease the Leased Facilities, or any portion thereof, subject to all of the following conditions:

the Lease and the obligation of the City to make Lease Payments thereunder must remain obligations of the City;

the City must, within 30 days after the delivery thereof, furnish or cause to be furnished to the Agency and the Trustee a true and complete copy of such sublease;

no such sublease by the City may cause the Leased Facilities to be used for a purpose which is not authorized under the provisions of the laws of the State; and

the City must furnish to the Agency and the Trustee a written opinion of Bond Counsel stating that such sublease does not cause the interest on the Bonds to become included in gross income for purposes of federal income taxation or to become subject to personal income taxation by the State.

Substitution or Release of Leased Facilities

Under the Lease, the City has the option, at any time and from time to time, to substitute other real property (the "Substitute Property") for any portion of the Leased Facilities (the "Former Property") or release any identifiable real property and/or improvements currently constituting the Leased Facilities (in such case, Substitute Property shall mean the Former Property less any released portion) upon satisfaction of all of the requirements set forth in the Lease, which include the following requirements:

No Event of Default under the Lease has occurred and is continuing;

The City must file with the Agency and the Trustee, and cause to be recorded in the office of the San Luis Obispo County Recorder, sufficient memorialization of amendments to the Lease and the Site Lease which replaces each respective Exhibit A with a description of such Substitute Property which deletes therefrom the description of the Former Property;

The City has obtained a California Land Title Association ("CLTA") or American Land Title Association (ALTA) policy of title insurance insuring the City's fee or leasehold estate under the Lease in the Substitute Property, and the Agency's leasehold estate under the Site Lease in such Substitute Leased Property subject only to Permitted Encumbrances ( as defined in the Lease), in

10

an amount at least equal to the aggregate principal amount of the Outstanding Bonds provided, however, that this requirement shall not apply to Substitute Property that consists only of Former Property less any released portion;

The City shall certify in writing to the Agency and to the Trustee that such Substitute Property serves an essential governmental function of the City, and constitutes property which the City is permitted to lease under the laws of the State of California;

The substitution of the Substitute Property will not cause the City to violate any of its covenants, representations and warranties made under the Lease;

The City has certified in writing to the Agency and the Trustee that the annual fair rental value of the Substitute Property after substitution or release will be at least equal to 100% of the maximum amount of the Base Rental Payments becoming due in the then current fiscal year or in any subsequent fiscal year, and that the useful economic life of the Substitute Property shall be at least equal to the maximum remaining term of the Lease; and

The City shall furnish to the Trustee an opinion of Bond Counsel addressed to the Trustee, the City and the Agency to the effect that the substitution or release is permitted under the Lease and will not in and of itself (i) impair the validity and enforceability of the Lease or (ii) impair the exclusion of interest on the Bonds, and, if applicable, any Additional Bonds, from the gross income of the owners thereof for federal income tax purposes.

Upon the satisfaction of all conditions precedent to substitution set forth in the Lease, the Term of the Lease will thereupon end as to the Former Property and commence as to the Substitute Property, and all references to the Former Property will apply with full force and effect to the Substitute Property. The City will not be entitled to any reduction, diminution, extension or other modification of the Base Rental Payments whatsoever as a result of such substitution or release. The City and the Agency will execute, deliver and cause to be recorded all documents required to properly discharge the Lease lien of record against the Former Property. See "APPENDIX A- SUMMARY OF PRINCIPAL LEGAL DOCUMENTS" herein.

THE BONDS

Authority for Issuance

The Bonds are being issued pursuant to the Marks-Roos Local Bond Pooling Act of 1985, constituting Article 4 of Chapter 5 of Division 7 of Title 1 of the Government Code of the State of California (the "Bond Law"), and pursuant to the Indenture.

General Provisions

General. The Bonds will initially be issued in book-entry only form, registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York ("DTC"). Purchasers of the Bonds will not receive certificates representing their interests therein, which will be held at DTC. See "THE BONDS - Book-Entry System" herein.

11

The Bonds. The Bonds will be issued as fully registered bonds in denominations of $5,000 or any integral multiple thereof and will be dated the date of delivery. Interest on the Bonds will be payable semiannually on June 1 and December 1 of each year ( each, an "Interest Payment Date"), commencing December 1, 2017, by check mailed by the Trustee on each Interest Payment Date to the person whose name appears in the registration books kept by the Trustee as the registered owner thereof as of the close of business on the fifteenth calendar day of the month immediately preceding an interest payment date ( a "Record Date"); provided, however, that payment of interest may be by wire transfer in immediately available funds to an account in the United States of America to any Owner of Bonds in the aggregate principal amount of $1,000,000 or more. Interest on the Bonds shall be calculated based on a 360-day year consisting of twelve 30-day months.

Each Bond will bear interest from the Interest Payment Date next preceding the date of registration thereof, unless (a) it is authenticated after a Record Date and on or before the following Interest Payment Date, in which event it shall bear interest from such Interest Payment Date, or (b) unless it is authenticated on or before November 15, 2017, in which event it shall bear interest from the date of delivery; provided, however, that if, as of the date of authentication of any Bond, interest thereon is in default, such Bond shall bear interest from the Interest Payment Date to which interest has previously been paid or made available for payment thereon.

The Bonds will mature in the amounts and on the dates, and bear interest at the rates per annum, set forth on the inside front cover of this Official Statement. Principal of and premium, if any, on the Bonds are payable upon presentation and surrender of the Bonds at the principal office of the Trustee in Costa Mesa, California.

Transfer or Exchange of the Bonds. Any Bond may, in accordance with its terms, be transferred on the Registration Books by the person in whose name it is registered, in person or by his duly authorized attorney, upon surrender of such Bond for cancellation, accompanied by delivery of a written instrument of transfer, duly executed in a form approved by the Trustee.

Transfer of any Bond shall not be permitted by the Trustee during the period established by the Trustee for selection of Bonds for redemption or if such Bond has been selected for redemption pursuant to the Indenture.

Whenever any Bond or Bonds shall be surrendered for transfer, the Agency will execute and the Trustee will authenticate and deliver a new Bond or Bonds for a like aggregate principal amount and of like maturity. The Trustee will require the Bond Owner requesting such transfer to pay any tax or other governmental charge required to be paid with respect to such transfer.

If a Bond is mutilated, lost, stolen or destroyed, the Trustee, at the expense of the Owner of such Bond, will authenticate, subject to the provisions of the Indenture, a new Bond of like tenor and amount. In the case of a lost, stolen or destroyed Bond, the Trustee may require that an indemnity be furnished and payment of an appropriate fee for each new Bond delivered in replacement of such Bond, and the Agency may require payment of the expenses of the Agency, the City and the Trustee incurred in connection therewith.

12

Redemption Provisions

Optional Redemption. The Bonds maturing on or before December 1, 2026, are not subject to optional redemption prior to their stated maturities. The Bonds maturing on or after December 1, 2027, are subject to redemption prior to their stated maturities, on any Business Day on or after June 1, 2027, as a whole or in part by such maturities as may be designated by the Agency to the Trustee at least forty-five ( 45) days prior to the redemption date, and by lot within any one maturity, from prepayments of Base Rental Payments made at the option of the City pursuant to the Lease, at a redemption price equal to the principal amount of the Bonds to be redeemed, without premium, plus accrued but unpaid interest to the redemption date.

Extraordinary Redemption. The Bonds are subject to redemption on any date prior to their respective stated maturities, upon notice (as described below), as a whole, or in part on a pro rata basis among maturities, on any date, from any Net Proceeds of insurance or an eminent domain award with respect to the Leased Facilities which are not applied to repair, rebuild or replace the Leased Facilities as provided in the Lease and Indenture, at a redemption price equal to 100% of the principal amount to be redeemed plus interest accrued thereon to the date fixed for redemption, without premium.

Mandatory Sinking Account Redemption. The Term Bonds maturing December 1, 2042 are subject to mandatory redemption, in part by lot, from sinking account payments in each year as set forth in the following schedule, commencing December 1, 2038, and on December 1 in each year thereafter to and including December 1, 2042 at a redemption price equal to the principal amount of the Term Bonds to be redeemed, plus accrued but unpaid interest thereon to the date fixed for redemption, without premium.

Redemption Date (December 1)

2038 2039 2040 2041 2042 (Maturity)

Principal Amount To be Redeemed

$290,000 300,000 310,000 320,000 330,000

The Term Bonds maturing December 1, 2047 are subject to mandatory redemption, in part by lot, from sinking account payments in each year as set forth in the following schedule, commencing December 1, 2043, and on December 1 in each year thereafter to and including December 1, 2047 at a redemption price equal to the principal amount of the Term Bonds to be redeemed, plus accrued but unpaid interest thereon to the date fixed for redemption, without premium.

Redemption Date (December 1)

2043 2044 2045 2046 2047 (Maturity)

13

Principal Amount To be Redeemed

$340,000 355,000 365,000 380,000 390,000

Notwithstanding the foregoing, if some but not all of the Term Bonds are redeemed pursuant to the optional or special mandatory provisions of the Indenture, the aggregate principal amount of the Term Bonds to be prepaid in each year thereafter under shall be reduced by the aggregate principal amount of Term Bonds so prepaid, to be allocated among sinking fund payments on a pro rata basis in integral multiples of $5,000.

Selection of Bonds for Redemption. If less than all Outstanding Bonds maturing by their terms on any one date are to be redeemed at any one time, the Trustee shall select the Bonds of such maturity date to be redeemed in any manner that it deems appropriate and fair and shall promptly notify the Agency in writing of the numbers of the Bonds so selected for redemption. For purposes of such selection, Bonds shall be deemed to be composed of $5,000 multiples of principal and any such multiple may be separately redeemed.

Notice of Redemption. Notice of redemption shall be given by the Trustee not less than thirty (30) nor more than sixty (60) days prior to the redemption date by first class mail to each of the Owners designated for redemption at their addresses appearing on the Bond registration books of the Trustee and to one or more Securities Depositories and the Municipal Securities Rulemaking Board.

Neither failure to receive any notice of redemption nor any defect in such notice of redemption so given shall affect the sufficiency of the proceedings for such redemption.

Purchase in Lieu of Redemption. At any time prior to the selection of Bonds for redemption, the Trustee may, upon written direction of the City, apply amounts held for redemption of Bonds to the purchase of Bonds at public or private sale, as and when and at such prices (including brokerage and other charges, but excluding accrued interest payable from the Interest Account) as the City may direct the Trustee, except that the purchase price (exclusive of accrued interest) may not exceed the redemption price of such Bonds; and provided further that in the case of optional redemption, in lieu of redemption at such next succeeding date of redemption, or in combination therewith, amounts for redemption may be used for payment of such Bonds to be redeemed in order of their due date as set forth in a request of the City.

Effectof Redemption. Notice of redemption having been duly given as provided above, and moneys for payment of the amount necessary for the redemption of the Bonds called for redemption having been set aside for that purpose pursuant to the Indenture, the Bonds designated for redemption shall become due and payable on the redemption date thereof.

No interest will accrue on such Bonds called for redemption after the redemption date specified in the notice of redemption. The Bonds called for redemption shall, after the redemption date, cease to be entitled to any benefit or security under the Indenture, and the Owners of such Bonds shall have no right in respect thereof except to receive payment of the redemption price. All Bonds redeemed shall be canceled by the Trustee and shall not be reissued.

Rescission of Redemption. The Agency has the right to rescind any notice of optional redemption of Bonds by written notice to the Trustee on or prior to the date fixed for redemption. Any notice of redemption shall be cancelled and annulled if for any reason funds will not be or are not available on the date fixed for redemption for the payment in full of the Bonds then called for redemption, and such cancellation shall not constitute an Event of Default. The Agency and the Trustee have no liability to the Bond Owners or any other party related to or arising from such rescission of redemption. The Trustee shall mail notice of such rescission of redemption in the same manner as the original notice of redemption was sent under the Indenture.

14

Book-Entry System

The Bonds will be issued as fully registered bonds in book-entry only form, registered in the name of Cede & Co. as nominee ofDTC, and will be available to ultimate purchasers in integral multiples of $5,000, under the book-entry system maintained by DTC. While the Bonds are subject to the book-entry system, the principal, interest and any redemption premium with respect to a Bond will be paid by the Trustee to DTC, which in tum is obligated to remit such payment to its DTC Participants for subsequent disbursement to Beneficial Owners of the Bonds. Purchasers of the Bonds will not receive certificates representing their interests therein, which will be held at DTC.

The Agency and the Trustee cannot and do not give any assurances that DTC, DTC Participants or others will distribute payments of principal, interest or premium with respect to the Bonds paid to DTC or its nominee as the registered owner, or will distribute any redemption notices or other notices, to the Beneficial Owners, or that they will do so on a timely basis or will serve and act in the manner described in this Official Statement. The Agency and the Trustee are not responsible or liable for the failure of DTC or any DTC Participant to make any payment or give any notice to a beneficial Owner with respect to the Bonds or an error or delay relating thereto.

See "APPENDIX F - DTC AND THE BOOK-ENTRY ONLY SYSTEM" for further information regarding DTC and the book-entry system.

SECURITY FOR THE BONDS

General

This section provides summaries of the security for the Bonds and certain provisions of the Indenture and the Lease. See "APPENDIX A- SUMMARY OF PRINCIPAL LEGAL DOCUMENTS" for a more complete summary of the Indenture and the Lease. Capitalized terms used but not defined in this section have the meanings given in APPENDIX A.

Revenues

The Bonds are special obligations of the Agency secured by and payable solely from Revenues, defined in the Indenture as all amounts received by the Agency as lessor under the Lease, including, without limiting the generality of the foregoing, scheduled Base Rental Payments, prepayments, and insurance and condemnation proceeds, and all interest, profits or other income derived from the investment of amounts in any fund or account established under the Indenture.

TI-IE BONDS ARE SPECIAL LiivlITED OBLIGATIONS OF THE AGENCY PAY ABLE SOLELY FROM REVENUES AND AMOUNTS HELD IN THE FUNDS AND ACCOUNTS ESTABLISHED UNDER THE INDENTURE. THE OBLIGATION OF THE CITY TO MAKE BASE RENTAL PAYMENTS DOES NOT CONSTITUTE AN OBLIGATION FOR WHICH THE CITY IS OBLIGATED TO LEVY OR PLEDGE ANY FORM OF TAXATION OR FOR WHICH THE CITY HAS LEVIED OR PLEDGED ANY FORM OF TAXATION. THE OBLIGATION OF TI-IE CITY TO MAKE BASE RENTAL PAYMENTS DOES NOT CONSTITUTE AN INDEBTEDNESS OF THE CITY, THE STATE OF CALIFORNIA OR ANY OF ITS POLITICAL SUBDIVISIONS WITI-IIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

15

Base Rental Payments

Under the Lease, the City will pay to the Agency the Base Rental Payments in amounts equal to the scheduled debt service on the Bonds.

Pursuant to the Indenture, the Agency transfers in trust, grants a security interest in and assigns to the Trustee, for the benefit of the Bondowners, all of the Revenues ( consisting primarily of Base Rental Payments) and other assets pledged under the Indenture, except only amounts required for the compensation or indemnification of the Trustee as provided in the Indenture, and all of the Agency's rights under the Lease, including its right to receive Base Rental Payments, but excluding the right to receive Additional Rental.

Under the Lease, the City agrees to make Base Rental Payments for the beneficial use of the Leased Facilities, and to take such action as is necessary to budget for and to appropriate such amounts.

See "THE LEASED FACILITIES" and "APPENDIX A- SUMMARY OF PRINCIPAL LEGAL DOCUMENTS - The Lease" herein.

The Base Rental Payments are equal to the principal of and interest on the Bonds, and are payable in semiannual installments on the 25th day of the month immediately preceding each Interest Payment Date. The Base Rental Payments will be paid by the City to the Trustee for the benefit of the Owners of the Bonds.

The City's obligation to make Base Rental Payments is subject to abatement in the event of substantial interference with the use and possession of all or a part of the Leased Facilities. See "BOND OWNERS' RISKS - Abatement" herein.

Lease Payments; Covenant to Appropriate

The City covenants, under the Lease, to make Lease Payments as rental for the right to use and occupy the Leased Facilities under the Lease. Amounts of the scheduled Lease Payments are calculated to be sufficient to pay debt service on the Bonds when due. Lease Payments will be paid by the City semiannually to the Trustee on the Business Day immediately preceding each Interest Payment Date. Upon receipt, the Trustee will deposit the Lease Payments in the Bond Fund for the purposes of paying principal of and interest on the Bonds. The City covenants under the Lease to take such action as maybe necessary to include all Lease Payments in its annual budgets and to make the necessary annual appropriations for all such rental payments.

Under certain circumstances described in the Lease, however, Lease Payments are subject to abatement during periods of substantial interference with the City's use and occupancy of all or a portion of the Leased Facilities. See "-Abatement" below.

Budget and Appropriation of Base Rental Payments

The Lease provides that, from and after the date on which the City takes possession of the Leased Facilities and unless the Lease is terminated, the City shall take such action as may be necessary to include all Base Rental Payments in each of its budgets and to make necessary appropriations for all such Base Rental Payments coming due and payable during the period covered by such budget, and the public officials of the City shall take such actions and do other things required by law to enable the City to carry out and perform this covenant. The amounts payable to the Trustee under the Lease are to be used to make payments of the

16

principal of and interest on the Bonds, plus other fees, expenses and reimbursements as specified in the Indenture.

The City's revenues are derived in part from ad valorem property taxes. Such taxes are subject to limitations under Article XIIIA of the California Constitution. The City has the capacity to enter into other obligations which may constitute additional charges against its general revenues. To the extent that additional obligations are incurred by the City, the funds available to make Base Rental Payments and Additional Rental payments, if any, may be decreased. Appropriations of the City are subject to limitation under Article XIIIB of the California Constitution. See "BOND OWNERS' RISKS - Risks Related to Taxation in California" herein.

Abatement

The Lease provides that the obligation of the City to pay Lease Payments will be subject to abatement by reason of (i) any damage or destruction such that there is substantial interference with the use and occupancy of all or any portion of the Leased Facilities, or (ii) a temporary taking of the Leased Facilities or a permanent taking of a portion of the Leased Facilities. Such abatement will be in an amount determined by the City, such that the resulting unabated portion of the Lease Payments will represent fair consideration for the use and occupancy of the remaining usable portions of the Leased Facilities not damaged or destroyed.

In the case of abatement due to damage or destruction of the Leased Facilities, such abatement will continue for the period commencing with such damage or destruction and ending with the substantial completion of the work of repair or reconstruction. In the event of any such damage or destruction, the Lease continues in full force and effect and the City waives any right to terminate the Lease by virtue of any such damage and destruction.

In the case of abatement due to a partial or temporary taking of the Leased Facilities under the power of eminent domain, (i) the Lease shall continue in full force and effect with respect thereto and (ii) the Lease Payments are subject to abatement in an amount determined by the City such that the resulting Lease Payments represent fair consideration for the use and occupancy of the remaining usable portions of the Leased Facilities not damaged or destroyed. If all of the Leased Facilities is taken permanently under the power of eminent domain or sold to ceases as of the day such possession is taken.

Notwithstanding the foregoing, under the Lease, the Lease Payments will not be subject to abatement to the extent that amounts in the Insurance and Condemnation Fund (i.e. proceeds of insurance against accident to or destruction of the Leased Facilities collected by the City or the Agency in the event of any such accident or destruction (including rental interruption insurance)) or in the Bond Fund are available to pay Lease Payments which would otherwise be abated.

Insurance

The Lease requires the City to maintain insurance coverage on the Leased Facilities, so long as the Lease is outstanding, consisting of the following types of insurance. The City may adopt alternative risk management programs to insure against any of the risks required to be insured against under the Lease, including a program of self-insurance, in whole or in part; provided that any such alternative risk management program shall be similar in nature and scope to self-insurance programs maintained by other California cities of comparable size and operations and shall be reviewed by a qualified independent insurance consultant. The

17

City is not required to maintain or cause to be maintained any insurance which is not available from reputable insurers on the open market or more insurance than is specifically required under the Lease.

Fire and Extended Coverage Insurance. The City is to maintain insurance against loss or damage to the Leased Facilities resulting from fire, lightning, vandalism, malicious mischief and such other perils as the City may determine should be insured against, in an amount equal to the replacement cost (subject to deductible clauses not exceeding $100,000 for any one loss) of improvements located on or to be located on the Leased Facilities, or an amount equal to or greater than the aggregate principal amount of the Bonds Outstanding (the "Hazard Insurance Policy").